GUYANA GOLDFIELDS INC....Guyana Goldfields Inc. (the "Company" or "Guyana Goldfields") is a company...

18

GUYANA GOLDFIELDS INC. UNAUDITED CONDENSED INTERIM CONSOLIDATED FINANCIAL STATEMENTS FIRST QUARTER 2019

Transcript of GUYANA GOLDFIELDS INC....Guyana Goldfields Inc. (the "Company" or "Guyana Goldfields") is a company...

GUYANA GOLDFIELDS INC. UNAUDITED CONDENSED INTERIM CONSOLIDATED

FINANCIAL STATEMENTS

FIRST QUARTER 2019

1

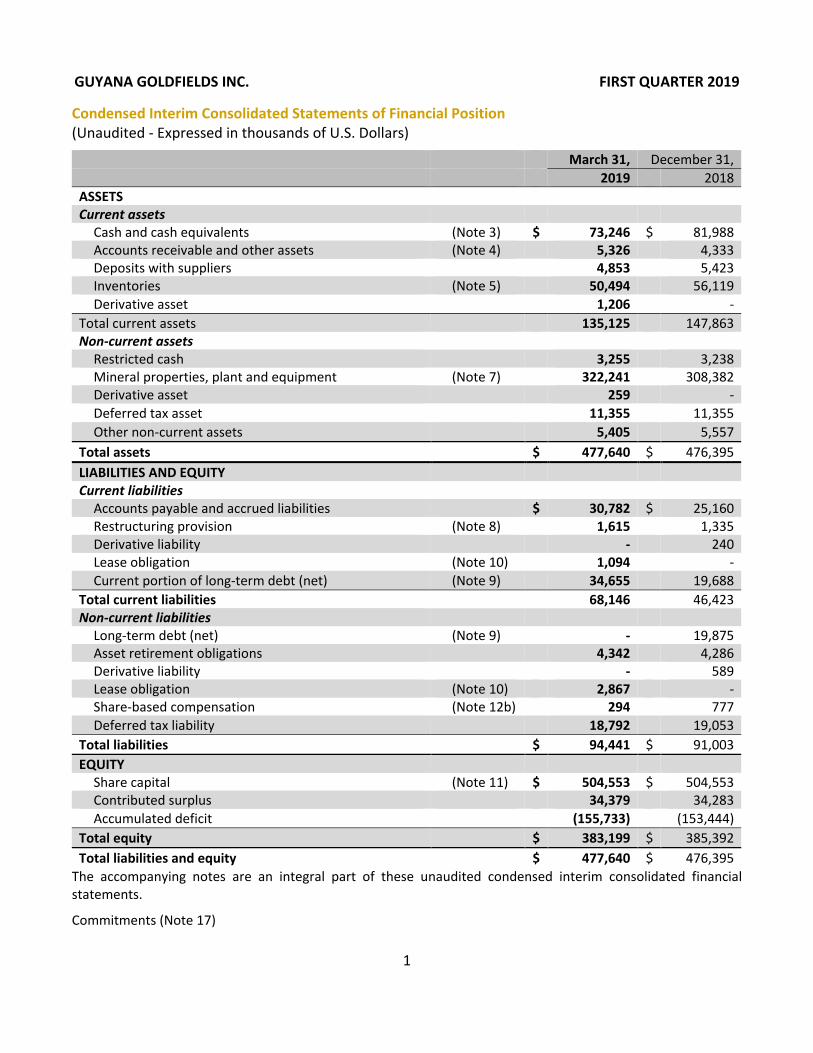

GUYANA GOLDFIELDS INC. FIRST QUARTER 2019 Condensed Interim Consolidated Statements of Financial Position (Unaudited - Expressed in thousands of U.S. Dollars)

March 31, December 31, 2019 2018

ASSETS Current assets

Cash and cash equivalents (Note 3) $ 73,246 $ 81,988 Accounts receivable and other assets (Note 4) 5,326 4,333 Deposits with suppliers 4,853 5,423 Inventories (Note 5) 50,494 56,119 Derivative asset 1,206 -

Total current assets 135,125 147,863 Non-current assets

Restricted cash 3,255 3,238 Mineral properties, plant and equipment (Note 7) 322,241 308,382 Derivative asset 259 - Deferred tax asset 11,355 11,355 Other non-current assets 5,405 5,557

Total assets $ 477,640 $ 476,395 LIABILITIES AND EQUITY Current liabilities

Accounts payable and accrued liabilities $ 30,782 $ 25,160 Restructuring provision (Note 8) 1,615 1,335 Derivative liability - 240 Lease obligation (Note 10) 1,094 - Current portion of long-term debt (net) (Note 9) 34,655 19,688

Total current liabilities 68,146 46,423 Non-current liabilities

Long-term debt (net) (Note 9) - 19,875 Asset retirement obligations 4,342 4,286 Derivative liability - 589 Lease obligation (Note 10) 2,867 - Share-based compensation (Note 12b) 294 777 Deferred tax liability 18,792 19,053

Total liabilities $ 94,441 $ 91,003 EQUITY

Share capital (Note 11) $ 504,553 $ 504,553 Contributed surplus 34,379 34,283 Accumulated deficit (155,733) (153,444)

Total equity $ 383,199 $ 385,392 Total liabilities and equity $ 477,640 $ 476,395

The accompanying notes are an integral part of these unaudited condensed interim consolidated financial statements.

Commitments (Note 17)

2

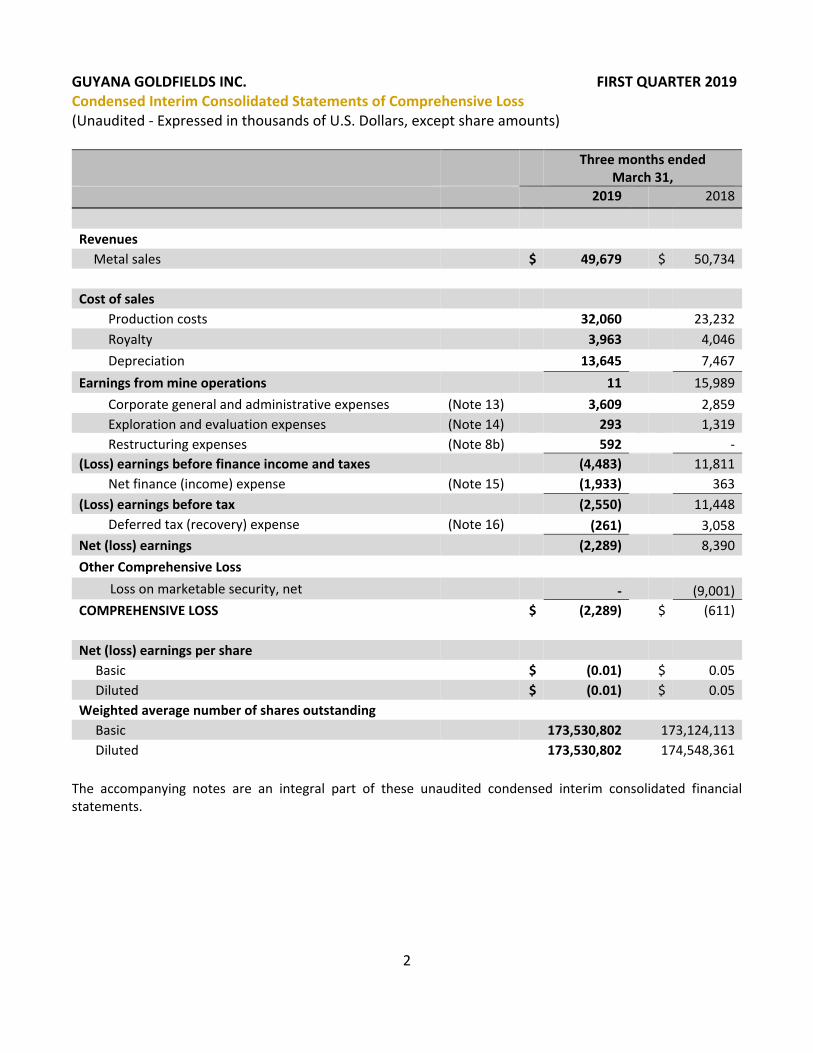

GUYANA GOLDFIELDS INC. FIRST QUARTER 2019 Condensed Interim Consolidated Statements of Comprehensive Loss (Unaudited - Expressed in thousands of U.S. Dollars, except share amounts)

Three months ended March 31,

2019 2018

Revenues

Metal sales $ 49,679 $ 50,734

Cost of sales Production costs 32,060 23,232 Royalty 3,963 4,046 Depreciation 13,645 7,467

Earnings from mine operations 11 15,989 Corporate general and administrative expenses (Note 13) 3,609 2,859 Exploration and evaluation expenses (Note 14) 293 1,319 Restructuring expenses (Note 8b) 592 -

(Loss) earnings before finance income and taxes (4,483) 11,811 Net finance (income) expense (Note 15) (1,933) 363

(Loss) earnings before tax (2,550) 11,448 Deferred tax (recovery) expense (Note 16) (261) 3,058

Net (loss) earnings (2,289) 8,390 Other Comprehensive Loss

Loss on marketable security, net - (9,001) COMPREHENSIVE LOSS $ (2,289) $ (611)

Net (loss) earnings per share Basic $ (0.01) $ 0.05 Diluted $ (0.01) $ 0.05 Weighted average number of shares outstanding

Basic 173,530,802 173,124,113 Diluted 173,530,802 174,548,361

The accompanying notes are an integral part of these unaudited condensed interim consolidated financial statements.

3

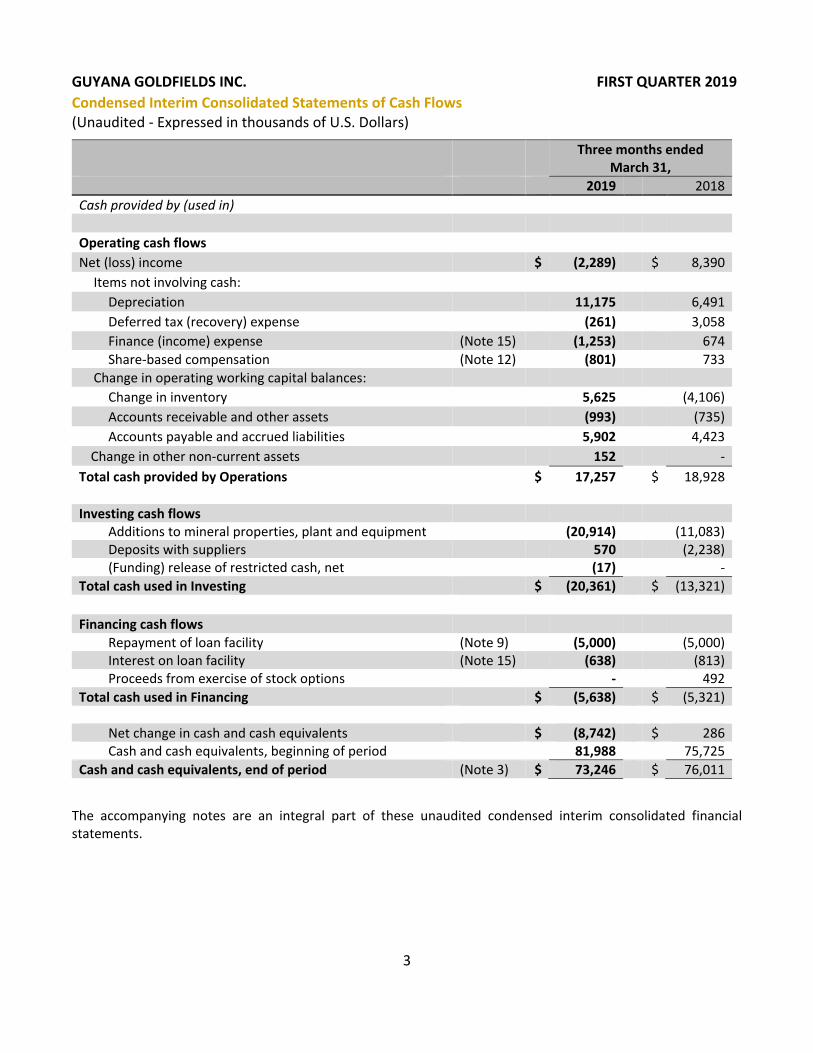

GUYANA GOLDFIELDS INC. FIRST QUARTER 2019 Condensed Interim Consolidated Statements of Cash Flows (Unaudited - Expressed in thousands of U.S. Dollars)

Three months ended March 31,

2019 2018 Cash provided by (used in)

Operating cash flows

Net (loss) income $ (2,289) $ 8,390 Items not involving cash:

Depreciation 11,175 6,491 Deferred tax (recovery) expense (261) 3,058 Finance (income) expense (Note 15) (1,253) 674 Share-based compensation (Note 12) (801) 733

Change in operating working capital balances: Change in inventory 5,625 (4,106) Accounts receivable and other assets (993) (735) Accounts payable and accrued liabilities 5,902 4,423

Change in other non-current assets 152 - Total cash provided by Operations $ 17,257 $ 18,928 Investing cash flows

Additions to mineral properties, plant and equipment (20,914) (11,083) Deposits with suppliers 570 (2,238) (Funding) release of restricted cash, net (17) -

Total cash used in Investing $ (20,361) $ (13,321) Financing cash flows

Repayment of loan facility (Note 9) (5,000) (5,000) Interest on loan facility (Note 15) (638) (813) Proceeds from exercise of stock options - 492

Total cash used in Financing $ (5,638) $ (5,321)

Net change in cash and cash equivalents $ (8,742) $ 286 Cash and cash equivalents, beginning of period 81,988 75,725

Cash and cash equivalents, end of period (Note 3) $ 73,246 $ 76,011

The accompanying notes are an integral part of these unaudited condensed interim consolidated financial statements.

4

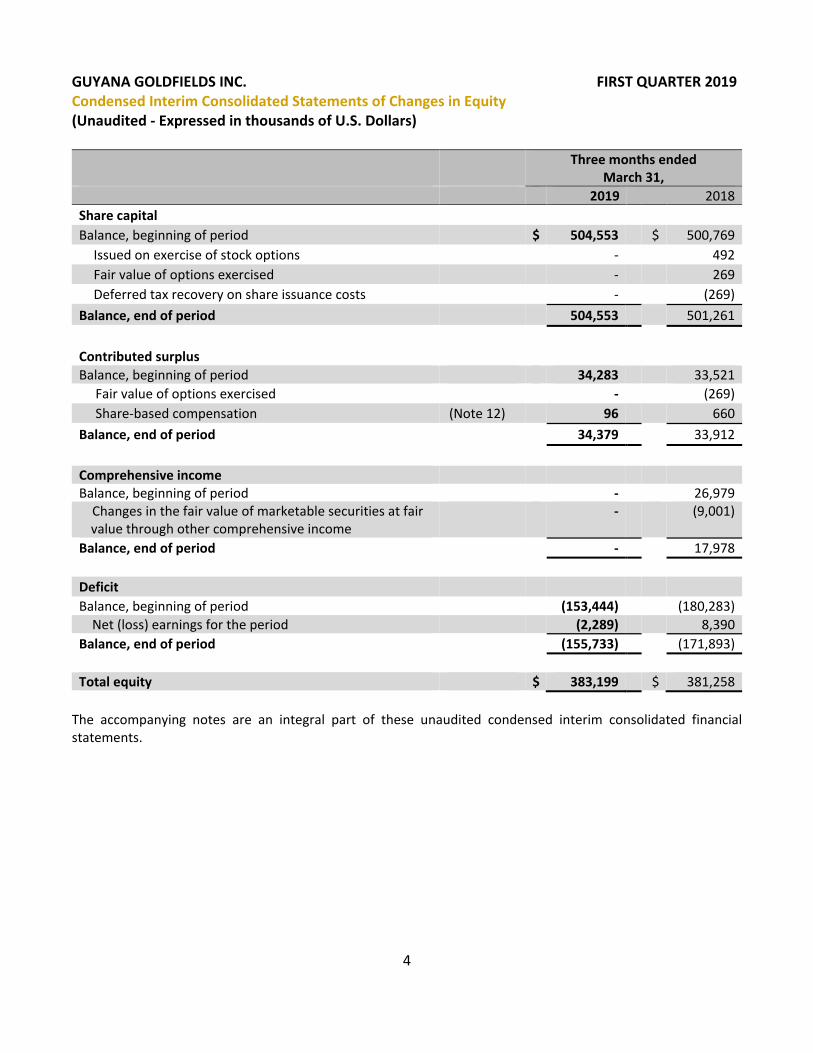

GUYANA GOLDFIELDS INC. FIRST QUARTER 2019 Condensed Interim Consolidated Statements of Changes in Equity (Unaudited - Expressed in thousands of U.S. Dollars)

Three months ended March 31,

2019 2018 Share capital

Balance, beginning of period $ 504,553 $ 500,769 Issued on exercise of stock options - 492 Fair value of options exercised - 269 Deferred tax recovery on share issuance costs - (269)

Balance, end of period 504,553 501,261

Contributed surplus

Balance, beginning of period 34,283 33,521 Fair value of options exercised - (269) Share-based compensation (Note 12) 96 660 Balance, end of period 34,379 33,912 Comprehensive income Balance, beginning of period - 26,979 Changes in the fair value of marketable securities at fair

value through other comprehensive income - (9,001)

Balance, end of period - 17,978 Deficit

Balance, beginning of period (153,444) (180,283) Net (loss) earnings for the period (2,289) 8,390 Balance, end of period (155,733) (171,893) Total equity $ 383,199 $ 381,258

The accompanying notes are an integral part of these unaudited condensed interim consolidated financial statements.

GUYANA GOLDFIELDS INC. FIRST QUARTER 2019 Notes to the Condensed Interim Consolidated Financial Statements For the three months ended March 31, 2019 and 2018 (Unaudited - Expressed in thousands of U.S. Dollars, unless otherwise indicated)

5

NATURE OF OPERATIONS Guyana Goldfields Inc. (the "Company" or "Guyana Goldfields") is a company domiciled in Canada and was incorporated on December 12, 1994, under the Canadian Business Corporations Act. The Company shares are publicly traded on the Toronto Stock Exchange (TSX:GUY). The Company’s head office is registered at 375 University avenue, Suite 802, Toronto, Ontario, Canada.

Guyana Goldfields Inc. and its wholly owned subsidiaries are engaged in the acquisition, exploration, development and operation of precious metal mineral properties, principally in Guyana, South America. The Company’s primary asset is its wholly owned Aurora Gold Mine, located in Guyana South America.

BASIS OF PRESENTATION AND SIGNIFICANT ACCOUNTING POLICIES

(a) Basis of presentation and measurement

The unaudited condensed interim consolidated financial statements have been prepared in accordance with International Financial Reporting Standards (“IFRS”) as issued by the International Accounting Standards Board (“IASB”) and Interpretations of the International Financial Reporting Interpretations Committee (“IFRIC”) which the Canadian Accounting Standards Board has approved for incorporation into Part 1 of the CPA Canada Handbook – Accounting including IAS 34 Interim financial reporting. The condensed interim consolidated financial statements should be read in conjunction with the annual consolidated financial statements for the year ended December 31, 2018.

The Company’s presentation currency is United States dollars. Some figures in these statements have been expressed in Canadian Dollars (Cdn$) for information purposes and have been denoted as such.

The preparation of these condensed interim consolidated financial statements requires management to make judgements, estimates and assumptions that affect the application of policies and reported amounts of assets, liabilities and expenses. See Note 4 for significant judgements, estimates and assumptions.

The condensed interim consolidated financial statements were authorized for issue by the Board of Directors on April 29, 2019.

(b) Critical accounting estimates and judgments

Areas of judgement that have the most significant effect on the amounts recognized in the financial statements are disclosed in Note 4 of the Company’s consolidated financial statements for the year ended December 31, 2018.

GUYANA GOLDFIELDS INC. FIRST QUARTER 2019 Notes to the Condensed Interim Consolidated Financial Statements For the three months ended March 31, 2019 and 2018 (Unaudited - Expressed in thousands of U.S. Dollars, unless otherwise indicated)

6

(c) Changes in significant accounting policies

Except as described below, the accounting policies applied in these condensed interim consolidated financial statements are the same as those applied in the Company’s consolidated financial statements for the year ended December 31, 2018.

The changes in accounting policies are also expected to be reflected in the Company’s consolidated financial statements for the year ending December 31, 2019.

IFRS 16 – Leases (see Note 20)

IFRIC 23 – Uncertainty over Income Tax Treatments

The Company has adopted IFRIC 23 Uncertainty over Income Tax Treatments effective January 1, 2019 using the modified retrospective approach and accordingly the information presented for 2018 has not been restated. The adoption of this standard did not have a material impact on the Company’s consolidated financial statements. IFRIC 23 requires: (a) the management to contemplate whether uncertain tax treatments should be considered separately, or together as a group, based on which approach provides better predictions of the resolution; (b) the management to determine if it is probable that the tax authorities will accept the uncertain tax treatment; and (c) if it is not probable that the uncertain tax treatment will be accepted, measure the tax uncertainty based on the most likely amount or expected value, depending on whichever method better predicts the resolution of the uncertainty.

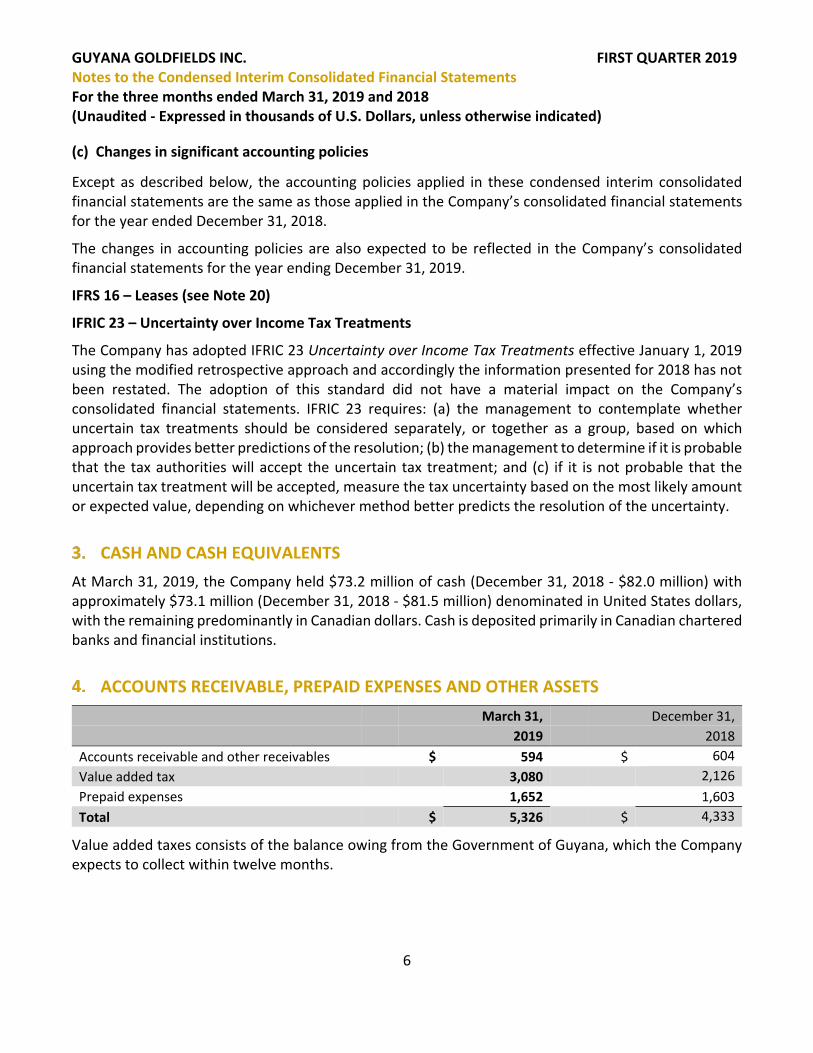

CASH AND CASH EQUIVALENTS At March 31, 2019, the Company held $73.2 million of cash (December 31, 2018 - $82.0 million) with approximately $73.1 million (December 31, 2018 - $81.5 million) denominated in United States dollars, with the remaining predominantly in Canadian dollars. Cash is deposited primarily in Canadian chartered banks and financial institutions.

ACCOUNTS RECEIVABLE, PREPAID EXPENSES AND OTHER ASSETS March 31, December 31, 2019 2018 Accounts receivable and other receivables $ 594 $ 604 Value added tax 3,080 2,126 Prepaid expenses 1,652 1,603 Total $ 5,326 $ 4,333

Value added taxes consists of the balance owing from the Government of Guyana, which the Company expects to collect within twelve months.

GUYANA GOLDFIELDS INC. FIRST QUARTER 2019 Notes to the Condensed Interim Consolidated Financial Statements For the three months ended March 31, 2019 and 2018 (Unaudited - Expressed in thousands of U.S. Dollars, unless otherwise indicated)

7

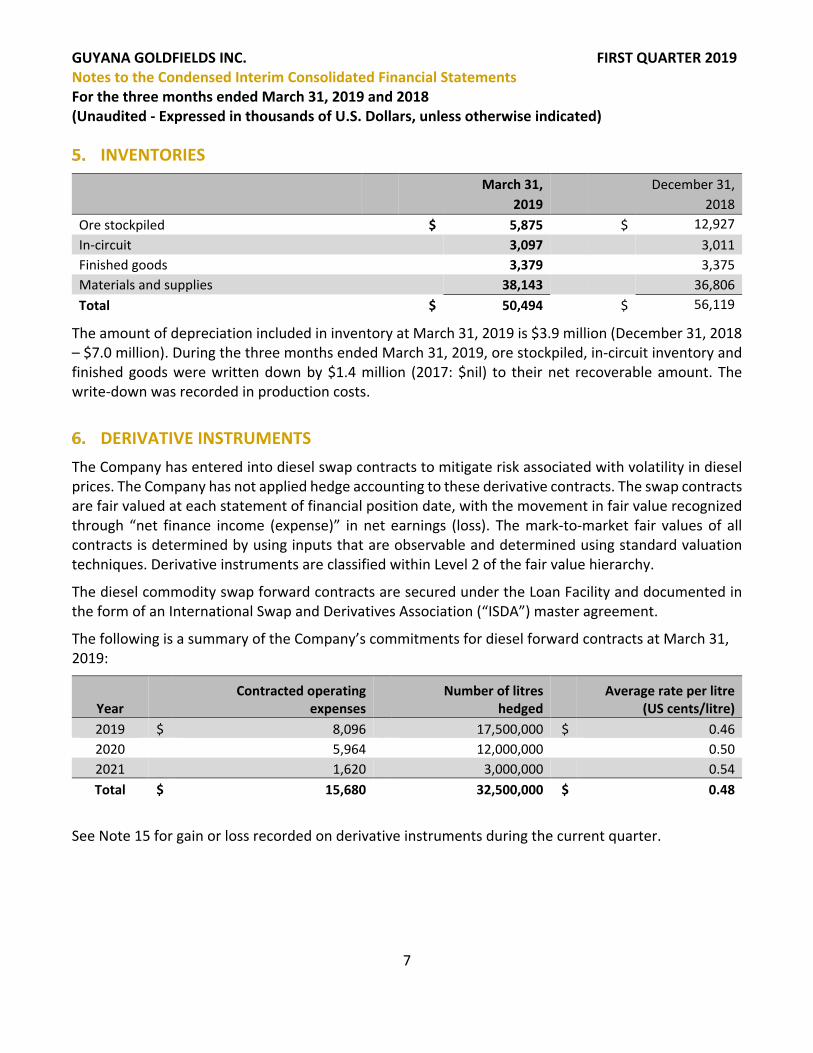

INVENTORIES

March 31, December 31, 2019 2018 Ore stockpiled $ 5,875 $ 12,927 In-circuit 3,097 3,011 Finished goods 3,379 3,375 Materials and supplies 38,143 36,806 Total $ 50,494 $ 56,119

The amount of depreciation included in inventory at March 31, 2019 is $3.9 million (December 31, 2018 – $7.0 million). During the three months ended March 31, 2019, ore stockpiled, in-circuit inventory and finished goods were written down by $1.4 million (2017: $nil) to their net recoverable amount. The write-down was recorded in production costs.

DERIVATIVE INSTRUMENTS The Company has entered into diesel swap contracts to mitigate risk associated with volatility in diesel prices. The Company has not applied hedge accounting to these derivative contracts. The swap contracts are fair valued at each statement of financial position date, with the movement in fair value recognized through “net finance income (expense)” in net earnings (loss). The mark-to-market fair values of all contracts is determined by using inputs that are observable and determined using standard valuation techniques. Derivative instruments are classified within Level 2 of the fair value hierarchy.

The diesel commodity swap forward contracts are secured under the Loan Facility and documented in the form of an International Swap and Derivatives Association (“ISDA”) master agreement.

The following is a summary of the Company’s commitments for diesel forward contracts at March 31, 2019:

Year Contracted operating

expenses Number of litres

hedged Average rate per litre

(US cents/litre) 2019 $ 8,096 17,500,000 $ 0.46 2020 5,964 12,000,000 0.50 2021 1,620 3,000,000 0.54 Total $ 15,680 32,500,000 $ 0.48

See Note 15 for gain or loss recorded on derivative instruments during the current quarter.

GUYANA GOLDFIELDS INC. FIRST QUARTER 2019 Notes to the Condensed Interim Consolidated Financial Statements For the three months ended March 31, 2019 and 2018 (Unaudited - Expressed in thousands of U.S. Dollars, unless otherwise indicated)

8

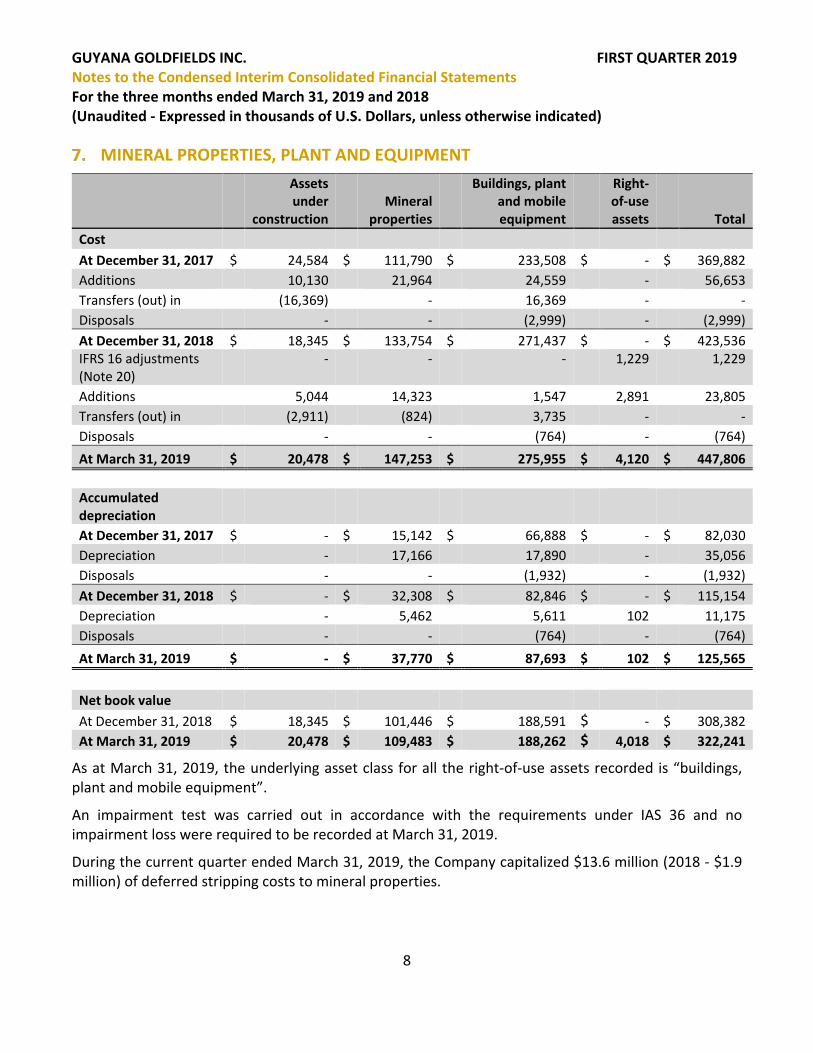

MINERAL PROPERTIES, PLANT AND EQUIPMENT

Assets under

construction Mineral

properties

Buildings, plant and mobile equipment

Right-of-use assets Total

Cost

At December 31, 2017 $ 24,584 $ 111,790 $ 233,508 $ - $ 369,882 Additions 10,130 21,964 24,559 - 56,653 Transfers (out) in (16,369) - 16,369 - - Disposals - - (2,999) - (2,999) At December 31, 2018 $ 18,345 $ 133,754 $ 271,437 $ - $ 423,536 IFRS 16 adjustments (Note 20)

- - - 1,229 1,229

Additions 5,044 14,323 1,547 2,891 23,805 Transfers (out) in (2,911) (824) 3,735 - - Disposals - - (764) - (764) At March 31, 2019 $ 20,478 $ 147,253 $ 275,955 $ 4,120 $ 447,806

Accumulated depreciation

At December 31, 2017 $ - $ 15,142 $ 66,888 $ - $ 82,030 Depreciation - 17,166 17,890 - 35,056 Disposals - - (1,932) - (1,932) At December 31, 2018 $ - $ 32,308 $ 82,846 $ - $ 115,154 Depreciation - 5,462 5,611 102 11,175 Disposals - - (764) - (764) At March 31, 2019 $ - $ 37,770 $ 87,693 $ 102 $ 125,565 Net book value At December 31, 2018 $ 18,345 $ 101,446 $ 188,591 $ - $ 308,382 At March 31, 2019 $ 20,478 $ 109,483 $ 188,262 $ 4,018 $ 322,241

As at March 31, 2019, the underlying asset class for all the right-of-use assets recorded is “buildings, plant and mobile equipment”.

An impairment test was carried out in accordance with the requirements under IAS 36 and no impairment loss were required to be recorded at March 31, 2019.

During the current quarter ended March 31, 2019, the Company capitalized $13.6 million (2018 - $1.9 million) of deferred stripping costs to mineral properties.

GUYANA GOLDFIELDS INC. FIRST QUARTER 2019 Notes to the Condensed Interim Consolidated Financial Statements For the three months ended March 31, 2019 and 2018 (Unaudited - Expressed in thousands of U.S. Dollars, unless otherwise indicated)

9

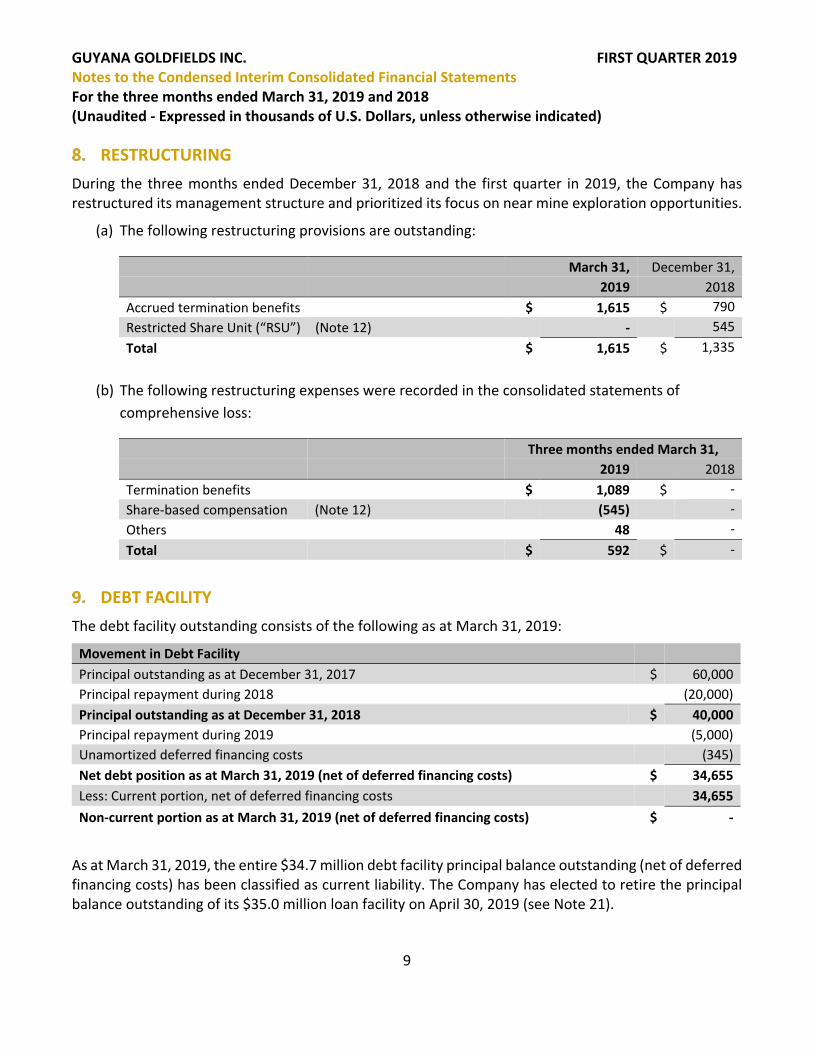

RESTRUCTURING During the three months ended December 31, 2018 and the first quarter in 2019, the Company has restructured its management structure and prioritized its focus on near mine exploration opportunities.

(a) The following restructuring provisions are outstanding:

March 31, December 31, 2019 2018 Accrued termination benefits $ 1,615 $ 790 Restricted Share Unit (“RSU”) (Note 12) - 545 Total $ 1,615 $ 1,335

(b) The following restructuring expenses were recorded in the consolidated statements of

comprehensive loss:

Three months ended March 31, 2019 2018 Termination benefits $ 1,089 $ - Share-based compensation (Note 12) (545) - Others 48 - Total $ 592 $ -

DEBT FACILITY The debt facility outstanding consists of the following as at March 31, 2019:

Movement in Debt Facility Principal outstanding as at December 31, 2017 $ 60,000 Principal repayment during 2018 (20,000) Principal outstanding as at December 31, 2018 $ 40,000 Principal repayment during 2019 (5,000) Unamortized deferred financing costs (345) Net debt position as at March 31, 2019 (net of deferred financing costs) $ 34,655 Less: Current portion, net of deferred financing costs 34,655 Non-current portion as at March 31, 2019 (net of deferred financing costs) $ -

As at March 31, 2019, the entire $34.7 million debt facility principal balance outstanding (net of deferred financing costs) has been classified as current liability. The Company has elected to retire the principal balance outstanding of its $35.0 million loan facility on April 30, 2019 (see Note 21).

GUYANA GOLDFIELDS INC. FIRST QUARTER 2019 Notes to the Condensed Interim Consolidated Financial Statements For the three months ended March 31, 2019 and 2018 (Unaudited - Expressed in thousands of U.S. Dollars, unless otherwise indicated)

10

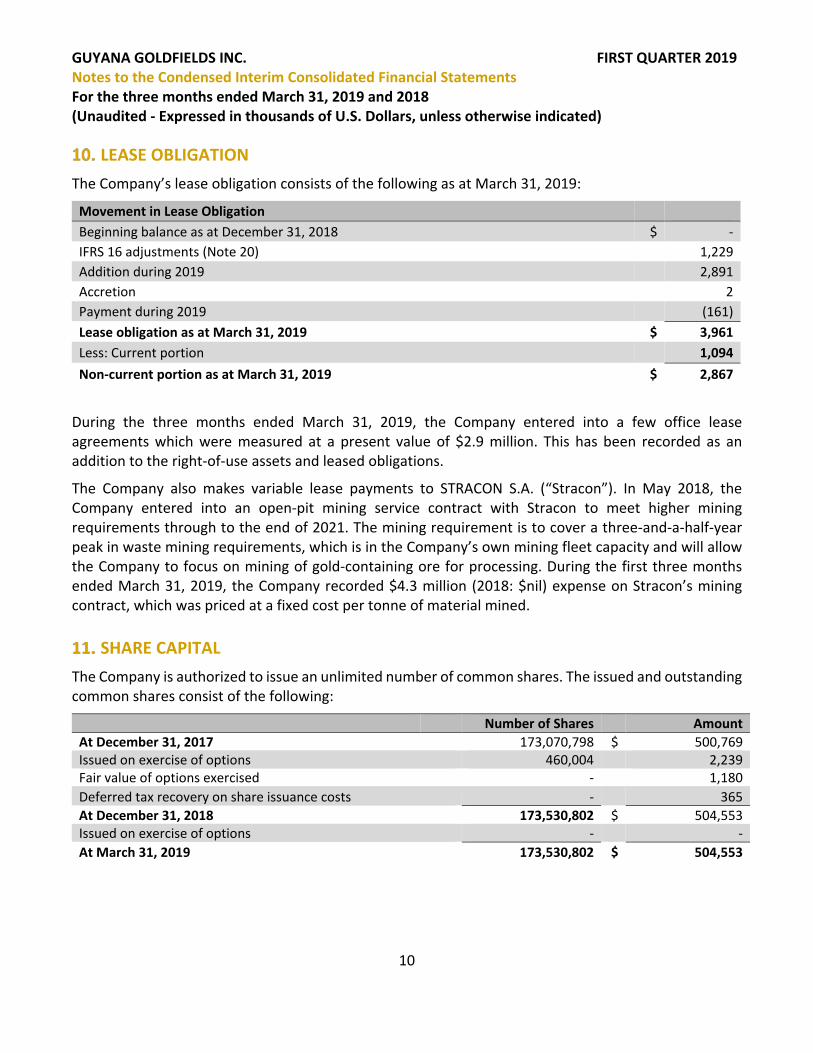

LEASE OBLIGATION The Company’s lease obligation consists of the following as at March 31, 2019:

Movement in Lease Obligation Beginning balance as at December 31, 2018 $ - IFRS 16 adjustments (Note 20) 1,229 Addition during 2019 2,891 Accretion 2 Payment during 2019 (161) Lease obligation as at March 31, 2019 $ 3,961 Less: Current portion 1,094 Non-current portion as at March 31, 2019 $ 2,867

During the three months ended March 31, 2019, the Company entered into a few office lease agreements which were measured at a present value of $2.9 million. This has been recorded as an addition to the right-of-use assets and leased obligations.

The Company also makes variable lease payments to STRACON S.A. (“Stracon”). In May 2018, the Company entered into an open-pit mining service contract with Stracon to meet higher mining requirements through to the end of 2021. The mining requirement is to cover a three-and-a-half-year peak in waste mining requirements, which is in the Company’s own mining fleet capacity and will allow the Company to focus on mining of gold-containing ore for processing. During the first three months ended March 31, 2019, the Company recorded $4.3 million (2018: $nil) expense on Stracon’s mining contract, which was priced at a fixed cost per tonne of material mined.

SHARE CAPITAL The Company is authorized to issue an unlimited number of common shares. The issued and outstanding common shares consist of the following:

Number of Shares Amount At December 31, 2017 173,070,798 $ 500,769 Issued on exercise of options 460,004

2,239

Fair value of options exercised - 1,180 Deferred tax recovery on share issuance costs - 365 At December 31, 2018 173,530,802 $ 504,553 Issued on exercise of options - - At March 31, 2019 173,530,802 $ 504,553

GUYANA GOLDFIELDS INC. FIRST QUARTER 2019 Notes to the Condensed Interim Consolidated Financial Statements For the three months ended March 31, 2019 and 2018 (Unaudited - Expressed in thousands of U.S. Dollars, unless otherwise indicated)

11

SHARE-BASED PAYMENTS The following share-based payments (recoveries) have been recognized in the consolidated statements of comprehensive loss:

Stock option plan

(equity settled) RSU plan

(cash settled) DSU plan

(cash settled) Total Production costs $ 9 $ (94) $ - $ (85) Corporate administration 85 (94) (162) (171) Restructuring expense - (545) - (545) Exploration and evaluation 2 (2) - - Three months ended March 31, 2019 $ 96 $ (735) $ (162) $ (801)

Production costs $ 64 $ (49) $ - $ 15 Corporate administration 569 143 (22) 690 Exploration and evaluation 27 1 - 28 Three months ended March 31, 2018 $ 660 $ 95 $ (22) $ 733

(a) Stock option plan

The stock option plan of the Company (the “Option Plan”) was approved by the shareholders on May 15, 2015, amended and restated as of February 4, 2016. The exercise price of stock options granted in accordance with the plan will be not less than the closing price of the common shares on the trading day immediately prior to the effective date of grant. All option exercises to be settled in the Company’s shares.

The following table shows the continuity of stock options during the periods presented:

Number of options Weighted average exercise price (Cdn$) At December 31, 2017 6,337,515 $ 4.02 Granted 200,000 3.01 Exercised (1,110,004) 2.67 Forfeited (48,333) 3.87 Expired (12,500) 2.73 At December 31, 2018 5,366,678 $ 4.26 Forfeited (1,250,000) 5.00 Expired (98,335) 2.98 At March 31, 2019 4,018,343 $ 4.05

GUYANA GOLDFIELDS INC. FIRST QUARTER 2019 Notes to the Condensed Interim Consolidated Financial Statements For the three months ended March 31, 2019 and 2018 (Unaudited - Expressed in thousands of U.S. Dollars, unless otherwise indicated)

12

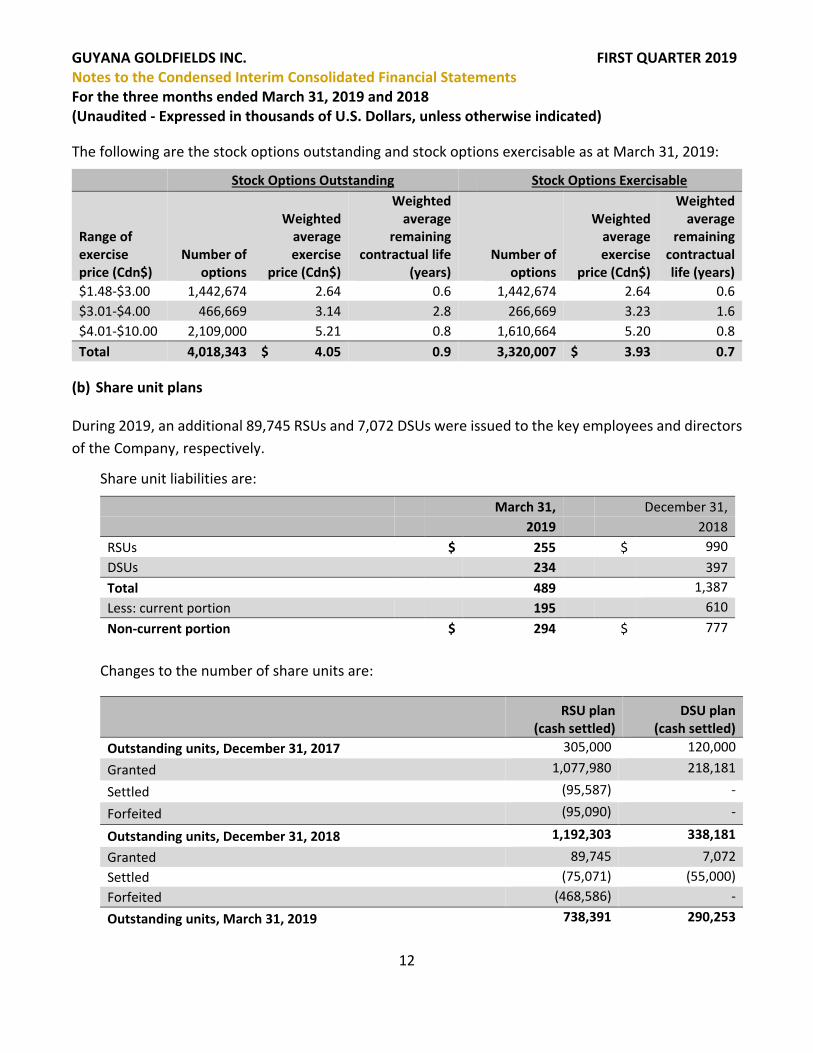

The following are the stock options outstanding and stock options exercisable as at March 31, 2019: Stock Options Outstanding Stock Options Exercisable

Range of exercise price (Cdn$)

Number of options

Weighted average exercise

price (Cdn$)

Weighted average

remaining contractual life

(years) Number of

options

Weighted average exercise

price (Cdn$)

Weighted average

remaining contractual life (years)

$1.48-$3.00 1,442,674 2.64 0.6 1,442,674 2.64 0.6 $3.01-$4.00 466,669 3.14 2.8 266,669 3.23 1.6 $4.01-$10.00 2,109,000 5.21 0.8 1,610,664 5.20 0.8 Total 4,018,343 $ 4.05 0.9 3,320,007 $ 3.93 0.7

(b) Share unit plans

During 2019, an additional 89,745 RSUs and 7,072 DSUs were issued to the key employees and directors of the Company, respectively.

Share unit liabilities are:

March 31, December 31, 2019 2018 RSUs $ 255 $ 990 DSUs 234 397 Total 489 1,387 Less: current portion 195 610 Non-current portion $ 294 $ 777

Changes to the number of share units are:

RSU plan (cash settled)

DSU plan (cash settled)

Outstanding units, December 31, 2017 305,000 120,000 Granted 1,077,980 218,181

Settled (95,587) -

Forfeited (95,090) -

Outstanding units, December 31, 2018 1,192,303 338,181 Granted 89,745 7,072 Settled (75,071) (55,000) Forfeited (468,586) - Outstanding units, March 31, 2019 738,391 290,253

GUYANA GOLDFIELDS INC. FIRST QUARTER 2019 Notes to the Condensed Interim Consolidated Financial Statements For the three months ended March 31, 2019 and 2018 (Unaudited - Expressed in thousands of U.S. Dollars, unless otherwise indicated)

13

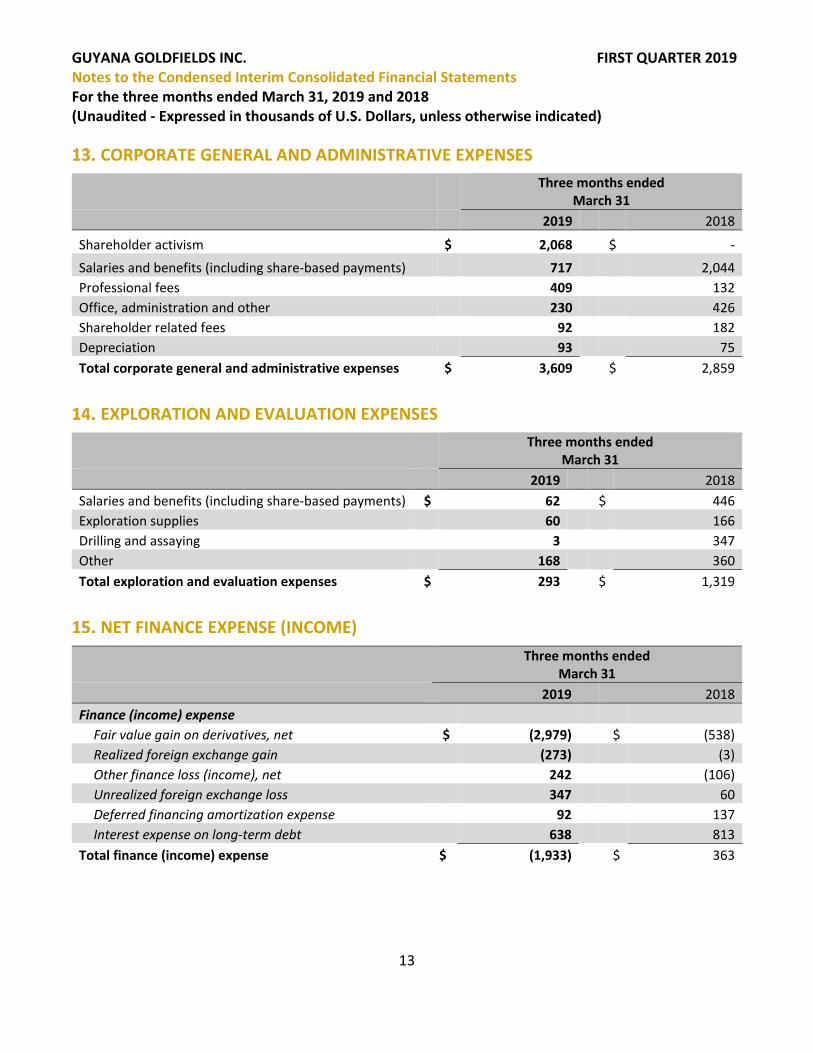

CORPORATE GENERAL AND ADMINISTRATIVE EXPENSES

Three months ended

March 31 2019 2018

Shareholder activism $ 2,068 $ - Salaries and benefits (including share-based payments) 717 2,044 Professional fees 409 132 Office, administration and other 230 426 Shareholder related fees 92 182 Depreciation 93 75 Total corporate general and administrative expenses $ 3,609 $ 2,859

EXPLORATION AND EVALUATION EXPENSES

Three months ended

March 31 2019 2018 Salaries and benefits (including share-based payments) $ 62 $ 446 Exploration supplies 60 166 Drilling and assaying 3 347 Other 168 360 Total exploration and evaluation expenses $ 293 $ 1,319

NET FINANCE EXPENSE (INCOME)

Three months ended

March 31 2019 2018 Finance (income) expense

Fair value gain on derivatives, net $ (2,979) $ (538) Realized foreign exchange gain (273) (3) Other finance loss (income), net 242 (106) Unrealized foreign exchange loss 347 60 Deferred financing amortization expense 92 137 Interest expense on long-term debt 638 813

Total finance (income) expense $ (1,933) $ 363

GUYANA GOLDFIELDS INC. FIRST QUARTER 2019 Notes to the Condensed Interim Consolidated Financial Statements For the three months ended March 31, 2019 and 2018 (Unaudited - Expressed in thousands of U.S. Dollars, unless otherwise indicated)

14

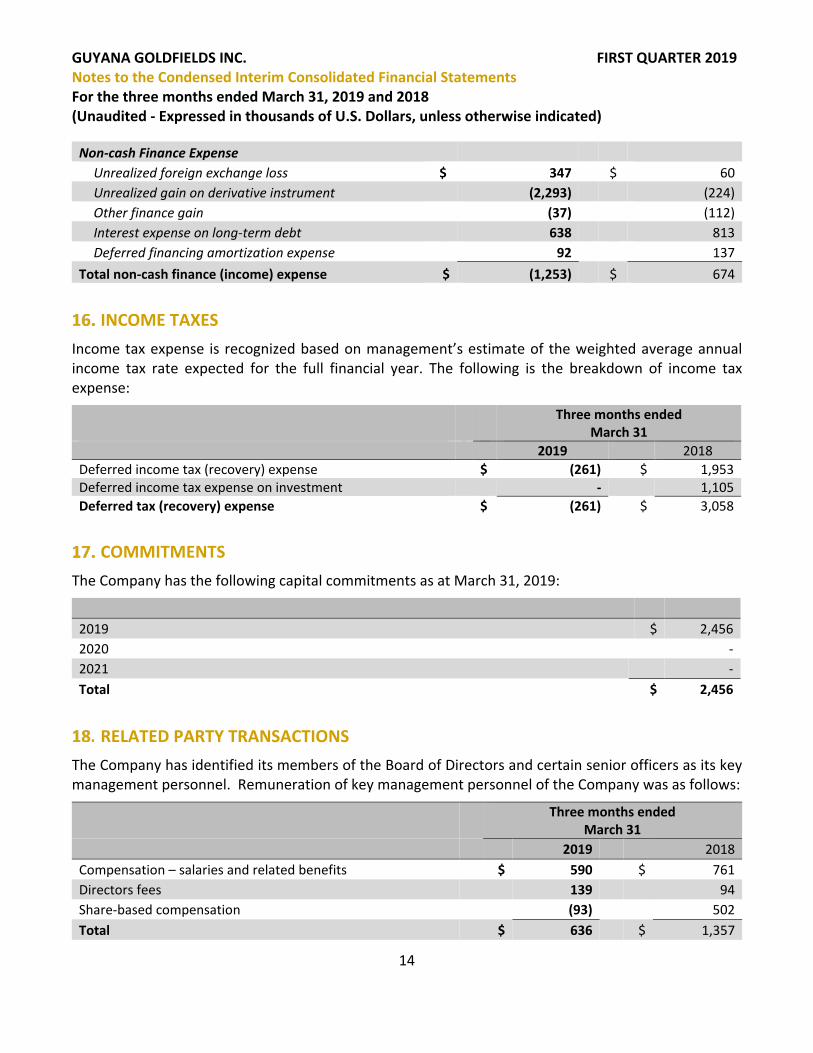

Non-cash Finance Expense Unrealized foreign exchange loss $ 347 $ 60 Unrealized gain on derivative instrument (2,293) (224) Other finance gain (37) (112) Interest expense on long-term debt 638 813 Deferred financing amortization expense 92 137

Total non-cash finance (income) expense $ (1,253) $ 674

INCOME TAXES Income tax expense is recognized based on management’s estimate of the weighted average annual income tax rate expected for the full financial year. The following is the breakdown of income tax expense:

Three months ended

March 31 2019 2018 Deferred income tax (recovery) expense $ (261) $ 1,953 Deferred income tax expense on investment - 1,105 Deferred tax (recovery) expense $ (261) $ 3,058

COMMITMENTS The Company has the following capital commitments as at March 31, 2019:

2019 $ 2,456 2020 - 2021 - Total $ 2,456

RELATED PARTY TRANSACTIONS The Company has identified its members of the Board of Directors and certain senior officers as its key management personnel. Remuneration of key management personnel of the Company was as follows:

Three months ended

March 31 2019 2018 Compensation – salaries and related benefits $ 590 $ 761 Directors fees 139 94 Share-based compensation (93) 502 Total $ 636 $ 1,357

GUYANA GOLDFIELDS INC. FIRST QUARTER 2019 Notes to the Condensed Interim Consolidated Financial Statements For the three months ended March 31, 2019 and 2018 (Unaudited - Expressed in thousands of U.S. Dollars, unless otherwise indicated)

15

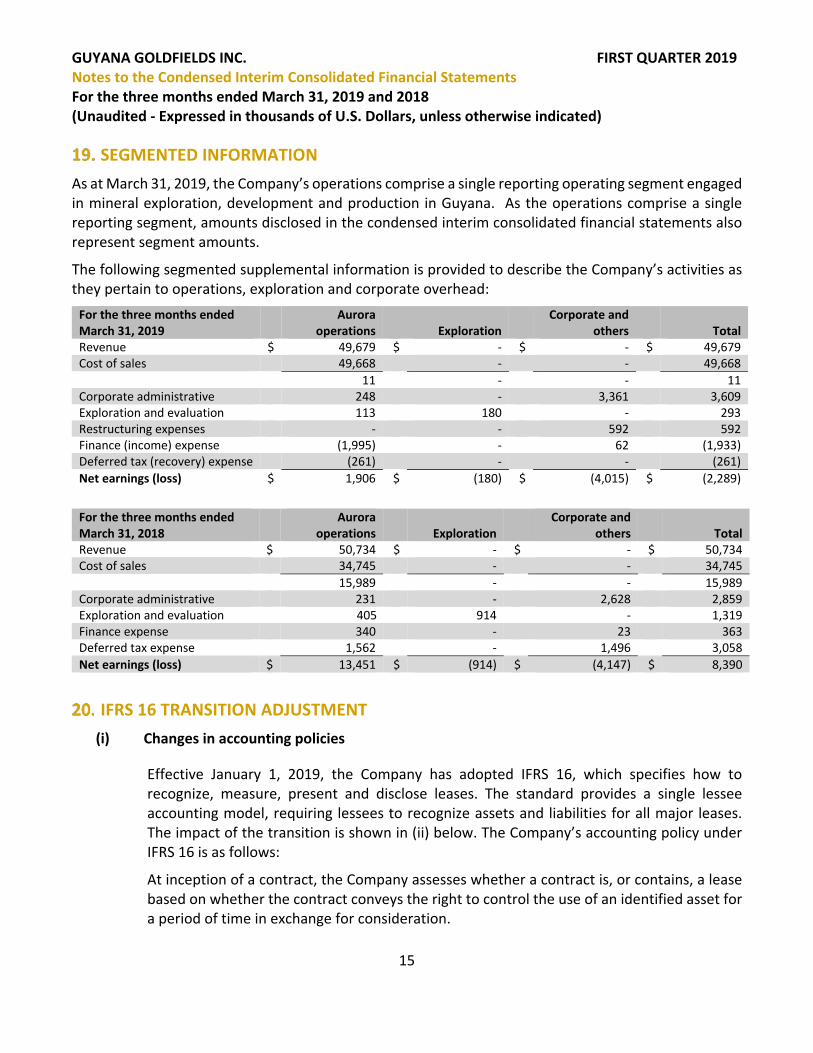

SEGMENTED INFORMATION As at March 31, 2019, the Company’s operations comprise a single reporting operating segment engaged in mineral exploration, development and production in Guyana. As the operations comprise a single reporting segment, amounts disclosed in the condensed interim consolidated financial statements also represent segment amounts.

The following segmented supplemental information is provided to describe the Company’s activities as they pertain to operations, exploration and corporate overhead:

For the three months ended March 31, 2019

Aurora operations Exploration

Corporate and others Total

Revenue $ 49,679 $ - $ - $ 49,679 Cost of sales 49,668 - - 49,668 11 - - 11 Corporate administrative 248 - 3,361 3,609 Exploration and evaluation 113 180 - 293 Restructuring expenses - - 592 592 Finance (income) expense (1,995) - 62 (1,933) Deferred tax (recovery) expense (261) - - (261) Net earnings (loss) $ 1,906 $ (180) $ (4,015) $ (2,289)

For the three months ended March 31, 2018

Aurora operations Exploration

Corporate and others Total

Revenue $ 50,734 $ - $ - $ 50,734 Cost of sales 34,745 - - 34,745 15,989 - - 15,989 Corporate administrative 231 - 2,628 2,859 Exploration and evaluation 405 914 - 1,319 Finance expense 340 - 23 363 Deferred tax expense 1,562 - 1,496 3,058 Net earnings (loss) $ 13,451 $ (914) $ (4,147) $ 8,390

IFRS 16 TRANSITION ADJUSTMENT (i) Changes in accounting policies

Effective January 1, 2019, the Company has adopted IFRS 16, which specifies how to recognize, measure, present and disclose leases. The standard provides a single lessee accounting model, requiring lessees to recognize assets and liabilities for all major leases. The impact of the transition is shown in (ii) below. The Company’s accounting policy under IFRS 16 is as follows:

At inception of a contract, the Company assesses whether a contract is, or contains, a lease based on whether the contract conveys the right to control the use of an identified asset for a period of time in exchange for consideration.

GUYANA GOLDFIELDS INC. FIRST QUARTER 2019 Notes to the Condensed Interim Consolidated Financial Statements For the three months ended March 31, 2019 and 2018 (Unaudited - Expressed in thousands of U.S. Dollars, unless otherwise indicated)

16

The Company has elected to apply the practical expedient to account for each lease component and any non-lease components as a single lease component.

The Company recognizes a right-of-use asset and a lease obligation at the lease commencement date. The right-of-use asset is initially measured based on the initial amount of the lease obligation adjusted for any lease payments made at or before the commencement date, plus any initial direct costs incurred and an estimate of costs to dismantle and remove the underlying asset or to restore the underlying asset or the site on which it is located, less any lease incentives received. The assets are depreciated to the earlier of the end of the useful life of the right-of-use asset or the lease term using the straight-line method as this most closely reflects the expected pattern of consumption of the future economic benefits. The lease term includes periods covered by an option to extend if the Company is reasonably certain to exercise that option. Lease terms range from 3 to 45 years for mining contracts and lands. In addition, the right-of-use asset is periodically reduced by impairment losses, if any, and adjusted for certain remeasurements of the lease obligation.

The lease obligation is initially measured at the present value of the lease payments that are not paid at the commencement date, discounted using the interest rate implicit in the lease or, if that rate cannot be readily determined, the Company’s incremental borrowing rate. Generally, the Company uses its incremental borrowing rate as the discount rate.

The lease obligation is measured at amortized cost using the effective interest method. It is remeasured when there is a change in future lease payments arising from a change in an index or rate, if there is a change in the Company’s estimate of the amount expected to be payable under a residual value guarantee, or if the Company changes its assessment of whether it will exercise a purchase, extension or termination option.

When the lease obligation is remeasured in this way, a corresponding adjustment is made to the carrying amount of the right-of-use asset or is recorded in profit or loss if the carrying amount of the right-of-use asset has been reduced to zero.

The Company has elected to apply the practical expedient not to recognize right-of-use assets and lease obligations for short-term leases that have a lease term of twelve months or less and leases of low-value assets. The lease payments associated with these leases are recognized as an expense on a straight-line basis over the lease term.

(ii) Impact of transition to IFRS 16

Effective January 1, 2019, the Company adopted IFRS 16 using the modified retrospective approach and accordingly the information presented for 2018 has not been restated. It remains as previously reported under IAS 17 and related interpretations.

On initial application, the Company recognized lease obligations in relation to leases which had previously been classified as “operating leases” under the principles of IAS 17 Leases.

GUYANA GOLDFIELDS INC. FIRST QUARTER 2019 Notes to the Condensed Interim Consolidated Financial Statements For the three months ended March 31, 2019 and 2018 (Unaudited - Expressed in thousands of U.S. Dollars, unless otherwise indicated)

17

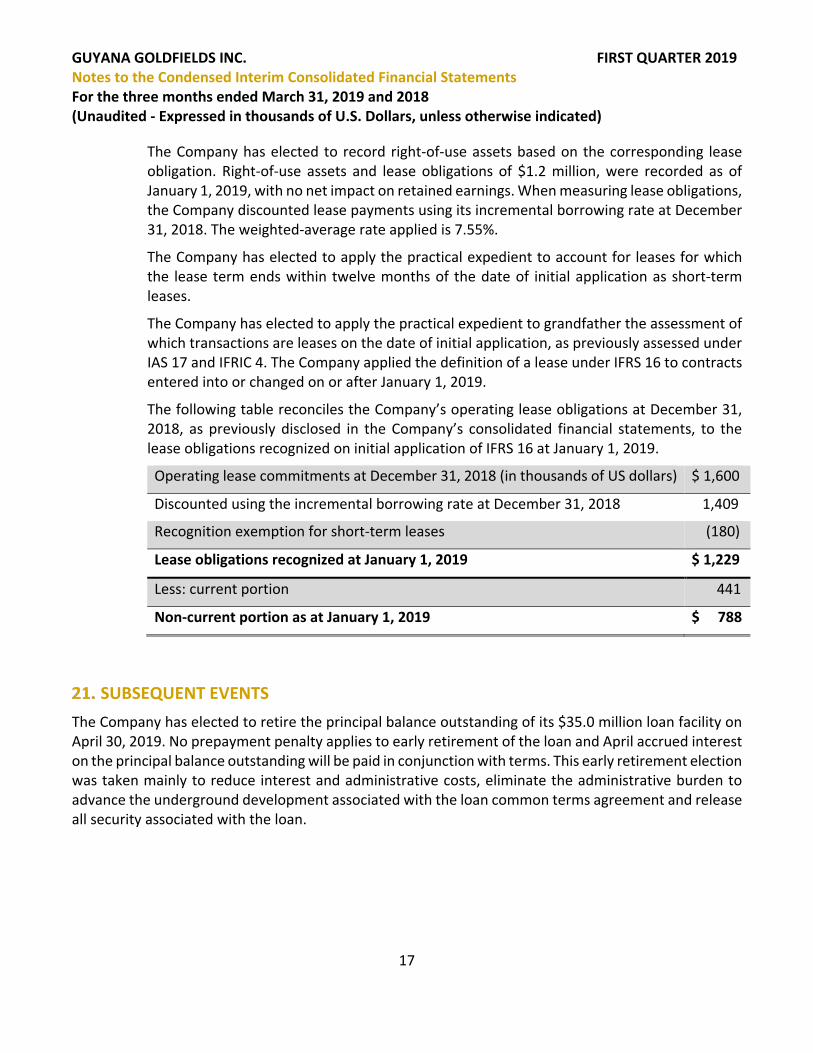

The Company has elected to record right-of-use assets based on the corresponding lease obligation. Right-of-use assets and lease obligations of $1.2 million, were recorded as of January 1, 2019, with no net impact on retained earnings. When measuring lease obligations, the Company discounted lease payments using its incremental borrowing rate at December 31, 2018. The weighted-average rate applied is 7.55%.

The Company has elected to apply the practical expedient to account for leases for which the lease term ends within twelve months of the date of initial application as short-term leases.

The Company has elected to apply the practical expedient to grandfather the assessment of which transactions are leases on the date of initial application, as previously assessed under IAS 17 and IFRIC 4. The Company applied the definition of a lease under IFRS 16 to contracts entered into or changed on or after January 1, 2019.

The following table reconciles the Company’s operating lease obligations at December 31, 2018, as previously disclosed in the Company’s consolidated financial statements, to the lease obligations recognized on initial application of IFRS 16 at January 1, 2019.

Operating lease commitments at December 31, 2018 (in thousands of US dollars) $ 1,600

Discounted using the incremental borrowing rate at December 31, 2018 1,409

Recognition exemption for short-term leases (180)

Lease obligations recognized at January 1, 2019 $ 1,229

Less: current portion 441

Non-current portion as at January 1, 2019 $ 788

SUBSEQUENT EVENTS The Company has elected to retire the principal balance outstanding of its $35.0 million loan facility on April 30, 2019. No prepayment penalty applies to early retirement of the loan and April accrued interest on the principal balance outstanding will be paid in conjunction with terms. This early retirement election was taken mainly to reduce interest and administrative costs, eliminate the administrative burden to advance the underground development associated with the loan common terms agreement and release all security associated with the loan.