Guidance issued on employer shared responsibility...

12

1 Volume 36 | Issue 11 | January 30, 2013 Guidance issued on employer shared responsibility requirements The shared responsibility requirements are one of the most significant provisions that employers need to address under the Affordable Care Act (ACA). Failure to satisfy these requirements could subject employers to significant penalties starting in 2014. The IRS has issued guidance describing the shared responsibility requirements and defined significant terms, like full-time employee. Pending the issuance of final regulations or other guidance, employers can rely on these proposed regulations now to strategize and prepare for compliance with the shared responsibility mandate. In this article: Background | Concept of full-time employee | Hours of Service | Determining large employer status | Identifying full-time employees | Transition relief | Shared responsibility in controlled groups | “Play or pay” shared responsibility requirement | “Play and pay” shared responsibility requirement | Non-calendar year plans — transition rules | Multi-employer plans | Conclusion Background Beginning in 2014, large employers (e.g., employers that employed on average at least 50 full-time employees on business days during the preceding calendar year) may be subject to one of two "shared responsibility" penalties: An employer that fails to offer minimum essential coverage (MEC) to its full-time employees and their dependents may be subject to a nondeductible "play or pay" penalty if any full-time employee enrolls in Exchange coverage and receives a premium tax credit or cost-sharing reduction. The maximum annual “play or pay” penalty is $2,000 for each full-time employee of the employer, disregarding the first 30 full- time employees. Employers that offer MEC to their full-time employees and their dependents may be subject to a nondeductible "play and pay” penalty of $3,000 for each full -time employee who enrolls in Exchange coverage and receives a premium tax credit or cost-sharing reduction because the employer coverage fails to provide minimum value or is unaffordable. Over the past two years, the IRS has issued four notices addressing the shared responsibility requirements. Using concepts expressed in this past guidance, on January 2, 2013, the IRS published proposed regulations on the employer shared responsibility requirements under ACA. The IRS issued additional guidance in Questions and

Transcript of Guidance issued on employer shared responsibility...

1

Volume 36 | Issue 11 | January 30, 2013

Guidance issued on employer shared responsibility requirements

The shared responsibility requirements are one of the most significant provisions that employers

need to address under the Affordable Care Act (ACA). Failure to satisfy these requirements

could subject employers to significant penalties starting in 2014. The IRS has issued guidance

describing the shared responsibility requirements and defined significant terms, like full-time

employee. Pending the issuance of final regulations or other guidance, employers can rely on

these proposed regulations now to strategize and prepare for compliance with the shared

responsibility mandate.

In this article: Background | Concept of full-time employee | Hours of Service | Determining large employer status | Identifying full-time

employees | Transition relief | Shared responsibility in controlled groups | “Play or pay” shared responsibility requirement | “Play and pay”

shared responsibility requirement | Non-calendar year plans — transition rules | Multi-employer plans | Conclusion

Background

Beginning in 2014, large employers (e.g., employers that employed on average at least 50 full-time employees on

business days during the preceding calendar year) may be subject to one of two "shared responsibility" penalties:

An employer that fails to offer minimum essential coverage (MEC) to its full-time employees and their

dependents may be subject to a nondeductible "play or pay" penalty if any full-time employee enrolls in

Exchange coverage and receives a premium tax credit or cost-sharing reduction. The maximum annual

“play or pay” penalty is $2,000 for each full-time employee of the employer, disregarding the first 30 full-

time employees.

Employers that offer MEC to their full-time employees and their dependents may be subject to a

nondeductible "play and pay” penalty of $3,000 for each full-time employee who enrolls in Exchange

coverage and receives a premium tax credit or cost-sharing reduction because the employer coverage fails

to provide minimum value or is unaffordable.

Over the past two years, the IRS has issued four notices addressing the shared responsibility requirements. Using

concepts expressed in this past guidance, on January 2, 2013, the IRS published proposed regulations on the

employer shared responsibility requirements under ACA. The IRS issued additional guidance in Questions and

2

Volume 36 | Issue 11 | January 30, 2013

Answers on Employer Shared Responsibility Under the Affordable Care Act. Comments are due by March 18,

2013, and a public hearing on the regulations will be held on April 23, 2013. The guidance confirmed that

employers can rely on these proposed regulations, and that if the final regulations are more restrictive than the

proposed regulations, they will be applied prospectively.

Concept of full-time employee

Full-time employee status is used both for determining whether an employer meets the definition of a large

employer and for purposes of assessing the penalties. Therefore, it is important to understand the concepts used in

identifying those employees.

The proposed regulations define employee as an individual who is considered a common-law employee under

general applicable principles. Common-law employees are generally individuals directed and controlled by an

employer and for whom an employer would be required to report and pay employment taxes. (See IRS publication

15-A.) Leased employees, sole proprietors, partners in a partnership and 2% S corporation shareholders are not

considered employees.

Generally, a full-time employee is an employee who, for a given calendar month, either averages at least 30 hours

of service per week or has worked at least 130 hours of service during that month. As discussed below, the method

of identifying full-time employees for purposes of determining large employer status differs from the method used

for purposes related to the assessment of the shared responsibility penalty.

Buck Comment. In addressing the shared responsibility requirements and which employees are subject to

these requirements, it is important for employers to determine the employment status of employees — e.g.,

common-law vs. independent contractors; part-time vs. full-time.

Hours of service taken into account in determining full-time employee status

For this purpose, an hour of service means each hour for which an employee is paid or is entitled to payment. This

includes periods during which no services are performed, such as vacation, holiday, illness, incapacity (including

disability), layoff, jury duty, military duty, or a leave of absence.

All hours of service performed by an employee for members of a controlled group are taken into account in

determining status as a full-time employee. Hours of service worked outside of the US are not counted, regardless

of the residency or citizenship of the individual.

Methods of counting The proposed regulations require an employer to count actual hours of service for employees paid on an hourly

basis. For employees not paid on an hourly basis, an employer may use one of the following three methods to

determine hours of service:

Actual hours of service

A days-worked equivalency, with eight hours of service credited for each day worked

A weeks-worked equivalency, with 40 hours of service credited for each week worked

3

Volume 36 | Issue 11 | January 30, 2013

An employer can use different methods for different classifications of non-hourly employees, as long as the

classifications are reasonable and consistently applied. The equivalency methods cannot be used if they would

substantially understate employees’ hours and cause them not to be treated as full-time employees. The employer

may change the method for each calendar year.

Determining large employer status

A large employer is defined as having employed on average at least 50 full-time employees (including full-time

equivalent employees, or FTEs) on business days during the preceding calendar year. This average generally is

determined by adding the total number of full-time employees and FTEs employed during each month of that

calendar year and then dividing by 12. The number of FTEs for a calendar month is determined by adding the

number of hours of service for each employee who was not a full-time employee during that month, up to a

maximum of 120 hours per employee, and dividing the total number by 120. (For purposes of the shared

responsibility penalty, FTEs are used solely to determine large employer status.) Special rules apply for seasonal

workers.

When an employer is a member of a controlled group, all employees of the controlled group are taken into account

when determining whether the 50 full-time employee threshold is reached. An employer that did not exist in the

preceding calendar year will be considered a large employer for the current calendar year if it is reasonably

expected to employ at least an average of 50 full-time employees on business days during the current calendar

year.

The proposed regulations provide transition relief for 2014 by allowing an employer to use a period of at least six

consecutive calendar months in 2013 to determine its status as a large employer, rather than using the entire 2013

calendar year. This is intended to give an employer sufficient time to determine whether it a large employer subject

to the shared responsibility requirements and to implement changes in its health coverage offering, if necessary.

Identifying full-time employees for penalty assessment purposes

The shared responsibility penalties are calculated on a monthly basis. The potential liability of a large employer for

the “play or pay” penalty is determined by the number of full-time employees it had during a calendar month, while

the liability under the “play and pay” penalty is determined by the number of full-time employees who enrolled in

Exchange coverage and received a premium tax credit or cost-sharing reduction during the calendar month. The

IRS acknowledged the difficulties employers may have with making monthly determinations of full-time status.

Concerned that monthly determinations could result in employees moving in and out of employer coverage, and

possibly Exchange coverage, as frequently as monthly, the proposed regulations include an optional “look-back

measurement” method that employers can use as an alternative to making a monthly determination. The approach

builds on the method described in earlier guidance. (See our September 10, 2012 For Your Information.) The look-

back measurement method varies for different groups of employees.

Ongoing employees Ongoing employees are employees who have been employed for at least one “standard measurement period.” To

determine an ongoing employee’s full-time status, the employer may look back over a standard measurement

period that is not less than three months, or more than 12 months. As an administrative accommodation, the

4

Volume 36 | Issue 11 | January 30, 2013

proposed regulations permit employers to use the beginning and end of payroll periods as the beginning and end of

the measurement period provided the payroll periods are one week, two weeks, or semi-monthly in duration.

If the employer determines that an employee averaged at least 30 hours of service over the standard measurement

period, the employee must be treated as a full-time employee over a subsequent “stability period.” The employer

has the option of including an “administrative period” of up to 90 days between the standard measurement period

and the stability period. This administrative period would be used by the employer to determine the employee’s full-

time status and to offer health coverage to those determined to be full-time. These periods are illustrated below:

Look-back method for ongoing employees

Administrative Period

Up to 90 Days

Period used to determine employee

eligibility and enroll employees.

Standard Measurement Period

3 to 12 Calendar Month Period

Period used to determine employee status

as full-time employee. Employee considered

full-time if averaged at least 30 hours per

week during this period.

Stability Period

Period during which employee status

determined in the standard measurement

period is fixed regardless of hours worked

during the stability period.

5

Volume 36 | Issue 11 | January 30, 2013

Determined to be a full-time employee. An employee who is determined to be a full-time employee during a

standard measurement period must be treated as a full-time employee during the subsequent stability period,

regardless of the employee’s actual hours of service during the stability period. In this case, the duration of the

stability period must be the greater of six months or the length of the standard measurement period.

Determined to be a non-full-time employee. An employee who is determined not to be a full-time employee during

the standard measurement period may be treated as a non-full-time employee during the subsequent stability

period, regardless of the employee’s actual hours of service during the stability period. In this case, the duration of

the stability period cannot exceed the length of the standard measurement period.

The standard measurement period and stability period used by an employer must be uniform for all ongoing

employees. However, an employer can use different measurement, stability, and administrative periods for the

following categories of employees:

Each group of collectively bargained employees covered by a separate bargaining agreement

Collectively bargained and non-collectively bargained employees

Salaried and hourly employees

Employees whose primary places of employment are in different states

An employer may change its standard measurement and stability periods each year but cannot make a change for

a given year once the standard measurement period has begun.

Buck Comment. Employers may want to consider coordinating the ongoing employee administrative and

stability periods with the plan year for the health plan. The example below illustrates this approach for a

2015 calendar year plan. The standard measurement period would be the 12-month period from October

15, 2013 through October 14, 2014. The administrative period would be coordinated with the annual open

enrollment period from October 14, 2014, through December 31, 2014. The resulting stability period would

be the 2015 calendar year.

Look-back method example for ongoing employees

Standard Measurement Period

October 15, 2013 to October 14, 2014

Stability Period

January 1, 2015 to December 31, 2015

Administrative Period

October 14, 2014 to December 31, 2014

6

Volume 36 | Issue 11 | January 30, 2013

New full-time employees If a new employee is reasonably expected to be employed on average at least 30 hours a week, then coverage

must be offered within three months of his or her start date (the date the employee is first required to be credited

with an hour of service with the employer).

New variable hour or seasonal employees A new employee is considered a “variable hour employee” if, at the start date, it cannot be determined that the

employee is reasonably expected to be employed on average at least 30 hours per week. The proposed

regulations do not define “seasonal employee,” and employers are permitted to use a reasonable good faith

interpretation of the term through 2014. The preamble to the proposed regulations specifies that educational

organizations may not treat employees who work only during the active portions of the academic year as seasonal

employees.

The method of determining the full-time employee status of new variable hour employees and seasonal employees

is similar in concept to that used for ongoing employees, but it is more complicated. An employer may use an “initial

measurement period” of between three and 12 months that begins on any date between the employee’s start date

and the first day of the calendar month following the start date. An administrative period of up to 90 days is also

allowed. But, the combination of the initial measurement period and the administrative period “may not extend

beyond the last day of the first calendar month beginning on or after the one-year anniversary of the employee’s

start date.”

Determined to be a full-time employee. An employer must treat an employee who is determined to be a full-time

employee during the initial measurement period as a full-time employee during the subsequent stability period. In

this case, the duration of the stability period must be the same length as the stability period for ongoing employees.

Determined to be a non-full-time employee. If the employee is determined to be a non-full-time employee during the

initial measurement period, then the employee would be treated as a non-full-time employee during the subsequent

stability period. In this case, the stability period can be no more than one month longer than the initial measurement

period.

New employee — variable hour employees

Administrative Period

Up to 90 Days

Standard

Measurement Period

3 to 12 calendar month

period

Stability

Period

Waiting Period

7

Volume 36 | Issue 11 | January 30, 2013

After a new variable hour or seasonal employee has been employed by an employer for a “standard measurement

period,” the employee is considered to be an ongoing employee and must have his or her hours measured on the

same basis as other ongoing employees.

Other employee situations The proposed regulations also address other special situations:

A new variable hour employee or seasonal employee who has a change in employment status, such that

the individual is now reasonably expected to work 30 or more hours of service per week during the initial

measurement period, must be treated as a full-time employee on the first day of the fourth month following

the change in status. However, a change in employment status of an ongoing employee does not change

the employee’s status as a full-time or non-full-time employee. (In both of these situations, an employer is

always allowed to change the employee’s status to full-time.)

Special rules are provided for determining the status of new variable hour employees who are rehired after

a termination of employment or return to service after other absences.

New employees who are expected to be employed on average at 30 hours or more per week for a short

term of employment are subject to the same rules described above. Similarly, there are no special rules for

employees hired into high-turnover positions.

Identifying full-time employees — transition relief for 2014 stability periods

In order to use the look-back measurement method for determining full-time employees for 2014, employers will

need to start their measurement periods in 2013. Employers who want to use a 12-month measurement period with

a corresponding 12-month stabilization period will face time constraints in doing so. Therefore, solely for the

purposes of stability periods beginning in 2014, employers can use a transition measurement period that meets

these conditions:

Is shorter than 12 months, but no less than six months

Begins no later than July 1, 2013

Ends no earlier than 90 days before the first day of the plan year beginning on or after January 1, 2014

Buck Comment. This is significant transition relief of which employers who want to use a 12-month

measurement and stability period will likely want to take advantage for 2014. However, employers still need

to implement procedures quickly for collecting data on employee work hours, if they are not already

tracked.

For example, an employer with a calendar year plan could use a six-month measurement period starting April 15,

2013, with an administrative period starting October 14, 2013, as shown below:

8

Volume 36 | Issue 11 | January 30, 2013

2014 transition relief — look-back method example

Separate assessment of shared responsibility penalties within controlled group

While determination of large employer status is made on a controlled group basis, the assessment of the shared

responsibility penalties will be determined on a member-by-member basis within the controlled group. Therefore,

shared responsibility penalties will be “computed and assessed separately for each applicable large employer,

taking into account that member’s offer of coverage and based on that member’s number of full-time employees.”

Buck Comment. The application of the shared responsibility requirements separately to each employer

within a controlled group is welcome news for employers in a controlled group. This guidance will enable

those affected employers to develop compliance strategies separately for each employer in the controlled

group. However, it is important to note that the nondiscrimination requirements under Section 105(h) for

self-funded plans still apply, and ACA also includes similar nondiscrimination requirements for insured

plans. The nondiscrimination rules under 105(h) appear to limit an employer’s ability to offer coverage to

some members of a controlled group, while not offering coverage to other members, unless done on a

nondiscriminatory basis.

The guidance does not permit the application of the shared responsibility requirements independently to

separate lines of business within an employer.

Within a controlled group, only a single 30 full-time employee reduction in determining the penalty is allowed. It

must be prorated among the employers in the controlled group to prevent smaller members of the group from

avoiding the penalty altogether.

Measurement Period

April 15, 2013 to October 14, 2013

Stability Period

January 1, 2014 to December 31, 2014

Administrative Period

October 14, 2013 to December 31, 2013

9

Volume 36 | Issue 11 | January 30, 2013

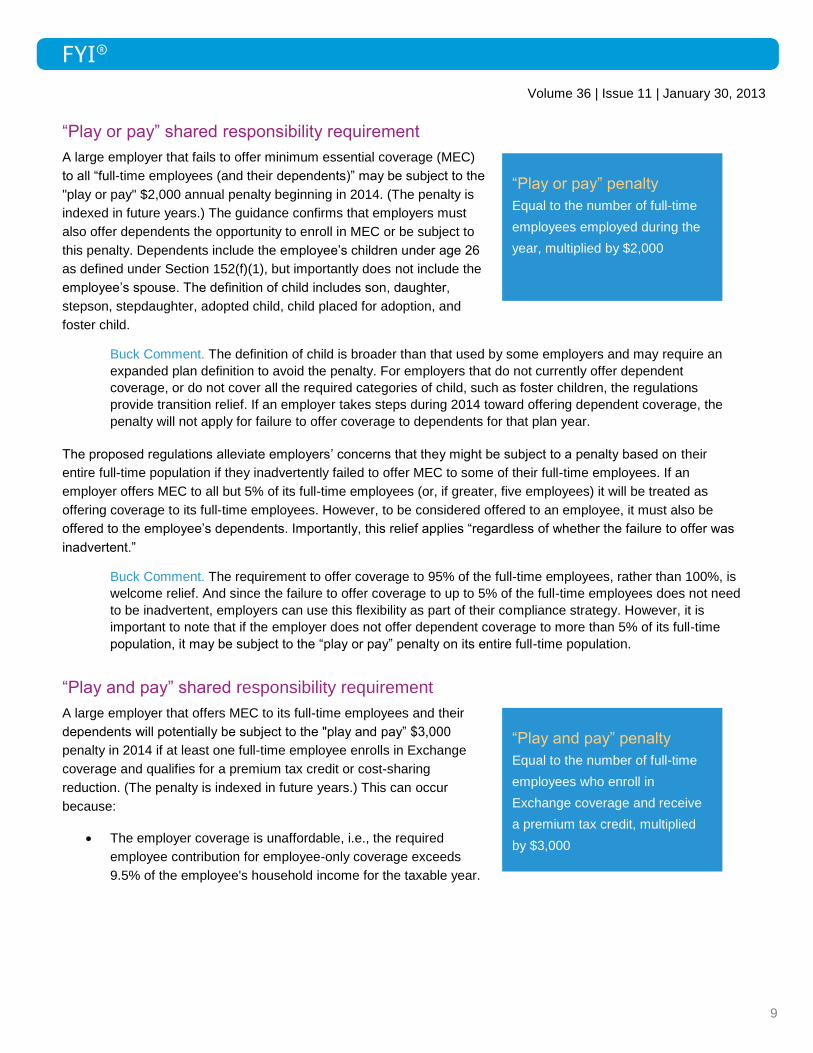

“Play or pay” shared responsibility requirement

A large employer that fails to offer minimum essential coverage (MEC)

to all “full-time employees (and their dependents)” may be subject to the

"play or pay" $2,000 annual penalty beginning in 2014. (The penalty is

indexed in future years.) The guidance confirms that employers must

also offer dependents the opportunity to enroll in MEC or be subject to

this penalty. Dependents include the employee’s children under age 26

as defined under Section 152(f)(1), but importantly does not include the

employee’s spouse. The definition of child includes son, daughter,

stepson, stepdaughter, adopted child, child placed for adoption, and

foster child.

Buck Comment. The definition of child is broader than that used by some employers and may require an

expanded plan definition to avoid the penalty. For employers that do not currently offer dependent

coverage, or do not cover all the required categories of child, such as foster children, the regulations

provide transition relief. If an employer takes steps during 2014 toward offering dependent coverage, the

penalty will not apply for failure to offer coverage to dependents for that plan year.

The proposed regulations alleviate employers’ concerns that they might be subject to a penalty based on their

entire full-time population if they inadvertently failed to offer MEC to some of their full-time employees. If an

employer offers MEC to all but 5% of its full-time employees (or, if greater, five employees) it will be treated as

offering coverage to its full-time employees. However, to be considered offered to an employee, it must also be

offered to the employee’s dependents. Importantly, this relief applies “regardless of whether the failure to offer was

inadvertent.”

Buck Comment. The requirement to offer coverage to 95% of the full-time employees, rather than 100%, is

welcome relief. And since the failure to offer coverage to up to 5% of the full-time employees does not need

to be inadvertent, employers can use this flexibility as part of their compliance strategy. However, it is

important to note that if the employer does not offer dependent coverage to more than 5% of its full-time

population, it may be subject to the “play or pay” penalty on its entire full-time population.

“Play and pay” shared responsibility requirement

A large employer that offers MEC to its full-time employees and their

dependents will potentially be subject to the "play and pay” $3,000

penalty in 2014 if at least one full-time employee enrolls in Exchange

coverage and qualifies for a premium tax credit or cost-sharing

reduction. (The penalty is indexed in future years.) This can occur

because:

The employer coverage is unaffordable, i.e., the required

employee contribution for employee-only coverage exceeds

9.5% of the employee's household income for the taxable year.

“Play or pay” penalty

Equal to the number of full-time

employees employed during the

year, multiplied by $2,000

“Play and pay” penalty

Equal to the number of full-time

employees who enroll in

Exchange coverage and receive

a premium tax credit, multiplied

by $3,000

10

Volume 36 | Issue 11 | January 30, 2013

The employer coverage does not provide minimum value (i.e., the plan’s share of the total allowed costs is

less than 60% of the costs).

The employer offers coverage to at least 95%, but less than 100%, of its full-time employees, and one of

the full-time employees not offered coverage enrolls in Exchange coverage.

Buck Comment. Only one employer health option needs to satisfy the affordability and minimum value

requirements to avoid the penalty. The proposed regulations confirm that affordability for purposes of the

employer penalty will be based on the cost of employee-only coverage, and not the cost of family coverage.

Still not addressed in guidance is the treatment of wellness incentives and surcharges in determining

affordability. The guidance notes that the determination of affordability for purposes of the individual

premium tax credit based on the affordability of family coverage will be addressed in future guidance.

While ACA does not require that MEC provide minimum value or be affordable, guidance is required on what

employer-provided coverage will be considered MEC for purposes of the employer penalties. The proposed

regulations state that additional guidance will be provided in the future.

In Notice 2011-73 (see our September 20, 2011 For Your Information), the IRS outlined a proposed safe harbor

approach for determining affordability based on Form W-2 reporting for purposes of the employer “play and pay”

penalty and asked for other potential safe harbor approaches. Based on comments received, the proposed

regulations provide two additional safe harbor approaches that employers can use to determine affordability.

W-2 Safe Harbor – Affordability is based on the amount reported in Box 1 of the Form W-2 for the

employee. If the employee annual contribution for employee-only coverage does not exceed 9.5% of the

Form W-2 amount, the employer coverage would be deemed affordable. This determination would be made

at the end of the year. Adjusted W-2 amounts and employee contributions are used for employees who did

not work the entire year for the employer.

Rate of Pay Safe Harbor – Affordability is based on the rate of pay as of the beginning of the coverage

period (usually the first day of the plan year). For an hourly employee, the monthly wage equals the hourly

rate of pay times 130 hours (for a salaried employee, it is the monthly salary). If the employee’s monthly

contribution for employee-only coverage does not exceed 9.5% of the monthly wages, the employer

coverage would be affordable. Note that this safe harbor is not available if the employer reduces wages for

the applicable group during the year.

Federal Poverty Line Safe Harbor – Affordability is based on the federal poverty line (FPL) for a single

individual. If the employee contribution for self-only coverage does not exceed 9.5% of the FPL, the

employer coverage would be affordable for all employees. For example, the 2012 FPL for a single

individual is $11,170. Assuming this FPL applies in 2014, if the annual employee contribution for self-only

coverage is not greater than $1,061.15 (9.5% of the FPL), the employer coverage would be affordable.

The use of these safe harbors is optional. An employer can also choose to use a different safe harbor for any

reasonable category of employees, as long as the basis is uniform and consistent for all employees in a category. It

is also important to note that the safe harbors are only used for determining affordability for purposes of the

employer penalty and do not affect the employee’s eligibility for Exchange subsidies, which will still be based on the

employee’s household income.

11

Volume 36 | Issue 11 | January 30, 2013

Buck Comment. While the other two safe harbors will likely support higher employee contribution levels, the

FPL safe harbor provides a simple approach that employers can use prospectively to determine quickly if a

coverage option is affordable for all employees, or to design a coverage option that will be affordable for all

employees.

Non-calendar year plans — transition rules

The January 1, 2014 effective date of the shared responsibility requirements presents special issues for non-

calendar year (fiscal year) plans for both employers and employees.

Employer issues Employers with non-calendar year plans would either need to comply with the shared responsibility requirements at

the beginning of the plan year in 2013, or change the terms and conditions of the plan mid-year. Also, to use the

look-back measurement method for determining full-time employees, employers with non-calendar year plans

would have been required to track employee hours of service before the guidance in these regulations was

released. To address these concerns, the preamble outlines transition relief for non-calendar year plans in effect as

of December 27, 2012.

If the employer with a non-calendar year plan offers employees MEC that is affordable and satisfies the minimum

value coverage by the first day of the plan year starting in 2014, no employer shared responsibility penalties would

apply for the period prior to the plan year that begins in 2014.

Buck Comment. This transition rule provides important relief for non-calendar year plans and provides

these plans with additional time for compliance. However, it is not clear how the transition rule would

operate if the employer did not offer MEC that is affordable and satisfies the minimum value requirement for

all employees. The proposed regulations indicated that appropriate transition rules are being developed for

employees in these plans to account for premium tax credits being available for the 2014 calendar year.

Employee issues Most employers allow employees to pay their contributions on a pre-tax basis through a Section 125 cafeteria plan.

These pre-tax contribution elections are irrevocable during the plan year, unless the employee experiences a

“change in status event” that affects eligibility for coverage, and the cafeteria plan permits a change in election.

With the availability of health plan coverage through an Exchange on January 1, 2014, some employees may want

to drop employer coverage and enroll in an Exchange plan. Similarly, to avoid the individual mandate penalty,

employees not covered under the employer plan may want to enroll in the employer plan effective January 1, 2014.

However, these election changes are not allowed under Section 125 regulations.

The guidance provides transition relief for non-calendar year cafeteria plans beginning in 2013. The plan may

permit:

An employee who elected to make pre-tax contributions for health coverage to revoke prospectively or

change that election once during the plan year that begins in 2013.

An employee who failed to elect health coverage under an employer plan to enroll prospectively in that

coverage during the plan year that begins in 2013.

12

Volume 36 | Issue 11 | January 30, 2013

An employer who wants to permit these election changes must incorporate these rules into its plan document. The

guidance allows a retroactive amendment to the first day of the 2013 plan year, if made by December 31, 2014.

Multi-employer plans

Special transition relief is provided for 2014 for large employers participating in a multi-employer plan. A large

employer will not be treated as failing to offer MEC to a full-time employee if:

The employer is required to make a contribution to a multi-employer plan for a full-time employee pursuant

to a collective bargaining agreement or related participation agreement.

Coverage under the multi-employer plan is offered to the full-time employee (and the employee’s

dependents).

The coverage offered to the full-time employee is affordable and provides minimum value.

The multi-employer plan must also comply with the 90-day limitation on waiting periods under ACA.

Conclusion

While additional guidance is still needed in many significant areas of ACA, plan sponsors now have the key

guidance required to develop a 2014 compliance strategy to address the employer shared responsibility

requirements.

Authors

Richard Stover, FSA, MAAA

Sharon Cohen, JD

Mary Harrison, JD

Leslye Laderman, JD, LLM

Produced by the Knowledge Resource Center of Buck Consultants at Xerox

The Knowledge Resource Center is responsible for national multi-practice compliance consulting, analysis and publications,

government relations, research, surveys, training, and knowledge management. For more information, please contact your

account executive or email [email protected].

You are welcome to distribute FYI® publications in their entireties. To manage your subscriptions, or to sign up to receive our

mailings, visit our Subscription Center.

This publication is for information only and does not constitute legal advice; consult with legal, tax and other advisors before applying this

information to your specific situation.

©2014 Xerox Corporation and Buck Consultants, LLC. All rights reserved. Xerox® and Xerox and Design® are trademarks of Xerox

Corporation in the United States and/or other countries. Buck Consultants® is a registered trademark of Buck Consultants, LLC in the United

States and/or other countries.