Home Buying Process

28

www.YourCompanyRE.com Buying A Home In 7 Steps STEPS TO SUCCESS For Buying A Home

-

Upload

peggy-warren -

Category

Real Estate

-

view

78 -

download

0

Transcript of Home Buying Process

www.YourCompanyRE.com

Buying A Home

In 7 Steps

S T E P S TO S U C C E S S

For Buying A Home

Buying a home can be one of the most exciting adventures in your life.

It can also be one of the most overwhelming if you try to go at it alone.

You should also have an experienced Realtor® working for you, guiding you and

looking out for your best interests. And the best part is that hiring a Realtor® as a

buyer, it is basically at no cost to you. In most circumstances, the Buyer’s agent is

paid by the Seller from the proceeds of the sale.

Introduction

www.YourCompanyRE.com

Buying A Home

In 7 Steps

Affiliate Broker

Accredited Realtor and Senior Real Estate Specialist

• Full-time Real Estate Professional since 2014

• Knoxville Board of REALTORS® - Member

• Originally from North Carolina

• Tellico Village Resident for over 3 years

• Loves Boating, Hiking, Reading and History

• Extensive B2B Sales and New Business Development Experience

Peggy Warren

Real Estate Agent

IntroductionA Little About Who I Am

Peggy WarrenAffiliate Broker

Accredited Realtor and Senior Real Estate Specialist

• Full-time Real Estate Professional since 2014

• Knoxville Board of REALTORS® - Member

• Originally from North Carolina

• Tellico Village Resident for over 3 years

• Loves Reading, History, Boating, and Hiking

• Extensive B2B Sales and New Business Development Experience

Buying A Home in 7 Steps

Step 1 - Buying Consultation

Step 2 - Loan Pre-Approval

Step 3 - Searching for a Home

Step 4 - Viewing Homes

Step 5 - Develop a Pricing Strategy

Step 6 - Writing and Negotiating an Offer

Step 7 - Managing the Transaction Through Closing

www.YourCompanyRE.com

Buying A Home

In 7 Steps

There are 3 types of Agency Relationships between parties in a real estate transaction:

• Seller’s Agent - An agent who represents the Seller

• Buyer’s Agent - An agent who represents the Buyer

• Dual Agency (Limited Agent) - An agent who represents both the Seller and Buyer

When you select Your Realtor to assist you in finding and purchasing a home, they

become your “Buyer’s Agent.” Typically the seller already has an agent representing

them, who is working hard for their best interests, not yours. You too should also be

represented with an agent who will be working on your behalf and looking out for your

best interests. I will help you to find a home, evaluate pricing, negotiate offers, and

guide you throughout the entire transaction to ensure a successful closing.

The greatest part of hiring a Buyer’s Agent is that in most cases there is no cost

to you!

I am compensated for my services only when I successfully close on a home for you.

When a seller lists their home with a Seller’s Agent, a commission amount for the

Seller’s Agent and for the Buyer’s Agent is pre-determined and paid for by the Seller

upon the closing of the sale.

Working for You as Your Buyer’s Agent

Step 1Buying Consultation

www.YourCompanyRE.com

Buying A Home

In 7 Steps

Motivation - Why have you decided to buy a home?

Timing - Are you flexible in timing or are we working towards closing before a certain date?

Pricing - What is your price range? Have you begun talking with a mortgage professional?

Decision Making - Will anyone else (family member, financial advisor) be involved in the

transaction?

Location - What areas of town do you prefer, or are you not yet sure?

Home Type - Are you looking for a condominium, townhome, single family residence or land?

Home Size - What size of home are you looking for? How many bedrooms, bathrooms, etc.?

Lot Size - What size of property are you looking for?

Floorplan - What is important to you in the layout of a home?

Architectural Style - Is there any particular style you prefer - rustic, traditional or contemporary?

Amenities - What additional features will you be looking for? (pool, hot tub, clubhouse, golf, etc.)

What Exactly Are You Looking For?

Determine Your Needs

What is Most Important to You?

Step 1Buying Consultation

Buying A Home in 7 Steps

Step 1 - Buying Consultation

Step 2 - Loan Pre-Approval

Step 3 - Searching for a Home

Step 4 - Viewing Homes

Step 5 - Develop a Pricing Strategy

Step 6 - Writing and Negotiating an Offer

Step 7 - Managing the Transaction Through Closing

www.YourCompanyRE.com

Buying A Home

In 7 StepsHow Much Can You Afford?

It can be discouraging to find that your salary won't stretch as far as the home you want to own.

However, sacrificing a huge part of your income just to pay the mortgage can very quickly make

home ownership a burden rather than a point of pride. It may be better to buy a modest home

now and look at purchasing your "dream home" in a few years.

A Pre-Approval Adds Strength to Your Offer

Once you have been successfully pre-approved for a mortgage with a local lender, you will

appear to be a stronger buyer to sellers. When I submit an offer, I will include a written letter of

your pre-approval. This demonstrates to the seller that you are indeed a serious and capable

buyer.

Securing a Pre-Approval for Your Home Loan

Step 2Loan Pre-Approval

www.YourCompanyRE.com

Buying A Home

In 7 Steps

There are many variables to consider when choosing a mortgage loan. Your income, job

history, and credit rating can determine what programs are available to you. Also other

considerations such as how long you plan to be in the home can also be an important factor.

As a real estate agent, I cannot answer these important mortgage questions, but I will be sure

to help you get to the right mortgage provider to help you with this very important part of the

process. Below is a list of mortgage programs and definitions to be familiar with.

Interest Rate - What are current interest rates? What rates are you being quoted?

Fixed Rate Mortgage - A mortgage where the rate remains the same through the life of the

loan.

Adjustable Rate Mortgage (ARM) - A mortgage where the rate changes based on a financial

index.

Down Payment - What amount do you have for a down payment? How much will you really

need?

Origination Fee - A charge levied by a lender for underwriting a loan. Typically 1% of the loan

amount.

Points - A point equals 1% of a mortgage. Should you pay "discount points" to reduce the

loan's interest rate?

Mortgage Term - 15, 20, 30 year loan terms. What is best for you?

Conventional Mortgage - A fixed-rate, 30-year mortgage that is within the limits set by FNMA

& FDMC.

Jumbo Mortgage - Exceeds the limits set by FNMA & FDMC. Usually has a slightly higher

interest rate.

FHA Mortgage - Usually requires less money down, but has tighter guidelines. Can you

qualify?

Balloon Mortgage - Can be a great option for short term situations, but will you be ready to

pay it off at the end?

Interest-Only Mortgage - This will give you a lower monthly payment, but is it the best route

to go?

Pre-Payment Penalty - If you pay the loan off early, or refinance, will there be a penalty or

fee?

Mortgage Industry Conditions - Any issues with the current mortgage industry that could

affect your financing?

What Type of Loan is Best?

Step 2Loan Pre-Approval

www.YourCompanyRE.com

Buying A Home

In 7 Steps

Just like any major purchase, it is usually worthwhile to shop around

for the best deal. It is also important to choose a local lender with

long term experience.

Obtaining A Mortgage Lender

Step 2Loan Pre-Approval

What is your debt-to-income ratio?

This is something that lenders take very seriously. Your overall debt

should not be more than 40% of your income, and your housing debt

should not be more than 32%. What 32% of your income will buy

depends on where you want to live. In rural or downtrodden areas for

example, it can buy a very comfortable residence and ample

acreage. In highly sought-after urban areas however, it may not even

buy a 400 square foot bachelor suite.

www.YourCompanyRE.com

Buying A Home

In 7 Steps

• Do NOT change jobs, become self-employed or quit your current job!

• Do NOT buy a car, truck, boat or RV!

• Do NOT use your credit cards excessively or miss payments!

• Do NOT transfer balances or open new credit cards!

• Do NOT pay off any credit cards or other revolving debts!

• Do NOT spend money set aside for closing costs!

• Do NOT withhold debts or liabilities from your loan application!

• Do NOT open new credit accounts to buy new furniture, appliances, etc.!

• Do NOT make any inquiries into your credit!

• Do NOT make large deposits or withdrawals from your bank accounts!

• Do NOT change banking accounts!

• Do NOT co-sign any loans for anyone!

Inquire with your lender before considering any of the above.

Until You Close on a Mortgage Loan...

Step 2Loan Pre-Approval

Buying A Home in 7 Steps

Step 1 - Buying Consultation

Step 2 - Loan Pre-Approval

Step 3 - Searching for a Home

Step 4 - Viewing Homes

Step 5 - Develop a Pricing Strategy

Step 6 - Writing and Negotiating an Offer

Step 7 - Managing the Transaction Through Closing

www.YourCompanyRE.com

Buying A Home

In 7 Steps

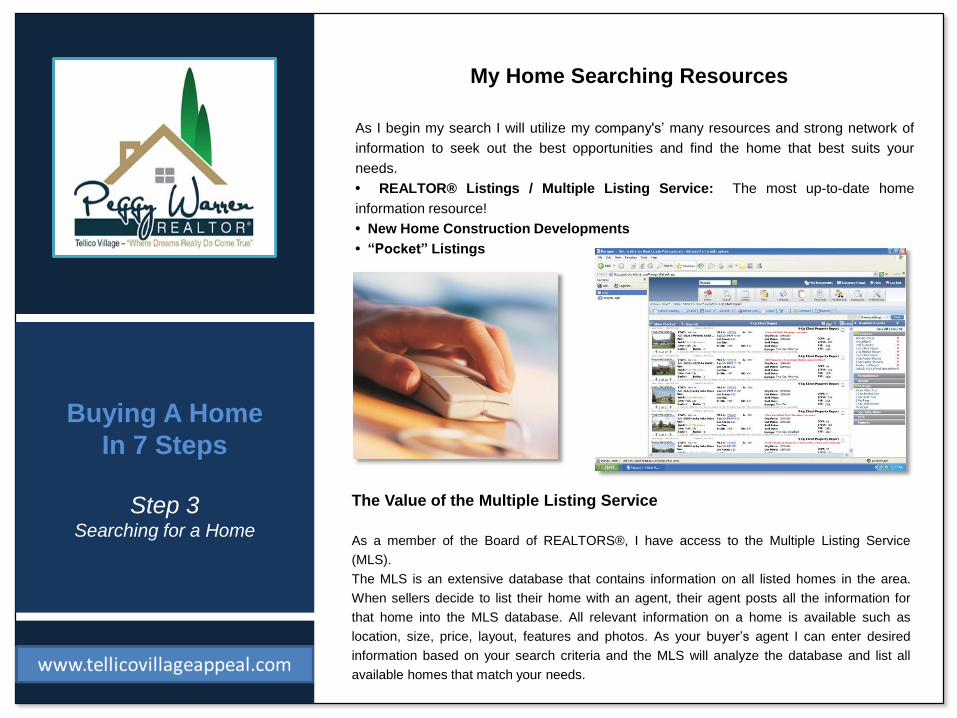

As I begin my search I will utilize my company's’ many resources and strong network of

information to seek out the best opportunities and find the home that best suits your

needs.

• REALTOR® Listings / Multiple Listing Service: The most up-to-date home

information resource!

• New Home Construction Developments

• “Pocket” Listings

My Home Searching Resources

Step 3Searching for a Home

The Value of the Multiple Listing Service

As a member of the Board of REALTORS®, I have access to the Multiple Listing Service

(MLS).

The MLS is an extensive database that contains information on all listed homes in the area.

When sellers decide to list their home with an agent, their agent posts all the information for

that home into the MLS database. All relevant information on a home is available such as

location, size, price, layout, features and photos. As your buyer’s agent I can enter desired

information based on your search criteria and the MLS will analyze the database and list all

available homes that match your needs.

www.YourCompanyRE.com

Buying A Home

In 7 Steps

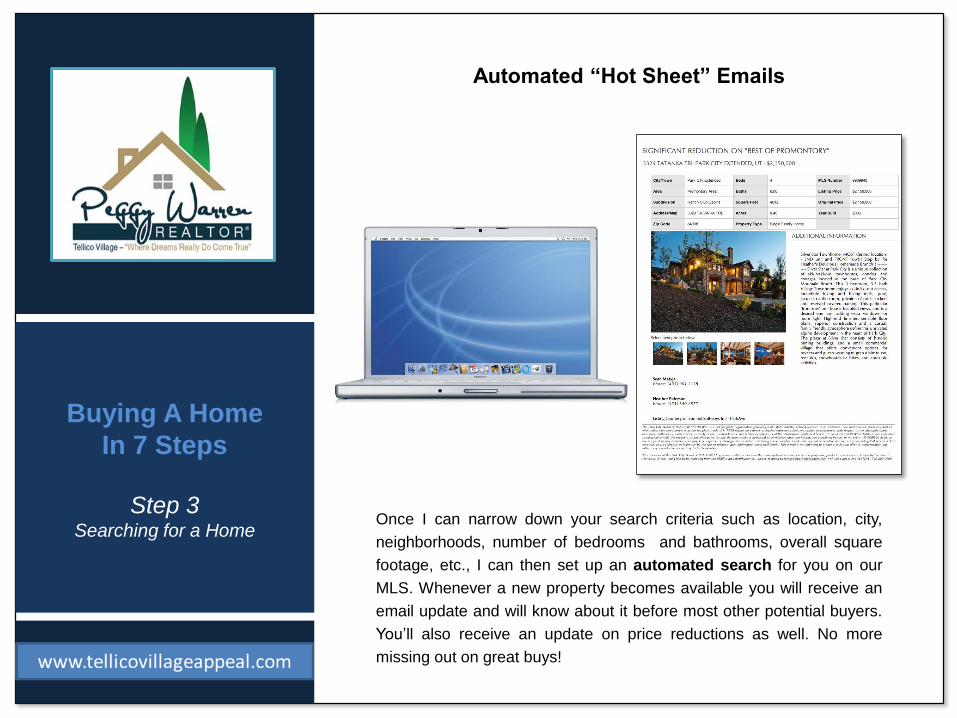

Once I can narrow down your search criteria such as location, city,

neighborhoods, number of bedrooms and bathrooms, overall square

footage, etc., I can then set up an automated search for you on our

MLS. Whenever a new property becomes available you will receive an

email update and will know about it before most other potential buyers.

You’ll also receive an update on price reductions as well. No more

missing out on great buys!

Automated “Hot Sheet” Emails

Step 3Searching for a Home

www.YourCompanyRE.com

Buying A Home

In 7 Steps

Internet 37%

Step 3Searching for a Home

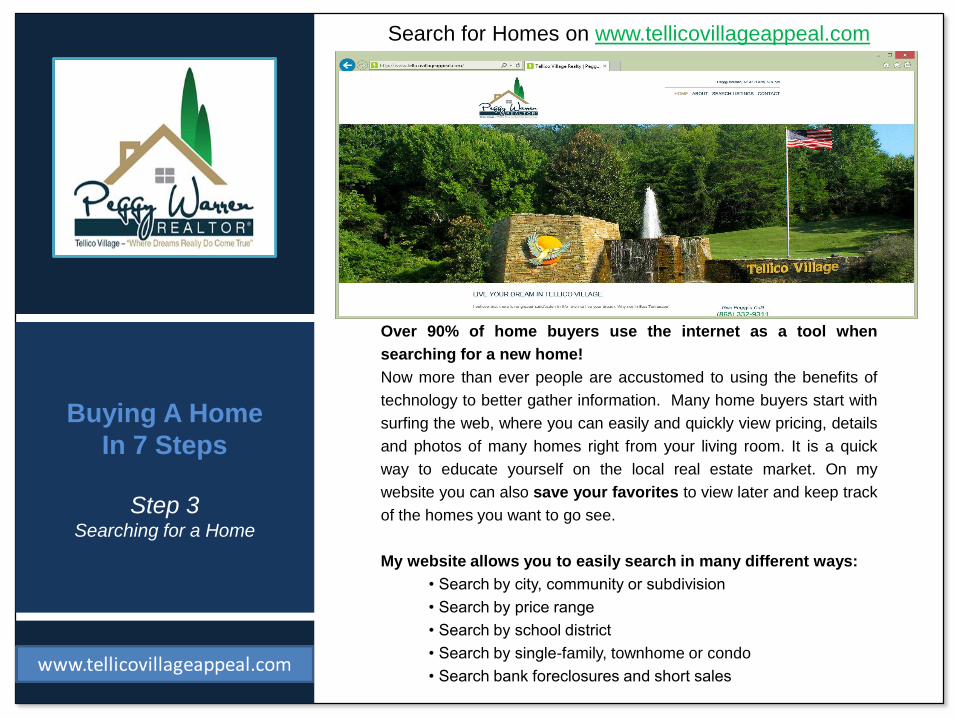

Over 90% of home buyers use the internet as a tool when

searching for a new home!

Now more than ever people are accustomed to using the benefits of

technology to better gather information. Many home buyers start with

surfing the web, where you can easily and quickly view pricing, details

and photos of many homes right from your living room. It is a quick

way to educate yourself on the local real estate market. On my

website you can also save your favorites to view later and keep track

of the homes you want to go see.

My website allows you to easily search in many different ways:

• Search by city, community or subdivision

• Search by price range

• Search by school district

• Search by single-family, townhome or condo

• Search bank foreclosures and short sales

Search for Homes on www.tellicovillageappeal.com

www.YourCompanyRE.com

Buying A Home

In 7 Steps

Short Sales and Bank Foreclosures

Step 3Searching for a Home

A short sale is a property where the seller owes more to the bank than what the

property is worth. For example the home may only be worth $300,000 but the seller

owes $350,000. So how do they sell the home? They will need to get special

permission form the bank (third party approval) to sell the home for less than what

is owed. For a buyer It can be discouraging to wait for this lengthy process. Often a

short sale can take months to obtain the approval from the bank, especially if there

are multiple mortgages or additional liens on the property. If you are trying to

coordinate a move based on your current home selling or lease ending, this can be

a very difficult process to go through.

A bank owned or foreclosure property is a property where the owner failed to

make the mortgage payments, and the bank completed a foreclosure process and

is now the owner of the home. Banks are not in the business of owning homes so

they typically will price the home low to get it sold quickly. But buyer beware, bank

owned homes play by different rules. These homes are sold “as-is” with no

warranties on the condition of the home. Additionally bank owned sales are often

sold with limited Title Insurance coverage.

Buying A Home in 7 Steps

Step 1 - Buying Consultation

Step 2 - Loan Pre-Approval

Step 3 - Searching for a Home

Step 4 - Viewing Homes

Step 5 - Develop a Pricing Strategy

Step 6 - Writing and Negotiating an Offer

Step 7 - Managing the Transaction Through Closing

www.YourCompanyRE.com

Buying A Home

In 7 Steps

Your role and participation in this stage is obviously crucial to my success. You

may even find or preview homes on your own (Open Houses) but it is very

important to keep me notified and included in the process so I can better assist you

to be sure your best interests are are fully met.

Determine Neighborhoods Prior to Viewing - I can do an area tour to examine &

discuss potential neighborhoods. I encourage you to spend some time driving

through desired areas on your own to get the feel of different locations.

Clearly Know Your Criteria - Think about what is the right fit for you. We select

homes together based on the criteria you give me. We may drive by many other

homes on our property tour that may look interesting from the exterior. If it is not

on my list, it is most likely because it was priced too high, home size is too small,

did not have enough bedrooms, etc. It is best to stay focused on the homes that do

meet your needs.

Immediately call me if you find a home - In a newspaper or magazine ad, driving

by a “For Sale By Owner" sign, or visiting an open house.

When approached by other REALTORS® - They will appreciate you letting them

know you are working with another REALTOR®.

Narrowing Your Search

Step 4Viewing Homes

www.YourCompanyRE.com

Buying A Home

In 7 Steps

Now the fun part begins, time to go view some homes. Now that we know what your

price range is, and what your wants and needs are, I can schedule to see the homes

you are most interested in.

Be Mindful of the Appointments Made - It takes a great deal of time to set up a

smooth, productive property viewing tour. Please do not be late, and we must stay

on track with the timing of all the homes. Many of the homes we will be viewing are

primary residences and families must make plans to accommodate our visit.

Comfortable Shoes - Most homes will ask us to remove our shoes, so wear easy

slip-on/off shoes.

Eat Prior to Tour - You will feel much more alert & productive if you simply eat

before our tour.

Take Notes - Be sure to take descriptive notes on each home - good, bad, etc. After

viewing many homes, they all seem to blend together when trying to think back.

Share these notes with me, it will help me to better know what you like and do not

like. If you have questions on a property, write them down so I can work on getting

answers from the seller's agent quickly.

Scheduling Viewing Tours

Step 4Viewing Homes

Buying A Home in 7 Steps

Step 1 - Buying Consultation

Step 2 - Loan Pre-Approval

Step 3 - Searching for a Home

Step 4 - Viewing Homes

Step 5 - Develop a Pricing Strategy

Step 6 - Writing and Negotiating an Offer

Step 7 - Managing the Transaction Through Closing

www.YourCompanyRE.com

Buying A Home

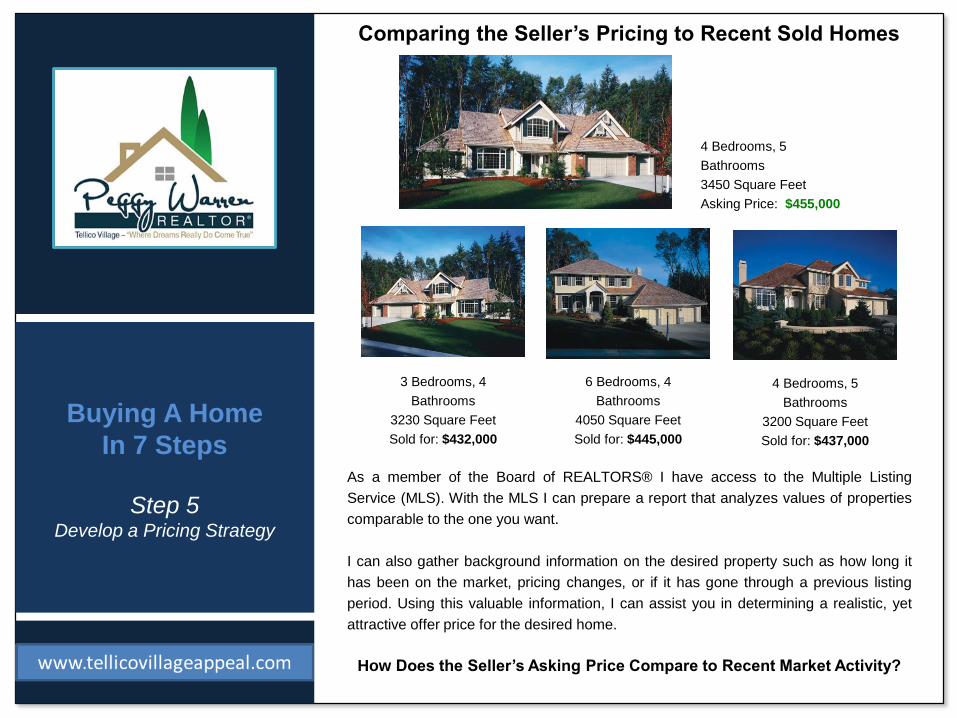

In 7 StepsAs a member of the Board of REALTORS® I have access to the Multiple Listing

Service (MLS). With the MLS I can prepare a report that analyzes values of properties

comparable to the one you want.

I can also gather background information on the desired property such as how long it

has been on the market, pricing changes, or if it has gone through a previous listing

period. Using this valuable information, I can assist you in determining a realistic, yet

attractive offer price for the desired home.

How Does the Seller’s Asking Price Compare to Recent Market Activity?

Comparing the Seller’s Pricing to Recent Sold Homes

Step 5Develop a Pricing Strategy

4 Bedrooms, 5

Bathrooms

3450 Square Feet

Asking Price: $455,000

3 Bedrooms, 4

Bathrooms

3230 Square Feet

Sold for: $432,000

6 Bedrooms, 4

Bathrooms

4050 Square Feet

Sold for: $445,000

4 Bedrooms, 5

Bathrooms

3200 Square Feet

Sold for: $437,000

www.YourCompanyRE.com

Buying A Home

In 7 Steps

Using a Comparative Market Analysis as a Guide

A Comparative Market Analysis (CMA) is the strongest tool I use when estimating the

potential market value for a home. As a member of the Board of REALTORS® with

access to the Multiple Listing Service, I can prepare a report that analyzes comparable

homes in your area. Using this valuable information, I can assist you in determining an

attractive, yet realistic offer price for the home.

A Comparative Market Analysis highlights similar homes in your area that are:

Active Listings - Homes that are currently available for sale. I can see what

comparable asking prices are, but remember these homes have not yet received an

acceptable offer.

Under Contract - Homes that have received and accepted an offer

and give a good indication of realistic pricing.

Sold - Looking at the prices paid for recently sold

homes provides the best foundation in

determining a home's most accurate market

value. Once adjustments are made for square

footage and features, I can make a qualified

recommendation for the offer price on the home.

Expired - Homes that have gone through the

duration of a listing period, but failed to sell.

Many factors could be responsible such as lack

of marketing or the home’s condition, but most

often it is simply because the home was priced

too high.

Step 5Develop a Pricing Strategy

Buying A Home in 7 Steps

Step 1 - Buying Consultation

Step 2 - Loan Pre-Approval

Step 3 - Searching for a Home

Step 4 - Viewing Homes

Step 5 - Develop a Pricing Strategy

Step 6 - Writing and Negotiating an Offer

Step 7 - Managing the Transaction Through Closing

www.YourCompanyRE.com

Buying A Home

In 7 Steps

I will write an offer for your desired home in the form of a Purchase and Sale Agreement (RF401) - a

Tennessee State approved form that is used to present an offer. The RF401-Purchase Sells Agreement is a 9

page contract with many details to carefully fill in. Each section should be thoroughly read and reviewed

before any decisions are made. All accepted terms of the RF401-Purhase Sells Agreement must be carried

through the life of the contract. The signed, accepted Purchase Sells Agreement (with all addenda &

counteroffers) is a LEGALLY BINDING CONTRACT.

Below are some of the items that we will need to pay close attention to:

Purchase Price - You want a good buy, but your offer must also be attractive to the Seller.

Included Items - What is included - Refrigerator, Washer & Dryer, Hot Tub, Furniture, Artwork, etc.?

Excluded Items - What is excluded - Refrigerator, Washer & Dryer, Hot Tub, Furniture, Artwork, etc.?

Water Rights - Do they apply? We may need to employ the services of a Water Lawyer.

Earnest Money - This is the initial deposit. The importance of this item is often overlooked.

Method of Payment - Will this be a cash sale, traditional mortgage or seller financing? How much down

payment?

Special Assessments - Are there any outstanding or upcoming assessments? Who pays, Buyer or Seller?

Possession - When does the property legally change ownership? (You receive keys and move in)

Seller Disclosures - What information about the home should you be asking for?

Due Diligence Condition - What "outs" will you have?

Appraisal Condition - Will the sale be contingent on the home's appraisal amount?

Financing Condition - Will the sale be contingent on you securing financing?

Additional Earnest Money - Will you be offering an additional deposit to your earnest money?

Additional Addenda - Are there any additional terms or addenda to consider?

Home Warranty - Will you be asking for a home warranty? Will you ask for the Seller to pay for it?

Mediation - If a dispute arises, how are you and the Seller directed to handle it?

Seller Disclosure Deadline - What should the deadline date be for the Seller to provide all seller disclosures?

Due Diligence Deadline - What should the deadline date be for you to complete due diligence?

Financing & Appraisal Deadline - What should the deadline date be for you to cancel based on loan denial?

Settlement Deadline - What should the deadline date be for you and the Seller to complete closing?

Response Deadline - How long should you allow for the Seller to respond to your offer?

After considering all terms... The Seller may Accept, Counteroffer, or Reject the Offer.

Writing an Offer - Important factors should you consider?

Step 6Writing and Negotiating an Offer

Buying A Home in 7 Steps

Step 1 - Buying Consultation

Step 2 - Loan Pre-Approval

Step 3 - Searching for a Home

Step 4 - Viewing Homes

Step 5 - Develop a Pricing Strategy

Step 6 - Writing and Negotiating an Offer

Step 7 - Managing the Transaction Through Closing

www.YourCompanyRE.com

Buying A Home

In 7 Steps

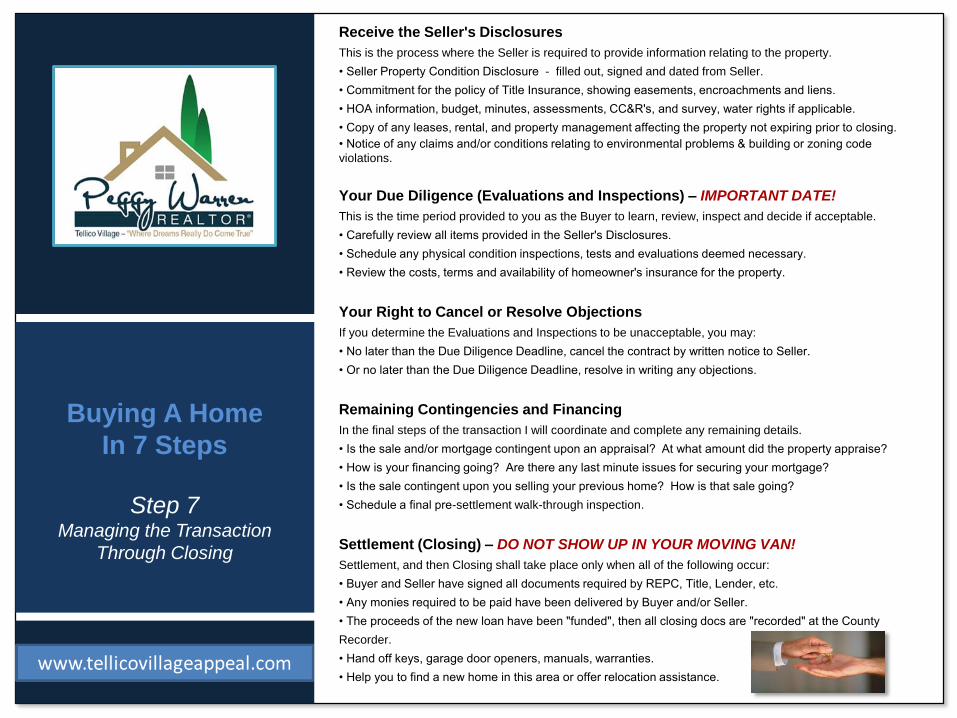

Receive the Seller's Disclosures

This is the process where the Seller is required to provide information relating to the property.

• Seller Property Condition Disclosure - filled out, signed and dated from Seller.

• Commitment for the policy of Title Insurance, showing easements, encroachments and liens.

• HOA information, budget, minutes, assessments, CC&R's, and survey, water rights if applicable.

• Copy of any leases, rental, and property management affecting the property not expiring prior to closing.

• Notice of any claims and/or conditions relating to environmental problems & building or zoning code

violations.

Your Due Diligence (Evaluations and Inspections) – IMPORTANT DATE!

This is the time period provided to you as the Buyer to learn, review, inspect and decide if acceptable.

• Carefully review all items provided in the Seller's Disclosures.

• Schedule any physical condition inspections, tests and evaluations deemed necessary.

• Review the costs, terms and availability of homeowner's insurance for the property.

Your Right to Cancel or Resolve Objections

If you determine the Evaluations and Inspections to be unacceptable, you may:

• No later than the Due Diligence Deadline, cancel the contract by written notice to Seller.

• Or no later than the Due Diligence Deadline, resolve in writing any objections.

Remaining Contingencies and Financing

In the final steps of the transaction I will coordinate and complete any remaining details.

• Is the sale and/or mortgage contingent upon an appraisal? At what amount did the property appraise?

• How is your financing going? Are there any last minute issues for securing your mortgage?

• Is the sale contingent upon you selling your previous home? How is that sale going?

• Schedule a final pre-settlement walk-through inspection.

Settlement (Closing) – DO NOT SHOW UP IN YOUR MOVING VAN!

Settlement, and then Closing shall take place only when all of the following occur:

• Buyer and Seller have signed all documents required by REPC, Title, Lender, etc.

• Any monies required to be paid have been delivered by Buyer and/or Seller.

• The proceeds of the new loan have been "funded", then all closing docs are "recorded" at the County

Recorder.

• Hand off keys, garage door openers, manuals, warranties.

• Help you to find a new home in this area or offer relocation assistance.

Step 7Managing the Transaction

Through Closing

Lets Get Started!

There is so much thought, knowledge and preparation that

goes into a successful home-buyer process. I will be your

resourceful guide through every step. Lets get started right

away and we’ll find your dream home soon.

Thank You for Your Business

Much of my business is based on referrals from satisfied clients.

If you know anyone who could benefit from my services,

please let me know how I can be of help!