Headline Verdana Bold - Deloitte US€¦ · • Manufacturing not to including Software...

49

Headline Verdana Bold India tax landscape update Committed to your success December 2019

Transcript of Headline Verdana Bold - Deloitte US€¦ · • Manufacturing not to including Software...

Headline Verdana BoldIndia tax landscape updateCommitted to your successDecember 2019

India tax landscape update© 2019 Deloitte & Touche LLP 2

1. Current India tax landscape 3

2. Tax ordinance 5

• Key amendments

• Key announcements

• Tax considerations

• Case studies

2. MLI impact and recent Permanent Establishment (PE) rulings 20

• MLI impact on tax treaties—Case studies

• Recent direct tax ruling on PE

3. Unified approach 37

Content

Headline Verdana Bold

Current India tax landscape

India tax landscape update© 2019 Deloitte & Touche LLP 4

01Changes in tax and regulatory framework

• New Direct Tax Code unlikely—Select suggestions of the tax

force to be incorporated in the current laws

• MLI ratified by India—Effective from 1 April 2020

• Synthesised text of tax treaty giving effect to MLI realised for

UAE, Serbia, Japan, Singapore …

• Sunset clause on exemptions—Talks of reintroducing sops

• Consultation paper on Unified approach for profit allocation

02Litigation trends

• PE, expense cross charge, transfer pricing emerging as latest

trends of litigation

• Tax authorities invoking GAAR during court proceedings for

restructuring approvals

• Income-tax audits not yet initiated for GAAR

03Increased disclosure norms

• SFT, FLA, DPT-3, ultimate beneficial owners—ITR, SBO

under company laws

Tax Administration

• Aggressive audits and interpretation of laws continue

• Co-ordinated approach and flow of information between

regulators

• On-ground implementation of various schemes lagging

• E-assessment scheme notified

05Dispute resolution

• Judiciary continues to be burdened with high volume of

cases

• Supreme Court saddled with other judicial matters—

Important tax rulings struck

• Special Bench of ITAT to decide on taxability of

reimbursement of salary

06

Regulatory reform to match emerging business trends

• Relaxation of ECB policy

• Law on unregulated deposits

• Changes in allied laws—Exchange control, Securities Law04

Current India tax landscape

Headline Verdana Bold

Tax ordinance

India tax landscape update© 2019 Deloitte & Touche LLP 6

Key amendments

India tax landscape update© 2019 Deloitte & Touche LLP 7

Key amendments

Tax ordinance

• No tax holiday /relief /incentives [additional deprecation, weighted deduction for R&D etc..] being claimed [exception

for IFSC, 80JJAA]

• Loss / unabsorbed depreciation attributable to the above are not carried forward

• Adjustment in the written down value of the block for unabsorbed depreciation

• MAT provisions not applicable

• Unutilized MAT to be forgone

• Option once exercised cannot be reversed

Scheme 1—

Lower headline rate of 22% plus surcharge and cess [25.17%] subject to

India tax landscape update© 2019 Deloitte & Touche LLP 8

Key amendments

Tax ordinance

• Commence manufacture prior to March 31, 2023

• Engaged only in manufacturing/production

• No tax holiday /relief /incentives [additional deprecation /R&D deductions etc..]

• New plant and machinery [20% threshold]

• Not formed by splitting up /reconstruction

• MAT provisions not applicable

• Option once exercised cannot be reversed

• Manufacturing not to including Software development, Mining, Conversion of marble blocks into slabs, bottling gas into

cylinder, printing books or production of cinematograph film or any other business as ma be notified by the central

government

• Non manufacturing income (neither derived nor incidental) shall be taxable at 22% without any deduction for expenses

where there is no specified rates

Scheme 2—

Lower headline rate of 15% plus surcharge and cess [17.16%] for new manufacturing companies set up post Oct 1, 2019 subject to:

India tax landscape update© 2019 Deloitte & Touche LLP 9

Key announcements

India tax landscape update© 2019 Deloitte & Touche LLP 10

Key announcements

Tax ordinance

• From FY 2019-20, MAT rate shall stand reduced 18.5% to 15% plus applicable surcharge and cess [17.47 at the

highest rate]

Change in MAT rate

• Enhanced surcharge not to apply on capital gains in respect of STT paid securities

• Enhanced surcharge not to apply to capital gains, in the hands of Foreign Portfolio Investors (FPIs)

• Relief from buyback tax has provided to listed companies that have made a public announcement of buy-back before 5

July 2019

Other changes

India tax landscape update© 2019 Deloitte & Touche LLP 11

Comparative table of tax rates

Tax ordinance

Particulars

Pre amendment scenario Post amendment scenarios

Branch LLP Company [Turnover >400 Cr for pre amendment]

30% 22% 15%

Taxable income 100.00 100.00 100.00 100.00 100.00

Less: Indian tax liability (A) 43.68 34.94 34.94 25.17 17.16

Profit after tax 56.32 65.06 65.06 74.83 82.84

Profit available for distribution 56.32 65.06 65.06 74.83 82.84

Less: DDT (B) 0.00 0.00 11.09 12.76 14.13

Distributed amount 56.32 65.06 53.96 62.07 68.71

Total tax outflow (A+B) 43.68 34.94 46.04 37.93 31.29

% increase in Cash Flow 8.11 14.75

India tax landscape update© 2019 Deloitte & Touche LLP 12

Comparative tax rates—Asia Pacific region

Tax ordinance

Revised tax rates puts India into competitive position as compared to its peers in Asia Pacific region

0

5

10

15

20

25

30

35

India tax landscape update© 2019 Deloitte & Touche LLP 13

Tax considerations

India tax landscape update© 2019 Deloitte & Touche LLP 14

Tax considerations

Tax ordinance

I. No carry forward & Set-off of MAT Credit

II. Brought forward loss on additional depreciation

• Generation of power

• Contract manufacturing/ Toll manufacturing

• Construction related activity

III. Companies qualifying for the lower rate of 15%

• Adjustment of unabsorbed depreciation to the written down value of the block

• Adjustment of brought forward loss /unabsorbed depreciation in respect of tax holiday entitled units under old and new regime

• Splitting up /reconstruction – disputes as in tax holiday provisions

• Will transfer of an entire undertaking lead to ‘splitting up/ reconstruction’

• Transfer of ‘capital work in progress’ to new company

IV. Splitting up or Reconstruction for Section 115BAB

India tax landscape update© 2019 Deloitte & Touche LLP 15

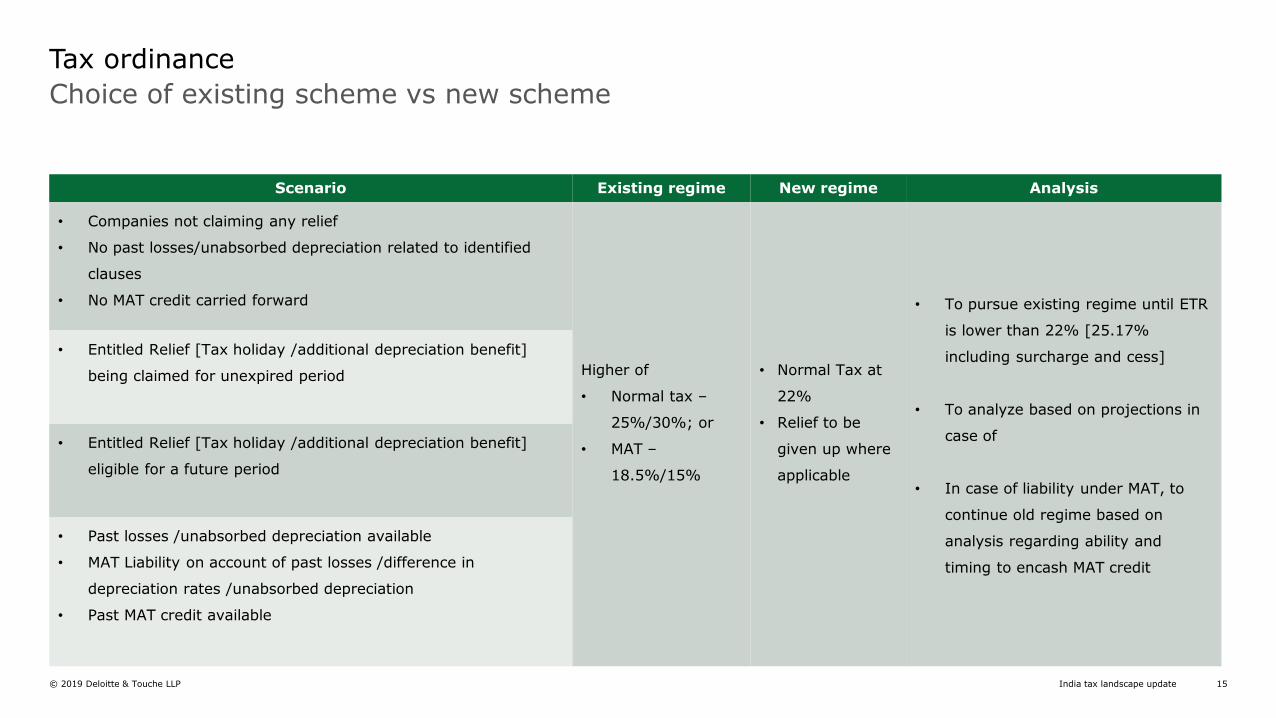

Choice of existing scheme vs new scheme

Tax ordinance

Scenario Existing regime New regime Analysis

• Companies not claiming any relief

• No past losses/unabsorbed depreciation related to identified

clauses

• No MAT credit carried forward

Higher of

• Normal tax –

25%/30%; or

• MAT –

18.5%/15%

• Normal Tax at

22%

• Relief to be

given up where

applicable

• To pursue existing regime until ETR

is lower than 22% [25.17%

including surcharge and cess]

• To analyze based on projections in

case of

• In case of liability under MAT, to

continue old regime based on

analysis regarding ability and

timing to encash MAT credit

• Entitled Relief [Tax holiday /additional depreciation benefit]

being claimed for unexpired period

• Entitled Relief [Tax holiday /additional depreciation benefit]

eligible for a future period

• Past losses /unabsorbed depreciation available

• MAT Liability on account of past losses /difference in

depreciation rates /unabsorbed depreciation

• Past MAT credit available

India tax landscape update© 2019 Deloitte & Touche LLP 16

Case studies

India tax landscape update© 2019 Deloitte & Touche LLP 17

Determination of preferred option

Case study 1

Year 1 profits - 100

Brought forward MAT credit - 100

MAT tax under old regime FY 2020-21 onwards -17.47%

Brought forward loss/Unabsorbed depreciation -200

MAT tax under old regime forFY 2019-20 -21.55%

Year on year growth in profit - 10%

Normal tax under old regime -34.94% Tax rate

under new regime -25.17%

Assumptions

India tax landscape update© 2019 Deloitte & Touche LLP 18

Taxation Laws (amendment) Bill, 2019—Changes in corporate tax rate

Analysis:

• In the red highlighted cells represent years under the current/old regime that are subject to MAT liability—portion of the liability is claimed as MAT credit• The blue highlighted cells represents years where the tax liability is after utilization of MAT credit

Determination of preferred option

Case study 1—Analysis

S/NoFinancial Year

Current/Old Regime New Regime

Profits Tax liability Cumulative tax impact (old regime)

Tax liability Cumulative tax impact (new regime)

Ideal scenarioCash tax outflow

1 2019-20 100 21.55 21.55 - - Old regime 21.55

2 2020-21 110 19.22 40.77 2.52 2.52 Old regime 19.22

3 2021-22 121 21.14 61.91 30.45 32.97 Old regime 21.14

4 2022-23 133 23.26 85.16 33.50 66.47 Old regime 23.26

5 2023-24 146 25.58 110.75 36.85 103.32 Old regime 25.58

6 2024-25 161 28.14 138.88 40.53 143.85 Old regime 28.14

7 2025-26 177 30.95 169.84 44.59 188.44 Old regime 30.95

8 2026-27 195 59.89 229.73 49.05 237.48 Old regime 59.89

9 2027-28 214 74.91 304.63 53.95 291.43 New regime 53.95

Total 304.63 291.43 283.68

India tax landscape update© 2019 Deloitte & Touche LLP 19

Determination of preferred option in a scenario which involves litigation exposure

Regime adopted in the Return of Income

Position post assessment proceedings

Litigation exposure

Case study 2

Financial Year RegimeTax liability under normal provisions

Tax liability under MAT

MAT credit Tax outflow

2017-18 Old regime 100 60 NIL 100

2018-19 Old regime 150 90 NIL 150

2019-20 New regime 125 Not applicable MAT credit lapse 125

TOTAL 375

Financial Year RegimeTax liability under normal provisions

Tax liability under MAT

MAT credit Tax outflowProbable tax outflow

2017-18 Old regime 100 60 NIL 100 100

2018-19 Old regime 150 300 150 300 300

2019-20 New regime 125 Not applicable MAT credit to lapse

125 86.77

TOTAL 525 486.77

Headline Verdana BoldMLI impact and recent Permanent Establishment (PE) ruling

India tax landscape update© 2019 Deloitte & Touche LLP 21

Overview

MLI impact and recent Permanent Establishment (PE) rulings

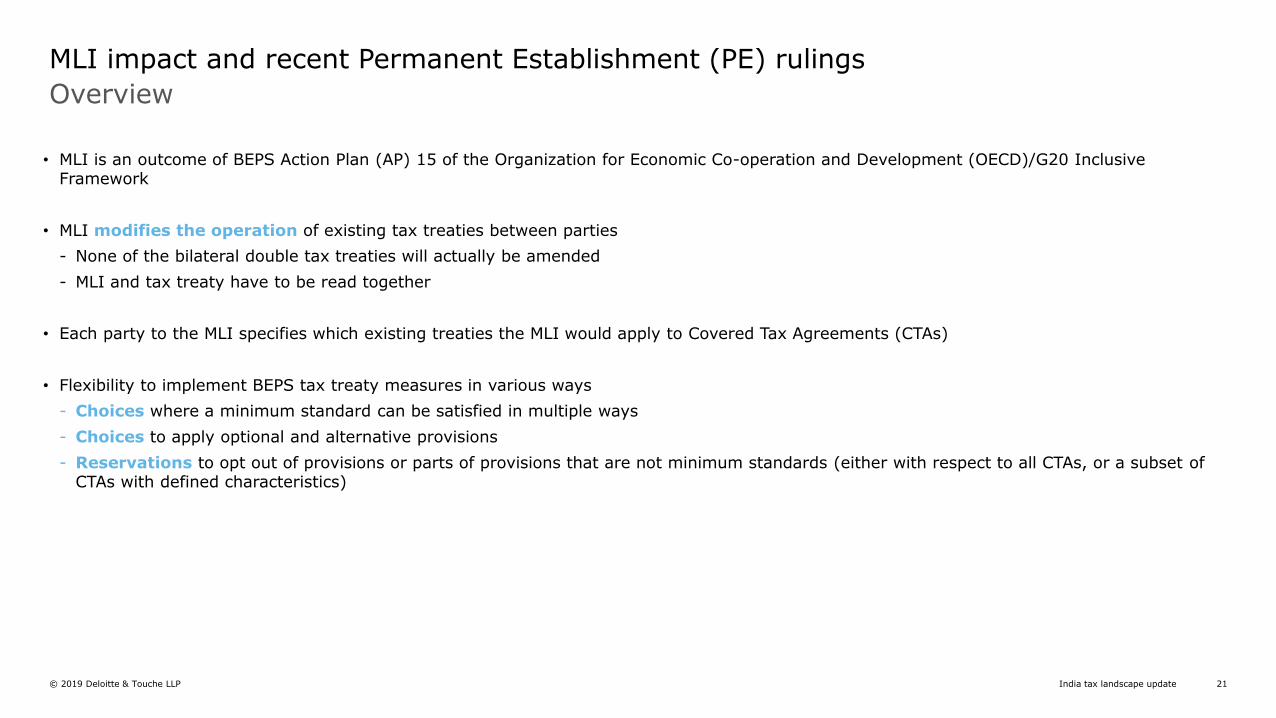

• MLI is an outcome of BEPS Action Plan (AP) 15 of the Organization for Economic Co-operation and Development (OECD)/G20 Inclusive Framework

• MLI modifies the operation of existing tax treaties between parties

- None of the bilateral double tax treaties will actually be amended

- MLI and tax treaty have to be read together

• Each party to the MLI specifies which existing treaties the MLI would apply to Covered Tax Agreements (CTAs)

• Flexibility to implement BEPS tax treaty measures in various ways

- Choices where a minimum standard can be satisfied in multiple ways

- Choices to apply optional and alternative provisions

- Reservations to opt out of provisions or parts of provisions that are not minimum standards (either with respect to all CTAs, or a subset of CTAs with defined characteristics)

India tax landscape update© 2019 Deloitte & Touche LLP 22

Broad architecture

MLI impact and recent Permanent Establishment (PE) rulings

39 Articles

Articles 1 and 2 Scope of MLI and the interpretation of terms used therein

1Articles 3 to 17—BEPS tax treaty measures

2

Articles 18 to 26 Provisions related to mandatory binding arbitration

3Articles 27-39—procedural provisions such as provisions relevant to adoption and implementation of the MLI including ratification, entry into force and entry into effect dates, withdrawal, etc.

4

India tax landscape update© 2019 Deloitte & Touche LLP 23

How MLI operates

MLI impact and recent Permanent Establishment (PE) rulings

Each party to the MLI must notify tax treaties to which the MLI provisions would apply. MLI provisions would apply to a tax treaty only if both parties to the tax treaty notify it as CTA.

For a specific bilateral tax treaty, MLI would have effect after both parties to a CTA have deposited their ratification instrumentswith the OECD Secretariat

MLI would modify application of all CTAs at least to the extent of implementation of following minimum standards viz:

• Counter treaty abuse (Article 6—Purpose of CTA and Article 7—Prevention of treaty abuse)

• Improve dispute resolution (Article 16—mutual agreement procedure)

Flexibility to implement BEPS tax treaty measures in various ways:

• Choices to apply optional and alternative provisions

• Reservations to opt out of provisions or parts of provisions that are not minimum standards (either for all CTAs, or a selectCTAs)

India tax landscape update© 2019 Deloitte & Touche LLP 24

The India story

MLI impact

*That is, on the first day of the month following the expiration of three months beginning on the date of deposit of ratification instrument by India with the OECD Secretariat

**That is, Indian tax treaties with jurisdictions that have already deposited their ratification instrument with the OECD Secretariat latest by 30 June 2019 and have notified tax treaty with India as CTA

24 Nov 2016Publication of MLI

7 Jun2017

Signing ceremony:68 jurisdictions including India signed MLI

25 Jun2019

Deposit of ratification instrument (along with final MLI positions) by India

13 Jun 2019Indian Government approved ratification of MLI

1 Oct2019*

MLI enters into force for India

MLI provisions to enter into effect for 23 Indian bilateral tax treaties**

1 Jul 2018MLI entered into force

1 Apr2020

India tax landscape update© 2019 Deloitte & Touche LLP 25

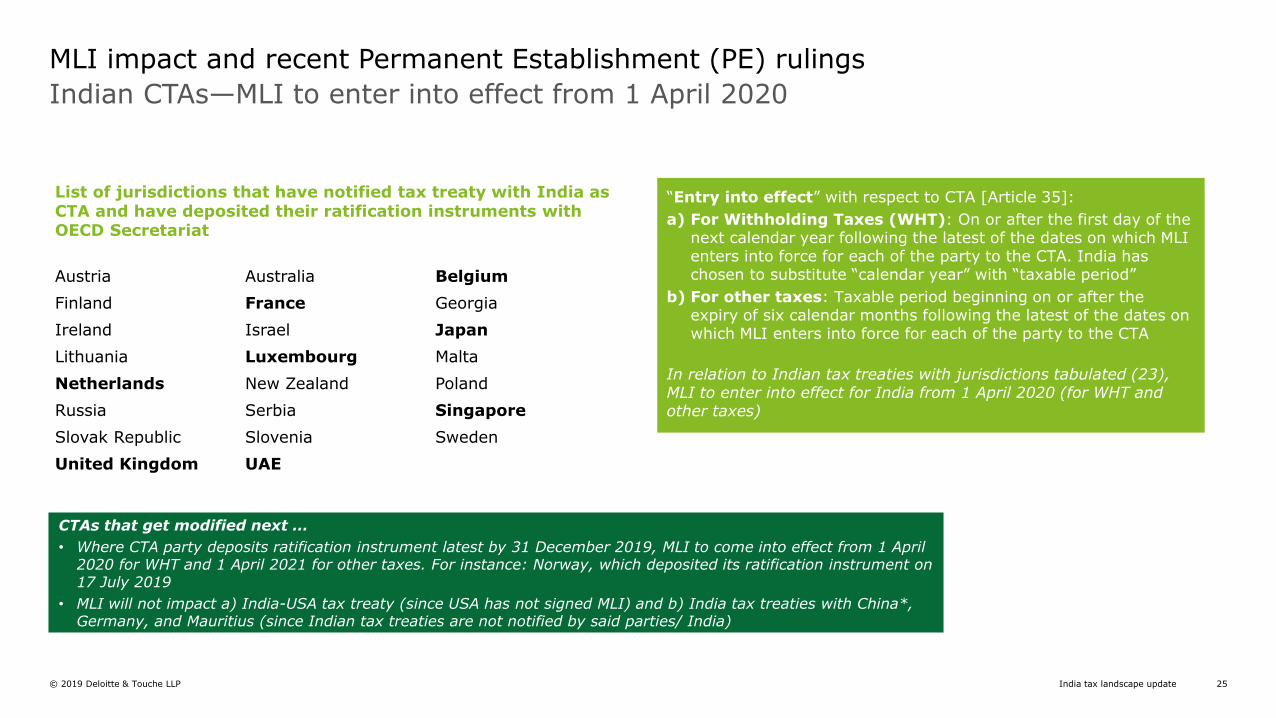

Indian CTAs—MLI to enter into effect from 1 April 2020

MLI impact and recent Permanent Establishment (PE) rulings

“Entry into effect” with respect to CTA [Article 35]:

a) For Withholding Taxes (WHT): On or after the first day of the next calendar year following the latest of the dates on which MLI enters into force for each of the party to the CTA. India has chosen to substitute “calendar year” with “taxable period”

b) For other taxes: Taxable period beginning on or after the expiry of six calendar months following the latest of the dates on which MLI enters into force for each of the party to the CTA

In relation to Indian tax treaties with jurisdictions tabulated (23), MLI to enter into effect for India from 1 April 2020 (for WHT and other taxes)

List of jurisdictions that have notified tax treaty with India as CTA and have deposited their ratification instruments with OECD Secretariat

Austria Australia Belgium

Finland France Georgia

Ireland Israel Japan

Lithuania Luxembourg Malta

Netherlands New Zealand Poland

Russia Serbia Singapore

Slovak Republic Slovenia Sweden

United Kingdom UAE

CTAs that get modified next …

• Where CTA party deposits ratification instrument latest by 31 December 2019, MLI to come into effect from 1 April 2020 for WHT and 1 April 2021 for other taxes. For instance: Norway, which deposited its ratification instrument on 17 July 2019

• MLI will not impact a) India-USA tax treaty (since USA has not signed MLI) and b) India tax treaties with China*, Germany, and Mauritius (since Indian tax treaties are not notified by said parties/ India)

India tax landscape update© 2019 Deloitte & Touche LLP 26

MLI impact on tax treaties—Case studies

India tax landscape update© 2019 Deloitte & Touche LLP 27

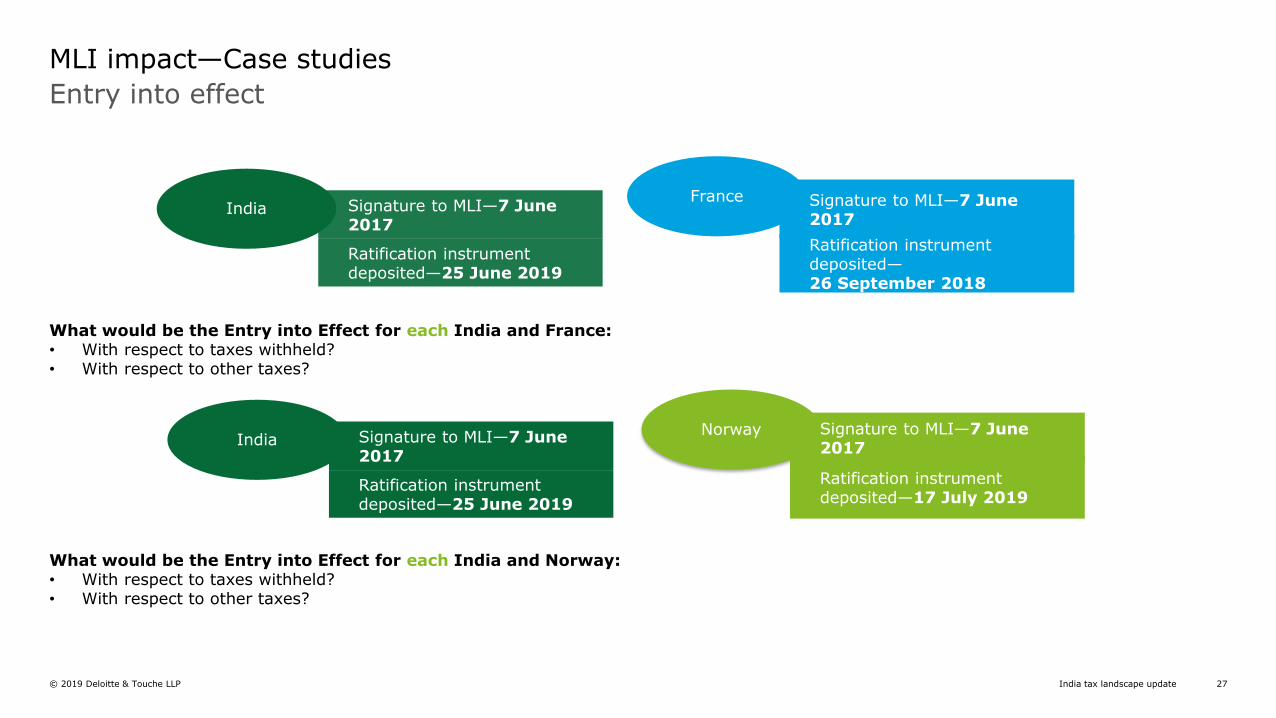

Norway

Entry into effect

MLI impact—Case studies

What would be the Entry into Effect for each India and France:• With respect to taxes withheld?• With respect to other taxes?

What would be the Entry into Effect for each India and Norway:• With respect to taxes withheld?• With respect to other taxes?

Signature to MLI—7 June 2017

Ratification instrument deposited—25 June 2019

IndiaSignature to MLI—7 June 2017

Ratification instrument deposited—26 September 2018

France

Signature to MLI—7 June 2017

Ratification instrument deposited—17 July 2019

Signature to MLI—7 June 2017

Ratification instrument deposited—25 June 2019

India

India tax landscape update© 2019 Deloitte & Touche LLP 28

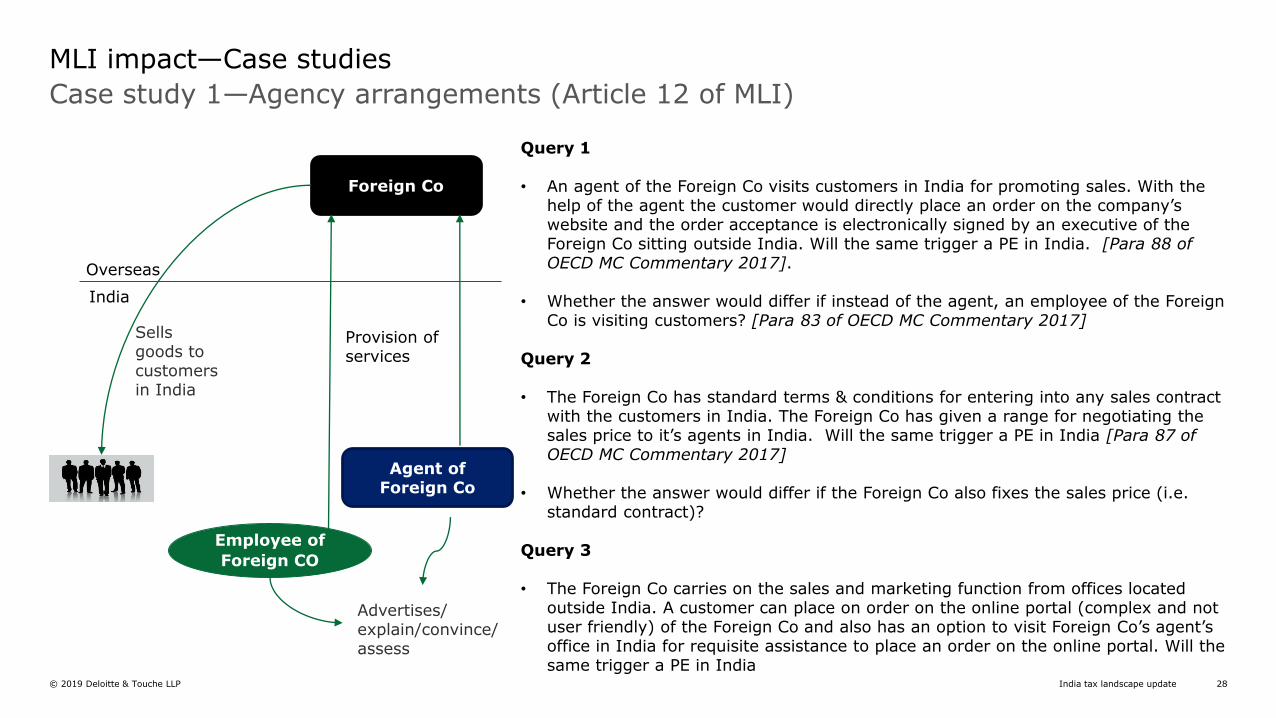

Foreign Co

Agent of Foreign Co

Overseas

India

Provision of services

Sells goods to customers in India

Employee of

Foreign CO

Advertises/ explain/convince/assess

Case study 1—Agency arrangements (Article 12 of MLI)

MLI impact—Case studies

Query 1

• An agent of the Foreign Co visits customers in India for promoting sales. With the help of the agent the customer would directly place an order on the company’s website and the order acceptance is electronically signed by an executive of the Foreign Co sitting outside India. Will the same trigger a PE in India. [Para 88 of OECD MC Commentary 2017].

• Whether the answer would differ if instead of the agent, an employee of the Foreign Co is visiting customers? [Para 83 of OECD MC Commentary 2017]

Query 2

• The Foreign Co has standard terms & conditions for entering into any sales contract with the customers in India. The Foreign Co has given a range for negotiating the sales price to it’s agents in India. Will the same trigger a PE in India [Para 87 of OECD MC Commentary 2017]

• Whether the answer would differ if the Foreign Co also fixes the sales price (i.e. standard contract)?

Query 3

• The Foreign Co carries on the sales and marketing function from offices located outside India. A customer can place on order on the online portal (complex and not user friendly) of the Foreign Co and also has an option to visit Foreign Co’s agent’s office in India for requisite assistance to place an order on the online portal. Will the same trigger a PE in India

India tax landscape update© 2019 Deloitte & Touche LLP 29

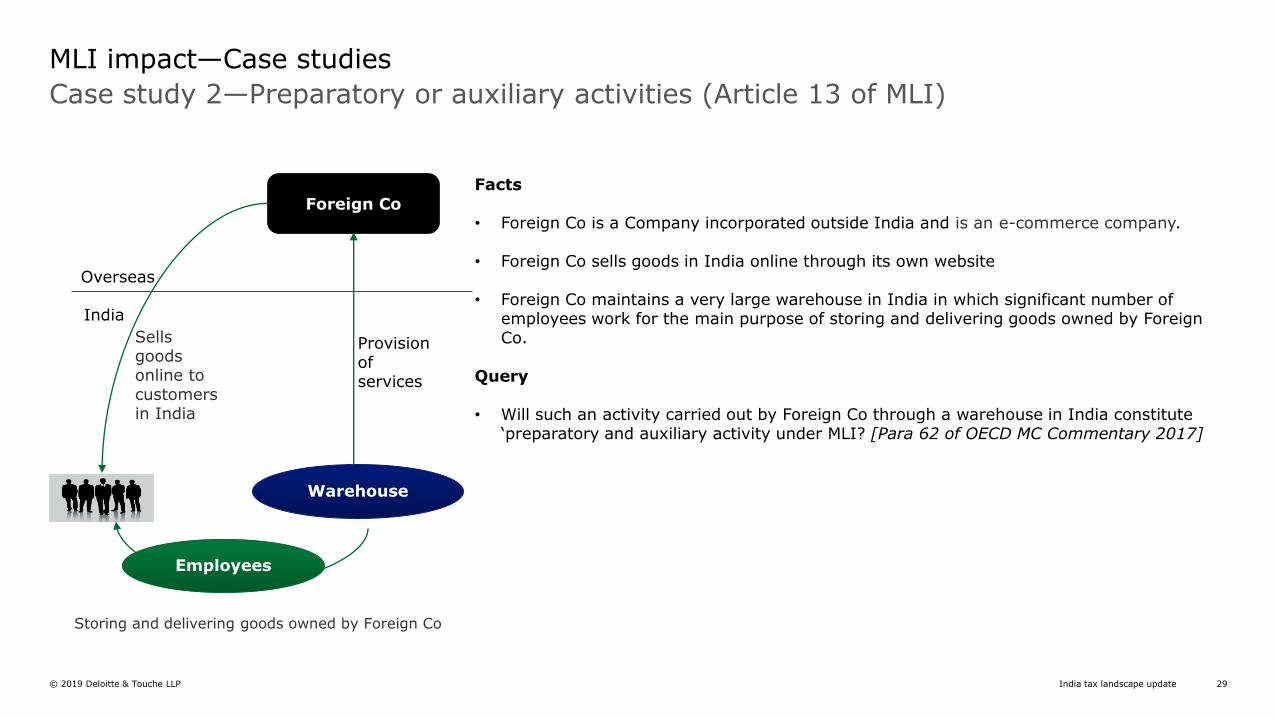

Case study 2—Preparatory or auxiliary activities (Article 13 of MLI)

MLI impact—Case studies

Facts

• Foreign Co is a Company incorporated outside India and is an e-commerce company.

• Foreign Co sells goods in India online through its own website

• Foreign Co maintains a very large warehouse in India in which significant number of employees work for the main purpose of storing and delivering goods owned by Foreign Co.

Query

• Will such an activity carried out by Foreign Co through a warehouse in India constitute ‘preparatory and auxiliary activity under MLI? [Para 62 of OECD MC Commentary 2017]

Foreign Co

Overseas

India

Provision of services

Sells goods online to customers in India

Storing and delivering goods owned by Foreign Co

Employees

Warehouse

India tax landscape update© 2019 Deloitte & Touche LLP 30

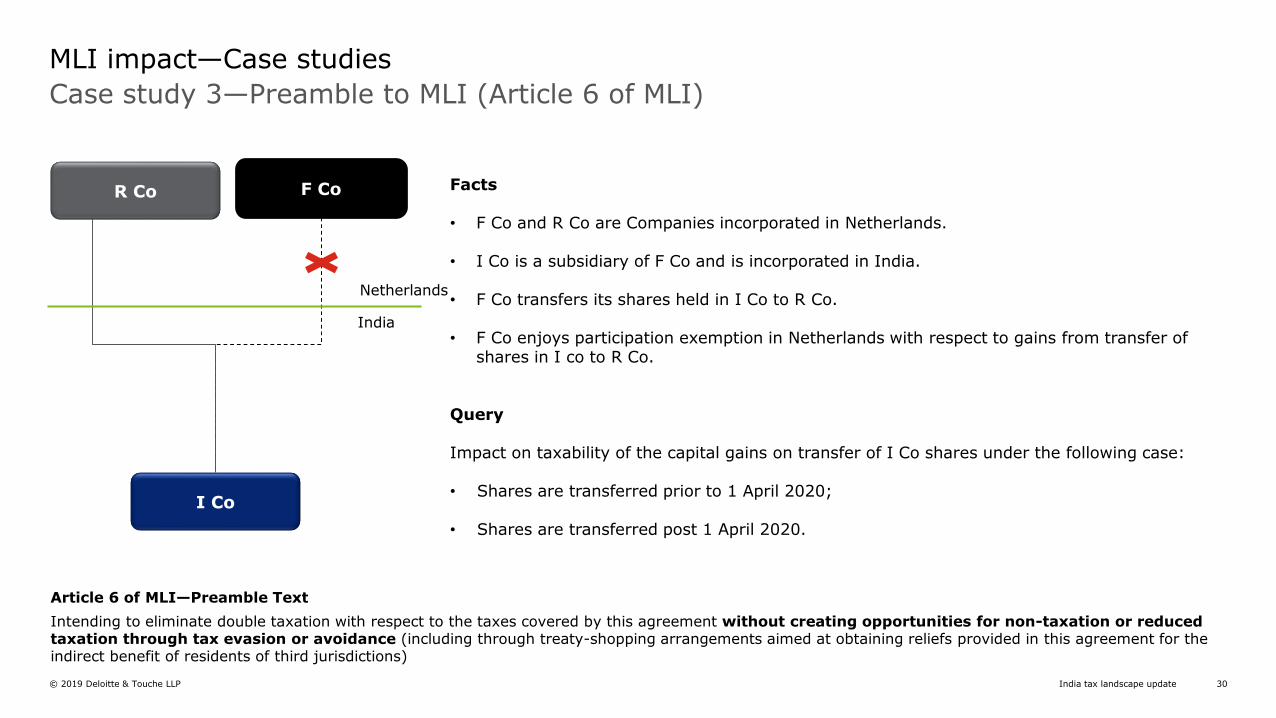

Case study 3—Preamble to MLI (Article 6 of MLI)

MLI impact—Case studies

Facts

• F Co and R Co are Companies incorporated in Netherlands.

• I Co is a subsidiary of F Co and is incorporated in India.

• F Co transfers its shares held in I Co to R Co.

• F Co enjoys participation exemption in Netherlands with respect to gains from transfer of shares in I co to R Co.

Query

Impact on taxability of the capital gains on transfer of I Co shares under the following case:

• Shares are transferred prior to 1 April 2020;

• Shares are transferred post 1 April 2020.

F Co

Netherlands

India

I Co

R Co

Article 6 of MLI—Preamble Text

Intending to eliminate double taxation with respect to the taxes covered by this agreement without creating opportunities for non-taxation or reduced taxation through tax evasion or avoidance (including through treaty-shopping arrangements aimed at obtaining reliefs provided in this agreement for the indirect benefit of residents of third jurisdictions)

India tax landscape update© 2019 Deloitte & Touche LLP 31

Case study 4—Principal Purpose Test vs General Anti Avoidance Rules

MLI impact—Case studies

Facts

• Foreign Co is a Company incorporated outside India.

• Indian Co is a subsidiary of Foreign Co and is incorporated in India.

Assumptions

• Assumption 1—The investment is before 31 March 2017

• Assumption 2—The investment is after 31 March 2017

Queries

• Analysis under the following scenarios:

― Is the scope of PPT wider than GAAR—‘one of the main purpose’ test vs ‘main purpose’ test

― Applicability of GAAR and/or PPT on transfer of investments acquired post 1 April 2017

― Applicability of GAAR and/or PPT on transfer of investments acquired prior to 31 March 2017—Impact of the CBDT circular grandfathering pre 31 March 2017 investment

Foreign Co

Indian Co

Overseas

India

Subsidiary

s

India tax landscape update© 2019 Deloitte & Touche LLP 32

Recent direct tax ruling on PE

India tax landscape update© 2019 Deloitte & Touche LLP 33

Liaison Office carrying on activity other than preparatory and auxiliary services constitutes PE in India per DTAA between India and Singapore

Recent direct tax ruling on PE

1. Background and Facts

• The taxpayer, a wholly owned subsidiary of a Japanese Company—a Liaison Office (LO) in India since April 1988 for carrying market research and liaison activities.

• The LO had offices in Delhi, Bangalore and Mumbai.

• In July 2007, the offices in Bangalore and Mumbai were closed and the LO was converted into a branch office in India.

• Under an income-tax survey, the Assessing Officer (AO) alleged that the LO was engaged in executing/negotiating contracts for the taxpayer in India

• The AO concluded proceedings and computed the total income of the taxpayer in the hands of the PE (i.e. LO) applying the Global Profit Margin of the taxpayer, to the sales revenue made by the taxpayer in India and attributed 50 percent thereof to the PE in India aggregating to INR 7.21 crores for all these years.

• In the first round of litigation before Income Tax Appellate Tribunal (ITAT), the matter was remanded back to Dispute Resolution Panel (DRP) for passing a speaking order

• In the re-adjudication proceedings, the final assessment order was passed by the AO assessing the aggregate total income at INR 123.16 crores for all the years, by applying 16.5 percent as sale commission for the total sales value made to India, less the expenses.

TaxpayerSingapore

Overseas

IndiaMarket research and liaison activities

Employees

LO

India tax landscape update© 2019 Deloitte & Touche LLP 34

Liaison Office carrying on activity other than preparatory and auxiliary services constitutes PE in India per DTAA between India and Singapore

Recent direct tax ruling on PE

2. Issue under consideration before the ITAT

• Had the DRP exceeded the directions of the ITAT?

• Whether there was a PE of the taxpayer in India?

• If there was a PE of the taxpayer, what was the profit amount that could be attributed to the PE?

3. Decision of the ITAT

Issue 1

• The ITAT held that “in all fairness, the entire proceedings should now be restricted to adjudication upon the assessed income for all the fiveyears under consideration to the extent of INR 7.21 crores.”

India tax landscape update© 2019 Deloitte & Touche LLP 35

Liaison Office carrying on activity other than preparatory and auxiliary services constitutes PE in India per DTAA between India and Singapore

Recent direct tax ruling on PE

3. Decision of the ITAT (cont.)

Issue 2

• Based on documentary evidence during search/survey proceedings and key employee statements and email exchanges with tax consultant, that:

− At least six employees were working in LO.− The employees were actively involved in ascertaining customer requirements, price negotiation, obtaining of purchase orders, following

up on delivery of material and payments, etc.− There was clear relation between the business of the taxpayer and the activities in India, as business of the taxpayer was trading and

activities of the LO are core activities for a trading business.− As per communication with a tax consultant of taxpayer, it was clear that he was advising the taxpayer on the probable tax litigation

which may arise after survey operations, owing to substantial commercial activities carried out by LO.

• “As per India-Singapore DTAA, unless fixed place of business [LO in the case of the taxpayer] was being used only for the purpose of advertisement, for supply of information, for scientific research or for similar activities which have preparatory or auxiliary character, it could not have been excluded from the definition of PE” unlike DTAA with India-USA/Canada. Accordingly, the taxpayer was held to have a PE in India.

India tax landscape update© 2019 Deloitte & Touche LLP 36

Liaison Office carrying on activity other than preparatory and auxiliary services constitutes PE in India per DTAA between India and Singapore

Recent direct tax ruling on PE

3. Decision of the ITAT (cont.)

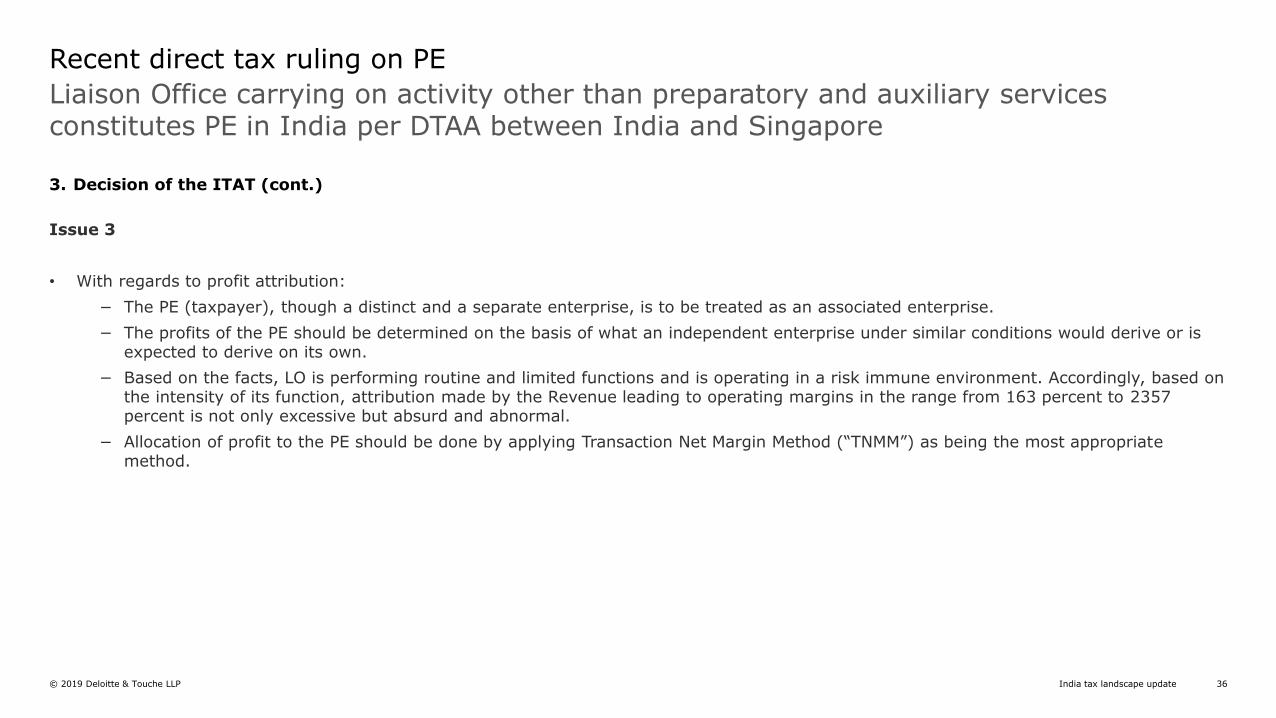

Issue 3

• With regards to profit attribution:

− The PE (taxpayer), though a distinct and a separate enterprise, is to be treated as an associated enterprise.

− The profits of the PE should be determined on the basis of what an independent enterprise under similar conditions would derive or is expected to derive on its own.

− Based on the facts, LO is performing routine and limited functions and is operating in a risk immune environment. Accordingly, based on the intensity of its function, attribution made by the Revenue leading to operating margins in the range from 163 percent to 2357 percent is not only excessive but absurd and abnormal.

− Allocation of profit to the PE should be done by applying Transaction Net Margin Method (“TNMM”) as being the most appropriate method.

Headline Verdana Bold

Unified approach

India tax landscape update© 2019 Deloitte & Touche LLP 38

G20/OECD: Tax challenges of the digitalized economy—Work to date

Unified Approach

• BEPS action 1: 2015 final report—October 2015

• 2018 OECD interim report—March 2018

• OECD policy note—January 2019

– Sets out the two pillar approach

• Public consultation document—February 2019

– Comments sought on policy issues and technical aspects

– Followed by public consultation meeting—March 2019

• Programme of work—May 2019

– Roadmap towards agreeing consensus solution by the end of 2020

• OECD secretariat proposal—9 October 2019

– Unified approach: nexus and profit allocation rules

• OECD secretary general report to G20

India tax landscape update© 2019 Deloitte & Touche LLP 39

New nexus and profit allocation rules

Unified Approach

OECD secretary-general report to G20 Finance Ministers—October 2019

“…it is essential to move forward now

to construct the architecture of a

global long-term solution through

the G20/OECD Inclusive Framework”

“…the current rules do not fit

the growing challenges of

the digitalization of the

economy…”

“…providing more certainty and

stability in the international tax system

for all countries and jurisdictions in the

world”

“…a proposal aimed at facilitating

consensus on common rules on

nexus and profit allocation…”

India tax landscape update© 2019 Deloitte & Touche LLP 40

New nexus and profit allocation rules

Unified Approach

The unified approach proposal draws on the commonalities identified in the May programme of work

Reallocating taxing rights in favour of the user/market country

Searching for simplicity, stabilisation of the tax system, and increased tax certainty in implementation

Going beyond the arm’s length principle and departing from the separate entity principle

The proposal does not, at this stage, have consensus political support from the G20/OECD inclusive framework on BEPS

Envisaging a new nexus rule not dependent on physical presence in the user/market country

India tax landscape update© 2019 Deloitte & Touche LLP 41

New nexus and profit allocation rules

Unified Approach

Key features of OECD secretariat’s proposed unified approach

• Scope of new taxing right

– Large consumer-facing businesses

• New nexus rules

– Not dependent on physical presence

• New profit allocation rules

– Calculated using a three-tier mechanism

• Robust dispute prevention and resolution

– Including binding arbitration

India tax landscape update© 2019 Deloitte & Touche LLP 42

New nexus and profit allocation rules

Unified Approach

Scope

Possible exclusionsPossible revenue threshold?

“Businesses that generate revenue from supplying consumer products or providing digital services that have a consumer-facing element.”

Approach covers highly digital business models but goes wider...

...broadly focussing on consumer-facing businesses

Extractives commodities financial services

€750 million revenue

India tax landscape update© 2019 Deloitte & Touche LLP 43

New nexus and profit allocation rules

Unified Approach

New nexus in a market country

Largely based on sales

Self-standing treaty provision in addition

to existing permanent establishment and

business profit articles

Applicable where a business has sustained

and significant involvement in the

economy of a market country...

1

6

Captures all forms of remote

involvement in the economy of a market

country e.g., remote selling, and groups

that sell in a market through a distributor

Possible country-specific sales

thresholds for smaller economies

3

...irrespective of level of physical presence

in the country

2

4

5

India tax landscape update© 2019 Deloitte & Touche LLP 44

New nexus and profit allocation rules

Unified Approach

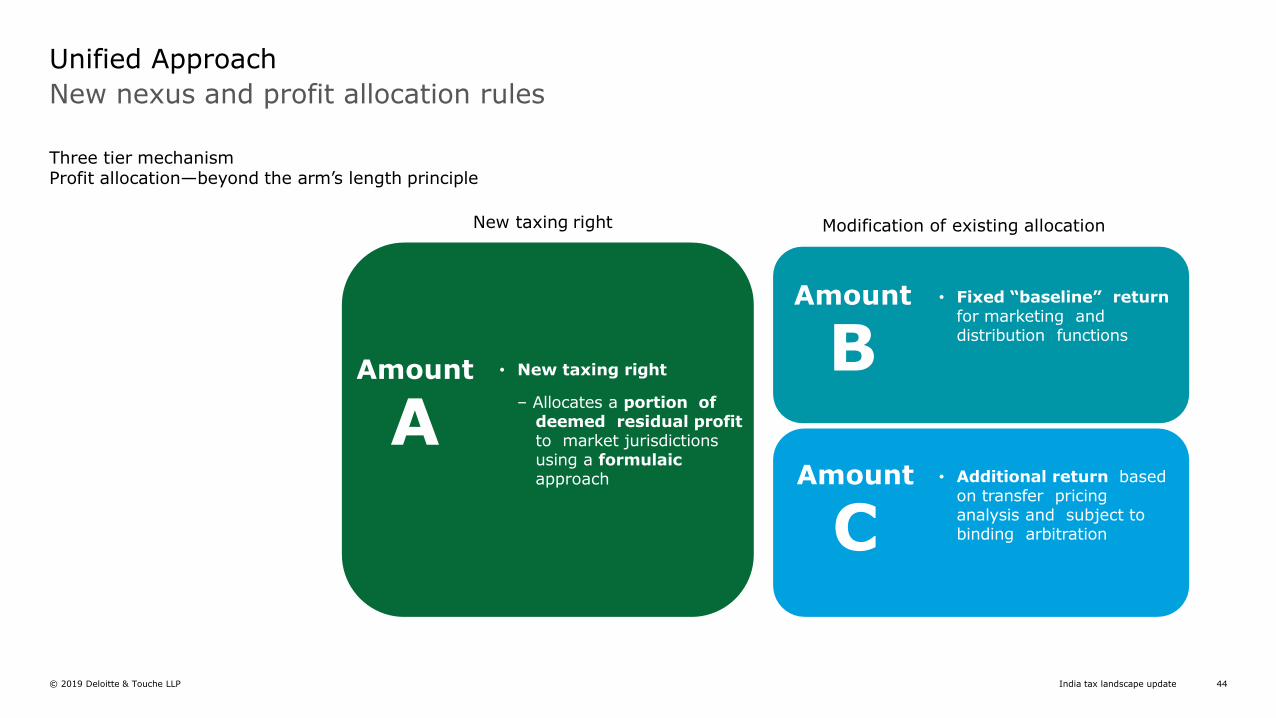

Three tier mechanismProfit allocation—beyond the arm’s length principle

Amount

B

Amount

C

• Fixed “baseline” return for marketing and distribution functions

• Additional return based on transfer pricing analysis and subject to binding arbitration

New taxing right Modification of existing allocation

• New taxing right

– Allocates a portion of deemed residual profit to market jurisdictions using a formulaic approach

Amount

A

India tax landscape update© 2019 Deloitte & Touche LLP 45

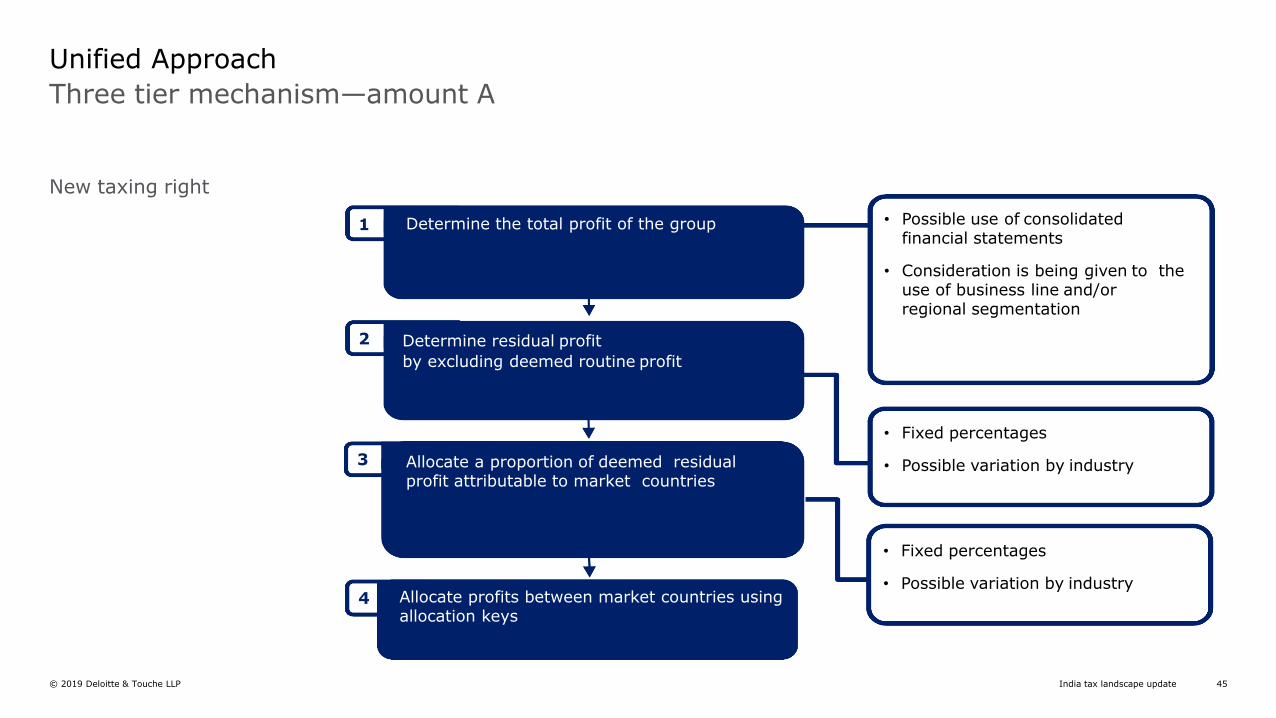

Three tier mechanism—amount A

Unified Approach

New taxing right

4

1

2

3

• Possible use of consolidated financial statements

• Consideration is being given to the use of business line and/or regional segmentation

• Fixed percentages

• Possible variation by industry

• Fixed percentages

• Possible variation by industry

Determine the total profit of the group

Determine residual profit

by excluding deemed routine profit

Allocate a proportion of deemedresidual profit attributable to market

countries

Allocate a proportion of deemed residual profit attributable to market countries

Allocate profits between market countries using allocation keys

India tax landscape update© 2019 Deloitte & Touche LLP 46

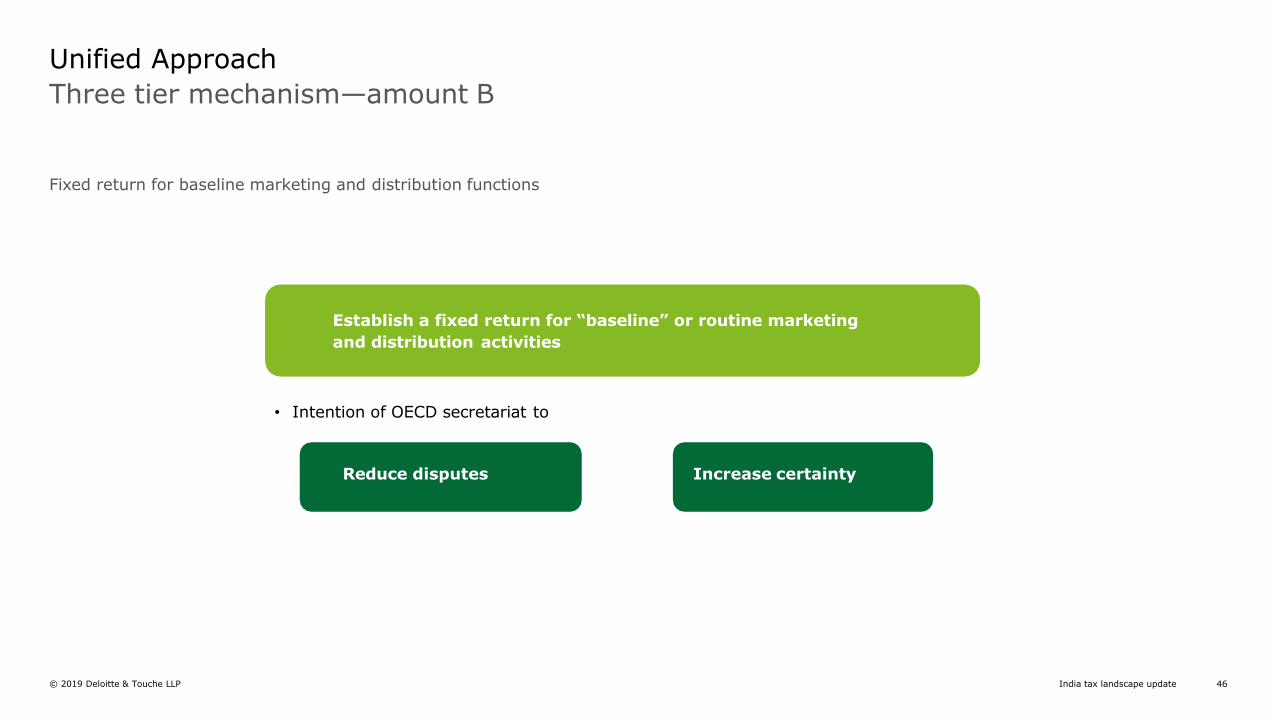

Three tier mechanism—amount B

Unified Approach

Fixed return for baseline marketing and distribution functions

• Intention of OECD secretariat to

Establish a fixed return for “baseline” or routine marketing

and distribution activities

Reduce disputes Increase certainty

India tax landscape update© 2019 Deloitte & Touche LLP 47

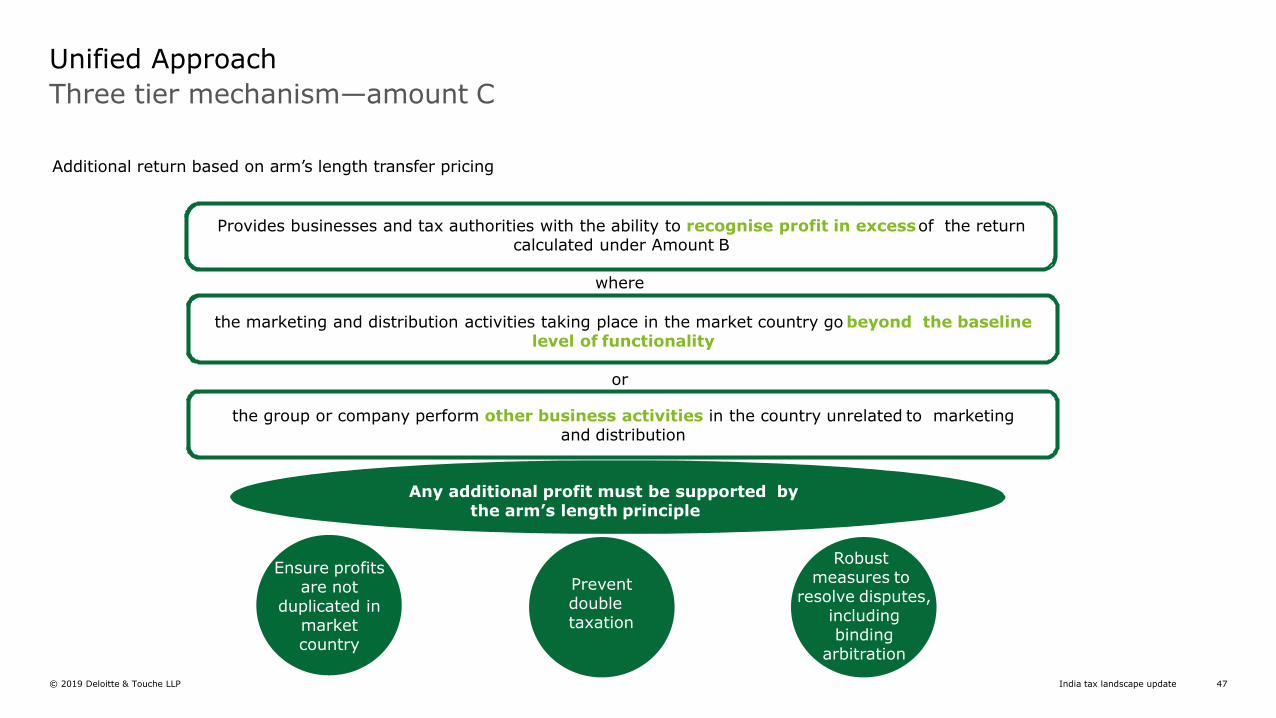

Three tier mechanism—amount C

Unified Approach

Additional return based on arm’s length transfer pricing

Ensure profits are not

duplicated in market country

Preventdoubletaxation

Robust measures to

resolve disputes, including binding

arbitration

Provides businesses and tax authorities with the ability to recognise profit in excessof the return calculated under Amount B

where

the marketing and distribution activities taking place in the market country go beyond the baseline level of functionality

or

the group or company perform other business activities in the country unrelated to marketing and distribution

Any additional profit must be supported by the arm’s length principle

India tax landscape update© 2019 Deloitte & Touche LLP 48

Impact assessments—preliminary findings

Unified Approach

OECD secretary-general’s report to G20 finance ministers

Final outcomes “will depend on the reform design and the behavioural

responses of countries and multinational enterprises”

“Low and middle-

income

economies would gain from

pillar 1”

“Larger market jurisdictions

will benefit more in absolute”

“Pillar 1 involves a significant change to the

way taxing rights are allocated among

jurisdictions but it would also lead to a modest

increase in tax revenues”

“Investment hubs, where the analysis suggests that

levels of residual profit are high, would experience

significant losses in tax base”

Deloitte refers to one or more of Deloitte Touche Tohmatsu Limited (“DTTL”), its global network of member firms, and their related entities. DTTL (also referred to as “Deloitte Global”) and each of its member firms and their affiliated entities are legally separate and independent entities. DTTL does not provide services to clients. Please see www.deloitte.com/about to learn more.

Deloitte is a leading global provider of audit and assurance, consulting, financial advisory, risk advisory, tax & legal and related services. Our global network of member firms and related entities in more than 150 countries and territories (collectively, the “Deloitte organisation”) serves four out of five Fortune Global 500® companies. Learn how Deloitte’s approximately 312,000 people make an impact that matters at www.deloitte.com.

Deloitte Asia Pacific Limited is a company limited by guarantee and a member firm of DTTL. Members of Deloitte Asia Pacific Limited and their related entities, each of which are separate and independent legal entities, provide services from more than 100 cities across the region, including Auckland, Bangkok, Beijing, Hanoi, Ho Chi Minh City, Hong Kong, Jakarta, Kuala Lumpur, Manila, Melbourne, Osaka, Shanghai, Singapore, Sydney, Taipei, Tokyo and Yangon.

About Deloitte SingaporeIn Singapore, services are provided by Deloitte & Touche LLP and its subsidiaries and affiliates.

Deloitte & Touche LLP (Unique entity number: T08LL0721A) is an accounting limited liability partnership registered in Singapore under the Limited Liability Partnerships Act (Chapter 163A).

This communication contains general information only, and none of Deloitte Touche Tohmatsu Limited, its member firms, or their related entities (collectively, the “Deloitte Network”) is, by means of this communication, rendering professional advice or services. Before making any decision or taking any action that may affect your finances or your business, you should consult a qualified professional adviser. No entity in the Deloitte Network shall be responsible for any loss whatsoever sustained by any person who relies on this communication.

© 2019 Deloitte & Touche LLP