HEADOFFICE:D.M.COLONY,BANDA …allahabadgraminbank.in/tender/CREDIT GRADING.pdf · The risk grading...

63

ALLAHABADUPGRAMINBANK HEADOFFICE:D.M.COLONY,BANDA RecoveryDepart ment Instruction Circular No - 679 Date: 01.07.2013 AllBranches/Offices/InspectingOfficers/RBTC/ProjectOffice INTRODUCTION OF CREDIT GRADING SYSTEM HIGH LIGHTS AND ACTION POINTS 1. In the Bank transition to the Basel II compliant the Bank has developed CRG module to improve the efficacy of credit portfolio of the Bank. 2. All the accounts are to be risk graded. 3. All standard accounts will be graded between 1 to7 depending upon scores obtained whereas substandard Doubtful and Loss Accounts will be catergorised as 8,9,10 respectively. 4. Branches will use the Risk Rating System strictly as per the guidelines provided in this regard. 5. All the lending rates except those specifically exempted by RBI are to be linked with the risk grade of the account. 6. The risk grading does not supersede the Discretionary authority level of the field functionary. The field functionary should exercise the authority as vested in the lending policy of the bank. 7. The credit rating would be applied to all the new sanctions and existing accounts on their review/renewal. 8. The risk grading of Borrowal Accounts and comments must be incorporated in appraisal note and a copy of the same should be enclosed with MDA statement.

Transcript of HEADOFFICE:D.M.COLONY,BANDA …allahabadgraminbank.in/tender/CREDIT GRADING.pdf · The risk grading...

ALLAHABADUPGRAMINBANKHEADOFFICE:D.M.COLONY,BANDA

RecoveryDepartment

Instruction Circular No - 679 Date: 01.07.2013

AllBranches/Offices/InspectingOfficers/RBTC/ProjectOffice

INTRODUCTION OF CREDIT GRADING SYSTEM

HIGH LIGHTS AND ACTION POINTS

1. In the Bank transition to the Basel II compliant the Bank has developed CRG module to improve the

efficacy of credit portfolio of the Bank.

2. All the accounts are to be risk graded.

3. All standard accounts will be graded between 1 to7 depending upon scores obtained whereas

substandard Doubtful and Loss Accounts will be catergorised as 8,9,10 respectively.

4. Branches will use the Risk Rating System strictly as per the guidelines provided in this regard.

5. All the lending rates except those specifically exempted by RBI are to be linked with the risk grade of

the account.

6. The risk grading does not supersede the Discretionary authority level of the field functionary. The

field functionary should exercise the authority as vested in the lending policy of the bank.

7. The credit rating would be applied to all the new sanctions and existing accounts on their

review/renewal.

8. The risk grading of Borrowal Accounts and comments must be incorporated in appraisal note and a

copy of the same should be enclosed with MDA statement.

IntroductionOfCreditRiskGradingModule

Preamble

Credit Risk is arguably the most critical risk, a bank faces. Major cause of

serious banking problems continues to be directly related to lax credit

administration/standards for borrowers. Reserve Bank of India and BASEL committee on

Banking Supervision laid guidelines with a very detailed emphasis on effective risk

management system to identify measure, monitor and control credit risk as part

of an approach to risk management.

Need for Credit Risk Management Policy

Every banking activity is fraught with Risk. Prudent Banking entails identifying each Risk

& managing the same for the benefit of the organisation & society in general.

Basel Committee on Banking Supervision, and RBI’s guidance note on credit risk

management of October 2002 among other things state that “EVERY BANK SHOULD

HAVE A CREDIT RISK POLICY DOCUMENT APPROVED BY THE BOARD.” Credit Risk Policy

should include risk identification, risk measurement, risk grading techniques, risk

control /mitigation techniques.

Credit Risk Management Policy is akin to the Bank’s lending policy, which is the basis on

which the entire loaning Process and administration rests. In the Bank transition to the

Basel II compliance, an elaborate Credit Risk Management Policy could only form the

foundation of Bank’s assets growth.

This policy has been designed, in super-cession to all the previous guidelines issued on

the above subject, so as to have a uniform policy across the board for the entire credit

portfolio of the Bank.

Objectives

The policy is designed to:

1. Enhance the risk management capabilities to ensure orderly and healthy credit

growth.

2. Maintain asset quality.

3. Maintain credit exposure within acceptable parameter/prudential exposure.

4. Establishing an appropriate Credit Risk Management environment.

5. Maintaining an appropriate Credit administration, risk management and monitoring

process.

6. Optimising resource use, earning protection by maximising return and minimising

losses.

7. Managing risks to boost long term profit and competitive position.

8. Maintaining an appropriate credit administration, risk measurement and monitoring

process.

Credit Risk –

Definition

Credit Risk is defined as the possibility that a borrower or counterparty will fail to meet

its obligations in accordance with the agreed terms.

Credit Risk For Counter Party Arises From An Aggregation Of The Following:

EXTERNAL RISK:

Activity Risk or Industry Risk (Assessment is usually based on: Demand – Supply

position, Govt. Policy for the sector, Extent of competition etc.

INTERNAL RISK

Mainly divided into three parts:

a. Business Risk: Assessment is usually based on : brand equity, consistency

in quality ,product range, distribution set up , diversity of market, availability of

raw material, capacity utilisation, energy cost, cost effective technology etc)

b. Financial Risk: assessment is usually based on: Financial Ratios in balance

sheet/ profit and loss statement.

c. Management Risk: assessment is usually based on: experience of

promoters/management, business and financial policy, track record etc.

Credit Risk Management:

As per RBI guidelines on Credit Risk management, the credit risk management involve

following:

1- Measurement of risk through Credit Rating/Scoring

2- Quantification of Risk–Expected & Unexpected Loan losses

3- Risk Pricing on scientific basis

4- Controlling / monitoring the risk

Action Points

The Bank has developed Ten CRG modules (CRG1 To CRG10) to cover all the Borrowal

accounts .These module will be applicable as under:

CRG

MODULES

Applications

CRG-01 RISK GRADING OF:

1. Advance against full liquid security.

2. Advance to Staff (irrespective of credit limit).

3. Clean Advances & Non Performing Assets, irrespective of Credit Limit.

4. Advance under Retail Credit scheme up to `10 lacs

5. Agriculture advances up to `10 lac

CRG-02 Risk Grading of Borrowal accounts (with existing units/ Project)

having Aggregate Credit Limit of `10.00 Lac to `200.00Lac.

CRG-03 Risk Grading of Borrowal accounts (with existing units/project)

having aggregate Credit Limit above `200.00 Lac.

CRG-04 Risk Grading of Borrowal accounts (with New units/ project) having

Aggregate Credit Limit of `10.00 Lac and above but excluding SSI&SME)

CRG-05 Risk Grading of Borrowal Accounts with `1 0 Lakh & above aggregate

credit limit falling under following categories:

1 Service Sectors (Railway, Airways, State Road Transport

Corp,Transport Business, Nursing Home, Amusement Park, Hospital etc)

2 Municipality or Corporation/Development Authority

3 Educational Institute

CRG-06 Risk Grading of Borrowal Accounts with `1 0 Lakh & above aggregate

credit limit falling under following categories:

1 NBFC / Financial Institution

2 Intermediaries engaged in lending activities (like lending for

Project, Infrastructural Development, and Housing.)

3 Financial Corporation like IRFC

CRG-07 For Risk Grading of Borrowal accounts under SSI/SME category (existing

Accounts) with credit limit of 10lac and above

CRG-08 For Risk Grading of borrowers under SSI/SME category (new connection)

with credit limit `10 lac and above.

CRG-09 For risk grading for borrowal a/c under MSME segment up to `10 lakhs

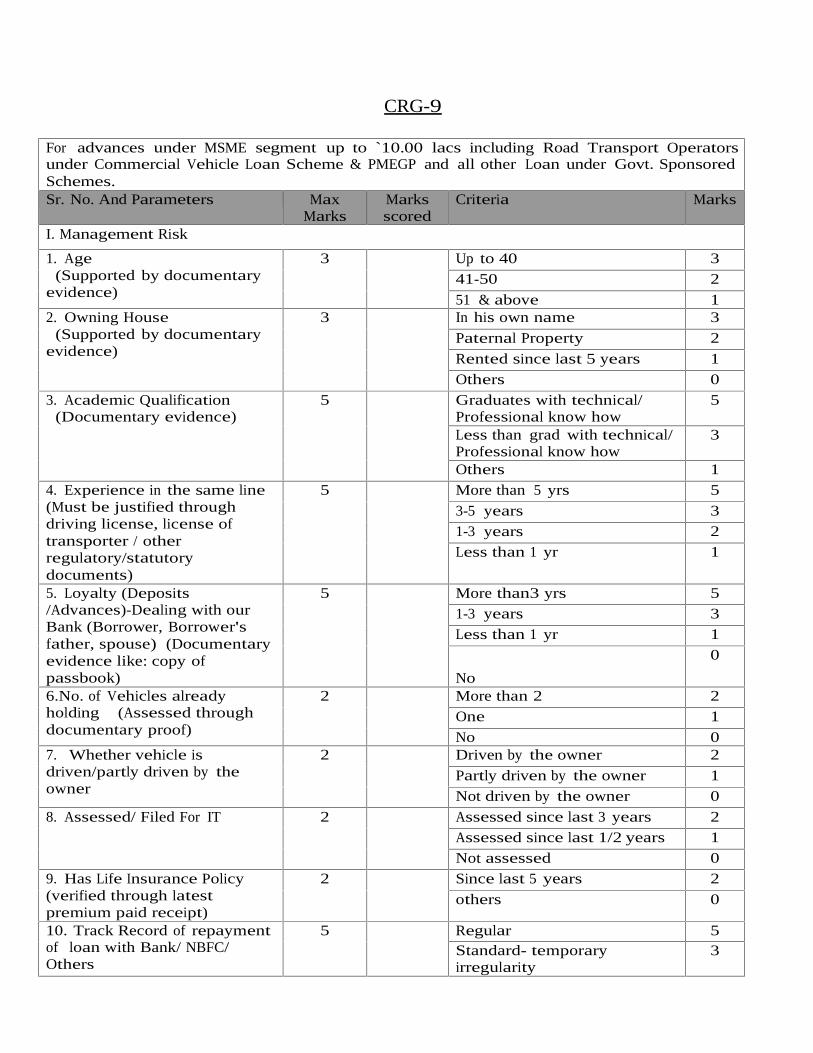

including commercial vehicles, PMEGP and other Govt. sponsored

schemes

CRG-10 For risk grading for borrowal a/c under MSME segment above `10 lakhs

including commercial vehicles, PMEGP and other Govt. sponsored

schemes

CRG1 Module is used for risk grading of Borrowal accounts with credit limit below `10

lacs as also some other category of advances as detailed above. There will not be

scoring system for various Risk Factors under this module and grade will be allocated

as per thumb rule for various categories of advances. However, risk grading of

Borrowal accounts covered under CRG -2 to CRG - 10 Modules will involve scoring

system for various risk factors/categories.

Scoring Norms for overall Risk Gradation

All Standard Assets will be graded between 1 to7 depending upon scores obtained

whereas Substandard, Doubtful and Loss Accounts will be categorised as 8, 9

10 respectively.

The Aggregate Score for all Risk Categories vis-a-vis Grades to be assigned as under:

Grade Risk Nature Scores under1 Very Low Above 902 Low Above 80 & Up to 903 Moderately Low Above 70 & Up to 804 Fair Above 60 & Up to 705 Moderate Above 50 & Up to 606 High Above 40 & Up to 507 Very High Above 35 & Up to 408,9,10 Default 35 or Below

HurdleRate:

Definition:

The Hurdle Rate is defines as the required rate of return in a discounted cash

flow analysis above which an investment makes sense and below which it does not.

This is based on expected rate of inflation, anticipated change in the rate of inflation,

Risk of defaulting a loan and risk profile of a particular venture.

Pricing:

Risk return pricing for loan product is a fundamental tenet of Risk Management. General

dictum shall be ‘Higher The Risk Higher The Price, Lower The Risk Lower The Price’. All

the lending rates except those specifically exempted by RBI are to be determined with

reference to PLR as per Bank’s interest policy. With the introduction of Risk

Grading Policy, a risk premium will be added to interest rate to be paid by the

borrower. This

Rate will be decided in the Lending Rate policy of the Bank. The Bank shall

adopt competitive approach in pricing with regard to nature of risk and market

forces like competition, our exposure to the particular segment of the market etc.

Validation/ApprovalofRiskGrading-GeneralConcept:

• Risk Grading for each Borrowal account covered under CRG 2 to CRG 10 Modules is

to be finalised at two/three levels of officers as detailed under:-

SanctioningAuthority No.oflevels

I.Branch Heads Two

II.Regional Heads Two

III.Head office Three

• Level 1 Officer refers to the officer appraising the credit proposal. Level 2 Officer

refers to the official to whom the appraising officer (level 1) is required to report or

other senior officer to whom such task has been assigned. Level 3 Officer refers to the

officials of Risk Management Deptt (Presently managed by Advanced Dept.

Head Office) (for proposals under H.O Authority) who will give final approval of rating.

• Level 1 Officer will do the entire risk grading exercise and put his signature

with his comments in the space provided for the purpose in various modules.

• Level 2 & Level 3 Officials have to confirm/validate the Risk Rating finalised by the

Level 1. They may modify the ratings if they do not agree with the grading/scoring

provided by their Lower level official. Separate Space has been provided in the

Module for putting their comments along with signature.

GeneralGuidelines:

• The credit risk grading would be done at least once in each year for all existing

& fresh standard Borrowal accounts. The Risk Grading of Borrowal Accounts

& Comments on the same must be incorporate in appraisal note whenever a

credit facility is sanctioned/reviewed/renewed. A Validated/ Approved Risk Grading

Sheet must be held with each loan document and should also be sent with

MDA/RMDA Statements. When a loan is sanctioned by RO/HO, a copy of the approved

risk grading sheet should also be enclosed with the sanction letter sent to the

Branch for their record.

• The rating modules provided will be used at all levels for the risk rating. Rating

Framework for CRG1 to CRG 10 Module is given in part-2.

• Risk Grading of Accounts enjoying Credit Facility from more than one Branch of

our Bank: In such cases, risk grading finalised by the branch having main limit of the

account will also be used by the branch/es having sub-limit of that account and they

should obtain the same for the purpose of reporting in the Statements on CRG. In Such

Accounts, Name of the Branch Having Main Limit should also be mentioned in

the Statement on CRG by the Branches having Sub-Limit.

• Credit Appraisal: Risk Grading System is a tool to identify & measure the

risk associated with a credit/facility without diluting the Standard Credit

Appraisal System of the Bank. Credit decisions should strictly be taken in the light

of merit of the proposal and Bank’s lending policy.

• In case of new sanction/renewal/enhancement the proposal with risk grading of 1 to

3 may be considered by the branch head provided the proposal is within their

discretionary authority. The proposal with risk grading 4 may be considered by

Regional Head falling within their delegated authority. The Proposal with risk grading

5&6 may be considered for sanction by Head Office. The Proposal for loan under Risk

Grading 7 will be submitted to the Board for consideration.

• An account which has slipped from the existing risk grading shall be

considered after permission from one step higher than the sanctioning authority.

• The Risk Grading does not supersede the Discretionary Authority level set under the

Lending Policy of the Bank. The field functionaries would exercise the authority vested

in the by virtue of the said lending policy.

• For Existing Units/Projects, as far as possible, rating will be made on the basis of the

audited balance sheets of the last financial year. Wherever, such audited

financial statements are not available, the proponents would submit an undertaking

that there would not be a difference of more than 5% between the audited & the

unaudited balance sheets. In case of higher difference a penalty of 2% of the loan

amount would be charged and the Bank would also be at liberty to recall the entire

loan.

• The proposals for which CGTSME Cover may be available would be treated as

collaterally secured to the extent the cover is available and suitable points will be

allocated while rating the proposal.

• Thecreditratingwouldbeappliedtoallthenewsanctions.Theratingwouldalsobe

applied to existing accounts on review/renewal. A time frame of 2 years has been

envisagedforimplementation.

Organisationalstructure:

Sound Organisational structure is Sine-Qua-Non for successful implementation of an

effective Credit Risk Management System. Organisational structure in our Bank

for Credit Risk Management will cover the following:

1. The Board of Directors shall have overall responsibility for Management of Credit

Risk. The Board of Director will consider the Credit Risk Management Policy and various

prudential norms. Such norms will be decided in the lending policy of the Bank.

2. A Credit Risk Management committee headed by General Manager shall oversee

Credit Risk Management in entire lending functions.

3. There will be a separate Credit Risk Management cell under Advance deptt, which

will be responsible for day to day functioning, which cover implementation of credit risk

policy, support & promotion of risk awareness/training in relation to credit risk.

All concern should take a careful note for meticulous compliance.

Hindi version of this circular will follow shortly.

(RAKESH KUMAR)

GENERAL MANAGER

ALLAHABAD UP GRAMIN BANKCREDIT RISK GRADING MODULES

(CRG 01 to CRG 10)

1. All Advances allowed asclean advances up to90 days (includingDebit Balance arising

5 Moderate Clean Outstanding,recovery risk is high.However, branches arepermitted to allow

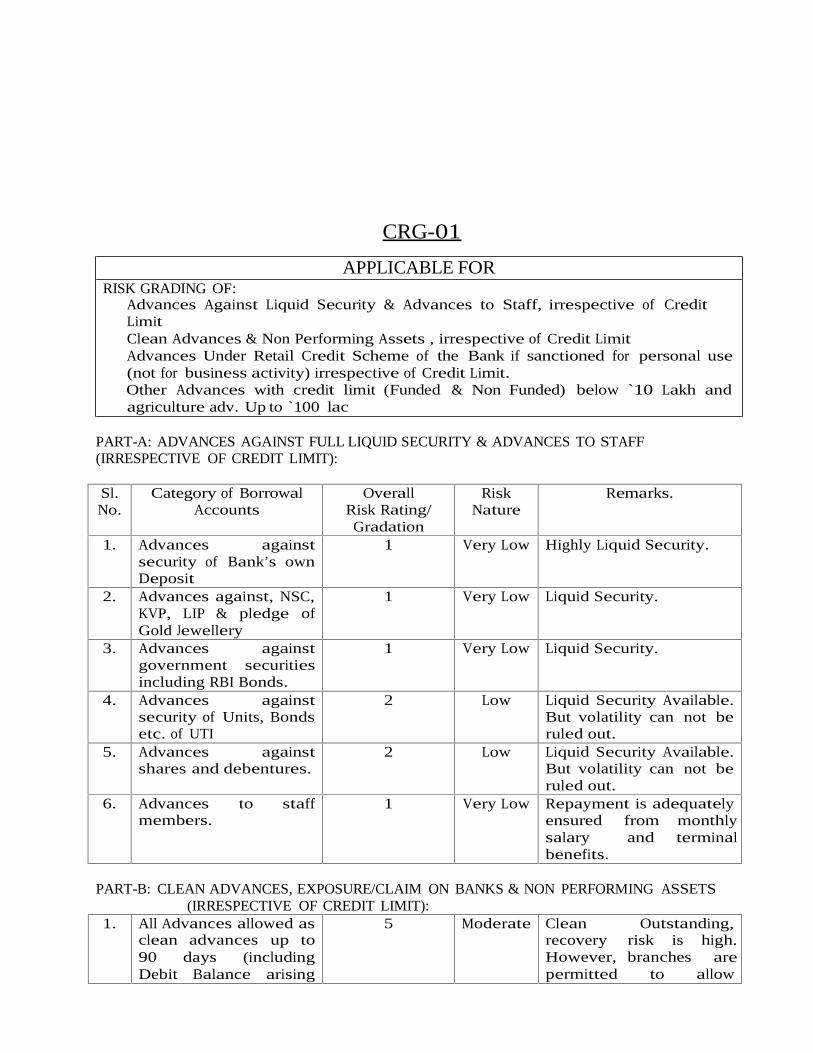

RISK GRADING OF:

CRG-01

APPLICABLE FOR

Advances Against Liquid Security & Advances to Staff, irrespective of CreditLimitClean Advances & Non Performing Assets , irrespective of Credit LimitAdvances Under Retail Credit Scheme of the Bank if sanctioned for personal use(not for business activity) irrespective of Credit Limit.Other Advances with credit limit (Funded & Non Funded) below `10 Lakh andagriculture adv. Up to `100 lac

PART-A: ADVANCES AGAINST FULL LIQUID SECURITY & ADVANCES TO STAFF(IRRESPECTIVE OF CREDIT LIMIT):

Sl.No.

Category of BorrowalAccounts

OverallRisk Rating/Gradation

RiskNature

Remarks.

1. Advances againstsecurity of Bank’s ownDeposit

1 Very Low Highly Liquid Security.

2. Advances against, NSC,KVP, LIP & pledge ofGold Jewellery

1 Very Low Liquid Security.

3. Advances againstgovernment securitiesincluding RBI Bonds.

1 Very Low Liquid Security.

4. Advances againstsecurity of Units, Bondsetc. of UTI

2 Low Liquid Security Available.But volatility can not beruled out.

5. Advances againstshares and debentures.

2 Low Liquid Security Available.But volatility can not beruled out.

6. Advances to staffmembers.

1 Very Low Repayment is adequatelyensured from monthlysalary and terminalbenefits.

PART-B: CLEAN ADVANCES, EXPOSURE/CLAIM ON BANKS & NON PERFORMING ASSETS(IRRESPECTIVE OF CREDIT LIMIT):

from Bank’s CreditCard, Bills Remittedunder Bank’s CustomerService Guidelines, andDrawls’ against uncleareffect of Cheques etc)and classified asStandard Assets.

advance subject to theirdiscretionary authority.

2. Of above CleanAdvances,Advances notliquidated within duedate.

6 HighRisk.

Recovery prospects isminimum, Likely to beNPA.

3. Claims/Exposure onScheduled Bank

2 Low Reasonable degree ofcomfort.

4. All advances Classifiedas Non PerformingAssets

8(8/9/10 for SST/DT/ Loss).

Default Yielding Interest from theAssets Ceased. It maycause loss to the Bank.

PART-C: ADVANCES UNDER RETAIL CREDIT SCHEME IRRESPECTIVE OF THE CREDIT LIMITSl.No.

Category of BorrowalAccounts

Overall RiskRating/ Gradation

RiskNature

Remarks

1. a) Secured Advances toPublic Where Salary TieUp is available (i.e.Housing Loan, ConsumerLoan, Car/ mo-bike Loanetc)b) Personal loans onsalary tie-up where 50%or more Security isavailable

2 Low Repayment Risk is lowdue to tie-uparrangement for loanrepayment andreasonable degree ofrisk mitigation byavailable security.

2. Personal loans on salarytie-up where availablesecurity is below 50%

3 ModeratelyLow

Though RepaymentRisk is less due to LoanRepayment tie-upbut no full riskmitigation by availablesecurity.3. Existing Regular

accounts under oldpersonal loan scheme ofthe Bank with salary tie-up or any otherunsecured loan schemeon salary tie-up which isnot specified else- where.

4 Fair Risk of recovery is fairin view of no riskmitigation by securityin case tie-uparrangement for loanrepayment isdiscontinued.

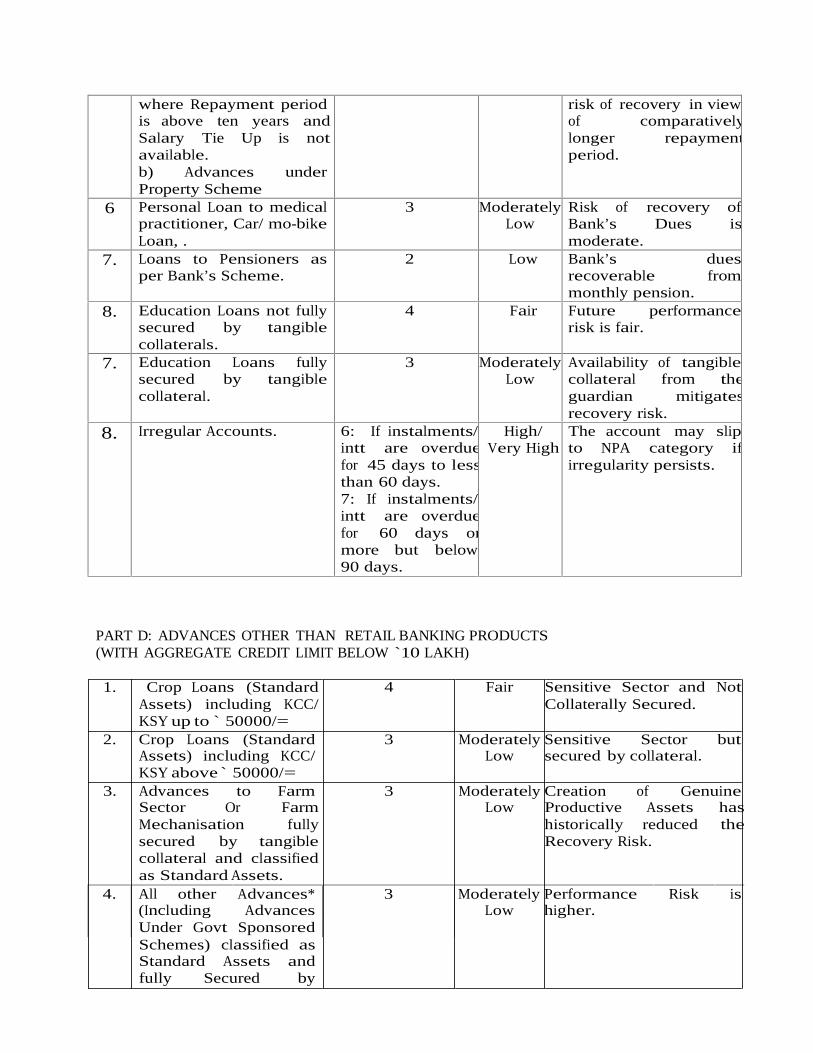

4. Public Housing Loanwhere Repayment Periodis up to ten years andSalary Tie Up is notavailable.

3 ModeratelyLow

Secured loan withcomparatively low riskof recovery in view ofshorter repaymentperiod.

5. a) Public Housing Loan 4 Fair Secured loan with fair

where Repayment periodis above ten years andSalary Tie Up is notavailable.b) Advances underProperty Scheme

risk of recovery in viewof comparativelylonger repaymentperiod.

6 Personal Loan to medicalpractitioner, Car/ mo-bikeLoan, .

3 ModeratelyLow

Risk of recovery ofBank’s Dues ismoderate.

7. Loans to Pensioners asper Bank’s Scheme.

2 Low Bank’s duesrecoverable frommonthly pension.

8. Education Loans not fullysecured by tangiblecollaterals.

4 Fair Future performancerisk is fair.

7. Education Loans fullysecured by tangiblecollateral.

3 ModeratelyLow

Availability of tangiblecollateral from theguardian mitigatesrecovery risk.

8. Irregular Accounts. 6: If instalments/intt are overduefor 45 days to lessthan 60 days.7: If instalments/intt are overduefor 60 days ormore but below90 days.

High/Very High

The account may slipto NPA category ifirregularity persists.

PART D: ADVANCES OTHER THAN RETAIL BANKING PRODUCTS(WITH AGGREGATE CREDIT LIMIT BELOW `10 LAKH)

1. Crop Loans (StandardAssets) including KCC/KSY up to ` 50000/=

4 Fair Sensitive Sector and NotCollaterally Secured.

2. Crop Loans (Standard 3 Moderately Sensitive Sector butAssets) including KCC/KSY above ` 50000/=

Low secured by collateral.

3. Advances to Farm 3 Moderately Creation of GenuineSector Or FarmMechanisation fullysecured by tangiblecollateral and classifiedas Standard Assets.

Low Productive Assets hashistorically reduced theRecovery Risk.

4. All other Advances* 3 Moderately Performance Risk is(Including Advances Low higher.Under Govt SponsoredSchemes) classified asStandard Assets andfully Secured by

Tangible Collaterals.5. All other Advances*

(Including AdvancesUnder Govt SponsoredSchemes) classified asStandard Assets andpartly Secured/ NotSecured by TangibleCollaterals.

4 Fairtt

Recovery Risk is high dueo non-availability ofangible collaterals.

6. Irregular Accounts 6: If instalments/intt areoverdue for 45days or morebut below60 days.7: If instalments/intt areoverdue for 60days or morebut below90 days.

High/Very High

The account may slip toNPA category ifirregularity persists.

CRG-02APPLICABLE FOR

Risk Grading Of Borrowers (With Existing Units/Projects) Having Aggregate Limitof ` 10.00 Lakh to ` 200 Lakh

NameoftheBorrower:…………………………………….LineofActivity:……………………….Branch: ……………………………………… Region:- …………………………..ScoringBasedonAuditedBalanceSheetAsAt: ………………….ExistingFacility:

Nature of Facility(TL/ WC/Others)

Credit Limit Outstanding Overdue/Other irregularities, if any

TotalScoringUnderVariousRiskCategories:

A. FINANCIAL RISK: (Aggregate Score 36)Parameter Score

A.1) CURRENT RATIO• 1.33 or More 6• 1.25 or More but below 1.33 5• 1.17 or More but below 1.25 4• 1.13 or More but below 1.17 2• Below 1.13 0Comment:A.2) TOL /TNW RATIO

• 2.00 and below 6• Above 2.00 & up to 3.00 5• Above 3.00 & up to 4.50 4• Above 4.50 &up to 5.00 (Up to7.50 for Infrastructure/construction/PSU

Sector)2

• Above 5.00 ( above 7.50 for Infrastructure/construction/PSU Sector) 0Comment:A.3 a) INTEREST COVERAGE RATIO (PBDIT/Interest) :• 3 or More 6• 2.50 or More but below 3 5• 1.75 or More but below 2.50 4• 1.50 or More but below 1.75 2• Below 1.50 00Comment:

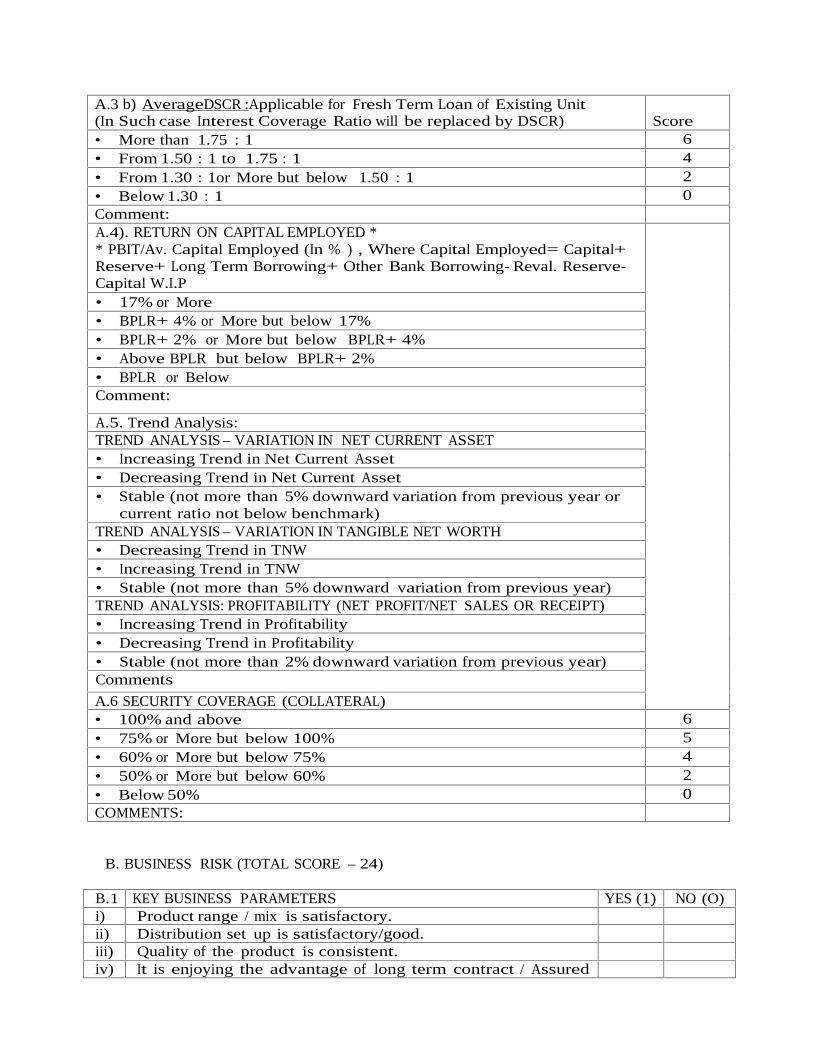

A.3 b) AverageDSCR :Applicable for Fresh Term Loan of Existing Unit(In Such case Interest Coverage Ratio will be replaced by DSCR)• More than 1.75 : 1 6• From 1.50 : 1 to 1.75 : 1 4• From 1.30 : 1or More but below 1.50 : 1 2• Below 1.30 : 1 0Comment:A.4). RETURN ON CAPITAL EMPLOYED *=* PBIT/Av. Capital employed (In % Term), Where Capital Employed=Capital+ Reserve+ Long term borrowing+ other Bank borrowing- Reval.Reserve-Capital W.I.PA.5 SECURITY COVERAGE (COLLATERAL) SCORE• 100% and above 6• 75% or More but below 100% 5• 60% or More but below 75% 4• 50% or More but below 60% 2• Below 50% 0COMMENTS:

• 18% or More 6• BPLR+ 4% or More but below 18% 5• BPLR+ 2% or More but below BPLR+ 4% 3• Above BPLR but below BPLR+ 2% 2• BPLR or Below 0Comment:A.6. Trend Analysis:TREND ANALYSIS – VARIATION IN NET CURRENT ASSET• Increasing Trend in Net Current Asset (+) 2• Decreasing Trend in Net Current Asset (-) 2• Stable ( not more than 5% downward variation from previous year or

current ratio not below bench mark)0

TREND ANALYSIS – VARIATION IN TANGIBLE NET WORTH• Decreasing Trend in TNW (-) 2• Increasing Trend in TNW (+) 2• Stable (not more than 5% downward variation from previous year) 0TREND ANALYSIS: PROFITABILITY (NET PROFIT/NET SALES OR RECEIPT)• Increasing Trend in Profitability (+) 2• Decreasing Trend in Profitability (-) 2• Stable (not more than 2% downward variation from previous year) 0Comments:

PARAMETERS SCORE• More than 12 % 6• More than 10% but up to 12% 5• More than 8% but up to 10% 4• More than 6% but up to 8% 2• 6% or below 0COMMENTS:

C.1.Key Management Features: Score- Yes:1

Score- No:0

i) Management is established player for more than 5Years./PSUs

B. BUSINESS RISK: (Aggregate Score: 26) : 22/24B.1 Key Business Features: Score- Yes:

2Score-No: 0

1. Product Range/Mix is satisfactory2. After sale service is satisfactory3. The borrowers are financially able to withstand

competition.4. Borrowers not dealing in perishable goods.5. Future growth potential is high.6. Capacity utilisation is 80% or more. (For mfg)7. Business is not cyclical or there is no cyclical earnings.8. Borrowers not dependent on limited customers.9. The business is not sensitive to changes in Govt Policies

like price control, pollution, custom/excise duty etc.10.There are only few competitors in local market.

Total: Eligible Scores under B.1 … Scores Obtained: …

B.2. INCOME VALUE OF THE BANK:(Interest, Commission, Exchange etc. from the Account as Percentage of Total FundBased Limit- Projected figure if new connection but previous year actual ifexisting account)

C. MANAGEMENT RISK: (Aggregate Score: 36) : 23/30

ii) Having good reputation and track record (no litigationwith customers/suppliers , no penal action from anytax/ govt /statutory authority, fair dealingwith customers, timely wage payment to theirworkmen/employees etc)

iii) Having satisfactory relation with Bank for more than 2years.

iv) Business is not managed by one or two persons.v) The associate concern/group/ family is financially

sound & their support is available to the borrower,when in need.

vi) The management is proactive rather than reactive andtheir business policy is sound.

TOTAL :C.2. Payment Records & Operations in the Account: SCOREC.2.A Payment of interest/instalment, payment of amount involved indevolved LC or Invoked B.G., Payment of Bills :

NA

Due amt paid within 15 working days and less 6Due amt paid between 16 working days to 30 working days. 5Due amt paid between 31 working days to 45 working days. 3Due amt paid between 46 working days to 60 working days. 2Due amt paid after 60 working days or since un paid . (-) 3

Operations in the account (for working capital limit):In case of consortium/multiple financing, sales would mean proportionatesales based on our share in total limit

High turnover (above 90% of sales) in the account & negligible returnof cheques.

6

Good turnover (80-90% of sales)in the account & nominal return ofcheques.

4

Average turnover (70-80% of sales) & average level of return ofcheques.

2

Unsatisfactory turnover (below 70% of sales or 2 times of workingcapital limit, whichever is low ) &/or frequent return of cheques.

0

C.3. COMPLIANCE OF TERMS & CONDITIONS: SCORE• All Terms and Conditions complied with. 6• Compliance of terms & Conditions other than creation of Collateral

Security due to reasons duly accepted by the Sanctioning Authority.4

• Non- Compliance of Major Terms & Conditions. 0C.4. Credibility:C.4.A. PAST COMMITMENT WITH RESPECT TO NET SALES:• Achievement is 95% or above of Projection 6• Achievement is 90% or More but below 95% of Projection 5• Achievement is 75% or More but below 90% of Projection 3• Achievement is 60% or More but below 75% of Projection 2• Achievement is below 60% of Projection &/or below last year actual. 0C.4.A.1 FOR FRESH CONNECTIONS WHERE PROJECTIONS NOT AVAILABLE(In place of C.4.A)

NA

• Sales Growth during the year Exceeds 20% of last two year averageSales

6

• Sales Growth during the year is 15% -20%of last two year average 5

PARTICULARS Yes (1) No (0)1. Present industry/activity scenario dealt by is favourable.2. Technology/Activity is proven for medium term.3. Demand of the product is increasing.4. Availability of Raw Material/Products (Traders) isadequate.5. Industry/Activity does not depend on the vagaries ofnature.6. The products are having established markets.INDUSTRY/ACTIVITY RISK (D.1.) CONTD---7. Quality of the Product is satisfactory.8. Requisite infrastructural facility (power, fuel, road or rail,water supply, telephone etc) are available.9. Threat of substitute/competitors to the product/s is notthere.10. Firm is not assembler or trader of unbranded items.TOTAL SCORE FOR INDUSTRY/ ACTIVITY RISK:

Sales• Sales Growth during the year is 10% -15% of last two year average

Sales4

• Sales Growth during the year is 5%- 10% of last two year averageSales

2

• Sales Growth during the year is below 5% of last two year averageSales

0

C.4.B. PAST COMMITMENT WITH RESPECT TO NET PROFIT:

• Achievement is 95% or above of Projection 6• Achievement is 90% or More but below 95% of Projection 5• Achievement is 75% or More but below 90% of Projection 3• Achievement is 60% or More but below 75% of Projection 2• Achievement is below 60% of Projection &/or below last year actual. 0C.4.B.1. FOR FRESH CONNECTIONS WHERE PROJECTIONS FOR NET PROFITNOT AVAILABLE (IN PLACE OF C.4.B)

SCORENA

• N. Profit Growth during the year Exceeds 20% of last two yearaverage N. Profit

6

• N. Profit Growth during the year is 15% -20%of last two year averageN. Profit

5

• N. Profit Growth during the year is 10% -15% of last two yearaverage N. Profit

3

• N. Profit Growth during the year is 5%- 10% of last two year averageN. Profit

2

• N. Profit Growth during the year is below 5% of last two year averageN. Profit

0

Scores under Credibility (“C.4.A+C.4.B” or C.4.A.1+C.4.B.1)

D) INDUSTRY/ACTIVITY RISK: (Aggregate Score 10)-D.1.For allIndustries/ActivitiesotherthanD.2below

COMPUTATION OF FINAL SCORE/GRADE:Sl.No.

RISKCATEGORY

MAXM.SCORE

ELIGIBLESCORE

SCOREOBTAINED

RISKWEIGHTS

(%)

RISKADJUSTED

SCOREX y Z y/x * z

A Financial Risk 36 35B Business Risk 26 20C Management Risk 36 35D Industry/Act. Risk 10 10E Total Marks 108 100

TOTAL RISK ADJUSTED SCORE: …… RATING AWARDED: …….

Marks Gradation Risk NatureMore than 90 1 Very LowMore than 80 & up to 90 2 LowMore than 70 & up to 80 3 Moderately LowMore than 60 & up to 70 4 FairMore than 50 & up to 60 5 ModerateMore than 40 & up to 50 6 HighMore than 35 & up to 40 7 Very High35 or below 8 Critical/Default

Comments of Level-1 Officer:-.

Comments of Level -2 Officer:-

CRG-03APPLICABLE FOR

Risk Grading Of Borrowers (With Existing Units / Projects)Having Aggregate Limit Above ` 200 Lakh

NameoftheBorrower:………………………………………..LineofActivity…………………………..Branch: ………………………………….. REGION:-

………………………………… ScoringBasedonAuditedBalanceSheetAsAt : -

ExistingFacility:Nature of Facility(TL/ WC/Others)

Credit Limit Outstanding Overdue/Other irregularities, if any

Total

ScoringUnderVariousRiskCategories:

A. FINANCIAL RISK: (Aggregate Score 36)Parameter Score

A.1) CURRENT RATIO• 1.33 or More 6• 1.25 or More but below 1.33 5• 1.17 or More but below 1.25 4• 1.13 or More but below 1.17 2• Below 1.13 0Comment:A.2) TOL /TNW RATIO• 3.00 and below 6• Above 3.00 but up to 4.00 5• Above 4.00 but up to 5.00 4• Above 5.00 but up to 7.50 2• Above 7.50 0Comment:A.3 a) INTEREST COVERAGE RATIO (PBDIT/INTERSET)• 3 or More 6• 2.50 or More but below 3 5• 1.75 or More but below 2.50 4• 1.50 or More but below 1.75 2• Below 1.50 0Comment:

A.3 b) AverageDSCR :Applicable for Fresh Term Loan of Existing Unit(In Such case Interest Coverage Ratio will be replaced by DSCR) Score• More than 1.75 : 1 6• From 1.50 : 1 to 1.75 : 1 4• From 1.30 : 1or More but below 1.50 : 1 2• Below 1.30 : 1 0Comment:A.4). RETURN ON CAPITAL EMPLOYED ** PBIT/Av. Capital Employed (In % ) , Where Capital Employed= Capital+Reserve+ Long Term Borrowing+ Other Bank Borrowing- Reval. Reserve-Capital W.I.P• 17% or More• BPLR+ 4% or More but below 17%• BPLR+ 2% or More but below BPLR+ 4%• Above BPLR but below BPLR+ 2%• BPLR or BelowComment:

A.5. Trend Analysis:TREND ANALYSIS – VARIATION IN NET CURRENT ASSET• Increasing Trend in Net Current Asset• Decreasing Trend in Net Current Asset• Stable (not more than 5% downward variation from previous year or

current ratio not below benchmark)TREND ANALYSIS – VARIATION IN TANGIBLE NET WORTH• Decreasing Trend in TNW• Increasing Trend in TNW• Stable (not more than 5% downward variation from previous year)TREND ANALYSIS: PROFITABILITY (NET PROFIT/NET SALES OR RECEIPT)• Increasing Trend in Profitability• Decreasing Trend in Profitability• Stable (not more than 2% downward variation from previous year)Comments

A.6 SECURITY COVERAGE (COLLATERAL)• 100% and above 6• 75% or More but below 100% 5• 60% or More but below 75% 4• 50% or More but below 60% 2• Below 50% 0COMMENTS:

B. BUSINESS RISK (TOTAL SCORE – 24)

B.1 KEY BUSINESS PARAMETERS YES (1) NO (O)i) Product range / mix is satisfactory.ii) Distribution set up is satisfactory/good.iii) Quality of the product is consistent.iv) It is enjoying the advantage of long term contract / Assured

B.1 KEY BUSINESS PARAMETERS YES (1) NO (O)off take.

v) Having financial ability to withstand competition.vi) The borrower is having bargaining power with suppliers.vii) Energy cost is reasonable / not effecting the bottom line to a

great extent.viii) The company / firm have adopted cost effective

management.ix) The company/ firm is having multi locational advantage.x) The after sale service of the company is good.xi) The future growth potential is high.xii) Capacity Utilisation is satisfactory (For mfg)

Total: Eligible Scores ---------------- , Scores Obtained

• More than 12 % 6• More than 10% but up to 12% 5• More than 8% but up to 10% 4• More than 6% but up to 8% 2• 6% or below 0COMMENTS:B.2. INCOME VALUE OF THE BANK: (Interest, Commission, Exchange etc.fromthe Account as Percentage of Total Fund Based Limit- Projected figure if newconnection but previous year actual if existing account)

SCORE

B. 3.MARKETABILITY (Tick the allotted Scores)• Market is broad based / diversified 6• Market is diversified but competitive. 5• Localised market but market share is good. 4• Market is confined to few customers 2.• Market is fragmented and highly competitive 1.

C. MANAGEMENT RISK (TOTAL SCORE – 42)

C.1. TRACK RECORD ( Tick the allotted Scores) SCOREi) High reputation in the market, good relationship with the Bank and

5 year & more experience in the line of activity.6.

ii) Good reputation in the market, good relationship with the Bank and3-5 years of experience in the line of activity.

5.

iii) Good reputation, good relationship with the Bank and 2-3 years ofexperience in the line of activity.

3.

iv) Moderate reputation, satisfactory relationship with the Bank andless experienced.

2.

v) Bad reputation/ no experience/ Bad relationship with the Bank (-)3C. 2. COMPOSITION OF MANAGEMENT (Tick the allotted Scores)i) Management is broad based and controlled by professionals./GOI

PSU6.

ii) Management is broad based & controlled by experiencedpersons./State Govt PSU

5

iii) Management is confined to family members.(closely held company) 4iv) Management is controlled by more than two key persons. 3v) Management is controlled by two persons. 2

vi) Management is controlled by sole person. 0C.3. Payment Records & Operations in the Account (In takeover cases,

assessment may be based on statement of accounts with existingBank & enquiry etc)

Score

C.3.a Payment of interest/instalment, payment of amount involved indevolved LC or Invoked B.G., Payment of Bills :

i) Due amt paid within 15 working days and less 6ii) Due amt paid between 16 working days to 30 working days. 5iii) Due amt paid between 31 working days to 45 working days. 3iv) Due amt paid between 46 working days to 60 working days. 2v) Due amt paid after 60 working days or since un paid. (-) 3

C.3.b Operations in the account (for working capital limit):In case of consortium/ multiple financing, sales would meanproportionate sales based on our share in total limit

i) High turnover (above 90% of sales) in the account & negligiblereturn of cheques.

6

ii) Good turnover (80-90% of sales)in the account & nominal return ofcheques.

4

iii) Average turnover (70-80% of sales) & average level of return ofcheques.

2

iv) Unsatisfactory turnover (below 70% of sales or 2 times of workingcapital limit, whichever is low ) &/or frequent return of cheques.

0

C.4. COMPLIANCE OF TERMS & CONDITIONS: SCOREi) All Terms and Conditions complied with. 6ii) Compliance of terms & Conditions other than creation of Collateral

Security due to reasons duly accepted by the Sanctioning Authority.4

iii) Non- Compliance of Major Terms & Conditions. 0C.5. Credibility: (C.5.A + C.5.B) OR (C.5.A.1 + C.5.A.2)C.5.A. PAST COMMITMENT WITH RESPECT TO NET SALES:• Achievement is 95% or above of Projection 6• Achievement is 90% or More but below 95% of Projection 5• Achievement is 75% or More but below 90% of Projection 3• Achievement is 60% or More but below 75% of Projection 2• Achievement is below 60% of Projection &/or below last year actual. 0C.5.A.1. FOR FRESH CONNECTIONS WHERE PROJECTIONS NOT AVAILABLE(IN PLACE OF C.5.A)• Sales Growth during the year Exceeds 20% of last two year average

Sales6

• Sales Growth during the year is 15% -20%of last two year average Sales 5• Sales Growth during the year is 10% -15% of last two year average

Sales4

• Sales Growth during the year is 5%- 10% of last two year average Sales 2• Sales Growth during the year is below 5% of last two year average Sales 0C.5.B. PAST COMMITMENT WITH RESPECT TO NET PROFIT:• Achievement is 95% or above of Projection 6• Achievement is 90% or More but below 95% of Projection 5• Achievement is 75% or More but below 90% of Projection 3• Achievement is 60% or More but below 75% of Projection 2• Achievement is below 60% of Projection &/or below last year actual. 0C.5.B.1. FOR FRESH CONNECTIONS WHERE PROJECTIONS FOR NET PROFIT SCORE

NOT AVAILABLE (IN PLACE OF C.5.B)• N. Profit Growth during the year Exceeds 20% of last two year average

N. Profit6

• N. Profit Growth during the year is 15% -20%of last two year averageN. Profit

5

• N. Profit Growth during the year is 10% -15% of last two year averageN. Profit

3

• N. Profit Growth during the year is 5%- 10% of last two year average N.Profit

2

• N. Profit Growth during the year is below 5% of last two year averageN. Profit

0

D. INDUSTRY /ACTIVITY RISKD.1. For allIndustries/ActivitiesotherthanD.2.below (Score-40)

1. TECHNOLOGY (FOR MANUFACTURING)(Tick the allotted Scores)

SCORES

i) Modern Technology has been adopted and operation is integrated. 6.ii) Technology is proven in the medium term & cost effective 5iii) Technology requires for updating & steps initiated by the

management.3

iv) Technology is old and no modernisation has been undertaken. 2v) Technology is new and untested 0vi) Technology is obsolete (-6)1A. ACTIVITY (IT WILL REPLACE S. No D.1 IN CASE OF NON MFG. UNITS)

(Tick the allotted Scores)i) Activity undertaken widely accepted by the customers / or strong

brand equity and proven for long term.6

ii) Activity is concentrated amongst organised sector and proven formedium term.

5

iii) Activity is concentrated amongst unorganised sector and proven formedium term.

3

iv) Large number of players engaged in same activity and brand andhaving future growth potential.

2

v) Activity undertaken is not having growth potential. 02. REGULATORY (Tick the allotted Scores)i) Govt. regulations / policy for the activity undertaken is highly

favourable.6

ii) Govt. regulations / policies is moderately favourable. 5iii) Govt. Regulations is negligible and having negligible adverse impact 4iv) Govt. Regulations is negligible but imposition of higher sales tax/

excise duty etc. or withdrawals of subsidies may affect the overallperformance.

3

v) Present govt. policies are stringent. 03. IMPORT THREAT (For manufacturing)

(Tick the allotted Scores)i) Indigenous product/s leads the market and no import threat 6ii) Price & quality of indigenous product/s having edge over imported

products.5

iii) Price of imported product is lower than indigenous product but 4

customer prefers indigenous product.iv) Both imported & indigenous product/s have nearly equal market

share.3

v) Import substitute is available but distribution network of indigenousproduct is stronger.

2

vi) Imported substitute is having edge over indigenous product both interms of market and quality.

(-3)

4. AVALIBILITY OF RAW MATERIAL/PRODUCT(Tick the allotted Scores)

i) Adequately available locally from several suppliers or manufacturers& volatility of price (increasing trend) is less than 7.5%

6.

ii) Generally available from several suppliers and price is volatile butless than 7.50% which can be passed on to customers with ease.

5

iii) Normally available but sourced from outside states. 4iv) Normally available but partly sourced indigenously and partly from

export.3

v) Outsourced from foreign suppliers. 2vi) Scarce item & dependent on few supplier/s. 15. OTHER KEY FEATURES OF THE INDUSTRY/ ACTIVITY

(Score to be allowed 2 or 0 in respect of each parameters )YES(2)

NO (0)

i) The demand for Product is adequate / increasing.ii) Borrowers not dealing with perishable products.iii) Foreign exchange component (cost) of the business is not

significant.iv) Advantageous Location of the Industry/ activityv) No pollution / environmental risk.vi) Not dependent on job work / unbranded item.vii) Business does not fall under sensitive sector as declared by

RBI.viii) Industry / activity does not depend not depend on the

vagaries of nature.TOTAL 16

COMPUTATION OF TOTAL SCORES UNDER CRG3:

Sl.No.

RISKCATEGORY

MAXIMUMSCORE

ELIGIBLESCORE

SCOREOBTAINE

D

RISKWEIGHTS

(%)

RISKADJUSTED

SCOREX Y z y/x * z

A Financial Risk 36 35B Business Risk 24 25C Management Risk 42 20D Industry/Act. Risk 40 20E Total Marks 142 100

TOTALRISKADJUSTEDSCORE: RATINGAWARDED:

Marks Gradation Risk NatureMore than 90 1 Very LowMore than 80 & up to 90 2 LowMore than 70 & up to 80 3 Moderately Low

More than 60 & up to 70 4 FairMore than 50 & up to 60 5 ModerateMore than 40 & up to 50 6 HighMore than 35 & up to 40 7 Very High35 or below 8 Critical/Default

Comments of Level-1 Officer:-

Comments of Level -2 Officer:-

Comments of Level-3 Officer:-

CRG-04

APPLICABLE FORRisk Grading of Borrowal accounts (with New units/ project) having Aggregate CreditLimit of `10.00 Lac and above but excluding SSI & SME with `1.00 crore or more limit/ service sector / FIs etc. which are covered under CRG-05 to CRG 7 Modules.

NameoftheBorrower:-

LineofActivity:-

Branch:- REGION: -

ScoringBasedonAuditedBalanceSheetAsAt: -

A. FINANCIALRISK:(AggregateScore-36) :-

Parameter ScoreA.1. Promoter’s Contribution (For Term Loan or TL + WC )• 33% or more of the Total Project Cost 6• 25% or More but below 33% 4• 20% or More but below 25% 2• Below 20% 0A.1 a ).Net Working Capital/ Total Current Assets(For Working Capital): Projected Figure accepted by the Bank to betaken.• 33% or more 6 6• 25% or More but below 33% 4• 20% or More 2• Below 20% 0A.2. Projected Average DSCR (For Term Loan)• Average DSCR is more than 2.00:1 6• Average DSCR is ranging from 1.75:1 to 2.00:1 4• Average DSCR is 1.33:1or More but below 1.75:1 2• Average DSCR is less than 1.33:1 0A.3. Projected interest coverage ratio (For Working Capital)• 3 or More 6• 2.50 or More but below 3 4• 1.75 or More but below 2.50 2• Below 1.75 0A.4. Repayment Period ,Including Moratorium (For term loan)• Up to 4 years 6• Above 4 years to 5 Years 4• Above 5 years to 7 years 2• Above 7 years 0A.5. Return (PBIT) on Capital EmployedCapital Employed = Capital+ Reserve+ Long Term Borrowing+Other Bank Borrowing- Revaluation Reserve-Capital W.I.P (Total of

Score

year wise projections covering the repayment period shall beconsidered in TL and following year projection in Working Capital)• 17% or More 6• BPLR+ 4% or More but below 17% 5• BPLR+ 2% or More but below BPLR+ 4% 3• Above BPLR but below BPLR+ 2% 2• BPLR or Below 0A.6. Asset Coverage Ratio ( Primary + Collateral / Total SecuredLoan)• 2:1 or More 6• 1.50:1 or More but below 2:1 4• 1.25:1 or More but below 1.50:1 2• Below 1.25:1 0

B. MANAGEMENT RISK: TOTAL SCORE: - 30

B.1. TRACK RECORD SCORE•High Reputation ,Technically qualified and Experienced 6•High Reputation and Experienced 5•Good Reputation and Experienced 4•Good Reputation Less Experienced 3•Market reputation is Bad (-)3

B.2. COMPOSITION OF MANAGEMENT•Management is in the hand of several key persons 6•Management is controlled by few persons 4•Management is controlled by only two persons 3•Management Controlled by sole person. 2

B.3. QUALITY OF MANAGEMENT•Excellent 6•Good 4•Satisfactory 2

B.4. RELATIONSHIP WITH THE BANK•Management is having relationship with Bank for more than 5

years6

•Past five years Relationship with the Bank is highly satisfactory 5•Past Relationship with the Bank is Good 4•Management is having relationship with other Banks with good

Reputation3

•Management is new to the Bank and well experienced in theBusiness

2

B.5. EXPERIENCE•Management is in the line of business for more than 5 years 6•Management is in the line of business for 3-5 years 4•The Line of Business is new to the Management but

Experienced in other areas.3

•The Line of Business is new to the Management but havingfamily Background.

2

•Management is totally new entrant in the business and no 0

family Background.Total Score under Management

Comment on Management Aspects:

C. BUSINESS RISK: TOTAL SCORE: - 20

C.1. Key Business Features SCOREScore to be allowed 2 or 0 for each parameter in respect ofthe following :

YES (2) NO (0)

Wide Fluctuation is not expected in demand and supply innear futureBorrowers not dealing in perishable goods.Future Growth potential is highForeign Exchange component of the Firm’s business is notsignificant.The business is not sensitive to the changes in Govt.policies like price control, pollution, changes in Custom andExcise duties etc.Energy and employee cost is not high enough or puttingpressure on bottom line.Borrowers not dependent on few customersProduct range / mix is satisfactoryManagement is financially able to withstand competition.There are only few competitors in the market.Score ObtainedComment on Business Aspects:

D.INDUSTRY/ACTIVITY RISK: TOTAL SCORE: - 20D.1.For allIndustries/ActivitiesotherthanD.2below

Key Features of Industry/Activity SCOREScore to be allowed 2 or 0 for each parameter in respect of thefollowing :

YES(2)

NO(0)

i) Present industry/activity scenario dealt by is favourable 2ii) Technology/Activity is proven for medium term 2iii) Availability of raw materials/products (Traders) is adequate 2iv) The prices of raw material/finished goods do not show much

fluctuation.2

v) Adequate power and fuel is available. 2vi) All other infrastructure facilities like road or rail, water supply,

telephone etc are available.2

vii) Skilled manpower is available in the locality 2viii) Presence of large cost-competitive organised sector is nominal 2ix) Industry/Activity does not depend on the vagaries of nature. 0x) Firm is not assembler or trader of unbranded items. 0

Score Obtained 16Comment on Industry/Activity Aspects:

COMPUTATION OF TOTAL SCORE:

COMPUTATION OF TOTAL SCORES UNDER CRG4:

Sl.No.

RISKCATEGORY

MAXIMUMSCORE

ELIGIBLESCORE

SCOREOBTAINED

RISKWEIGHTS

(%)

RISKADJUSTED

SCOREX Y z y/x * z

A Financial Risk 36 25B Management Risk 30 35C Business Risk 20 20D Industry/Act. Risk 20 20E Total Marks 106 100

TOTAL RISK ADJUSTED SCORE: RATING AWARDED:

Marks Gradation Risk NatureMore than 90 1 Very LowMore than 80 & up to 90 2 LowMore than 70 & up to 80 3 Moderately LowMore than 60 & up to 70 4 FairMore than 50 & up to 60 5 ModerateMore than 40 & up to 50 6 HighMore than 35 & up to 40 7 Very High35 or below 8 Critical/Default

Comments of Level-1 Officer:-

Comments of Level -2 Officer:-

Comments of Level-3 Officer:-

S. No RISK FACTORS SCOREA.1 TOL/TNW (As per Last Audited Balance Sheet in Existing Unit

& Highest during Projection Period in case of New Unit/Project)

i) Less than 4.00:1 6ii) 4 or More but up to 5 5iii) More than 5 but up to 6 4iv) More than 6 but up to 7.5 2v) Above 7.50 0

Score Obtained ---A.2 (a) Interest Coverage Ratio (ICR)- PBDIT / INTERESTi) More than 3 times 6

ii) More than 2 but up to 3 times 4iii) More than 1.5 but up to 2 times 2iv) 1.50 times or Less 0

Score obtained --A.2 (b) Average Debt Service Coverage Ratio ( ICR to be replaced in

case of fresh term loan)i) Avg. DSCR more than 1.75:1 6ii) Avg. DSCR more than 1.60 but up to 1.75 5iii) Avg. DSCR 1.50 or more but up to 1.60 4iv) Avg. DSCR 1.30 or more but below 1.50 2

CRG-05

APPLICABLE FORRisk Grading of Borrowal Accounts with 10 Lakh & above aggregate credit limitfalling under following categories:

Service Sectors (Railway, Airways, State Road Transport Corp, TransportBusiness, Nursing Home, Amusement Park Hospital etc)Municipality Or Corporation/Development AuthorityEducational Institute

FUNDED-TERM LOAN/WORKINGCAPITAL&/OR NONFUNDBASEDFACILITY

Name of the borrower:Line of Activity:Branch: Region:

Existing Facility:Nature of Facility(TL/ WC/Others)

Credit Limit Outstanding Overdue/Other irregularities, if any

Total

ScoringUnderVariousRiskCategories:

A. FINANCIALRISK (AGGREGATE SCORE- 42 )

v) Avg. DSCR less than 1.30 0Score Obtained ---

A.3. RETURN ON CAPITAL EMPLOYED *PBIT/Capital Employed (In % ) , Where Capital Employed =Capital+ Reserve+ Long Term Borrowing+ Other BankBorrowing- Revaluation Reserve-Capital W.I.P (In case of newunits, Total of year wise projections covering the repaymentperiod shall be considered)

SCORE

i) 17% or More 6ii) BPLR+ 4% or More but below 17% 5iii) BPLR+ 2% or More but below BPLR+ 4% 3iv) Above BPLR but below BPLR+ 2% 2v) BPLR or Below 0vi) Incurring Net Loss for existing unit only (-2)vii) Incurring cash loss for existing unit only (--4)

Score obtained ---A.4. Current Ratio (As per Last Audited Balance Sheet in Existing

Unit & average of first 3 years of projection for New Unit/Project will be considered)

i) 1.33:1 or More 6ii) 1.30 :1 or More but below 1.33:1 5iii) 1.25:1 or More but below 1.30:1 4iv) 1.17 :1 or More but below 1.25:1 2v) Below 1.17:1 0

Score Obtained ---A.5. REPAYMENT PERIOD (INCLUDING MORATORIUM PERIOD):

(In case of existing term loan residual period to beconsidered provided the Account is regular)

i) Up to 3 years 6ii) Above 3 years and up to 4 years 5iii) Above 4 years and up to 5 years 4iv) Above 5 years and up to 7 years 2v) Above 7 years 0

Score Obtained ---A.6. Security Coverage (Primary + Collateral / Aggregate Secured

Loan from Bank) NOTE :-If outstanding is covered only byGovt. Guarantee, Score will be 4

i) 2.25:1or More 6ii) 2:1 or More but below 2.25:1 5iii) 1.75:1 or More but below 2:1 4iv) 1.50:1 or More but below 1.75:1 2v) 1.25:1 or More but below 1.50:1 1vi) Below 1.25:1 0

Score obtained ---A.7. Contingent Liabilityi) No/Low effect on the overall financial position 6ii) Moderate effect on overall financial position 4iii) Significant effect on overall financial position (-2)

Score Obtained ---

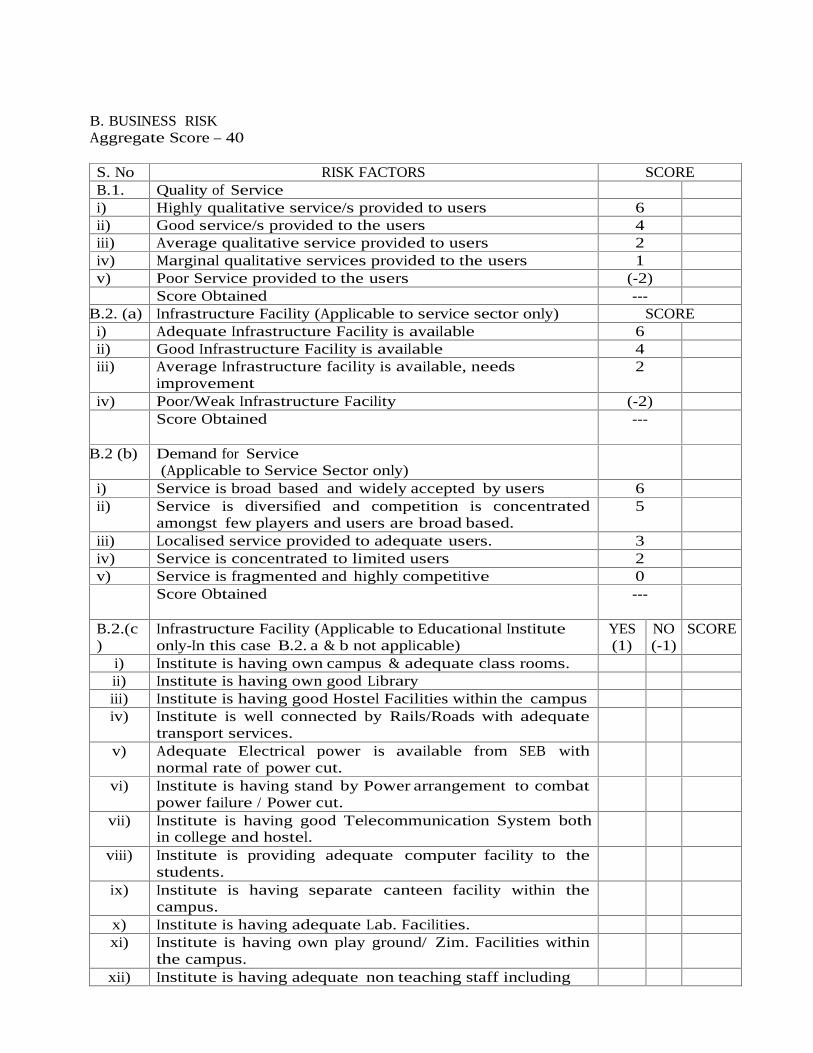

B. BUSINESS RISKAggregate Score – 40

S. No RISK FACTORS SCOREB.1. Quality of Servicei) Highly qualitative service/s provided to users 6ii) Good service/s provided to the users 4iii) Average qualitative service provided to users 2iv) Marginal qualitative services provided to the users 1v) Poor Service provided to the users (-2)

Score Obtained ---B.2. (a) Infrastructure Facility (Applicable to service sector only) SCORE

i) Adequate Infrastructure Facility is available 6ii) Good Infrastructure Facility is available 4iii) Average Infrastructure facility is available, needs

improvement2

iv) Poor/Weak Infrastructure Facility (-2)Score Obtained ---

B.2 (b) Demand for Service(Applicable to Service Sector only)

i) Service is broad based and widely accepted by users 6ii) Service is diversified and competition is concentrated

amongst few players and users are broad based.5

iii) Localised service provided to adequate users. 3iv) Service is concentrated to limited users 2v) Service is fragmented and highly competitive 0

Score Obtained ---

B.2.(c)

Infrastructure Facility (Applicable to Educational Instituteonly-In this case B.2. a & b not applicable)

YES(1)

NO(-1)

SCORE

i) Institute is having own campus & adequate class rooms.ii) Institute is having own good Libraryiii) Institute is having good Hostel Facilities within the campusiv) Institute is well connected by Rails/Roads with adequate

transport services.v) Adequate Electrical power is available from SEB with

normal rate of power cut.vi) Institute is having stand by Power arrangement to combat

power failure / Power cut.vii) Institute is having good Telecommunication System both

in college and hostel.viii) Institute is providing adequate computer facility to the

students.ix) Institute is having separate canteen facility within the

campus.x) Institute is having adequate Lab. Facilities.xi) Institute is having own play ground/ Zim. Facilities within

the campus.xii) Institute is having adequate non teaching staff including

Security Staffs.Score Obtained ---- ----

B.3. Business Aspects YES(2)

NO(0)

FINALSCORE

i) Service/s provided is/are users’ friendly / adequateeducational streams available with the Institute.

ii) Users are not enjoying multiple choices to avail from otherplayers/ Institutes for same type of service.

iii) Quality of services are consistentiv) Average work force / Teaching staffs are skilled / qualified

& experienced.v) Having financial ability to withstand competition.

Score ObtainedB.4. Regulatory Risk SCOREi) No price control or monopoly business. 6ii) Price control with escalation clause / subsidies 4iii) Price control without subsidies but reviewed by the

regulator from time to time.2

iv) Price fixed by the Regulator without any adjustment clause 0Score Obtained

B.5 Income Value of the Bank on annualised basis(in case of new connection, give value based on projection)

i) 12% or More 6ii) 11% or More but below 12% 5iii) 10% or More but below 11% 4iv) 8% or More but below 10% 2v) 6% or More but below 8% 1vi) Below 6% 0

Score obtainedTOTAL SCORE FOR BUSINESS (Sum of B1 to B5)

C. MANAGEMENT RISK Aggregate Score – 36

C.1. Type of Management Scorei) Reputed multinationals/ PSU sector (G.O.I) / Quoted Public

Limited Co. with professional directors/ Professionallymanaged institute with financial supportfrom Government.

6

ii) PSU sector (State Govt. Undertaking)/ Joint venture/Professionally managed Institute/ Private Ltd. Promoted byreputed Group or Professionals.

4

iii) Closely held Private Ltd. 3iv) Partnership/ Closely managed institute 2v) Proprietorship / Co-operative Society./ Trustee 1

Score Obtained ---C.2. Quality of Management

i) Management is in the hands of professionals with lessinterference from promoters.

6

ii) Promoters are supported by professionals & experiencedpersons.

5

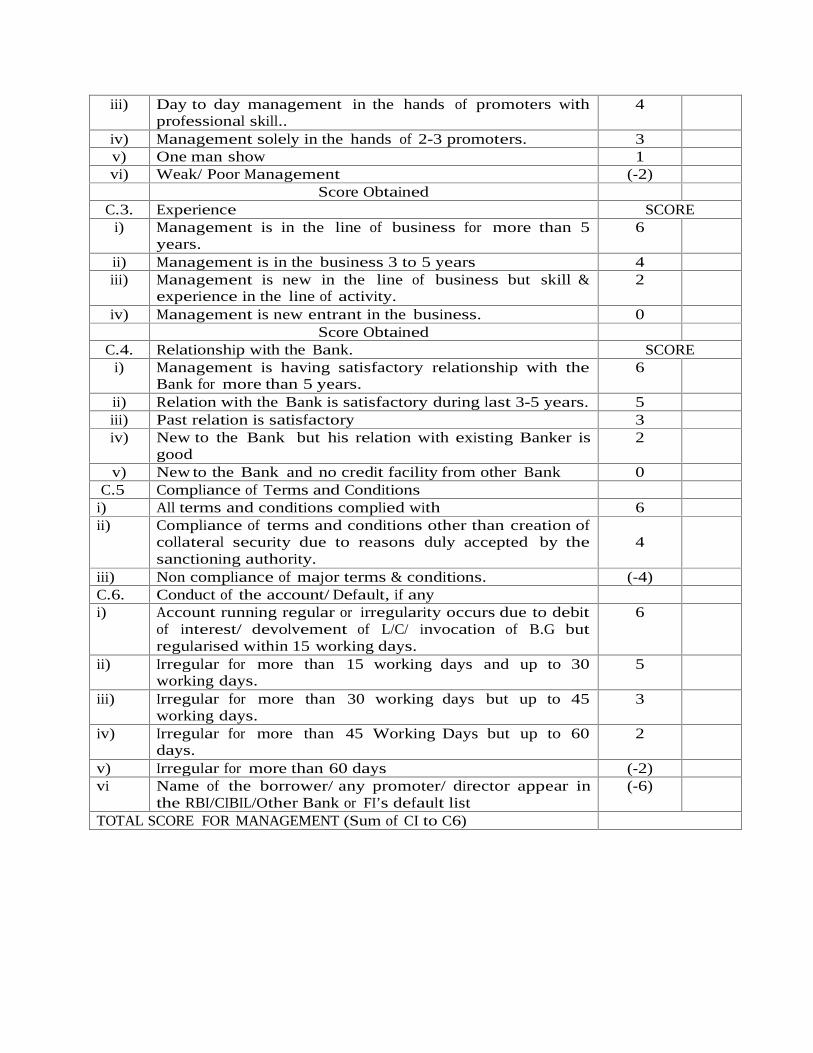

iii) Day to day management in the hands of promoters withprofessional skill..

4

iv) Management solely in the hands of 2-3 promoters. 3v) One man show 1vi) Weak/ Poor Management (-2)

Score ObtainedC.3. Experience SCORE

i) Management is in the line of business for more than 5years.

6

ii) Management is in the business 3 to 5 years 4iii) Management is new in the line of business but skill &

experience in the line of activity.2

iv) Management is new entrant in the business. 0Score Obtained

C.4. Relationship with the Bank. SCOREi) Management is having satisfactory relationship with the

Bank for more than 5 years.6

ii) Relation with the Bank is satisfactory during last 3-5 years. 5iii) Past relation is satisfactory 3iv) New to the Bank but his relation with existing Banker is

good2

v) New to the Bank and no credit facility from other Bank 0C.5 Compliance of Terms and Conditions

i) All terms and conditions complied with 6ii) Compliance of terms and conditions other than creation of

collateral security due to reasons duly accepted by thesanctioning authority.

4

iii) Non compliance of major terms & conditions. (-4)C.6. Conduct of the account/ Default, if anyi) Account running regular or irregularity occurs due to debit

of interest/ devolvement of L/C/ invocation of B.G butregularised within 15 working days.

6

ii) Irregular for more than 15 working days and up to 30working days.

5

iii) Irregular for more than 30 working days but up to 45working days.

3

iv) Irregular for more than 45 Working Days but up to 60days.

2

v) Irregular for more than 60 days (-2)vi Name of the borrower/ any promoter/ director appear in

the RBI/CIBIL/Other Bank or FI’s default list(-6)

TOTAL SCORE FOR MANAGEMENT (Sum of CI to C6)

D. ACTIVITY RISKD.1.For allIndustries/ActivitiesotherthanD.2below

Aggregate Score – 32

1. Nature of Activity SCOREi) Services or educations provided are basic necessities and

users are crazy to avail the services/education.6

ii) Services or education provided are proven for mediumterm / utility in nature.

5

iii) Services or education provided are proven but usershaving multiple options.

3

iv) Services /Courses are new and untested 0v) Services or education provided are not users friendly or

quality of education is discouraging.(-6)

2. Major Input Costi) Input cost (like overhead, Power, Maintenance,

advertisement etc) is steady & nominal price variation (notmore than 5%).

6

ii) Input cost is volatile but increased cost can be passed onto users.

5

iii) Input cost is volatile but increased price can be passed onto users as per price structure determined by the Govt.from time to time.

3

iv) Input cost is volatile but due to extreme competitivemarket a part of increased price can be passed on tousers.

2

v) Input cost is highly volatile and increased cost can not bepassed on to users frequently.

0

3. Position within the sectori) Dominant Player 6ii) One of the major players 4iii) Smaller player reasonably performing well 3iv) Marginal player with gradual increase in market share 2v) Marginal player with declining market share (-3)4. Users Basei) Broad based users having high demand. 6ii) Considerable spread of users having adequate demand 5iii) Reasonable spread of users having fair/average demand 3iv) Dependence on few users having stable demand 2v) Dependence on few users having unstable demand 05 Key Activity aspects Yes

(2)No(-2)

Scores

i) Advantageous location of the business activity.ii) Govt. Regulations and Policies are favourable.iii) The Institute is affiliated to a reputed University / Services

are having brand equity in the market.iv) Services rendered are cost effective to users applicable to

services sector/ Placement cell facility available applicablefor Educational Institute...

TOTAL SCORE FOR INDUSTRY/ACTIVITY (Sum of 1 to 5 of D.1.)

COMPUTATION OF FINAL SCORE/GRADE (CRG 5)

SL.NO.

RISK CATEGORY MAXM.SCORE

ELIGIBLESCORE

SCOREOBTAINED

RISKWEIGHT

(%)

RISKADJUSTED

SCOREX Y Z Y/X * Z

A. FINANCIAL RISK 42 30B. BUSINESS RISK 40 30C MANAG. RISK 36 20D ACTIVITY RISK 32 20E TOTAL MARKS 150 100

TOTAL RISK ADJUSTED SCORE :- RATING AWARDED:

TOTAL RISK ADJUSTEDSCORE

GRADATION NATURE OF RISK

More than 90 1 Very LowMore than 80 & up to 90 2 LowMore than 70 & up to 80 3 Moderately LowMore than 60 & up to 70 4 FairMore than 50 & up to 60 5 ModerateMore than 40 & up to 50 6 HighMore than 35 & up to 40 7 Very High35 or below 8 Critical/Default

Comments of Level-1 Officer:-

Comments of Level -2 Officer:-

Comments of Level-3 Officer:-

CRG-06

APPLICABLE FOR RISK GRADING OFRisk Grading of Borrowal Accounts with 10 Lakh & above aggregate credit limitfalling under following categories:

NBFC / Financial InstitutionIntermediaries engaged in lending activities (like lending for Project,Infrastructural Development, and Housing.)Financial Corporation like IRFC etc.

FUNDED-TERM LOAN/WORKINGCAPITAL&/OR NONFUNDBASEDFACILITYWITHAGGREGATELIMITOF`25LAKHORMORE

Name of the borrower:Line of Activity:Branch: Region:

Existing Facility:Nature of Facility(TL/ WC/Others)

Credit Limit Outstanding Overdue/Other irregularities, if any

Total

ScoringUnderVariousRiskCategories:

A. FINANCIAL RISK AGGREGATE SCORE:- 42

S. No RISK FACTORS SCOREA.1. CURRENT RATIO:

i) 1.50:1 or More 6ii) 1.40:1 or More but below 1.50:1 5iii) 1.33 :1 or More but below 1.40:1 4iv) 1.25:1 or More but below 1.33:1 2v) 1.17 :1 or More but below 1.25:1 1vi) Below 1.17:1 0

Score Obtained ---A.2 (a). TOL/ NOF (Applicable To Nbfc Other Than Housing

Intermediaries)i) Below 3.00:1 6ii) 3:1 or More but below 4:1 5iii) 4:1 or More but below 5:1 4iv) 5:1 or More but below 6.5:1 2v) 6.5:1 or More but below 7.50:1 1vi) 7.5:1 or More 0

Score Obtained ---A.2(b) TOL/NOF (Applicable To Housing Intermediaries Only)

i) Below 7:1 6

ii) 7:1 or More but below 7.50 5iii) 7.50 or More but below 8:1 4iv) 8:1 or More but below 8.50:1 2v) 8.50:1 or More but below 9:1 1vi) 9:1 or More 0

Score Obtained ---

A.3(a)Capital To Risk Weighted Asset Ratio (CRAR): ApplicableTo NBFC Other Than Housing Intermediaries

i) CRAR 16 % or more (NBFC) and 13.50% or more(Housing Finance Companies)

6

ii) CRAR 15.50% or more but below 16% (NBFC) & CRAR13% or more but below 13.50% (Housing FinanceCompanies)

5

iii) CRAR above 15% but below 15.50% (NBFC) & CRARabove 12.5% but below 13% (Housing Finance)

4

iv) CRAR equals to 15% (NBFC) & CRAR 12.5% or more butup to 12% (Housing Finance Companies)

3

v) CRAR less than 15% (NBFC) & 12% (Housing FinanceCompany)

(-2)

Score Obtained ---A.3 (b) Interest Coverage Ratio [PBDIT/ Total Interest Paid]:

Applicable To Govt Companies / Institution Where CRARIs Not Applicable)

i) Above 3 times 6ii) 2.50 times or more but up to 3 times 5iii) 2 times or more but less than 2.50 times 4iv) 1.50 times or more but less than 2.00 times 2v) Below 1.50 times 0

Score Obtained ---A.4. % Profit Before Tax To Total Tangible Assets

i) 14% or More 6ii) 12% or More but below 14% 5iii) 10% or More but below 12% 4iv) 8% or More but below 10% 2v) Below 8% 1

Score Obtained ---A.5 (a). NPA / Total Working Assets In Percentage Terms

(Applicable To NBFC)i) Below 1% 6ii) 1% or more but below 2% 5iii) 2% or more but below 3% 4iv) 3% or more but below 4% 2v) 4% or more but up to 5% 1vi) Above 5% 0

Score obtained ---A.5.

(b)RECOVERY RATE %(Where above factor 5(a) is not applicable)

i) 90% & Above 6ii) 85% or More but below 90% 5iii) 80% or More but below 85% 4iv) 75% or More but below 80% 2

v) 65% or More but below 75% 1vi) Below 65% (-2)

Score obtained ---A.6. RETURN ON CAPITAL EMPLOYED= PBIT / Avg. Capital

Employed (In % ), Where Capital Employed= Capital+Reserve+ Long Term Borrowing+ Other BankBorrowing- Revaluation Reserve-Capital W.I.P

i) 17% or More 6ii) BPLR+ 4% or More but below 17% 5iii) BPLR+ 2% or More but below BPLR+ 4% 3iv) Above BPLR but below BPLR+ 2% 2v) BPLR or Below 0

Score obtained ---A.7. PAT/ TOTAL INCOME (Net Of Non Recurring Income) %

i) 10% & above 6ii) 8.50% or More but below 10% 5iii) 7.50% or More but below 8.50% 4iv) 5.50% or More but below 7.5% 2v) 3% or More but below 5.50% 1vi) Below 3% 0

Score obtained ---

B. BUSSINESS RISK AGGREGATE SCORE -34

B.1. REGULATORY RISK SCOREi) Business not affected by regulatory framework. 6ii) Favourable regulatory and financial environment. 5iii) Regulatory and legislative issues create some

vulnerability but potential impact on the company notsignificant & the issues can be tackled appropriately.

3

iv) Demanding legal and financial regulatory environmentscan be problematic if company does not take care.

0

v) Legal, regulatory environment problematic; can delivershocks affecting the viability of the company.

(-2)

Score obtainedB.2. Prospect of the businessi) Long term prospects of the business are excellent. 6ii) Long term outlook / Business aspect is stable. 4iii) Business aspect is volatile due to competition but

company has the capability to withstand competition.2

iv) Business aspect is uncertain 0Score obtained

B.3. Market Positioni) Market is broad based due to multi locational

advantage./ Financial services of wide acceptance.6

ii) Market is diversified and competition is concentratedamongst very few players.

5

iii) Localised market with stable or increasing demand. 3iv) Market is concentrated to limited acceptors. 1v) The users are increasingly employing other alternative 0

methods for raising resources/ Market share isdeclining.Score obtained

B.4 Income Value of the Bank on annualised basis (Totalinterest earned / Average Funded Limit of the Bank)

Score

i) 12.50% or More 6ii) 10.00% & More but below 12.50% 5iii) 9.00% & More but below 10.00% 4iv) 8.00% & More but below 9% 2v) 7.50% & More but below 8.00% 1vi) Below 7.50% 0

Score obtained -B.5. Key Business Aspects YES

(2)NO(0)

i) Financial Service/s provided is/are users’ friendly.ii) The Company is above average playeriii) The company is complying with regulatory

requirement.iv) The business is not crowded in that particular area of

operationv) The business is having strategic alliance with

International company/ Banks/Financial Institution./Govt.

Score ObtainedC. MANAGEMENT RISK AGGREGATE SCORE:- 50

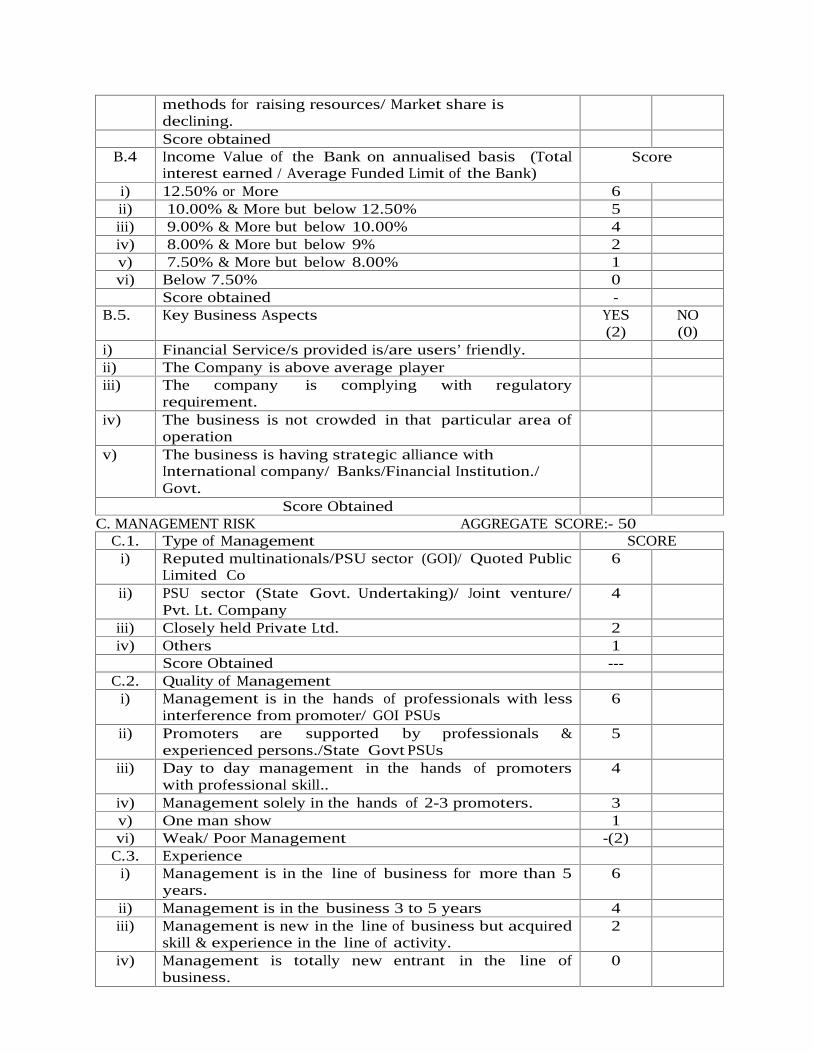

C.1. Type of Management SCOREi) Reputed multinationals/PSU sector (GOI)/ Quoted Public

Limited Co6

ii) PSU sector (State Govt. Undertaking)/ Joint venture/Pvt. Lt. Company

4

iii) Closely held Private Ltd. 2iv) Others 1

Score Obtained ---C.2. Quality of Management

i) Management is in the hands of professionals with lessinterference from promoter/ GOI PSUs

6

ii) Promoters are supported by professionals &experienced persons./State Govt PSUs

5

iii) Day to day management in the hands of promoterswith professional skill..

4

iv) Management solely in the hands of 2-3 promoters. 3v) One man show 1vi) Weak/ Poor Management -(2)

C.3. Experiencei) Management is in the line of business for more than 5

years.6

ii) Management is in the business 3 to 5 years 4iii) Management is new in the line of business but acquired

skill & experience in the line of activity.2

iv) Management is totally new entrant in the line ofbusiness.

0

C.4. Relationship with the Bank.i) Management is having satisfactory relationship with

the Bank for more than 5 years.6

ii) Relation with the Bank is satisfactory during last 3-5years.

5

iii) Past relation is satisfactory 3iv) New to the Bank but good relation with existing

Banker.2

v) New to the Bank. 0C.5. Key Management Aspects YES (2) NO(-2)

i) The company is having easy access to tap capitalmarket.

ii) The policy of the management for disclosure in thebalance sheet is fair.

iii) The management has a well defined strategy for thefuture.

iv) The management is not prone to unrelateddiversification.

v) In case of need Group support/Govt. support isavailable.

vi) The management is not prone to take exposure to thehigh risk stock market through its subsidiaries.

vii) The management is giving thrust on retail business.Score Obtained

C.6. Compliance of Terms and Conditions.(For existing A/C)i) All terms and conditions complied with 6ii) Compliance of terms and conditions other than creation

of collateral security due to reasons duly accepted bythe sanctioning authority.

4

iii) Non compliance of major terms & conditions. (-2)Score Obtained ---

C.7. Conduct of the account/Default Positioni) Account running regular or irregularity occurs due to

debit of interest/ devolvement of L/C/ invocation of B.Gbut regularised within 15 working days.

6

ii) Irregular for more than 15 working days and up to 30working days.

5

iii) Irregular for more than 30 working days but up to 45working days.

3

iv) Irregular for more than 45 Working Days but up to 60days.

2

v) Irregular for more than 60 days (-3)vi) Name of the Borrower/Promoter/Director appear in

RBI/CIBIL/Other Bank or FI’s Default list(-6)

Score Obtained ---

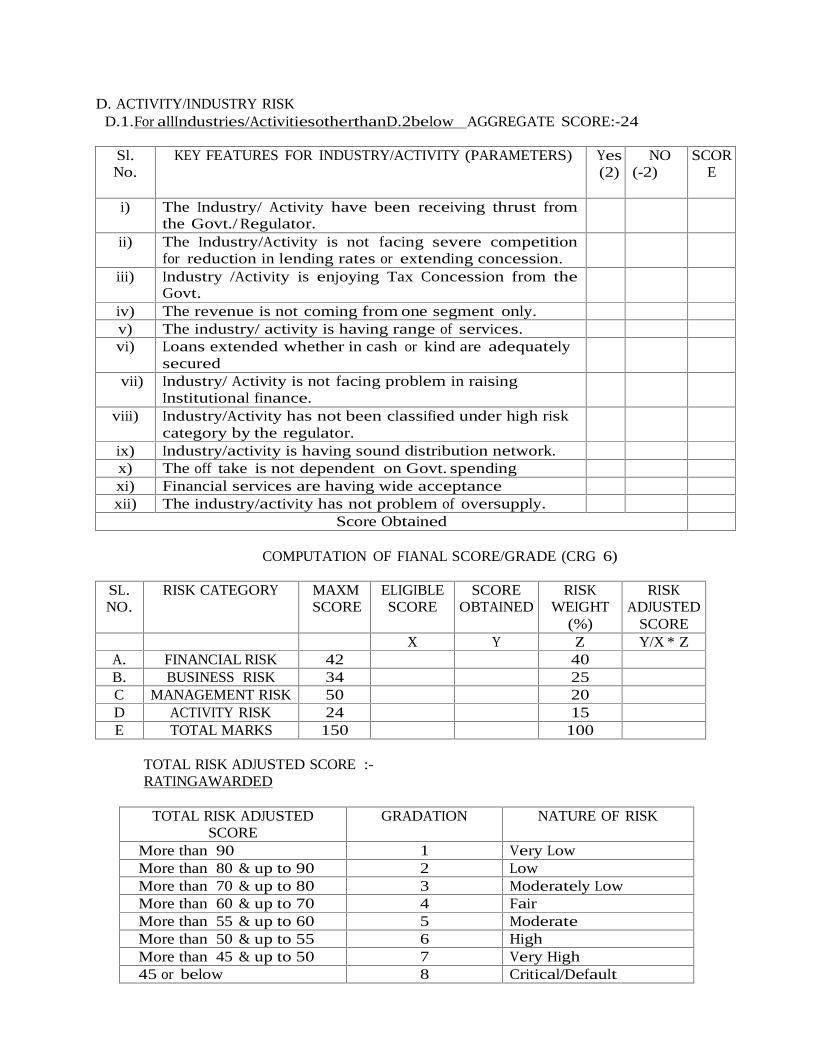

D. ACTIVITY/INDUSTRY RISKD.1.For allIndustries/ActivitiesotherthanD.2below AGGREGATE SCORE:-24

Sl.No.

KEY FEATURES FOR INDUSTRY/ACTIVITY (PARAMETERS) Yes(2)

NO(-2)

SCORE

i) The Industry/ Activity have been receiving thrust fromthe Govt./ Regulator.

ii) The Industry/Activity is not facing severe competitionfor reduction in lending rates or extending concession.

iii) Industry /Activity is enjoying Tax Concession from theGovt.

iv) The revenue is not coming from one segment only.v) The industry/ activity is having range of services.vi) Loans extended whether in cash or kind are adequately

securedvii) Industry/ Activity is not facing problem in raising

Institutional finance.viii) Industry/Activity has not been classified under high risk

category by the regulator.ix) Industry/activity is having sound distribution network.x) The off take is not dependent on Govt. spendingxi) Financial services are having wide acceptancexii) The industry/activity has not problem of oversupply.

Score Obtained

COMPUTATION OF FIANAL SCORE/GRADE (CRG 6)

SL.NO.

RISK CATEGORY MAXMSCORE

ELIGIBLESCORE

SCOREOBTAINED

RISKWEIGHT

(%)

RISKADJUSTED

SCOREX Y Z Y/X * Z

A. FINANCIAL RISK 42 40B. BUSINESS RISK 34 25C MANAGEMENT RISK 50 20D ACTIVITY RISK 24 15E TOTAL MARKS 150 100

TOTAL RISK ADJUSTED SCORE :-RATINGAWARDED

TOTAL RISK ADJUSTEDSCORE

GRADATION NATURE OF RISK

More than 90 1 Very LowMore than 80 & up to 90 2 LowMore than 70 & up to 80 3 Moderately LowMore than 60 & up to 70 4 FairMore than 55 & up to 60 5 ModerateMore than 50 & up to 55 6 HighMore than 45 & up to 50 7 Very High45 or below 8 Critical/Default

Comments of Level-1 Officer:-

Comments of Level -2 Officer:-

Comments of Level-3 Officer:-

CRG-7APPLICABLE FOR

RISK GRADING OF SSI/SME BORROWERS UNDER SSI/SME CATEGORY (EXISTINGACCOUNT) WITH CREDIT LIMIT ` 10 Lakh & Above

NameoftheBorrower:LineofActivity:Branch: Region:ScoringBasedonAuditedBalanceSheetAsAt:

ExistingFacility:Nature of Facility Sanctioned Limit Outstanding Overdue/ Other irregularities,

if anya. Term-LoanIIIb. WorkingCapitalIIIc. OthersIIITotal

ScoringUnderVariousRiskCategories:

(A) MANAGEMENT RISK:

S.No Parameters ScoreA.I Ownership pattern

Public/ Private Limited Company controlled by professional 5Other Public & Private Limited Company confined to familymembers

4

Partnership since last 3Years 3Other Partnership Company 2Proprietorship/ Society/Trustee 1Comment:-

A.II Experience of ManagementManagement is in the line of business for more than 5 years. 4Management is in the business for 2 - 5 Years. 3Management is new in the line of business but experiencedin other area.

2

Management is totally new entrant in the line business. 1Comment:-

A.III Qualification/ Experience MarksPromoter(s) technically qualified ( degree /diploma/ ITI ) insame line

5

Non technical Graduate / having experience in same line ofactivity for 3 yrs

3

Experience in same line of activity for 3 yrs 2

B.I Input Related RiskRaw Material is easily available at Steady price. 5Raw Material is available by tie-ups with suppliers but notlocally

4

Timely availability is critical, which causes to store the RawMaterial in advance

2

Availability extremely seasonal 1Comment:-

B.II Past performance of sales achievement (Accepted by Bank)or Growth rate ( lower of the achievement/ growth rate to betaken)

MARKS

Achievement is equal to 95 % or more / (Growth More than25%).

5

Achievement below 95% and up to 90% / (Growth Morethan 20%)

4

Other 0Comment:-

A.IV Payment Record(Other Institution)No NPA reported/ No default from any of the Bank/FIs/ RBIList/ CIBIL/Other Lists

3

Yes -3Comment:-

A.V Relationship With the Bank:Borrower/Group having satisfactory borrowing relationshipsince last 5Years

4

Borrower/Group having satisfactory borrowing relationshipsince last 3Years

3

Borrower/Group having satisfactory borrowing relationshipsince last 1Years

2

None of the Above 1Comment:-

A.VI Credibilitya. Sales is increasing consistently 2

Sales is not consistently growing in last 3 Years -1b. Borrower maintains financial disciplines, no serious audit

qualification.1

Borrower does not maintain financial discipline, serious auditqualification

-2

c. Market Reputation about commitments is favourable 2Market Reputation about commitments is adverse -2

d. For Product quality/development company receivedcertification i.e. Best exporter etc.

2

No thrust in R&D/quality, no product flexibility in system. 1Comment:-

TOTAL SCORE MANAGEMENT RISKB. BUSINESS RISK

Achievement below 90% and up to 80% / (Growth Morethan 18%)

3

Achievement below 80% and up to 70% / (Growth Morethan15%)

2

Achievement below 70% / (Growth of 15% or less) 1Comment:-

B.III Past performance of Profit achievement (Accepted by Bank)or Growth rate ( lower of the achievement/ growth rate to betaken)Achievement is equal to 95 % or more / (Growth Morethan 25%).

5

Achievement below 95% and up to 90% / (Growth Morethan 20%)

4

Achievement below 90% and up to 80% / (Growth Morethan 18%)

3

Achievement below 80% and up to 70% / (Growth Morethan15%)

2

Achievement below 70% / (Growth of 15% or less) 1Comment:-

B.IV MarketabilityMarket is broad based & diversified 5Market is diversified but not competitive 4Localised market but market share is good 3Confined to few customers 2Market is fragmented and highly competitive. 1Comment:-

TOTAL SCORE FOR BUSINESS RISK

C. FINANCIAL RISK:

C.I DSCR(Average) for tenure of the loan (applicable for Term Loan only)*Average DSCR is more than 2:1 5Average DSCR is from 2:1 to 1.75:1 4Average DSCR is up to 1.30:1 but below 1.75 :1 3Average DSCR is less than 1.30:1 1

Comment:-

C.II D/E RATIORatio Less than 2.00 5Ratio 2.00 to 3 4Ratio more than 3 to 4 3Ratio more than 4 1Comment:-

C.III Term of Repayment(Including Moratorium in Proposed expansion) FOR TL*Less than 5 Years 55 Years to less than 6 Years 4

6 Years to less than 7 Years 3

7 Years and more 1Comment:-

C.IV Promoters contribution (applicable for Term Loan only) MARKS33% or more of the total Project cost 525% or more but below 33% 420% or more but below 25% 3Below 20% 1Comment:-

C.V ROCE(PBIT/TNW +LTB+STB)Equal to 18% and above 5Below 18% but up to 15% 4Below 15% but up to 12% 3Below 12% but up to 8% 2Below 8% 1Comment:-

C.VI Current RatioRatio 1.33 & Above 5Ratio less than 1.33 & up to 1.25 4Ratio less than 1.25 & up to 1.17 3Ratio less than 1.17 1Comment:-

C.VII TOL/TNWRatio Less than 3.00 5Ratio 3.00 to 4 4Ratio more than 4 to 5 3Ratio more than 5 to 7.50 2Ratio more than 7.50 1Comment:-

C.VIII Net Profit Ratio (PAT/Net Sales%)5% and above 5Less than 5% & up to 3% 4Less than 3% & up to 1% 3Less than 1% 2Comment:-

TOTAL SCORE FINANCIAL RISK-EXISTING

D. INDUSTRY RISK:

D.I Customer & MarketA. Steady Market 3B. Average Market 2C. Unsteady & Seasonal Market 0

Comment:-

D.II Competition MARKSA. Near Monopoly 3B. Moderate 2C. Tough 0

Comment:-D.III Product Viability

A. Boom 3B. Normal demand 2C. Recession 0Comment:-

D.IV Small Industry is working in cluster basis(Same product)A. Cluster of same type of product 3B. Cluster of different type of product 2C. Single Unit 0Comment:-

D.V Government PoliciesA. Subsidy Available 3B. Other incentive like tax holidays, basic infrastructureavailable

2

C. Others 0Comment:-