2012 & Beyond ARSHIA KHURSHID MANAGER SKILLS & LIVELIHOOD BAHAWALPUR.

date post

20-Dec-2015Category

view

216download

2

Herd Behaviour?

Khurshid Ahmad,Chair of Computer Science

Trinity College, Dublin, IRELAND

http://en.wikipedia.org/wiki/Herd_behavio

Economics and Finance

Herd behavior describes how individuals in a group can act together without planned direction. The term pertains to the behavior of animals in herds, flocks and schools, and to human conduct during activities such as stock market bubbles and crashes, street demonstrations, sporting events, religious gatherings, episodes of mob violence and even everyday decision making, judgment and opinion forming.

Dyer, John, et al (2008). Consensus decision making in human crowds. Animal Behaviour. Vol . 75, pp 461-470

Economics and Finance

In groups of animals only a small proportion of individuals may possess particular information, such as a migration route or the direction to a resource. Individuals may differ in preferred direction resulting in conflicts of interest and, therefore, consensus decisions may have to be made to prevent the group from splitting. Recent theoretical work has shown how leadership and consensus decision making can occur without active signalling or individual recognition.

Economics and Finance

Dyer et al (2008) tested these predictions using humans:

1. A small informed minority could guide a group of naıve individuals to a target without verbal communication or obvious signalling

2. Both the time to target and deviation from target were decreased by the presence of informed individuals.

3. When conflicting directional information was given to different group members, the time taken to reach the target was not significantly increased; [...] consensus decision making in conflict situations is possible, and highly efficient.

4. Where there was imbalance in the number of informed individuals with conflicting information, the majority dictated group direction.

Economics and Finance

Dyer et al’s results suggest that the spatial starting position of informed individuals influences group motion, which has implications in terms of crowd control and planning for evacuations.

http://www.investopedia.com/university/behavioral_finance/behavioral8.asp

Economics and Finance

The Dotcom HerdHerd behavior was exhibited in the late 1990s as venture capitalists and private investors were frantically investing huge amounts of money into internet-related companies, even though most of these dotcoms did not (at the time) have financially sound business models. The driving force that seemed to compel these investors to sink their money into such an uncertain venture was the reassurance they got from seeing so many others do the same thing.

Economics and Finance

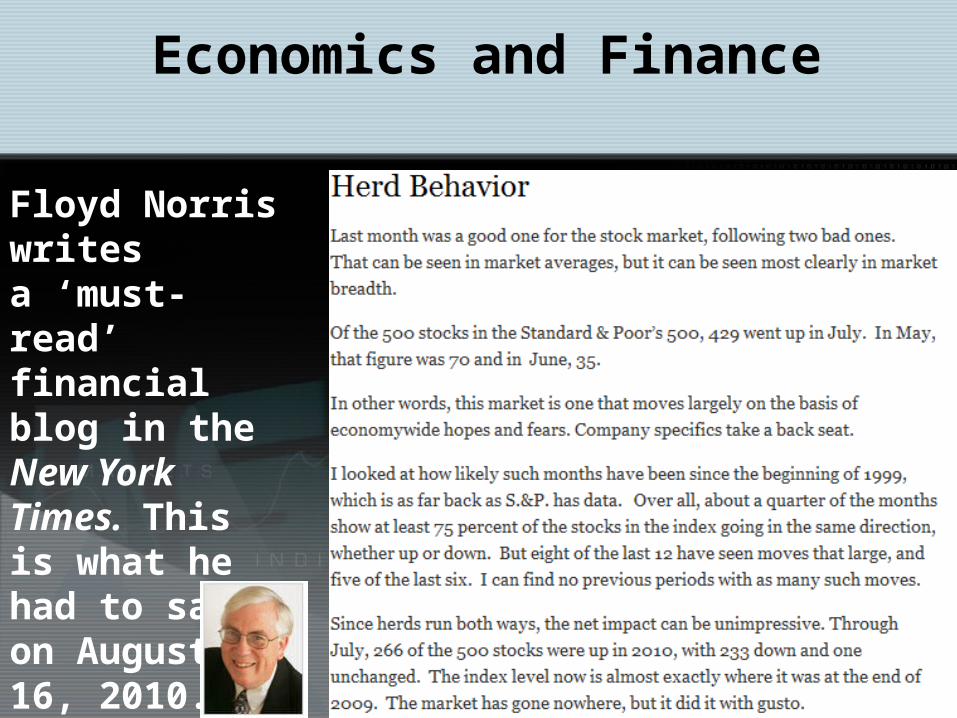

Floyd Norris writesa ‘must-read’ financial blog in the New York Times. This is what he had to say on August 16, 2010.

What interests me is the so-called herd behaviour that can be observed in the different segments of human society.

Exuberant financial trading is one example. Exuberant labeling of groups of people is another. Exuberant scientists is yet another example

Economics, Finance and Behaviour

Exuberant behaviour: reckless risk taking; unwarranted self belief shared with an equally (mis)informed community; no rational basis for evaluation; always related to the 5-year boom-busts we have gotten used to (dot com, sub-prime)

Economics, Finance and Behaviour

Harry F. Griffin. (2006). Did Investor Sentiment Foretell the Fall of ENRON? The Journal of Behavioral Finance 2006, Vol. 7, No. 3, 126–127

Economics and Finance

In the aftermath of the ENRON Corporation failure, […] many investors experienced a financial loss when their ENRON equity holdings lost market value. Griffin (2006) looked at ‘the loss of that market value, and when the capital market first signaled the positive potential of that loss.’

An examination of ENRON optionopen interest from January 1, 2000 through December 31, 2001 reveals that such information was available, observable, and inferential a year earlier.

Economics and Finance

Harry F. Griffin. (2006). Did Investor Sentiment Foretell the Fall of ENRON? The Journal of Behavioral Finance 2006, Vol. 7, No. 3, 126–127

Economics and Finance

Griffin concludes that ‘the most likely reason why the stockholder held on to their ENRON positions long after the erosion of firm value became evident is that senior management made several strong endorsements and recommendations as to the holding of ENRON common equity. Management insistence to maintain and even to increase the size of their positions temporarily assuaged investor’s fears and protected their ego.’ (2006:127)

Harry F. Griffin. (2006). Did Investor Sentiment Foretell the Fall of ENRON? The Journal of Behavioral Finance 2006, Vol. 7, No. 3, 126–127

Markets and Behaviour

Electronic ‘future markets’ for presidential campaigns are better predictors’ of the outcome of the elections than the opinion polls:

http://iemweb.biz.uiowa.edu/graphs/graph_DConv08.cfm

Markets and Behaviour

Electronic ‘future markets’ for presidential campaigns are better predictors’ of the outcome of the elections than the opinion polls:

http://iemweb.biz.uiowa.edu/graphs/graph_DConv08.cfm

Markets and Behaviour

Electronic ‘future markets’ for presidential campaigns are better predictors’ of the outcome of the elections than the opinion polls:

http://iemweb.biz.uiowa.edu/graphs/graph_DConv08.cfm

Markets and Behaviour

Electronic ‘future markets’ for presidential campaigns are better predictors’ of the outcome of the elections than the opinion polls:

http://iemweb.biz.uiowa.edu/graphs/graph_DConv08.cfm

Markets and Behaviour

Electronic ‘future markets’ for presidential campaigns are better predictors’ of the outcome of the elections than the opinion polls:

http://iemweb.biz.uiowa.edu/graphs/graph_RConv08.cfm

We know of traders in financial and commodity markets mimicking each other and not being cognisant of their private information which contradicts what is happening in the markets; we know about long queues of depositors acting on rumour and literally follow their co-depositors; but do institutions act like herds? Banks for example?????????

Economics, Finance and Behaviour

Herd Behaviour causes individuals to over value public information and undervalue private information.

Economics, Finance and Behaviour

Helge Berger and Ulrich Woitek (2005). DOES CONSERVATISM MATTER? A TIME-SERIES APPROACH TO CENTRAL BANK BEHAVIOUR. The Economic Journal, Vol 115 (July), 745–766.

Economics, Finance and Behaviour

There is some evidence of herding from the deliberations of the various committees, and indeed the Council of the revered Budensbank, comprising of some individuals that are open about their econo-political orientation (left/right, conservative/social democrat).

Berger and Woitek (2005) have noted that, for example, in setting the key discount rate ‘political background of [the Council] member matters’. More importantly for us: ‘there is some herd behaviour: the dissenting vote was highly correlated among groups. [...] all groups were more inclined to vote no if members of other groups did so as well.’( ibid:752)

Haiss (2010) has argued that a combination of ‘certain regulatory and governance issues […], the embedded micro-structure of banks [….], and environmental shifts […], force banks into herding behaviour’ and UNFORTUNATELY ‘herd into the same direction’ (ibid:31)’

Economics, Finance and Behaviour

Haiss, Peter (2010). ‘Bank Herding and Incentive Systems as Catalysts for the Financial Crisis’. The IUP Journal of Behavioral Finance. Vol 7 (Nos. 1 &2), pp 30-58

Haiss (2010) suggests that ‘inconsistent decision rules, rigid bank regulations, shareholder focused incentive structures within banks and uncritical adoption of innovations may force the banks into decisions that are micro-functional but macro-dysfunctional.’ (ibid:30). Behavioral aspects may alleviate this catastrophic herding behavior

Economics, Finance and Behaviour

Haiss, Peter (2010). ‘Bank Herding and Incentive Systems as Catalysts for the Financial Crisis’. The IUP Journal of Behavioral Finance. Vol 7 (Nos. 1 &2), pp 30-58

There are, it appears two polar views [bank] herding’:1.Rational Herding;2. Behavioral Herding

Economics, Finance and Behaviour

Haiss, Peter (2010). ‘Bank Herding and Incentive Systems as Catalysts for the Financial Crisis’. The IUP Journal of Behavioral Finance. Vol 7 (Nos. 1 &2), pp 30-58

1. Rational Herding

This includes information cascades: prior investment analyst choices influence post choices small bank operative follow large bank operative into sub-prime and risky loans; readily available information sources have a greater following because every trader thinks that all other traders have access to the sources. Information asymmetries cause cascading.

Reputation-based herding relates to risk-seeking/risk averse behaviour precipitated by investment managers/gurus who are famous/notorious for their choice of assets;

Economics, Finance and Behaviour

Haiss, Peter (2010). ‘Bank Herding and Incentive Systems as Catalysts for the Financial Crisis’. The IUP Journal of Behavioral Finance. Vol 7 (Nos. 1 &2), pp 30-58

1. Rational Herding

Compensation: Investment managers are remunerated on the return performance of other managers […] rather than on absolute performance. This may lead to herd behaviour as investment managers merely follow other investment managers.

Payoff Externalities: Refusal to re-negotiate outstanding loans of a distressed firm by one bank may lead to others to follow (similar to depositors running on distressed banks) in a herd. ‘The observation of payoffs from the repeated actions of other firms may similarly lead to boom and bust patterns in the adoption of financial innovations [like securitization]’ (Haiss 2010:37)

Economics, Finance and Behaviour

Haiss, Peter (2010). ‘Bank Herding and Incentive Systems as Catalysts for the Financial Crisis’. The IUP Journal of Behavioral Finance. Vol 7 (Nos. 1 &2), pp 30-58

Behavioral herdingDependence of behaviour upon the observed behaviour of others, or the results of behaviour;

Procrastination in taking a decision and then rushing to implement it;

Imitation

Responding to affect

Economics, Finance and Behaviour

Haiss, Peter (2010). ‘Bank Herding and Incentive Systems as Catalysts for the Financial Crisis’. The IUP Journal of Behavioral Finance. Vol 7 (Nos. 1 &2), pp 30-58

In an experiment with 7 traders, Cipriani and Guarino conducted a trading experiment where the participants actually traded with ‘real’ money. There was evidence of herd behaviour in their experiment:

Economics, Finance and Behaviour

Marco Cipriani and Antonio Guarino (2008). Herd Behavior in Financial Markets: An Experiment with Financial Market Professionals. IMF Working Paper WP/08/141. (http://www.imf.org/external/pubs/ft/wp/2008/wp08141.pdf)

Decision Percentage

Following Private Information 45.7%

Partially Following Private information 19.6%

Cascade Trading 19.0%

Cascade No-Trading 12.3%

Errors 3.4%

Total 100%

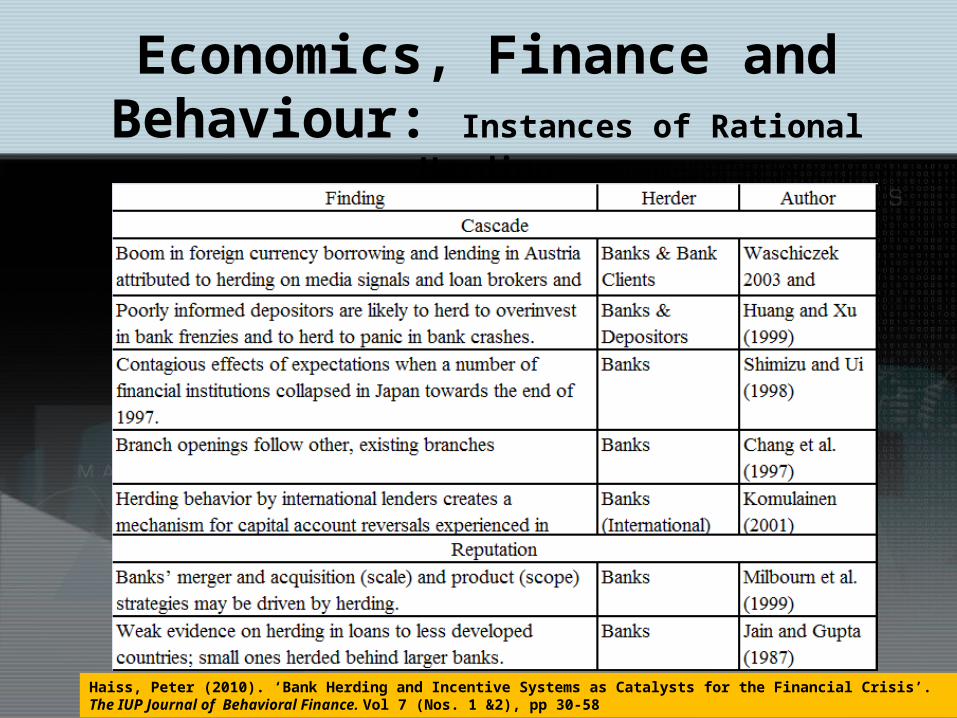

Economics, Finance and Behaviour: Instances of Rational

Herding

Haiss, Peter (2010). ‘Bank Herding and Incentive Systems as Catalysts for the Financial Crisis’. The IUP Journal of Behavioral Finance. Vol 7 (Nos. 1 &2), pp 30-58

Economics, Finance and Behaviour: Instances of Rational

Herding

Haiss, Peter (2010). ‘Bank Herding and Incentive Systems as Catalysts for the Financial Crisis’. The IUP Journal of Behavioral Finance. Vol 7 (Nos. 1 &2), pp 30-58

Economics, Finance and Behaviour: Instances of Rational Herding

Haiss, Peter (2010). ‘Bank Herding and Incentive Systems as Catalysts for the Financial Crisis’. The IUP Journal of Behavioral Finance. Vol 7 (Nos. 1 &2), pp 30-58

Economics, Finance and Behaviour: Instances of Behavioral

Herding

Haiss, Peter (2010). ‘Bank Herding and Incentive Systems as Catalysts for the Financial Crisis’. The IUP Journal of Behavioral Finance. Vol 7 (Nos. 1 &2), pp 30-58

Economics, Finance and Behaviour: Instances of Rational/Behavioral

Herding

Haiss, Peter (2010). ‘Bank Herding and Incentive Systems as Catalysts for the Financial Crisis’. The IUP Journal of Behavioral Finance. Vol 7 (Nos. 1 &2), pp 30-58

Economics, Finance and Behaviour

Haiss, Peter. (2010). Bank Herding and Incentive Systems as Catalysts for the Financial Crisis. The IUP Journal of Behavioral Finance, Vol. 7 (Nos.1&2) pp31-58.

Economics, Finance and Behaviour

Haiss, Peter. (2010). Bank Herding and Incentive Systems as Catalysts for the Financial Crisis. The IUP Journal of Behavioral Finance, Vol. 7 (Nos.1&2) pp31-58.

Incentive structures faced by bank managers appear ‘central’ in mitigating ‘herding, as myopic and asymetric reward structures in many banks were among the key drivers of the excess of the most recent financial boom [..]’ (Haiss 2010:50)