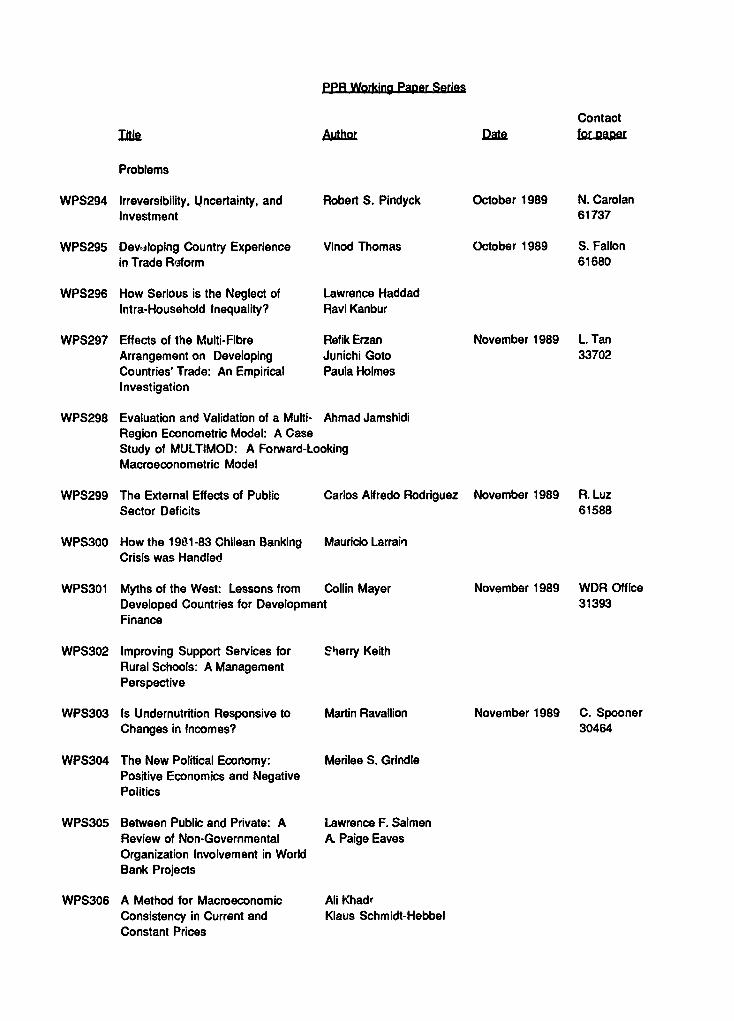

Harmonizing Tax Policies in Central America€¦ · WORKING PAPERS Country Operations Latin America...

54

Policy, Planning, and R WORKING PAPERS Country Operations LatinAmerica and the Caribbean Country Department 11 TheWorldBank November 1989 WPS 308 Harmonizing Tax Policies in Central America Yalcin M. Baran Transforming the Central American Customs Union into a modem common market can be achieved only by reforming the tariff regime. Here is an action plan for rationalizing and harmonizing Central American tax structures. The Policy, Planning, and Research Complex distributes PPR Working Papers to dissariinate the findings of work in progress and to encouragethe exchange of ideas among Bank staff and all othcrs interested in development issues. These papers carry the names of the authors, reflect only their views, and should be used and cited accordingly. The finr-ings.interpretations, and conclusions are the authors'own. They should not be attributedto the World Bank, its Boardof Directors, its management, orany of its membercountries. Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized

Transcript of Harmonizing Tax Policies in Central America€¦ · WORKING PAPERS Country Operations Latin America...

Policy, Planning, and R

WORKING PAPERS

Country Operations

Latin America and the CaribbeanCountry Department 11

The World BankNovember 1989

WPS 308

Harmonizing Tax Policiesin Central America

Yalcin M. Baran

Transforming the Central American Customs Union into amodem common market can be achieved only by reforming thetariff regime. Here is an action plan for rationalizing andharmonizing Central American tax structures.

The Policy, Planning, and Research Complex distributes PPR Working Papers to dissariinate the findings of work in progress and toencourage the exchange of ideas among Bank staff and all othcrs interested in development issues. These papers carry the names ofthe authors, reflect only their views, and should be used and cited accordingly. The finr-ings. interpretations, and conclusions are theauthors' own. They should not be attributed to the World Bank, its Board of Directors, its management, or any of its member countries.

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

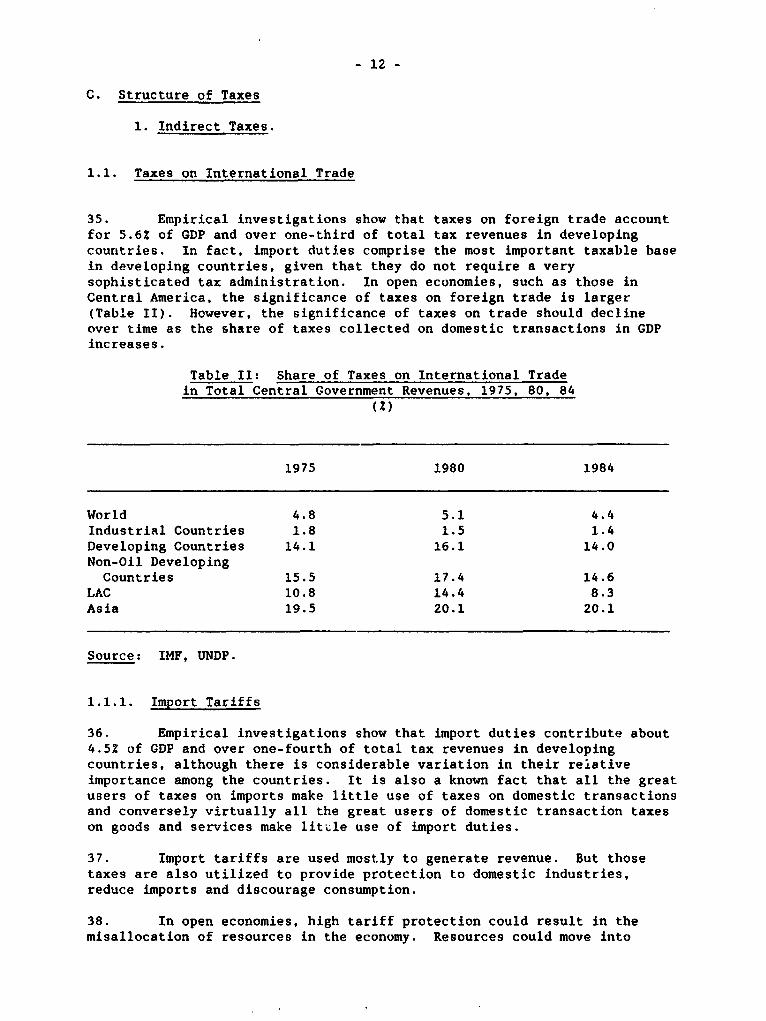

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

| Pollcy, Planning, ~and Reseafch

Country Operations

To harmonize tax policies among Central * Harmonizing taxes on inputs and exemptingAmerican nations, Baran recommends the nontraditional exporters from paying importfollowing: duties.

e Continuing trade liberalization, by reducing * Moving toward coordinating taxes on factorthe level and dispersion of effective trade incomes (personal and corporate income,protection. property and land taxes, and taxes on financial

gains) to avoid double taxation.* Shifting the tax system from reliance on

trade to reliance on domestic transactions and * Eliminat.ng all quantitative import restric-income. tions, prior imports deposits, non-common

import tariffs, and other restrictions on imports* Making the value-added tax (cum selective from other CACM members.

consumption taxes) the backbone of the taxsystem, and harmonizing those taxes among the * Applying similar principles in designingmember countries of the Central American export taxes on coffee and bananas.Common Market (CACM).

* Not using differential exchange rates to dis-* Improving tax administration criminate against regional trade.

This paper is a product of the Country Operations Division, Latin America and theCaribbean Country Department II. Copies are available free from the World Bank,1818 H Street NW, Washington DC 20433. Please contact Tipawan Watana, room18-155, extension 31882 (48 pages with tables).

'Pe PPR Working Paper Series disseminates the Pindings of work undem way in the Bank's Policy, Planning, ard ResearchComplex. An objective of the series is to get these fundings out quickly, even if presentations are less than fully polished.'. ie rtndings. interpretations, and conclusions in these papers do not necessariIy represent official policy of the Banlc.

Produced at the PPR Disserniination Center

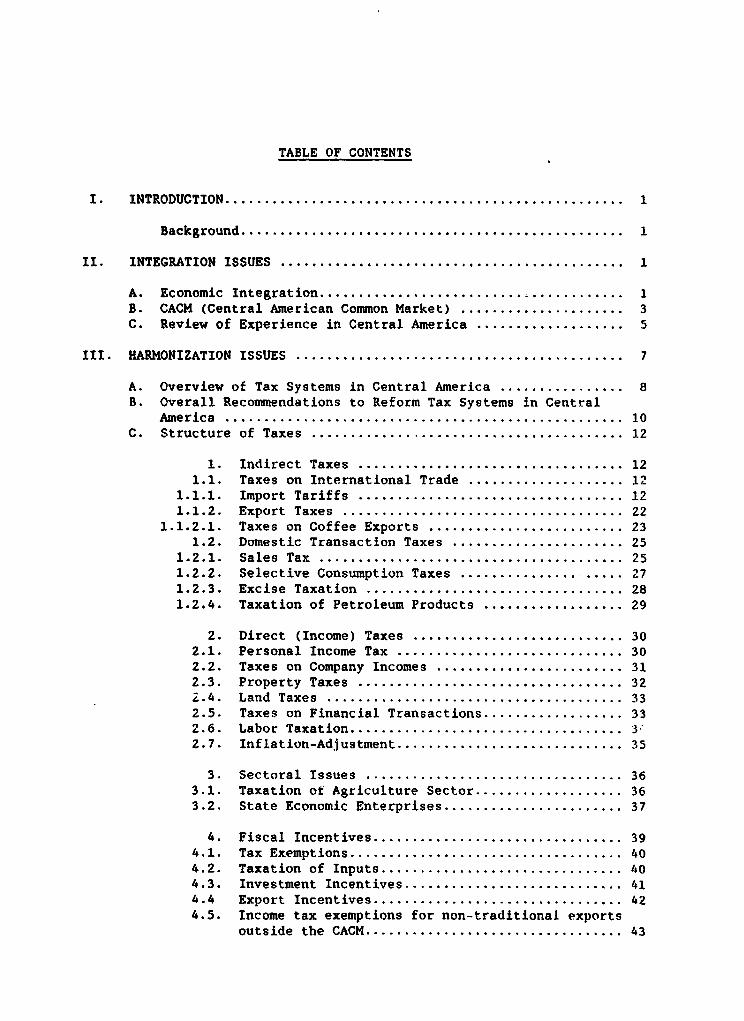

TABLE OF CONTENTS

I. INTRODUCTION ................................................... 1

Background ................................................. 1

II. INTEGRATION ISSUES ............. ............................... 1

A. Economic Integration .......................... ............ 1B. CACM (Central American Common Market) ..................... 3C. Review of Experience in Central America ................... 5

III. HARMONIZATION ISSUES ........................... 7

A. Overview of Tax Systems in Central America .... ............ 8B. Overall Recommendations to Reform Tax Systems in Central

America .............................................. 10C. Structure of Taxes .............. .......................... 12

1. Indirect Taxes .............................. 121.1. Taxes on International Trade ...... .............. 1I

1.1.1. Import Tariffs . ................................. 121.1.2. Export Taxes .................................... 22

1.1.2.1. Taxes on Coffee Exports .231.2. Domestic Transaction Taxes ...... ................ 25

1.2.1. Sales Tax ....................................... 251.2.2. Selective Consumption Taxes . ..................... 7. 71.2.3. Excise Taxation . ................................ 281.2.4. Taxation of Petroleum Products ..... ............. 29

2. Direct (Income) Taxes ........ ................... 302.1. Personal Income Tax ......... .................... 302.2. Taxes on Company Incomes ....... ................. 312.3. Property Taxes ................................... 32Z.4. Land Taxes ....................................... 332.5. Taxes on Financial Transactions .................. 332.6. Labor Taxation ................................... 3-2.7. Inflation-Adjustment ............................. 35

3. Sectoral Issues . ................................ 363.1. Taxation of Agriculture Sector ................... 363.2. State Economic Enterprises ....................... 37

4. Fiscal Incentives ................................ 394.1. Tax Exemptions ................................... 404.2. Taxation of Inputs ............................... 404.3. Investment Incentives ............................ 414.4 Export Incentives ................................ 424.5. Income tax exemptions for non-traditional exports

outside the CACH ................................ 43

TABLE OF CONTENTS (CONTINUED)

5. Institutional Issues (The Practice of TaxEarmarking) ...................................... 43

6. Tax Administration ................................ 44

D. Impact of Liberalization Policies on Fiscal Revenues ........ 46

E. Medium-Term Economic Goals .. 46

F. Phasing Reforms ............................................. 46

G. Main 3onclusions ............................................ 47

Tables

Table I Central America: Tax Ratios, 1983-86 .10

Table II Share of Taxes on International Trade in Total CentralGovernment Revenues, 1975, 80, 84 .12

Table III Comparison of Old Tariff Regime, New Tariff Regime andPlanned Regime .17

Table IV Number of Contributors Under Major Taxes in El Salvador,1987 .45

I. INTRODUCTION

1. This report proposes an action plan for the rationalization of taxstructures for Central America. The report also outlines broad principlesto harmonize taxes among the Central American Comon Market (CACH) membercountries. For the purpose of this study, the CACM excludes Nicaragua (amember), but includes Honduras (a non-member). A separate study underprogress in the Bank will undoubtedly analyze benefits and costs ofintegration and review conditions under which integration would beeconomic. This report assumes that harmonization is indeed economic.However, the report's main conclusions on the rationalization of taxsystems in Central America would still be valid even if integration isfound to be unsound. Furthermore, the report excludes Nicaragua from theanalysis due to lack of information. This report does not deal with theissue of expenditure rationalization. Clearly, an introduction of arevenue-yielding tax package should only be considered if expenditures areefficiently spent and all low-priority programs are eliminated.

Background

2. Central American economies are very open, with exports and importsaccounting for a substantial share of GDP compared to other countries atthe same level of development. The resource endowments of each country inthe Region are not as homogeneous as would appear based on a cursoryexamination. Land/population ratio, for example, is more favorable inHonduras compared to El Salvador. Forest resources are relatively abundantin Honduras and in Costa Rica compared to El Salvador. Costa Rica'sliteracy rate is the highest in the Region, and hence its workforce isbetter educated. However, literacy rates in other countries are lowcompared to most other Latin American countries. On the other hand, allcountries have a comparative advantage in traditional agriculture, althougheach country has a different combination of traditional products (i.e.coffee, bananas, sugar, cotton, and cocoa etc).

3. The degree of resource mobilization in the Region is inadequate,with low tax to GDP ratios (with the exception of Costa Rica) compared tocountries at similar GDP per capita levels. Tax systems are rudimentary.Financial disequilibrium of the public sectors is the norm, as evidenced bylarge--although declining--public sector deficits and domestic financing ofthose deficits, leading to domestic inflationary pressures. Furthermore,in all the countries in Central America, the elasticity of the tax systemis low. As a result, growth in tax revenues has lagged behind that ofincome and GDP in the recent past.

II. INTEGRATION ISSUES

A. Economic Integration

4. The objective of harmonization of tax systems is to facilitateeconomic integration among countries joining a common market. As explained

-2-

below, there are essentially five different forms of economic integration.CACM fits into the definition of a customs union (ii below) rather than acommon market (iii below). Economic integration is intended to expandtrade among member countries as well as to encourage deeperindustrialization by permitting the utilization of scale economies inproduction. The following is a description of different forms ofintegration:

(i) Free Trade Area: Tariffs are abolished among membercountries, but each country retains its tariffs on importsfrom non-member countries.

(ii) Customs Union: In addition to abolishing tariffs on tradeamong member countries as in (i) above, countries alsoadopt a common external tariff for imports from non-membercountries.

(iii) Common Market: Common market is based on a free tradeamong member countries and a common external tariff forimports from non-member countries as in (ii) above plus afree movement of factors of production (i.e. labor andcapital).

(iv) Economic Union: In addition to free trade and freemovement of factors of production among the membercountries as well as a common external tariff (iii above),member countries harmonize economic policies (a laCOMECON). In particular, fiscal, monetary and exchangerate policies are closely coordinated and harmonized amongthe member countries.

(v) Total Economic Integration: In addition to having all theattributes of an economic union, total economicintegration requires an establishment of a supernationalauthority, which determines economic policies for all themember countries. Decisions of this entity would bebinding on all countries.

5. Integration among various countries is prevalent in the worldtoday. The Central American Common Market (CACM) is one of several suchintegration efforts. Other integration efforts include: European EconomicCommunity (EEC): the Committee on Mutual Economic Assistance (COMECON) forthe Centrally Planned Economies 'n Eastern Europe; European Free TradeAssociation for north European nations; the Latin American Free TradeAssociation and the Andean Group for South American countries; theCaribbean Community; the free-trade agreement between the United States andIsrael; the Association of South East Asia Nations (ASEAN) that seeks freetrade among the six nations of that region; the recently concluded free-trade agreements between Australia and New Zealand, and between the U.S.A.and Canada.

B. CACM (Central American Common Market)

6. Based on the premise that the strategy of autarky is not a viabledevelopment option, the five countries in Central America established aCustoms Union in 1960. Integration helped accelerate the industrializationof the Region. However, industrialization did not go beyond the easy stageof consumer goods production (i.e. mostly food and textiles). The tradediversion that this integration caused also led to a welfare loss, as theprices of most import-substitutes were higher than their internationalequivalents. After the mid-1970s, the Customs Union lost its dynamism,with Honduras leaving, following a war with El Salvador. The sharpincrease in intra-regional trade in the early 19809 resulted from heavypurchases by Nicaragua to rebuild its internal war-damaged economy. Butthe expansion in trade proved unsustainable as Nicaragua could not pay allits debts to other CACH members. As a result, the CACM member countriessharply reduced their trade with Nicaragua. Coupled with the fall in GDPper capita in the Region, the accumulated unpaid Nicaraguan debt to othermember countries led to a reduction in intra-regional trade after 1983. Asa result, intra-regional trade, after peaking at US$1.1 billion in 1980,fell to US$757 million in 1983.

7. The present challenge confronting the policymakers in CentralAmerica is to transform the Union to a modern common market. This couldonly be achieved through a strong reform of the tariff regime. This reportdescribes an action plan to achieve this objective. It does not analyzepolitical feasibility of the recommended actions, and assumes that they arefeasible. It is important to note, however, that at this juncture, optionsto grow out of the present macroeconomic problems are limited and hence thetimely introduction of reforms is vital to regain high growth ratesrecorded by the countries in the Region in the past.

8. Given that the economic costs of implementing an import-substitution strategy are higher the smaller the size of a country, CACMattempted to implement this strategy on a regional basis. However, theenlarged regional market proved to be too small for most products, giventhe larger economies of scale needed for economic operations. Hence, theintegration of the regional economies to the world economy is essential forensuring the viability of the customs Union. This requires that Unionmembers accelerate the process underway in reducing the level anddispersion of effective protection.

9. The Customs Union appears to be in disarray. First, Honduraspulled out from the Union, following its war with El Salvador in 1967 anddid not join the Union thereafter, conducting its trade with other CACMmembers through bilateral treaties. Second, following the 1979 revolution,Nicaragua shifted to a centrally-managed economy, therefore, tariffs becameirrelevant for protection purposes in Nicaragua. Also, financialdifficulties faced by Nicaragua resulted in a large increase in arrears onits regional trade with other countries ir. the Customs Union. Third, ElSalvador has been going through a difficult period of internal warfare,with a consequent adverse impact on production, investment and on itsbalance of payments. These factors coupled with the unresolved issue ofensuring equitable distribution of costs and benefits from integrationamong the member countries have resulted in a weakened Customs Union.

-4-

10. To achieve a smooth functioning of trade within a common marketwith partners of unequal wealth and productive capacity, a number ofconditions need to be fulfilled. First, the impact of trade creationshould outweigh that of trade diversion. Second, related to the firstpoint, large trade imbalances among member countries may not be sustainableover long periods of time and countries shot l take measures to reduce themto sustainable levels (i.e. through deflati%.iary domestic policies andappropriate use of the exchange rate). Third, indirect taxes on domectictransactions should be harmonized among the member countries to ensure thatthese taxes are not used to counterbal&nce or negate the commonality of theexternal tariff. Fourth, having a common external tariff implies that alltariffs on imports should be the same for all member countries. Fifth,common external tariffs should cover all product categories andquantitative import restrictions should be phased out. Sixth,harmonization of national policies is also an essential ingredient in thesuccessful functioning of a common market. Specifically, harmonization offiscal and monetary policies and management of the exchange rate areessential. Otherwise, with widely varying exchange rate and domesticpolicies, countries may opt to use tariffs as an instrument to achievetheir domestic objectives. For example, expansionary domestic policiesunder a fixed exchange rate regime could lead to the distortionary use oftariffs to protect the balance of payments. For example, Costa Ricaheightened existing surcharges and established new ones on imports in theearly 1980s to protect its balance of payments as expansionary domesticpolicies under the fixed exchange rate regime led to an overvaluation ofits currency as domestic inflation accelerated. Seventh, for the commonmarket to be successful, all members, including the relatively weaker onesshould be given incentives to stay within the common market. Hence,countries with higher levels of wealth and productive capacity should helpcountries with more limited levels of wealth and productive capacity.Eighth, there has to be a legal framework to monitor the functioning of thecommon market. Lastly, Governments should accept the fact that membershipin a common market implies foregoing part of their power of unilaterallydetermining domestic policies.

11. The creation of the CACM gave rise to a number of importantstructural changes. First, it led to a large increase in the share ofindustry in GDP. For most of the 1960s and 1970s, the growth of industryoutstripped GDP growth by a wide margin, while agriculture grew slower thanoverall GDP. Growth of industry was also facilitated by the expansion inmanufactured exports mostly to the regional market. As a result, tradewithin the CACM--mostly manufactured goods--grew rapidly. Thesedevelopments also led to a structural shift in the composition of imports,with intermediate and capital goods imports increasing and final consumergoods imports decreasing. The openness of economies in Central Americarose, paralleling the expansion in exports to CACM and in imports ofintermediate and capital goods.

12. There is a need to review the extent to which the creation of CACMled to trade creation and/or trade diversion. On an apriori basis, itcould be assumed that trade was diverted in final consumer goods, while itwas created for intermediate and capital goods for the Region as a whole.

-5-

13. The agricultural sectors in the Region face a number of issues.coffee and bananas are the most important commodities in export agriculturein virtually all the countries in the Region. Coffee exports are regulatedunder the International Coffee Agreement. btagnation in world demand keptproduction increases to low levels despite yield improvements in coffee.In fact, Costa Rica's yields are one of the highest in the world. Cyclicalchanges in coffee prices exerted an important impact on money incomes. Thelarge increase in coffee prices during 1976-77 and in 1986 provided largewindfall foreign exchange revenues. Banana exports, however, grew veryslowly. Because of labor problems and increases in transport costs. oneinternational banana company left Costa Rica. Other traditional products,such as cotton, sugar, and cocoa faced difficulties as a result of reducedinternational prices, increases in costs and management problems. Overall,the performance of export agriculture has been mixed. On the other hand,basic grains production increased, benefiting from quantitative importrestrictions and generous price and interest rate subsidies and creditallocation schemes, which favored basic grains production such as in CostaRica. In particular, rice production grew substantially because of yieldimprovements based on new technology. However, since basic grainsproduction is high-cost in the Region, rice had to be exported at a loss,subsidized by the public sector as in the case of Costa Rica. As a result,the increase in basic grains production was obtained at substantialeconomic and fiscal costs.

C. Review of Experience In Central America

14. The experience in Central America as outlined above did notrespcad to the requirements for a well-functioning common market. First,the trade diversion effect appears to have dominated trade creation. Therehave been some calculations on trade creation and trade diversion by Mr.Larry Wilmore. These calculations confirm that trade diversion dominatedtrade creation in the CACM. This has had significant implications forcountries which have a relatively undeveloped productive capacity forexports. For example, within the common market, Honduras would import alarge share of its requirements for final consumer goods from other CommonMarket member countries at prices higher than international prices, leadingto a net loss of foreign exchange on its balance of payments. For acountry like Honduras with a large disequilibrium in its balance ofpayments, this presents a serious problem. However, it is difficult toquantify the exact trade diversion and creation effects with any degree ofprecision without undertaking a serious study.

15. Second. large imbalences have occurred among the CACM membercountries in their trade with each other since 1980. For example, by yearend-1986, Costa Rica's creditor balances with other counties amounted toover US$350 million. A large part of this imbalance in trade resulted fromNicaragua's lack of payments for its net debtor balances. Nicaraguastepped up its imports from other CACM member countries in 1980-81,following destruction of some of its productive capacity after the 1979revolution. However, since the country ran into balance of paymentsproblems, it has accumulated large arrears with the rest of the CACH membercountries, and could not sustain the same level of demand.

- 6 -

16. Third, member countries resorted zo establishing different ratesfor domestic transaction taxes on goods imported from other CACM memberscompared to non-member countries. Differential rates of consumption taxeswere used to raise protection over and above those provided by impoattariffs and surcharges.

17. Fourth, member countries also established additional charges onimports--which are not applied uniformly by all member countries. Thesecharges were sometimes applied to imports from other CACM member countries.The imposition of thcse additional charges on imports implied the break-upof the common external tariff for most products: it assigned differentnominal and hence effective protection rates to various industries in eachmember country and violated the principle of free trade among the membercountries. Furthermore, some countries also used the exchange rate as atool for protection against imports from other CACM members.

18. Fifth, some product categories were excluded from the commonexternal tariff, leading to a weakening of the customs union's instruments.For example, trade in basic grains was regulated in each country throughthe implementation of quantitative import restrictions and importation by apublic sector marketing agency. This arrangement effectively ruled out theuse of a common external tariff on agricultural products. Furthermore,member countries excluded some final consumer goods from the commonexternal tariff, and assigned higher tariff rates for these products asdiscussed in the section on import tariffs. The intention of theauthorities in the Region is to reach an agreement quickly on common ratesfor these products. Given the importance of these products in domesticproduction (i.e. they account for about one-third to one-fourth of domesticproduction in Costa Rica), this exclusion clearly weakens the customsUnion. Given that most of these products are not competitive, thisexclusion and the increased nominal rates reversed some of the benefits ofthe tariff reform.

19. Sixth, although an effort has been made in the past to coordinatenational economic policies, no concrete result has yet been obtained onoverall policy coordination, with countries following divergent monetary,fiscal and exchange rate policies. Clearly, those policies reflect notonly policymakers' divergent objectives, but they also show diverse social,political and economic conditions in each country. For example, given thepolitical difficulties in raising revenues, Guatemala has generallypreferred to follow contractionary domestic policies by cuttingexpenditures to confront short-term financial difficulties in the recentpast. Costa Rica, on the other hand, has opted to increase revenues forthe same purpose. Furthermore, management of the exchange rate has notbeen coordinated among member countries. Frequent changes in exchange ratemanagement coupled with the development of parallel markets has made policycoordination difficult.

20. Seventh, to speed up development in the Region and, particulLrly,to help Honduras (the country perceived not to benefit from integration inthe Customs Union) a Regional Development Bank, CABEI, was established.But, financial difficulties did not permit CABEI to play the role envisagedfor it since its inception. A study underway in the World Bank for CABEIwould presumably propose a plan of action to help promote an equitabledistribution of the development effort in the Region.

-7-

21. Eighth, no legal body was created to monitor compliance with therules of the Customs Union. Lastly, each country preferred to set its owndomestic policies, sometimes at cross purposes with the policies of therest of the member countries. The end result of all these policies hasbeen a we&kened Customs Union.

22. The following attributes are needed for a well-functioning commo.zmarket:

(i) The net effect of trade creation should outweigh tradediversion;

(il) large imbalances in intra-trade should be avoided throughthe use of appropriate domestic policy instruments as wellas by the appropriate use of the exchange rate;

(iii) indirect taxes on domestic transactions should beharmonized among member countries;

(iv) all charges .n imports, except the common external tariff,should be eliminated;

(v) The CACM common external tariff should also coveragricultural products and should be the only means ofimport protection, while quantitative import restrictionsishould be phased out;

(vi) All CACM countries should make an effort to coordinatetheir domestic policies and the management of theirexchange rates;

(vii) CABEI should be revitalized to help the developmenteffort, especially for countries with weakerinfrastructures;

(viii) a legal framework for the functioning of the system has tobe prepared and put into place to ensure compliance withthe rules of the Common Market; and

(ix) all countries should accept the fact that integration to aComn:on Market implies a partial surrender of theirnational sovereignty in determ3ning domestic policies.

III. HARMONIZATION ISSUES

23. Harmonization of a tax system implies uniformity in taxes, basesand rates as well as compatibility in tax structures. Harmonization oftaxes is an essential component of any common market. While uniformity oftaxes is desirable in intercommodity relationships, this is not the case ininter-country relationships. As the example of the EEC indicates, a CommonMarket can function with different tax rates. In Central America, CACMmember countries aimed at harmonizing only import tariffs and some fiscalincentives at the inception of the Common Market in 1960. Ov.!r time,member countries began to restrict regional trade as well, applyingdifferent tariff rates on some products traded with third countries through

- 8 -

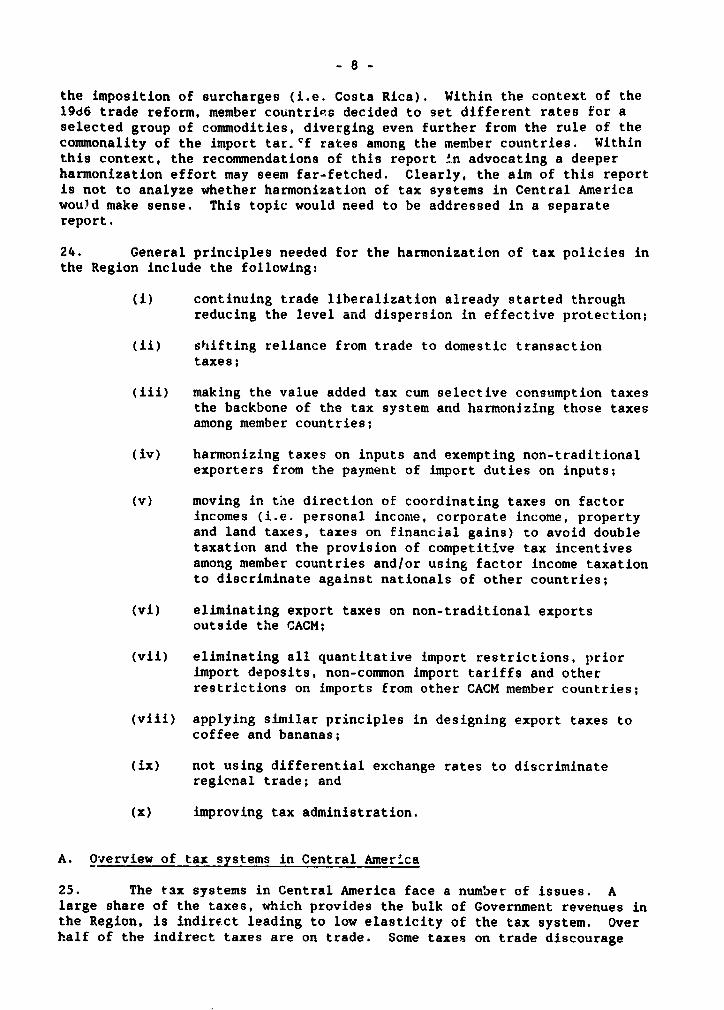

the imposition of surcharges (i.e. Costa Rica). Within the context of the19d6 trade reform, member countrips decided to set different rates for aselected group of commodities, diverging even further from the rule of thecommonality of the import tar.Cf rates among the member countries. Withinthis context, the recommendations of this report !n advocating a deeperharmonization effort may seem far-fetched. Clearly, the aim of this reportis not to analyze whether harmonization of tax systems in Central Americawould make sense. This topic would need to be addressed in a separatereport.

24. General principles needed for the harmonization of tax policies inthe Region include the following:

(i) continuing trade liberalization already started throughreducing the level arnd dispersion in effective protection;

(ii) shifting reliance from trade to domestic transactiontaxes;

(iii) making the value added tax cum selective consumption taxesthe backbone of the tax system and harmonizing those taxesamong member countries;

(iv) harmonizing taxes on inputs and exempting non-traditionalexporters from the payment of import duties on inputs;

(v) moving in tie direction of coordinating taxes on factorincomes (i.e. personal income, corporate income, propertyand land taxes, taxes on financial gains) to avoid doubletaxation and the provision of competitive tax incentivesamong member countries and/or using factor income taxationto discriminate against nationals of other countries;

(vi) eliminating export taxes on non-traditional exportsoutside the CACM;

(vii) eliminating all quantitative import restrictions, priorimport deposits, non-common import tariffs and otherrestrictions on imports from other CACM member countries;

(viii) applying similar principles in designing export taxes tocoffee and bananas;

(ix) not using differential exchange rates to discriminateregional trade; and

(x) improving tax administration.

A. Overview of tax systems in Central America

25. The tax systems in Central America face a number of issues. Alarge share of the taxes, which provides the bulk of Government revenues inthe Region, is indirect leading to low elasticity of the tax system. Overhalf of the indirect taxes are on trade. Some taxes on trade discourage

-9-

exports. Large price fluctuations make the system highly vulnerable toex.ogenous shocks. Variability in receipts makes it difficult for theauthorities to plan public expenditures. Most taxes have high rates, butnarrow bases. Unttil recently, most excise taxes were also specific,leading to reduced collection as domestic inflation rose. In fact,domestic inflation has eroded collection from specific taxes dramaticallyin the last eight years. Furthermore, a large number of exemptions undermost taxes are unnecessarily high and hence they reduce the taxable incomebase and necessitate higher rates on reduced bases. Another issue is theinefficient collection procedures which result in considerable losses offiscal revenues. As there is a large discrepancy between statutory andeffective tax systems, the tax collection effort in Central America leavesmuch to be desired.

26. There are other problems. First, the existence of a large numberof nuisance taxes increases the cost of collection while not yielding muchrevenue. Second, there are a r.umber of taxes on the same base, creatingdistortions and reducing the efficiency of tax administration. Third, somerevenues are earmarked to be spent in predetermined ways for pre-determinedagencies, reducing the flexibility in assigning budgetary resources.Fourth, frequent changes in the tax systems create uncertainty.

27. Some observations can be made base on an examination of changes inratios of main categories of taxes as a share of GDP during 1982-87.First, two countries--Costa Rica and Honduras--raised their tax ratiosduring the period through increasing taxes on domestic transactions andintroducing additional surcharges on imports. Second, the reliance onincome taxes do not show any correlation with the levels of income. Thepoorest country in the Region, Honduras, collects three times as muchrevenue--as a share of GDP--from income taxes than Guatemala. Third, it isimportant to note the dismal impact of the tax reform introduced inGuatemala in 1983 on tax revenues. This underscores the need to ensurethat any rationalization effort should respond to the need for generatingsufficient levels of revenues. In fact, despite the coffee boom in 1986,tax revenues as a share of GDP in Guatemala were lower in 1986 than in1982--a year before the introduction of the reform. Fourth, thesubstantial impact of coffee prices on tax revenues can be observed in ElSalvador during 1986-87. As coffee prices declined in 1986, the drop incoffee revenues of about 3? of GDP caused the tax ratio to fall from 13.1Zin 1986 to 9.7Z in 1987.

28. Tax Ratios. Table I shows tax ratios (tax revenues/GDP) for allCentral American countries for a few selected years. As the tableindicates, rates range from 5.62 of GDP in Guatemala in 1984 to 16.2Z inCosta Rica in 1985. In fact, tax ratios in Guatemala and El Salvador aretwo of the lowest in the Western Hemisphere.

29. As countries develop, tax bases grow more than proportionatelythan the growth of income. Other factors such as the level of urbanizationfacilitates tax collection. Hence, tax ratios should increase over time.It is important to note that each country in the Region feels pressure toraise different levels of revenues based on their levels of publicexpenditures, their possibilities of financing deficits as well as the

- 10 -

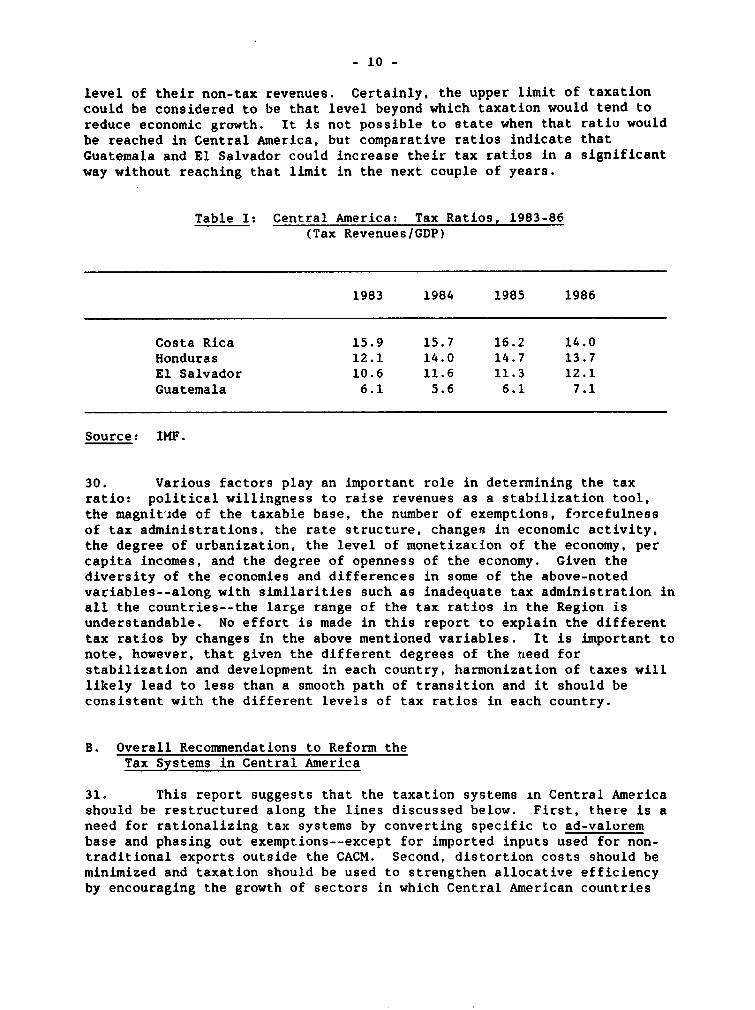

level of their non-tax revenues. Certainly, the upper limit of taxationcould be considered to be that level beyond which taxation would tend toreduce economic growth. It is not possible to state when that ratio wouldbe reached in Central America, but comparative ratios indicate thatGuatemala and El Salvador could increase their tax ratios in a significantway without reaching that limit in the next couple of years.

Table I: Central America: Tax Ratios, 1983-86(Tax Revenues/GDP)

1983 1984 1985 1986

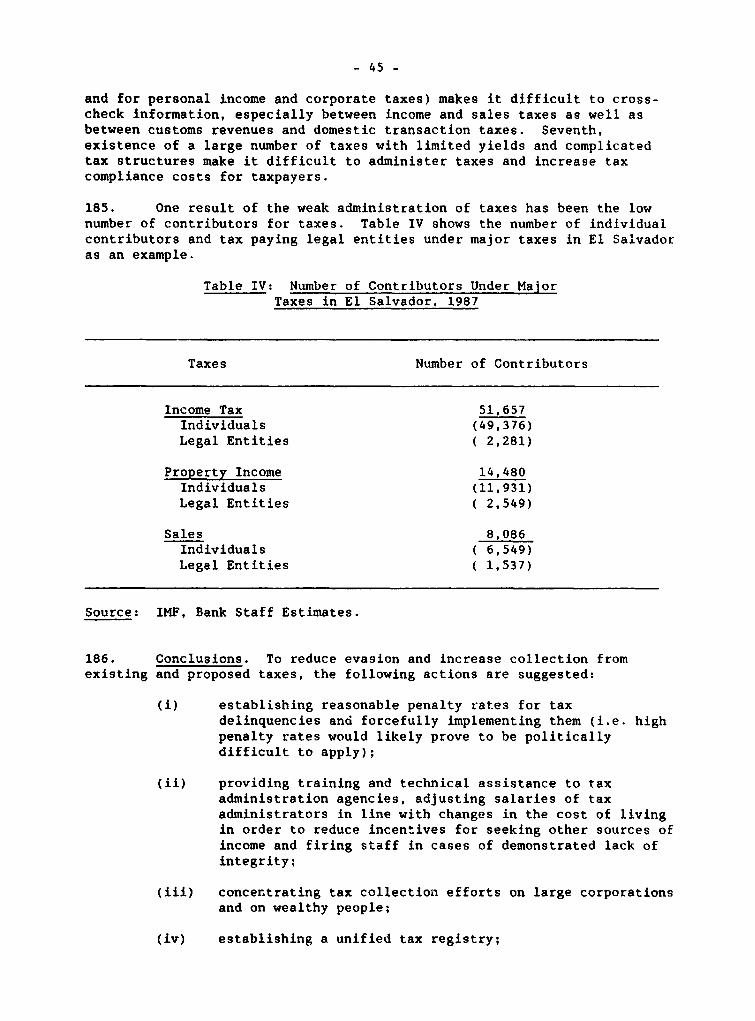

Costa Rica 15.9 15.7 16.2 14.0Honduras 12.1 14.0 14.7 13.7El Salvador 10.6 11.6 11.3 12.1Guatemala 6.1 5.6 6.1 7.1

Source: IMF.

30. Various factors play an important role in determining the taxratio: political willingness to raise revenues as a stabilization tool,the magnitide of the taxable base, the number of exemptions, forcefulnessof tax administrations, the rate structure, changes in economic activity,the degree of urbanization, the level of monetization of the economy, percapita incomes, and the degree of openness of the economy. Given thediversity of the economies and differences in some of the above-notedvariables--along with similarities such as inadequate tax administration inall the countries--the large range of the tax ratios in the Region isunderstandable. No effort is made in this report to explain the differenttax ratios by changes in the above mentioned variables. It is important tonote, however, that given the different degrees of the need forstabilization and development in each country, harmonization of taxes willlikely lead to less than a smooth path of transition and it should beconsistent with the different levels of tax ratios in each country.

B. Overall Recommendations to Reform theTax Systems in Central America

31. This report suggests that the taxation systems in Central Americashould be restructured along the lines discussed below. First, there is aneed for rationalizing tax systems by converting specific to ad-valorembase and phasing out exemptions--except for imported inputs used for non-traditional exports outside the CACM. Second, distortion costs should beminimized and taxation should be used to strengthen allocative efficiencyby encouraging the growth of sectors in which Central American countries

- 11 -

have an apparent comparative advantage. The reliance of the tax systemsshould also be shifted from production to consumption-based taxes. Fourth,administrative costs should be reduced. Any revision in the tax systemshould aim at reducing collection costs as well as compliance costs fortaxpayers. For example, it is not desirable to design complicated taxes,which would lead taxpayers to rearrange their financial affairs in such away as to avoid payment of trxes. Hence, effective tax systems should beapproximated to statutory systems. Fifth, changes should be designed toprovide progressivity to the tax system in order to ensure vertical equityto the extent possible. Sixth, a large share of total tax revenue shouldbe derived from few taxes and tax rates. Seventh, structural rigidities intax systems, such as the practice of earmarking of revenues for particularuses or groups. should be phased out. Lastly, frequent changes in the taxsystem should be avoided.

32. As discussed earlier in the report, tax ratios, with the exceptionof Costa Rica, are low in the Region. Two obvious options to increase theratio would be to improve collection and phase out most exemptions.Furthermore, there is scope for increasing revenues on imports andconsumption. Through these efforts, taxable income could be approximatedto its potential base. However, it is important to note that tax increasesshould not be recommended unless there are worthy expenditures. Otherwise,the supply side effects of higher taxes may have a welfare cost thatexceeds the welfare gains of higher expenditures.

33. Regarding minimizing distortions, the most significant issuerelates to trade taxes as discussed in the rest of this report.Particularly, a reduction in effective protection through further tariffreform is discussed. A decrease in exemptions and deductions is alsoneeded to avoid applying higher rates on the remaining lowered bases.Furthermore, shifting the reliance from production to consumption taxeswill be needed to decrease disincentives to work and reduce variability inreceipts. Lastly, payroll taxes need to be minimized to avoid discouragingemployment and output. Efficiency, on the other hand, could be encouragedby low marginal tax rates.

34. Overall obiectives of a taxation system. Any action plan torationalize the tax systems in the Region should aim at the following:

(i) generating adequate government revenues;(ii) minimizing adverse effects on incentives and distortions

and encouraging resource allocation based on comparativeadvantage;

(iii) encouraging efficiency, output and employment growth aswell as savings; and

(iv) reducing variability in collection to provide betterprogramming of expenditures and to avoid a sharp increasein public sector deficits when terms of trade worsen.

- 12 -

C. Structure of Taxes

1. Indirect Taxes.

1.1. Taxes on International Trade

35. Empirical investigations show that taxes on foreign trade accountfor 5.6Z of GDP and over one-third of total tax revenues in developingcountries. In fact, import duties comprise the most important taxable basein developing countries, given that they do not require a verysophisticated tax administration. In open economies, such as those inCentral America, the significance of taxes on foreign trade is larger(Table II). However, the significance of taxes on trade should declineover time as the share of taxes collected on domestic transactions in GDPincreases.

Table II: Share of Taxes on International Tradein Total Central Government Revenues, 1975, 80, 84

(2)

1975 1980 1984

World 4.8 5.1 4.4Industrial Countries 1.8 1.5 1.4Developing Countries 14.1 16.1 14.0Non-Oil DevelopingCountries 15.5 17.4 14.6

LAC 10.8 14.4 8.3Asia 19.5 20.1 20.1

Source: IMF, UNDP.

1.1.1. Import Tariffs

36. Empirical investigations show that import duties contribute about4.52 of GDP and over one-fourth of total tax revenues in developingcountries, although there is considerable variation in their reiativeimportance among the countries. It is also a known fact that all the greatusers of taxes on imports make little use of taxes on domestic transactionsand conversely virtually all the great users of domestic transaction taxeson goods and services make lit.le use of import duties.

37. Import tariffs are used mostly to generate revenue. But thosetaxes are also utilized to provide protection to domestic industries,reduce imports and discourage consumption.

38. In open economies, high tariff protection could result in themisallocation of resources in the economy. Resources could move into

- 13 -

sectors in which countries do not have a comparative advantage.Furthermore, during balance of payments crises, tariffs could also be usedas a substitute for devaluation and hence help postpone needed adjustmentefforts.

39. The CACM framework establishes the import tariff regime. Thisframework consists of a Common External Tariff (CET) on imports fromcountries outside the CACM, while exempting import duties for regionaltrade. The rate structure is complex and is based on the principle ofmade-to-measure protection by assigning higher nominal rates to regionallyproduced goods.

40. Previous studies conducted for the countries in the Region haveindicated that prices of importables have been higher than their domesticequivalents, showing the impact of trade protection. Furthermore, tariffshave been used as an instrument for protecting the balance of payments.For example, the San Jose protocol surcharge was established by all theCACH countries (i.e. equal to 30% of the Common External Tariff) in 1975when the Region was facing acute balance of payments difficulties. Thesesurcharges also helped raise revenue to compensate for the reduction intariff revenues from imports--caused by the introduction of incentivepolicies of the CACH. Additionally, Costa Rica and Honduras set up highsurcharges on imports in the early 1980s, when terms of trade for theRegion worsened.

41. The rate structure is designed to provide protection to regionallyproduced goods. First, higher rates are applied to final consumer goods.Second, lower rates are assigned to intermediate and capital goods, withrelatively higher rates on regionally produced intermediate and capitalgoods. Third, generous tax exemptions are provided for non-regionallyproduced raw materials, intermediate and capital goods. Some "essentialgoods" (i.e. wheat) are either exempt from the payment of import duties orare taxed at low rates.

42. Before the introduction of the reform on January 1, 1986, CETincluded both an ad-valorem and a specific component. With increasinginternational inflation, the specific component of the import tariffsdeclined over the years. Following the introduction of the reform of thetariff regime, all rates on imports were converted into ad-valorem rates.

Issues

43. Honduras is not a legal member of the CACM. It left the CustomsUnion after a war with El Salvador in 1967. Since then, it has traded withthe other CACH members mostly on the basis of bilateral treaties. Beingthe least developed country in the Region, Honduras has demanded specialfavors from other CACM members.

44. As the Region began to face balance of payments difficulties, eachcountry introduced restrictions on their trade, including trade within theCACM. First, following the overvaluation of currencies after 1981,parallel markets for foreign exchange developed in most of these countries.Quantitative restrictions on imports were established, while foreignexchange restrictions were intensified. Costa Rica also imposed surchargeson imports and Honduras raised import surcharge rates.

- 14 -

45. Costa Rica's surcharges on imports served several purposes. Thoseon inputs and capital goods (2Z - 52 - 10Z) and low rates on final consumergoods (12.5X) were designed for revenue purposes. Higher rates on finalconsumer goods (402 - 50?) were designed to provide protection forregionally produced goods, while higher rates on final consumer goods (i.e..OOZ and 2002 in 1984) were intended to reduce or avoid imports.

46. Nicaragua's new econemic direction after 1980 presents achallenge. Since the country switched to a centrally managed economy, thesignificance of tariffs in resource allocation and 1i regulating tradebecame irrelevant. As the country faced enormous balance of paymentsdifficulties, cther CACM member countries reduced their trade withNicaragua to low levels to ensure that their creditor balances do notincrease further as discussed earlier in this report.

47. Countries in the Region have not harmonized their import regimesfor basic grains. In fact, most countries maintain quantitative importrestrictions on the importation of basic grains.

Results of high import protection

48. High import tariffs on final consumer goods coupled with low rateson non-regionally produced intermediate and capital goods led to higheffective protection rates for industrial products. Quantitativerestrictions on imports of basic grains also resulted in high effectiveprotection for basic grains. Furthermore, dispersion in nominal rates ledto even larger dispersion in effective rates.

49. High effective protection rates led to a number of results.First, it resulted in misallocation of resources by stimulating the growthof sectors in which the countries in the Region do not have an apparentcomparative advantage. Even, some activities with low value added werecreated, indicating inefficiency and waste. Most domestic prices have beenwell over their international price equivalents. Furthermore, the grantingcf exemptions on imports encouraged high capital and import-intensity inmanufacturing and favored the creation of low employment generating jobs,aggravating the already serious unemployment problems in these countries.

50. The implementation of the tariff regime also led to an expansionin the share of industry in the economy. Before the CACM was created,industry accounted for a small share of GDP in all the countries in theRegion. Following the creation of the Common Market, however, this sharerose considerably. The sub-sectors which developed rapidly were mostlyfinal consumer goods, in which CACM countries presumably have comparativeadvantage. However, high effective protection provided to industry did notcreate incentives for firms to become internationally competitive. Importsubstitution in final consumer goods should not create a chronic deficit inthe trade balance since input imports are generally smaller than outputimports. As industry developed and regional imports were exempted from thepayment of tariffs, regional trade also grew substantially. It nowaccounts for a little less then one-fifth of total exports in the Region.

51. Since the new industries which developed in response to thegranting of new incentives relied heavily on the importation of

- 15 -

intermediate and capital goods, import intensity in all the countries rosesubstantially. This created a rigidity in the balance of payments, sincereduction in imports--during a balance of payment crisis--depresses outputand employment. Furthermore, heightened import intensity in industry ledto a chronic deficit in the trade balance of the industrial sectors in theRegion, making it difficult to adjust to external shocks.

52. The implementation of the regional tariff regime also had asignificant impact on the structure of imports. Following the creation ofthe CACH, and the consequent sharp growth in the industrial sector--mostlyin final consumer goods--the share of consumer goods in total imports fell,while the share of intermediate and capital goods imports rose.

53. Trade policies pursued so far have been successful in stimulatingindustrial development based otl regional import-substitution. By theearly 1980s, however, the possibilities for further efficient import-substitution have been virtually exhausted. For example, the production ofmany consumer goods industries was limited in Costa Rica before it joinedthe CACM. By 1980, however, imports fell to about one-tenth of totalsupply in many consumer goods industries, such as in food products,beverages, tobacco, clothing and furniture.

54. The anti-export bias of the trade regime. The protection systemdiscourages the growth of exports. The regional tariff regime created asignificant bias against exports to markets outside the CACM in general andagainst export agriculture in particular, where the Region's comparativeadvantage lies. For example, in Costa Rica, effective protection providedto regional import substitution activities averaged about 126% in 1982compared to 15% for non-traditional exports to markets outside the CACM.As a result, the growth of non-traditional exports outside the CACM wassluggish in the past. Compared with other small sized developing countriessuch as Hong Kong and Singapore, growth of non-traditional exports was veryslow in the recent past.

55. The tariff regime also led to an erosion of the tax base onimports. First, imports from other CACM countries were exempted fromduties. Second, generous tariff exemptions were granted to intermediateand capital goods. These exemptions led to large fiscal losses, averagingabout 52 of GDP a year for some countries in the Region. Third,prohibitively high tariffs on final consumer goods also reduced fiscalrevenues by limiting the growth of imports.

Progress in import liberalization

56. After having remained unchanged since the inception of the CommonMarket, Central American countries took an initial step in rationalizingtheir trade policies and in beginning to reduce the anti-export bias intheir trade strategy by introducing a new regime on January 1, 1986. Thesereforms were supported by a US$80.0 million SAL I Loan by the World Bank toCosta Rica. Costa Rica took further and stronger steps in importliberalization during the Second Tranche disbursement of SAL I byeliminating import surcharges on final consumer goods. Costa Rica plans tocontinue to reforis its trade regime and reduce the level and dispersion ineffective protection in the next several years. The World Bank is

- 16 -

supporting these positive efforts of the Costa Rican authorities through aUS$100 million SAL II operation. Although the reforms, both implementedand planned, are in the right direction, there is a long way to go inachieving a fully satisfactory liberalized trade regime in the Region.This report suggests targets to be achieved to eliminate the anti-exporLbias in the trade regime of the Region within a Common Market. Thesuggested policies could well be introduced by one or several countries orthey could be adopted by all the Common Market members. Although it isdesirable that these policies be adopted by all the members, if thenegotiations for reaching a common understanding fail to materialize, theneach member would obviously weigh the costs and benefits of staying in theCommon Market versus taking a unilateral action. This report does not dealwith the strategy of introducing reforms in the Region, but it favors ajoint action.

57. Because of the importance of the tariff reform supported under theSAL I operation for Costa Rica, the following describes the progressachieved in the liberalization of trade:

(i) eliminated all specific rates in nominal tariffs andconverting them to ad-valorem rates;

(ii) converted the classification system for goods from theCentral America classification system (NAUCA) to theBrussels nomenclature;

(ii) terminated all tariff exemptions under the Central AmericanAgreement on Fiscal incentives;

(iv) abrogated the regional investment incentives and the SanJose Protocol (a 30Z surcharge on the common externaltariff; and

(v) created a Central American Council for tariffs and customswith authority to establish and modify import tariffswithout the need for legislative action by member countries.

58. In terms of the modification of rates, the Regional Treaty aimedat the following targets;

(a) goods produced outside the CACM (non-competing imports):

(i) essential final consumer goods, raw materials,intermediate and capital goods: a minimum 5 percentrate, and exemptions for goods which are considered tobe strategic for development on an exceptional basis;and

(ii) non-essential final consumer goods and inputs used inthe production of these goods: a 10 percent rate.

(b) goods produced within the CACM (competing imports):

(i) raw materials, intermediate and capital goods: a 10, 20or 30 percent rate, depending on the level ofprocessing; and

(ii) final consumer goods: a rate ranging from 35 to 70percent, with few exceptions for fiscal and balance ofpayments purposes up to and including 90 percent.

- 17 -

59. Since the effect of the planned regional tariff regime in loweringeffective protection was small, the Costa Rican Government agreed to gobeyond the regional agreement to further reduce effective protection byundertaking the following modifications to the regionally agreed rates:

(a) intermediate and raw material goods produced outside theCACM (non-competing goods): a minimum 10 percent; and

(b) capital goods: a minimum 20 percent.

To achieve these rates, the Costa Rican Government agreed to addthe indicated rates through import _urcharges:

(a) raw materials and intermediate goods (non-competing goods):a 5 percent rate; and

(b) capital goods: between a 10-15 percent rate.

60. Implementation of tariff reform. Based on regional negotiations,the following rate structure emerged:

TABLE III: COMPARISON OF OLD TARIFF REGIME, NEW TARIFF REGIMEAND PLANNED REGIME

(z)

Old New 1/ PlannedRegime Regime Regime

Max. Avg. Max. AvR. Avg.

Final Consumer GoodsRegionally Produced 530.2 92.5 143.0 65.I 32.6Non-Regionally Produced

Essential 130.3 40.6 65.5 15.2 5.4Non-Essential 314.2 135.0 253.0 18.4 34.0

Intermediate Goods and Raw MaterialsRegionally Produced 1393.4 54.3 203.0 34.1 20.9Non-Regionally Produced 332.8 32.6 108.0 11.2 5.0

Capital GoodsRegionally Produced 248.5 73.9 153.0 35.6 24.7Non-Regionally Produced 73.0 23.7 28.0 15.1 5.5

1I The two rows indicate the planned rates as of January 1, 1986. Some ofthe parametes might likely have changed since then, as Costa Rica modifiedsome surcharge rates.

Source: SIECA, Central Bank of Costa Rica, Bank Staff Estimates.

- 18 -

61. The initial reform reduced effective protection and its dispersionin a modest way. The decrease ill effective protection resulted mainly fromthe introdiction of import duties on raw materials, intermediate productsand capital goods. The impact of the reduction in high legal tariff rateson lowering effective protection was limited. Increases in tariffs forcompeting raw materials, intermediate and capital goods raised effectiveprotection for these goods.

62. The structure of protection remained similar to the previousregime. Rates for final consumer goods are still high and rates forintermediate and capital goods are low ar.d are exempted under nationalincentive schemes as compared to the regional one prior to the reform.

63. Member countries could not agree on common rates for some of therates (Part II of the new tariff schedule). This category of productsincludes .ostly textiles, clothing and paper. Rates for some of theseproducts were actually raised under the new system, leading to increasedeffective protection. These products were heavily protected under theprevious tariff regime and are important in relation to domesticproduction. It is essential that rates for these products be unifiedwithin the overall target rates in the next stages of the tariff reform.

64. Member countries agreed to set rates for some products (Part IIIof the new tariff schedule) on a national basis. This agreement broke thecommon external tariff concept for this category of goods. The main itemin this group is petroleum.

65. The Costa Rican Government phased out surcharges on final consumergoods during SAL I - Second Tranche negotiations, reducing effectiveprotection. But, the Government also decreased surcharges on intermediateinputs and capital goods, increasing effective protection after the SecondTranche of the SAL I was disbursed.

66. The net impact of the tariff reform in 1986 on reducing effectiveprotection should be explored in more detail. The preliminary evidenceshows that the reform reduced only the water in the tariff, while effectiveprotection was increased for some products, which were heavily protectedbefore the reform.

67. To improve resource allocation as well as to harmonize taxes onimports, it is essential that tariffs not be used as an instrument toprotect the bala.nce of payments and hence tariff-like surcharges should notbe imposed on top of regional tariffs.

Targets for tariff reform

68. There is a need for specifying targets to be achieved for the nextfew years to reduce effective protection. Owing to difficulties indecreasing tariffs in one step, a staged approach is suggested. The nextstage of the reform would need to aim at reducing the highest tariff rateto 40Z, while increasing the lowest tariff rate to 20Z. The increase inthe lowest rate would not only help reduce effective protection, it wouldalso generate government revenues. However, the lowest tariff should notbe allowed to increase much further than the suggested 20? rate since

- 19 -

raising low tariffs on intermediate products and capital goodsdiscriminates against exports by raising the anti-export bias of theincentive system and results in an appreciation of the exchange rate.

69. If the increase of the lowest rate to 20Z is not politicallyfeasible, then a reduction of the highest rate is vital for decreasingeffective protection in a meaningful way. Without raising the lowesttariff rate, a reduction in tariff rates on final consumer goods would notlead to a significant decrease in overall effective protection rates.Obviously, the above-mentioned targets could be modified to take intoaccount the political difficulties in raising the floor rate. This couldbe achieved by scaling down the highest rate to 302. Likewise, maintainingthe present 52 floor rate would be consistent with a highest tariff rate of252. Clearly, it is desirable to establish a higher minimum rate to ensurethat changes in tariff rates would not lead to reduced government revenues.In case politically viable options rule out raising the floor tariff rateover 52 and fiscal revenues decline, then authorities in the Region willneed to raise other revenues to compensate for the fall in revenues fromimports. Raising selective consumption taxes or increasing the rate of thevalue added tax would be options to consider.

70. Agreement on a politically viable target floor tariff ratepresents a number of problems. First, imported inputs used in producingnon-traditional exports would need to be exempted from payment of duties.It is vitally important to exempt the export sector from payment of dutiesto ensure that it purchases inputs at world market prices. It is importantthat all the countries in the Region tollow these principles to avoidcreation of any disadvantage to any particular country, providingexemptions.

71. Second, the minimum rate on capital goods should be high enough toencourage employment of labor in view of the underpricing of capital andthe need to encourage firms to use domestic inputs by making these inputscheaper compared to domestically available inputs, but low enough to ensurereactivation of the economies through high levels of investment. Third,since the Region does not possess an apparent comparative advantage in theproduction of most capital goods and intermediate goods, it is importantnot to provide excessive protection to these goods. This is especiallyimportant if these products are used as inputs to non-traditional exportsto markets outside the CACM. Those products would need to be produced at ahigh quality if they are to be produced domestically and used in exports asinputs. In any case, countries should provide exemptions on regionallyproduced inputs if they are utilized in manufacturing exports outside theCACM. Fourth, given the large share of these products in total imports aswell as in GDP, they provide a good taxable base. Exempting them fromimport taxes would unnecessarily lead to large reductions in potentialtariff revenues.

72. Fifth, it may also prove to be difficult to reduce higher rates,hence an increase in the floor rate is needed to reduce effectiveprotection. Sixth, since at the final phase of the tariff reform, ratesshould be unified, unification at the minimum rate of 52 does not seem tobe realistic. Therefore, the minimum rate will need to be raised in laterstages of the tariff reform if unification is to be achieved. Hence, thisparagraph underscores the need for establishing a floor tariff rate of atleast 102 (which indicates that the highest rate should be no more than

- 20 -

302). Seventh, no other non-distortionary revenue source could match themagnitude of revenues which could be collected from this source. Eighth,taxing imports of intermediate and capital goods used in the manufacture ofgoods sold in the regional market will increase the relative profitabilityof non-traditional exports outside the CACM, which will be exempted fromsuch duties under various drawback schemes discussed in this report.Lastly, sustainability of a trade reform hinges on maintaining financialstability. To the extent additional revenues, which could be collectedthrough raising the import tariff floor rate, compensate for the fall inrevenues caused by the tariff reduction and help maintain macro-financialstability, they would contribute to the sustainability of the tariffreform.

73. Regarding the highest tariff rate, it is important to note thatsome exceptions to the rule could be accepted on infant industry protectiongrounds. But the principle of harmonization indicates that the rate shouldbe set on a regional basis, be applied to few commodity groups for adefinite time period. If these exceptions are provided to non-competitiveproducts and for long periods of time, the benefits from tradeliberalization will not likely be obtained. In this context, it isimportant to note that most countries in the Region still prefer to providehigh protection to inefficient industries such as textiles and footware forat least the next few years. This report suggests that this policy bereversed and trade liberalization for this group of products beaccelerated.

74. Another issue regards the preference of the countries to taxluxury imports through high tariffs or surcharges on imports. These ratescould encourage the development of domestic industries producing suchgoods. This report suggests that these imports be taxed through domestictransaction taxes, which would be levied on both d3mestic and importedgoods at the same rates.

75. Intermediate goods. Considering that tax rates or. intermediateproducts would be increased, those goods may require some do-gree ofprotection after the introduction of further stages of the tariff reform.However, additional protection to be granted to intermediate goods has tobe reviewed carefully on a product-by-product basis to ensure thatinefficient production of these goods not be given undue encouragement.

76. Complementary exchange rate policies. Implementation of an activeexchange rate policy during a period of reduction of high tariffs onconsumer goods would be needed to ensure that the trade balance in thebalance of payments not deteriorate unnecessarily. To achieve a realdepreciation, however, the authorities in the Region should drasticallyreduce or eliminate public sector deficits. Otherwise, real devaluationcoupled with domestic financing of high public sect:or deficits--given thatexternal financing is limited--would likely lead to inflationary pressuresand would not permit an improvement in the trade account of the balance ofpayments.

- 21 -

Sustainability of tariff liberalization efforts

77. The World Bank has released interim conclusions os a study onlessons to be derived from trade liberalization episodes based on a studyof various countries. According to this study, some resource-poor andsmall countries have undergone successful trade liberalization efforts.Since Central American countries fit well into this category of countries,it can be inferred that being small and resource-poor should not precludeany of the countries in the Region from undertaking a successful tradeliberalization program. The main conclusions for the successfulliberalization episodes include the following:

(i) maintaining a depreciated exchange rate in real terms;

(ii) having a low budget deficit;

(iii) achieving favorable export performance;

(iv) being implemented under extreme duress;

(v) introducing strong reforms ("strong liberalization attemptstend to be sustained. These are mostly episodes whichstart with significant, rather than minor and marginalsteps of liberalization"); and

(vi) maintaining political stability.

78. This report does not analyze to what extent the conditions incountries in Central America fit into the criteria deemed to be desirablefor achieving and sustaining a successful trade liberalization effort.However, it is important to note that further changes in tradeliberalization should be strong to lead--presumably--to robust exportgrowth--through eliminating the anti-export bias of the trade regime--needed for the survival of the reform efforts.

Revenue implications of a tariff reform

79. This report suggests that the next steps in the tariff reformwould need to take account of revenue implications of the reforms.Assuming that both the exchange rate and import volumes remain unchangedfollowing trade liberalization, reductions in tariffs on final consumergoods would lead to a loss in fiscal revenues by the amount of the decreasein tariffs. If the reform also includes an increase in the floor rate,revenues would likely increase. Given the share of intermediate andcapital goods in total imports and depending on the amount of the increasein the floor rate, overall tariff revenues would likely expand. However,if import volumes respond to changes in tariff rates, fiscal revenues couldincrease slowly, given that price sensitive category of capital goods andsome intermediate goods would likely decline if tariff rates are increased.Expansion in final consumer goods imports, however, could offset the ratedecline proposed for final consumer goods. If a real devaluationaccompanies the tariff reform, then tariff revenues could increase, despitelower volumes and lower rates on final consumer goods.

- 22 -

80. Assuming that the tariff reform does i,et include an increase inthe floor rate, then the impact of the tariff reform on fiscal revenueswill likely be negative. In the absence of a real devaluation, a declinein high rates wouid lead to a decrease in tariff revenues, while a volumeincrease would expand it. A real devaluation would lead to an expansion infiscal revenues in domestic currencies, but the final impact depends onchanges in import volumes and in tariff rates.

1.1.2. Export taxes

81. In general, the structure of production and exports is a majordeterminant of the tax structure. This is especially important, regardingthe choice of corporate income taxes and export taxes. Empiricalinvestigations of tax structures of developing countries indicate thatcountries which rely heavily on export taxes make little use of corporateincome taxes and vice versa.

82. Empirical investigation of developing countries also indicatethat, on average, export taxes generate 11% of tax revenue (1.7Z of GDP)for low income countries and less than 32 (0.52 of GDP) for middle incomedeveloping countries. The ratio of export taxes to exports is 11Z for thelow income groups and about 42 in middle income developing countries.

83. Export taxes account for a large share of fiscal revenues inCentral America. Because of the relative ease of administration, countriesin the Region rely on these taxes as a substitute for income tax. Theshare of these taxes in total Central Government revenues also correlatepositively with the share of exports in GDP. Since export growth is acritically important objective--badly needed to put the Region on asustainable growth path--care needs to be exercised in not overtaxingexports to the point at which export growth is discouraged.

84. Taxation of exports shows differences according to commoditygroups. It is mostly concentrated on traditional commodities, andspecifically on coffee and bananas. Those two commodities provide the bulkof revenues from exports. Exports to CACM are exempted from taxation asnoted earlier in this report. Similarly, non-traditional exports outsidethe CACH are either not taxed or taxed at low rates.

Conclusions

85. It is desirable to implement common principles regarding exporttaxation. However, there is no point in harmonizing these taxes among themember countries. Taxes on coffee exports are discussed in the followingsection. In the short-term, taxes on banana exports should be maintainedas a substitute for income taxes. However, care needs to be exercised toensure that tax rates are maintained at the same or similar levels and atad-valorem rates, and that their levels are set in such a way that they arenot permitted to discourage exports. Since marketing for banana exports isin the hands of the large multinational corporations in the Region, someform of taxation as a proxy for income tax would be useful. However,taxation of these companies has to take note of the circumstances of theinternational banana market and the possibility of banana companies leavingCentral America to other countries which do not have a similar tax burden.

- 23 -

Regarding taxation of non-traditional exports, it is strongly recommendedto eliminate any tax which might exist in any country in the Region, giventhe urgent need to encourage the growth of these exports. In fact, taxingnon-traditional exports coupled with granting of incentives for the samecategory of goods doed not make sense.

1.1.2.1. Taxes on coffee exports

86. Coffee has a significant impact on the economies in CentralAmerica. The five countries of the CACM are, as a group, one of thelargest coffee producers in the world. Since these economies arerelatively small, the coffee sector plays a key role in each of thosecountries. All the countries in the Region produce and export coffee. TheCoffee sector accounts for a significant share of fiscal revenues andexport earnings ir. all the countries in the Region. The degree ofdependence of each country on foreign exchange earnings from coffee,however, is different.

87. There are various reasons for the importance of export taxes oncoffee. First, coffee exports, as mentioned earlier, account for animportant share of GDP in all the countries in the Region. Second, thesector hardly pays any income tax, and hence export taxes can be consideredas a substitute for income taxes. Third, low collection costs and easyadministration of the tax makes it an attractive instrument. Fourth, thestupply elasticity of exports is relatively low, with limited possibilitiesof diversification into other crops, at least in the short-term, while slowgrowth in international demand limits exports. As a result, taxation ofcoffee exports can be considered a second-best alternative to taxingincomes from export earnings.

88. Coffee exports need to be taxed as long as the InternationalCoffee Agreement (ICA) operates. Each country in the Region has adifferent set of taxes on coffee exports. These differences stem from:

(i) different levels of production costs in each country,resulting in varying levels of a tax-free threshold price;and

(ii) the particular method by which windfall profits are sharedbetween producers, exporters, and the public sector.

Conclusions

89. The design of a tax on coffee exports needs to take into accountthe large swings in the international price of coffee. Given theimportance of the commodity in the Region, a good macro management of boomsas well as reduced prices is crucial to avoid inflationary pressures in thecase of increases in coffee prices as well as recessions during drops incoffee prices. Taxation of coffee exports appears to be the most effectivetool to achieve the above-noted objectives. The Central American countriesshould be in a position to capitalize on and improve growth and debt-servicing prospects during windfalls. Poor management of booms hasgenerally led to over-consumption, with the public sectors starting or

- 24 -

expanding inefficient investments as well as increasing currentexpenditures. The experience of the counties during 1976-77 as well as in1986 are good examples of bad management of coffee booms. For example,Costa Rica undertook an ambitious public investment program and expandedcurrent expenditures while borrowing on a large scale. Conversely, hightaxes on coffee exports could accelerate the initial recessionary impact ofa drop in coffee prices.

90. An expansion in domestic demand following a boom in prices couldlead to a sharp increase in imports and hence a deterioration in thebalance of payments of these countries. However, if restrictive fiscal andmonetary policies are introduced, international reserves could bestrengthened, permitting a higher rate of domestic investment over thecoffee cycle while coffee prices return to normal levels.

91. If international coffee prices increase, authorities are facedwith various options. These include: (i) strengthening internationalreserves; (ii) reducing foreign liabilities; (iii) raising domestic capitalinvestment (i.e. public investment); and (iv) increasing current publicsector expenditures. This report suggests that part of the windfallrevenues should be saved to increase international reserves. To the extentthat capital expenditure programming is possible, increased capitalexpenditures is also recommended to utilize the windfall to enhancedevelopment. Given that price increases are generally temporary, however,care needs to be taken in planning these expenditures, including planningand budgeting for the current expenditure requirements for thoseinvestments.

92. The use of fiscal policies is more apprapriate than monetarypolicies in dealing with problems created by coffee booms. Following anincrease in coffee prices, liquidity in the financial system expands. Toabsorb the excess liquidity, authorities could either use monetary policyby increasing reserve requirements, reducing credit or they could usefiscal policies by introducing higher tax rates. In the latter case, thepublic sector would absorb part of the windfall.

93. Tight monetary policies would likely lead to large swings in theavailability of credit, whereas restrictive fiscal policies could be usedto stabilize economic activity through taxing part of the increasedrevenues. When prices rise, a part of the increase in internationalreserves would be transferred into a coffee stabilization fund.Conservely, when prices drop below a pre-determined level, fundsaccumulated in the coffee stabilization fund would be utilized. Hence, thefunctioning of the fund could help stabilize economic activity, limitexcessive increases in consumption, and permit a better use of financialavailabilities through helping to finance a carefully screened andevaluated investment projects.

94. Any tax on coffee exports should take into account the need toprotect production and employment in the sector. Hence, it is recommendedto exempt coffee exports from the tax when inteinational prices fall belowa pre-determined level. This level could be set above the highest cost ofproduction in each country. The coffee sector is generally labor-intensiveand wage costs and availability of labor varies in each country in CentralAmerica. As a result, unit production costs need to be taken into account

- 25 -

in establishing an export price below which exports will be exempted fromtaxes. In the case of Honduras, for example, average production cost perquintal (i.e. 46 kg.) was estimated by the Honduran authorities to be equalto 165.0 lempira (US$82.5 at the official exchange rate) in 1988. Hence,the World Bank Mission, which visited Honduras during January 1988,recommended a floor price for exemptions on taxes on coffee exportsequalling 180.0 lempira per quintal, to allow for a possible increase inthe cost of production in the next few years.

95. Regarding the structure of rates, it is recommended that beyond apre-determined export price (i.e. a high value, perhaps US$ 2.0 a pound), a50 tax rate be established on the price exceeding that limit. Thisstructure would permit the public sector to share windfall gains withproducers/exporters in equal proportions. It is to be noted that thefloor-ceiling prices for the price stabilization fund do not necessarilyhave to coincide with minimum and maximum tax rates.

96. There is no obvious reason to harmonize taxes on coffee exports inthe Region. Given the differences in unit cost of production, and thereliance of the tax system on these taxes (i.e. much more significant in ElSalvador compared to Costa Rica) and lack of interdependence among membercountries on coffee exports, a specific rate structure in each country doesnot necessarily have to be the same. However, the main principlesdescribed in this section of the report could be applied to all thecountries in the Region.