Healthcare Insights from Clearwater International...

6

Animal health market breakdown clearthought Healthcare Insights from Clearwater International Animal Health Increasing rates of pet ownership plus innovation in disease prevention and treatment are leading to significant sector growth One of the family The first is the growing demand for protein- rich foods across the world which has increased demand for commercial animal vaccines. To mitigate the risk of disease in livestock, producers rely heavily on vaccines and feed additives. As such, animal health pharmaceuticals now account 1 for 61% of the global market followed by biological products (26%) and medical feed additives (13%). Secondly, we have seen a significant increase in pet ownership and the ‘humanisation’ of companion animals, as people increasingly treat their pets like members of the family and more people use pets to counteract loneliness. Annual spending on pets reached more than ¤90bn in 2016 2 . Taken together, these trends mean the animal health market is forecast to grow at a CAGR of 3% until 2020. Commercial animal health products currently account for 59% of the market, with companion animal products making up the remainder 3 . M&A activity Given these market dynamics the sector has seen significant M&A activity. One of the most notable deals the industry has ever seen came earlier this year when Mars paid ¤8.6bn for US animal hospital chain VCA, a deal that certainly made investors stand up and take notice. Veterinary services have, in particular, benefitted from the increasing humanisation of pets. Historically, the market was highly fragmented with large numbers of smaller practices, but in recent years we have seen a number of private equity players enter the market with ambitious buy-and-build strategies. Across the wider animal health sector there has been significant M&A activity too, and this is expected to continue as larger companies look to acquire the unique products and capabilities of smaller players. Large pharmaceutical companies have also entered the market. For example, one of Bayer’s immediate strategic objectives is to strengthen its leadership in the companion animal segment and achieve profitable growth in the livestock segment. The company aims to do this by expanding its research and development activities, and through selective in- licensing and acquisitions. Many other large pharmaceutical companies are also following suit. 1 Vetnosis 2 Euromonitor 3 Vetnosis The global animal health market - which includes commercial animal products and companion animals such as pets - is experiencing significant growth driven by the convergence of two mega trends. Sector 41% 59% Commercial animal products Companion animals Geography 31% 23% 46% Americas Europe Rest of the World Product 13% 26% 61% Pharmaceuticals Biologicals Medical feed additives SOURCE: Vetnosis

-

Upload

hoangtuong -

Category

Documents

-

view

223 -

download

0

Transcript of Healthcare Insights from Clearwater International...

Animal health market breakdown

clearthoughtHealthcare Insights from Clearwater International

Animal Health Increasing rates of pet ownership plus innovation in disease prevention and treatment are leading to signifi cant sector growth

One of the family

The fi rst is the growing demand for protein-rich foods across the world which has increased demand for commercial animal vaccines. To mitigate the risk of disease in livestock, producers rely heavily on vaccines and feed additives. As such, animal health pharmaceuticals now account1 for 61% of the global market followed by biological products (26%) and medical feed additives (13%).

Secondly, we have seen a signifi cant increase in pet ownership and the ‘humanisation’ of companion animals, as people increasingly treat their pets like members of the family and more people use pets to counteract loneliness. Annual spending on pets reached more than ¤90bn in 20162.

Taken together, these trends mean the animal health market is forecast to grow at a CAGR of 3% until 2020. Commercial animal health products currently account for 59% of the market, with companion animal products making up the remainder3.

M&A activity

Given these market dynamics the sector has seen signifi cant M&A activity. One of the most notable deals the industry has ever seen came earlier this year when Mars paid ¤8.6bn for US animal hospital chain VCA, a deal that certainly made investors stand up and take notice.

Veterinary services have, in particular, benefi tted from the increasing humanisation of pets. Historically, the market was highly fragmented with large numbers of smaller practices, but in recent years we have seen a number of private equity players enter the market with ambitious buy-and-build strategies.

Across the wider animal health sector there has been signifi cant M&A activity too, and this is expected to continue as larger companies look to acquire the unique products and capabilities of smaller players.

Large pharmaceutical companies have also entered the market. For example, one of Bayer’s immediate strategic objectives is to strengthen its leadership in the companion animal segment and achieve profi table growth in the livestock segment. The company aims to do this by expanding its research and development activities, and through selective in-licensing and acquisitions. Many other large pharmaceutical companies are also following suit.

1 Vetnosis2 Euromonitor3 Vetnosis

The global animal health market - which includes commercial animal products and companion animals such as pets - is experiencing signifi cant growth driven by the convergence of two mega trends.

Sector41% 59%

Commercial animal products

Companion animals

Geography

31%

23%

46%

Americas

Europe

Rest of the World

Product

13%

26% 61%

Pharmaceuticals

Biologicals

Medical feed additives

SOURCE: Vetnosis

clearthought | 2017 Healthcare Insights from Clearwater International

Market driversPet ownership

In the companion animal space, growth is being driven by rising middle-class household incomes, the humanisation of animals, and increasing rates of pet ownership. For instance, it is suggested that as many as two-thirds of pet owners now view their pets as members of the family.

A significant proportion of this spending is in relation to pet health and veterinary services to increase pet lifespans, and to treat diseases such as obesity which has become more prevalent in animals just as it has among humans. Spending on animal health has also been boosted by increasing take-up of pet insurance, especially in the European market, with some countries such as Sweden experiencing very high levels of insurance.

Disease

New variations of animal diseases pose both challenges and opportunities for the market, leading to constant innovation.

For instance, The Animal Health Institute says member companies spend 10–12% of revenues investing in innovation to combat the challenges caused by new disease.

Over the past few decades, innovation through R&D has led to developments that have resulted in dramatic improvements in the prevention and treatment of animal health issues such as flea and tick infestation, Lyme disease, rabies, diabetes, feline leukaemia, and other types of cancers. This has both increased companion animal lifespans and also improved the global food chain.

Regulation

The animal pharma segment is less heavily regulated than the human pharma market and so is attractive to large pharmaceutical companies and other investors. Requirements for animal pharma products are much less stringent so animal health products have a much shorter time to market, meaning there is less pipeline risk for new products when compared to human pharma.

The sector has experienced minimal threat from generic brands because of the high barriers to entry, but this is changing due to the combination of regulatory changes that promote generics and distribution channel shifts.

Emerging economies

Strongly driven by China, the Asia-Pacific region has seen the fastest growth rate in the animal health market.

In particular, China has a mandatory vaccination programme for certain animal diseases and, historically, has supplied these vaccines to farmers at very low prices. This is, however, expected to change as the government wants to drive competition in the market.

The growth in animal vaccinations in China now represents a significant opportunity to current players as the market is expected to consolidate quickly.

clearthought | 2017 Healthcare Insights from Clearwater International

M&A activity The sector has recorded slightly fewer deals globally over the past 12 months - 39 deals compared to 46 transactions in the preceding 12 months. Total aggregated deal value was ¤10.3bn in the past year, compared to ¤2.4bn in the 12 months before1 although this figure was skewed by a number of mega deals including the Mars/VCA and LG Chem/LG Life Sciences transactions.

The US has been the most active market with 42% of total deals. However, there was significant growth in Indian and Chinese markets which saw five deals compared to just three in the preceding 12 months.

In the veterinary care sector, high levels of European M&A activity have been driven by consolidation as private equity firms pursue buy-and-build strategies. In the animal pharma sector, companies are increasingly entering new geographic markets through acquisition.

Rise of big players

The UK is a good example of how the veterinary services market is now dominated by several sizeable corporate players. These include Pets at Home, Independent Vets, CVS and the Linnaeus Group.

While the market was previously characterised by a large number of small family-owned practices, decreased regulation and higher training costs have led to many of the smaller players selling up to more sizeable groups.

These larger companies offer centralised back office support such as payroll, HR functions, training and bulk buying benefits, which can lead to huge cost savings and better profit margins.

Many of these groups are now consolidating, trying to buy up small animal clinics and referral centres to drive in-house referral opportunities, and to add scale to their businesses. They are also moving into

more specialist areas such as the equine and farm vetting ends of the market. For instance, last year Pets at Home acquired a 90% stake in Eye-Vet, a specialist veterinary ophthalmology centre, while Independent Vetcare acquired Robson and Prescott, a provider of veterinary hydrotherapy.

Some companies are also diversifying into other areas including pet crematoriums, online pharmacies and shops, laboratories, out-of-hours surgeries and vet locum agencies.

In Ireland - where the agrifood sector is worth ¤26bn - several major players have emerged such as Chanelle, a producer of generic animal pharmaceuticals and Ireland’s largest indigenous pharmaceuticals manufacturer.

The company has more than 1,700 animal health licenses registered in the EU and 500 animal health licenses registered

across the rest of the world. It also holds the largest number of registered veterinary licences of any company in Europe.

Cross-border moves

These big players are increasingly looking beyond their own shores.

Nordic Capital-backed AniCura of Sweden, for example, now has up to 200 animal health clinics across Europe. And Irish player Bimeda, a manufacturer and distributor of animal health products and veterinary pharmaceuticals, now operates in more than 70 countries. It has made a number of recent acquisitions to enter new markets and expand its product base, including acquiring the marketing rights to Ceva Animal Health’s portfolio of equine products in the US.

Dechra of the UK has also been highly acquisitive. Last year it acquired Apex Laboratories Pty, an Australian provider of generic and proprietary veterinary pharmaceuticals and pet care products.

It also bought Putney, a US-based developer and distributor of generic drugs for pets, and Brazilian veterinary pharmaceuticals provider Laboratorios Brovel.

Other notable cross-border deals include Valeant’s acquisitions of Humax Pharmaceutical S.A, Farmatech S.A. and Cambridge S.A.S.; Merial’s acquisition of a manufacturing facility in Barceloneta, Puerta Rico from Merck & Co; and Alivira’s acquisition of Interchange Veterinaria Industria e Comercio SA, the Brazilian producer of veterinary pharmaceutical preparations.

Private equity

The animal health sector is attractive to private equity for a number of reasons. In animal pharma the R&D model is more predictable and less risky than the human pharmaceuticals market, while animal pharma companies also have a lower-risk revenue stream as growth is steady and predictable due to expected long product life.

The fragmented veterinary care market has been a particular focus for buyers implementing a buy-and-build strategy, with the sector’s attractiveness underpinned by long-term positive market trends.

The trend has been particularly evident in the UK and Nordic markets, driven by the deregulation of the sector. Previous regulatory barriers to creating larger vet care groups have been lowered in both regions, paving the way for economies of scale.

Although veterinarians have historically owned their own clinics, the prospect of relinquishing some of the administrative and financial burden that comes with operating an independent practice has been welcomed by many, as has the investment in expensive education, equipment and IT that can be made by new investors.

1 Capital IQ

The US has been the most active market with 42% of total deals. However, there was significant growth in Indian and Chinese markets which saw five deals compared to just three in the preceding 12 months.

clearthought | 2017 Healthcare Insights from Clearwater International

Announced date Target name Country Target description Acquirer name Country Deal size (¤m)

Jun 17 Altano Gruppe GmbH Germany Operator of equine clinics Ufenau Capital Partners AG Germany n.a

Dec 16 Independent Vetcare Limited UK Owns and operates veterinary practices in the UK

EQT Partners AB Sweden n.a

Dec 15 ALK-Abelló A/S, European veterinary business

Denmark Develops, manufactures, and markets immunotherapy products for veterinary use

Fidelio Capital Sweden n.a

Jul 15 North Downs Specialist Referrals Limited

UK Provides multi-disciplinary referral services for dogs and cats

Linnaeus Group Limited UK n.a

Feb 15 Audevard SAS France Provides medical and dietary supplement solutions for equine health

Ekkio Capital France n.a

Jan 15 PetVet Care Centers, Inc. US Provides services for veterinary clinics and practices

Teachers' Private Capital Canada 368.9

Sep 14 Willows Veterinary Services Limited

UK Owns and operates veterinary practices

Sovereign Capital Partners LLP

UK n.a

Jul 14 Independent Vetcare Limited UK Owns and operates veterinary practices

Summit Partners LLP US n.a

Announced date Target name Country Target description Acquirer name Country Deal size (¤m)

Jun 17 Village Vet Limited UK Provides veterinary services Linnaeus Group Limited UK n.a

May 17 Cevasa SA Argentina Veterinary pharmaceutical products manufacturer

Farmabase Saúde Animal Ltda Brazil n.a

Apr 17 Casvet Portugal Operates veterinary hospitals and clinics

OneVet Group SA Portugal n.a

Mar 17 Pieneläinklinikka Tuhatjalka Oy Finland Operates a veterinary clinic Omaeläinklinikka Oy Finland n.a

Feb 17 Kliniek voor Gezelschapsdieren Eersel B.V.

Netherlands Operates a veterinary clinic AniCura AB Sweden n.a

Feb 17 Donnachie & Townley Limited UK Provides veterinary services for farm and companion animals

Linnaeus Group Limited UK n.a

Feb 17 VRCC Limited UK Provides veterinary services for companion animals

Linnaeus Group Limited UK n.a

Jan 17 VCA, Inc. US Animal healthcare company Mars, Inc. US 8674.0

Oct 16 Jaguar Animal Health, Inc. US Develops and commercialises gastrointestinal products for companion and production animals

Napo Pharmaceuticals, Inc. UK n.a

Sep 16 Apex Laboratories Australia Manufactures and markets generic and proprietary veterinary pharmaceuticals and petcare products

Dechra Pharmaceuticals plc UK 37.0

Sep 16 LG Life Sciences South Korea Researches and commercialises animal health products and specialty chemicals

LG Chem Ltd. South Korea 1156.0

Jul 16 Vallée S.A. Brazil Manufacturer and distributor of vaccines, therapeutics and supplements for veterinary use

Merck Sharp & Dohme Saude Animal Ltda.

Brazil 358.9

Mar 16 Putney, Inc. US Develops and sells generic prescription medicines for pets

Dechra Pharmaceuticals plc UK 180.0

Mar 16 Polchem Hygiene Laboratories Pvt. Limited

India Biosecurity and biotechnology company

Ceva Sante Animale S.A. France n.a

Mar 16 Rubinum S.A. (50%) Spain Animal nutrition company Lallemand, Inc. Canada n.a

Feb 16 CAPNA, Inc. US Owns and operates veterinary hospitals

VCA, Inc. US 317.0

Jan 16 MVP Laboratories, Inc. US Manufactures vaccines for livestock animals

Phibro Animal Health Corporation

US 43.0

Jan 16 Zoetis, Inc. Select brands and manufacturing operations in Haridwar

US Manufacturing operations in Haridwar of global animal health company

Zydus Animal Health Limited India 27.0

Recent private equity transactions

Recent trade transactions

SOURCE: Capital IQ, Mergermarket

SOURCE: Capital IQ, Mergermarket

clearthought | 2017 Healthcare Insights from Clearwater International

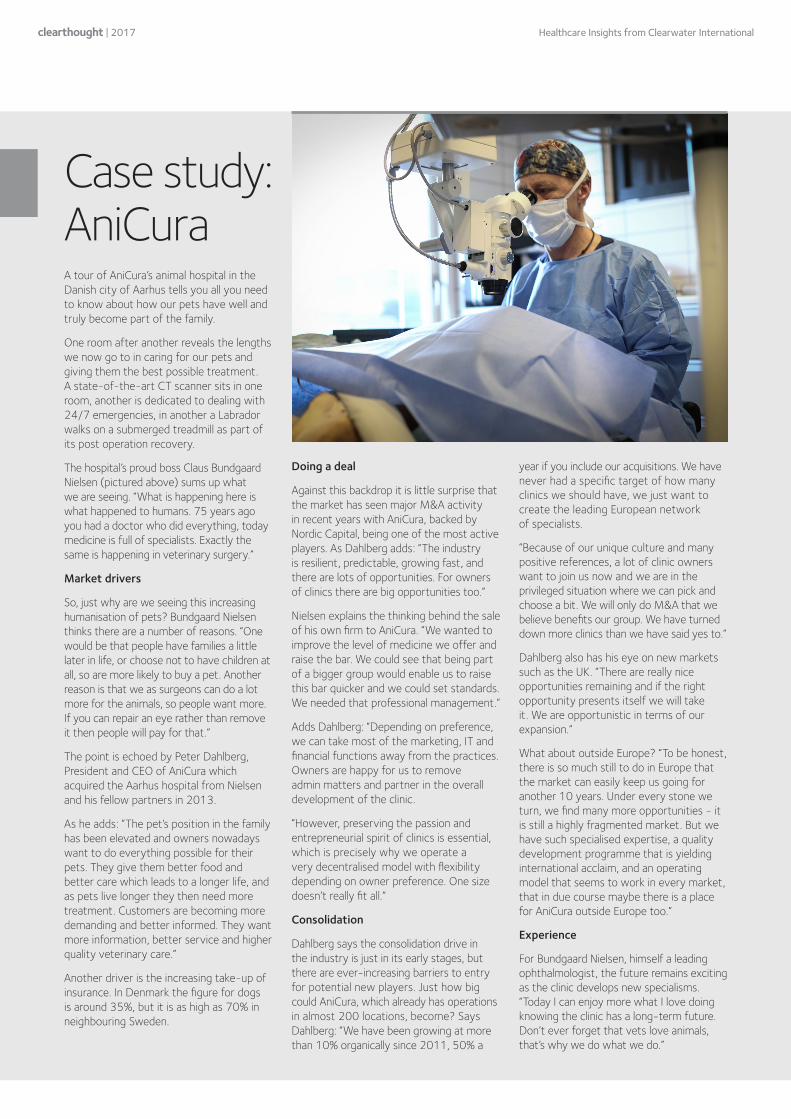

A tour of AniCura’s animal hospital in the Danish city of Aarhus tells you all you need to know about how our pets have well and truly become part of the family.

One room after another reveals the lengths we now go to in caring for our pets and giving them the best possible treatment. A state-of-the-art CT scanner sits in one room, another is dedicated to dealing with 24/7 emergencies, in another a Labrador walks on a submerged treadmill as part of its post operation recovery.

The hospital’s proud boss Claus Bundgaard Nielsen (pictured above) sums up what we are seeing. “What is happening here is what happened to humans. 75 years ago you had a doctor who did everything, today medicine is full of specialists. Exactly the same is happening in veterinary surgery.”

Market drivers

So, just why are we seeing this increasing humanisation of pets? Bundgaard Nielsen thinks there are a number of reasons. “One would be that people have families a little later in life, or choose not to have children at all, so are more likely to buy a pet. Another reason is that we as surgeons can do a lot more for the animals, so people want more. If you can repair an eye rather than remove it then people will pay for that.”

The point is echoed by Peter Dahlberg, President and CEO of AniCura which acquired the Aarhus hospital from Nielsen and his fellow partners in 2013.

As he adds: “The pet’s position in the family has been elevated and owners nowadays want to do everything possible for their pets. They give them better food and better care which leads to a longer life, and as pets live longer they then need more treatment. Customers are becoming more demanding and better informed. They want more information, better service and higher quality veterinary care.”

Another driver is the increasing take-up of insurance. In Denmark the figure for dogs is around 35%, but it is as high as 70% in neighbouring Sweden.

Doing a deal

Against this backdrop it is little surprise that the market has seen major M&A activity in recent years with AniCura, backed by Nordic Capital, being one of the most active players. As Dahlberg adds: “The industry is resilient, predictable, growing fast, and there are lots of opportunities. For owners of clinics there are big opportunities too.”

Nielsen explains the thinking behind the sale of his own firm to AniCura. “We wanted to improve the level of medicine we offer and raise the bar. We could see that being part of a bigger group would enable us to raise this bar quicker and we could set standards. We needed that professional management.“

Adds Dahlberg: “Depending on preference, we can take most of the marketing, IT and financial functions away from the practices. Owners are happy for us to remove admin matters and partner in the overall development of the clinic.

“However, preserving the passion and entrepreneurial spirit of clinics is essential, which is precisely why we operate a very decentralised model with flexibility depending on owner preference. One size doesn’t really fit all.”

Consolidation

Dahlberg says the consolidation drive in the industry is just in its early stages, but there are ever-increasing barriers to entry for potential new players. Just how big could AniCura, which already has operations in almost 200 locations, become? Says Dahlberg: “We have been growing at more than 10% organically since 2011, 50% a

year if you include our acquisitions. We have never had a specific target of how many clinics we should have, we just want to create the leading European network of specialists.

“Because of our unique culture and many positive references, a lot of clinic owners want to join us now and we are in the privileged situation where we can pick and choose a bit. We will only do M&A that we believe benefits our group. We have turned down more clinics than we have said yes to.”

Dahlberg also has his eye on new markets such as the UK. “There are really nice opportunities remaining and if the right opportunity presents itself we will take it. We are opportunistic in terms of our expansion.”

What about outside Europe? “To be honest, there is so much still to do in Europe that the market can easily keep us going for another 10 years. Under every stone we turn, we find many more opportunities - it is still a highly fragmented market. But we have such specialised expertise, a quality development programme that is yielding international acclaim, and an operating model that seems to work in every market, that in due course maybe there is a place for AniCura outside Europe too.”

Experience

For Bundgaard Nielsen, himself a leading ophthalmologist, the future remains exciting as the clinic develops new specialisms. “Today I can enjoy more what I love doing knowing the clinic has a long-term future. Don’t ever forget that vets love animals, that’s why we do what we do.”

Case study: AniCura

Healthcare Insights from Clearwater International clearthought | 2017

www.clearwaterinternational.com

Deal highlightsSome of our recent healthcare deals

Meet the team

Leading animal hospital in Denmark

Clearwater International advised Varde Dyrehospital on its sale to AniCura, backed by private equity groups

Varde Dyrehospital

Danish animal hospital, treating 12,000 patients annually

Clearwater International advised Aarhus Dyrehospital on its sale to Djursjukhusgruppen

Aarhus Dyrehospital

Group of private clinics located in the east of France

Clearwater International advised C2S, a company owned by Bridgepoint, on the acquisition of Avenir Santé, one of the leading private clinic companies in Bourgogne-Franche Comté

C2S

Pressure area care solutions

Clearwater International advised private equity house NorthEdge Capital on the MBO of Direct Healthcare Services

Direct Healthcare Services

Manufacturer of hospital and home healthcare beds, furniture and accessories

Clearwater International advised Sidhil Ltd on its sale to Drive DeVilbiss Healthcare Ltd

Sidhil Group

Company specialising in home care services for the elderly

Clearwater International advised Colisée Group on the acquisition of Nouvel Horizon Services

Colisée Group

CHINA • DENMARK • FRANCE • GERMANY • IRELAND • PORTUGAL • SPAIN • UK • US

Ramesh Jassal International Head of Healthcare, UK+44 845 052 [email protected]

Franc KaiserPartner, China+ 86 21 6341 0699 [email protected]

Louise Kamp NørbækAssociate Director, Denmark+45 40 17 86 [email protected]

Philippe GuezenecPartner, France+33 1 53 89 [email protected]

Markus Otto,Partner, Germany+49 611 360 39 [email protected]

John CurtinPartner, Ireland+353 1 517 58 [email protected]

Rui MirandaPartner, Portugal+351 918 766 [email protected]

Miguel Ángel LorenzoDirector, Spain+34 659 094 [email protected]