Pro Team Auction Co., LLC. 1715 Garden Village Drive White ...

Hafelein White LLC

22 W. Washington, Suite 1500, Chicago, IL 60602 Phone: (312) 854-8062 | Fax: (312) 265-3965 | www.hafeleinwhite.com

Law Offices

What the Institutional Investment Manager Needs to Know About SEC Reporting under

Section 13(f)

By Cory White1 and Blake Brockway

2

INTRODUCTION

Since the mid-1970‟s institutional investors have been required to report their security

holdings to the public under Section 13(f) of the Securities Exchange Act.3 The measure was

initially enacted to increase public confidence in the United States securities market, and has

evolved into a useful tool for the U.S. investor. Many media outlets now report institutional

holdings, and some industry professionals have even suggested that individual investors can

profit from mimicking the holdings of institutional investors.4 Despite its utility, Section 13(f)

has been neglected by the U.S. Securities and Exchange Commission (the “Commission”). On

September 27, 2010, the Commission‟s Office of Inspector General released a detailed review of

the agencies practices and procedures for enforcing the Section 13(f) Reporting Requirements.5

The report concluded that the several improvements were needed in order to fulfill the

Commission‟s statutory obligation to provide useful and reliable data.6 Among the other things,

the OIG report recommended that the Commission designate a department to review the

completeness and accuracy of Form 13F.7

1 Cory White is a 2009 graduate of Depaul University College of Law. He is currently a managing member at the

law firm Hafelein | White, LLC where he focuses his practice on securities compliance. 2 Blake Brockway is a 2009 graduate of DePaul University College of Law. He has worked in various compliance

environments, previously serving as a legal intern for the U.S. Securities and Exchange Commission. 3 Filing and Reporting Requirements Relating to Institutional Investment Managers, Release No. 34-14852 (June 15,

1978), 43 Fed. Reg. 26700-01 (June 22, 1978). 4 What Hedge Fund Managers Know About Making Money, available at http://www.marketwatch.com/story/what-

hedge-fund-managers-know-about-making-money-2011-03-25 5 Office of Inspector General, Review of the SEC‟s Section 13(f) Reporting Requirement, Report No. 480

(Securities and Exchange Commission, September 27, 2010). 6 Review of the SEC‟s Section 13(f) Reporting Requirement, Report No. 480 at 4-5.

7 Review of the SEC‟s Section 13(f) Reporting Requirement, Report No. 480 at 9.

2 of 31

In the wake of the OIG report the Commission will be increasing its review of Form 13F

filings as well as enforcement actions against institutional investment managers that are failing to

meet the Section 13(f) reporting obligations. Current filers could also face audits, reviews, or

enforcement actions as the Commission implements procedures to substantively review Form

13F Holding Reports for the first time. As the securities industry endures the regulatory upswing

resulting from the recent recession, flash crash, and other market events and the Commission

prepares to expand its review of Section 13(f) reporting, now is the ideal time to review the

institutional investment manager reporting requirements. This paper is intended to serve as a

refresher for current reporting managers as well as a guide for first time filers. The paper is

organized into three substantive sections. The first section provides a brief summary of the

history, purpose, utility of Section 13(f) and a detailed overview of the reporting requirements.

This section also reviews the definition for the key terms used in the statute, the reporting

threshold, and when and how to report. The second section reviews the possible penalties for

failing to file Form 13F and discusses a recent enforcement action that resulted in a $100,000

penalty for an institutional investment manager that willfully failed to file Form 13F. The third

section provides technical details for completing the Form 13F Information Table and requesting

confidential treatment of certain holdings information. Finally, sample forms and templates are

provided that should be useful for reporting managers.

SECTION I – OVERVIEW OF SECTION 13(F) REPORTING

A) An Overview of the History, Purpose, and Utility of Section 13(f)

Section 13(f) was enacted as a part of the Securities Acts Amendments of 1975 with the

intent “to create in the Commission a central repository of historical and current data about the

3 of 31

investment activities of institutional investment managers.”8 The institutional investment

reporting requirement outlined in Section 13(f) was adopted to achieve two objectives.9 The first

objective was to improve the availability of factual data to evaluate the influence, impact, and

public policy implications of institutional investment managers on the securities markets.10

The

second objective was to establish a uniform reporting standard and centralized database of

institutional holdings that is gathered, processed and disseminated by the Commission.11

Congress believed that collecting and disseminating data about institutional investment

managers‟ holdings would simulate a higher degree of confidence in the integrity of the U.S.

securities markets and would be useful to regulatory bodies in fulfilling their responsibilities.12

President Gerald Ford echoed these sentiments and specifically referenced the reporting

requirements outlined in Section 13(f) when he signed the Securities Act of 1975 into law.

Public confidence is a vital ingredient if our capital markets are to continue to

attract a wide variety of investors. Though large institutions have become

increasingly active as owners and traders of securities, individuals still represent

the backbone of the American capital system. This act provides important new

safeguards which will help insure public trust in the securities markets. Among

these safeguards are new rules for brokers' financial strength and accountability.

The act imposes new restrictions on "self-dealing" to eliminate a potential conflict

of interest and deny institutions a special advantage over individual investors. The

8 Filing and Reporting Requirements Relating to Institutional Investment Managers, Release No. 34-14852 (June 15,

1978), 43 Fed. Reg. 26700-01 (June 22, 1978). 9 Review of the SEC‟s Section 13(f) Reporting Requirement, Report No. 480 at 1(citing Filing and Reporting

Requirements Relating to Institutional Investment Managers, Release No. 34-14852 (June 15, 1978), 43 Fed. Reg.

26700-01 (June 22, 1978)). 10

Filing and Reporting Requirements Relating to Institutional Investment Managers, Release No. 34-14852 (June

15, 1978), 43 Fed. Reg. 26700-01 (June 22, 1978). 11

Filing and Reporting Requirements Relating to Institutional Investment Managers, Release No. 34-14852 (June

15, 1978), 43 Fed. Reg. 26700-01 (June 22, 1978). 12

Report of Senate Comm. on Banking, Housing and Urban Affairs, S. Rep. No. 94-75 at 78 (1975),

reprinted in 1975 U.S.C.C.A.N. 179, 261. See also Division of Investment Management: Frequently Asked

Questions About Form 13F (Securities and Exchange Commission, May 2005), Question 1

http://www.sec.gov/divsions/investment/13ffaq.htm (“Congress believed that this institutional disclosure program

would increase investor confidence in the integrity of the United States securities markets”).

4 of 31

act further requires periodic disclosure by institutional investors of their holdings

and transactions in securities.13

Institutional holdings reports are currently used by regulators, academics, and industry

participants.14

The Commission has identified several uses for the information reported pursuant

to Section 13(f). Commission Economists utilize Form 13F data to analyze holding information,

formulate penalty recommendations, and conduct valuation comparisons.15

Regulators also

utilize Form 13F academic research to make informed rule-making decisions.16

In fact, the

Commission indicated that it utilized research based on institutional holdings reports while

formulating the recently adopted Proxy Access rules adopted under the Dodd-Frank Wall Street

Reform and Consumer Protection Act.17

Media outlets utilize Form 13F to report institutional

ownership of publicly traded companies,18

and investment professionals utilize this information

to glean market intelligence. The legislative history, purpose, and uses of Form 13F can be

helpful in understanding the sometimes complicated statute and corresponding rules.

B) Overview of the Section 13(f) Reporting Requirements

Section 13(f) requires every institutional investment manger that exercises investment

discretion with respect to accounts holding an aggregate fair market value of at least

$100,000,000 in Section 13(d)(1) securities to file reports in such form, for such periods, and at

such times as the Commission may prescribe by rule.19

Under the statute, the reports must

include at least the name of the issuer, title of the class, CUSIP number, number of shares or

13

Gerald R. Ford: Statement on Signing the Securities Acts Amendments1975, available at

http://www.presidency.ucsb.edu/ws/index.php?pid=4970#ixzz1GQuyvDWr (emphasis added).

14 Review of the SEC‟s Section 13(f) Reporting Requirement, Report No. 480 at 7.

15 Review of the SEC‟s Section 13(f) Reporting Requirement, Report No. 480 at 7-8.

16 Review of the SEC‟s Section 13(f) Reporting Requirement, Report No. 480 at 7.

17 Review of the SEC‟s Section 13(f) Reporting Requirement, Report No. 480 at 8.

18 See e.g. MSN Money Ownership, Institutional Ownership, 5% Ownership, available at

http://moneycentral.msn.com/ownership 19

15 U.S.C. § 78m (f)(1).

5 of 31

principal amount, aggregate fair market value, and voting authority for each equity security held

on the last day of the reporting period.20

Section 13(f) also requires the reports to be filed for

periods not longer than one year or shorter than one quarter.21

In order to fulfill the requirements of Section 13(f) the Commission adopted Rule 13f-1.22

Rule 13f-1 specifies the reporting periods and other procedures for filing Form 13F. The rule

requires institutional investment managers to file Form 13F within 45 days after the last day of

the calendar year that it first reaches the $100,000,000 reporting threshold and within 45 days of

the last day of the first three calendar quarters of the subsequent calendar year.23

The

Commission also adopted Form 13F as a standardized report for institutional investment

managers.24

The terms “institutional investment manager” and “investment discretion” play an

important role in determining whether the Section 13(f) reporting requirements apply to a

specific investment manager. Importantly, applicability of Section 13(f) does not turn on

whether or not the investment manager is deemed an investment advisor under Section

202(a)(11) of the Investment Advisors Act. Additionally, reporting under any other Section of

the federal securities laws does not alleviate the need to report under Section 13(f) if the

reporting requirements are met.

20

15 U.S.C. § 78m (f)(1). 21

15 U.S.C. § 78m (f)(1). 22

17 C.F.R. § 13f-1(a). 23

17 C.F.R. § 13f-1(a) See also Division of Investment Management Frequently Asked Questions About Form 13F,

Question 28. (noting that an institutional investment manager should file its first Form 13F for the December quarter

for the calendar during which it first reaches the $100 million filing threshold, and will then need to submit filings

for the

March, June, and September quarters of the following calendar year, even if the market value of its Section

13(f) securities falls below the $100 million level) 24

17 C.F.R. § 249.325.

6 of 31

a) Determination of Institutional Investment Manager Status

Section 13(f)(5)(A) states, “the term „institutional investment manager‟ includes any

person, other than a natural person, investing in or buying and selling securities for its own

account, and any person exercising investment discretion with respect to the accounts of another

person.”25

The Commission has clarified that an institutional investment manager is either (1) an

entity that invests in, or buys and sells securities for its own account; or (2) a natural person or an

entity that exercises investment discretion over the account of any other natural person or

entity.26

In the first category, any entity that manages and has investment discretion over its own

securities accounts (also referred to as “investment accounts” throughout) is considered an

institutional investment manager, including corporations, banks, and pension funds that manage

their own portfolios and any other entity that manages its own investments.27

Importantly, this

category of institutional investment manager does not include natural persons who buy and sell

securities for their accounts. In the second category, both natural persons and entities can qualify

as institutional investment managers if they manage and exercise investment discretion over the

securities accounts of any other person, including other entities.28

Broker-dealers, proprietary

trading firms, investment advisors, hedge funds and others that manage the accounts of others

will be considered institutional investment managers under Section 13(f). Importantly, the

definition of institutional investment manager is not pinned to the value determination that

triggers the reporting requirement, i.e. whether or not someone is considered an institutional

investment manager is not dependent on the collective monetary value of the securities accounts

managed.

25

15 U.S.C. § 78m (f)(5)(A). 26

See Division of Investment Management Frequently Asked Questions About Form 13F, Question 3. 27

See Division of Investment Management Frequently Asked Questions About Form 13F, Question 3. 28

See Division of Investment Management Frequently Asked Questions About Form 13F, Question 3.

7 of 31

b) Determination of Investment Discretion

In order to trigger the reporting requirement under Section 13(f), the institutional

investment manager must exercise investment discretion over investment accounts that hold

more than $100 million of Section 13f securities.29

Rule 13f-1 states that “investment

discretion” shall have the meaning set forth in Section 3(a)(35) of the Securities Exchange Act

(“Act”).30

Under the Act, an institutional investment manager exercises investment discretion

over an account if, directly or indirectly, such person is (1) authorized to determine what

securities shall be purchased or sold by or for the account; (2) makes decisions as to what

securities shall be purchased or sold by or for the account even though some other person may

have responsibility for such investment decisions; or (3) otherwise exercises such influence with

respect to the to the purchase and sale of securities by or for the account as the Commission may

determine by rule.31

It is important to stress the implication of the second instance, which may

deem an institutional investment manager to have shared investment discretion.

Any manager that has control over another person, such as a natural person, entity, or

government instrumentality, that exercises investment discretion over any investment account

will also be considered to have investment discretion over that same account.32

For example, if a

parent company controls a subsidiary that acts as an investment management firm that

determines what securities are held in an investment account, both the parent company and the

subsidiary will be deemed to have investment discretion over the account.33

When a parent

company controls a subsidiary that acts as an institutional investment manager both entities will

29

15 U.S.C. § 78m (f). 30

17 CFR § 240.13f-1. 31

15 U.S.C. § 78c(a)(35). 32

See Division of Investment Management Frequently Asked Questions About Form 13F, Question 6. 33

See Division of Investment Management Frequently Asked Questions About Form 13F, Question 6; See also 17

C.F.R. § 240.13f-1.

8 of 31

report that they exercise shared investment discretion.34

Reporting shared investment discretion

will be specifically touched on in Section III of this paper.

C) Type of Investment Account that Triggers Reporting

Section 13(f) requires that only institutional investment managers that exercise

investment discretion over investment accounts that total $100,000,000 or more in Section 13(f)

securities must report those holdings on Form 13F.35

Each Quarter the Commission publishes a

List of Section 13F Securities (the “Official List”).36

Only securities on the Official List

contribute to that $100,000,000 reporting threshold.37

The Official List includes exchange-

traded or NASDAQ quoted equity securities that include: stocks, equity options and warrants,

shares of close-end investment companies, shares of exchange traded funds, and certain

convertible debt securities.38

Securities not included on the Commission‟s list should not be

counted toward the $100,000,000 threshold value.

Is it very important to note that calculating the value of the securities necessary for hitting

the $100,000,000 threshold may not be the same as calculating value when compiling the Section

13(f) report. For example, in looking to calculate the $100,000,000 threshold the institutional

investment manager should look to the value of any options, as noted on the Commission‟s

Official List, at the end of the reporting period and not the value of the underlying securities.39

34

See Division of Investment Management Frequently Asked Questions About Form 13F, Question 6; See also 17

C.F.R. § 240.13f-1. 35

15 U.S.C. § 78m (f); 17 CFR § 240.13f-1. 36

17 CFR § 240.13f-1; See “Official List of 13(f) Securities” available at

http://www.sec.gov/divisions/investment/13flists.htm. 37

17 CFR § 240.13f-1; See “Official List of 13(f) Securities” available at

http://www.sec.gov/divisions/investment/13flists.htm. 38

See Division of Investment Management Frequently Asked Questions About Form 13F, Question 7.

39 See Form 13F, Special Instructions at 11(17 C.F.R. § 249.325).

9 of 31

When actually reporting those option holdings the firm must report the value as if it owed the

securities underlying those options.40

Finally, the securities of the institutional investment manager or a controlled entity, even

if listed by the Commission as Section 13(f) securities will not be considered Section 13(f)

securities for the purpose of reaching the $100,000,000 threshold.41

Still, if the institutional

investment manager otherwise reaches the $100,000,000 threshold it must report holdings of its

own securities if listed by the Commission.42

Control, for this purpose or as mentioned

throughout this paper is deemed to mean operational control.

D) When and How and to Report

Just as important as knowing whether or not Section 13(f) reporting is required is

knowing when and how to report.

a) When to Report

An institutional investment manager will have to report under Section 13(f) if, at the end

of the last trading day of any month during the current the calendar year, holdings of Section

13(f) securities reach the $100,000,000 threshold. The institutional investment manager will

have to report the holdings at the end of that initial period ending on December 31.43

Following

this initial period, the institutional investment manager must reporting holdings as of the last day

of each of the first three calendar quarters of the subsequent calendar year, regardless of the

value of the holdings in questions.44

At the end of each reporting period (the initial and

40

See Form 13F, Special Instructions at 4-5 (17 C.F.R. § 249.325). 41

17 CFR § 240.13f-1. 42

17 CFR § 240.13f-1. 43

15 U.S.C. § 78m (f). 44

15 U.S.C. § 78m (f); 17 CFR § 240.13f-1.

10 of 31

subsequent quarterly periods) the institutional investment manager will have forty-five days to

submit the report. To illustrate:

Super Investment Management, Inc. reaches $100,000,000 in Section 13(f) securities for

the first time in March of 2010, as calculated at the end of the last trading day in March.

The first reporting period will begin on October 1, 2010 and end on December 31, 2010.

On the last day of that reporting period Super Investment Management must report its

holdings as of that last day, namely December 31, 2010. It will have forty-five days after

the end of the reporting period to compile and file the report. It will also have to file

reports as of the end of March 2011, June 2011, and September 2011, which are not

dependent on holding amounts of 2011, i.e. the amount may be below $100,000,000 at

the end of the subsequent quarterly reporting periods. Again, the holdings as of the last

day of the quarter must be reported, and the company will have forty-five days to compile

and file the report.

Whether or not reports will be required into 2012 will depend on whether or not the

holding amounts of 2011 reach the $100,000,000 threshold during the end of any

calendar month in 2011. In this instance, if Super Investment Management holds

$100,000,000 in Section 13(f) securities at the end of any calendar month in 2011 this

will trigger reporting requirements at the end of the December 2011 and into 2012.

b) How to Report

Compiling the Section 13(f) report can be a complex process and a qualified compliance

expert or attorney should be consulted. The information required must be submitted on a Form

13F Holdings Report using the Commission‟s EDGAR system (Electronic Data Gathering,

Analysis, and Retrieval system). All filers must apply for a new CIK (Central Index Key) for the

Section 13(f) filing, although, if the filer in question has a CIK used only to file a Schedule 13D

or Schedule 13G, the filer must use that CIK number.45

The Form 13F Holdings Report must be

filed after filing out the cover page, the summary page, and the information table, which lists

each holding of Section 13(f) securities line by line.

45

See Division of Investment Management Frequently Asked Questions About Form 13F, Question 18.

11 of 31

SECTION II - WHY FILE: THE QUATTRO ACTION

Failing to file the Section 13(f) report can have harsh consequences on the institutional

investment manager, consequences that include both monetary and non-monetary sanctions.

One of the most illustrative SEC administrative proceedings on the consequences of not filing is

The Matter of Quattro Global Capital, LLC, decided in August of 2007.46

Quattro was a

registered investment advisor to a collection of hedge funds with assets of approximately

$900,000,000 (collectively) as of 2007.47

Quattro directed the investment strategies of the funds

in question.48

From 2002 to 2005, although the $100,000,000 threshold was reached, Quattro

repeatedly failed to file the Section 13(f) report.49

Quattro had repeat notice of the requirement

as early as March 2004, yet no steps were taken to rectify the fact that no filings had been

made.50

This serious failure was found out during a Commission inspection of Quattro in

2005.51

On July 20, 2005 Quattro filed the current Form 13F for the quarter ending on June 30th

and fourteen retrospective Form 13Fs dating back to 2002.

Prior to finding it appropriate to issue sanctions against Quattro, the Commission was

stressed the purpose of the Section 13(f) report. The Commission stated:

“The purpose of this disclosure requirement is to collect and disseminate to the public

information about the holdings and investment activities of institutional money managers

in order to assist investors, issuers, and government regulators . . . The Congressional

purpose in enacting Section 13(f) of the Exchange Act was „to create a central depository

of historical and current data about the investment activities of institutional investment

managers‟ to assist investors and government regulators. The information is valuable to

the Commission because it „facilitates consideration of the influence and impact of

46

Quattro Global Capital, LLC, File No. 3-12725 (Securities and Exchange Commission, August 15, 2007)

(Administrative Proceeding). 47

Quattro Global Capital, LLC, File No. 3-12725. 48

Quattro Global Capital, LLC, File No. 3-12725. 49

Quattro Global Capital, LLC, File No. 3-12725 (Quattro had reached the $100,000,000 threshold as early as

2001). 50

Quattro Global Capital, LLC, File No. 3-12725. 51

Quattro Global Capital, LLC, File No. 3-12725; See 15 U.S.C. § 80b-9 for the Commission‟s power to inspect.

12 of 31

institutional investment managers on the securities markets and the public policy

implications of that influence.”52

The Commission found that Quattro willfully violated Section 13(f) for the period of 2002 to

2005. The Commission has the power to sanction under any applicable provision of the federal

securities laws. Accordingly, the Commission sanctioned Quattro under Section 203(e) of the

Investment Advisors Act by censuring it as a registered investment advisor.53

Under Section

21C of the Exchange Act, Quattro was ordered to cease any current or future violations of

Section 13(f). Finally, Quattro was fined $100,000 in civil penalties under Section 21B of the

Exchange Act.54

Perhaps more importantly, Quattro would potentially now be on the

Commission‟s watch list and have its activities more open to scrutiny and frequent audits by the

Commission.

A very important take away from this is that penalties will only be handed down for

willful violations of Section 13(f), a conclusion based both on the opinion of the Commission

and Section 21C of the Exchange Act.55

Still, under both relevant case law and Commission

interpretation “willful” means intentionally committing the act that constitutes the violation and

without the requirement that the actor also be aware that he is violating one of the rules or

sections of the securities acts.56

Although the Commission spoke of notice in the Quattro

decision, institutional investment managers covered under Section 13(f) need not know of the

filing requirement to face sanctions by the Commission. Knowing of the filing requirement and

still not complying with it, may lead to more serious sanctions. If an institutional investment

52

Quattro Global Capital, LLC, File No. 3-12725. 53

Quattro Global Capital, LLC, File No. 3-12725; 15 U.S.C. § 80b-3(e). 54

Quattro Global Capital, LLC, File No. 3-12725; See 15 U.S.C. § 78u-2 for the ability of the Commission to levy

civil penalties. 55

See 15 U.S.C. § 78u-3. 56

See Generally Wonsover v. SEC, 202 F.3d 408, 414 (D.C. Cir. 2000); See Generally Tager v. SEC, 344 F.2d 5,8

(2nd Cir. 1965).

13 of 31

manager comes to find out about the filing requirement long after those duties have accrued, the

best course of action is to file the report that is immediately due and all retrospective reports.

SECTION III – PARTICULAR ISSUES WITH

SECTION 13(F) FILINGS

A) Specific Reporting Instructions

As a preliminary note, three types of Form 13F reports are currently used: a Form 13F

Holdings Report is used if all of the manager‟s Section 13(f) securities are listed on the report, a

Form 13F Combination Report is used if some of a manager‟s securities are reported on another

report, and a Form 13F Notice Report is used if all of the manager‟s securities are reported on

another report (typically used by a parent company when a subsidiary files a Form 13F Holdings

Report).57

The remainder of this section will provide guidance on common reporting challenges

for completing Form 13F Holdings Reports. Combination Reports and Notice Reports are

reduced versions of the Holdings Report; therefore, the instructions that follow are also

applicable to these of reports.58

A Form 13F Holdings Report contains three sections: a cover page, summary page and

information table.59

The cover page contains basic information about the filing, such as the

name, address, and 13F File Number of the institutional investments manger, person signing on

behalf of the reporting manager, date of the filing, and report type.60

The summary page

contains a list of other managers, the total number of entries from the information table, and the

total value of the positions reported.61

The Form 13F Information Table is the substantive

portion of the report. It contains ten sections (aggregated into eight columns): Name of Issuer,

57

See Division of Investment Management Frequently Asked Questions About Form 13F, Question 33. 58

See Form 13F, Special Instructions, at 4 (17 C.F.R. § 249.325). 59

Form 13F, Special Instructions, at 3 (17 C.F.R. § 249.325). 60

Form 13F, Special Instructions, at 3 (17 C.F.R. § 249.325). 61

Form 13F, Special Instructions, at 4 (17 C.F.R. § 249.325).

14 of 31

Title of Class, CUSIP, Value, Shares or Principal Amount, a notation for Shares or Principal,

Put/Call, Investment Discretion, Other Managers, and Voting Authority, which has three sub

columns (Sole, Shared, and None).62

To an initial observer, the Form 13F Information Table

appears simple and straightforward. However, this seemingly simple table is based on obscure

instructions that may seem counter-intuitive to investment professionals.

Not all security positions need to be reported on the Information Table. By carefully

reviewing the Official List of Section 13(f) securities and utilizing the small holding exception

institutional investment managers can minimize the burden of publicly reporting certain security

positions. Other areas that give rise to reporting problems include: dealing with short positions,

calculating market value, and options reporting.

The Name of Issue, Title of Class, and CUSIP columns on the information table should

match the Commission‟s Official List. At the end of each calendar quarter the Commission

publishes an Official List, which includes most but, not all, publicly traded equity securities.63

Only positions on the list need to be reported on Form 13F and institutional investment managers

are entitled to rely upon the most recent iteration of the Official List.64

Options are listed

separately and do not need to be reported on Form 13F when only the underlying stock appears

on the Official List. In addition, securities with a deleted status on the Official List do not need

to be reported on Form 13F. If the reporting manager‟s goal is to minimize the positions

reported, a careful review of the Official List is likely to yield some results. A recent report

published by the Commission‟s Office of Inspector General revealed that the Commission

utilizes a third party to prepare the Official List, and that the list is not audited or reviewed by an

62

Form 13F, Special Instructions, at 4-5 (17 C.F.R. § 249.325). 63

17 C.F.R. § 13f-1(c). 64

17 C.F.R. § 13f-1(c).

15 of 31

independent party or the Commission‟s staff.65

Recently listed securities, particularly options,

and securities that have recently undergone a corporate action are often omitted from the Official

List.

Reporting managers can also omit certain positions that qualify for the small holding

exception. Under Form 13F Special Instruction number ten, reporting managers may omit

positions if they hold fewer than 10,000 shares (or less than $200,000 principal amount in the

case of convertible debt securities) and less than $200,000 aggregate fair market value (and

option holdings to purchase only such amounts).66

Both of these requirements must be met in

order to omit small positions.67

As indicated by the permissive language, these positions may be

included in the filing at the discretion of the reporting manager.68

This instruction could be

particularly useful for hedge funds and proprietary trading firms that are holding small positions

in lightly traded symbols, such as micro-cap companies, and would prefer to maintain

confidentiality.

The next step in completing the information table is determining the number of shares or

principal and the market value of each security. Certain convertible debt securities can be found

on the Official List, and the principal amount, market value and Column 5 designation “PRN”

should be listed for these securities.69

The number of shares of long stock (including loaned

shares) and market value of those shares (rounded to the nearest thousand dollars) should be

reported for stock securities.70

Short stock is not included on Form 13F and should not be

65

Office of Inspector General, Review of the SEC‟s Section 13(f) Reporting Requirement, Report No. 480, at 14-15

(Securities and Exchange Commission, September 27, 2010). 66

Form 13F, Special Instructions, at 4 (17 C.F.R. § 249.325). 67

See Division of Investment Management Frequently Asked Questions About Form 13F, Question 39. 68

See Division of Investment Management Frequently Asked Questions About Form 13F, Question 39. 69

See Division of Investment Management Frequently Asked Questions About Form 13F, Question 7. 70

See Division of Investment Management Frequently Asked Questions About Form 13F, Question 41.

16 of 31

deducted from a long position.71

For emphasis, Questions 41 from the Commissions Frequently

Asked Questions About Form 13F is printed below.

Question 41

Q: What about short positions?

A: You should not include short positions on Form 13F. You also should not

subtract your short position(s) in a security from your long position(s) in

that same security; report only the long position.72

The methodology for calculating both the number of “shares” and market value of

options will strike industry professionals as bizarre and contrary to the purported purpose of

Section 13(f). Like stock, only long options positions are reported on Form 13F; thus written or

short positions in calls and puts should be excluded or ignored.73

Long options positions are

converted to shares based on the number of shares each option contract controls.74

Although the

industry standard is 100 shares, special dividends or other corporate actions sometime impact the

number of shares per contract. Market value for options is calculated by taking the number of

shares as calculated above times the market price for the underlying stock.75

Finally, all options

series are aggregated onto two lines, one line for puts and a separate line for calls, using the Title

of Class and CUSIP for the underlying instrument.76

No discussion of options and Form 13F is complete without an important note on options

value and the $100,000,000 reporting threshold. For reporting purposes, options contracts are

converted to shares controlled and listed at the market value of the shares controlled.77

However,

71

See Division of Investment Management Frequently Asked Questions About Form 13F, Question 41. 72

See Division of Investment Management Frequently Asked Questions About Form 13F, Question 41. 73

See Division of Investment Management Frequently Asked Questions About Form 13F, Question 43. 74

Form 13F, Special Instructions, at 4-5 (17 C.F.R. § 249.325). 75

Form 13F, Special Instructions, at 4-5 (17 C.F.R. § 249.325). 76

See Division of Investment Management Frequently Asked Questions About Form 13F, Question 44. 77

Form 13F, Special Instructions, at 11 (17 C.F.R. § 249.325).

17 of 31

for purposes of the $100,000,000 reporting threshold options are valued at their actual market

value.78

In Column 6, reporting managers are asked to list one of three types of investment

discretion: sole, shared-defined, or shared other.79

Sole investment discretion occurs when a

single filer has control of the securities reported on Form 13F.80

Reporting sole means that you

do not control another reporting person, are not controlled by another reporting person, and do

not otherwise share investment discretion with another institutional investment manager.81

An

investment advisory firm that operates on a single legal entity is an example of a firm that would

report sole investments discretion.82

Shared-defined investment discretion is used when the

reporting manager controls or is controlled by another legal entity.83

For example, a bank

holding company and its subsidiary would utilize the shared-defined category.84

Shared-defined

is also used when investment discretion is shared between investment companies and investment

advisers who advise those companies.85

Finally, the shared-other category is used for any

security in which investment discretion is shared in a manner other than the shared-defined

category, such as multiple levels of shared investment discretion.86

If investment discretion is shared, the reporting manager must identify the other

institutional investment manager that shares investment discretion.87

Other managers should be

listed on the Summary Page under the List of Other Included Managers heading and assigned a

78

Form 13F, Special Instructions, at 11 (17 C.F.R. § 249.325). 79

Form 13F, Special Instructions, at 12 (17 C.F.R. § 249.325). 80

Form 13F, Special Instructions, at 12 (17 C.F.R. § 249.325). 81

Form 13F, Special Instructions, at 12 (17 C.F.R. § 249.325). 82

See Division of Investment Management Frequently Asked Questions About Form 13F, Question 45. 83

Form 13F, Special Instructions, at 12 (17 C.F.R. § 249.325). 84

Frequently Asked Questions, Question 46. 85

Form 13F, Special Instructions, at 12 (17 C.F.R. § 249.325). 86

Form 13F, Special Instructions, at 12 (17 C.F.R. § 249.325). See also Frequently Asked Questions, Question 47. 87

Form 13F, Special Instructions, at 12 (17 C.F.R. § 249.325).

18 of 31

two digit number (beginning with 01, 02, etc.).88

The two digit number is then reported on the

13F Information Table in the Other Managers column.89

Voting Authority is different than investment discretion, and is defined as the ability to

vote on non-routine matters such as: contested election of directors, mergers and acquisitions,

and changes in corporate documents.90

A manager should report sole voting authority if it

exercises sole authority to vote on non-routine matters or if voting authority is only shared

through the arrangement that caused the manager to report shared-defined investment

discretion.91

The voting authority sub-column “none” is used if the reporting manager can only

vote on routine matters such as selecting an accountant, electing uncontested directors, or

approving an annual report.92

The number of shares that fall within each of these categories

should be listed in the voting authority sub-column.93

This section can be used as a basic guide for dealing with many of the issues that first

time filers encounter; however, it is also illustrative of the complexity embedded in the tedious

and often counter-intuitive Form 13F Instructions. Institutional Investment Managers should

consult an experienced compliance professional or licensed attorney for assistance in preparing,

reviewing and filing Form 13F. Even experienced reporting managers should take additional

precautions as the Commission works to expand its review and audits of Form 13F filings.94

88

See Division of Investment Management Frequently Asked Questions About Form 13F, Question 37. 89

Form 13F, Special Instructions, at 12 (17 C.F.R. § 249.325). 90

See Division of Investment Management Frequently Asked Questions About Form 13F, Question 50. 91

See Division of Investment Management Frequently Asked Questions About Form 13F, Question 50. 92

See Division of Investment Management Frequently Asked Questions About Form 13F, Question 50. 93

See Division of Investment Management Frequently Asked Questions About Form 13F, Question 50. 94

Review of the SEC‟s Section 13(f) Reporting Requirement, Report No. 480, at 9.

19 of 31

B) Treatment of Confidential Information in Section 13(f) Reports

a) The Public Nature of Section 13(f) Reports

By default, the information reported under Section 13(f), other than that concerning

securities held by the account of a natural person95

or estate or trust (other than a business trust or

investment company) (“the personal holdings exemption”), is public information freely

searchable and discoverable through EDGAR. Still, under Section 13(f)(3), the Commission has

the ability to exempt certain other information from public disclosure. As noted in the Section:

“ . . . the Commission, as it determines to be necessary or appropriate in the public

interest or for the protection of investors, may delay or prevent public disclosure of any

such information in accordance with section 552 of title 5 (The Freedom of Information

Act) . . . Notwithstanding the preceding sentence, any such information and securities

held by the account of a natural person or an estate or trust (other than a business trust or

investment company) shall not be disclosed to the public.”96

It is important to note that even though the Commission may exempt certain information from

public disclosure under Section 13(f)(3), such grant by the Commission does not exempt the filer

in question from actually reporting the information on Form 13F.97

In requesting confidential

treatment, certain steps need to be taken by the filer during the Section 13(f) filing process.

b) Requesting Confidential Treatment of Reported Information under 13(f)(3)

The rules and procedures for requesting the confidential treatment of reported

information are found in Rule 24b-2, Instructions for Confidential Treatment 1 and 2 of Form

13F, and Rule 101(c)(1)(i) of Regulation S-T. Rule 24b-2 describes the procedure in which the

confidential treatment application (“CT request/application”) is made.98

Form 13F speaks

specifically to certain categories of information that can be exempted from public disclosure as

95

The purpose of the personal holding exemption is to prevent the disclosure of the identity of the natural person,

estate, or trust in question. See Frequently Asked Questions, Question 54. 96

15 U.S.C. § 78m (f)(3). 97

15 U.S.C. § 78m (f)(3) but see 15 U.S.C. § 78m (f)(2). 98

See 17 C.F.R. § 240.24b-2.

20 of 31

well as further describing the applicable procedure for filing the CT application.99

Rule

101(c)(1)(i) speaks to the actual method of filing the CT application.100

Under Rule 24b-2 the filer must submit a CT application, noting the legal and factual

grounds for sustaining the request for confidential treatment.101

Those legal grounds for

confidential treatment must be based on applicable rules and regulations exempting certain

classes of information from public disclosure.102

The filer must also specify the factual link

between those rules and regulations and the information being reported in the Section 13(f)

filing.103

Additionally, the filing must suggest a reasonable time to keep confidential the

information for that particular Section 13(f) filing.104

Other than confidential treatment based on

the personal holdings exemption, the Commission will prescribe a specific length of time for

confidential protection relating to information dealing with special investment strategies and

open risk arbitrage positions.105

Rule 24b-2 and Form 13F both require CT applications and the confidential section of the

Form 13F Holdings Report to be submitted at the same time. This material should not be filed

with the rest of Form 13F that is filed through EDGAR. Instead, the public portion of the Form

13F Holdings Report should indicate that a portion of the report has been submitted for

confidential treatment to the Commission. Rule 101 of Regulation S-K requires that all CT

applications and supporting materials be submitted not on EDGAR but submitted to the

99

See Form 13F, Instruction for Confidential Treatment, at 1-4 (17 C.F.R. § 249.325). 100

See 17 C.F.R. § 232.101(c)(1)(i). 101

17 C.F.R. § 240.24b-2. 102

17 C.F.R. § 240.24b-2. 103

17 C.F.R. § 240.24b-2. 104

17 C.F.R. § 240.24b-2. 105

See Form 13F, Instruction for Confidential Treatment, at 2 (17 C.F.R. § 249.325); See also See Division of

Investment Management Frequently Asked Questions About Form 13F, Questions 55a, 56, 57 and 57a.

21 of 31

Commission‟s DC office in paper format.106

These procedures must be followed for every

Section 13(f) filing, even if the certain holdings information for which confidential treatment is

requested has not changed.107

c) Duration of Confidential Treatment and the Limits of Confidentiality

Confidential treatment, if granted, is granted for the particular Section 13(f) filing in

question and only applies to the information in that specific filing. Confidential treatment will be

given for a particular duration of time based on the reasoning used to exempt the information in

question from public disclosure. Additionally, the Commission may withdraw confidential

treatment protection if the Commission determines that it is in the best interest of investors

and/or market protection.108

i) Personal Holdings Exemption

As noted above, the personal holdings exemption is specifically noted in Section 13(f)(3)

and exempts from public disclosure information concerning securities held by the account of a

natural person or estate or trust (other than a business trust or investment company).109

When

confidential treatment is granted for the personal holdings exemption that treatment will last

indefinitely for the report filed.110

The filer will have to file subsequent Section 13(f) reports and

reapply for the confidential treatment of the information as it pertains to those subsequent

reports.111

106

17 C.F.R. § 232.101(c)(1). 107

See Form 13F, Instruction for Confidential Treatment, Preliminary Note (17 C.F.R. § 249.325); Seealso17 C.F.R.

§ 232.101(c)(1). 108

17 C.F.R. § 240.24b-2. 109

15 U.S.C. § 78m (f)(3). 110

See Division of Investment Management Frequently Asked Questions About Form 13F, Question 55a. 111

See Division of Investment Management Frequently Asked Questions About Form 13F, Questions 55 and 55a.

22 of 31

ii) Exemption for Information Pertaining to Certain Investment Strategies

The Commission will also allow information relating to certain investment strategies, that

if disclosed could cause harm to the filer and its clients, to be exempted from public disclosure.

In order to gain confidential treatment for this information the filer must provide the factual and

legal support in the CT application as prescribed in Instruction 2a-2e of Form 13F and in various

Commission releases.112

In requesting the exemption, the filer may request a period of

confidentiality of three months, six months, nine months, or one year.113

Those requests must

correlate factually to the time period needed to effectuate the filer‟s investment strategy.114

After

the granted period expires the filer must amend the filed Form 13F with the confidential

information that is no longer protected from disclosure.115

iii) Exemption for Open Risk Arbitrage Positions

Open risk arbitrage position may be exempt from public disclosure and confidential

treatment given if the conditions and factual circumstances as stated in Instruction 2f of Form

13F exist on the last day of the period for which the Section 13(f) report is being filed.116

If the

filer in question has a reasonable belief at the end of the filing period that it may not close the

entire position in question before the date the report is due (45 days after the end of the period)

and makes that representation on the CT application the Commission will automatically grant

confidential treatment with respect to those positions.117

Confidential treatment will be granted

through the end of the quarterly period in which a deal is completed or terminated but not longer

112

See Form 13F, Instruction for Confidential Treatment, at 2 (17 C.F.R. § 249.325); See SEC Letter, Section 13(f)

Confidential Treatment Requests (Securities and Exchange Commission, June 17, 1998) available at

http://www.sec.gov/divisions/investment/guidance/13fpt2.htm. 113

See Division of Investment Management Frequently Asked Questions About Form 13F, Question 57a. 114

See Division of Investment Management Frequently Asked Questions About Form 13F, Question 57a. 115

See Division of Investment Management Frequently Asked Questions About Form 13F, Question 58. 116

See Form 13F, Instruction for Confidential Treatment, at 2 (17 C.F.R. § 249.325). 117

See Form 13F, Instruction for Confidential Treatment, at 2 (17 C.F.R. § 249.325).

23 of 31

than the one year from the date that the originally filing is due. At expiration of that time, the

filer in question must report the information via amendment to the filed Form 13F.118

iv)Commission Termination of Confidential Treatment prior to the Applicable

Expiration Date.

For the protection of investors or upon appropriate Freedom of Information Act requests,

the Commission, in its discretion, may revoke confidential status for all or part of the

information which has been granted such status prior to the expiration of such status.119

This is

true regardless of the exemption which allows for confidential treatment. If confidential

treatment is revoked, the Commission will contact the filer and the filer will have to amend the

filed Form 13F with the information that is no longer considered confidential.120

If confidential

treatment is denied or revoked, the filer may appeal that determination under the Commission‟s

Rules of Practice.121

d) Application of Section 13(f)(2)

As discussed above, Section 13(f)(3) allows filers to petition the Commission for the

confidential treatment of certain information, but it does not alleviate the need for a filer to make

the appropriate filing of Form 13F. Section 13(f)(2) allows the Commission, through the

showing of extraordinary circumstances, to exempt a potential filer from the filing requirement

all together.122

Section 13(f)(2) states:

“The Commission, by rule or order, may exempt, conditionally or unconditionally, any

institutional investment manager or security or any class of institutional investment

118

See Form 13F, Instruction for Confidential Treatment, at 2 (17 C.F.R. § 249.325). 119

17 C.F.R. § 240.24b-2(d)(1). 120

17 C.F.R. § 240.24b-2(f). 121

17 C.F.R. § 240.24b-2(d)(2). 122

Wynnefield Capital Management LLC and Wynnefield Capital, Inc., Release No. 61930 (Securities and

Exchange Commission, April 16, 2010) (SEC Release).

24 of 31

managers or securities from any or all of the provisions of this [Section 13] subsection or

the rules thereunder”123

The Commission has noted that there is no formal rule or procedure that specifically covers the

Section 13(f)(2) exemption.124

Accordingly the Commission looks to Section 13(f)(4), Section

36 of the Exchange Act, and Rules 0-12 under the Exchange Act in determining whether or not

to grant a Section 13(f)(2) exemption.125

In considering the need to protect investors and the

markets the Commission has held that if the protection sought is covered by Section 13(f)(3), a

filer must make a good faith effort to obtain that protection through the CT application process,

as discussed above.126

If a good faith effort is made, the CT application is denied and

extraordinary circumstances exist the Commission may find cause to grant the Section 13(f)(2)

exemption. Pursuing a CT request and failing to obtain it does not by itself amount to the

extraordinary circumstances needed that would justify a Section 13(f)(2) exemption.127

In one instance an investment management firm sought a the Section 13(f)(2) exemption

in an attempt to protect investment strategies that it considered “trade secrets.”128

The firm noted

that continually filing CT requests was unduly burdensome and there was no assurance that the

Commission would grant or continue to grant confidential treatment to certain information.129

The Commission found that the current CT application process would provide adequate

protection to the investment strategies in question and the firm failed to file the required CT

application.130

Furthermore, the “burdensome” nature of filing the CT application process did

123

15 U.S.C. § 78m (f)(2). 124

Wynnefield Capital Management, LLC, Release No. 61930. 125

Wynnefield Capital Management, LLC, Release No. 61930. 126

Wynnefield Capital Management, LLC, Release No. 61930. 127

Wynnefield Capital Management, LLC, Release No. 61930. 128

Wynnefield Capital Management, LLC, Release No. 61930. 129

Wynnefield Capital Management, LLC, Release No. 61930. 130

Wynnefield Capital Management, LLC, Release No. 61930.

25 of 31

not amount to an extraordinary circumstance.131

Accordingly, the Commission denied the

Section 13(f)(2) exemption.132

The practical consequence of this that unless some very extreme

circumstances exist, the Commission will not grant a Section 13(f)(2) exemption. The reasoning

for this lies in the power of the exemption and the need to prevent institutional investment

managers from subverting the purpose of Section 13(f) and Rule 13f-1.133

CONCLUSION

The filing of the Section 13(f) report can be a complex and tedious process, but it is also

a necessary process for the institutional investment manager that has investment discretion over

$100,000,000 or more in Section 13(f) securities.134

The Commission, as revealed by the recent

OIG (Office of Inspector General) report, is making a concerted effort to step up the enforcement

of Section 13(f).135

This increased enforcement effort will involve greater systemic checks for

both the completeness and accuracy of all filings made, with inaccurate or erroneous filings

rejected at the time of submission.136

The OIG has also stressed the need to properly monitor for

instances in which managers fail to file and to continuously monitor those particular managers

for Section 13(f) deficiencies.137

The Commission has agreed with the OIG and is beginning to

streamline its monitoring and review efforts.138

The duty of the Commission to properly execute

its duties under Section 13(f) will be split among various Commission divisions going forward,

including the Division of Investment Management (IM) and the Office of Compliance

131

Wynnefield Capital Management, LLC, Release No. 61930. 132

Wynnefield Capital Management, LLC, Release No. 61930. 133

Supra Section II. 134

15 U.S.C. § 78m (f). 135

Review of the SEC‟s Section 13(f) Reporting Requirement, Report No. 480 at 6-13. 136

Review of the SEC‟s Section 13(f) Reporting Requirement, Report No. 480 at 12. 137

Review of the SEC‟s Section 13(f) Reporting Requirement, Report No. 480 at 10. 138

Memorandum from the Office of the Chairman, Response to Report No. 480 (Securities and Exchange

Commission, September 24, 2010).

26 of 31

Inspections and Examinations (OCIE).139

Along with the stepped up enforcement efforts, the

Commission is analyzing the need to change the substantive reporting requirements, including

the need to increase the reporting threshold and the reporting of aggregate purchase and sales of

Section 13(f) securities.140

With the sound of the 2008 financial crisis still ringing in its ear, the Securities and

Exchange Commission has been compelled to change the landscape of securities compliance. In

doing so, it has been reminded of the Congressional purpose of Section 13(f), namely to “. . .

[C]reate a central repository of historical and current data . . . designed to improve the body of

factual data available and, thus, facilitate the consideration of the influence and impact of

institutional investment managers on the securities markets and the public policy implications of

that influence.”141

As a consequence, it is vital that institutional investment managers know their

duties under Section 13(f) and how to properly execute those duties.

139

Memorandum from the Office of the Chairman, Response to Report No. 480 at 1. 140

Memorandum from the Division of Investment Management, Response to Report No. 480 (Securities and

Exchange Commission, September 24, 2010) at 3-4. 141

Review of the SEC‟s Section 13(f) Reporting Requirement, Report No. 480 at 1 (citing Filing and Reporting

Requirements Relating to Institutional Investment Managers, Release No. 34-14852 (June 15, 1978), 43 Fed. Reg.

26700-01 (June 22, 1978)).

27 of 31

SAMPLE HOLDINGS REPORT

The following is a sample Form 13F Holdings Report. It includes the cover page, the

summary page, and the information table.

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 13F

FORM 13F COVER PAGE

Report for the Calendar Year or Quarter Ended: _______________________________

Check here if Amendment [ ]; Amendment Number: ______

This Amendment (Check only one.): [ ] is a restatement.

[ ] adds new holdings entries.

Institutional Investment Manager Filing this Report:

Name: __________________________________________

Address: __________________________________________

Form 13F File Number: 28-____________

The institutional investment manager filing this report and the person by whom it is signed

hereby represent that the person signing the report is authorized to submit it, that all information

contained herein is true, correct and complete, and that it is understood that all required items,

statements, schedules, lists, and tables, are considered integral parts of this form.

Person Signing this Report on Behalf of Reporting Manager:

Name: __________________________________________

Title: __________________________________________

Phone: __________________________________________

28 of 31

Signature, Place, and Date of Signing:

________________________ ______________________ ____________________

[Signature] [City, State] [Date]

Report Type (Check only one.):

[ ] 13F HOLDINGS REPORT. (Check here if all holdings of this reporting manager are

reported in this report.)

[ ] 13F NOTICE. (Check here if no holdings reported are in this report, and all holdings are

reported by other reporting manager(s).)

[ ] 13F COMBINATION REPORT. (Check here if a portion of the holdings for this reporting

manager are reported in this report and a portion are reported by other reporting manager(s).)

List of Other Managers Reporting for this Manager:

[If there are no entries in this list, omit this section.]

Form 13F File Number Name

28-________________ ____________________

[Repeat as necessary.]

29 of 31

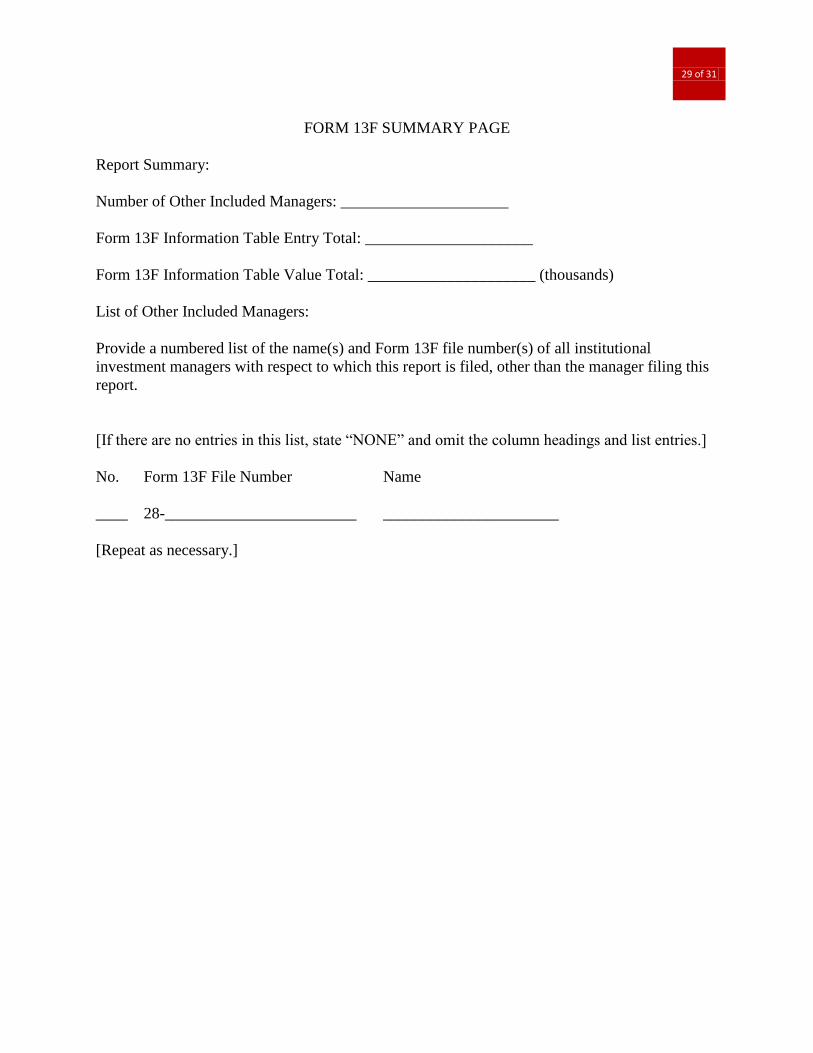

FORM 13F SUMMARY PAGE

Report Summary:

Number of Other Included Managers: _____________________

Form 13F Information Table Entry Total: _____________________

Form 13F Information Table Value Total: _____________________ (thousands)

List of Other Included Managers:

Provide a numbered list of the name(s) and Form 13F file number(s) of all institutional

investment managers with respect to which this report is filed, other than the manager filing this

report.

[If there are no entries in this list, state “NONE” and omit the column headings and list entries.]

No. Form 13F File Number Name

____ 28-________________________ ______________________

[Repeat as necessary.]

30 of 31

FORM 13F INFORMATION TABLE (BLANK)

Column 1 Column 2 Column 3 Column 4 Column 5 Column 6 Column 7 Column 8

______ ______ ______ ______ ____________________ _________ ________ _________

Name of

Issuer

Title of

Class

CUSIP Value

(x1000) SHR or

PRN AMT SH/

PRN PUT/

CALL INVESTMENT

DISCRETION OTHER

MANAGERS

VOTING

AUTHORITY

31 of 31

FORM 13F INFORMATION TABLE (FILLED IN)

![[XLS]Motor Fuel Tax Retailers - The Official Web Site for The … · Web viewBHIM AND BHARAT LLC PHILIPSBURG WHITE TWP RYNA PETROLEUM LLC FLANDERS ROUTINE MANAGEMENT LLC WASHINGTON](https://static.fdocuments.net/doc/165x107/5aff1ee67f8b9a444f8fc0b9/xlsmotor-fuel-tax-retailers-the-official-web-site-for-the-viewbhim-and-bharat.jpg)