HAME510: Raising Capital: The Process, the Players, and … · positive NPV project that, to the...

76

Copyright © 2012 eCornell. All rights reserved. All other copyrights, trademarks, trade names, and logos are the sole property of their respective owners. 1 HAME510: Raising Capital: The Process, the Players, and Strategic Considerations

Transcript of HAME510: Raising Capital: The Process, the Players, and … · positive NPV project that, to the...

Copyright © 2012 eCornell. All rights reserved. All other copyrights, trademarks, trade names, and logos are the sole property of their respective owners. 1

HAME510: Raising Capital: The Process, the Players, andStrategic Considerations

Copyright © 2012 eCornell. All rights reserved. All other copyrights, trademarks, trade names, and logos are the sole property of their respective owners. 2

This course includes

Seven self-check quizzes

Three discussions

One tool to download and use on the job

One course project

Completing all of the coursework should take

about five to seven hours.

What you'll learn

View the process of raising capital

in a broad context regarding the

mix of capital and the process of

entering into capital markets

Understand why changes in the

industry and in the economy are

important to investment and

financing decisions in your

organization

Contribute to decisions in your

own firm more meaningfully with a

more complete understanding of

corporate restructuring, mergers,

acquisitions, and bankruptcy

Course Description

The capital projects your firm undertakes need to be funded. You need to know how to choose between debt and equity

funding and when to consider acquiring funds from capital markets. These outside funding sources will have their own

expectations for rates of return, and the cost of this funding is driven by a number of external factors such as the state of

Copyright © 2012 eCornell. All rights reserved. All other copyrights, trademarks, trade names, and logos are the sole property of their respective owners. 3

the economy and the industry.

Making sound capital budgeting and funding decisions is a vital part of your role as a manager, and this course

shows you how characteristics of capital markets impact the process and prospects of raising capital. We show

you how to observe external economic data and develop strategies to balance debt and equity at your firm and

how decisions regarding corporate restructuring, mergers, acquisitions, and bankruptcy are made.

These concepts, when put into action, will help ensure that you are maximizing the value of your firm using the correct

balance of debt and equity.

Steven Carvell Professor and Associate Dean for Academic Affairs, School of Hotel Administration, Cornell University

has taught finance courses at Cornell University since 1986. Professor Carvell is the co-author of Steven Carvell In the

(Prentice-Hall, Inc. Strebel, Paul and Steven Carvell, 1988). Carvell has worked for professionalShadows of Wall Street

money managers in applied strategy in the equity market and served as a consultant to the Presidential Commission on

the 1987 stock market crash. Professor Carvell has conducted numerous specialized Executive Education seminars for

some of the largest hotel companies in the world. Carvell holds a Ph.D. from the State University of New York,

Binghamton.

Scott Gibson Zollinger Professor of Finance, Mason School of Business, College of William and Mary

is the Zollinger Professor of Finance at the College of William and Mary Mason School of Business andScott Gibson

previously held academic appointments at Cornell University and the University of Minnesota. He holds a B.S. and Ph.D.

in Finance from Boston College. Prior to his academic career, he worked as an analyst with Fidelity Investments and as a

credit team leader serving Fortune 500 clientele with HSBC Bank. He's won outstanding teaching awards on numerous

occasions, including being named an outstanding faculty member in .BusinessWeek Guide to the Best Business Schools

Copyright © 2012 eCornell. All rights reserved. All other copyrights, trademarks, trade names, and logos are the sole property of their respective owners. 4

His finance research has appeared in top academic journals and has been featured in the financial press, including the

, , , , , and .Wall Street Journal Financial Times New York Times Barron's BusinessWeek Bloomberg

Start Your Course

Copyright © 2012 eCornell. All rights reserved. All other copyrights, trademarks, trade names, and logos are the sole property of their respective owners. 5

Module Introduction: Financing Choices and the Debt-Irrelevance Proposition

In this module, you will examine financing choices as well as some of the complex considerations that finance managers

take into account when they consider how best to raise capital. You will examine the question of how we think about the

optimal mix of debt and equity, and you will examine some of the types of financing that are available to firms, including

stock, preferred equity, and debt. You will have an opportunity to discuss some of your initial questions with your peers in

a discussion forum, and you will get to confirm your mastery of key learning points.

Copyright © 2012 eCornell. All rights reserved. All other copyrights, trademarks, trade names, and logos are the sole property of their respective owners. 6

1.

2.

3.

4.

5.

Read: The Assumptions of the Debt-Irrelevance Proposition

Key Points

The debt-irrelevance proposition: the value of a firm

is unaffected by its capital structure if certain

assumptions are true

It assumes we live in a world with no taxes

It assumes we have no direct or indirect financial

distress costs

To begin the examination of raising capital, let's explore a key theory. Franco Modigliani and Merton Miller, two

researchers studying capital structure in the 1950s, formulated what is known as (or thethe debt-irrelevance proposition

MM debt-irrelevance proposition), which states that the value of a firm is unaffected by its capital structure if certain

assumptions are true. Five of the key assumptions required by the MM debt-irrelevance proposition include that the firm

exists in a world with:

No taxes

No direct financial distress costs (that is, no costs associated with bankruptcy)

No indirect financial distress costs (In other words, the firm's financing decisions do not affect its investment

decisions, and there are no conflicts of interest between its debt holders and stockholders.)

No direct transaction costs (For example, there are no investment-banking commissions on debt or equity

issuances.)

No information advantages for managers about the firm's prospects relative to outside investors

Franco Modigliani and Merton Miller

Modigliani and Miller knew full well that the five assumptions are not true in the real world. Their point was not to show that

the value of a firm is unaffected by its capital structure, but to show that if capital structure does matter, then it must be

because of these assumptions. The importance of the MM debt-irrelevance proposition is that it laid the groundwork for

Copyright © 2012 eCornell. All rights reserved. All other copyrights, trademarks, trade names, and logos are the sole property of their respective owners. 7

the rigorous study of how value can be created through capital-structure decisions. It provided a framework for academics

and practitioners to use to focus their efforts. In the decades that followed, insights were gained as each of the five

assumptions was relaxed.

This course presents information you can use to gain an understanding of the intuition behind the MM debt-irrelevance

proposition. Then you can turn your attention to learning what relaxing each of the five assumptions indicates in terms of

optimal capital structure.

Copyright © 2012 eCornell. All rights reserved. All other copyrights, trademarks, trade names, and logos are the sole property of their respective owners. 8

Watch: The Optimal Mix of Debt and Equity

When you think about capital structure, you're thinking about the mix of debt and equity that a firm uses to finance its

activities. In this video, Professors Carvell and Gibson introduce the concept of the optimal mix of debt and equity for a

firm. They'll also discuss how financial professionals look at both equity and debt when making strategic decisions.

Copyright © 2012 eCornell. All rights reserved. All other copyrights, trademarks, trade names, and logos are the sole property of their respective owners. 9

Read: Strategic Financing Considerations at Four Firms

Here are a few brief scenarios and questions to get you thinking about the strategic considerations of raising capital. Here

you will examine types of financing that are available to firms, as well as some of the advantages of each.

Types of Financing

Type Issued by Description

Security

Corporations,

governments, or other

organizations

Securities are investment instruments and are broadly categorized into debt securities such as loans

from banks and bonds; equity securities, which include common stocks; and derivative contracts.

Common Stock Corporations Gives the holder a residual claim on the firm's assets and cash flows (net of liabilities and debt service).

Debt

Corporations,

governments, or other

organizations

For our purposes, debt is any financial claim issued by a firm that has a fixed payment that the firm must

make at a specified time if it is to avoid default.

Preferred equity

and preferred

stock

CorporationsPreferred shareholders are senior to common shareholders and junior to everyone else; they typically do

not have the same voting rights as common stock shareholders.

Consider, for example, Firm One. It has a high proportion of debt in its capital structure. Firm Two is a competitor of Firm

One. It possesses similar capital such as trucks, equipment, etc., and similar competitive dynamics and cash-flow

projections.

However, Firms One and Two have very different levels of debt and equity in their capital structures. Even so, the two

firms appear to enjoy the same level of consumer confidence.

How is it possible that Firm One and Firm Two are so similar and yet one carries so much more debt than the other? Is

one firm smarter than the other? Aren't there significant risks involved with carrying greater debt? In fact, why would either

of these firms continue to maintain a positive debt balance; why wouldn't they just pay off their debt?

Meanwhile, across town, Firm Three currently has a significant amount of debt outstanding and is concerned about

meeting its payment obligations. One of its managers has proposed a negative NPV project that is clearly high risk-it's the

sort of project your intuition tells you to avoid. Yet Firm Three's executive management, which has a reputation for smart,

savvy decision making, just approved it! Under what circumstances would this decision make sense?

Finally, let's examine a fourth firm: Firm Four is facing financial distress. Management there has recently rejected a

Copyright © 2012 eCornell. All rights reserved. All other copyrights, trademarks, trade names, and logos are the sole property of their respective owners. 10

positive NPV project that, to the outside observer, looks very likely to produce significant profits in the future. Why do you

think this firm would reject a positive NPV project?

These are the considerations that we will examine as we move through the concepts in this course.

Copyright © 2012 eCornell. All rights reserved. All other copyrights, trademarks, trade names, and logos are the sole property of their respective owners. 11

Read: Slicing the Cash Flow Pie

Key Points

Consider the source underlying value in a company

Cash flows and combined NPV in projects = total

value

When considering the impact of a company's choice of financing mix between debt and equity, it is useful to begin with an

understanding of the source underlying value in a company. Economic value in a company is created when investments

are made in projects that generate cash flows in excess of their cost of required funds. When we consider the cash flows

and the combined net present value of the company's projects, that gives us the company's total value.

For the purposes of illustration, let's think of a company's value as a pizza pie. Yours may be small, medium, large, or

even an extra-large pie. But the size of the pie, for our example here, is a consequence of the size or amount of our

company's total value. The issue now is, does it matter how we slice up the cash flow value of the pie, or does debt

matter? These projects just mentioned that are generating cash flows were financed by some mix of debt and equity.

Does it matter whether we finance the company's project with all equity or some mix of debt and equity? Will the

company's value change or be affected depending on the financing mix? Let's take our pie and split it up. We'll show three

different examples to make the point.

In this first example, the cash flow value goes to all equity. This is simply a case where the company has no debt at all and

all cash flows over time go to the equity providers of the company's capital.

Copyright © 2012 eCornell. All rights reserved. All other copyrights, trademarks, trade names, and logos are the sole property of their respective owners. 12

In this second example, one-half of the pie goes to equity, and one-half of the pie goes to our debt providers. The pie

hasn't changed...just that we now have half going to a different group of capital providers.

In the third example, most of the pie goes to debt and just a little to equity. Again, the pie is the same size, just most of it is

now going to the debt providers. In all of these examples, the cash flow from the projects that we've invested in are going

to providers of capital. Those providers of capital may be equity, debt, or some combination of the two. But again, the size

of the pie, which is related to the cash flows coming in from the projects, remains unchanged. We can refer to this

example as the "debt-irrelevance proposition."

Copyright © 2012 eCornell. All rights reserved. All other copyrights, trademarks, trade names, and logos are the sole property of their respective owners. 13

Watch: Debt vs. Equity

Does it really matter what you think of as debt and what you think of as equity, or is the critical consideration only, how

much value is there in my firm? In this video, Professors Gibson and Carvell discuss an intuitive way to think about debt

and equity and what they mean to you.

Copyright © 2012 eCornell. All rights reserved. All other copyrights, trademarks, trade names, and logos are the sole property of their respective owners. 14

Module Wrap-up: Financing Choices and the Debt-Irrelevance Proposition

In this module, you explored the debt-irrelevance proposition and how the valuation of a company is not impacted by its

capital structure based on this theory. You examined key assumptions to this proposition that are necessary for it to apply.

You also identified what you need to focus on when thinking about capital structure.

Copyright © 2012 eCornell. All rights reserved. All other copyrights, trademarks, trade names, and logos are the sole property of their respective owners. 15

Module Introduction: Factoring Taxes into the Financing Decision

Are there benefits to a corporation in carrying debt? And what are the some of the implications of taxes? In this module,

you will examine the way that debt can work to a firm's advantage. Professors Carvell and Gibson will lead you on an

examination of the role of debt in firm valuation. You will review a case study that demonstrates how debt affects a

fictional company, and you will have an opportunity to participate in a discussion with your peers about the tax shield.

Copyright © 2012 eCornell. All rights reserved. All other copyrights, trademarks, trade names, and logos are the sole property of their respective owners. 16

Watch: MM's Modified Theory

In this video, Professor Carvell will explain the relevance of "MM's Modified Theory," and how it relates to this exploration

of raising capital. It may seem counterintuitive at first, but as Professor Carvell explains here, you can add value to a

company when you add to its debt. Let's find out the rationale for this theory.

Copyright © 2012 eCornell. All rights reserved. All other copyrights, trademarks, trade names, and logos are the sole property of their respective owners. 17

Read: The Unlevered Firm

The first of the assumptions of MM's debt-irrelevance proposition is this: no taxes. Do taxes make a difference in the value

of the firm, and if so, how? To find out the answer, let's take a look at FlatCorp.

Case Study FlatCorp Limited

FlatCorp currently has no debt outstanding-that is, it is an firm. Its tax rate is 40% and its earnings beforeunlevered

interest and taxes (EBIT) are expected to average $10 million per year indefinitely. All net income is paid to stockholders

as dividends. FlatCorp's stockholders currently require an expected return of 15% on their shares. FlatCorp's expected net

income is the earnings before interest and taxes minus the amount paid in taxes:

Expected net income = $10m - (.40)($10m) = $6m/year (perpetuity)

FlatCorp's equity value is the expected net income divided by the required return on equity:

Equity value = (expected net income)/(required return on equity)

= ($6m) / (.15) = $40 million

Thus, when FlatCorp is financed entirely by equity, its investors as a group value the cash flows its operations are

expected to produce at $40 million.

FlatCorp's Market-Value Balance Sheet ($ Millions)

Assets Liabilities and Equity

Present value of unlevered cash

flows (V )UA

40 Equity 40

We refer to the market value of the firm on an all-equity basis as the or V . We can think of Vvalue of unlevered assets, UA

Copyright © 2012 eCornell. All rights reserved. All other copyrights, trademarks, trade names, and logos are the sole property of their respective owners. 18

as the present value of future cash flows that goes to investors of an all-equity financed firm.UA

As we continue to explore the significance of the assumption no taxes, we need to explore what happens when FlatCorp

takes on debt.

Copyright © 2012 eCornell. All rights reserved. All other copyrights, trademarks, trade names, and logos are the sole property of their respective owners. 19

Consider the Role of Taxes

In this video, Professors Carvell and Gibson explore the ways that taxes influence our thinking about capital structure, and

they explain what it means that corporations can accrue tax benefits by writing off, on their taxes, the interest paid on the

debt to creditors.

Copyright © 2012 eCornell. All rights reserved. All other copyrights, trademarks, trade names, and logos are the sole property of their respective owners. 20

Read: How Debt Creates Benefits for the Firm

Key Points

When debt is introduced, net income goes down

An unlevered firm carries no debt

Now you will examine the ways that debt can create benefits for a firm. The debt-irrelevance proposition states that the

value of a firm is unaffected by its capital structure if, among other things, there are no taxes.

Annual Cash Flows ($ Millions)

"Unlevered"

(No Debt)

$10 Million Debt @10%

EBIT 10.0 10.0

Less: Interest 0.0 1.0

EBT 10.0 9.0

Less: Taxes (40%) 4.0 3.6

Net Income 6.0 5.4

Case Study FlatCorp Limited

We are exploring how taxes are important to the value of a firm and we are using FlatCorp as an example. What if

FlatCorp, currently unlevered, adds debt to its mix of capital? Specifically, assume it issues $10 million in debt at an

interest rate of 10% and pays the $10 million out to equity holders as a dividend.

In this scenario, FlatCorp's operations are unaffected, and so earnings before interest and taxes (EBIT) remains the same

as before it issued debt: $10 million. However, it would now pay 10%, or $1 million in interest, on its $10 million debt. This

payment would reduce FlatCorp's earnings before taxes (EBT) to $9 million and, subsequently, reduce the tax payment

FlatCorp must make. At 40%, the tax payment on $9 million is $3.6 million.

FlatCorp's net income would be $9 million - $3.6 million = $5.4 million.

"Unlevered"

(No Debt)

$10 Million Debt

@10%

Debt holders receive 0.0 1.0

Equity holders receive 6.0 5.4

Total for investors is 6.0 6.4

Copyright © 2012 eCornell. All rights reserved. All other copyrights, trademarks, trade names, and logos are the sole property of their respective owners. 21

The first table shown here presents a comparison of the levered and unlevered cases.

When debt is introduced, net income goes down. But as you can see in the second table, the total payment to investors,

both debt holders and equity holders, goes up! It changes from $6 million to $6.4 million.

An unlevered firm carries no debt, so the value of the firm can be represented in two pieces: expected net income and tax payments.

We can look at this scenario in terms of the cash flow pie. In the unlevered firm, a large slice of the value pie goes to the

government as a tax payment. In a firm that carries debt (a levered firm), the government and net income slices are both

reduced in order to create a third slice for debt payment.

The value of a firm carrying debt can be represented in three pieces: expected net income, tax payments, and debt payments.

While the size of the cash flow pie isn't changing, the slice sizes do change. With more debt, the government slice shrinks

because more of FlatCorp's taxable earnings are shielded from taxation. As the government slice shrinks, the combined

size of the debt holder and equity holder slices increases. This means more pie (i.e., more value) for investors as a group.

Copyright © 2012 eCornell. All rights reserved. All other copyrights, trademarks, trade names, and logos are the sole property of their respective owners. 22

Read: The Value of the Levered Firm

Key Points

When debt is introduced to the unlevered firm, net

income goes down

Interest paid out on debt is tax deductible, whereas

stock dividends and additions to retained earnings

are not

Recall that FlatCorp was an unlevered firm with an EBIT of $10 million year after year. Before FlatCorp took on debt,

investors as a group valued the cash flows its operations are expected to produce at $40 million. Let's take a look at what

happens to FlatCorp's value at the point at which the firm acquires debt.

Case Study FlatCorp Limited

When debt is introduced to the unlevered firm, net income goes down. But the total payment to investors, both debt

holders and equity holders, goes up! This is due to the debt tax shield-the reduction in taxes realized by deducting interest

expense.

FlatCorp's value now consists of expected net income, tax payments, and debt payments.

FlatCorp's annual tax shield is the product of three values: the tax rate for the corporation, T ; the amount of the debt, D;c

and the rate on the debt, r . The annual tax shield is:D

T (r D) = (.40)($1.0 million) = $0.4 millionc D

If the risk of the tax shield is roughly the same as the risk of the debt itself, these cash flows should be discounted at rate r

. Furthermore, if the debt is always rolled over and not expected to grow, the tax shield can be treated as a perpetuity. InD

this special case, the present value of the tax shields is shown to the right.

PV (tax shields) = T (r D)/r c D D

= T Dc

= (0.40)($10 million)

Copyright © 2012 eCornell. All rights reserved. All other copyrights, trademarks, trade names, and logos are the sole property of their respective owners. 23

= $4.0 million

FlatCorp's equity value is the expected net income divided by the required return on equity:

Equity value = ($6m)/(.15) = $40 million

FlatCorp's market value to its investors after the debt issue is:

$40 million + $4 million = $44 million

(This is the market value of FlatCorp to its investors, both debt and equity, as a group.)

The market value consists of the value of the all-equity financed firm (in this case, $40 million) and the present value of the

interest tax shields (in this case, $4 million).

Remember, interest paid out on debt is tax deductible, whereas stock dividends and additions to retained earnings are

not. This fact creates a tax advantage for debt.

Copyright © 2012 eCornell. All rights reserved. All other copyrights, trademarks, trade names, and logos are the sole property of their respective owners. 24

Watch: Taxes Matter

In this video, Professors Carvell and Gibson place the content of this section into a helpful context for the non-financial

manager by explaining how it will help you perform better in your position and what it means for you.

Copyright © 2012 eCornell. All rights reserved. All other copyrights, trademarks, trade names, and logos are the sole property of their respective owners. 25

Module Wrap-up: Factoring Taxes into the Financing Decision

In this module, you explored how taxes can change our approach to capital structure. You examined the levered firm and

the unlevered firm. You also identified some of the advantages debt can have for a company. You examined the

ramifications of taxes and financial distress costs to the value of the firm. You also explored the factors that motivate

companies to take on debt, as well as some reasons that firms may choose to limit the amount of debt they carry. You

also had an opportunity to discuss the ramifications of the fact that the U.S. government allows interest payments to be

deducted from taxes.

Copyright © 2012 eCornell. All rights reserved. All other copyrights, trademarks, trade names, and logos are the sole property of their respective owners. 26

Module Introduction: Financial Distress Costs

In this module, you will examine key concepts related to financial distress. You will look at liquidation and reorganization

and will examine the real-life example provided by the U.S. savings and loan industry. You will investigate the difference

between a fixed rate and a floating rate and begin an exploration of risk. You will have an opportunity to participate in a

discussion with your peers on the strategic implications of cost. You will also get to demonstrate your mastery of critical

concepts by completing quizzes related to direct costs, indirect costs, and how much debt is too much.

Copyright © 2012 eCornell. All rights reserved. All other copyrights, trademarks, trade names, and logos are the sole property of their respective owners. 27

Debt Funding

Now that we know that there are tax advantages to corporations taking on debt, do we assume that all corporations are

taking advantage? No, say Professors Carvell and Gibson. They explore the reasons for that in this video.

Copyright © 2012 eCornell. All rights reserved. All other copyrights, trademarks, trade names, and logos are the sole property of their respective owners. 28

Read: Costs Due to Liquidation, Reorganization, and Shareholder Perceptions

Let's explore the reasons why companies may incur costs due to liquidation, reorganization, and shareholder perceptions.

Click each icon below to learn more.

Use the within each screen to see all relevant content. embedded scroll bar

Liquidation

In the United States, bankruptcy that leads to liquidation of the firm's assets in the settlement of creditors'

claims is called a c named for its chapter in the . Chapter 7hapter 7 bankruptcy, Federal Bankruptcy Code

bankruptcy can be initiated by the firm itself or by creditors if the firm does not make required contractual

payments. A chapter 7 bankruptcy is overseen by a federal bankruptcy trustee under the supervision of a

federal bankruptcy court.

The federal bankruptcy trustee liquidates the firm's assets and distributes proceeds to claim holders according

to the . This rule specifies that claims are paid in the following order:absolute priority rule

• Collateral to secured creditors. Secured creditors have first ("prior") claim on their collateral or its value,

regardless of their seniority in other respects. If more than one claimant has claim to the same collateral, the

claimant that registered ("perfected") its collateral rights first has priority.

• Administrative expenses incurred as the result of the bankruptcy process: court costs, lawyers' fees, the

trustee's expenses, and any debts incurred (with the court's permission) after the bankruptcy filing. Debts of

the latter sort are often referred to as financing.debtor in possession

• Various claims singled out for priority, including: unpaid employee wages and benefits accrued before the

bankruptcy filing, consumer deposits (for example, security deposits on apartments), and taxes.

• Claims by unsecured creditors (bondholders, trade creditors, banks, etc.). These creditors have equal status

unless their credit agreements specifically give them senior or junior status, in which case they are paid

according to order of seniority.

• Dividends to preferred shareholders.

• Dividends to common shareholders.

Copyright © 2012 eCornell. All rights reserved. All other copyrights, trademarks, trade names, and logos are the sole property of their respective owners. 29

In liquidation, claims that have higher priority must be paid in full before claims with lower priority are paid at

all.

Reorganization

If the firm's value as an ongoing concern exceeds its liquidation value, then it is in all claimants' interests to

attempt to reorganize the firm. In this case, the firm would be an economically viable entity, and the

presumption is that its current capital structure is not conducive to continued operations. Bankruptcy that

allows the firm to reorganize its debt and equity claims and continue to operate is called a c hapter 11

named for its chapter in the . Like a chapter 7 bankruptcy, a chapter 11bankruptcy, Federal Bankruptcy Code

bankruptcy can be initiated by the firm itself or by creditors if the firm does not make required contractual

payments. A chapter 11 bankruptcy is overseen by a federal bankruptcy trustee under the supervision of a

federal bankruptcy court.

In a successful reorganization, the firm continues operating and claim holders receive new financial claims in

exchange for their old ones. All old claims (including equity) are null and void afterward, so those holding

shares in the firm prior to its reorganization must secure shares in the reorganized firm or lose their

investments.

Steps in the reorganization process:

• Management has 120 days (often extended by the judge) to submit a reorganization plan.

• Claimants vote. The judge determines whether at least half the number and two-thirds the dollar amount of

each claimant class (including equity) accepted the plan.

• If , the plan is adopted yes

• If , the judge may take one of three actions: no

Instruct management to devise a new reorganization plan (then return to another round of voting).

Instruct claimants to devise their own reorganization plan or plans (then return to another round of voting).

Copyright © 2012 eCornell. All rights reserved. All other copyrights, trademarks, trade names, and logos are the sole property of their respective owners. 30

Force a "cramdown." A cramdown plan must give all claimants at least as much as they would get under a

chapter 7 liquidation.

Shareholder

When a firm with significant debt in its capital structure experiences a downturn in its operations, non-financial

stakeholders may take actions that adversely affect the firm's operations. Let's consider the actions of three

key non-financial stakeholder groups: consumers, suppliers, and employees.

Consumers

Suppose you're shopping for a new car. You've narrowed it down to two similar cars offered by two different

firms: Crystal Motors and Fjord. Crystal is financed by a high ratio of debt-to-equity. Fjord has a low

debt-to-equity ratio. The economy is currently in recession, and you've seen news headlines expressing

concerns that weak firms may be heading for bankruptcy. The two cars offer similar features and warranties

and are currently priced the same. However, the weaker company may need to cut prices to raise cash quickly

in the short term. From which company do you buy?

Fjord would be your best bet. Buying from Crystal is risky. Given the possibility of the financial distress at

Crystal caused by their high debt ratio, operating budgets may be adversely affecting quality controls.

Moreover, if Crystal declares bankruptcy, there's a possibility that its car warranties will be voided. There is

also a possibility that spare parts and service may be difficult to find. If Crystal is going to sell cars, it's going to

have to cut prices relative to Fjord, which will impair the profitability of operations. Even if it never declares

bankruptcy, these are revenues that are lost forever.

What we have now is capital structure affecting the operations of the firm. When a firm with significant debt in

its capital structure experiences a downturn in its operations, it may have to lower prices to attract customers

or it may lose its customers outright. Financial distress leads to particularly severe customer revenue losses for

Copyright © 2012 eCornell. All rights reserved. All other copyrights, trademarks, trade names, and logos are the sole property of their respective owners. 31

firms that sell products with quality that is important yet hard to observe, and for firms that sell products that

require future servicing.

Suppliers

Let's now suppose you're the CEO of Elle and Dee's Bakery, a supplier of individually wrapped cupcakes, fruit

pies, cream-filled sponge cakes, and other delectable confections to convenience stores and grocery stores.

Once you've delivered the product to the store, you offer net-30 trade credit terms (that is, you require full

payment within 30 days). Snack-N-Gas, one of the convenience store chains you supply, has significant debt

in its capital structure and of late has been experiencing a downturn in its operations. You become concerned

that Snack-N-Gas may have difficulty making contractual payments to its creditors. As CEO of Elle and Dee's,

what might you do?

You may decide to do nothing because terminating trade credit makes a bad operating situation considerably

worse for Snack-N-Gas. However, there are good reasons to terminate their trade credit. In the event of

bankruptcy, recall that absolute priority dictates the order in which claims are satisfied. Trade credit is far

enough down the absolute priority list that it is seldom repaid more than a few cents on the dollar. Of course,

you'll be willing to sell Elle and Dee's delectable confections for cash, but Snack-N-Gas is unlikely to have the

cash given its financial difficulties. Clearly Snack-N-Gas will have difficulty restocking its shelves once Elle and

Dee's and other suppliers terminate their trade credit, which makes a bad operating situation considerably

worse for Snack-N-Gas. In fact, suppliers terminating their trade credit is often a strong sign that bankruptcy is

imminent, as the business will not last long without an ability to restock and sell products. Again, we have the

firm's capital structure affecting its operations. When a firm with significant debt in its capital structure

experiences a downturn in its operations, it increases the likelihood that trade credit will be terminated.

Financial distress leads to severe supplier problems for firms that rely heavily on trade credit.

Employees

Let's now suppose that you're an employee of a firm with significant debt in its capital structure that

experiences a downturn in its operations. You grow concerned that your employer may be heading for

bankruptcy. What might you do?

Doing nothing is not a good idea. It would be wise to look for another job. In fact, everybody at the the firm

would be wise to look for another job. What will happen? Most employees will look for other jobs. The most

competent, highly motivated employees will likely find jobs. The less competent, less motivated employees will

likely not. Will the loss of its best employees adversely affect the firm's operations? Absolutely. Even if the firm

never actually declares bankruptcy, it will be left with only the employees who were unable to find work, and

those employees will run the firm. Again, we have the firm's capital structure affecting its operations. When a

firm with significant debt in its capital structure experiences a downturn in its operations, it increases the

likelihood that it will lose its best employees. Financial distress leads to severe problems for firms that rely on

Copyright © 2012 eCornell. All rights reserved. All other copyrights, trademarks, trade names, and logos are the sole property of their respective owners. 32

highly trained, specialized employees.

Copyright © 2012 eCornell. All rights reserved. All other copyrights, trademarks, trade names, and logos are the sole property of their respective owners. 33

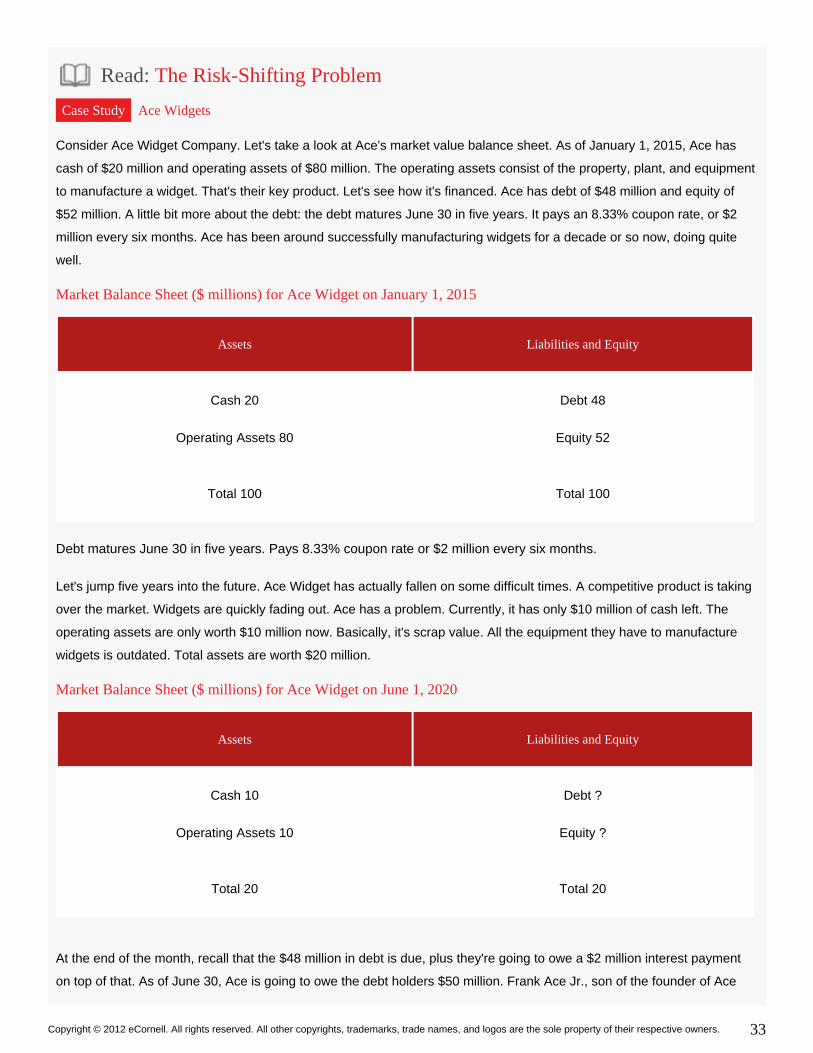

Read: The Risk-Shifting Problem

Case Study Ace Widgets

Consider Ace Widget Company. Let's take a look at Ace's market value balance sheet. As of January 1, 2015, Ace has

cash of $20 million and operating assets of $80 million. The operating assets consist of the property, plant, and equipment

to manufacture a widget. That's their key product. Let's see how it's financed. Ace has debt of $48 million and equity of

$52 million. A little bit more about the debt: the debt matures June 30 in five years. It pays an 8.33% coupon rate, or $2

million every six months. Ace has been around successfully manufacturing widgets for a decade or so now, doing quite

well.

Market Balance Sheet ($ millions) for Ace Widget on January 1, 2015

Assets Liabilities and Equity

Cash 20

Operating Assets 80

Debt 48

Equity 52

Total 100 Total 100

Debt matures June 30 in five years. Pays 8.33% coupon rate or $2 million every six months.

Let's jump five years into the future. Ace Widget has actually fallen on some difficult times. A competitive product is taking

over the market. Widgets are quickly fading out. Ace has a problem. Currently, it has only $10 million of cash left. The

operating assets are only worth $10 million now. Basically, it's scrap value. All the equipment they have to manufacture

widgets is outdated. Total assets are worth $20 million.

Market Balance Sheet ($ millions) for Ace Widget on June 1, 2020

Assets Liabilities and Equity

Cash 10

Operating Assets 10

Debt ?

Equity ?

Total 20 Total 20

At the end of the month, recall that the $48 million in debt is due, plus they're going to owe a $2 million interest payment

on top of that. As of June 30, Ace is going to owe the debt holders $50 million. Frank Ace Jr., son of the founder of Ace

Copyright © 2012 eCornell. All rights reserved. All other copyrights, trademarks, trade names, and logos are the sole property of their respective owners. 34

Widget, has a dilemma. If he sits and does nothing, what happens? Well, the debt holders are going to ask for their $50

million. Ace only has $20 million. He'll just have to pay off the debt holders the $20 million and say, "Sorry about the other

$30 million." Equity holders will be left with nothing.

But Frank gets an idea. How about if he heads off to Las Vegas? What he's going to do is walk up to the roulette table.

He's going to put it all down on 17 black-all $10 million in cash that Ace has left. Let's think of the roulette gamble as a

project. Well, one in 38 times, 17 black is going to hit. If you've ever been to Vegas, the payoff is 36 to 1. That $10 million

will turn into $360 million. Now, the 37 of the 38 times, Frank's basically going to walk away with a free cocktail. He gets

nothing. Of course, Frank puts all of Ace's $10 million on the line. If we calculate the net present value, we get minus .53

million, or a loss of $530,000. Clearly, this is a negative NPV project.

Capital budgeting teaches us that we don't want to take negative NPV projects. But recall: what is management's goal?

What is the objective of the firm? Well, it's to maximize the value of equity or maximize shareholder wealth.

So let's think about Frank's position here-not a great one. Remember, if Frank sits and does nothing, the equity holders

get nothing. One in 38 times, 17 black is going to come in. Let's look at the balance sheet as of June 30. Well, Ace now

has cash of $360 million. The operating assets are still $10 million. Remember that's the scrap value of the equipment.

Debt holders come to Ace at the end of the month. They demand the $50 million they're due. No problem. Ace has the

$50 million to pay the debt holders in full. That leaves equity holders with $320 million.

The other 37 of 38 times, Frank is going to lose and walk away with his free cocktail. Let's look at the balance sheet in that

instance. Well, Frank has lost the $10 million, so Ace Widget has no cash left, a zero balance. Again, we have the

operating assets worth $10 million. Debt holders come to Ace at the end of the month. They ask for their $50 million.

Frank can only send his apologies and the $10 million. Debt holders take a $40 million loss. Of course, we have nothing

left for equity-it's worth zero.

Let's take a look at their expected payoff. One in 38 times, equity holders will get the $320 million-that's when 17 black

hits. The other 37 of 38 times, they get zero. The expected payoff to the equity holders is $8.42 million. How about the

debt holders' perspectives? What can they expect? One in 38 times, they'll get paid off in full the $50 million when 17

black hits. The other 37 of 38 times, they'll get their $10 million-basically the scrap value of the equipment. Their expected

payoff is $11.05 million.

When Frank Wins vs. When Frank Loses

When Frank Wins When Frank Loses

$320 million Equity holders

Expected payoff is 1/38 ($320) + 37/38 ($0) = $8.42 million if Vegas.

Expected payoff is $0 if nothing.

$0

$50 million Debt holders

Copyright © 2012 eCornell. All rights reserved. All other copyrights, trademarks, trade names, and logos are the sole property of their respective owners. 35

Expected payoff is 1/38 ($50) + 37/38 ($10) = $11.05 million if Vegas.

Expected payoff is $20 million if nothing.

$10 million

How are equity holders and debt holders going to feel about Frank heading off to Vegas?

Well, equity holders will like it. If Frank stays home, equity holders get zero for sure. Frank heads off to Vegas, equity

holders, at least now they're in the game. Their expected payoff is $8.42 million. Debt holders, however, want Frank to

stay home; they don't want him going off to Vegas. If Frank stays home, they get $20 million for sure. If Frank heads off to

Vegas, their expected payoff drops to $11.05 million. What should Frank do?

Well, the goal of the firm is to maximize the value of equity, so Frank should head off to Vegas despite the fact that it's a

negative NPV project. This is the idea of risk shifting. If the project comes in, equity holders get all of the upside. Debt

holders have a fixed payment. It's a fixed contract. However, if the project doesn't come in, if Frank doesn't hit 17 black,

the debt holders have all the downside risk. Equity holders get all the upside; debt holders get all the downside. Another

way to put it-heads, equity holders win; tails, debt holders lose. This creates a perverse incentive. When we get a lot of

debt, operations hit a rough patch, the firm finds itself in a position where it will take risky projects even if they're negative

NPV.

Copyright © 2012 eCornell. All rights reserved. All other copyrights, trademarks, trade names, and logos are the sole property of their respective owners. 36

Read: The Debt-Overhang Problem

Case Study Ace Widgets

Recall that as of 2015, Ace was making widgets and had $20 million in cash. The operating assets-primarily property,

plant, and equipment to manufacture the widgets-worth $80 million, total assets of $100 million. That was financed with

debt of $48 million and equity of $52 million. Recall the debt matures June 30, 2020; it pays a coupon of 8.33%, or $2

million every six months.

Market Balance Sheet ($ millions) for Ace Widget on January 1, 2015

Assets Liabilities and Equity

Cash 20

Operating Assets 80

Debt 48

Equity 52

Total 100 Total 100

Debt matures June 30 in five years. Pays 8.33% coupon rate or $2 million every six months.

Let's fast forward to June 1, 2020. The debt is now due. Frank's friend comes along and has a great idea. He says, "Why

don't we upgrade the factory to the manufacture of a more competitive product?"

Let's take a look at the numbers.

If Frank upgrades the factory, it's going to cost $12 million in cash. The present value of the future cash flows will be $25

million. Let's calculate the net present value of the factory updates. Twenty-five million dollars is the present value of the

future cash flows. Twelve million dollars is the cash required to convert the factory. Ten million dollars is the opportunity

cost of the factory that he could have sold for scrap. The net is a positive $3 million. So the net present value is a positive

$3 million. But where does the $12 million come from?

NPV= PV - cost of upgrading factory - opportunity cost of factory for scrap

= $25 million - $12 million - $10 million = $3 million

Well, Ace Widgets has $10 million cash on hand, so there's $2 million needed. Let's think about trying to raise it from the

equity holders.

Let's look at it from equity holders' perspective. They put up the $2 million. Ace combines that with their $10 million cash

and upgrades the factory. What do they have left? The cash is a zero balance. The operating assets are now worth $25

million. That's the present value of the future cash flows for the manufacture of upgraded widgets.

Copyright © 2012 eCornell. All rights reserved. All other copyrights, trademarks, trade names, and logos are the sole property of their respective owners. 37

So what will Frank's debt holders receive? They come and ask for their $50 million. Well, Frank has $25 million for them.

Equity holders receive nothing. So will equity holders want to provide $2 million if they will get zero for sure? No. Even

though this is a positive NPV project, it is not in the interest of the firm to undertake the investment. Recall that the

objective of management, the goal of the firm, is to maximize the value of the equity or maximize its shareholder wealth.

Market Balance Sheet ($ millions) for Ace Widget on June 30, 2020

Assets Liabilities and Equity

Cash 0

Operating Assets 25

Debt 25

Equity 0

Total 25 Total 25

Consider the debt-overhang problem. Here equity holders put up the $2 million, but debt holders have first claim on the

assets. With the debt overhang, equity holders will not fund the project, even though it is a positive net present value.

Well, could the firm raise money from additional debt? Typically not. Typically, debt that's already in place will have a claim

that is senior to any debt that follows on. We call this -this debt that follows on.subordinate debt

What that means, in the case of a bankruptcy, is the debt that is already in place that is senior will have first claim on the

assets. The subordinated debt that follows on will have a second claim. In this case, if the subordinated debt holders

provide the $2 million, again, they will receive nothing, just like the equity holders.

So a firm that finds itself with a debt overhang, even though it has positive net present value projects to undertake, it is

shut off from funding. It cannot raise equity, and it cannot raise debt.

When a firm gets debt in its capital structure, considerable amounts of debt, and hits a rough patch with its operations, the

debt-overhang and the risk-shifting problems combine. With a debt-overhang problem, it cannot fund positive net value

present projects. With the risk-shifting problem, it has an incentive to take high-risk projects even though they might be

negative net present value. This destroys the value of the operating assets.

Copyright © 2012 eCornell. All rights reserved. All other copyrights, trademarks, trade names, and logos are the sole property of their respective owners. 38

Read: The Savings and Loan Industry Example

Key Points

Without knowledge of risk shifting, the actions of

savings-and-loan management that contributed to

the losses in the early 1980s make little sense. But

once you understand risk shifting, the rationale

becomes clear.

Real-world examples of the risk-shifting and debt-overhang problems are not rare, particularly during economic

recessions. Consider the collapse of the savings-and-loan industry that cost U.S. taxpayers more than $100 billion. An

understanding of risk shifting makes clear the motives for otherwise puzzling S&L management actions.

Imagine that you are a CEO of a savings-and-loan institution in the early 1970s. You, like other CEOs in the

savings-and-loan business, have successfully followed a simple business model for years: originate and hold 30-year

mortgages at a fixed rate of roughly 7% and raise capital primarily by taking in short-term deposits paying roughly 4%. The

3% difference between the 7% you are taking in on long-term mortgages and the 4% you are paying out on short-term

deposits leaves your savings and loan with a handsome profit year after year!

Copyright © 2012 eCornell. All rights reserved. All other copyrights, trademarks, trade names, and logos are the sole property of their respective owners. 39

Now fast forward a few years to 1980 and a very different world. Oil embargoes, Federal Reserve policies designed to

fight unemployment rather than inflation, and other factors have resulted in an inflation rate of 13.5%. What does this

mean for you? Your savings and loan assets are mostly the long-term 7% mortgages originated over past decades. Your

savings and loan finances those assets primarily with short-term deposits that now pay double-digit interest to

compensate depositors for inflation. If, as CEO, you take no action, how long will your savings and loan stay in business?

The answer is not very long; you'll go out of business and your stockholders will receive nothing. But what can you do?

Actual CEOs of the savings-and-loan industry found an option in 1980: they bought high-risk junk bonds and made

high-risk loans. Assuredly, many of these "projects" had a negative net present value. Under normal circumstances,

buying these high-risk junk bonds and making high-risk loans would not have made sense. But, savings-and-loan

management was doing its job. If management had done nothing, stockholders would have lost everything. By gambling

on the high-risk junk bonds and loans, management gave its stockholders a chance. If the gamble had paid off, depositors

could have been paid and money would have been left for stockholders. Unfortunately, the gamble did not pay off, with

many of the junk bonds and loans later proving worthless.

Without knowledge of risk shifting, the actions of savings-and-loan management that contributed to the losses in the early

1980s make little sense. But once you understand risk shifting, the rationale becomes clear.

When you sit down to catch up on the financial news, keep risk shifting in mind. It may help you to assess the motives

behind management's actions.

Copyright © 2012 eCornell. All rights reserved. All other copyrights, trademarks, trade names, and logos are the sole property of their respective owners. 40

Read: Structuring Debt to Mitigate Financial Distress Costs

Key Points

Firms have incentives to include debt in their capital structure

Firms can incur the least amount of financial distress costs by using protective covenants on debt, convertible bonds,

short-term vs. long-term debt, and floating-rate vs. fixed-rate debt

Financial distress costs shrink the "cash-flow pie" shared by investors. Clearly these costs can be reduced by lowering the

ratio of debt to equity in the firm's capital structure. In the extreme, financing a firm entirely by equity eliminates all financial

distress costs. However, as we have seen, debt offers benefits such as the ability to deduct interest payments from

corporate income tax. Thus, firms have an incentive to include debt in their capital structure. But how can they do so while

incurring the least amount of financial distress costs? This question is answered here and on the next course page, where

we look at protective covenants on debt, convertible bonds, short-term vs. long-term debt, and floating-rate vs. fixed-rate

debt.

Protective covenants on debt

Recall that conflicts of interest between debt holders and stockholders can result in either risk-shifting or debt-overhang

problems. Rational investors recognize these conflicts of interest and may demand higher interest rates on the firm's debt

to compensate. This would result in shareholders paying for the expected costs of potential conflicts of interest. To avoid

this outcome-to mitigate the concerns of debt holders and lower costs due to higher interest rates-the firm can add

protective covenants to debt contracts.

Debt contracts often include covenants that require the firm to meet standards determined by metrics such as the ratio of

current assets to current liabilities, the ratio of debt to equity, or the ratio of operating income to interest. Other covenants

may restrict new debt to be of junior priority in the event of bankruptcy or prohibit new debt outright. Additional covenants

may restrict excessive dividend payments to stockholders or limit stock repurchases. A final example is covenants that

place constraints on mergers or asset sales. All these covenants provide protections to debt holders against the firm

investing in risky assets or moving closer to a debt-overhang situation.

Several notes about protective covenants are in order:

If covenants are violated, then the firm is said to be in "technical default," meaning that debt holders can demand

repayment even if the firm has not missed any payments.

While covenants may mitigate conflicts of interest between debt holders and stockholders, the firm loses flexibility.

For example, covenant restrictions may prevent the firm from undertaking a project with a positive net present

value.

Debt contracts with particularly restrictive covenants often include a "call" feature, which gives the firm the right to

retire the debt prior to maturity for an agreed-upon price.

Convertible bonds

Convertible bonds can help mitigate risk shifting and associated costs. A convertible bond is one the bondholder is able to

Copyright © 2012 eCornell. All rights reserved. All other copyrights, trademarks, trade names, and logos are the sole property of their respective owners. 41

exchange for a fixed number of shares of stock. In effect, the debt holder is also an equity holder. So in those risk-shifting

scenarios that offer a reward for equity holders but no reward for debt holders (only a penalty if the gamble is lost), the

convertible bond provides an avenue for debt holders to benefit. They can share in the reward when the debt is converted

to equity. This reduces management's incentives to engage in risk shifting.

Short-term debt versus long-term debt

Using short-term debt instead of long-term debt is another way to mitigate conflicts of interest between debt holders and

stockholders. Short-term debt provides a way for debt holders to gain some control over the firms they finance.

Let's illustrate with an example. Suppose you're a chief financial officer seeking a bank loan. Your banker offers a 30-year

loan that you accept. Let's fast forward one year. When you sit down with your banker, he expresses displeasure with

some of the decisions the firm's management has made. He requests that your firm make some changes. Given that 29

years are left on the loan, you aren't concerned about whether this banker currently feels inclined to renew the debt.

Chances are that you won't go out of your way to address your banker's concerns.

Now let's repeat the scenario, but instead let's suppose that it's a one-year loan rather than a 30-year loan. When you sit

down with your banker after one year, he expresses displeasure with some of the decisions the firm's management has

made. He requests that your firm make some changes, or the debt will not be renewed. How might you respond now?

Chances are that your attitude toward the banker's request will be very different and you will address his concerns.

By using short-term debt, the debt holder gains control and can allay potential conflicts of interest between debt holders

and stockholders.

Copyright © 2012 eCornell. All rights reserved. All other copyrights, trademarks, trade names, and logos are the sole property of their respective owners. 42

Read: Fixed Rate vs. Floating Rate

Key Points

In selecting either fixed- or floating-rate debt, the idea is to match your interest payments to your operating cash flows

Download an additional reading: "The Use of Fixed-rate and Floating-rate Debt for Hotels"

Can the choice of fixed-rate debt versus floating-rate debt affect financial distress costs? Let's look at how it might. First of

all, consider what "floating rate" (or variable rate) means. For floating-rate debt, the interest rate is variable over a fixed

range that itself changes over time, depending on changes in a benchmark rate. A common "prevailing benchmark rate"

used for corporate debt is the London Interbank Offer Rate (LIBOR). The LIBOR typically fluctuates with the strength of

the economy: it tends to be high when the economy is strong and low when the economy is weak. Fixed-rate debt, on the

other hand, is just what the name implies: fixed.

In selecting either fixed- or floating-rate debt, the idea is to match your interest payments to your operating cash flows. To

illustrate what this means, let's compare two firms: Firm A is a utility company handling residential accounts, and Firm B

owns and operates a cruise line. Firm A charges its customers a fixed rate, so the cash flows generated by Firm A's

operations are likely to be fairly steady as the economy fluctuates. Firm B, on the other hand, books passengers on its

cruises at market rates. Thus, the cash flows generated by Firm B's operations are likely to move with fluctuations in the

economy. Should Firm A choose to finance with fixed-rate debt or floating-rate debt? How about Firm B?

Think about the cash flows of these two firms in a recession. Firm A's cash flows are likely to remain more or less the

same-utility customers are required to pay the same amount regardless of the state of the economy. Fixed-rate debt is the

right choice for Firm A.

On the other hand, Firm B's cash flows will decline significantly in the recession. Leisure travelers will reduce their demand

for vacation cruises. If Firm B chose to finance with fixed-rate debt, it is likely to experience difficulties in meeting the fixed

interest payments. Financial distress costs will climb as risk-shifting or debt-overhang problems materialize or as

relationships with non-financial stakeholders (such as suppliers or key employees) are strained.

If, instead, Firm B chose to finance with floating-rate debt, the situation would be different. In a recession, LIBOR is likely

to decrease, easing interest payments. Thus, although the cash flows generated by Firm B's operations will decline

significantly in a recession, so too will the interest payments, decreasing financial distress costs. Floating-rate debt is a

good choice for Firm B.

Additional Reading

In their article, course author Scott Gibson and John B. Corgel"The Use of Fixed-rate and Floating-rate Debt for Hotels,"

of Cornell University examine the choice between fixed-rate and floating-rate debt in the context of the hotel industry. They

compare the hotel-industry metric "revenue per available room" (RevPAR) with London Interbank Offer Rate (LIBOR) and

find a strong correlation between the two. They find evidence of a relationship between RevPAR and floating interest

rates.

According to this research, hotels using variable-rate mortgages are more likely to cover their debts in good times and bad

Copyright © 2012 eCornell. All rights reserved. All other copyrights, trademarks, trade names, and logos are the sole property of their respective owners. 43

than are hotels financed with fixed-rate loans. Hotel investors, it appears, fare more favorably with floating-rate loans than

with the commonly used fixed-rate financing.

Copyright © 2012 eCornell. All rights reserved. All other copyrights, trademarks, trade names, and logos are the sole property of their respective owners. 44

Watch: The Strategic Implications of Cost

In this video, Professors Carvell and Gibson discuss what costs can mean to an organization. How will competitors, and

even clients, look at the amount of debt your organization carries?

Copyright © 2012 eCornell. All rights reserved. All other copyrights, trademarks, trade names, and logos are the sole property of their respective owners. 45

Module Wrap-up: Financial Distress Costs

In this module, you identified the need for a company to balance the tax advantages to carrying debt with the financial

distress costs of not meeting contractual obligations. You explored the risk-shifting problem and the debt-overhang

problem. You considered some of the reasons that firms may not choose to finance primarily through debt. You also

compared fixed rates and floating rates.

Copyright © 2012 eCornell. All rights reserved. All other copyrights, trademarks, trade names, and logos are the sole property of their respective owners. 46

Module Introduction: Factoring Transaction Costs into the Financing Decision

In this module, you will examine some of the transaction costs that influence financing decisions. You will examine some

of the direct and indirect costs of initial public offerings and explore examples. You will also have an opportunity to confirm

mastery of key concepts through an activity related to weighing the costs related to an initial public offering.

Copyright © 2012 eCornell. All rights reserved. All other copyrights, trademarks, trade names, and logos are the sole property of their respective owners. 47

Transaction Costs

In this video, Professors Carvell and Gibson offer an explanation of initial public offerings (IPOs) and explain for the

non-financial professional what they are, how they work, and what some of the related costs are.

Copyright © 2012 eCornell. All rights reserved. All other copyrights, trademarks, trade names, and logos are the sole property of their respective owners. 48

Read: IPO Direct Costs

Key Points

Direct costs: underwriting syndicate fee ("spread"), filing fees, legal fees, taxes

Spread = 7% of IPO proceeds

Other direct costs = 4% of IPO proceeds

When a firm issues shares of its stock to the public for the first time, certain direct and indirect costs are involved. Let's

consider the direct costs.

The firm hires investment bankers to underwrite the equity issue for the IPO. The investment bankers, referred to as the

charge a fee that is the difference (usually expressed as a percentage) between the price theunderwriting syndicate,

issuing firm receives and the offer price at which shares are sold to investors. This underwriting syndicate's fee is typically

referred to as the .spread

Other direct costs incurred by the issuing firm above and beyond the spread include filing fees, legal fees, and taxes.

Historically, the spread averages approximately 7% of the IPO proceeds, and other direct costs average about 4% of IPO

proceeds. Thus, the total direct costs associated with an IPO are about 11% of the money raised.

While the direct costs of an IPO are quite large, there are also additional and equally important costs that arise because of

asymmetric information issues, covered next.

Copyright © 2012 eCornell. All rights reserved. All other copyrights, trademarks, trade names, and logos are the sole property of their respective owners. 49

Read: Akerlof's Lemons Problem

Key Points

Developed by Nobel Prize-winner George Akerlof

Information asymmetry: sellers know more than

buyers do

Let's talk about the market for lemons. George Akerlof, back in 1970, on his way to a Nobel Prize, wrote a paper on the

market for lemons. Now, he wasn't talking about the fruit-a lemon-he was talking about the market for used cars. "Lemon"

is an American term for a used car that doesn't work well.

In the used car market, imagine there are good cars worth $20,000 and there are lemons worth only $10,000. In this

market, the sellers of these cars, who've been driving them around for a number of years-they know whether the car

they've been driving is a good car or a lemon.

The buyers, however, cannot tell whether it's a good car or a lemon just by looking at it and, perhaps, taking it for a short

test-drive.

In this market for used cars, the sellers know more about the condition of the car than do the buyers. This is a market that

financial economists would say is characterized by .asymmetric information

How will this market work when the buyers and sellers are asymmetrically informed?

Suppose half of the cars for sale are good and the other half are lemons. First, let's think about what would happen if all

the sellers were to sell their cars regardless of type. What is the fair price of a car in this market? Well, half the cars are

good cars with a value of $20,000. The other half are lemons with a value of $10,000. It's half and half. Well, the fair price

of a car would be $15,000.

Now what will happen if we give sellers, who own good cars, a choice of whether or not they want to sell? What if the price

for used cars is $15,000? As a seller of a good car, will you sell a car worth $20,000 for $15,000? The answer is no.

Type of Car Value

Good $20,000

Lemon $10,000

Fair price of used car = (1/2) $20,000 + (1/2) $10,000 = $15,000

Copyright © 2012 eCornell. All rights reserved. All other copyrights, trademarks, trade names, and logos are the sole property of their respective owners. 50

Now let's think about buyers in this market. What will buyers presume if they see a car for sale? Buyers will know that the

sellers of the good cars are not selling. If the buyers see a car for sale, they will correctly presume that it is a lemon for

sale. They're only willing to pay $10,000.

If we leave buyers of used cars and sellers of used cars to their own, the market will collapse. Only lemon cars will

exchange hands at lemon prices. When Akerlof wrote this paper, it was a fair representation of the used-car market. The

used-car market, however, has changed dramatically.

When an entrepreneur named Wayne Huizenga looked at the used-car market and saw that the sellers of good cars could

not sell because of asymmetric information, he saw an opportunity. He created what is known as an . In thisintermediary

case, it was an intermediary for used cars. That was his AutoNation.

Here's Huizenga's idea: AutoNation would hire competent mechanics. These mechanics can look at the cars that used-car

sellers were selling. They can ascertain whether it was a good car or a lemon car. Huizenga would only buy the good cars

and would then offer these good cars for sale. AutoNation would be in the business of selling good cars. As a buyer going

to AutoNation, do you have any confidence that you'd be getting a good car rather than a lemon? Well, let's think about

AutoNation's business if it decided to pull a fast one and sell lemons. Soon news would get out that AutoNation was selling

lemons. How do you think that would be for business at AutoNation? Well, nobody would be willing to pay good-car prices

for what they thought to be a lemon going forward. AutoNation's business model would no longer work. AutoNation's

reputation would be lost. The key that Huizenga recognized here with AutoNation is that, for AutoNation, the selling of a

car could be a repeated game. AutoNation was going to be in business every day selling good cars. For sellers of used

cars, it's a one-time deal. They don't have a reputation they need to protect. So if they were to pass off a lemon as a good

car, true, they lose their reputation. But they're only selling one car. Huizenga, by stepping between the used-car sellers

and the used-car buyers, putting AutoNation's reputation on the line, successfully created a market for good used cars.

Copyright © 2012 eCornell. All rights reserved. All other copyrights, trademarks, trade names, and logos are the sole property of their respective owners. 51

Read: Creating a Truthful Prospectus

Key Points

The prospectus presents an information asymmetry problem

IPO market: issuing firms and potential investors

The problems that come about due to information asymmetries are exemplified in the market for initial public offerings

(IPOs). This is the market for private firms that are issuing equity for the first time to the public. Let's think about the

structure of the information in this market and why it might present challenges.

In the IPO market, we have two groups: the issuing firms and the potential investors. Think about what the management of

the issuing firm knows that the outside potential investors don't know. Clearly, management knows more about the

operations, the risks, and the potential of the firm. It knows much more about the value of the firm than do outside

investors. Now let's look at the issuing process to see how this asymmetry plays out.

The first step in the process is for the issuing firm to put together a . The prospectus provides information aboutprospectus

the management of the company, the risks and opportunities associated with it, the products it offers, historical financial

information, financial projections going forward, and more.

Next, the prospectus is sent to potential investors, all of whom have received or will receive prospectuses from a hundred

or so other firms. Then the potential investors must differentiate the good companies from the bad.

Of course, the prospectuses are written by the owners of the issuing firms, who might be inclined to take this opportunity

to stretch the truth a bit to make their companies look more attractive than they actually are. Firm owners have no

motivation to tell the truth; potential investors have no way to tell the good firms from the bad.

The prospectus presents an information asymmetry problem. The solution is found in an intermediary-the investment

banker. The investment banker will send in a team of experts to go over the inventory and all the financials, talk to

management, and consider the marketing plans. Then, with this unbiased information, the investment banker creates a

prospectus that prospective investors can trust.

The investment banker brings firms public time after time: it's a repeated game. To play the game at all, the investment

banker must have a spotless reputation. For this reason, he or she is going to be perfectly forthright and truthful in every

prospectus. Prospective investors know this, and so the information asymmetry problem is solved.

Copyright © 2012 eCornell. All rights reserved. All other copyrights, trademarks, trade names, and logos are the sole property of their respective owners. 52

Read: The Firm Commitment Process

Key Points

IPOs are underpriced

Underpricing leads to truth-telling in an asymmetric

information market

On the first day a stock trades in the public markets on average, it goes up about 15%. What that means is that as an

investor, if you were to invest in every single IPO, you would earn on average 15%. It seems like a great deal: a 15%

one-day return.

IPOs are underpriced. Let's turn our attention to understanding why.

Think about the market for initial public offerings, the structure of the information in this market, and the challenges we

face. We have a problem: the potential investors are not going to reveal what they're willing to pay for the shares in the

issuing firm. How can the investment banker solve this problem? Well, the investment banker has set up a game. It's

called the .firm commitment process

Here's how the process works:

First Step

The investment banker puts together the prospectus, and part of that prospectus, stamped on the front cover, will be

something called the initial offer range. As an example, the investment banker might say that they expect the offer to price

out at between $15 to $17 per share. That's called the . It's the investment banker's best estimate of theinitial offer range

price at which the shares will sell into the market-$15 to $17 in this case.

Second Step

Then what the investment banker does is take a road trip. The investment banker, together with the firm's management,

conducts a road show. They present the story of the firm. The investors who attend the road show, called regular investors

, have a chance to ask questions of management and refine their thoughts and opinions of what's contained in the

prospectus. An important aspect of the road show is that indications of interest are gathered. The investment banker asks

each of the regular investors, "What is your interest in this particular issue?" "How many shares would you like to buy at,

oh say, $10? How about $12? $15? $17? Do you still like it at $20? How about $25?" In effect, what the investment

banker is collecting from each regular investor is their individual demand curve for the issue.

Building the Book

This process, where these indications of interest are gathered, is called . The regular investors are thebuilding the book

important money managers such as mutual funds, pension funds, and endowments. Basically the smart money in the

market. It's the same group of investors that is invited back time after time. It's the regular group. The investment banker

has gathered, from each of the regular investors, the indication of interest or their individual demand curve.

Copyright © 2012 eCornell. All rights reserved. All other copyrights, trademarks, trade names, and logos are the sole property of their respective owners. 53

Suppose you're one of the regular investors. Will you tell the truth freely and willingly? The investment banker's challenge

is to get you to tell the truth.

The Rules of the Game

The rules of the firm commitment process:

The indications of interest are not binding.

All investors get their shares at the same price.

The offer price is related to the strength of the indications of interest or the strength of the book.

The investment banker promises to maintain a direct link between the and the strength and breadth of thediscount*

indications of interest.

If the regular investors as a group say they really like the issue, the shares will be priced higher.

If the regular investors as a group say they don't like the issue, the shares will be priced lower.

Now stop and think for a moment. If you're one of the regular investors, will you tell the truth? If you really like the offer, will