Harte Gold Corp. - axino.de filePage 1 of 15 Ryan Walker, MSc | 416.479.8997 |...

15

Page 1 of 15 Ryan Walker, MSc | 416.479.8997 | [email protected] 8 July 2019 Precious Metals Event: We recently visited Harte Gold Corp.’s 100%-owned Sugar Zone mine in White River, Ontario, and came away struck by the ease of access and compact nature of the mine, the ease of ore vein visual identification, the simplicity of processing, and the compelling near-mine and regional exploration potential at Ontario’s newest gold producer. Commercial Production Declared on January 1: During Q119, the mine produced 32,044t (10% below plan) owing to labour, equipment, and weather-related issues. The mill performed 8% above plan, processing 38,278t (425tpd) at 4.86g/t Au, with feed supplemented by low-grade stockpile. Recovery averaged 92%, in line with plan, to yield 5,476oz of gold, 9% below plan. In the mill, recovery via the gravity circuit was 38%, with subsequent flotation recovering another 53%. HRT notes that gravity recovery is expected to increase with higher grade ore — the April 2019 Feasibility Study (FS) envisages 61%. Operating costs were 16% higher than expected (mining +20%, G&A +26%, processing in line). As such, AISC came in at ~$2,750/oz. HRT recently reported April and May production of 5,438oz, with final June results yet unavailable. Importantly, mill has stabilized and demonstrated the ability to run at 800tpd at planned recoveries. May and June mill feed continued to be supplemented with stockpile material as underground ramp-up continues. Production is currently sourced from Sugar Zone south sill development and stoping, with Sugar Zone north limb development ongoing. Stoping there is expected by September. Thereafter, HRT expects the mill to be solely fed run-of-mine production by Q419. HRT maintains 2019 guidance of 39,200oz at AISC of US$1,300-1,350/oz. Looking Ahead: In 2020, HRT expects to produce 65,078oz on higher throughput (800tpd) and grade (6.98g/t vs. the 6.18g/t average expected during 2019), with lower AISC of US$913/oz. The FS envisages base-case LOM average production of 61,000oz at AISC of US$845/oz over 14 years. The study also considered an expansion to 1,200tpd from 800tpd (at estimated capex of $20-25M), which would see production rise to 95,000oz/yr (2022 onwards), offering potential for lower cash costs with reportedly ~40% of mining costs fixed. HRT expects permits for such expansion by the end of 2020. HRT also notes that conversion of existing Inferred Resources could potentially support an expansion to 1,400tpd for ~120,000oz of annual production at a modest additional capex of ~$26M. Substantial Exploration Potential: Near-Mine. HRT is ramping up 2019 drilling, targeting near- mine areas, with a focus on the Sugar Zone southern extension, and convergence at depth of the Sugar-Middle zones (highlighted by 10.5g/t Au over 3.2m, 12.14g/t over 2.0m, 4.42g/t over 1.96m, and 3.66g/t over 1.9m), and Middle-Wolf zones (10.27g/t over 1.58m, 12.95g/t over 3.9m, 13.39g/t over 3.57m, and 12.14g/t over 2.0m) (Exhibit 3). More recent drilling along strike to the south of Sugar Zone returned 27.6g/t over 1.68m, 21.07g/t Au over 1.68m, including 115g/t over 0.34m, 8.62g/t over 1.90m, and 3.92g/t over 3.31m, including 0.39m at 26.5g/t (Exhibit 4). While early days, such relatively shallow mineralization proximal to planned development has the potential to have a greater nearer-term impact on the mine plan than the compelling potential extensions and coalescence of existing zones at greater depths. Step- out drilling continues along strike and down-dip of the new zone. HRT also plans regional exploration elsewhere on the 838.5km 2 land package, which covers a significant Greenstone Belt. High-priority targets include the Hambleton Lake and K7 areas defined by geophysics, prospecting, and limited previous drilling (Exhibit 2). Harte Gold Corp. Ontario’s Newest Gold Producer Casts an Eye to the Future via Near-Mine and Regional Exploration HRT-TSX: $0.25 Not Rated N/A Target Source: FactSet Market Data C$ Market Capitalization ($M) 148.1 Net Debt ($M) 94.7 Cash & Equivalents ($M) - Mar. 31/19 0.7 Debt ($M) 95.4 Enterprise Value ($M) 242.8 Basic Shares O/S (M) 604.5 Fully Diluted Shares O/S (M) 675.1 Avg. Weekly Volume (M) 2.67 52-Week Range $0.21 - $0.55 Sugar Zone Mine NI 43-101 Inferred Category Zone Tonnes Au Au M g/t Moz Probable Sugar 2.44 7.4 0.58 Wolf 2.95 6.6 0.31 Indicated Sugar 2.55 8.6 0.71 Wolf 1.70 7.3 0.40 Top Shareholders Holder Shares (M) % S/O Institutional US Global Investors, Inc. (Asset Mana 1.50 0.25% Insiders/Stakeholders Appian Capital Advisory Llp 176.1 29.14% Orion Mine Finance 41.1 6.80% Stephen Roman 30.4 5.03% Michael Cowie 4.5 0.74% Norman Campbell 1.8 0.29% Risks Operational Risk Exploration Results - 2019 Commodity Risk Production Ramp-up - 2019 Company Description Events/Catalysts Harte Gold is Ontario’s newest gold producer via its 100%-owned Sugar Zone Mine in White River, ON. At a 3g/t Au COG, NI 43-101-compliant Indicated Resources total 4.24M tonnes grading 8.12 g/t, for 1,108,000 ounces, with Inferred Resources of 2.95M tonnes grading 5.88 g/t, for 558,000 ounces. The mine is situated on the like-named 83,850ha property covering a significant greenstone belt. Harte Gold also holds the Stoughton-Abitibi property east of the Holt Holloway Mine in Timmins, ON. Sugar M iddle Wo lf 2.90 5.88 0.56 Inferred 0 500 1,000 1,500 2,000 2,500 $0.00 $0.10 $0.20 $0.30 $0.40 $0.50 $0.60 Jul-18 Oct-18 Jan-19 Apr-19 Jul-19 Volume Price

Transcript of Harte Gold Corp. - axino.de filePage 1 of 15 Ryan Walker, MSc | 416.479.8997 |...

Page 1 of 15 Ryan Walker, MSc | 416.479.8997 | [email protected]

8 July 2019

Precious Metals

Event: We recently visited Harte Gold Corp.’s 100%-owned Sugar Zone mine in White River, Ontario, and came away struck by the ease of access and compact nature of the mine, the ease of ore vein visual identification, the simplicity of processing, and the compelling near-mine and regional exploration potential at Ontario’s newest gold producer.

Commercial Production Declared on January 1: During Q119, the mine produced 32,044t (10% below plan) owing to labour, equipment, and weather-related issues. The mill performed 8% above plan, processing 38,278t (425tpd) at 4.86g/t Au, with feed supplemented by low-grade stockpile. Recovery averaged 92%, in line with plan, to yield 5,476oz of gold, 9% below plan. In the mill, recovery via the gravity circuit was 38%, with subsequent flotation recovering another 53%. HRT notes that gravity recovery is expected to increase with higher grade ore — the April 2019 Feasibility Study (FS) envisages 61%. Operating costs were 16% higher than expected (mining +20%, G&A +26%, processing in line). As such, AISC came in at ~$2,750/oz.

HRT recently reported April and May production of 5,438oz, with final June results yet unavailable. Importantly, mill has stabilized and demonstrated the ability to run at 800tpd at planned recoveries. May and June mill feed continued to be supplemented with stockpile material as underground ramp-up continues. Production is currently sourced from Sugar Zone south sill development and stoping, with Sugar Zone north limb development ongoing. Stoping there is expected by September. Thereafter, HRT expects the mill to be solely fed run-of-mine production by Q419. HRT maintains 2019 guidance of 39,200oz at AISC of US$1,300-1,350/oz.

Looking Ahead: In 2020, HRT expects to produce 65,078oz on higher throughput (800tpd) and grade (6.98g/t vs. the 6.18g/t average expected during 2019), with lower AISC of US$913/oz. The FS envisages base-case LOM average production of 61,000oz at AISC of US$845/oz over 14 years. The study also considered an expansion to 1,200tpd from 800tpd (at estimated capex of $20-25M), which would see production rise to 95,000oz/yr (2022 onwards), offering potential for lower cash costs with reportedly ~40% of mining costs fixed. HRT expects permits for such expansion by the end of 2020. HRT also notes that conversion of existing Inferred Resources could potentially support an expansion to 1,400tpd for ~120,000oz of annual production at a modest additional capex of ~$26M.

Substantial Exploration Potential: Near-Mine. HRT is ramping up 2019 drilling, targeting near-mine areas, with a focus on the Sugar Zone southern extension, and convergence at depth of the Sugar-Middle zones (highlighted by 10.5g/t Au over 3.2m, 12.14g/t over 2.0m, 4.42g/t over 1.96m, and 3.66g/t over 1.9m), and Middle-Wolf zones (10.27g/t over 1.58m, 12.95g/t over 3.9m, 13.39g/t over 3.57m, and 12.14g/t over 2.0m) (Exhibit 3). More recent drilling along strike to the south of Sugar Zone returned 27.6g/t over 1.68m, 21.07g/t Au over 1.68m, including 115g/t over 0.34m, 8.62g/t over 1.90m, and 3.92g/t over 3.31m, including 0.39m at 26.5g/t (Exhibit 4). While early days, such relatively shallow mineralization proximal to planned development has the potential to have a greater nearer-term impact on the mine plan than the compelling potential extensions and coalescence of existing zones at greater depths. Step-out drilling continues along strike and down-dip of the new zone. HRT also plans regional exploration elsewhere on the 838.5km2 land package, which covers a significant Greenstone Belt. High-priority targets include the Hambleton Lake and K7 areas defined by geophysics, prospecting, and limited previous drilling (Exhibit 2).

Harte Gold Corp.

Ontario’s Newest Gold Producer Casts an Eye to the Future via Near-Mine and Regional Exploration

HRT-TSX: $0.25

Not Rated

N/A Target

Source: FactSet

Market Data C$

Market Capitalization ($M) 148.1

Net Debt ($M) 94.7

Cash & Equivalents ($M) - Mar. 31/19 0.7

Debt ($M) 95.4

Enterprise Value ($M) 242.8

Basic Shares O/S (M) 604.5

Fully Diluted Shares O/S (M) 675.1

Avg. Weekly Volume (M) 2.67

52-Week Range $0.21 - $0.55

Sugar Zone Mine NI 43-101 Inferred

Category Zone Tonnes Au Au

M g/t Moz

Probable Sugar 2.44 7.4 0.58

Wolf 2.95 6.6 0.31

Indicated Sugar 2.55 8.6 0.71

Wolf 1.70 7.3 0.40

Top Shareholders

Holder Shares (M) % S/O

Institutional

US Global Investors, Inc. (Asset Management)1.50 0.25%

Insiders/Stakeholders

Appian Capital Advisory Llp 176.1 29.14%

Orion Mine Finance 41.1 6.80%

Stephen Roman 30.4 5.03%

Michael Cowie 4.5 0.74%

Norman Campbell 1.8 0.29%

Risks

Operational Risk Exploration Results - 2019

Commodity Risk Production Ramp-up - 2019

Company Description

Events/Catalysts

Harte Gold is Ontario’s newest gold producer via its

100%-owned Sugar Zone Mine in White River, ON. At a

3g/t Au COG, NI 43-101-compliant Indicated Resources

total 4.24M tonnes grading 8.12 g/t, for 1,108,000

ounces, with Inferred Resources of 2.95M tonnes

grading 5.88 g/t, for 558,000 ounces. The mine is

situated on the like-named 83,850ha property covering

a significant greenstone belt. Harte Gold also holds the

Stoughton-Abitibi property east of the Holt Holloway

Mine in Timmins, ON.

Sugar

M iddle

Wolf

2.90 5.88 0.56Inferred

0

500

1,000

1,500

2,000

2,500

$0.00

$0.10

$0.20

$0.30

$0.40

$0.50

$0.60

Jul-18 Oct-18 Jan-19 Apr-19 Jul-19

Volume Price

Page 2 of 15

Harte Gold Corp. (HRT-TSX) | 8 July 2019

Ryan Walker, MSc | 416.479.8997 | [email protected]

Harte Gold Corp. (HRT-CA, $0.25) - Data Sheet Not Rated | PT: NAGeography - White River, Ontario Recommendation

Close Price $0.25Target: NAReturn: N/AConsensus 3 Mo. Ago Current Return

Rating: Buy Buy

Target: $0.78 $0.75 206%

Median: $0.80 $0.75 206%

High: $0.80 $0.80 227%

Low: $0.75 $0.70 186%

Consensus Distribution 2

Sector Outperform/Buy 2

Sector Perform/Hold 0

Sector UnderPerform/Sell 0

Stock Price / Volume Chart

Comparables Key Statistics

Ticker SP MC Cash Debt Current Price (C$) $0.25

$/shr $M $M $M P/'19EPS P/'20EPS P/'19CFPS P/'20CFPS 52-Week Range (C$) $0.21 - $0.55

AGB-CA 2.88 684.1 36.1 118.0 19.2x 20.7x 8.9x 9.5x Avg. Vol. (3-Mo, k) 534.1

ALO-CA 1.01 85.6 25.3 11.9 17.1x 14.4x 6.5x 6.4x Shares Outstanding (M) 604.5

AR-CA 1.84 328.3 37.5 18.7 8.7x 6.2x 3.3x 2.6x Shares Outstanding (diluted) (M) 675.1

DGC-CA 16.78 2955.7 268.7 348.3 35.0x 26.8x 8.2x 8.1x Cash 0.7

DPM-CA 4.72 844.1 18.6 82.4 16.2x 8.4x 5.6x 3.9x Debt 95.4

GCM-CA 4.18 201.7 53.7 99.4 3.4x 3.8x 2.0x 2.4x Market Cap $148.1

GSC-CA 5.32 580.5 109.4 132.5 19.0x 9.4x 7.3x 4.8x Resource (M,I&I - Moz) 1.66

JAG-CA 0.16 50.9 17.0 23.2 23.7x 7.9x 2.6x 2.6x Enterprise Value $242.8

KNT-CA 1.90 358.3 13.2 6.7 8.0x 2.9x 7.6x 3.3x Enterprise Value/oz (C$/oz) $146

LMC-CA 2.01 572.6 87.2 337.6 8.4x 9.6x 3.3x 3.4x FYE Dec 31

MND-CA 1.32 120.2 49.5 83.5 10.1x 3.4x 2.5x 1.4x CEO Stephen G. Roman

PRU-CA 0.56 666.7 62.2 66.1 40.0x 29.2x 4.5x 4.4x Employees 20

RED-AU 0.21 238.5 3.0 11.7 57.5x 14.4x 12.8x 5.3x Website http://www.hartegold.com

ROXG-CA 1.07 395.9 63.9 60.8 8.5x 7.8x 3.6x 3.7x Top Ownership Shares % Held

SGI-CA 0.72 50.4 21.7 10.1 219.7x 5.1x 3.1x 1.8x Appian Capital Advisory Llp 176.1 29.1%

TMR-CA 5.90 666.4 25.6 151.7 16.5x 10.7x 6.0x 4.8x Orion Mine Finance 41.1 6.8%

WDO-CA 5.50 750.8 27.8 10.9 27.2x 20.6x 13.3x 10.8x Stephen Roman 30.4 5.0%

HRT-CA 0.25 148.1 0.7 84.2 0.0x 6.1x 8.2x 3.5x Michael Cowie 4.5 0.7%

Bold - EWP Coverage Avg. 29.9x 11.5x 6.1x 4.6x Norman Campbell 1.8 0.3%

US Global Investors, Inc. (Asset Management) 1.5 0.2%

Management & Board of Directors NI 43-101 Inferred Resources (3g/t Au Cutoff) Flagship Asset

Stephen G. Roman, Ch, Pre., & CEO

Rein Lehari, CFO Tonnes Gold Silver

Roger Emdin, VP Operations Sugar Zone Mine M g/t oz

Timothy Campbell, Exec. VP and Secretary IND 4.24 8.08 1.10

Shawn Howarth, VP Corp. Dev. INF 2.90 5.88 0.56

Gordon Reed, Mine GM Global 7.14 7.19 1.66 Date Last Financing Price Value

Robert Kusins, Resource Geologist 19-Jun-19 Sub. Agreement $0.27 US$10

John Kita, Chief Mine Geologist Prob. Reserve 5.39 7.54 0.89 23-Nov-18 Non-Brokered PP $0.42 $1.4

George Flach, Independent Consultant 31-Oct-18 Non-Brokered FT PP $0.52 $7.0

Source: Consensus data - FactSet, Historical Data – Company Filings, Forecasts/estimates – Echelon Wealth Partners

All items in Millions except per share items

The Sugar Zone Property (“Sugar Zone”) is located in Ontario, approximately 80 km

east of the Hemlo gold camp and 24 km north of White River off the Trans-Canada

Highway (#17). The Sugar Zone property is comprised of 83,850 hectares covering a

significant greenstone belt. Harte Gold holds a 100% interest the property.

0

500

1,000

1,500

2,000

2,500

$0.00

$0.10

$0.20

$0.30

$0.40

$0.50

$0.60

Vo

lum

e (

00

0 S

har

es)

Sto

ck P

rice

($

)

Page 3 of 15

Harte Gold Corp. (HRT-TSX) | 8 July 2019

Ryan Walker, MSc | 416.479.8997 | [email protected]

Regional Exploration Targets

K7 comprises an area of widespread alteration south of the Sugar Zone mine, and represents areas of mineralization geologically different from the shear-hosted mineralization at the Sugar and Middle zones. Drilling to date has cut wide intervals of feldspar porphyry proximal to a mafic volcanic-sedimentary contact with anomalous gold values (up to 0.73g/t) associated with moderately silicified feldspar porphyry and iron formation. Previous Very Low-Frequency (VLF) surveying along the volcanic-sediment contact identified several prospective VLF trends, with subsequent mapping and sampling outlining several altered mafic volcanic and feldspar porphyry outcrops with anomalous copper (up to 0.175% Cu) and gold (up to 1g/t). Follow-up drilling is planned to fully define the extent of mineralization.

Hambleton Lake. Previous drilling at Hambleton Lake confirmed an extension of the Fisher Zone, cutting several altered mafic volcanic and porphyry units (up to 22m wide) accompanied by 1-2% pyrite and pyrrhotite. HRT notes that several holes included anomalous Zn values in iron formation (hole HG-19-27 cut 0.44% Zn over 0.35m and hole HG-19-26, 0.67m of 0.27% Zn). HRT plans a program of deeper drilling to test the alteration and iron formations down-dip.

Meanwhile, HRT is in the midst of interpreting data collected via a proprietary 2D Nanospectra Geophysical Survey (employing hyperspectral imaging and advanced satellite sensors) recently completed by Maximos Metals Corp. The campaign was aimed at identifying new exploration targets on the large property package.

Exhibit 1 — Regional VLF Geophysical Survey — Only ~10% of the Land Package Explored

Source: Harte Gold Corp.

Page 4 of 15

Harte Gold Corp. (HRT-TSX) | 8 July 2019

Ryan Walker, MSc | 416.479.8997 | [email protected]

Exhibit 2 — Planned 2019 Exploration Targets

Source: Harte Gold Corp.

Page 5 of 15

Harte Gold Corp. (HRT-TSX) | 8 July 2019

Ryan Walker, MSc | 416.479.8997 | [email protected]

Exhibit 3 — Location, Existing Resources, and Near-Mine Exploration Potential

Source: Harte Gold Corp.

Page 6 of 15

Harte Gold Corp. (HRT-TSX) | 8 July 2019

Ryan Walker, MSc | 416.479.8997 | [email protected]

Exhibit 4 — Early Near-Mine Exploration Success — Newly Emerging High-Grade Sugar Zone South

Source: Harte Gold Corp.

Page 7 of 15

Harte Gold Corp. (HRT-TSX) | 8 July 2019

Ryan Walker, MSc | 416.479.8997 | [email protected]

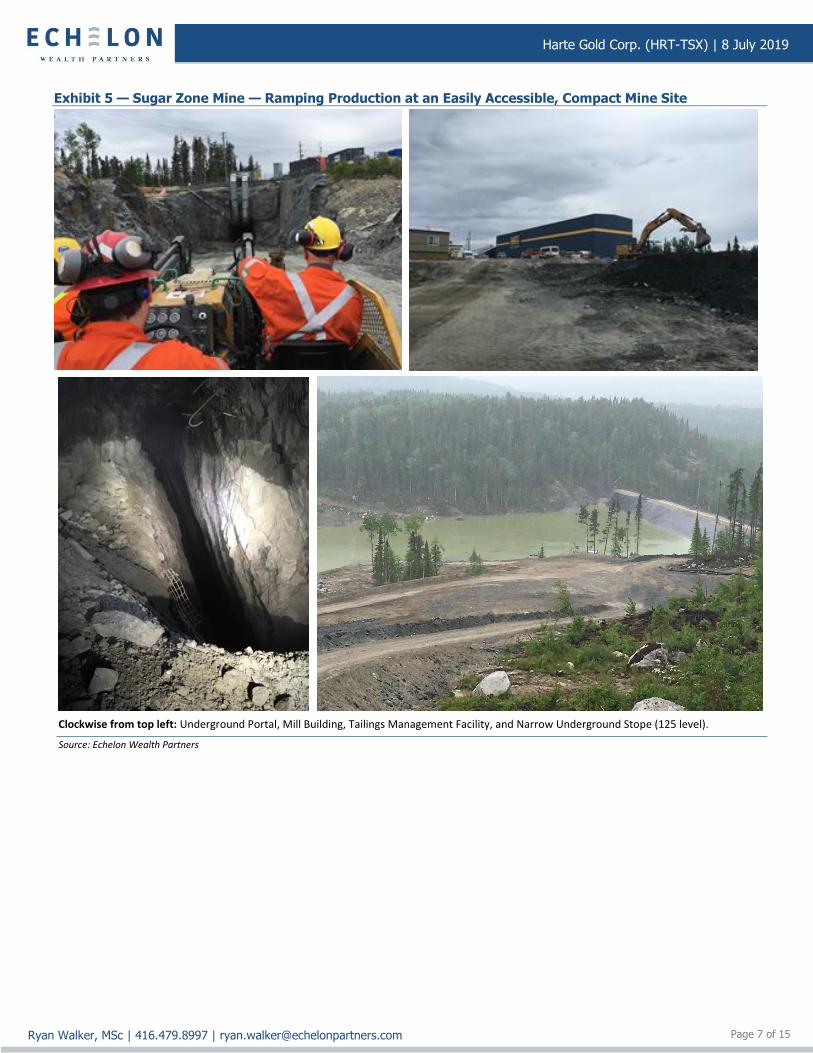

Exhibit 5 — Sugar Zone Mine — Ramping Production at an Easily Accessible, Compact Mine Site

Clockwise from top left: Underground Portal, Mill Building, Tailings Management Facility, and Narrow Underground Stope (125 level).

Source: Echelon Wealth Partners

Page 8 of 15

Harte Gold Corp. (HRT-TSX) | 8 July 2019

Ryan Walker, MSc | 416.479.8997 | [email protected]

Exhibit 6 — Sugar Zone Mine — Low-Tech Metallurgical Recovery — Gravity & Flotation

Clockwise from top left: Shaker Table, Gravity Recovered Coarse Gold, Flotation, and Bagging Concentrate.

Source: Echelon Wealth Partners

Page 9 of 15

Harte Gold Corp. (HRT-TSX) | 8 July 2019

Ryan Walker, MSc | 416.479.8997 | [email protected]

Production HRT notes that mining in Q119 (January and February) faced start-up challenges, including contractor equipment breakdowns, lack of manpower, reduced power voltage, power outages, and weather-related road closures. During March, ore supply consistently improved with increased underground equipment availability, upgrading of the underground electrical system, and a focus on recruitment of skilled mine workers. As a result, the Company reports that ore supply is on track as more stopes have been brought on line.

Indeed, mining operations achieved FS planned levels during April, hitting an average daily tonnage of ~540tpd, with mined grade also consistent with budget. HRT notes that stope blasting has gone smoothly, resulting in minimal overbreak or unplanned dilution.

Additionally, the mill and tailings management facility are operating to plan, with mill throughput exceeding plan owing to the processing of surface stockpiles to offset lower mine production in January and February. Overall, the mill saw recovery of 91% during Q119, in line with plan. Recovery from the gravity circuit was 38%, with the flotation recovering another 53%. HRT expects gravity recovery to improve with higher grade ore deliveries – and has since reportedly seen improved gravity recoveries.

More recently, ore production was below target during May and June owing to a lack of stope availability and ventilation development. HRT notes that ventilation work was subsequently completed, and mine performance is expected to improve with more efficient post-blast smoke clearing. Stope development is also ongoing in the Sugar Zone north limb, with stoping expected to ramp up there in September. In the mill, throughput again exceeded plan during Q219, with feed supplemented with surface stockpiles (6,000t at 2.5g/t remains in stockpile). HRT expects higher recoveries upon milling of higher grade material going forward.

Exhibit 7 — Working Through Teething Pains — Mill Operating as Planned

Source: Harte Gold Corp.

Page 10 of 15

Harte Gold Corp. (HRT-TSX) | 8 July 2019

Ryan Walker, MSc | 416.479.8997 | [email protected]

Looking Ahead Adjusting for Q119 performance, HRT expects to produce 39,200oz Au at cash costs of $1,050-1,100/oz (US$800-850/oz), and AISC of $1,700-1,775/oz (US$1,300-1,350/oz) during 2019, with lower AISC expected during H219 once mill throughput of 800tpd is attained. The Ministry of Energy, Northern Development and Mines and the Ministry of Environment, Conservation and Parks granted HRT approval to increase mine production to 800tpd in early May, earlier than previously expected. Production in 2020 is forecast to increase to 65,078oz Au on sustained higher throughput (800tpd) and grade (6.98g/t vs. the planned 2019 average of 6.18g/t). As such, HRT expects AISC to fall to US$913/oz.

Exhibit 8 — 2019 Quarterly Production Outlook — Adjusted for Q119 Results

Source: Harte Gold Corp.

Longer term, HRT sees potential for +100,000/yr. The FS also considered an expansion to 1,200tpd from the base-case 800tpd (estimated capex of $20-25M), which would see annual production increase to 95,000oz (2022-2025, followed by 1,100tpd in 2026-2027, and 1,000tpd in 2028). Such increased throughput would carry the potential for reduced cash costs, as HRT notes that ~40% of mining costs are fixed. Permits for such an expansion are expected by the end of 2020. HRT also notes that the conversion of existing Inferred Resources could potentially support an expansion to 1,400tpd for ~120,000oz of annual production at a modest additional capex of ~$26M.

Exhibit 9 — Expansion Potential — Permit for Expansion to 1,200tpd Expected by the end of 2020

Source: Harte Gold Corp.

Page 11 of 15

Harte Gold Corp. (HRT-TSX) | 8 July 2019

Ryan Walker, MSc | 416.479.8997 | [email protected]

Exhibit 10 — Feasibility Study Summary

Source: Harte Gold Corp.

Exhibit 11 — Feasibility Mine Plan Targets a Small Portion of Mineralization

Source: Harte Gold Corp.

Page 12 of 15

Harte Gold Corp. (HRT-TSX) | 8 July 2019

Ryan Walker, MSc | 416.479.8997 | [email protected]

Onerous Debt Re-jigged In early May, HRT announced the refinancing of its then-existing debt via a new US$72.5M Senior debt package from BNP Paribas. The facility comprises a 6-year US$52.5M term loan, and a 3-year US$20M revolving credit facility. The debt bears interest at the rate of LIBOR plus 2.875-3.875% (based on credit ratios), with repayment beginning on March 31, 2020.

Of the proceeds, US$40M will go toward extinguishing existing long term-debt from Sprott Private Resource Lending, which included interest at the rate of 7.5% plus the 3-month LIBOR. HRT will also extinguish a variable (calculated at 1.3% of the average monthly gold price, with a floor of US$1,250/oz and ceiling of US$1,450/oz) production payment agreement with Sprott. Another US$20M will be used to repay short-term debt financing with ANR Investments B.V. (Appian). The financing will also improve liquidity and working capital during the expansion to 800tpd.

At the same time, Appian agreed to a US$10M equity investment at $0.27/share, and to provide a standby commitment for an additional US$7.5M in non-equity financing, available at HRT’s option.

Page 13 of 15

Harte Gold Corp. (HRT-TSX) | 8 July 2019

Ryan Walker, MSc | 416.479.8997 | [email protected]

Important Information and Legal Disclaimers

Echelon Wealth Partners Inc. is a member of IIROC and CIPF. The documents on this website have been prepared for the viewer only as an example of strategy consistent with our recommendations; it is not an offer to buy or sell or a solicitation of an offer to buy or sell any security or instrument or to participate in any particular investing strategy. Any opinions or recommendations expressed herein do not necessarily reflect those of Echelon Wealth Partners Inc. Echelon Wealth Partners Inc. cannot accept any trading instructions via e-mail as the timely receipt of e-mail messages, or their integrity over the Internet, cannot be guaranteed. Dividend yields change as stock prices change, and companies may change or cancel dividend payments in the future. All securities involve varying amounts of risk, and their values will fluctuate, and the fluctuation of foreign currency exchange rates will also impact your investment returns if measured in Canadian Dollars. Past performance does not guarantee future returns, investments may increase or decrease in value and you may lose money. Data from various sources were used in the preparation of these documents; the information is believed but in no way warranted to be reliable, accurate and appropriate. Echelon Wealth Partners Inc. employees may buy and sell shares of the companies that are recommended for their own accounts and for the accounts of other clients.

Echelon Wealth Partners compensates its Research Analysts from a variety of sources. The Research Department is a cost centre and is funded by the business activities of Echelon Wealth Partners including, Institutional Equity Sales and Trading, Retail Sales and Corporate and Investment Banking.

Research Dissemination Policy: All final research reports are disseminated to existing and potential clients of Echelon Wealth Partners Inc. simultaneously in electronic form. Hard copies will be disseminated to any client that has requested to be on the distribution list of Echelon Wealth Partners Inc. Clients may also receive Echelon Wealth Partners Inc. research via third party vendors. To receive Echelon Wealth Partners Inc. research reports, please contact your Registered Representative. Reproduction of any research report in whole or in part without permission is prohibited.

Canadian Disclosures: To make further inquiry related to this report, Canadian residents should contact their Echelon Wealth Partners professional representative. To effect any transaction, Canadian residents should contact their Echelon Wealth Partners Investment advisor.

U.S. Disclosures: This research report was prepared by Echelon Wealth Partners Inc., a member of the Investment Industry Regulatory Organization of Canada and the Canadian Investor Protection Fund. This report does not constitute an offer to sell or the solicitation of an offer to buy any of the securities discussed herein. Echelon Wealth Partners Inc. is not registered as a broker-dealer in the United States and is not be subject to U.S. rules regarding the preparation of research reports and the independence of research analysts. Any resulting transactions should be effected through a U.S. broker-dealer.

U.K. Disclosures: This research report was prepared by Echelon Wealth Partners Inc., a member of the Investment Industry Regulatory Organization of Canada and the Canadian Investor Protection Fund. ECHELON WEALTH PARTNERS INC. IS NOT SUBJECT TO U.K. RULES WITH REGARD TO THE PREPARATION OF RESEARCH REPORTS AND THE INDEPENDENCE OF ANALYSTS. The contents hereof are intended solely for the use of, and may only be issued or passed onto persons described in part VI of the Financial Services and Markets Act 2000 (Financial Promotion) Order 2001. This report does not constitute an offer to sell or the solicitation of an offer to buy any of the securities discussed herein.

Copyright: This report may not be reproduced in whole or in part, or further distributed or published or referred to in any manner whatsoever, nor may the information, opinions or conclusions contained in it be referred to without in each case the prior express written consent of Echelon Wealth Partners.

ANALYST CERTIFICATION

Company: Integra Resources Corp. | HRT:TSX I, Ryan Walker, hereby certify that the views expressed in this report accurately reflect my personal views about the subject securities or issuers. I also certify that I have not, am not, and will not receive, directly or indirectly, compensation in exchange for expressing the specific recommendations or views in this report. IMPORTANT DISCLOSURES

Is this an issuer related or industry related publication? Issuer

Does the Analyst or any member of the Analyst’s household have a financial interest in the securities of the subject issuer? If Yes: 1) Is it a long or short position? Yes; and, 2) What type of security is it? Common shares

No

The name of any partner, director, officer, employee or agent of the Dealer Member who is an officer, director or employee of the issuer, or who serves in any advisory capacity to the issuer.

No

Does Echelon Wealth Partners Inc. or the Analyst have any actual material conflicts of interest with the issuer? No

Does Echelon Wealth Partners Inc. and/or one or more entities affiliated with Echelon Wealth Partners Inc. beneficially own common shares (or any other class of common equity securities) of this issuer which constitutes more than 1% of the presently issued and outstanding shares of the issuer?

No

During the last 12 months, has Echelon Wealth Partners Inc. provided financial advice to and/or, either on its own or as a syndicate member, participated in a public offering, or private placement of securities of this issuer?

No

During the last 12 months, has Echelon Wealth Partners Inc. received compensation for having provided investment banking or related services to this Issuer? No

Has the Analyst had an onsite visit with the Issuer within the last 12 months? Sugar Zone Mine site in White River, ON -- including mine office, underground workings, core facility, etc. (June 24, 2019)

Yes

Has the Analyst or any Partner, Director or Officer been compensated for travel expenses incurred as a result of an onsite visit with the Issuer within the last 12 months? No

Has the Analyst received any compensation from the subject company in the past 12 months? No

Is Echelon Wealth Partners Inc. a market maker in the issuer’s securities at the date of this report? No

Page 14 of 15

Harte Gold Corp. (HRT-TSX) | 8 July 2019

Ryan Walker, MSc | 416.479.8997 | [email protected]

RATING DEFINITIONS

Buy The security represents attractive relative value and is expected to appreciate significantly from the current price over the next 12 month time horizon.

Speculative Buy The security is considered a BUY but in the analyst’s opinion possesses certain operational and/or financial risks that are higher than average.

Hold The security represents fair value and no material appreciation is expected over the next 12-18 month time horizon.

Sell The security represents poor value and is expected to depreciate over the next 12 month time horizon.

Under Review While not a rating, this designates the existing rating and/or forecasts are subject to specific review usually due to a material event or share price move.

Tender Echelon Wealth Partners recommends that investors tender to an existing public offer for the securities in the absence of a superior competing offer.

Dropped Coverage

Applies to former coverage names where a current analyst has dropped coverage. Echelon Wealth Partners will provide notice to investors whenever coverage of an issuer is dropped.

RATINGS DISTRIBUTION

Recommendation Hierarchy Buy Speculative Buy Hold Sell Under Review Restricted Tender

Number of recommendations 53 40 14 0 6 0 0

% of Total (excluding Restricted) 47% 35% 12% 0% 5%

Number of investment banking relationships 10 15 4 0 2 0 0

% of Total (excluding Restricted) 32% 48% 13% 0% 6%

PRICE CHART, RATING & PRICE TARGET HISTORY

Date Target (C$) Rating

8 Jul 2019 N/A N/A

Data sourced from: FactSet

$0.00

$0.10

$0.20

$0.30

$0.40

$0.50

$0.60

$0.70

$0.80

Jun 17 Oct 17 Feb 18 Jun 18 Oct 18 Feb 19 Jun 19

Harte Gold Corp. (TSX:HRT)

Share Price

Page 15 of 15

Harte Gold Corp. (HRT-TSX) | 8 July 2019

Ryan Walker, MSc | 416.479.8997 | [email protected]

Toronto Wealth Management

1 Adelaide St East, Suite 2000

Toronto, ON M5C 2V9

416-572-5523

Toronto Capital Markets

1 Adelaide St East, Suite 2100

Toronto, Ontario M5C 2V9

416-572-5523

Montreal Wealth Management and Capital Markets

1000 De La Gauchetière St W., Suite 1130

Montréal, QC H3B 4W5

514-396-0333

Calgary Wealth Management

525 8th Ave SW, Suite 400

Calgary, AB T2P 1G1

403-218-3144

Calgary Wealth Management

123 9A St NE

Calgary, AB T2E 9C5

1-866-880-0818

Oakville Wealth Management

1275 North Service Road, Suite 612

Oakville, ON L6M 3G4

289-348-5936

Edmonton Wealth Management

8603 104 St NW

Edmonton, AB T6E 4G6

1-800-231-5087

London Wealth Management

495 Richmond St, Suite 200

London, ON N6A 5A9

519-858-2112

Ottawa Wealth Management

360 Albert St, Suite 800

Ottawa, ON K1R 7X7

613-907-0700

Vancouver Wealth Management and Capital Markets

1055 Dunsmuir St, Suite 3424, P.O. Box 49207

Vancouver, BC V7X 1K8

604-647-2888

Victoria Wealth Management

730 View St, Suite 210

Victoria, BC V8W 3Y7

250-412-4320

Saskatoon Wealth Management

402-261 First Avenue North

Saskatoon, SK S7K 1X2

306-667-2282