Hot Topics: Extending Treasury Structures for Growth · PDF fileHot Topics: Extending Treasury...

17

© Citibank, N.A. 2013 Citi Transaction Services | Liquidity Management Services Priorities for 2013 Hot Topics: Extending Treasury Structures for Growth Markets March 2013

Transcript of Hot Topics: Extending Treasury Structures for Growth · PDF fileHot Topics: Extending Treasury...

© Citibank, N.A. 2013

Citi Transaction Services | Liquidity Management Services

Priorities for 2013

Hot Topics: Extending Treasury Structures for Growth Markets

March 2013

Speakers

Gourang Shah Asia Head of Treasury Advisory, Treasury and Trade Solutions, Citi Transaction ServicesBased in Singapore, as Head of Treasury Advisory in Asia, Gourang leads a team that provides advisory service to clients in setting up best in class efficiency structures such as Treasury Center, Shared Service Center, Principal Structures, and In-house Bank. Gourang has over 20 years of experience in Corporate Treasury, Mergers and Acquisition, Financial Planning & Analysis, and Product Engineering. Prior to joining Citi, he was based in the United States as Vice President and Assistant Treasurer of Tyco Electronics.

65.6657.4344

Ron ChakravartiHead of Global Solutions & Advisory, Liquidity Management Services, Citi Transaction ServicesBased in New York, Ron leads a global team responsible for the design and delivery of integrated global treasury solutions for Citi’s corporate and financial institutional clients. He has been with Citi for six years. His prior experience includes senior positions in treasury consultancy; transaction banking strategy and product management; and, corporate banking while based in Asia, Europe, and the US.

1.212.816.6909

1

World’s Economic Center of Gravity Shifting Eastwards

Africa4%

Developing Asia27%

Western Europe19%

Australia & New Zealand

1%

Japan6%

North America22%

Middle East4%

Commonwealth of Independent

States4%

Central and Eastern Europe

4%

Latin America9%

Developing Asia44%

North America15%

Australia & New Zealand

1%

Japan3%

Africa7%

Western Europe11%

Middle East4%

Commonwealth of Independent

States4%

Central and Eastern Europe

3%

Latin America8%

Developing Asia49%

Middle East5%

North America11%

Central and Eastern Europe

2%

Commonwealth of Independent

States3%

Western Europe7%

Japan2%

Australia & New Zealand

1% Africa12%

Latin America8%

The shift in global economic dynamics is changing the way business is done.

Source: Citi

2010

Composition of World GDP

2030 2050

2

Trade Flows Shifting from OECD to EMs

• Significant shift in global trade to Emerging Markets will necessitate prudent management of associated sovereign, counterparty & supply chain risks

• Given the bulk of trade transactions are denominated in USD, the overall growth in world trade, especially in EMs, will significantly increase the need for USD funding

N. America

Asia

Latam

CEEMA

W. Europe

$13T $37T $122T $287TTotal Trade Flows

33% 55% 69% 75%Emerging Market Trade Flows1

Trillion USD

Emerging Markets includes Asia, LatAm and CEEMASource: World Bank, BEA, WTO, BIS, CIRA , Citi GPS: Global Perspectives & Solutions

For Treasury, managing liquidity, funding and risks in emerging markets is becoming a key focus.

3

Change Agents Impacting Treasury TodayThe rapidly globalizing supply chain, an evolving corporate finance environment and market forces makes 2013 a time to re-engineer treasury for growth markets.

Shift in supply chains to emerging markets is driving re-engineering of corporates’ core operating models – with profound

impact on Treasury

Fundamental regulatory changes are occurring globally, regionally & locally. Both restrictive & liberalizing policies

have direct effects on Treasury

Mixed global economic outlook, divergent interest rates, and relaxed financial markets

call on Treasury to take a close look at liquidity, funding, and cash investment

strategies

From Balance Sheet to Treasury Operations, pressure to do more with less is driving adoption of practices

for greater efficiency and productivity

Changes to Trading Model

Regulatory Upheaval

Market Conditions

Emphasis on EfficiencyWhat’s Driving

Change?

4

Convergence of Treasury & Working Capital Management

No

Yes

29%

TreasuryDirectlyInvolvedin WCM

+8%

71%(2012) 63%

(2009)

Source: Citi Treasury Diagnostics

Treasury & Working Capital Functions are converging as companies are centralizing activities at In House Banks

• Trading Models are changing in response to evolving global supply chains

• Treasuries must align their resources - People, Processes & Infrastructure – with the changing trading model

• Enterprise-level efficiency models – such as well-aligned Principal Trading Co & In House Bank infrastructures – help drive balance sheet & P&L efficiency

• Direct benefits include financial efficiency, improved liquidity management, better management of FX, operational efficiency

1Treasurers today are partnering with the business and re-engineering their departments to create more value for the firm.

5

Leveraging Convergence

Functional Evolution

Merger with Legacy Trading Principal & Legacy SSC

Geo

grap

hic

Evol

utio

n

Core Treasury Construct Convergence with WCM Legal Entity Convergence at Enterprise Level

In House Bank – Evolution of Scope

In House Banks are a catalyst for greater centralization from both functional and geographic perspectives.

Dev

elop

ed

Mar

kets

Emer

ging

M

arke

ts

Intercompany Funding

Pool Leadership,

Netting, Investments,

FX

Restricted Principal

for Emerging Markets

POBO ROBO

Improving treasury & banking technology is paving the way for POBO / ROBO structures. Concurrently, IHBs and Principal Trading Companies / SSCs are converging to drive maximum efficiency for the enterprise.

6

Re-engineering Banking Structures2

Banking structures need to be re-

engineered to derive maximum benefits

De-regulation in Emerging Markets

provides new opportunities

Legacy notional pooling structures may no longer be

efficient

Shifts in global supply chains

changing sources and uses of cash “On Behalf Of”

solutions via IHB & SEPA impact account

structures

Disparities in interest rates, WHT, etc. call

for concentration structures to be

reviewed

Changes in the operating business, market conditions, and centralization (e.g. through the deployment of IHBs) call for many legacy banking structures to be reassessed and made “fit for purpose”.

7

Multi-bank, decentralized account structure; manual liquidity

management

Rationalized account/liquidity structures and centralized liquidity management

Intercompany Netting (BUs transact in functional currency with

other Bus)

POBO and Third-party Netting (BUs only

transact in functional currency)

ROBO

Many accounts in multiple currencies across multiple banks

Many accounts across multiple currencies. Payments made from individual BU bank

accounts. The fewer banks, the least “cash leakage”.

Fewer non-functional currency bank accounts Fewer bank accounts Least bank accounts

Example: Global Liquidity Structure Evolution

Fewer Bank Accounts and more Efficient Liquidity Management (Where Allowed by Regulations)

Finance Company IHB Evolution

IHB(Integrated withBusiness Units)

USD

Local Currency Header Accounts

Local Currency Transaction Accounts

USD USD USD

IHB IHB IHB IHB

The banking structure evolves as the scope of the IHB expands.

Intercompany Loans (Term and Revolving)Collections

Intercompany Ledger (BU Virtual Account)Payments

Multi-currency Notional Pool

USD Transaction Accounts

8

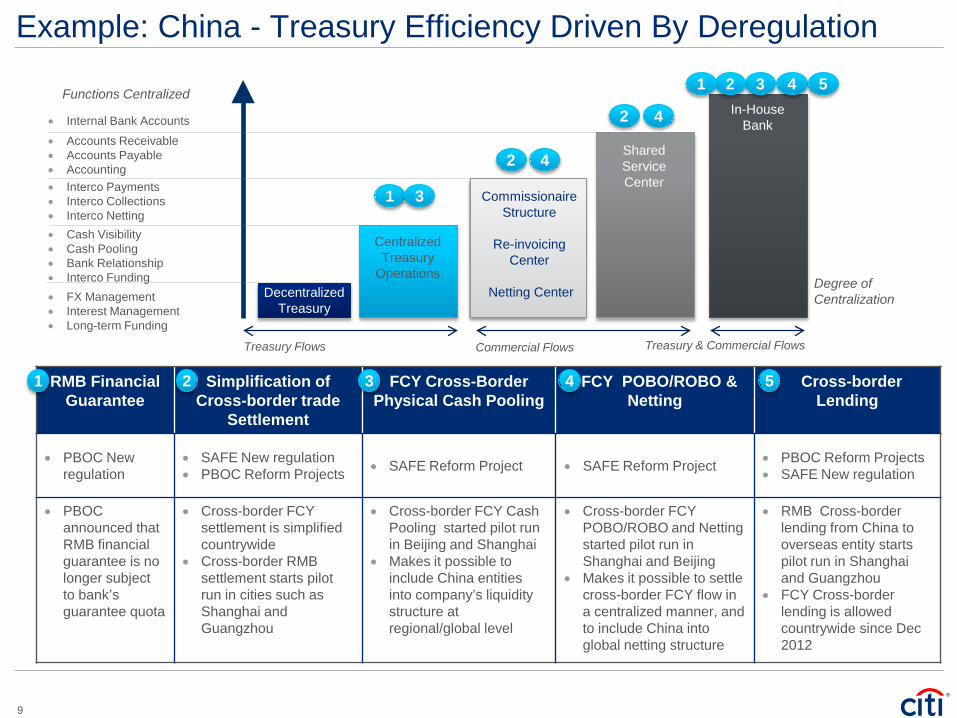

Example: China - Treasury Efficiency Driven By Deregulation

• Cash Visibility• Cash Pooling• Bank Relationship• Interco Funding

Decentralized Treasury

Centralized Treasury

Operations

Commissionaire Structure

Re-invoicing Center

Netting Center

Shared Service Center

In-House Bank• Internal Bank Accounts

• Accounts Receivable• Accounts Payable• Accounting• Interco Payments• Interco Collections• Interco Netting

• FX Management• Interest Management • Long-term Funding

Treasury Flows Commercial Flows Treasury & Commercial Flows

Degree of Centralization

Functions Centralized

1

4

4

4

2

2

321

3

5

RMB Financial Guarantee

Simplification of Cross-border trade

Settlement

FCY Cross-Border Physical Cash Pooling

FCY POBO/ROBO & Netting

Cross-border Lending

• PBOC New regulation

• SAFE New regulation• PBOC Reform Projects • SAFE Reform Project • SAFE Reform Project • PBOC Reform Projects

• SAFE New regulation

• PBOC announced that RMB financial guarantee is no longer subject to bank’s guarantee quota

• Cross-border FCY settlement is simplified countrywide

• Cross-border RMB settlement starts pilot run in cities such as Shanghai and Guangzhou

• Cross-border FCY Cash Pooling started pilot run in Beijing and Shanghai

• Makes it possible to include China entities into company’s liquidity structure at regional/global level

• Cross-border FCY POBO/ROBO and Netting started pilot run in Shanghai and Beijing

• Makes it possible to settle cross-border FCY flow in a centralized manner, and to include China into global netting structure

• RMB Cross-border lending from China to overseas entity starts pilot run in Shanghai and Guangzhou

• FCY Cross-border lending is allowed countrywide since Dec 2012

431 52

9

Improving Commercial Risk Management

ShortenDSO

Minimizecollection

float

Forecast Cash Flowsefficiently

Mitigateconcen-tration

risk

Gainaccess to low costliquidity

Seller

Extend DPO

ReduceCOGS

Captureearly paydiscounts

Stabilizethe supply

chain

Prevent“channelstuffing”

Buyer

3

• Business growth in emerging markets comes with associated counterparty, sovereign and supply chain risks that need to be managed

• Basel III will impact cost of credit for Sub-Investment Grade loans as well as L/Cs used by suppliers – with trickle-down effect on supply chain

• Treasury needs to be a partner to business in de-risking the physical and financial supply chain. Traditional Credit, Procurement & Working Capital approaches need to converge with Treasury strategies for maximum efficiency to the enterprise

• The post-financial crisis spike in usage of Documentary credit needs to be reviewed, with the goal to move towards greater open account sales

• A/R Financing & Supply Chain Financing tools should be considered for growth markets, in consideration of better risk and balance sheet management

10

Global Technology MNC

Background Desire to standardize all payment terms

Challenge to increase terms in low margin industry

MNC and MME suppliers – Quarterly volume of $1 BN

Client Benefits Average terms extended from 65 to 80 days

$133MM working capital improvement

Discounting cost was much lower than supplier’s proposed price increase for longer payment terms

Supplier Finance Platform

Payment Service

1 Buyer submits approved invoice file to the Bank Supplier Finance System

2Suppliers view invoice data & nominate receivables for sale (or auto approve)

3Bank reviews and accepts offer to sell receivables

4

Bank provides funding to Suppliers

5Buyer pays Bank full invoice amount on maturity date

Buyer Suppliers

Global Tire MNC

Background High borrowing rates for client

Decrease pressure on debt capacity

Financing of $120 MM for supplier of rubber

Client Benefits Increase terms from Advance Payment to 180 days

Trade payable treatment maintained

Free cash flow of $60MM; Cost of Capital benefit

Supplier financing solutions can stabilize the supply chain, as well as reduce working capital and decrease funding costs.

Bank

Example: Supplier Finance in Asia

11

Technology Topography Connectivity Account

Structure

Treasury Account Information

Liquidity, FXAccounting Transactions

• Rates/Prices

Inter Company Payables

Payment Instruction

Deal Instructions

Executed Deal Details

Reuters/Bloomberg

Inter Company Netting System

FX and MM Dealing Platform TMS

ERP

Bank Services

Treasury—Liquidity and Risk Management

Finance Ops/SSC—Working Capital Processes

Corporate Infrastructure

USD EUR

USD

SubUSD

SubLCY

EUR

Treasury Accounts(IHB)

Operating Accounts

Bank/System Integration (Connectivity and Execution)

Operating Account Balances,

Receivables ForecastPayables Forecast

Liquidity Structure

Operating Account Information

SubEUR

Investing in Technology as an EnablerGiven past technology consolidation, often only incremental investment is required to capture significant gains.

Deployment of globally homogenous systems and messaging standards coupled with seamless integration with a handful strategic Bank partners are key to successful convergence of Treasury & Working Capital work-streams

4

Deployment of globally homogenous systems and messaging standards, coupled with seamless integration with strategic bank partners, is key to successful convergence of Treasury & Working Capital work-streams.

12

• Simplify technical solution and reduce potential failure points by replacing various bank-proprietary connectivity channels with single secure, robust and scalable bank-neutral network, such as SWIFTNet.

Corporate

ERP

TMSISO20022

Industry Standard Connectivity

▲Flexibility to select banking partners

▲Scalable and Interoperable

▲Single File Format

▲Single channel

Ban

kS

yste

ms

Ban

kS

yste

ms

Ban

kS

yste

ms

▼ Multiple Banking Relationships

▼ Expensive and Complex

▼ Multiple File Formats

▼ Multiple Channels

Corporate

Proprietary Bank Connectivity

ERP

TMS

PAYMUL

EDIFACT

ANSI

Host to Host

Internet Banking

FTP

Internet

Internet

Ban

kS

yste

ms

Ban

kS

yste

ms

Ban

kS

yste

ms

Reducing integration points and harmonizing formats are key to achieving higher centralization and automation.

Consolidation of Connectivity Channels

• Achieve efficiency by building the process around strategic file format. This can be either existing core format or new industry standards, such as ISO 20022 XML

Harmonization of File Formats

• Reduce the integration effort and achieve greater consistency of services by consolidating Treasury and SSC activity around fewer banking partners offering wide geographical and functional footprint

Rationalization of Banking Relationships

Centralization of Treasury and

Operations

Automation of Processing and Reconciliation

Connectivity Best Practices

13

Key Takeaways: Transformation in Role of Treasury

Change Agents• Shift in Supply Chain to Emerging Markets• Regulatory & Market Forces• Improving Financial Markets Conditions• Emphasis on Efficiency

Re-engineering for Growth• Leverage convergence of Treasury & Working

Capital management to maximize efficiency• Realign banking structures with trading model and

convergence strategies• Partner with the business to mitigate shifts in

commercial risk profiles• Make case for incremental technology investment

to realize the benefits

Enabler of Business Strategic Partner to Business

14

SourcesOur discussion is based on our worldwide client advisory work and global research programs, including our Citi Treasury Diagnostics benchmarking program and joint projects with independent third-parties.

Liquidity Management

Working Capital Management

Risk Management

Subsidiary Funding and Repatriation

Policy and Governance

Systems and Technology

Proprietary Research: Citi Treasury Diagnostics

Benchmarks Benchmarks Relative Performance DetailPerformance Risk Management +/-

Policy &Governance

Liquidity

Working Capital

Sub Funding &Repatriation

Risk Management

Systems &Technology

3.0

2.9

3.0

2.9

3.0

2.9

3.0

2.9

Top 25% of responsesCore 50% (25-75%) of responsesBottom 25% of responsesAverage response

My Score Top 25% of responsesCore 50% (25-75%) of responsesBottom 25% of responsesAverage response

My Score

My Relative Performance

Process AreaAgainst Peer

GroupAgainst Universe

Liquidity/funding risk Worse Worse

Interest rate risk Worse Worse

Foreign Exchange (Transactional) Better Better

Citi/NeuGroup Principles of World Class Cash Management

Joint Research with Third-Parties include

Winner, Celent Model Bank Award

Silver Winner, Solution of the Year, Treasury and Risk Alexander Hamilton AwardsWinner, Innovative Product

15

© 2013 Citibank, N.A. All rights reserved. Citi and Citi and Arc Design are trademarks and service marks of Citigroup Inc. or its affiliates and are used and registered throughout the world.

Citi believes that sustainability is good business practice. We work closely with our clients, peer financial institutions, NGOs and other partners to finance solutions to climate change, develop industry standards, reduce ourown environmental footprint, and engage with stakeholders to advance shared learning and solutions. Highlights of Citi’s unique role in promoting sustainability include: (a) releasing in 2007 a Climate Change PositionStatement, the first US financial institution to do so; (b) targeting $50 billion over 10 years to address global climate change: includes significant increases in investment and financing of renewable energy, clean technology,and other carbon-emission reduction activities; (c) committing to an absolute reduction in GHG emissions of all Citi owned and leased properties around the world by 10% by 2011; (d) purchasing more than 234,000 MWh ofcarbon neutral power for our operations over the last three years; (e) establishing in 2008 the Carbon Principles; a framework for banks and their U.S. power clients to evaluate and address carbon risks in the financing ofelectric power projects; (f) producing equity research related to climate issues that helps to inform investors on risks and opportunities associated with the issue; and (g) engaging with a broad range of stakeholders on theissue of climate change to help advance understanding and solutions.Citi works with its clients in greenhouse gas intensive industries to evaluate emerging risks from climate change and, where appropriate, to mitigate those risks.

efficiency, renewable energy and mitigation

IRS Circular 230 Disclosure: Citigroup Inc. and its affiliates do not provide tax or legal advice. Any discussion of tax matters in these materials (i) is not intended or written to be used, and cannot be used or relied upon, by you for the purpose of avoiding any tax penalties and (ii) may have been written in connection with the "promotion or marketing" of any transaction contemplated hereby ("Transaction"). Accordingly, you should seek advice based on your particular circumstances from an independent tax advisor.In any instance where distribution of this communication is subject to the rules of the US Commodity Futures Trading Commission (“CFTC”), this communication constitutes an invitation to consider entering into a derivatives transaction under U.S. CFTC Regulations §§ 1.71 and 23.605, where applicable, but is not a binding offer to buy/sell any financial instrument.However, this is not a recommendation to enter into any swap with any counterparty or a recommendation of a trading strategy involving a swap. Prior to recommending a swap or a trading strategy involving a swap to you, Citigroup would need to undertake diligence in order to have a reasonable basis to believe that the recommended swap or swap trading strategy is suitable for you, obtain writtenrepresentations from you that you are exercising independent judgment in evaluating any such recommendation, and make certain disclosures to you. Furthermore, nothing in this pitch book is, or should be construed to be, an offer to enter into a swap. Any terms set forth herein are intended for discussion purposes only and are subject to the final terms as set forth in separate definitive written agreements. This presentation is not a commitment to lend, syndicate a financing, underwrite or purchase securities, or commit capital nor does it obligate us to enter into such a commitment, nor are we acting as a fiduciary to you. By accepting this presentation, subject to applicable law or regulation, you agree to keep confidential the information contained herein and the existence of and proposed terms for any Transaction.Prior to entering into any Transaction, you should determine, without reliance upon us or our affiliates, the economic risks and merits (and independently determine that you are able to assume these risks) as well as the legal, tax and accounting characterizations and consequences of any such Transaction. In this regard, by accepting this presentation, you acknowledge that (a) we are not in the business of providing (and you are not relying on us for) legal, tax or accounting advice, (b) there may be legal, tax or accounting risks associated with any Transaction, (c) you should receive (and rely on) separate and qualified legal, tax and accounting advice and (d) you should apprise senior management in your organization as to such legal, tax and accounting advice (and any risks associated with any Transaction) and our disclaimer as to these matters. By acceptance of these materials, you and we hereby agree that from the commencement of discussions with respect to any Transaction, and notwithstanding any other provision in this presentation, we hereby confirm that no participant in any Transaction shall be limited from disclosing the U.S. tax treatment or U.S. tax structure of such Transaction. We are required to obtain, verify and record certain information that identifies each entity that enters into a formal business relationship with us. We will ask for your complete name, street address, and taxpayer ID number. We may also request corporate formation documents, or other forms of identification, to verify information provided.Any prices or levels contained herein are preliminary and indicative only and do not represent bids or offers. These indications are provided solely for your information and consideration, are subject to change at any time without notice and are not intended as a solicitation with respect to the purchase or sale of any instrument. The information contained in this presentation may include results of analyses from a quantitative model which represent potential future events that may or may not be realized, and is not a complete analysis of every material fact representing any product. Any estimates included herein constitute our judgment as of the date hereof and are subject to change without any notice. We and/or our affiliates may make a market in these instruments for our customers and for our own account. Accordingly, we may have a position in any such instrument at any time.Although this material may contain publicly available information about Citi corporate bond research, fixed income strategy or economic and market analysis, Citi policy (i) prohibits employees from offering, directly or indirectly, a favorable or negative research opinion or offering to change an opinion as consideration or inducement for the receipt of business or for compensation; and (ii) prohibits analysts from being compensated for specific recommendations or views contained in research reports. So as to reduce the potential for conflicts of interest, as well as to reduce any appearance of conflicts of interest, Citi has enacted policies and procedures designed to limit communications between its investment banking and research personnel to specifically prescribed circumstances.