HealthCare Global Enterprises Limited -...

25

HealthCare Global Enterprises Limited November 2017 ©2017, HCGEL – All Rights Reserved

Transcript of HealthCare Global Enterprises Limited -...

HealthCare Global Enterprises Limited

November 2017

©2017, HCGEL – All Rights Reserved

Disclaimer

THIS PRESENTATION AND ITS CONTENTS ARE CONFIDENTIAL AND ARE NOT FOR RELEASE, PUBLICATION OR DISTRIBUTION, IN WHOLE OR IN PART,DIRECTLY OR INDIRECTLY, IN OR INTO OR FROM THE UNITED STATES OF AMERICA, CANADA, AUSTRALIA, JAPAN OR ANY JURISDICTION WHERE SUCHDISTRIBUTION IS UNLAWFUL.

This presentation has been prepared by HealthCare Global Enterprises Limited (the "Company"). These materials are not for publication or distribution,directly or indirectly, in or into the United States (including its territories and possessions, any state of the United States and the District of Columbia). Thesematerials are not an offer of securities for sale into the United States, Canada or Japan. Any securities of the Company have not been and will not be registeredunder the U.S. Securities Act of 1933, as amended, and may not be offered or sold in the United States, except pursuant to an applicable exemption fromregistration. No public offering of any securities of the Company is being made in the United States.

The information contained in this presentation is for information purposes only and does not constitute or form part of an offer or invitation for sale orsubscription of or solicitation or invitation of any offer to buy or subscribe for any securities, nor shall it or any part of it form the basis of or be relied on inconnection with any contract, commitment or investment decision in relation thereto in India, the United States or any other jurisdiction.

No person accepts any liability whatsoever for any loss howsoever arising from the use of this document or of its contents or otherwise arising in connectiontherewith. The information set out herein may be subject to updating, completion, revision, verification and amendment without notice and such informationmay change materially. Financial information contained in this presentation has been derived from the restated consolidated and standalone financialstatements of the Company and have been rounded off to the next integer, except percentages which have been rounded off to one decimal point.

This presentation contains certain "forward looking statements". Forward‐looking statements are based on certain assumptions and expectations of futureevents. Actual future performance, outcomes and results may differ materially from those expressed in forward‐looking statements as a result of a number ofrisks, uncertainties and assumptions. Although the Company believes that such forward‐looking statements are based on reasonable assumptions, it can giveno assurance that such expectations will be met. Neither the Company nor any of its advisors or representatives assumes any responsibility to updateforward-looking statements or to adapt them to future events or developments.

This presentation includes certain industry data and projections that have been obtained from industry publications and surveys. Industry publications andsurveys and forecasts generally state that the information contained therein has been obtained from sources believed to be reliable, but there is no assurancethat the information is accurate or complete. Neither the Company nor any of its advisors or representatives have independently verified any of the data fromthird-party sources or ascertained the underlying economic assumptions relied upon therein. No representation or claim is made that the results orprojections contained in this presentation will actually be achieved. All industry data and projections contained in this presentation are based on data obtainedfrom the sources cited and involve significant elements of subjective judgment and analysis, which may or may not be correct. For the reasons mentionedabove, you should not rely in any way on any of the projections contained in this presentation for any purpose.

This presentation is based on information regarding the Company and the economic, regulatory, market and other conditions as in effect on the date hereof. Itshould be understood that subsequent developments may affect the information contained in this presentation, which neither the Company nor its advisorsor representatives are under an obligation to update, revise or affirm.

© 2017 , ALL RIGHTS RESERVED. WWW.HCGEL .CO M

Table of Contents

© 2017 , ALL RIGHTS RESERVED. WWW.HCGEL .CO M

Overview of HCG

Financial Highlights and

Updates

Appendix

Overview of HCG

Comprehensive cancer diagnosis and

treatment services (through radiation

therapy, medical oncology and surgery)

206 comprehensive cancer centers, 3

freestanding diagnostic centers and one

day care chemotherapy center as of

September 30, 2017

Comprehensive reproductive medicine

services including assisted reproduction,

gynecological endoscopy and fertility

preservation

4 fertility centers in Bengaluru, 1 in Delhi, 1

in Chandigarh and 1 in Mumbai as of

September 30, 2017

Clinical reference laboratory with

specialization in oncology

Undertakes clinical trial management and

R&D services to pharmaceutical and

biotech companies

37 multispecialty hospitals in Ahmedabad,

Bhavnagar and Hubli as at September 30,

2017

Cancer Care

Fertility

Treatment

Clinical

Reference

Laboratory

Multi-specialty

Hospital

Snapshot of the Business

Specialty healthcare provider with a focus

on cancer and fertility

Largest1 provider of cancer care in India

under the “HCG” brand

Leading provider of fertility treatment under

the “Milann”2 brand

Key financials (FY17) : Revenue – INR

7,001mn, EBITDA before exceptional

items3 - INR 1,050mn and Net Profit – INR

222mn4

NABH, ISO 9001, NABL and CAP

accredited5

Future Outlook

6 new comprehensive cancer centers

under development across India

Expansion of Milann fertility centers across

India

Expansion into Africa in partnership with

CDC, UK with acquisition of cancer center

in Kenya

1 In terms of the total number of cancer treatment centers licensed by AERB as of March 31, 2015 (Source: Government of India, Atomic Energy Regulatory Board); 2 Through 50.1% equity interest in BACC Healthcare acquired in 2013 and its wholly owned subsidiary DKR Healthcare; 3 Discontinued operations 4 Post minority Interest 5 NABH accreditation for HCC Bengaluru, HMS Ahmedabad; ISO 9001 certification for pathology laboratory at HMS; NABL and CAP accreditations for Triesta; 6 Includes center in Kenya; 7 Suchiaryu, Hubli hospital managed under Operations and Management contract, not branded as HCG Hospital

4© 2017 , ALL RIGHTS RESERVED. WWW.HCGEL .CO M

Evolution of HCG

¹ In terms of the total number of cancer treatment centers licensed by AERB as of March 31, 2015 (Source: Government of India, Atomic Energy Regulatory Board)

India’s largest provider

of cancer care¹

Milann

ranked #1 nationally

Partnered with

CDC to enter Africa

IPO in March 20161989

2005

2006

2007

2011

2013

Today

1st cancer center in

the HCG network

was set up

Entry into the clinical

laboratory business

through acquisition of

Triesta

Operated 3 cancer

centers; began expansion

of the HCG network

Acquired HCG Medi-Surge

which operated a multi-

speciality hospital in

Ahmedabad

Awarded Oncology Leader

of the Year by Frost &

Sullivan

Entry into fertility business

through the acquisition of 50.1%

in BACC Healthcare Pvt. Ltd.

5© 2017 , ALL RIGHTS RESERVED. WWW.HCGEL .CO M

HCG’s Cancer Care Network

Bengaluru

KochiTiruchi

ChennaiMangalore

Shimoga

Hubli

Gulburga

VishakhapatanamMumbai

Delhi

Kanpur

Ranchi

Jaipur

Ahmedabad

Baroda

Nagpur Cuttak

Kolkata

Bhavnagar

Nashik

Ongole

Vijaywada

Kalinga

Rao Road

Double Road

Koramangala

M S Ramaiah Nagar

Network of Existing and Under

Development Cancer Care centers

Center of Excellence (CoE)1

Comprehensive Cancer center (20)2

Freestanding Diagnostic center (3)2

Day Care Chemotherapy center (1)

Cancer centers Under Development (6)

Regional Penetration

No. of Centers2

Estimated Beds

Karnataka 6 ~522

Gujarat 4 ~304

Maharashtra 4 ~400

North India 3 ~235

HCG Network

1,6591

BEDS

25 LINEAR

ACCELERATORS

14PET-CT

SCANNERS

225+ ONCOLOGISTS

52OPERATION THEATRES

6

1 Includes Multi-specialty beds

2 Existing and planned

1 Includes 2 centers, KR & DR; 2 As on 30th September’ 2017, includes center in Kenya

© 2017 , ALL RIGHTS RESERVED. WWW.HCGEL .CO M

Partnership driven model – select examples

7

Location: Bangalore

Partners

(Business):

M.S. Ramaiah Hospital,

through Gokula Education

Foundation

Educational Institute and

Multi-speciality Hospital

Nature of

Partnership:Revenue Share

Location: Nasik

Partners

(Business):

Dr. Raj Nagarkar

Surgical Oncologist

Nature of

Partnership:Joint Venture

Location: Chennai

Partners

(Business):

Sri Kavery Medical Care Ltd.

Multispeciality Hospital

Nature of

Partnership:Revenue Share

Location: Cuttack

Partners

(Business):

Dr. K.S. Panda, through

Panda Medicals Pvt. Ltd.

Surgical Oncologist

Nature of

Partnership:

Fee for service and rent

paid to our partner

Location: Hubli

Partners

(Business):

NMR Medical Institute Pvt. Ltd.

Freestanding Diagnostics center

Nature of

Partnership:Revenue Share

Location: Ahmedabad

Partners

(Business):

Astha Oncology Private Ltd.

Group of Surgical Oncologists

Nature of

Partnership:Joint Venture

© 2017 , ALL RIGHTS RESERVED. WWW.HCGEL .CO M

Strategy

Planning to establish additional 6 CCCs, which will commence operations in FY2018 / FY2019; 5 new CCCs

already opened as of 30th September’2017

Expanded existing CCCs (Hubli, Cuttack and Ahmedabad) and adding Phase-II in Nashik; Focusing on

Maharashtra and North India regions

Continuously carry out competitive assessment of markets in which we plan to expand

Plan to invest in strengthening the HCG brand, enhancing market presence, brand image and visibility

Intend to strengthen patient support groups comprising cancer survivors to spread awareness and educate

patients

Grow the base of physician partners / collaborators

In the process of establishing 1 new fertility centers in India (as of September 30, 2017)

Planning to set up additional centers; already launched in Delhi, Chandigarh and Mumbai

Invest in building the Milann brand, enhancing market presence and visibility

Intend to strengthen patient support groups and undertake awareness building activities targeting corporates

In the process of significantly upgrading IT infrastructure to enhance quality of care delivered to patients

IT infrastructure is based on a private-cloud computing system and will include a centralised EMR system

seamlessly integrated with RIS/ PACS, biorepository, HIS and ERP

Planning to establish a network of specialty cancer centers in Africa through partnership arrangements and

acquisitions;

Partnered with Commonwealth Development Corporation, UK (CDC) to establish a network of CCCs in Africa

Completed acquisition of Cancer Care Kenya (CCK) in Nairobi

Expand the Reach of

Cancer Care Network in

India

Strengthen HCG Brand

to Reach More Cancer

Patients

Expand Milann Network

of Fertility centers

Across India and Build

Milann Brand

Upgrade and Strengthen

Information Technology

Infrastructure

Expand Cancer Care

Network to Africa

8© 2017 , ALL RIGHTS RESERVED. WWW.HCGEL .CO M

Table of Contents

© 2017 , ALL RIGHTS RESERVED. WWW.HCGEL .CO M

Overview of HCG

Financial Highlights and

Updates

Appendix

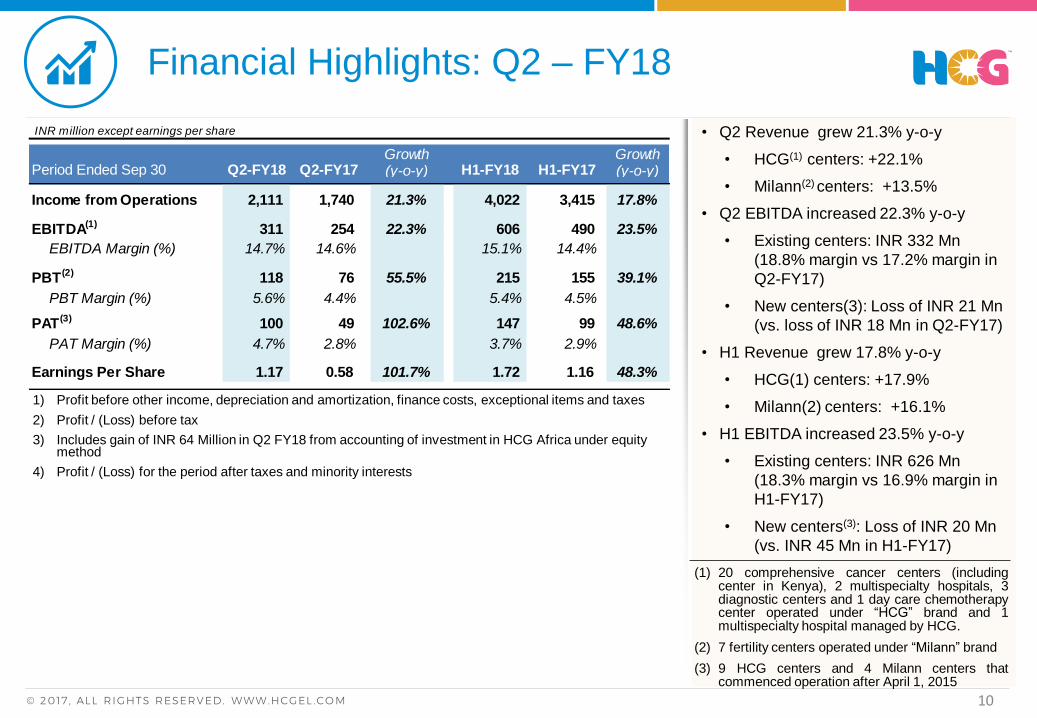

• Q2 Revenue grew 21.3% y-o-y

• HCG(1) centers: +22.1%

• Milann(2) centers: +13.5%

• Q2 EBITDA increased 22.3% y-o-y

• Existing centers: INR 332 Mn

(18.8% margin vs 17.2% margin in

Q2-FY17)

• New centers(3): Loss of INR 21 Mn

(vs. loss of INR 18 Mn in Q2-FY17)

• H1 Revenue grew 17.8% y-o-y

• HCG(1) centers: +17.9%

• Milann(2) centers: +16.1%

• H1 EBITDA increased 23.5% y-o-y

• Existing centers: INR 626 Mn

(18.3% margin vs 16.9% margin in

H1-FY17)

• New centers(3): Loss of INR 20 Mn

(vs. INR 45 Mn in H1-FY17)

Financial Highlights: Q2 – FY18

© 2017 , ALL RIGHTS RESERVED. WWW.HCGEL .CO M

1) Profit before other income, depreciation and amortization, finance costs, exceptional items and taxes

2) Profit / (Loss) before tax

3) Includes gain of INR 64 Million in Q2 FY18 from accounting of investment in HCG Africa under equity method

4) Profit / (Loss) for the period after taxes and minority interests

(1) 20 comprehensive cancer centers (includingcenter in Kenya), 2 multispecialty hospitals, 3diagnostic centers and 1 day care chemotherapycenter operated under “HCG” brand and 1multispecialty hospital managed by HCG.

(2) 7 fertility centers operated under “Milann” brand

(3) 9 HCG centers and 4 Milann centers thatcommenced operation after April 1, 2015

10

INR million except earnings per share

Growth GrowthPeriod Ended Sep 30 Q2-FY18 Q2-FY17 (y-o-y) H1-FY18 H1-FY17 (y-o-y)

Income from Operations 2,111 1,740 21.3% 4,022 3,415 17.8%

EBITDA(1) 311 254 22.3% 606 490 23.5%

EBITDA Margin (%) 14.7% 14.6% 15.1% 14.4%

PBT(2) 118 76 55.5% 215 155 39.1%

PBT Margin (%) 5.6% 4.4% 5.4% 4.5%

PAT(3) 100 49 102.6% 147 99 48.6%

PAT Margin (%) 4.7% 2.8% 3.7% 2.9%

Earnings Per Share 1.17 0.58 101.7% 1.72 1.16 48.3%

Revenue Mix: Q2 – FY18

© 2017 , ALL RIGHTS RESERVED. WWW.HCGEL .CO M

(1) 20 comprehensive cancer centers (including center in Kenya), 2 multispecialtyhospitals, 3 diagnostic centers and 1 day care chemotherapy center operated under“HCG” brand and 1 multispecialty hospital managed by HCG, as at Sept 30 2017

(2) 7 fertility centers operated under “Milann” brand

Karnataka

44%Gujarat

29%

Maharashtra

8%

East India

8%

A.P.

6%

Tamil Nadu

3%

North India

2%

Revenue:

INR 2,111 MnHCG Centers:

INR 1,942 Mn

(1)

(2)Fertility

centers

8%

HCG

centers

92%(91%) 1

(9%) 1

(44%)1(29%) 1

(8%) 1(6%) 1

(3%) 1

(5%) 1

(5%) 1

1(Q2-FY17)

11

• Continuing strong growth at several

existing centers in Q2-FY18

• Hubli: +32% y-o-y

• Cuttack: +21% y-o-y

• KR-DR +20% y-o-y

• Maharashtra scaling up on account of

growth across existing center in Nashik

and new centers in Nagpur and

Mumbai

• Delhi center successfully restructured.

Tiruchi center in process of being

restructured

• New centers contributed Revenues of

INR 314 Mn in Q2-FY18

• Revenue from existing HCG centers,

excluding centers being restructured,

grew 18% in Q2-FY18 on y-o-y basis

HCG Centers: Q2 – FY18 Revenues

© 2017 , ALL RIGHTS RESERVED. WWW.HCGEL .CO M 12

INR million

Growth GrowthPeriod Ended Sep 30 Q2-FY18 Q2-FY17 (y-o-y) H1-FY18 H1-FY17 (y-o-y)

Karnataka 853 701 21.6% 1,587 1,449 9.5%

Gujarat 567 463 22.6% 1,093 868 26.0%

Maharashtra 153 54 183.2% 276 107 158.5%

East India 147 124 18.5% 290 248 17.2%

Andhra Pradesh 115 95 21.9% 238 160 48.9%

Tamil Nadu 68 77 -11.3% 134 146 -8.1%

North India 38 77 -51.2% 69 151 -54.1%

1,942 1,591 22.0% 3,687 3,127 17.9%

• Borivali and Kenya cancer centers and Hubli

multispecialty operationalised in Q2-FY18

• 19.3% increase in occupied bed days on account of

new centers, offset partly by reduction in ALOS

• 5.9% increase in ARPOB, driven by focus on quality

of business across the network, offset by lower

ARPOB at new centers

• Continuing reduction in ALOS to 2.49 on account of

trend towards day care procedures and changing

patient profile

• EBITDA margins maintained inspite of new centers

operationalising and scaling-up. Existing centers

EBITDA margin improved by 160bps to 23.7%

HCG Centers: Q2 - FY18 Operating Metrics

Notes:

(1) No. of Centers includes Cancer and Multispecialty hospitals operated under HCG brand and managed by HCG

(2) Number of beds in operation as at the last day of the period

(3) Occupied Bed Days calculated based on mid-day census

(4) Average Occupancy Rate (“AOR”) calculated as Occupied Bed Days divided by available bed days in the period

(5) Average Revenue per Occupied Bed (“ARPOB”) calculated as Revenue (gross for the hospital) divided by Occupied Bed Days

(6) Average Length of Stay (“ALOS”) calculated as Occupied Bed Days divided by number of admissions (including day care admissions)

(7) EBITDA margin before corporate expenses

No. of Centers Beds Occupied Bed Days

Avg. Occupancy Rate ALOS ARPOB (INR / Day)

Revenue (INR mn) EBITDA Margin

Q2-FY18:

23

Q2-FY17:

19

Q2-FY18:

1,659

Q2-FY17:

1,263

Q2-FY18:

65,690Q2-FY17:

55,072

Q2-FY18:

45.8%Q2-FY17:

47.4%

Q2-FY18:

2.49Q2-FY17:

2.78

Q2-FY18:

30,598Q2-FY17:

28,889

+19.3%

+5.9%

Q2-FY18:

1,942Q2-FY17:

1,591

+22.1%

Q2-FY18:

18.9%Q2-FY17:

19.1%

-20 bps

-160 bps

13© 2017 , ALL RIGHTS RESERVED. WWW.HCGEL .CO M

HCG Centers: Q2 - FY18 Regional Highlights

© 2017 , ALL RIGHTS RESERVED. WWW.HCGEL .CO M

Karnataka

7 632 48.3% 33.8K 853 24.4%

+21.6%5.6%

Centers Beds AOR ARPOB(INR/Day)

Revenue (INR Mn)

EBITDA (%)

Gujarat

4 304 61.5 % 32.9K 567 12.5%

+22.6%

East India

2 165 62.9% 15.4K 147 25.4%

+18.5%+16.9%

New centersExisting centers

+8.4%

+20.5%(1)

+13.1%(1)

+1.4%(1)

Notes:(1) Increase / (Decrease) in Occupied Bed Days(2) Growth numbers are year-on-year basis(3) EBITDA before corporate expenses

COE EBITDA margin at 28% with ARPOB of INR 47k (15% growth y-o-y)

Increasing presence within the region Continuing drive towards improving quality

of business – patient and service mix

Baroda center achieved break-even and Bhavnagar center ramping-up well

EBITDA margin of existing centers at 15.7% for Q2 – FY18

Improved procedure mix and efficiencies in operations leading to optimal occupancy

Strong growth across the region

14

Maharashtra

3 261 42.0% 20.5K 153 9.7% Nagpur center operationalised and

commenced Borivali center Existing Nashik center EBITDA margins at

38% with strong growth+183.2%N.A.N.A.

Milann: Expansion on Track

© 2017 , ALL RIGHTS RESERVED. WWW.HCGEL .CO M

Delhi

Chandigarh

Existing centers(1)

New centers

M S Ramaiah

Bangalore (4 centers)

Indiranagar

JP Nagar

Shivananda

Ahmedabad

(1) Centers in operation prior to April 1, 2015, i.e. Shivananda, JP Nagar, and Indiranagar.

Milann – Ranked #1 nationally for the second consecutive year by the Times of India “All India Fertility & IVF Ranking Survey 2017”

Focus on Southern region with growing presence in North and West

Planned centers

Mumbai

15

H1-FY18 H1-FY17 Growth- - - - - -

New Registrations 2,432 2,231 9.0%

IVF Cycles 1,070 903 18.5%

Revenue (INR Mn) 335 288 16.1%- - -

Capital Expenditure and Net Debt

© 2017 , ALL RIGHTS RESERVED. WWW.HCGEL .CO M

Capital Expenditure Net Debt

1. Net of Bank balance held as margin money of INR 306 mn as at 30-Sep-17 , INR 147 mn as at 30-Jun-17 and INR 145 mn as at 31-Mar-17

2. Includes investment in mutual funds of INR 40 mn as at 30-Sep-17,INR 39 mn as at 30-Jun-17 and INR 113 mn as at 31-Mar-17 andinvestment in fixed deposits of INR 487 mn as at 30-Sep-17, 30-Jun-17

1. Includes amount given as Security Deposit for New Centers of INR 10 mn in Q2-FY18, INR 21 mn in Q1-FY18, and INR 159 mnin FY17

2. Investment of INR 186 mn in HCG Africa is additional

16

INR Million

Q2-FY18 Q1-FY18 FY17

HCG Centres

Existing Centres 72 126 260

Expansions 30 62 381 New Centres 504 520 1,336

606 708 1,976

Milann Centres

Existing Centres 3 5 21

New Centres 20 11 98

23 16 119

Total Capex 629 724 2,095

INR Million

30-Sep-17 30-Jun-17 31-Mar-17

Net Debt

Bank Debt(1)

2,422 1,911 1,320

Vendor Finance 1,993 1,961 1,834

Capital Leases 481 486 491

Other Debt 54 60 73

Less: Cash and Equivalents(2)

(743) (782) (652)

4,207 3,636 3,066

Debt in New Centres

Bank Debt 1,812 1,306 885

Vendor Finance 1,277 1,212 1,123

Other Debt 6 11 13

3,095 2,529 2,021

Net Debt (Excl. New Centres) 1,111 1,107 1,045

Project Update

© 2017 , ALL RIGHTS RESERVED. WWW.HCGEL .CO M

Location Bed

Capacity Project Cost

(INR mn)

Start Date

Kanpur, U.P. 90 839 Q4-FY17

Nagpur, Maharashtra 125 465 Q1-FY18

Borivali, Maharashtra 105 643 Q2-FY18

Nashik, Maharashtra 92 623 Q3-FY18E

Jaipur, Rajasthan 50 410 Q3-FY18E

Kolkata, West Bengal 50 370 Q3-FY18E

South Mumbai, Maharashtra

32 410 Q4-FY18E

1 new HCG center operational during Q2-FY18Additional 4 new HCG centers in FY18

Location Start Date

Delhi Q1-FY17

Chandigarh Q3-FY17

Mumbai Q4-FY17

Ahmedabad Q3-FY18E

3 new Milann centers launched during FY2017 1 new Milann center planned for launch by Q3-FY18

17

Table of Contents

© 2017 , ALL RIGHTS RESERVED. WWW.HCGEL .CO M

Overview of HCG

Financial Highlights and

Updates

Appendix

Appendix A : Investment Thesis

Industry trends

and backdrop

Largest provider of

cancer care in India with

a proven track record

High quality care provided

at a competitive price

Strong management

team with successful

track-record

© 2017 , ALL RIGHTS RESERVED. WWW.HCGEL .CO M

Industry Trends and BackdropCancer Incidences in India to Increase

¹ Call for Action: Expanding cancer care in India dated July 2015, published by Ernst & Young; 2 ASR-W is a weighted mean of the age-specific incidence rates . The weights are taken from the population distribution of the ‘World

Standard Population‘ defined by WHO, and the estimated incidence rate is expressed per 100,000 population for comparisons between different geographies, as age is a key determinant of cancer incidence; 3 Age Group 40-69 years; 4

Breast screening mammograms once in 24 months

Demographic Changes

Cancer incidence increases with age - India’s

population >50+ years to increase from 228m

(2015) to 262mn (2020)

Demographic factors alone are expected to result in

an increase in cancer incidences of 100,000 to

350,000 cases a year

Exposure to Risk Factor

Tobacco use, alcohol consumption, use of

processed food and air pollution

These factors are expected to result in an increase

in cancer incidences of 350,000 to 450,000 cases a

year

Narrowing Diagnosis Gap

Growing awareness and greater public emphasis

on screening and improvements

Expected to result in increased reported cancer

rates

Key Drivers of Cancer Incidence

0.9 1.11.6-2.2

3.4

1.7

Africa India(Reported)

India (Real) China US

Incidence of Cancer Across Countries¹

Estimated

incidence of

cancer in 2015

(mns)

94150-

200174 318123

ASR-W2

(per ’00,000)

Under Diagnosis of Cancer in India¹

62% 71%

31%

81% 70%

30%

72% 91%

19%43%

10% 8%

Breast Cancer Cervical Cancer Head and Neck CancerUSA UK China India

Cancer Diagnosis at Early Stages (Stage I or Stage II)

Cancer prevalence in India estimated to be 3.9mn in 2015

Estimated 1.1mn new cancer cases reported in 2015

Real incidence could be 1.5x to 2.0x times higher than

reported incidence

Difference between reported and real cancer incidence

due to under-diagnosis

Reported incidence of cancer in India based on data from

the cancer registries, which cover < 10% of the population

Late stage disease presentation due to lack of awareness

and participation in screening programs

For example, women³ participation in breast screening

mammograms4: USA (65%), China (30%) and India (<1%)

© 2017 , ALL RIGHTS RESERVED. WWW.HCGEL .CO M 20

Industry Trends and BackdropDemand Supply Gap and Treatment Landscape

Demand for CCCs Demand for LINACs Chemotherapy Cycles (millions)

Outlook for Treatment Landscape¹

200-250

450-550

2014 2020

342750-900

~2,000

2015 2020 2020

1.4-2.0

2.3-3.5

2015 2020(in the absence of

affordability and availability constraints)

¹ Call for Action: Expanding cancer care in India dated July 2015, published by Ernst & Young

77 110 137 200

1,238

Africa India China UK US

0.05 0.10 0.31 0.92 6.20

Per mn Incidence Per mn Population

Existing Demand Supply Gap in Diagnostics…

Lack of adequate infrastructure and absence of mass screening programs are key barriers to timely diagnosis

For example, as of 2014, only 30% of cancer centers in India had advanced imaging technologies like PET-CT

…and Treatment

A key requirement for successful radiation therapy is availability of Linear Accelerators (LINACs)

Region /Country

Number of LINACs(2015)

LINACs per Million

Population

Cancer Prevalence per

LINAC

Cancer Incidence per

LINAC

US 3,818 11.9 1,572 419

UK 323 5.0 3,096 929

China 986 0.7 6,288 3,144

India 342 0.3 7,310 3,216

Availability of LINACs¹

© 2017 , ALL RIGHTS RESERVED. WWW.HCGEL .CO M 21

Largest Provider of Cancer Care in India with a

Proven Track Record¹

HCG’s market leading position, successful track record and strong reputation in

India provides a significant advantage over its competitors

1 As per AERB as of March 31, 2015. (Source: Government of India, Atomic Energy Regulatory Board)

2 Expected to commence operation during FY2018 and FY2019

153

12 15

3

7

2006 Additions 31-Mar-16 2017/18/19

…With a Strong Track Record

Growth in No. of Comprehensive Cancer Care

Centers… Under

Development²

Largest Cancer Care Provider…

Largest provider of cancer care in India in terms of number of cancer

treatment centers listed by AERB as of 31-Mar-20151

HCG network spans 15 cities and towns across eight states in India

Through the extensive network, HCG is able to provide cancer care

beyond just the metropolitan cities

As of 30-Jun-2017, HCG had 599 specialist physicians including 190

oncologists, 37 radiologists and 29 pathologists and 343 other

specialist physicians

HCG believes, it has a strong reputation within the medical

community, driven by

Use of advanced technologies

Successful clinical outcomes

Extensive clinical experience of specialist physicians

© 2017 , ALL RIGHTS RESERVED. WWW.HCGEL .CO M 22

High Quality Care Provided at a Competitive Price

Ability to provide high quality care driven by a multidisciplinary and technology focused approach

…At a Competitive Price

India US¹

Cost of Cancer Treatment in India is lower (INR `000)

India US¹ India US¹

Chemotherapy Surgery Radiation Therapy

Source: Call for Action: Expanding cancer care in India dated July 2015, published by Ernst & Young

1 PPP adjusted 510-720; 2 PPP adjusted 600-720; 3 PPP adjusted 420-540; 4 Vijay Govindarajan and Ravi Ramamurti, Harvard Business Review, "Delivering world-class health Care, Affordably”, November 2013

150-24060-100 60-100

1,100 –

1,4001,500 –

1,800

1,300 –

1,800

Drivers of HCG’s Cost Competitiveness

Economies of scale arising out of expansive network

Optimal utilization of equipment

Centralized drug and consumables formulary

Large network gives competitive advantage in terms of

favourable economic terms of purchase and financing of

medical equipment

Approach to Providing High Quality Care…

Multidisciplinary approach to cancer care - specialist physicians from

various disciplines collaborate to provide the best course of treatment

Focus on identifying and adopting appropriate technology

Among first cancer care providers in India to standardise

molecular diagnostics technologies

First healthcare provider in India to perform computer assisted

tumor navigation surgery

Standardized clinical protocols for diagnosis and treatment

…Results in Successful Clinical

Outcomes…

Ability to manage the large volume of patients

across the network while maintaining quality

of clinical outcomes

For example, the five year survival rate for

breast cancer patients at HCG’s network is

comparable to U.S. benchmarks4

© 2017 , ALL RIGHTS RESERVED. WWW.HCGEL .CO M 23

Govindarajan et. al. .Harvard Business Review, November 2012,

“Delivering World Class Health Care Affordably, Innovative

hospitals in India are pointing the way”G

Survival Rate Cost

Coverage by Harvard

Comparable outcomes at fraction of costUnique and Successful Business Model

© 2017 , ALL RIGHTS RESERVED. WWW.HCGEL .CO M 24

© 2017 HealthCare Global Enterprises Limited., All Rights Reserved.

HCG Logo is trademarks of HealthCare Global Enterprises Limited

In addition to Company data, data from market research agencies, Stock Exchanges and industry publications has been used for this presentation.

This material was used during an oral presentation; it is not a complete record of the discussion. This work may not be used, sold, transferred,

adapted, abridged, copied or reproduced in whole on or in part in any manner or form or in any media without the prior written consent. All product

names and company names and logos mentioned herein are the trademarks or registered trademarks of their respective owners.

For updates and specific queries, please visit www.hcgel.com

or feel free to contact [email protected]

© 2017 , ALL RIGHTS RESERVED. WWW.HCGEL .CO M