Highlights from The future is today - EY - United States · ICT and telecoms, followed by other ......

28

Highlights from The future is today National conference — EY’s 2016 Malta Attractiveness Survey 07 October 2016 Proceedings in brief

Transcript of Highlights from The future is today - EY - United States · ICT and telecoms, followed by other ......

Highlights from

The future is todayNational conference — EY’s 2016 Malta Attractiveness Survey

07 October 2016 Proceedings in brief

Hig

hlig

hts The conference featured

Over 500 delegates

Over 55 leading speakers

Over 135 companies

Contents

04 EY’s vision: shaping Malta’s future, today

06 The future is indeed today

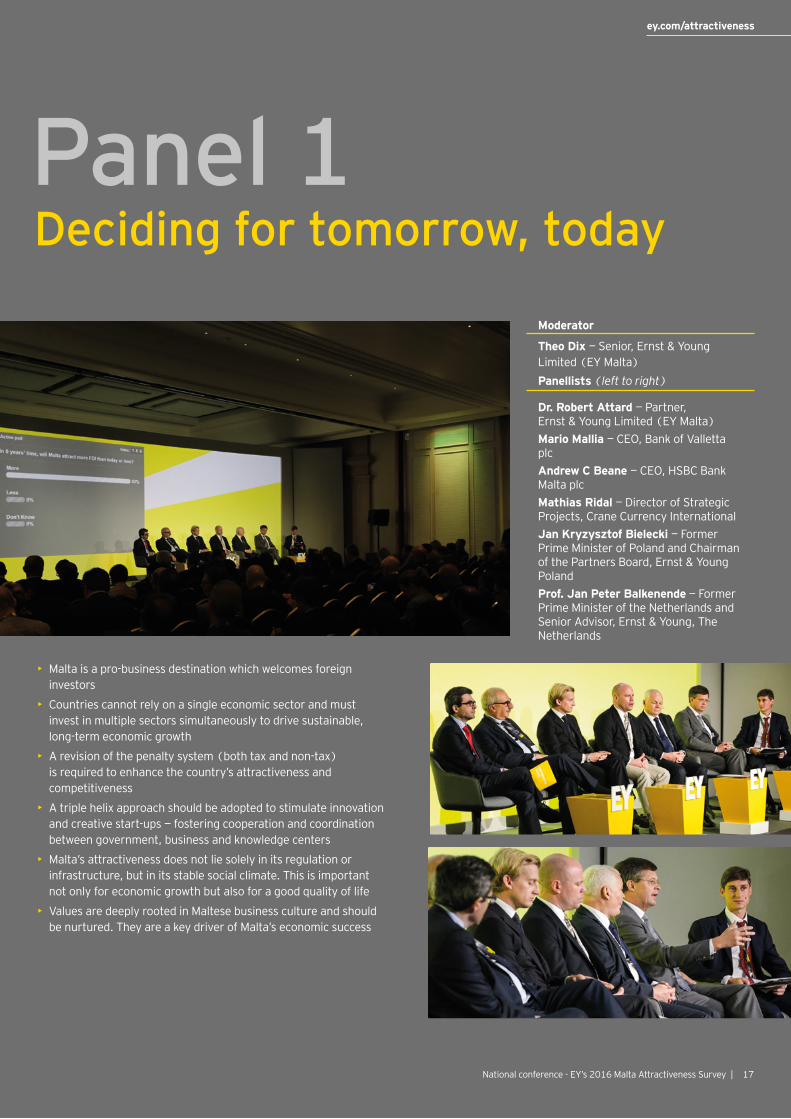

17 Panel 1: Deciding for tomorrow, today

18 Panel 2: Imagining Malta’s future

19 Breakout sessions

27 EY Malta’s upcoming events

27 Our team

Download EY’s 2016 Malta Attractiveness Survey: the future is today, from ey.com/attractiveness.

EY vision: shaping Malta’s future, today

“We need to build a better working world and let us start by building a better working Malta now.”Ronald A AttardErnst & Young Limited (EY Malta)Country Managing Partner

5National conference - EY’s 2016 Malta Attractiveness Survey |

ey.com/attractiveness

The theme of this year’s initiative was “The future is today”, the future that Malta, as a small island at the southernmost tip of the EU, has to sink or swim in.

We are living in an increasingly dynamic and digital world. Reassuringly, Malta seems to be doing relatively well on this front. Yet these are the sectors most prone to the powerful forces of change over which we have absolutely no control.

Following last year’s Malta Attractiveness Survey conference, EY has spearheaded policy proposals in five sectors – FinTech, commodity trading, Malta as a gateway for Asian eCommerce, logistics and reskilling regular immigrants. The active input of public and private stakeholders who came on board, as well as the quality of the final proposals themselves, were very encouraging.

Since EY launched these proposals, both the Prime Minister and the Opposition Leader have publicly endorsed some of them.

Beyond the political fences, it is also encouraging that there is already a heightened awareness of EY’s FinTech proposal. On the logistics side, the Chamber of Commerce, Enterprise and Industry, following the launch of the proposals earlier in July this year, opened a specific section to focus on this area immediately after EY’s session.

In the near future, EY will be launching a think-tank with the exclusive task of delving into what action should be taken in order to enhance Malta’s economic future further. EY’s vision is to generate a pipeline of concrete policy proposals grounded in solid research, acute insights and consensus.

EY’s starting point has been a detailed analysis of what the Malta Attractiveness Survey respondents divulged in terms of what can be better and where opportunities lie. The focus is set on three areas:

1 EducationEY would like to delve into what the education of the future, and for the future, would look like. As indicated in the survey, the challenge of finding the right human resources is paramount to investors. EY will therefore endeavor to see what the best paths from the classroom to the boardroom are.

2TechnologyEY’s think-tank will strive to draw the right policy conclusions from the massive and unprecedented way that technology and innovative ideas are disrupting so many aspects of the financial and economic world, the communications, and the way we hang together as nations and citizens. For EY, FinTech was only one example of the beginning of a deeper and more historically significant change.

3 InfrastructureEY shall be gearing its think-tank to address the challenge of infrastructure that Malta faces in the broadest sense. The era of patchwork, management by crisis and short-term planning is over. Again, even in this respect, a healthy, solid and prosperous future can only be met if it is anticipated from today.

6 | Highlights from: The future is today

The future is indeed today

The future is indeed today

Over the last few years, EY’s Malta Attractiveness Survey and National Conference have acquired a reputation as Malta’s largest business and investment forum benchmark. The event provides private and public stakeholders, as well as prospective investors, with up-to- date independent and game-changing information on Malta’s investment attractiveness on both the national and sectoral levels. The results of a survey carried out by EY among existing FDI companies in Malta were unveiled and the day-long event included both plenary sessions and a range of interactive sectoral breakout sessions.

The conference was addressed by over 60 speakers, including Malta’s top decision makers in the public and private sectors and high-profile international guests, including:

• Hon. Joseph Muscat, Prime Minister of Malta

• Hon. Dr. Simon Busuttil, Leader of the Opposition

• Hon. Dr. Chris Cardona, Minister for the Economy, Investment and Small Business

• Jeremy Paxman, Author, broadcaster and journalist

• Prof. Jan Peter Balkenende, former Prime Minister of the Netherlands

• Jan Krzysztof Bielecki, former Prime Minister of Poland and Chairman of the Partners Board, Ernst & Young Poland

• Paul Brody, Strategy Leader for EY’s technology practice in the America, Ernst & Young LLP United States

• Ian Stuart, Group General Manager and Head of Commercial Banking, HSBC Bank plc

Ronald Attard, EY Malta’s Country Managing Partner mapped out EY’s future prospects with the intention to delve into what action should be taken in order to enhance further Malta’s economic future.

EY’s attractiveness surveysEY’s attractiveness surveys are widely recognized by the clients, the media and major public stakeholders as a key source of insight into foreign direct investment (FDI). Examining the attractiveness of a particular region or country as an investment destination, the surveys are designed to help businesses to make sound financial decisions and governments to remove barriers to future growth. A two-step methodology analyzes both the reality and perception of FDI in the respective country or region. Findings are based on the views of representative panels of international and local opinion leaders and decision-makers.For more information, please visitey.com/attractiveness.

This year, EY welcomed and hosted more than 500 delegates for the 12th edition of the Malta Attractiveness Survey 2016 Conference.

7National conference - EY’s 2016 Malta Attractiveness Survey |

ey.com/attractiveness

Foreign investors’ confidence in Malta is strong. An overwhelming majority think that the country is currently attractive for FDI, and more than half believe that it will remain so in the near future.

Expansions and a long-term presence in the country are envisaged by a majority of current FDIs.

Malta’s access to the EU market, the relative stability of its political and economic environment, its skilled, English-speaking labor force and its attractive fiscal regime are key features that continue to be highlighted by many respondents.

Simon L. BarberiDirector, EU Advisory and Malta Attractiveness Survey Leader, Ernst & Young Limited (EY Malta)

“The number of companies forecasting to still be in Malta in 10 years’ time has risen for the second year in a row, and now stands at 79%. This is indeed very positive on all fronts.”

Investor confidence in Malta remains strong

8 | Highlights from: The future is today

The future is indeed today

Back-office expansions remain the most cited route, accounting for more than half of the total.

Sales and marketing projects are also becoming increasingly popular, with one in three respondents having some form of plans to expand in these areas.

As in previous years, the majority of respondents believe that iGaming will drive Malta’s growth over the next five years. ICT and telecoms, followed by other forms of financial services, are the next most popular choices.

Investments by type of facility

Sales and marketing

Investments by type of facility

R&D

Back-office

31%

19%

Source: 2016 survey respondents.Note: Respondents could choose more than one area.

22%

51%1 2

3 4 Headquarters

Functions and sectors expected to drive growth

The attractiveness scoreboard highlights the parameters that investors deem attractive or otherwise. Changes in scoreboard placings from last year’s survey results have occurred, but the three most attractive and unattractive FDI parameters remained unchanged.

Current attractiveness

Future attractiveness

Expansion plans

Future presence

believe Malta will remain attractive in three years' time.

believe they will expand operations in Malta in a year’s time.

believe that they will be present in Malta in 10 years' time.

Source: all 2016 survey respondents.

1

2

3

44%

39%1%

20%

7%6%

30%

17%

58%

find Malta attractive.87% 53%

79%

Yes No Don't know

2 31

2 31

Strengths: Malta's most attractive FDI parameters

Corporate taxation Stability of

social climate Stability and transparency of political, legal and

regulatory environment

91% 75%+16%

Source: All 2015 and 2016 survey respondents. Note: Addition of very attractive and attractive options.

88% 90%–2%

70% 85%–15%

Weaknesses: Malta's areas for improvement

Domestic or regional market R&D and innovation

environment Transport and logistics infrastructure

39% 21% 31% 21%

+10%

29% 32%

2016 % respondents2015 % respondents

+18% –3%

Malta’s attractiveness for FDI

9National conference - EY’s 2016 Malta Attractiveness Survey |

ey.com/attractiveness

47%

Other financial services

46%

Asset management

46%

Fund administration

Leading business sectors in the next five years

71%

iGaming

50%

ICT and telecoms

Source: All 2016 survey respondents. Note: Respondents could choose more than one area, total number of mentions: 778.

Actions to remain globally competitive

Top five focus areas for Malta to remain globally competitive

Support high-tech industries and innovation

71% 62%Support small and medium-sized enterprises

Increase incentives forFDI investors

60%Invest in major infrastructure and urban projects

51%Develop educationand skills

79%

Source: All 2016 survey respondents.Note: respondents could choose more than one area, total number of mentions: 595.

Local labor skill levels and labor costs are perceived to be attractive by 70% and 67% of investors.

On the downside, less than half of respondents are currently able to find and recruit some of the specialized skills they need from the local labor market, with 51% indicating that expansion plans are linked to filling skill gaps.

This year’s survey included a fresh question asking to rank policy measures to address this challenge. Most actions were seen to be very important by the large majority of investors.

10 | Highlights from: The future is today

The future is indeed today

Neighboring counties have recently faced economic and political difficulties. For a small economy like Malta’s, which is so dependent on foreign trade and FDI, to have managed to not just survive but double its economic growth over the past three years and hit the lowest unemployment rates in its history in this environment, is quite extraordinary.

The economic plan for Malta has three main pillars:

1. Give private firms the incentive to invent and grow: this is being done by focusing on cutting costs such as electricity prices for industry and fuel prices. In addition, investment and growth are being stimulated by diversifying the efforts to attract FDI as well as by supporting local investors.

• Boost the purchasing power of families by improving the labor market. Employment rates are currently very positive. The policies to increase economic growth helped generate jobs. Also, measures are being taken to make work pay, such as reduced taxes on work, free child care for working parents, boosted tax credits for persons returning to work, among others. Through the reinvigorated Jobsplus (formerly known as Jobsplus), active labor market programs such as the Youth Guarantee were introduced

• Restoring credibility in the management of public finances, while tackling long term challenges: Reducing the country’s deficit is one of the main areas of action

The vision is that the revenue has to be driven by economic growth and not by increasing burdens. In future, there will be the need to have more productive workers to make up for the declining numbers, while the infrastructures will need to be such as to help attract much more capital, both from the public and private sectors. There is an infrastructure deficit in this country. Malta has grown too much and the infrastructure has not grown in parallel. This is a priority for the country, be it mass transportation services, new infrastructural projects, or other important initiatives

2. Malta will become a hub for a wider range of sectors, ranging from logistics (a private or public call for an international logistics hub has been launched), to health (a new medical school will be created in Gozo and the facilities at St Luke’s hospital will be upgraded), to education (the new American University of Malta). There are other sectors in which the previous administration did a good job in, like life sciences, aviation and marine engineering, which Malta shall continue to build on

3. National control is very important, however no country can operate in a vacuum, especially with evolving globalization. Malta has role to play even if it is the smallest member state and the smallest country in the EU. The country must keep control, but without building walls which will isolate it

“The best is yet to come! We will continue to transform the economy into one of the best, or rather the best in Europe.”

Hon. Joseph MuscatPrime Minister of Malta

11National conference - EY’s 2016 Malta Attractiveness Survey |

ey.com/attractiveness

Past momentous decisions have shaped Malta’s future. Key among these is Malta’s EU membership which has given the island free access to a vast European and global markets as well as to €2.5 billion worth of EU development funds. Along with the adoption of the euro, this has enabled Malta to attract new investment and build new economic sectors, such as the gaming, aviation and pharma sectors. Crucially, it has helped Malta spur its economic growth and give it the resilience to endure and emerge unscathed from the worst economic recession of the past century.

The below is a reflection on how Malta should prepare today, for the future:

• Public finance: The island’s economic performance has certainly enabled Malta to steer its public finances in the right direction. But there are some worrying signs that could complicate things in the future such as public debt, public sector employment and government spending

• Infrastructure: Traffic congestion has become a problem for Malta’s economy. There is the need for an alternative public transport system, such as a tramway or light railway that connects Malta and Gozo

• The environment: The idea that economic growth can only come at the expense of the environment must be changed

• Energy tariffs: The reduction of the past two years has not been sufficient to reflect the huge savings that Malta have made on the cost of past energy investments

• Exploiting new economic niches such as logistics and distribution, FinTech, and digital media services

• Air Malta: Malta’s national airline is not just about tourism; it is about the connectivity to the world and therefore it is about the economy

• Corruption: Corruption is not pro-business. The conflict of interest of people in high public office undermines the level playing-field that investors need and expect

• The Opposition’s contribution: 91 proposals in the pre-budget document presented in five packages — economic development, public spending, social justice, the environment and infrastructure, and health and education

Hon. Dr. Simon Busuttil Leader of the Opposition and of the Nationalist Party

“The theme you have chosen for your conference — the future is today — is very appropriate because you are right that our future depends on the decisions we take today.”

12 | Highlights from: The future is today

The future is indeed today

• When things go well, it is time to say that the job was well done. But, it is also the time to be on your guard, because the market is never guaranteed

• While Malta wants its indigenous structures, and traditional sectors to do well, it is important that new sectors are developed too. This is why it is important to always seek out new investors and innovators

• Despite the island’s size, Malta has a reputation, as a solid and reliable jurisdiction• The legal framework is good

• Malta is an active member within the EU

• Regulation is robust and flexible

• There is political consensus on the importance of FDI

• The country’s communication skills and links are good

• The use of English language is an added value

• Malta is investing where it really matters, in education, health, and energy. All these areas of the economy are central to the advance and wellbeing of the people and business

• Young Maltese people are creative. Through the University of Malta Take-off programme, which is now in its third year, business ideas are being taken to the next level and placed in an incubator, in order to turn them into reality

“A conference like this helps us take stock, listen to others and think about what is going well and where we can improve. Such a conference is sometimes the spark needed to think anew.”

Hon. Dr. Chris CardonaMinister of the Economy, Investment and Small Business of Malta

13National conference - EY’s 2016 Malta Attractiveness Survey |

ey.com/attractiveness

Even though the European economy is going through turbulent crises, overall Malta’s economy remains strong. The continued resilience of the economy has been acknowledged by the EU and the major credit independent agencies. To ensure Malta’s continued attractiveness and develop a future proof economy, there is a desperate need to invest some of the proceeds of today’s success and enhance the island’s infrastructure. Malta has advanced in a number of sectors. However, further improvements need to be made in the following sectors of the economy:

• Education: There is the need for collaboration between the business sector and educational institutions to address the skills required today and in the future

• R&D, technology and innovation (RDTI): The country needs to assess and forecast the skills and human resources required for RTDI and the processes which have to be in place. Work permits to more third country researchers to work in Malta need to be facilitated

• Infrastructure and transport: The road networks are not in a state are not coping with the increasing number of private vehicles. This is a result of a lack of foresight and an inadequate public transportation system. Other modes of transport might help in this respect - electro mobility, sea transport links, and mass rapid transit system

• Pensions: Recently, the Chamber has accepted the notion of second pillar pensions as a means to supplement and ween off the reliance of unsustainable and low state pensions. In this way employees who voluntary join this scheme would contribute a percentage of their gross salary to a pay-roll deduction

• Healthcare: The potential cost savings from the efficiency gains in new and more effective remedies will foster the required sustainability in the public healthcare sector

“The theme: the future is today presents a unique opportunity to shed light on matters of urgent concern — they are today’s reality.”

Anton Borg President, Chamber of Commerce, Enterprise and Industry

14 | Highlights from: The future is today

The future is indeed today

Delivered with great poise and punctuated with razor sharp wit, Paxman shone the spotlight on the protagonists of British politics and the referendum.

• Great swathes of voters in Britain, the US and Europe have become disenchanted with mainstream politics and conventional politicians

• The decision to call a referendum on Brexit was an ill-thought out, short-sighted gamble taken to solve internal political problems

• The decision to leave does not indicate an innate dislike of the rest of Europe. The referendum was about membership of the EU – an entity which has transformed itself from a common market to a political union

• Today’s society is different. The large turnout for the Brexit vote proved that people still care about politics. However personal interests now trump those of political organizations

• The UK’s national health service has become an uncontrollable burden which politicians are afraid to talk about

• British politics is being increasingly run for retirees to the detriment of the young generations

“Does it matter that people care less about politics? Well, I think it does matter, because if we don’t have politics, then how on earth are we going to sort out the things we disagree about?”

Jeremy PaxmanAuthor, broadcaster and journalist

15National conference - EY’s 2016 Malta Attractiveness Survey |

ey.com/attractiveness

• Malta has seen positive growth in recent years• One of the main challenges for every enterprise is getting the

right skill sets into the business. The competition for skills is going to increase dramatically in the near future, especially when, in countries like Malta, there is full employment

• Malta is really well placed not only to take advantage but to grow and make the most out of its strategic location

• There are some positive signs in the economy at the moment: oil prices are stabilizing and development in China is on the move again

• The bank must ensure that it adapts to the ever-changing environment, not just to be ahead of the game but to thrive in the new world

• Brexit is currently a big concern as the Malta Attractiveness Survey itself points out

• Enterprises cannot wait for politicians to make decisions in the UK. They need to be proactive in order not to be negatively affected by Brexit and its implications

• The UK will need new treaty arrangements with World Trade Organization members and the EU in order to preserve its existing role

• There is a great opportunity for Malta to become a more important hub in the Mediterranean

“The Malta Attractiveness Survey results are exciting, and I think that they inspire confidence.”

Ian StuartGroup General Manager and Head of Commercial Banking Europe at HSBC Bank plc

16 | Highlights from: The future is today

The future is indeed today

• There are three things that make blockchain really interesting:• Consensus algorithm

• Distributed ledger

• Programmable ledger

• The bitcoin block chain is one of the most public, secure infrastructure ever invented

• Block chains are the perfect medium for setting up and recording the objectives and results of clinical trials

• Block chains also make an ultra-secure, distributed database platform for just about any cross-enterprise application

• Today’s most disruptive business models are not business models at all

• Compared with physical marketplaces, existing digital marketplace models have two drawbacks that still need to be addressed: lack of transparency and integration

“A year ago when I talked to you about block chain, people were wondering ‘Will this be real?’. I can tell you today 100% of the world’s leading banks are implementing this technology.”

Paul BrodyTechnology Sector Strategy Leader, Ernst & Young LLP United States

17National conference - EY’s 2016 Malta Attractiveness Survey |

ey.com/attractiveness

Deciding for tomorrow, today

• Malta is a pro-business destination which welcomes foreign investors

• Countries cannot rely on a single economic sector and must invest in multiple sectors simultaneously to drive sustainable, long-term economic growth

• A revision of the penalty system (both tax and non-tax) is required to enhance the country’s attractiveness and competitiveness

• A triple helix approach should be adopted to stimulate innovation and creative start-ups — fostering cooperation and coordination between government, business and knowledge centers

• Malta’s attractiveness does not lie solely in its regulation or infrastructure, but in its stable social climate. This is important not only for economic growth but also for a good quality of life

• Values are deeply rooted in Maltese business culture and should be nurtured. They are a key driver of Malta’s economic success

Moderator

Theo Dix — Senior, Ernst & Young Limited (EY Malta)Panellists (left to right)

Dr. Robert Attard — Partner, Ernst & Young Limited (EY Malta)Mario Mallia — CEO, Bank of Valletta plcAndrew C Beane — CEO, HSBC Bank Malta plcMathias Ridal — Director of Strategic Projects, Crane Currency InternationalJan Kryzysztof Bielecki — Former Prime Minister of Poland and Chairman of the Partners Board, Ernst & Young PolandProf. Jan Peter Balkenende — Former Prime Minister of the Netherlands and Senior Advisor, Ernst & Young, The Netherlands

Panel 1

Imagining Malta’s future

• Malta has done reasonably well in the last 10 years, especially when it comes to coping with change, such as EU membership

• The good thing about information societies is that size does not really matter - the functions that need to be developed are the same for all countries

• Technologically, Malta has very solid foundations. However, the country needs to be innovative and come up with new ideas that will make a difference and that create solid added-value

• A robust technological infrastructure is a must in every country. On its own, however, it is not sufficient. Technology is just the facilitator and it needs to be driven by people with creative and innovative ideas

• There are two opportunities on the horizon for Malta: the internet of things (IoT) and the ability to use assets more efficiently and effectively

• Biometric technology has potential and it would enable people to have more control over their lives and data

• One of Malta’s competences is that it adapts quickly to technology and that the ideal testbed for certain new technologies

Moderator

Kevin Mallia — Executive Director, Ernst & Young Limited (EY Malta)

Panellists (left to right)

Ronald A Attard — Country Managing Partner, Ernst & Young Limited (EY Malta)Robin Tombs — Co-founder and CEO, YotiAngel Moreu — Director, IBM Cloud South Europe RegionTaavi Kotka — CIO, Government of EstoniaPaul Brody — Technology Sector Strategy Leader, EYJulie Meyer — CEO, Ariadne Capital

Panel 2

18 | Highlights from: The future is today

19National conference - EY’s 2016 Malta Attractiveness Survey |

ey.com/attractiveness

Chaired by:

Grace Camilleri – Executive Director, Ernst & Young Limited (EY Malta)

Panellists (left to right)

Murali Subramanian — CEO, FIMBank plcMario Mallia — CEO, Bank of Valletta plcDavid G Curmi — CEO, MSV Life plcKenneth Farrugia — Chairman, FinanceMaltaMarianne Scicluna — Director General, Malta Financial Services Authority

Supported by: Bank of Valletta plc

• In recent years there has been a rapid increase in both the quantum and focus of regulation, from both the prudential and non-prudential sides

• Regulating the financial services sector properly is not easy. One must strike a balance between regulation aimed at preventing financial crises and over regulation which may suppress economic growth

• Regulation has moved to centre stage and is already featuring as a key topic on the agenda of banks and the insurance sector

• Financial institutions are focusing on driving culture change - defining and embedding a culture that resonates from the board and the higher echelons of the firm to all business areas

• Panellists noted that increased regulation is impacting business. It has been noted that with the increase of regulatory pressures banks are dedicating significant time and effort to meet regulatory requirements. This in turn impacts the level of growth

• Increased regulation increases costs. However it has also been mentioned that the cost of non-compliance coupled with reputational risk could in actual fact be higher than the cost of regulation

• The ultimate burden of increased regulation is being passed on to the end consumer in terms of additional documentation required as well as costs

• It has been noted that in general there is a lack of public awareness on regulation. It was argued that additional education/awareness would ease the pressures on financial institutions, particularly around customer experience and feedback

• It was pointed out that the regulator and financial institutions cannot work in isolation and that additional communication and coordination between both parties is required

Challenges aheadFinancial Services I – Banking, Insurance & AML

Breakout sessionsEight interactive breakout sessions provided the opportunity to delegates to delve deeper into what is affecting and shaping the current and future of Malta’s major sectors. During each one industry leaders, professionals from the sectors and personnel from the Government and regulatory authorities, together with the delegates engaged in deep and enlightening sector-specific discussions.

1

20 | Highlights from: The future is today

Breakout sessions

Chaired by:

Karl Mercieca — Senior Manager, Ernst & Young Limited (EY Malta)

Panellists (left to right)

Joseph Portelli — Chairman, Malta Stock Exchange plcPatrick L. Young — CEO, HanzaTradeChris Portelli — Executive Director, Ernst & Young Limited (EY Malta)Dr. Michael Xuereb — CEO, Valletta Cruise Port plc

Supported by: Malta Stock Exchange plc

• FinTech has brought about a revolution in financial services, including the asset management and investment advisory spheres

• Given the rapid evolution of FinTech, the industry has yet to determine whether it provides added value to the market and its clients in general in all aspects compared to traditional asset management and investment advice

• The financial services industry is in continuous need of flexibility and optionality of services from banks or asset management companies. FinTech could be seen as a result of such demand due to technological advancement and given that it intends to streamline and expedite financial services and making it accessible to a broader audience at affordable costs

Towards new frontiersFinancial Services II – Asset Management, Funds & FinTech 2

• FinTech has also brought about a disruption in asset management by providing innovative and tailor-made products and solutions to the customers

• From a regulatory perspective, given that most of FinTech may provide regulated activities, the Malta Financial Services Authority (MFSA) is continuously monitoring other jurisdictions. It was noted that debate EU level debate on whether and how FinTech companies should be regulated at is ongoing

• FinTech has also brought about changes as to how audit is conducted; audit on FinTech companies has become more focused on technologies

• There is the need for coordination and collaboration by all stakeholders in this area for Malta in order to succeed in the FinTech industry. More joint initiatives and consultation between government entities, regulator, consultants and international players are required in order for Malta to be in a position to cater for the growth in this industry

21National conference - EY’s 2016 Malta Attractiveness Survey |

ey.com/attractiveness

Chaired by:

Gilbert Guillaumier — Executive Director, Ernst & Young Limited (EY Malta)

Panellists (left to right)

Ing. Emanuel Darmanin — Head Strategy and Planning, MITA Dr. Ing. Joseph Attard — CTO, GO plcAngel Moreu — Director, IBM Cloud South Europe RegionSteve Agius — Chief of Information and Development, Malta Communications AuthorityTaavi Kotka — CIO, Government of EstoniaDr. Gege Gatt — Director, ICON Studios LtdSupported by: GO plc

• Two important pillars that Malta needs to focus on are the ability to innovate at a very fast pace and the need of a skilled workforce to build ICT related products

• In ICT and telecoms there is a high degree of skills shortages and mismatch. To mitigate these issues, new subjects should be introduced in schools, such as coding, artificial intelligence, big data and analytics

• There is a tendency for young students to focus on more traditional careers. This can be partly mitigated by having an effective role model in ICT - best practices that government can take up a leading role in, thereby generating more interest in the sector. An example could be for public entities to only accept digital signatures and eliminate paperwork entirely

• Malta needs to take the opportunity and be ‘smart’ to be able to compete with larger countries; infrastructure in Malta is present but penetration of ICT services is evolving at a slow rate

• Enterprises in Malta should be more innovative and diverse rather than replicate what others are doing, thereby missing an opportunity to deliver additional services in the broader ICT value chain. RDTI is the key to the generation of value and competitive advantage

• Incentives need to be created in order to attract more female workers in the field of ICT and telecoms• Bureaucracy can be a deterrent or a barrier to investment, ICT and the telecoms infrastructure. Administrative processes should be

streamlined to enable quicker roll out of infrastructure developments

Get your head in the cloudICT & Telecoms 3

22 | Highlights from: The future is today

Breakout sessions

Chaired by:

Simon L Barberi — Senior Manager, Ernst & Young Limited (EY Malta)

Panellists (left to right)

Andrew Agius Muscat — CEO, MHRAStephen Xuereb — CEO, Valletta Cruise Port plcPer Georg Braathen — Chairman and Owner, Braganza and BramoraDr. Alfred Quintano — Lecturer, University of MaltaMichael Camilleri Kamsky — General Manager, The Westin Dragonara Resort

Supported by: Valletta Cruise Port & The Westin Dragonara Resort

• The tourism industry remains one of Malta’s most important sectors and recent tourist arrival statistics are particularly encouraging. It is important that there is national consensus on the importance of tourism

• The authorities believe Malta’s attractiveness as a tourist destination should not be seen in isolation but in a wider regional context. Therefore it is important to share ideas, new concepts and help promote best practices throughout the region. It is also augured that the turmoil in the region should end as soon as possible

• The cruise liner industry is growing year-on-year and is increasingly contributing towards Malta’s economic growth. There is a wide consensus on the positive effects of this industry, both

To share or not to shareTourism

through actual expenditure while in Malta and through the generation of positive word of mouth and repeat visitors. This segment offers a number of challenges and opportunities which are also being acknowledged internationally

• Tourists are increasingly after an authentic and unique experience which differentiates Malta from other destinations. It is possible for this authenticity to be provided through the sharing economy. Although this development is a disruptor, it can have several positives. It however should be regulated to facilitate a level-playing field, in a similar manner whereby low-cost airlines were introduced in Malta several years ago

• Malta’s size is considered attractive from a tourism point of view. This also means that its natural heritage is limited and greater focus needs to be put on safeguarding the environment. Economic values need to be placed on environmental locations and sites need to be adequately managed

4

23National conference - EY’s 2016 Malta Attractiveness Survey |

ey.com/attractiveness

Chaired by:

Chris Meilak — Executive Director, Ernst & Young Limited (EY Malta)

Panellists (left to right)

Marika Tonna — COO, Malta EnterpriseMarcus Motschenbacher — CEO, Lufthansa Technik Malta LtdNormal Aquilina — CEO, Simonds Farsons Cisk plcMathias Ridal — Director of Strategic Project, Crane Currency International

Supported by: Malta Enterprise

• Manufacturing has also participated in the strong performance of the local economy, and remains a key contributor to FDI and employment figures

• Malta has a number of characteristics which remain attractive to manufacturing FDI, including the tax regime, the widespread use of the English language, quick access to regulators, political stability, and continental law as well as the general environment

• Challenges includes the infrastructure (water, power, transport) and human resources

• In terms of human resources, manufacturing companies are increasingly finding it hard to find qualified staff

• A manufacturing job is no longer a low-skill type of job – high quality skills are increasingly being sought

• As a result of this gap, companies end up competing for staff. Consequently, this industry is witnessing a high turnover of labor and a wage spiral

• Even though labor costs are important, they make up less than ten percent of the final product and hence other characteristics remain important. The Chamber of Commerce, Enterprise and Industry is continuously looking at how the public and private sector can collaborate to ensure the sustainability of such an industry

• It was suggested that manufacturing could target niche markets rather than opt for mass-market industry. This confirms that government and providers of finance continue to sustain this industry

Will the phoenix rise?Manufacturing & industry 5

24 | Highlights from: The future is today

Breakout sessions

Chaired by:

Shawn Falzon — Partner, Ernst & Young Limited (EY Malta)

Panellists (left to right)

Robert C Aquilina — Chairman, Salvo Grima GroupMichel Cordina — Head of Commercial Banking, HSBC Bank Malta plcHermann Mallia — Managing Director, Famalco GroupAlexander Borg — Director and Managing Consultant, SSM Group LtdDr. Aaron Farrugia — CEO, Malta Freeport CorporationGeorge Amato — Director, Hudson Holdings Ltd

Supported by: HSBC Bank Malta plc

• For a number of years, this sector has been somewhat neglected. The survey results rank transport and logistics last, showing that there are issues that need to be addressed

• However there have been new initiatives aimed at taking this sector further. During last year’s MAS conference EY had identified logistics as one of its key sectors on which proposals for action could be put forward

• The initiative followed up and an EY Logistics Forum was held last May, after consultation meetings with stakeholders in the various parts of the logistics chain. Concurrently a logistics section and a committee of the Chamber of Commerce, Enterprise and Industry were subsequently established.

Beyond the same “old”Logistics, distribution & warehousing

It was also announced that a logistics hub was planned for Hal Far, to be developed in partnership with the private sector. The call for proposals is imminent

• Malta has a strategic location which it should exploit • Government is creating a legal framework by amending the Business Promotion Act to include logistics as well as changing the Freeport

Act to introduce more free trade zones, through the identification of a number of areas (such as Hal Far)• Both public and private educational institutions are interested in introducing courses relating to logistics. There needs to be a road

infrastructure in place to cater for the logistics hub. The hub will lead to an increase in traffic and hence there needs to be adequate roads to service such cargo

• Ways to generate more value-added than is already present at the Freeport include distribution, warehousing, fund, and further actions to support trade

• There is no cohesive effort aimed at improving road haulage, although human resources remain an issue

6

25National conference - EY’s 2016 Malta Attractiveness Survey |

ey.com/attractiveness

Chaired by:

Chris Balzan — Executive Director, Ernst & Young Limited (EY Malta)

Panellists (left to right)

Prof. Alfred J Vella — Rector, University of MaltaClyde Caruana — Executive Chairman, JobsplusJosef Bugeja — Secretary General, GWUBernie Mizzi — Director, Chiswick House School and St. Martin’s CollegeJosef Vella — CEO, UHMJosef Said — Managing Director, KONNEKT Search & Selection Ltd

Supported by: KONNEKT Search & Selection Ltd

• Through Jobsplus (formerly known as ETC), government introduced new policies to increase Malta’s employment ratios as rates were behind the EU average. Today a new challenge is being faced — Malta is trying to seek ways to get more value from local employees

• The University of Malta is working hard to produce graduates not only with good qualifications but with transferable skills, writing proficiency and communication skills

• Personnel working in the education sphere must be empowered and the industry needs a vision which is measured, shared and adopted

• The next step is improving efficiency, competitiveness and corresponding salaries

• There is a three step approach which shall help address the skills mismatch problem:

• Set up a National Skills Council

• Go back to basics

• Revamp counselling units

• It is also important to find ways to make the processing/renewing of work permits for non-EU nationals and particularly for high net worth individuals more efficient

Knowledge to do what? Skills & human capital 7

26 | Highlights from: The future is today

Breakout sessions

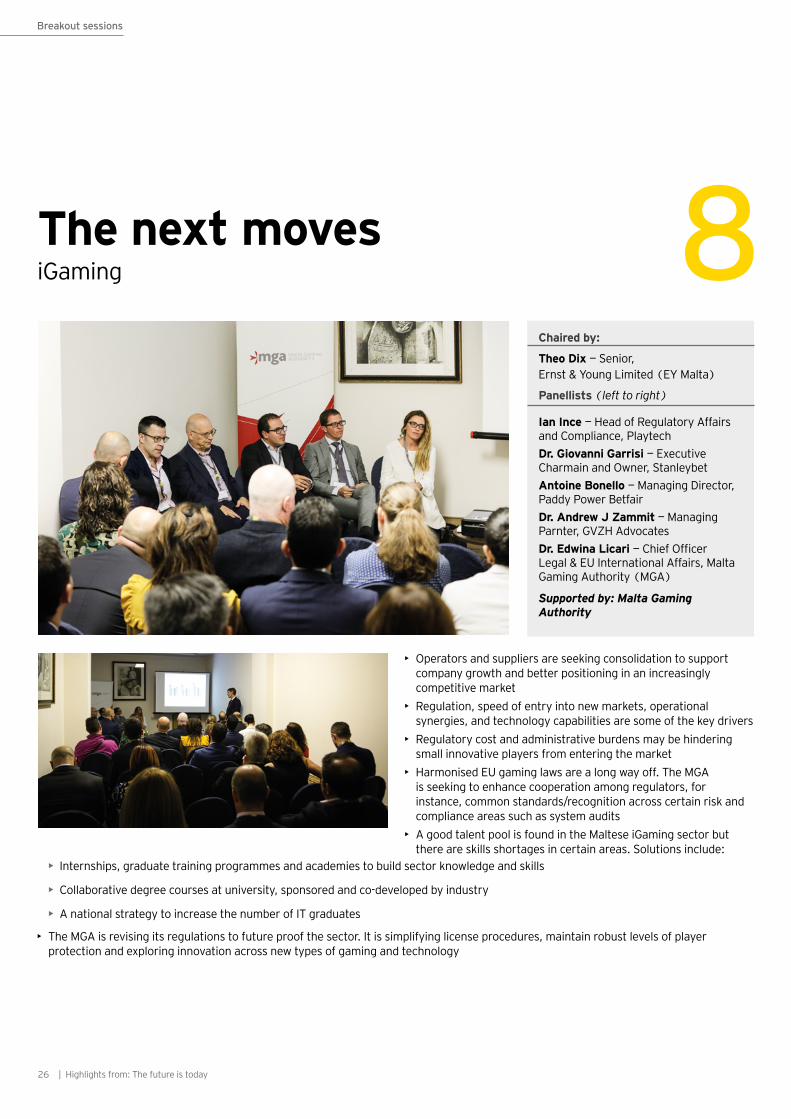

Chaired by:

Theo Dix — Senior, Ernst & Young Limited (EY Malta)

Panellists (left to right)

Ian Ince — Head of Regulatory Affairs and Compliance, PlaytechDr. Giovanni Garrisi — Executive Charmain and Owner, Stanleybet Antoine Bonello — Managing Director, Paddy Power BetfairDr. Andrew J Zammit — Managing Parnter, GVZH AdvocatesDr. Edwina Licari — Chief Officer Legal & EU International Affairs, Malta Gaming Authority (MGA)

Supported by: Malta Gaming Authority

• Operators and suppliers are seeking consolidation to support company growth and better positioning in an increasingly competitive market

• Regulation, speed of entry into new markets, operational synergies, and technology capabilities are some of the key drivers

• Regulatory cost and administrative burdens may be hindering small innovative players from entering the market

• Harmonised EU gaming laws are a long way off. The MGA is seeking to enhance cooperation among regulators, for instance, common standards/recognition across certain risk and compliance areas such as system audits

• A good talent pool is found in the Maltese iGaming sector but there are skills shortages in certain areas. Solutions include:

The next movesiGaming

• Internships, graduate training programmes and academies to build sector knowledge and skills

• Collaborative degree courses at university, sponsored and co-developed by industry

• A national strategy to increase the number of IT graduates

• The MGA is revising its regulations to future proof the sector. It is simplifying license procedures, maintain robust levels of player protection and exploring innovation across new types of gaming and technology

8

EY Malta’s upcoming eventsAt EY, we are committed to building a better working world – one with increased trust and confidence in business, sustainable growth, development of talent in all its forms, and greater collaboration. We want to fuel the discussion around the key issues the working world faces and inspire people and organizations to do more. We believe that our events provide an excellent platform to achieve this goal.

EY’s Regulatory Matters Series

In today’s highly regulated environment, keeping abreast of regulatory changes and matters has become an ongoing challenge. EY’s Regulator Matters Series aims to keep you informed and up to speed with professional analyses of recent regulatory changes and developments in the field of banking, insurance and asset management.

Exceptional Entrepreneurs Series

Entrepreneurs are the change makers who help us build a better working world. Exceptional Entrepreneurs is a speaker series organized by EY, in conjunction with the University of Malta’s TAKEOFF incubator. The event series features some of the world’s best tech entrepreneurs (including the alumni of EY’s global Entrepreneur Of The Year™ programme) and people connected to the industry. They will share their experiences with an audience of aspiring entrepreneurs, investors, students and the wider business community.

27National conference - EY’s 2016 Malta Attractiveness Survey |

ey.com/attractiveness

Our team

EY senior management team:

Ronald A Attard | Country Managing Partner | South East Europe Transaction Advisory Services Leader | [email protected]

Dr. Robert Attard | Partner | Tax | Central and South East Europe Tax Policy Leader | [email protected]

Chris Naudi | Partner | Tax | Head of Tax | [email protected]

Anthony Doublet | Partner | Assurance | Head of Assurance | [email protected]

Shawn Falzon | Partner | Leader | Insurance Assurance Services | [email protected]

Kevin Mallia | Executive Director | Advisory | Head of Advisory | [email protected]

Grace Camilleri | Executive Director | Leader | Banking Advisory Services | [email protected]

Gilbert Guillaumier | Executive Director | Leader | Transaction Support and Infrastructure Services | [email protected]

Christopher Balzan | Executive Director | Leader | Banking Assurance Services | [email protected]

Chris Portelli | Executive Director | Leader | Asset Management Assurance Services | [email protected]

Chris Meilak | Executive Director | Leader | Valuations, Business Modeling and Economic Advisory | [email protected]

Franco Borg | Director | Leader | Risk Advisory Services | [email protected]

Joseph P Galea | Senior Manager | IT Risk and Assurance Leader | [email protected]

Joseph Grech | Senior Manager | Industrial and Commercial Assurance Leader | [email protected]

Ediana Tabone | Senior Manager | Mergers & Acquisitions Leader | [email protected]

Karl Mercieca | Senior Manager | Wealth & Asset Management Advisory Leader | [email protected]

Joette Mallia | Senior Manager | Financial Crime Advisory Leader | [email protected]

For more information on the Malta Attractiveness Survey (MAS) initiative kindly contact:Simon Lee BarberiDirector | Leader | EU Advisory and Malta Attractiveness Survey Tel: +356 2134 2134 [email protected]

Our sponsors

About EY

EY is a global leader in assurance, tax, transaction and advisory services. The insights and quality services we deliver help build trust and confidence in the capital markets and in economies the world over. We develop outstanding leaders who team to deliver on our promises to all of our stakeholders. In so doing, we play a critical role in building a better working world for our people, for our clients and for our communities.

EY refers to the global organization, and may refer to one or more, of the member firms of Ernst & Young Global Limited, each of which is a separate legal entity. Ernst & Young Global Limited, a UK company limited by guarantee, does not provide services to clients. For more information about our organization, please visit ey.com.

© 2016 EYGM Limited. All Rights Reserved.

EYG no: 04011-162GBL

ED None

This material has been prepared for general informational purposes only and is not intended to be relied upon as accounting, tax or other professional advice. Please refer to your advisors for specific advice.

The views of third parties set out in this publication are not necessarily the views of the global EY organization or its member firms. Moreover, they should be seen in the context of the time they were made.

ey.com

EY | Assurance | Tax | Transactions | Advisory

Contact

Simon L BarberiSenior Manager, Ernst & Young Limited Tel: +356 2134 2134 [email protected]

Operated by Mizzi Motors

AUTO LEASING