Healthcare Opportunities for Banks

28

New Healthcare Revenue Opportunities for Banks April 5, 2011 Karen Doyle SVP, Sr. Product Manager, First Tennessee Bank John Reynolds President, Healthcare, Government & Biller Solutions, FIS

-

Upload

fis-healthcare -

Category

Health & Medicine

-

view

1.858 -

download

1

description

Presentation given by John Reynolds, President FIS Healthcare Solutions at the 2011 NACHA Payments Conference.

Transcript of Healthcare Opportunities for Banks

New Healthcare Revenue Opportunities for Banks April 5, 2011

Karen DoyleSVP, Sr. Product Manager, First Tennessee Bank

John ReynoldsPresident, Healthcare, Government & Biller Solutions, FIS

John & Karen - introductions

Session Overview

New Healthcare Revenue Opportunities for Banks

The recent healthcare reform bill creates new imperatives for stakeholders to take action to address the industry's chronic inefficiencies − creating opportunities for those that are part of the solution. Leading financial institutions cannot afford to ignore the healthcare sector as it represents significant opportunity for financial ignore the healthcare sector as it represents significant opportunity for financial institutions to strengthen existing customer relationships, grow deposits and fee income, increase household penetration, add new customers and stay ahead of competition. FIS™ and First Tennessee discuss the convergence of the healthcare and financial services industries − and the emerging revenue opportunities for banks, including provider revenue cycle management, payment automation and CDH accounts/services.

2

John

Introduction to FIS and First Tennessee BankExperience in Healthcare

FIS and First Tennessee Bank

4

John

Strategic Focus in Healthcare

We Are an

• Healthcare Payments Solutions Division created in 2006 to create a seamless consumer healthcare experience

• Leverage core financial institution solutions

• Investing in Strategic Acquisitions

− BenSoft We Are an Industry Leader

− BenSoft

− Printing for Systems (PSI)

− Medibank (MBI)

− AdminiSource

− CapMed

• Participate in the CAQH/CORE;ABA/ABIA HSA Council

• Leader in SIGIS and IIAS Initiatives

5

We Provide Mission Critical Solutions

• 60 million healthcare ID cards created in 2009: No. 2 Market Share

• More than 9 million benefit payment cards: No. 1 Market Share

• Over 190 financial institutions utilizing HSA Solution

Strategic Focus in Healthcare

6

Critical Solutions• Over 550,000 HSAs processed

• Over 1 million CDH accounts administered

• 7 million healthcare authorizations per month

• 260+ Third-party administrator clients

• 90+ Health plan clients

• 155+ TPAs use BenSoft full flexible benefits platform

At First Tennessee, we offer a package of dedicated services designed to take much of the manual process out of the provider’s back-office and streamline their cash conversion efforts.

Benefits that save time and money:

• Timely, accurate collection options that accommodate electronic payments, cash and checks

Acceleration of claim payments into cash for debt • Headquartered in Memphis, Tenn.

Treasury Management

• Acceleration of claim payments into cash for debt reduction or investment

• Management reporting tools for effectively monitoring payer performance and coding errors

• Electronic payment solutions provide for the timeliest, most efficient and secure processing of payment transactions

Employee benefits:

• Health Savings Accounts

• Headquartered in Memphis, Tenn.

• $23 billion in assets

• 180 financial centers in and around Tennessee

• 5,400 employees

• Provide a full complement of Treasury and Payment Management Services

Karen

Healthcare 101Today’s rapidly changing, healthcare landscape

Healthcare 101

News Update

Press Release dated, Friday, Oct., 8 2010

The NCVHS recently sent a letter to Secretary Sebelius, Department of Health and Human Services (HHS), advising that CAQH CORE meets the requirements as the authoring entity for operating rules for non-retail pharmacy-related eligibility and claim status transactions outlined in Section 1104 of the ACA.

Health spending rose to a record 17.6% of the U.S. economy in 2009 − an increase of 4% from 2008Source: Wall Street Journal, Jan. 7, 2011

claim status transactions outlined in Section 1104 of the ACA.

John

The Republican-controlled House of Representatives passed a repeal of H.R. 3590, which is not expected to reach the president

News Update

10

Timeline – Administrative SimplificationSection 1104 of H.R. 3590

Transaction Set Adopted Effective Penalty *

Eligibility (270/271) July 1, 2011 Jan. 1, 2013 Jan. 1, 2014

Claims Status (276/277) July 1, 2011 Jan. 1, 2013 Jan. 1, 2014

EFT/ERA (835) July 1, 2012 Jan. 1, 2014 Jan. 1, 2014

Medicare EFT July 1, 2014 Jan. 1, 2015 NA

11

Medicare EFT July 1, 2014 Jan. 1, 2015 NA

Member Services July 1, 2014 Jan. 1, 2016 NA

Notes:Health plans must document compliance with adopted transaction standards or face a penaltyof $1 per covered life, per day.

John

Average Collection Rates

100%

90%

80%

70%

60%

50%

Ave

rage

Col

lect

ions

Rat

e

Healthcare providers have abysmal receivables aging and bad debt rate.

Industry bad debt is widely gauged at around 50%.

Source: MGMA, Celent

40%

30%

20%

10%

0%

Number of DAR (Days in Accounts Receivable)

Ave

rage

Col

lect

ions

Rat

e

1-30 31-60 61-90 91-180 181-270 271-365 After 1 Year

around 50%.

John & Karen

30%

25%

20%

% P

erce

nt R

espo

nsib

ility

Patient Self-pay Ratios

Healthcare providers are going to have to increasingly collect from patients rather than from health plan carriers.

Source: Celent, Effective Solutions, athenahealth, CMS

20%

15%

10%

% P

erce

nt R

espo

nsib

ility

2007 2008 2009 2010 2011 2012

John & Karen

Convergence of Health and WealthOpportunities for financial institutions

and Wealth

Why Enter the Healthcare Market?

• Add potentially thousands of new client relationships– Practice Management System (PMS)

vendors– Claim adjudication vendors– Health payers and providers– Health payers and providers– All of us (consumers = members)

• Stickier, household penetration– Lines of credit– Mortgage/refinancing– Equipment financing/leasing– High net worth portfolio management

15

Believe it or not, you have much to offer.

Karen

What to Think About Next

How do your healthcare initiatives fit with your…..• Strategic goals • Growth plan• Client base • Timeline• Risk exposure

Identifying the right product(s)…..

16

Identifying the right product(s)…..• Evaluate …– Product/service gaps– Time to market– Development cost– Internal expertise (sales and

support)• Risk …– Reputation– Regulatory

• Expected benefits…

• Deployment options…– Develop “in-house”– Outsource– Referral

• Vendor Selection…– Strength of vendor– Product maturity– Product strategy– Partnership (defined roles)– References

Karen

Health and Financial Network SolutionsProduct overview, based on your client’s needs:HealthGateway and HealthCollect

Network Solutions

Revenue Cycle (RCM) FlowClaim creation, submission and reconciliation

18

HealthGateway HealthCollect HealthGateway

Karen & John

HealthGateway

• Complete, provider dashboard encompassing all claims and payment activity– Re-association of claims and payments– Integrated view of all receivables – payer,

patient, lockbox integration

Target Market: Providers

Value Proposition: Integrated claim submission, tracking, reconciliation and clearinghouse solution;

• Provider benefits– Elimination of manual processes and

disconnected systems– Reduced eligibility/claims handling costs due to

electronic processes– Provider member with an estimated cost, at time

of care– Vendor consolidation

19

clearinghouse solution; excellent complement to a weak or legacy PMS system

John & Karen

What’s New and Innovative

• Recessionary economy/rising healthcare costs creating significant market shift– Employers moving to low cost health plans, creating a cost shift from payers to

employees/consumers– Need for providers to supply members with an estimate of services rendered

• Providers need to shift revenue collections focus from payers to patients.

20

• Providers need to shift revenue collections focus from payers to patients.– Provider revenue collections currently lack patient cost transparency– 37% of provider locations expected to have RCM solutions by 2014

What’s on the horizon?

ID verification mobile ID cards patient estimatorpayment assurance and compliancy propensity to pay

John

Revenue Cycle (RCM) FlowPatient statement and payment

21

HealthGateway HealthCollect HealthGateway

John

HealthCollect

• White label/banking branding • Comprehensive print and electronic bill

presentment and payment solution– Streamlined bill creation– Electronic bill presentment (and

economical/streamlined print distribution)– Flexible payment options – credit, debit, ACH

Target Market: Providers

Value Proposition: Integrated receivables management, patient payments and collections; excellent compliment to the patient – Flexible payment options – credit, debit, ACH

acceptance via phone or Web

• Provider benefits– Ease of payment tracking and reconciliation– Reduction in bad debt/unpaid claims– Improved cash flow and collections

22

compliment to the patient accounting system

John & Karen

What’s New and Innovative

• Integration with provider PMS platform (their system or record)

• Receivables management– First-party collections– Third-party collections

What’s on the horizon?Mobile paymentsSMS textID verification

23

–

• Connectivity and “look and feel” to the partner’s Web site– Single Sign On (SSO)

John

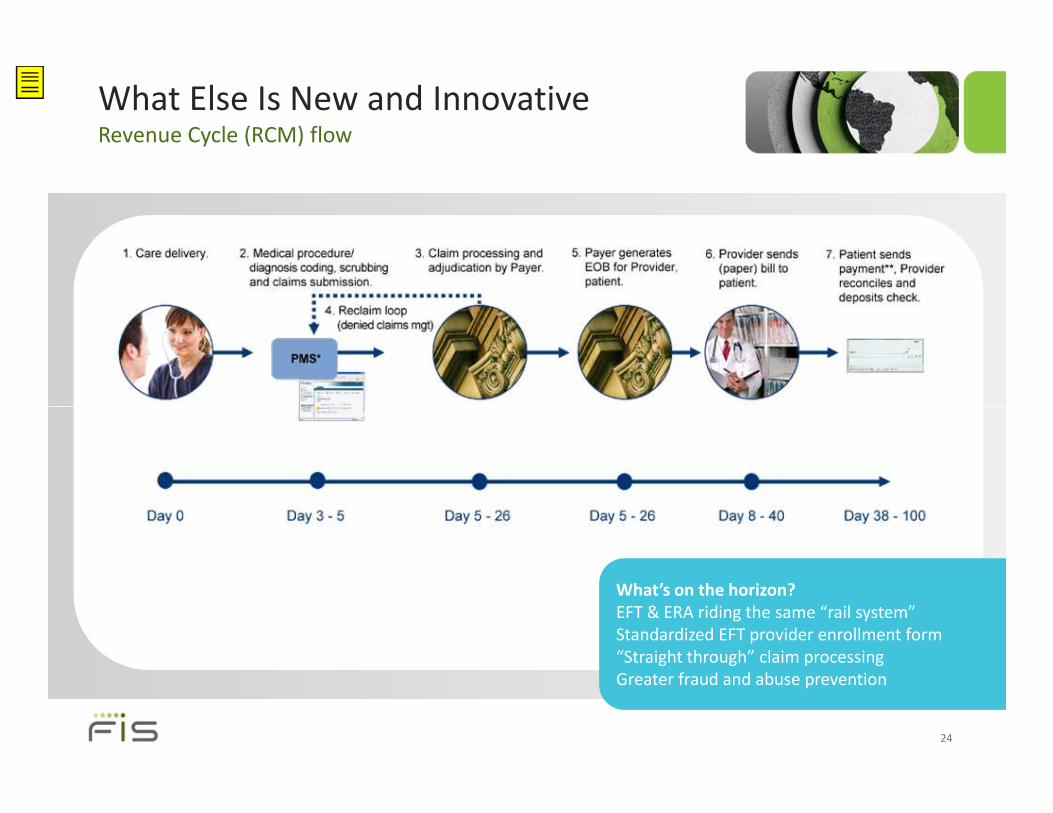

What Else Is New and InnovativeRevenue Cycle (RCM) flow

24

What’s on the horizon?EFT & ERA riding the same “rail system”Standardized EFT provider enrollment form“Straight through” claim processingGreater fraud and abuse prevention

John & Karen

ConclusionConclusion

Concluding Thoughts

• Leading financial institutions cannot afford to ignore the healthcare sector• Largest fast-growing sector of the

economy – and growth is likely to continue for the foreseeable future

Automating the Claim Payments

Process

• Significant opportunities for new entrants• Significant unmet customer needs• Retention and new customer

acquisition opportunity• Multiple product sales opportunity

26

Activating the Power of Point

of Service Streamline

Patient Pays

What will be your institution’s story in healthcare?

John & Karen

Questions and AnswersQuestions and Answers

Karen DoyleThank you Karen DoyleSVP, Sr. Product Manager, First Tennessee Bank

John ReynoldsPresident, Healthcare, Government & Biller

Solutions, FIS

Thank youKaren DoyleSVP, Sr. Product Manager, First Tennessee Bank

John ReynoldsPresident, Healthcare, Government & Biller Solutions, FIS