Hilton Maher Selto. 12 Financial and Cost-Volume-Profit Models McGraw-Hill/Irwin © 2003 The...

22

Hilton • Maher • Selto

-

date post

21-Dec-2015 -

Category

Documents

-

view

217 -

download

0

Transcript of Hilton Maher Selto. 12 Financial and Cost-Volume-Profit Models McGraw-Hill/Irwin © 2003 The...

Hilton • Maher • Selto

12Financial and Cost-Volume-Profit

Models

McGraw-Hill/Irwin © 2003 The McGraw-Hill Companies, Inc., All Rights Reserved.

12-3

Definition of Financial Models

Accurate, reliable Accurate, reliable simulations of simulations of

relations among relations among relevant costs, relevant costs,

benefits, value and benefits, value and risk that is useful for risk that is useful for supporting business supporting business

decisions.decisions.

Accurate, reliable Accurate, reliable simulations of simulations of

relations among relations among relevant costs, relevant costs,

benefits, value and benefits, value and risk that is useful for risk that is useful for supporting business supporting business

decisions.decisions.

Relationships between costs,

revenues, & income.

Relationships between costs,

revenues, & income.

Relationships between current

investments and value.

Relationships between current

investments and value.

Pro forma financial

statements.

Pro forma financial

statements.

12-4

Objectives of Financial Modeling

12-5

Basic Cost-Volume-Profit (CVP) Model

Profit = Revenue - Variable Cost - Fixed CostProfit = Revenue - Variable Cost - Fixed Cost

Makes the following assumptionsMakes the following assumptions::•Revenue can be estimated as:Revenue can be estimated as:Sales Price (SP) × Units SoldSales Price (SP) × Units Sold

•Variable Cost can be estimated as:Variable Cost can be estimated as:Variable Cost per unit (VC) × Units SoldVariable Cost per unit (VC) × Units Sold

•Fixed Cost (FC) will remain fixed over the relevant Fixed Cost (FC) will remain fixed over the relevant range.range.

Profit = Revenue - Variable Cost - Fixed CostProfit = Revenue - Variable Cost - Fixed Cost

Makes the following assumptionsMakes the following assumptions::•Revenue can be estimated as:Revenue can be estimated as:Sales Price (SP) × Units SoldSales Price (SP) × Units Sold

•Variable Cost can be estimated as:Variable Cost can be estimated as:Variable Cost per unit (VC) × Units SoldVariable Cost per unit (VC) × Units Sold

•Fixed Cost (FC) will remain fixed over the relevant Fixed Cost (FC) will remain fixed over the relevant range.range.

12-6

CVP Model and the Break-Even Point

Profit = Revenue - Variable Cost - Fixed CostProfit = Revenue - Variable Cost - Fixed Cost

Use the above model, but assume that Profit = $0Use the above model, but assume that Profit = $0so that Break-Even is where:so that Break-Even is where:

Revenue = Variable Cost + Fixed CostRevenue = Variable Cost + Fixed Cost(SP × Sales Units) = (VC × Sales Units) + FC(SP × Sales Units) = (VC × Sales Units) + FC

Using the above relationship, we can identify the Using the above relationship, we can identify the number of units we need to sell in order to break number of units we need to sell in order to break

even.even.

Profit = Revenue - Variable Cost - Fixed CostProfit = Revenue - Variable Cost - Fixed Cost

Use the above model, but assume that Profit = $0Use the above model, but assume that Profit = $0so that Break-Even is where:so that Break-Even is where:

Revenue = Variable Cost + Fixed CostRevenue = Variable Cost + Fixed Cost(SP × Sales Units) = (VC × Sales Units) + FC(SP × Sales Units) = (VC × Sales Units) + FC

Using the above relationship, we can identify the Using the above relationship, we can identify the number of units we need to sell in order to break number of units we need to sell in order to break

even.even.

12-7

Break-Even Model - Example

Planet, Inc. sells Model XT telescopes for $2,000 each. Fixed costs totaled $300,000,

variable costs were $800 per unit.How many units does Planet need to sell in

order to Break-Even?

Planet, Inc. sells Model XT telescopes for $2,000 each. Fixed costs totaled $300,000,

variable costs were $800 per unit.How many units does Planet need to sell in

order to Break-Even?

(SP × Sales Units) = (VC × Sales Units) + FC(SP × Sales Units) = (VC × Sales Units) + FC

??(SP × Sales Units) = (VC × Sales Units) + FC(SP × Sales Units) = (VC × Sales Units) + FC

??

12-8

Break-Even Model - Example

Planet, Inc. sells Model XT telescopes for $2,000 each. Fixed costs totaled $300,000,

variable costs were $800 per unit. How many units does Planet need to sell in

order to Break-Even?

Planet, Inc. sells Model XT telescopes for $2,000 each. Fixed costs totaled $300,000,

variable costs were $800 per unit. How many units does Planet need to sell in

order to Break-Even?

(SP × Sales Units) = (VC × Sales Units) + FC(SP × Sales Units) = (VC × Sales Units) + FCBreak Even Sales Units = FC ÷ (SP - VC)Break Even Sales Units = FC ÷ (SP - VC)

= $300,000 ÷ ($2,000 - $800)= $300,000 ÷ ($2,000 - $800)= $300,000 ÷ $1,200= $300,000 ÷ $1,200

= 250 Telescopes= 250 Telescopes

(SP × Sales Units) = (VC × Sales Units) + FC(SP × Sales Units) = (VC × Sales Units) + FCBreak Even Sales Units = FC ÷ (SP - VC)Break Even Sales Units = FC ÷ (SP - VC)

= $300,000 ÷ ($2,000 - $800)= $300,000 ÷ ($2,000 - $800)= $300,000 ÷ $1,200= $300,000 ÷ $1,200

= 250 Telescopes= 250 Telescopes

12-9

(SP - VC)(SP - VC)

is referred to as is referred to as Contribution Margin (CM)Contribution Margin (CM)

(SP - VC)(SP - VC)

is referred to as is referred to as Contribution Margin (CM)Contribution Margin (CM)

Contribution Margin Approach

In the previous In the previous example, we used:example, we used:

FC ÷ (SP - VC)FC ÷ (SP - VC)

to compute Break-to compute Break-Even Units.Even Units.

In the previous In the previous example, we used:example, we used:

FC ÷ (SP - VC)FC ÷ (SP - VC)

to compute Break-to compute Break-Even Units.Even Units.

12-10

Basic CVP in Graphical Format

CVP Graph: Fairfield Blues

$0

$250,000

$500,000

$750,000

$1,000,000

$1,250,000

0 50,000 90,000 130,000 170,000

Quantity of Tickets Sold

Cos

t &

Rev

enu

es Fairfield Blues Fairfield Blues sells tickets for sells tickets for

$7. Fixed $7. Fixed Costs are Costs are

$450,000 and $450,000 and Variable Costs Variable Costs per unit are $2 per unit are $2

per ticket. per ticket.

The Revenue and Cost lines can be overlaid to get a picture The Revenue and Cost lines can be overlaid to get a picture of the CVP relationship.of the CVP relationship.

The Revenue and Cost lines can be overlaid to get a picture The Revenue and Cost lines can be overlaid to get a picture of the CVP relationship.of the CVP relationship.

Exh.12-1

12-11

CVP Graph: Fairfield Blues

$0

$250,000

$500,000

$750,000

$1,000,000

$1,250,000

0 50,000 90,000 130,000 170,000

Quantity of Tickets Sold

Cos

t &

Rev

enu

esBasic CVP in Graphical FormatRevenue = $7 × Units SoldRevenue = $7 × Units SoldRevenue = $7 × Units SoldRevenue = $7 × Units Sold

Total Cost = ($2 × Units Sold) + $450,000Total Cost = ($2 × Units Sold) + $450,000Total Cost = ($2 × Units Sold) + $450,000Total Cost = ($2 × Units Sold) + $450,000

Fixed Costs = $450,000Fixed Costs = $450,000Fixed Costs = $450,000Fixed Costs = $450,000

Exh.12-1

12-12

CVP Graph: Fairfield Blues

$0

$250,000

$500,000

$750,000

$1,000,000

$1,250,000

0 50,000 90,000 130,000 170,000

Quantity of Tickets Sold

Cos

t &

Rev

enu

esBasic CVP in Graphical Format

Profit Area is Profit Area is the amount by the amount by which revenue which revenue exceeds total exceeds total

cost.cost.

Profit Area is Profit Area is the amount by the amount by which revenue which revenue exceeds total exceeds total

cost.cost.

Loss Area is the amount by which Loss Area is the amount by which total cost exceeds revenue.total cost exceeds revenue.

Loss Area is the amount by which Loss Area is the amount by which total cost exceeds revenue.total cost exceeds revenue. Break-Even is Break-Even is

where the two where the two lines intersect.lines intersect.

Break-Even is Break-Even is where the two where the two lines intersect.lines intersect.

Exh.12-1

12-13

CVP and Target Income

Break-Even analysis uses $0 for profit. Target Profit Break-Even analysis uses $0 for profit. Target Profit analysis, puts a $ target in the profit variable, but uses the analysis, puts a $ target in the profit variable, but uses the

same model as Break-Even analysis.same model as Break-Even analysis.

Break-Even analysis uses $0 for profit. Target Profit Break-Even analysis uses $0 for profit. Target Profit analysis, puts a $ target in the profit variable, but uses the analysis, puts a $ target in the profit variable, but uses the

same model as Break-Even analysis.same model as Break-Even analysis.

Planet, Inc. sells Model XT telescopes for $2,000 each. Fixed costs are $300,000, variable costs are $800 per

unit.How many units does Planet need to sell in order to

have target profit of $120,000?

Planet, Inc. sells Model XT telescopes for $2,000 each. Fixed costs are $300,000, variable costs are $800 per

unit.How many units does Planet need to sell in order to

have target profit of $120,000?

Target Target = (SP - VC) × Sales Units - FC = (SP - VC) × Sales Units - FC

??Target Target = (SP - VC) × Sales Units - FC = (SP - VC) × Sales Units - FC

??Target Target = (SP - VC) × Sales Units - FC = (SP - VC) × Sales Units - FC

Sales Units = (Target Sales Units = (Target + FC) ÷ CM per unit + FC) ÷ CM per unit= ($120,000 + $300,000) ÷ $1,200= ($120,000 + $300,000) ÷ $1,200

= 350 Telescopes= 350 Telescopes

Target Target = (SP - VC) × Sales Units - FC = (SP - VC) × Sales Units - FCSales Units = (Target Sales Units = (Target + FC) ÷ CM per unit + FC) ÷ CM per unit

= ($120,000 + $300,000) ÷ $1,200= ($120,000 + $300,000) ÷ $1,200= 350 Telescopes= 350 Telescopes

12-14

Operating Leverage

Reflects the risk of missing sales targets.Reflects the risk of missing sales targets.

Measured as the ratio between contribution Measured as the ratio between contribution margin and operating income.margin and operating income.

Reflects the risk of missing sales targets.Reflects the risk of missing sales targets.

Measured as the ratio between contribution Measured as the ratio between contribution margin and operating income.margin and operating income.

A high operating leverage is indicative

of high committed costs (e.g. interest).

A relatively small change in sales can

lead to a loss.

A high operating leverage is indicative

of high committed costs (e.g. interest).

A relatively small change in sales can

lead to a loss.

A low operating leverage is indicative

of low committed costs (e.g. interest). More of the costs are

variable in nature.

A low operating leverage is indicative

of low committed costs (e.g. interest). More of the costs are

variable in nature.

12-15

Computer Spreadsheet Models

1. Gather all the facts,

assumptions, and estimates

for your model; i.e., parameters.

1. Gather all the facts,

assumptions, and estimates

for your model; i.e., parameters. 2. Describe the relations

between the parameters. This usually results in an

algebraic equation.

2. Describe the relations between the parameters. This usually results in an

algebraic equation.

3. Separate parameters and

formulas.

3. Separate parameters and

formulas.

12-16

Modeling Taxes

After-tax After-tax = Before-tax = Before-tax × (1 - Tax Rate) × (1 - Tax Rate)

Adding the tax rate to your profit model, will have no Adding the tax rate to your profit model, will have no effect on the computation of break-even.effect on the computation of break-even.

Adding the tax rate to your profit model will increase Adding the tax rate to your profit model will increase the number of sales units necessary to reach target the number of sales units necessary to reach target

profit.profit.

After-tax After-tax = Before-tax = Before-tax × (1 - Tax Rate) × (1 - Tax Rate)

Adding the tax rate to your profit model, will have no Adding the tax rate to your profit model, will have no effect on the computation of break-even.effect on the computation of break-even.

Adding the tax rate to your profit model will increase Adding the tax rate to your profit model will increase the number of sales units necessary to reach target the number of sales units necessary to reach target

profit.profit.

With careful planning, many investments and transactions can be structured to minimize the tax implications.

With careful planning, many investments and transactions can be structured to minimize the tax implications.

12-17

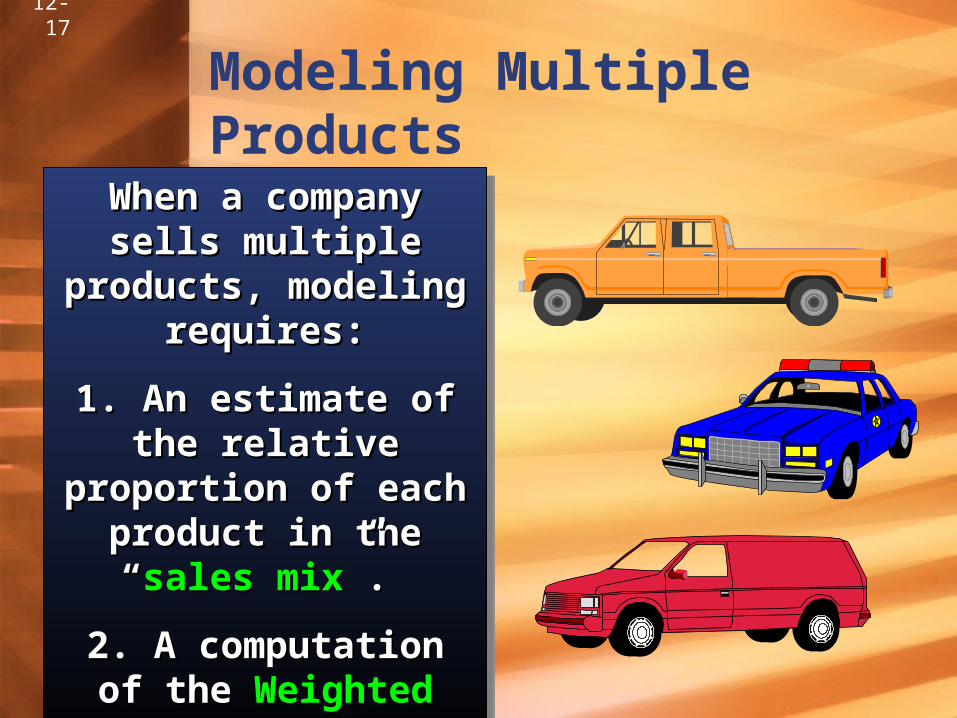

Modeling Multiple Products

When a company sells When a company sells multiple products, multiple products, modeling requires:modeling requires:

1. An estimate of the 1. An estimate of the relative proportion of relative proportion of

each product in the “each product in the “sales sales mixmix”. ”.

2. A computation of the 2. A computation of the Weighted Average Unit Weighted Average Unit

CM.CM.

When a company sells When a company sells multiple products, multiple products, modeling requires:modeling requires:

1. An estimate of the 1. An estimate of the relative proportion of relative proportion of

each product in the “each product in the “sales sales mixmix”. ”.

2. A computation of the 2. A computation of the Weighted Average Unit Weighted Average Unit

CM.CM.

12-18

Modeling Multiple Products

Planet plans to add two new telescopes to its line, The Earth II Model and the Junior Model. Relative sales and cost estimates are:

Planet plans to add two new telescopes to its line, The Earth II Model and the Junior Model. Relative sales and cost estimates are:

(CM(CM11 × Sales % × Sales %11) + (CM) + (CM22 × Sales % × Sales %22) + (CM) + (CM33 × Sales % × Sales %33))

??(CM(CM11 × Sales % × Sales %11) + (CM) + (CM22 × Sales % × Sales %22) + (CM) + (CM33 × Sales % × Sales %33))

??(CM(CM11 × Sales % × Sales %11) + (CM) + (CM22 × Sales % × Sales %22) + (CM) + (CM33 × Sales % × Sales %33))

= ($1,200 × 25%) + ($700 × 40%) + ($350 × 35%)= ($1,200 × 25%) + ($700 × 40%) + ($350 × 35%)= $300.00 + $280.00 + $122.50= $300.00 + $280.00 + $122.50

= $702.50= $702.50

(CM(CM11 × Sales % × Sales %11) + (CM) + (CM22 × Sales % × Sales %22) + (CM) + (CM33 × Sales % × Sales %33))

= ($1,200 × 25%) + ($700 × 40%) + ($350 × 35%)= ($1,200 × 25%) + ($700 × 40%) + ($350 × 35%)= $300.00 + $280.00 + $122.50= $300.00 + $280.00 + $122.50

= $702.50= $702.50

12-19

Limitations of Modeling

12-20

Modeling Multiple Cost Drivers

Cost drivers should be Cost drivers should be grouped based on their type. grouped based on their type. The cost model for multiple The cost model for multiple cost drivers would look like:cost drivers would look like:

Total Cost = (Unit variable cost × Sales Total Cost = (Unit variable cost × Sales units) + (Batch cost × Batch activity) + units) + (Batch cost × Batch activity) +

(Product cost × Product activity) + (Product cost × Product activity) + (Customer cost × Customer activity) + (Customer cost × Customer activity) +

(Facility cost × Facility activity)(Facility cost × Facility activity)

Cost drivers should be Cost drivers should be grouped based on their type. grouped based on their type. The cost model for multiple The cost model for multiple cost drivers would look like:cost drivers would look like:

Total Cost = (Unit variable cost × Sales Total Cost = (Unit variable cost × Sales units) + (Batch cost × Batch activity) + units) + (Batch cost × Batch activity) +

(Product cost × Product activity) + (Product cost × Product activity) + (Customer cost × Customer activity) + (Customer cost × Customer activity) +

(Facility cost × Facility activity)(Facility cost × Facility activity)

Note that Note that units sold is units sold is

no longer the no longer the sole cost sole cost driver.driver.

12-21

Theory of Constraints

5. Increase the bottleneck’s capacity

5. Increase the bottleneck’s capacity

1. Identify the appropriate

measures of value

1. Identify the appropriate

measures of value

4. Synchronize all other processes to

the bottlenecks

4. Synchronize all other processes to

the bottlenecks

6. Avoid inertia and return to Step #1

6. Avoid inertia and return to Step #1

2. Identify the bottlenecks

2. Identify the bottlenecks

3. Use bottlenecks properly

3. Use bottlenecks properly

12-22

End of Chapter 12

Yep! I’m Yep! I’m feeling feeling

constrained constrained NOW!NOW!