GST Mitra | 1apmh.in/apd/images/events/research/pdfs/1499327340-GST Mitra Boo… · GST -Mitra | 1...

92

| 1 | GST - Mitra 1. Registration 2. Invoice 3. Returns 4. Payment of Tax 5. Audit 6. Accounts & Records 7. Assessment 8. Refund 9. Inspection 10. Specific concept (i) Levy of tax (ii) Supply (iii) Job work Provisions (iv) Input Tax Credit (v) Input Service Distributor (vi) Electronic Commerce (vii) Transitional Provisions 11. Quick Reference Charts

Transcript of GST Mitra | 1apmh.in/apd/images/events/research/pdfs/1499327340-GST Mitra Boo… · GST -Mitra | 1...

| 1 |GST - Mitra

1. Registration2. Invoice3. Returns4. Payment of Tax5. Audit6. Accounts & Records7. Assessment8. Refund9. Inspection10. Specificconcept

(i) Levy of tax(ii) Supply(iii) Job work Provisions(iv) Input Tax Credit(v) Input Service Distributor(vi) Electronic Commerce(vii) Transitional Provisions

11. Quick Reference Charts

| 2 | GST - Mitra

| 3 |GST - Mitra

GST MITRA A n I m p l e m e n t a t i o n G u i d e

This B ook is based on CGST & IGST Act confirmed by Parliament on 12th April, 2017.

2 n d E d i t i o n | 1 9 t h J u n e 2 0 1 7

Co-Authored by

CA Pranav Kapadiaand

CA Atul Mehta

Published by

APMH & Associates LLPChartered Accountants

www.apmh.in

For Private Circulation Only

| 4 | GST - Mitra

Preface

GST Mitra – An Implementation Guide

GST is one indirect tax for the whole nation, which will make India a unified common market. While GST promises to usher in an era of unified indirect tax regime, integrating India into a single homogenous market, it comes with certain complications inherited from the legacy tax regime.The objective is to make available a hand book for reference at each step be it GST implementation, compliance, litigation. This shall cover the key provisions of GST in a brief and lucid manner with the business communities, CEO’s and CFO’s, without many technical jargons.GST Mitra is an attempt to simplify the basic concepts of GST with reference to registrations, returns, payment of tax and refund process. In addition to it, this book also explains specific areas like to Job work, E-Commerce, Transitional provisions with the help of examples, relevant images and flowcharts so as to provide practical insights as to how GST would impact the day-to-day business transactions.

- CA Amit Doshi

Chairman APMH & Associates LLP

| 5 |GST - Mitra

About the authors

CA Atul MehtaAtul Mehta is a Partner of APMH & Associates LLP. Atul focuses on accounting and taxation practice of the firm. He has exposure of more than 17 years in accounts outsourcing and tax advisory side with a specialization in Service Tax. His expertise lies in consultancy, opinions and Tax Planning for Corporates and Individuals. Atul can lucidly handle complex audits, advisory and assessment matters issues related

Works Contract matters, CENVAT Credit Rules, Point of Taxation (POT) Rules, Point of Provision of Services (POPS) Rule and so on. Currently Atul is a Convenor for Indirect Taxation Committee of the Chamber of Tax Consultants. He has led the Ghatkopar CA CPE Study Circle of WIRC. Atul has Conducted Training Session organized by WIRC-ICAI and has served at WIRC ICAI Committee for Research and Development and Direct Tax Committee.

Email: [email protected]

| 6 | GST - Mitra

CA Pranav KapadiaPranav Kapadia is a Partner of APMH & Assocaites LLP. Pranav’s expertise lies in Advisory, Audit, Compliance, and Litigation Matters on Value Added Tax (VAT), Central Sales Tax (CST), Profession Tax (PT) and Service Tax. Pranav has been consultant to large corporates with presence in Multiple States with complex structures in Indirect Tax, especially VAT. Pranav lucidly deals in complex legal matters like Works Contracts

(WCT), DDQ (Determination Disputed Question) now called Advance Ruling (AR), Assessments and Appeals related to VAT and Allied Tax Laws.He is the Vice President of The Goods and Services Tax Practitioners’ Association of Maharashtra for 2016-17. Pranav is also part of the Indirect Tax Research Committee of the WIRC of ICAI. He has been past Chairman of Indirect Tax Committee of The Chamber of Tax Consultants for 2014-15 and past Convenor of Ghatkopar CPE Study Circle of ICAI. Pranav has addressed various seminars and lectures on MVAT, CST and GST at the STPAM, Chamber of Tax Consultants, WIRC Study Circles of ICAI and various Industrial Associations in Mumbai and across Maharashtra. He has also bagged various awards at the STPAM.Email : [email protected]

| 7 |GST - Mitra

| 8 | GST - Mitra

| 9 |GST - Mitra

| 10 | GST - Mitra

| 11 |GST - Mitra

Table of Contents

Sr. No. Particulars

1. Registration • Liability for Registration (New Dealer) in GST ............. 15 • For whom registration compulsory? ............................... 15 • GST Registration for regular dealers / composite tax payer ............................................................................... 16 • Procedure for Migration (existing dealers) ..................... 17 • Amendment of Registration .............................................. 18 • Cancellation of registration ............................................... 19 • Revocation of cancelled Registration ............................... 20 • Issuance of registration certificate .................................... 20 • Display of registration Certificate .................................... 20 • GST registration form for other stakeholders ................. 21 2. Invoice • Format ............................................................................... 22 • Time limit for issuing Invoice ........................................ 24 • Manner of issuing Invoice ............................................. 24 3. Returns • Due date For Filing of Returns ...................................... 25 • Levy of Late Fees ............................................................. 26 • HSN / SAC Codes ............................................................ 26 • Key components of GSTR1, GSTR2, GSTR3 ................ 27 • Process flow for monthly filing of return .................... 30 4. Payment of Tax • Types of Electronic Ledger ............................................ 31 • Rules for Utilization of cash ........................................... 31 • Interest on delayed Payment of Tax.............................. 33 • Tax deduction at source .................................................. 33 • E-Commerce Operator .................................................... 33

| 12 | GST - Mitra

5 Audit • By tax authorities ............................................................. 34 • Special Audit .................................................................... 34 6 Accounts & Records • Accounts & records ......................................................... 35 • Period of retention of Accounts ..................................... 36

7 Assessment • Definitions ........................................................................ 36 • Self Assessment................................................................ 36 • Provisional assessment ................................................... 36 • Final assessment .............................................................. 36 • Assessment in case of Non filers of returns ................. 37 • Assessment in case of unregistered persons ............... 37 8 Refund • Refund of Tax ................................................................... 38 • Procedure for Claiming Refund .................................... 38 • GST Refund Forms .......................................................... 39 • Interest on delayed Refund ............................................ 40

9 Inspection • Inspection ......................................................................... 41 • Power to arrest ................................................................. 42 • Power to summon person .............................................. 42 • Access to business premises .......................................... 42

10 SpecificConcept (i) Levy of tax • Imposition (Levy) of tax ........................................... 43 • Reverse Charge .......................................................... 43 • Composition Levy ..................................................... 44

| 13 |GST - Mitra

(ii) Supply • Definition ................................................................... 45 • Time of supply of Goods & Services ...................... 45 • Value of Supply of Goods & Services..................... 49 (iii) Job work Provisions • Definition ................................................................... 51 • Normal provision ...................................................... 51 • Transitional provisions related to job work .......... 52 (iv) Input Tax Credit • Definitions .................................................................. 52 • Eligibility Present ITC ................................................................ 53 GST ITC...................................................................... 53 •Conditions for claiming credit ................................ 53 • Situations where credit not available ..................... 54 • Apportionment of credit .......................................... 56 • Availability of Credit ................................................ 57 (v) Input Service Distributor •Definition ................................................................... 58 • Elements OF ISD ....................................................... 58 • Distribution of Credit ............................................... 58 • Conditions for distribution of Credit ..................... 58 • Practical issue (ISD) .................................................. 59 (vi) Electronic Commerce • Definition ................................................................... 60 •Collection of Tax at source ....................................... 61 • Procedures ................................................................ 62 (vii) Export Transaction •Coverage of Export in GST Law ............................. 63 •“Zero Rated” Supplies ............................................. 63 •Conditions when services are considered as export ...63 •Format of Invoice in case of exports ...................... 64

| 14 | GST - Mitra

(viii) Transitional Provisions •Definitions .................................................................. 64 • Levy and payment of tax ......................................... 65 • Input tax credit .......................................................... 67 • Credit in Inputs held as stock ................................. 68 • Goods returned under GST Law ............................ 69 • Goods sent on approval basis ................................. 70 • Refund claims before appointed date .................... 70 • Refund claim after appointed date ......................... 71 •Existinglitigation Claims of credit ......................................................... 71 Output liability ......................................................... 71 • Revision of Returns................................................... 71 • Revision in Price ........................................................ 72

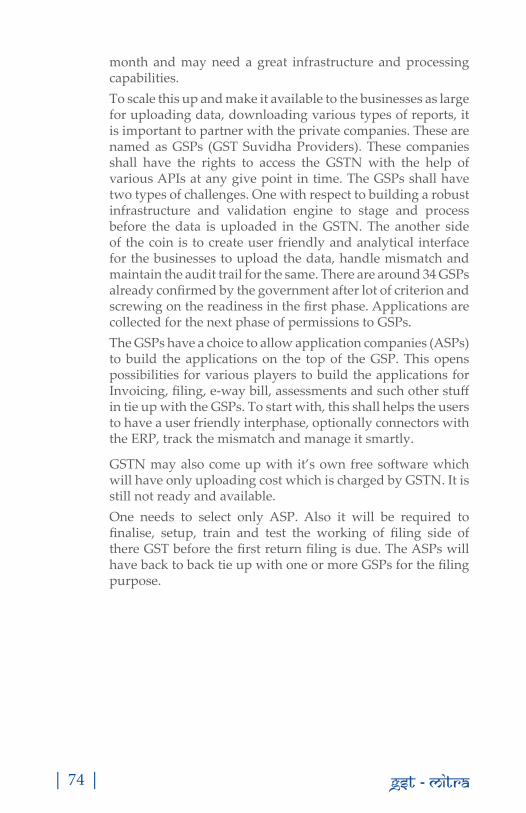

11. Quick Reference Charts • Filing sequence due dates for July, Aug. and Sec. 2017 GST returns ....................................... 73 • What is GSP and ASP ............................................... 73 • IT Changes Action plan for GST transition ........... 75

• Letter to Employees for GST awareness ................ 76

Disclaimer: Content published in this book is based on the GST Acts, Rules, Formats and notifications published till date of last edition. This is to simplify the legal provisions and procedural aspects of of the law keeping in mind a basic businessman and their accounting team, with the helps of simpler language and graphical representation and so may result into error or omission or interpretation differences. This may not be construed as a legal opinion and should not be relied solely upon for critical business and compliance decision.

GST Mitra - You friend and APMH has rolled out the GST Mitra App on Android. The app shall contain the Useful GST articles, GST Latest updates, Notifications, GST Acts, GST Rules.One can search GST Mitra App on Google Play store or use QR Code for GST Mitra App…

| 15 |GST - Mitra

1. GST 2016, Registration (Sec. 22 of CGST Act.)

• LiabilityforRegistration(NewDealer)inGSTRegion Aggregate Turnover

North Eastern States + Sikkim, J & K, Rs. 10 lakhs Himachal Pradesh and Uttarakhand

Rest Of India Rs. 20 lakhs

Aggregate turnover considered here is the total pan -India turnover (including value of taxable, exempt and export supplies) of a business entity, and not state wise.A Business entity has the option of obtaining Single Registration in a State or Multiple Registrations for its different business verticals in a State. Vertical means a distinguishable component of an enterprise that is engaged in supplying an individual product or service or group of related products or services.Eg: ABC LTD is an Indian company; its diversified business includes 4 segments: FMCG, hotels, paperboards, & packaging.If the company is making supplies from different states, then seperate registrations are required in each state.Further, the company has the option to obtain seperate registration for each segment (business vertical) in each state.

• Forwhomregistrationcompulsory?The following categories of suppliers need to mandatorily register irrespective of the turnover:• Taxable person carrying on interstate supply. It also includes

interstate branch transfer supplies.• Casual and nonresident taxable person*• Businesses liable to pay tax under reverse charge• Agents supplying on behalf of a taxable person• Input service Distributors• Sellers on E-commerce platforms• All e commerce operators Eg: Amazon, Flipkart etc.• Persons responsible to deduct TDS

| 16 | GST - Mitra

• Person supplying online information and database access or retrieval services from outside India to unregistered person in India.

• Voluntary registration by a person.• In case of succession of Companies • In case of Amalgamation of companies

* Casual Taxable person means a person who occasionally undertakes transactions involving supply of goods/ services in the course of business whether as principal, agent or in any other capacity, in taxable territory where he has no fixed place of business.

Eg: M/s ABC a Dealer Registered in Maharashtra takes part in an Exhibition-cum-sale at Gujarat will be treated as a Casual Taxable Person in Gujarat and liable for Registration in Gujarat.

* Non resident persons: means a taxable person who occasionally undertakes transactions involving supply of goods / services whether as principal or agent or in any other capacity but who has no fixed place of business in India.

Eg: Consultants with specialized skills coming for designing the residential/ commercial projects for builders.

• GSTRegistrationforregulardealers/compositetaxpayer

Procedure:• Fill part A of form GST REG-01.• GST REG-01 needs to be filed within 30days from the date

person becomes liable for registration. • Provide your PAN, mobile number, E mail– ID • You will receive an application reference number on your

mobile via email.• Fill part B of form GST REG-01 and specify the application

reference number you received.• GST REG-02 is an acknowledgement received for filing

registration.

Followingisthelistofdocumentstobeuploaded-

• Photograph, constitution of taxpayer, proof of place of business

| 17 |GST - Mitra

(own premises/ rented premises), Bank account related proof, Authorization Forms.

• If additional information is required, Form GST REG-03 will be issued to you. In case any other information is required, need to respond in form GST REG-04 within 7 days from the date of receipt of form GST REG 03.

• If all information in form GST REG 01/ 04 is provided , final certificate in form GST REG-06 will be issued

• If the details are not satisfactory, the registration application can be rejected in form GST REG-05.

• ProcedureforMigrationunderGSTfor exisiting dealers

Procedure:• All existing dealers registered under Excise , VAT, Service tax

laws etc and having valid PAN will be allotted a provisional certificate of registration in form GST REG-21

• For enrolment of existing dealers, first a provisional registration shall be granted by the proper officer

The dealers are required to submit Form GST REG-20 along with information and prescribed documents electronically with DSC or e-signature.

Within7working days

from thedate of formGST REG-03

GST - Registration Process

GST

N

Form GST REG-01PART-A

Form GST REG-01PART-B

Pan Mob No. E-Mail ID

Form GST REG - 06 Form GST REG - 04

Certificate ofRegistration

Provide additional details or clarifications

Form GST REG - 05

Rejection of registration application

Applicationreferencenumber

Requireddocuments

App

lican

t

Submission

Within 3 working days

Form GST REG - 02

Acknowledgement

Verification

PAN-verification in portalMob No. - OTP verificationE-Mail ID - OTP verification

Applicationreferencenumber isgenerated

If detailsare complete& satisfactory

If detailsare

satisfactory

Form GST REG - 03

Notice seeking additionaldetails or clarifications

Yes

Yes

No

No

| 18 | GST - Mitra

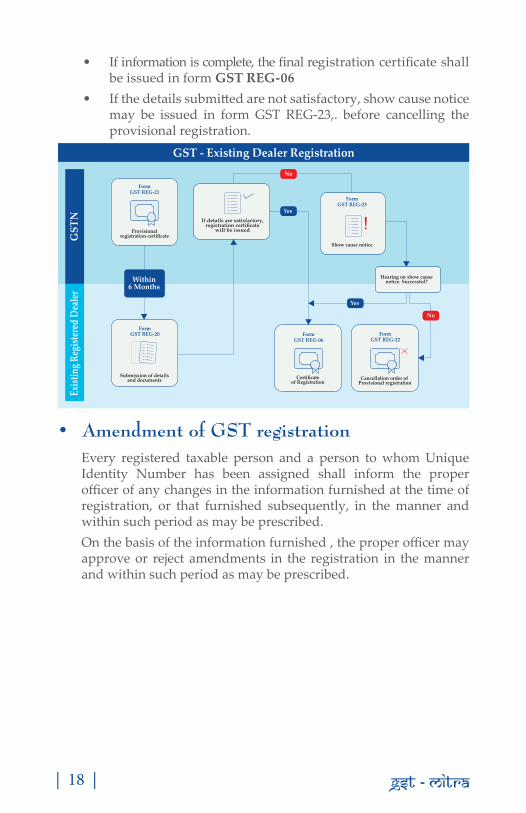

• If information is complete, the final registration certificate shall be issued in form GST REG-06

• If the details submitted are not satisfactory, show cause notice may be issued in form GST REG-23,. before cancelling the provisional registration.

• AmendmentofGSTregistration Every registered taxable person and a person to whom Unique

Identity Number has been assigned shall inform the proper officer of any changes in the information furnished at the time of registration, or that furnished subsequently, in the manner and within such period as may be prescribed.

On the basis of the information furnished , the proper officer may approve or reject amendments in the registration in the manner and within such period as may be prescribed.

GST - Existing Dealer Registration

Exist

ing R

egist

ered

Dea

ler

GST

N

FormGST REG-21

Provisionalregistration certificate

If details are satisfactory,registration certificate

will be issued

FormGST REG-23

Show cause notice

FormGST REG-20

Submission of detailsand documents

FormGST REG-06

Certificate of Registration

FormGST REG-22

Cancellation order of Provisional registration

Hearing on show causenotice. Successful?

Yes

No

Yes

No

Within6 Months

| 19 |GST - Mitra

• CancellationofGSTRegistration

Procedure:- Submit form GST REG-14 for cancellation- Within 7 days, form GST REG-15 issued to show cause reason

for cancellation- After verification, form GST REG-16 is issued within 30 DAYS

from the date of show cause

Applying for Cancellation of Registration

GST

NR

egis

tere

d D

eale

r Form GST REG-14

Application for cancellationof registration

Form GST REG-15

Show cause notice

Show cause hearing.Successful?

Form GST REG-16

Order tocancel registration

Within7 Days

Yes

Amending GST Registration DetailsG

STN

Reg

iste

red

Dea

ler

Form GST REG-11

Change inregistration details

For changes notspecified in rule

FormGST REG-22

Order to amend detailsOnly for changes specified in rule

Approvalby an officerfor changes

specified in rule

Form GST REG-11or

Form GST REG -12

Making changesas per

| 20 | GST - Mitra

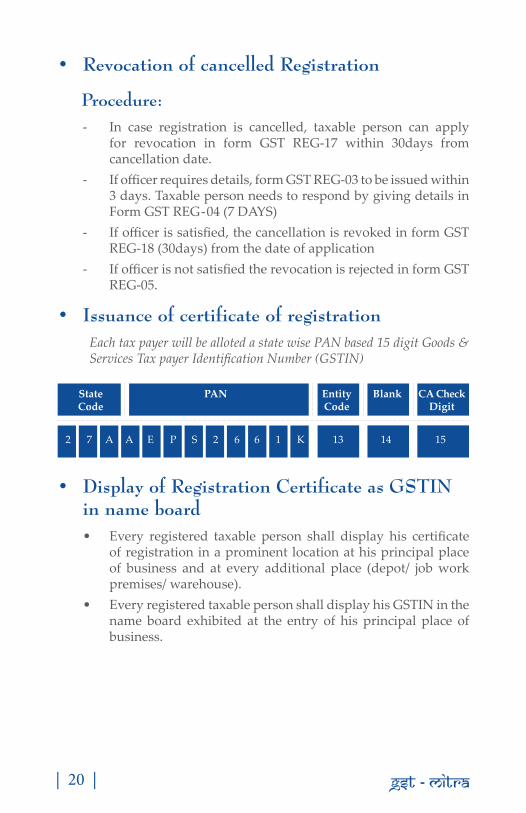

• RevocationofcancelledRegistration

Procedure:- In case registration is cancelled, taxable person can apply

for revocation in form GST REG-17 within 30days from cancellation date.

- If officer requires details, form GST REG-03 to be issued within 3 days. Taxable person needs to respond by giving details in Form GST REG-04 (7 DAYS)

- If officer is satisfied, the cancellation is revoked in form GST REG-18 (30days) from the date of application

- If officer is not satisfied the revocation is rejected in form GST REG-05.

• Issuanceofcertificateofregistration Each tax payer will be alloted a state wise PAN based 15 digit Goods &

Services Tax payer Identification Number (GSTIN)

State PAN Entity Blank CA Check Code Code Digit

2 7 A A E P S 2 6 6 1 K 13 14 15

• DisplayofRegistrationCertificateasGSTINin name board• Every registered taxable person shall display his certificate

of registration in a prominent location at his principal place of business and at every additional place (depot/ job work premises/ warehouse).

• Every registered taxable person shall display his GSTIN in the name board exhibited at the entry of his principal place of business.

| 21 |GST - Mitra

• GSTregistrationformforotherstakeholders

Form No Form TypeGST REG-07 Application for Registration as of person

required to deduct TDS or TCSGST REG-08 Cancellation of application for registration

as of person required to deduct TDS or TCSGST REG-09 Order for cancellation for application for

registration as of person required to deduct TDS or TCS

GST REG-10 Application for registration for non resident taxable person

| 22 | GST - Mitra

2. Tax Invoice (Section 31 of CGST Act)

• Format

DetailsofSupplier• Name, address, registration number (GSTIN) of the supplier• A consecutive serial number not exceeding sixteen

GSTIN: 27AAAAA1111A1Z1 Mode of Transport : By RoadVeh.No :Date & Time of SupplyPlace OF Supply:

Details of Receiver (Billed to)

State: State:State Code : State Code :

Rate Amount Rate Amount Rate Amount

1 1 25 500 12500.00 625.00 11875.00 9.00 1068.75 9.00 1068.75 0.002 1 12 750 9000.00 0.00 9000.00 6.00 540.00 6.00 540.00 0.00

20875 1608.75 1608.75 0.0024092.50

Authorised Signatory

IGST

Serial no. of Invoice:

Name:Address :

GSTIN/Unique ID:

Details of Consignee (Shipped to)

HSN/SAC

Codeunit

CGST

TERMS OF SALE1) Goods once sold will not be taken back or exchanged2)Seller is not responsible for any loss or damaged of goods in transit3)Buyer undertakes to submit prescribted ST declaration to sender ondamand.Disputes if any will be subject to seller court jurisdication

For XYZ

Product2

Remark :Certified that the Particulars given above are true and correct and the amountindicateda) represent the price actually charged and that there is no flow additionalconsideration directly or indirectly from the buyer orb) is provisional as additional consideration will be received from the buyer onaccount of

TotalInvoice Total ( In Words) :

Form GST INV – 1

Name:Address :

GSTIN/Unique ID:

Product1

S.No

SGST/UGST

XYZORIGINAL FOR RECEIPIENT

Plot No. _________________, Pune - 411019, Maharashtra, India

Email : Website : http://xyz.com/

LOGO

Phone : Fax :

Description of Goods Qty Rate Total Discount Taxable value

| 23 |GST - Mitra

characters, in one or multiple series, containing alphabets or numerals or special characters hyphen or dash and slash symbolised as “-” and “/” respectively, and any combination thereof, unique for a financial year

• Date of its issue

DetailsofRecipient• Name, address, and registration number of recipient• In case of URD recipients -Name & Address of recipient

alongwith address of delivery, state & code where taxable value of supply >50,000

OtherDetails• Description of goods or services• HSN code of goods/Accounting code of services• Quantity of goods and units or unique quantity code• Total value of goods and services• Taxable value of goods/ services including (abatements/

Discount)• Rate of Tax• Tax Class

| 24 | GST - Mitra

• Amount of tax charged if any• Place of supply along with the name of State, in case of a

supply in the course of inter-State trade or commerce• Place of delivery where the same is different from the place of

supply

• Time limit for issuing Tax Invoices

Supply of Goods Time Limit

In case of movement Invoice to be issued before or at theof goods time of removal of goods

In other case Invoice to be issued before or at the (no movement of goods) time of delivery of goods or making

available thereof to the recipient

Supply of Services Time Limit

Normal case 30 days from the date of supply of service

Continuous supply 30 days from the date of completionof services of an event in the contract

NBFC/ Bank/ 45 days from the date of supply of Financial Institution services

• Manner of issuing invoice(1) The invoice shall be prepared in triplicate, in case of supply of

goods, in the following manner:–(a) The original copy being marked as ORIGINAL FOR

RECIPIENT;(b) The duplicate copy being marked as DUPLICATE FOR

TRANSPORTER; and(c) The triplicate copy being marked as TRIPLICATE FOR

SUPPLIER.(2) The invoice shall be prepared in duplicate, in case of supply

of services, in the following manner:-(a) The original copy being marked as ORIGINAL FOR

RECIPIENT; and(b) The duplicate copy being marked as DUPLICATE FOR

SUPPLIER.

| 25 |GST - Mitra

3 RETURNS(Sec.37toSec.48ofCGSTAct.)Every registered taxable is required to furnish Electronically the prescribed Returns in the GST regime –There will be common e-return for CGST, SGST, IGST and UTGST for each state.

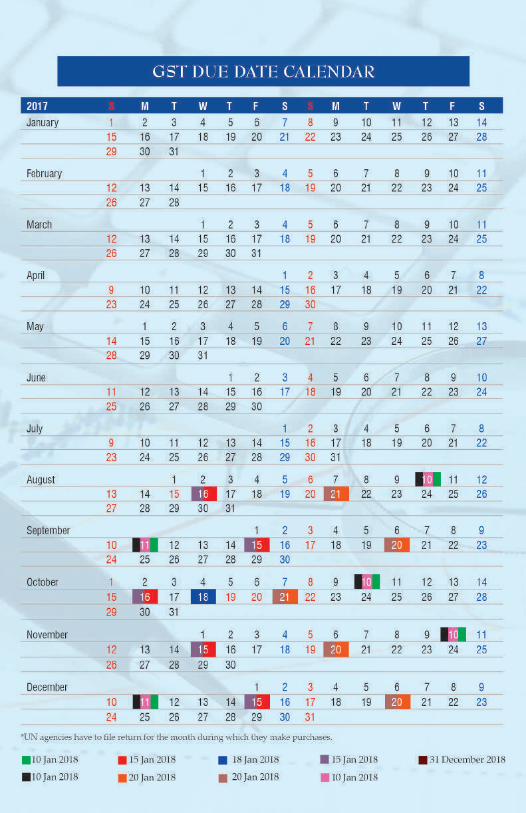

• DueDatesforfilingReturns

GSTR1(OutwardSupplies)• Due date of filing Return 10th next month

GSTR-2(InwardSupplies)• Due date of filing return is 15th of next month

GSTR-3(MonthlyReturns)• Due date of filing of return 20th of next month

GSTR-4(Compoundingtaxpayers)• Due date of filing return is 18 th of next quarter

GSTR-5(Nonresidenttaxpayers)• Due date of filing return is 20th of next month

GSTR-6(Inputservicedistributor)• Due date of filing returns is 15 th of next month

GSTR-7(Taxdeductedatsource)• Due date of filing return is 10th of next month

GSTR-8(TCSStatementforeCo)• Due date of filing return is 10th of next month

GSTR-9(AnnualReturn)• Due date of filing return is 31st december of next year• Annual return information should be matched with monthly/

quarterly return filled by an assessee

| 26 | GST - Mitra

• A return needs to be filed even if there is no business activity (Nil return) during the said tax period of return.

• UN agencies have to file return only for the month during which they make purchases.

• Levyoffeesforlatefilingofreturn

In case of Rs.100 for everyday tillAnnual default ContinuesReturn Or Amount calculated at 0.25% of turnover

in the state

• HSN/SACCodesFollowing parameters with respect to HSN code for goods and accounting codes for services will apply:In all GST Returns return HSN codes for GOODS & SAC CODES for services are mandatory. It is not mandatory if the total turnover is less than 1.5 crores.HSN (Harmonized System of Nomenclature) is an internationally accepted product coding system formulated under General Agreement on Tariffs and Trade (GATT). Services will be required to be classified per the Services Accounting Code (SAC).Under GST, government shall continue the concept of classification based on HSN but a slightly modified version will be implemented wherein the turnover of the tax payers will play a vital role in

whichever is lower Rs.100foreveryday

till default continuesor Rs.5000/-

| 27 |GST - Mitra

determining the code. However there will be separate codes for goods and services.

Broad Rule is as under:

- Summary of supplies effected against a particular HSN code to be reported in summary table in GSTR-1.

- It will be optional for taxpayers having annual turnover upto Rs. 1.50 Cr but they need to provide information about description of goods.

- It will be mandatory to report HSN code at two digits level for taxpayers having annual turnover in the preceding year above Rs.1.50 Cr but upto Rs. 5.00 Cr and at four digits level for taxpayers having annual turnover above Rs. 5.00 Cr.

TofindouttheHSNcodes

Please check www.cybex.in. Enter product name to get the HSN code

To find out SAC code

Please check www.aces.gov.in. Click on e payment, enter assessee code and Captche code. For the

new Service Code kindly refer www.cbec.gov.in.

KeyComponentsofGSTR1,GSTR2,GSTR3

GSTR 1This return would capture the following Information:• Basic details of the tax payer ie Name along with GSTIN• Period to which the return pertains• Aggregate turnover of the tax payer in the previous financial

year and for the period April to June 2017. The aggregate turnover of previous FY would be submitted by the tax payers only in the first year and will auto populated uploaded in the subsequent years.

• Final invoice-level supply information pertaining to the tax periodseparatelyforgoodsandserviceshastobesubmittedas follows:

Invoice-level information pertaining to the tax period should be reported for all supplies as under:(i) For all B to B supplies (whether inter-State or intra-State),

| 28 | GST - Mitra

invoice level details, rate-wise, should be uploaded in Table 4, including supplies attracting reverse charge and those effected through e-commerce operator. Outwards supply information in these categories are to be furnished separately in the Table.

(ii) For all inter-State B to C supplies, where invoice value is more than Rs. 2,50,000/- (B to C Large) invoice level details, rate-wise, should be uploaded in Table 5; and

(iii) For all B to C supplies (whether inter-State or intra-State) where invoice value is up to Rs. 2,50,000/- State-wise summary of supplies, rate-wise, should be uploaded in Table 7

• Details relating to amended taxable outward supplies to be submitted (B2B, B2C suppliers)

• Details relating to advance received against supply to be made in future to be submitted.

• Details relating to taxes already paid on advance receipts for which invoices are issued in the current tax period to be submitted.

• Details relating to nil rated, exempted goods, non taxable outward supplies (both inter-state and intra-state) need to be included in return.

• Details of Exports, Supplies to SEZ units/SEZ Developers, Deemed Exports to be submitted seperately

• Details of Supplies attracting tax on Reverse Charge basis to be submitted.

• There will be a separate table for submitting the details of revisions in relation to the outward supply invoices pertaining to previous tax periods. This will include the details of Credit/Debit Note issued by the suppliers.

• Separate table for modifications/ correcting errors in the returns submitted earlier.

• Details of supplies made through E-Commerce Operators attracting TCS (seperataly to be given operator wise, rate wise, B to B, B To C)

• Monthwise - HSN-wise - summary of Outward Supplies including quantity details to be submitted.

• Serial Numbers of Documents issued during the tax period to be submitted. The documents include 1. Invoices for outward supply 2. Invoices for inward supply from unregistered person

| 29 |GST - Mitra

3. Revised Invoice4. Debit Note5. Credit Note6. Receipt voucher7. Payment Voucher8. Refund voucher9. Delivery Challan for job work10. Delivery Challan for supply on approval11. Delivery Challan in case of liquid gas12. Delivery Challan in cases other than by way of supply

(excluding at S no. 9 to 11)

GSTR 2• The information in GSTR 1 shall be auto populated in concerned

tables in GSTR-2A. The recipient tax payer can accept, modify, reject or keep the transaction pending for action.

• Separate tables for submitting details in relation to ITC received on an invoice on which partial credit has been availed earlier.

• Inward supplies received from a registered person.- Inward supplies on which tax is to be paid on reverse charge.- Inputs/Capital goods received from Overseas or from SEZ

units on a Bill of Entry.- Amendments to details of inward supplies furnished in

returns for earlier tax periods [including debit notes/credit notes issued and their subsequent amendments].

- Supplies received from composition taxable person and other exempt/Nil rated/Non GST supplies received.

- Consolidated Statement of Advances paid/Advance adjusted on account of receipt of supply.

- Input Tax Credit Reversal / Reclaim - Addition and reduction of amount in output tax for

mismatch and other reasons.- Monthwise- HSN codewise summary of inward supplies

including quantity details.• Separate tables for submitting details in relation to ITC eligible

/ available in respect of inputs, input services, capital goods.• Separate tables for ISD credit and TDS/TCS credit received by

Tax payer.

| 30 | GST - Mitra

GSTR3• It consists of aggregate level of outward and inward supply

information which will be uploaded in GSTR 1 and GSTR 2• GSTR 3 can be generated only when GSTR-1 and GSTR- 2 of

the tax period have been filed.• Electronic liability register, electronic cash ledger and

electronic credit ledger of taxpayer will be updated on generation of GSTR-3 by taxpayer.

• Details of payment of tax under various tax heads of CGST, SGST/UTGST, IGST and Cess would be populated from the debit entry in credit/ cash ledger.

• Details of ITC balance of CGST, SGST/UTGST, IGST at the end of the tax period will be auto populated in ITC ledger irrespective of mode of filing return.

• The return would have a field to enable the tax payer to claim refund or to carry forward ITC balance.

• Taxpayer will not be allowed to furnish return for tax period, If valid return for previous tax period has not been furnished.

• If return is furnished without payment of tax, then such return would be invalid.

• Details in GSTR-3 will be auto-populated through GSTR- 1 (of suppliers), own GSTR-2, ISD return, TDS return of deductor, own ITC Ledger, own cash ledger and own tax liability ledger.

• Processflowformonthlyreturnfiling

• GSTR1 All vendors have to update / upload their outward all sales invoices (zero duty , Interstate , Rejected , debit note Or Credit note ) details in return GSTR1 on or before Latest by 10th of every month for last month.

• GSTR1A - deleted, added Or corrected sales invoices details by the recipient ( means Customers) after down Load of GSTR2A by customer on or before Latest by 17th

• All customers Down Load GSTR2A & accepting GSTR2A- (deleted, added Or corrected inward invoices by the suppliers /Vendors) on or before Latest by 15th

Update /Upload Input tax credits to be claimed submi�ing by GSTR2 based on GSTR2A on or before Latest by 15th

Outward goods & Services

In GSTR1 - HSN CODE for GOODS & SAC CODE for

SERVICES is mandatory.

Inwardgoods & Services

Outward goods & Services

Inwardgoods & Services

GSTR3 by 20th Monthly returns Outward Duty Minus Inward duty –Net to be paid (Auto GSTR1 – GSTR2 )

| 31 |GST - Mitra

4.PaymentofTax1. TypeofElectronicLedgers

ThreeElectronicLedgersofthetaxpayers• Amount deposited by the tax payer towards payment of tax,

interest, penalty or fees or any other amount shall be credited to the Electronic Cash Ledger.

• Input tax credit as self assessed by the taxable person shall be credited to his Electronic Credit Ledger

• All the tax liabilities of the taxable person will be recorded in Electronic Tax Liability Register.

Payment of tax through Electronic mode is mandatory.

Whenthepaymenttobemade?• Goods / Services: liability normally arises at the time of

supply of goods• Payment of taxes by the normal tax payers is to be done on

monthly basis by the 20th of the succeeding month. Cash payments to be deposited in the cash ledger and the tax payer will debit the ledger while making the payment in the monthly returns,

GSTR-3 part B will provide details of any tax, interest or penalty payable and return furnished. Without payment of whole tax will be treated as Invalid Return for allowing credit on supplies made.

2. Rules for utilization of cash and cross utilization of input tax credit of IGST, CGST and SGST• Amount in electronic cash ledger can be utilized for making

payment towards tax, penalty, fees or any other amount payable.

• Amount available in electronic credit ledger can only be used for making payment towards tax only not for payment of interest, penalty or fees.

| 32 | GST - Mitra

O/p Tax PREFERE NCE IGST CGST SGST

(-) I/P TAX 1 IGST CGST SGST

2 CGST IGST GST

3 SGST SGST CGST

• Input Tax means IGST/ Tax under reverse charge mechanism/ SGST / CGST / UTGST but does not include composition levy.

• Output Tax means the CGST/SGST chargeable (to be payable) on taxable supply and/or services made by Supplier or his agent.

• In case, any balance remains in cash or credit ledger After payment of Tax, interest, penalty, fee or any other amount would be refunded.

• ListofPaymentFormsareasfollows:

Sr No Form No Title of Return

1 GST PMT-1 Electronic Liability Register

2 GST PMT-2 Electronic credit ledger

3 GST PMT -3 Order by proper officer for Reduction / Rejection of amount of refund applied

4 GST PMT-4 Communication through portal by Registered person to Proper Officer informing discrepancy in electronic ledger

5 GST PMT-5 Electronic Cash Ledger

6 GST PMT-6 Challan for depositing Tax, Interest, penalty or fees

7 GST PMT-7 Communication by depositor to Bank / Electronic Gateway through common portal for non reflection of credit in Electronic Ledger

| 33 |GST - Mitra

3. Interestondelayedpaymentoftax:Every person who fails to pay the tax to the state or central government need to pay the interest at such rate (not exceeding 18%p.a.)asmaybenotifiedbythegovernment. The interest will be calculated from the first day on which such tax was due to be paid. Similarly, in case the taxable person makes an excess claim of input tax credit, then also he shall be liable to pay interest at the rated to prescribed (not exceeding 24% p.a.)• Input Tax is the tax paid or payable in the course of business

on purchases of any goods made from a registered dealer of the state.

• Input Tax Credit is the credit to be taken for tax paid on inputs.

4. TaxDeductionatSourceCentral or state government may mandate departments of central / state governments or local authority or government agencies or any other notified persons to deduct tax at source at the rate of 1 % from the payment made or credited to the supplier of taxable goods/ services notified by the central or State government where the total value of supply exceeds exceeds Two Lakh Fifty Thousand rupees.

| 34 | GST - Mitra

5.Audit

• ByTaxAuthorities1. The commissioner of CGST / Commissioner of SGST or any

officer authorized by them may undertake Audit of any taxable person for such period and in such manner as may be prescribed.

2. The tax Authorities may conduct audit at the place of business of the taxable person and/ or in their office.

3. The taxable person should be informed in advance for the period not less than 15 days prior to conduct of Audit

4. The Audit to be completed within period of 3 months from the date of commencement of Audit.

5. During the conduct of Audit, the Authorized officer may require the assessee.

6. (i) To give him necessary facility to verify the books of Accounts or other documents

(ii) To furnish such information, as he asks for and help him in timely completion of audit.

7. Where the Audit conducted results in tax not deducted or not paid or erroneously refunded or input tax credit wrongly availed or utilized, then proper officer may take action as given under section 66 or 67.

• Special Audit• If at any stage of investigation or any other proceedings before

him, any officer taking into account nature and complexity of the case is of the opinion that the value has not been correctly declared or the input tax credit availed is not within the normal limits (excess availed), then he may , with the prior approval of the commissioner direct the assessee to get his records audited by CA or Cost accountant as may be nominated by the commissioner in this behalf.

• The chartered Accountant or cost Accountant shall within 90days submit a report of such special audit duly signed and certified by him to the said commissioner mentioning therein other particulars as may be specified.

| 35 |GST - Mitra

6. Accounts and records

(a) Who to maintain Accounts and Records under GST?• Every person who get himself registered under GST Law

is required to maintain books of account

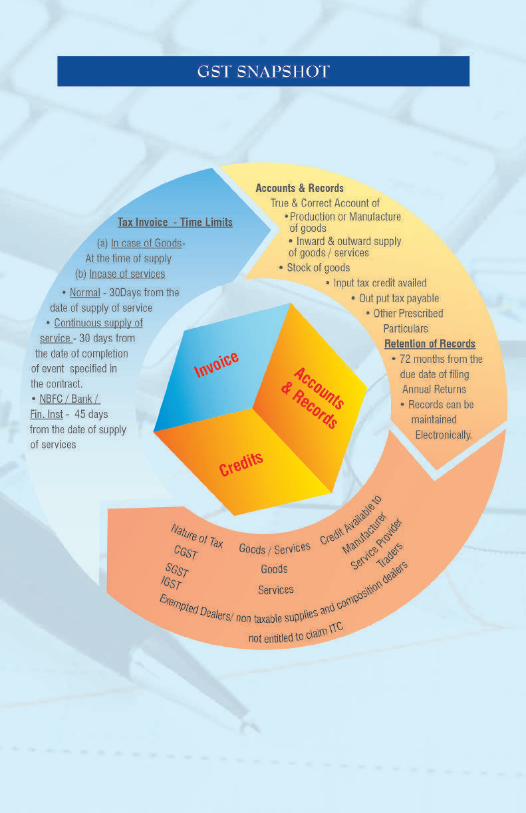

(b) What to maintain in accounts and records un-derGST?True and correct account of • Production or manufacture of goods• Inward and outward supply of goods and/ or services• Stock of goods• Input tax credit availed• Output tax payable and paid• Such other particulars as may be prescribedThese records may be maintained in Electronic form.

(c) Where Accounts and Records to be maintained underGST?• This records are to be kept at the place of business• If the registered taxable person has more than one place

of business, the accounts relating to each place of business shall be kept at such place of business concerned.

(d) Audit of Accounts and records under GST.• Every registered person whose turnover during a financial

year exceeds rupees Two Crore shall get his accounts audited by Chartered Accountant or Cost Accountant, and need to submit the copy of audit report and reconciliation statement

| 36 | GST - Mitra

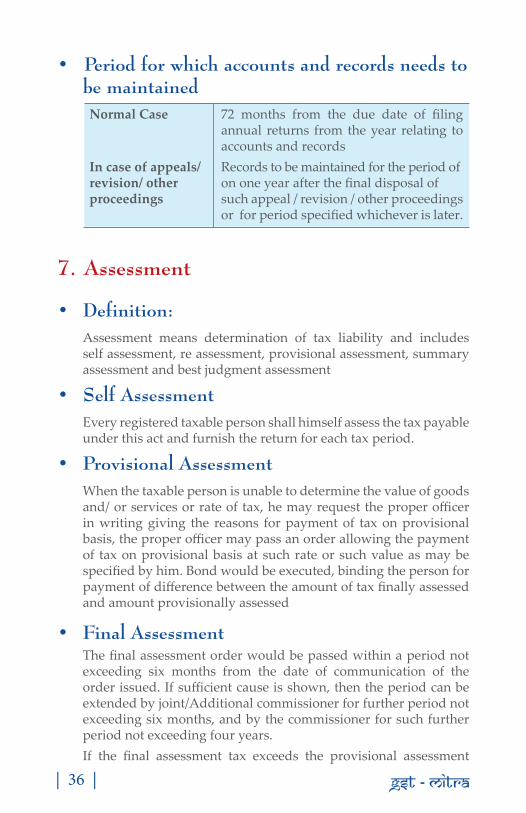

• Periodforwhichaccountsandrecordsneedstobe maintaineditle of

Normal Case 72 months from the due date of filing annual returns from the year relating to accounts and records

In case of appeals/ Records to be maintained for the period of revision/ other on one year after the final disposal of proceedings such appeal / revision / other proceedings

or for period specified whichever is later.

7.Assessment

• Definition:Assessment means determination of tax liability and includes self assessment, re assessment, provisional assessment, summary assessment and best judgment assessment

• SelfAssessmentEvery registered taxable person shall himself assess the tax payable under this act and furnish the return for each tax period.

• ProvisionalAssessmentWhen the taxable person is unable to determine the value of goods and/ or services or rate of tax, he may request the proper officer in writing giving the reasons for payment of tax on provisional basis, the proper officer may pass an order allowing the payment of tax on provisional basis at such rate or such value as may be specified by him. Bond would be executed, binding the person for payment of difference between the amount of tax finally assessed and amount provisionally assessed

• FinalAssessmentThe final assessment order would be passed within a period not exceeding six months from the date of communication of the order issued. If sufficient cause is shown, then the period can be extended by joint/Additional commissioner for further period not exceeding six months, and by the commissioner for such further period not exceeding four years.If the final assessment tax exceeds the provisional assessment

| 37 |GST - Mitra

tax paid then differential amount need to be paid along with the interest. Interest is to be calculated (as per the prescribed rate) from the first day after the due date of payment of tax till the date of actual payment.But in case, the provisional assessment tax exceeds the final assessment tax, it will lead to refund consequent to the order for final assessment. In case refund is not paid within 60 days from the date of application, then interest on refund shall be paid.

• AssessmentincaseofNonfilersofreturnsIf the registered taxable person fails to furnish the return even after the service of notice, the proper officer may proceed to assess the tax liability to the best of his judgment and issue an assessment order within the time limit specified.

• AssessmentincaseofunregisteredpersonsIn case the person fails to obtain registration though he is liable to do so, then the proper officer may assess the tax liability to the best of his judgment and issue assessment order within a period of 5 yearsfromtheduedateoffilingreturns,fortheyeartowhichtax not paid.

| 38 | GST - Mitra

8.Refunds(Sec.54ofCGSTAct.)

• Refund of Tax

WhatisRefundunderGST?Refund include rebate on inputs or input services. Registered taxable person can claim refund of Tax, interest, penalty, fees or any other amount paid by him. Any balance amount standing in the electronic cash ledger can be claimed as refund as per the return furnished in such manner as may be prescribed. It should be noted that no refund of unutilised input credit shall be granted except for 1) Zero Rated Supplies (Exports) made without payment of tax2) Accumulation of credit on account of tax of inputs being

higher than the rate of tax on output supplies (Other than nil rated and fully exempt supplies)

• ProcedureforclaimingrefundAny person claiming refund of any tax or interest needs to make an application to the proper officer of CGST/SGST before the expiry of 2 years from the relevant date.

Limitation period of 2 years will not be applicable if such tax or interest is paid under protest.

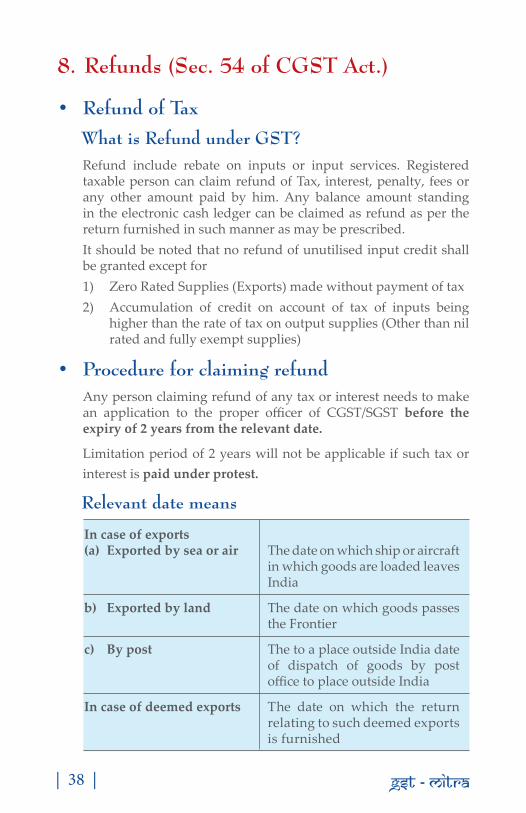

Relevant date means

In case of exports (a) Exported by sea or air The date on which ship or aircraft

in which goods are loaded leaves India

b) Exported by land The date on which goods passes the Frontier

c) By post The to a place outside India date of dispatch of goods by post office to place outside India

In case of deemed exports The date on which the return relating to such deemed exports is furnished

| 39 |GST - Mitra

In case Tax becomes The date of communication of refundable as per judgment, order or directionjudgment, order or direction of appellate tribunal or court

In case tax is The date of adjustment of tax provisionally paid after final assessment

In any other case The date of payment of tax

Theapplicationshouldbeaccompaniedby:

(a) Documentary evidence to establish that refund is due.(b) Other evidence if any to show the amount of tax and interest

is paid and the incidence of tax and interest is not passed on to any other person.

But in case the amount of Refund claim is less Than 2 lacs rupees, it is not necessary to furnish documents, he just have to file a declaration based on the documentary evidence or other evidence.

Incase the proper officer is satisfied that the whole amount claimed as refund is proper, he may make an order of refund and the amount is credited to the Fund. The proper officer will issue the order within 60days from the date of receipt of application.

• GSTrefundformsForm No Name of forms

GST RFD- 01 Refund application formGST RFD-02 AcknowledgmentGST RFD-03 Notice of deficiency on application for refundGST RFD-04 Provisional refund sanction orderGST RFD-05 Payment AdviceGST RFD-06 Order sanctioning RefundGST RFD-07 Refund Adjustment OrderGST RFD-08 Show cause Notice for Non-admissible claimsGST RFD-09 Reply by registered person for Show Cause NoticeGST RFD-10 Refund application form for international

organizationsGST RFD -11 Statement of inward Supplies of Goods or

Services

| 40 | GST - Mitra

Therearecaseswheretherefundcannotbeclaimed:

1. No refund claim of unutilized credit in cases other than exports.

2. In cases where the input credit accumulated is more than output tax liability except in specified cases.

3. No refund of unutilized input tax credit shall be allowed which are subjected to export Duty.

4. No refund of input tax credit shall be allowed if the supplier avails of drawback, central tax of claims refund of output tax paid under IGST Act.

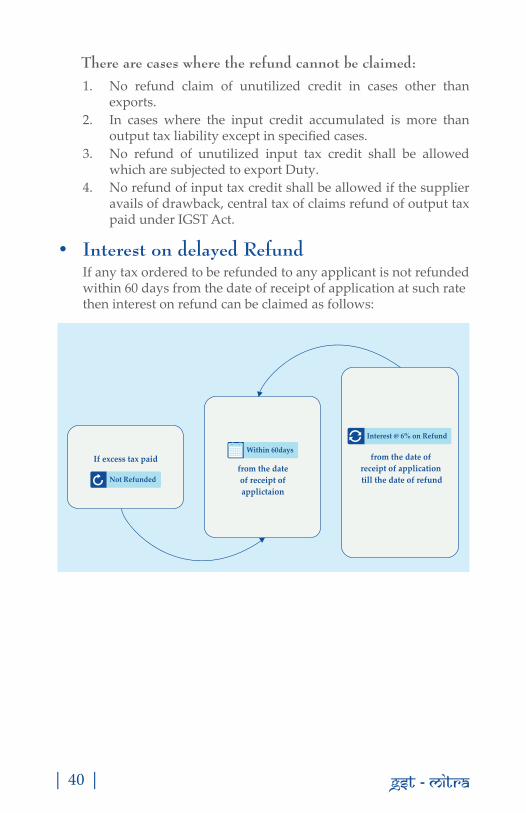

• InterestondelayedRefundIf any tax ordered to be refunded to any applicant is not refunded within 60 days from the date of receipt of application at such rate then interest on refund can be claimed as follows:

If excess tax paid

Not Refunded

from the date of receipt of application till the date of refund

Interest @ 6% on Refund

from the dateof receipt ofapplictaion

Within 60days

| 41 |GST - Mitra

9.Inspection,searchandseizure,arrest

• InspectionInspection can be carried out by an officer of CGST/SGST only upon a written authorization given by an officer of the rank of joint commissioner or above. A joint commissioner can give such authorization only if he has reason to believe that the person concerned has done one of the following:• Suppressed any transactions of supply• Suppressed stock of goods in hand• Claimed excess input tax credit• Contravened any of the provisions to evade the tax• Transporter/owner of warehouse is keeping goods which

have escaped payment of taxAuthorization will be given to carry out inspection of any of the following:• Any place of business of a taxable person.• Any place of business engaged in business of transporting

goods whether or not he is a registered person.• Any place of business of an owner or an operator of a

warehouse or godown.

other Procedure:

• Search and seizes the goods or books or things which in his opinion shall be useful or relevant to any proceedings.

• The officers have the power to seal or break open the door of any premises or to break open almirah, box, in which any goods, accounts etc. are suspected to be concealed.

• The custodian of the seized documents is entitled to make copies thereof or take extracts in the presence of an officer of CGST / SGST

• The officer is bound to issue the notice within 180 days of such seizure and if he fails to do so, then such seized goods are liable to be returned. Such period of 180 days would be extended by competent authority if sufficient cause exists.

• Officer can dispose of certain notified goods immediately after the seizure, if those goods are of perishable or hazardous nature or of depreciating value or there is constrained for shortage.

| 42 | GST - Mitra

• The officer who seizes the goods are liable to maintain the inventory of the said goods.

• Provisions of Criminal Procedure, 1973 relating to search and seizure shall be applicable to GST act and powers given to Magistrate under code of Criminal Procedure 1973 , will be possessed by Principal Commissioner of CGST/SGST.

• PowertoarrestIf the commissioner has the reason to believe that any person has committed an offence he may authorize any officer to arrest such person.

• PowertosummonpersonsProper officer shall have the power to summon (call) any person who he considers necessary either to give evidence or to produce any document which will be useful during the inquiry proceedings.

• Access to business premises• Any CGST/SGST officer so authorized shall have access to any

business premises to inspect books of account documents, computers, computer program, software and such other things as he may require and which may be available at such premises, for the purpose of carrying out Audit, scrutiny, verification as may be necessary to safeguard the interest of revenue.

• On demand by the audit officer or Chartered Accountant or Cost Accountant nominated by the department, for conducting the audit furnish followings :1) Records2) Trial Balance3) Duly Audited Financial Accounts4) Cost Audit Report5) Tax Audit Report6) Any other relevant records

• The person should produce the records related to GST, trial balance, audited financial reports etc within 15 days from the date of demand.

| 43 |GST - Mitra

10. Specific Concepts

1. LevyofTax

(i) Imposition(Levy)oftax (Sec.7ofCGSTAct.)

• Levy of CGST, SGST/UTGST on all intra state supplies of goods / services.

• Levy of IGST on all inter state supplies of goods / services.• Central/State Government may specify categories of

supply of goods / services for payment of tax on reverse charge mechanism.

• When Electronic Commerce Operator has no physical presence - his representative in taxable territory is liable.

• Neither physical presence of Electronic Commerce Operator nor representative appointed - Electronic Commerce Operator to appoint a person for paying tax.

(ii)LevyofGSTonReverseCharge (Sec9ofCGSTAct)”

TimeofSupply• Date of Receipt of Goods• Date of Payment in Books of Account / Dt of Debit to the

Bank Account

Reverse Charge

Notified Services Sec 9(3)

Purchases from Unregistered

Dealer Sec 9(4)

| 44 | GST - Mitra

• Date immediately following 30 days from the date of issue of invoice by Supplier

• Other case booking of entry in the books of Account of the Receipt• Debit in books of Account for Service receipt – For

Associate Enterprise* No Reverse Charge for Local Purchases upto Rs 5000 per day

from One or More Unregistered Suppliers. Notification 8 CT (Rate)of 28.6.17

(iii)CompositionLevy(Sec.10ofCGSTAct.)• “Turnover” < 75 lacs in previous Financial Year.• Turnover = aggregate value of all taxable supplies, exempt

supplies, exports, of goods and/or services, on all India basis excluding GST.

• Category of Supplier Composition levy - Manufacturer 1% CGST + 1% SGST.- Persons engaged in making supplies referred to in

clause (b) of paragraph 6 of Schedule II, 2.5% CGST + 2.5% SGST.

- Others 0.5% CGST + 0.5% SGST (Excluding Service Provider)

The limit for turnover for composition levy has been proposed to be increased to Rs.75 lakhs by the GST Council. ( It can be incrased max. upto Rs. 1 Crore).

Conditionsforcompositetaxpayer Apart from the threshold Limits, the following conditions are

applicable for composite tax payers.• Cannot be engaged in supply of services• Cannot be engaged in manufacture of specified notified

goods• Cannot supply goods not taxable under GST• Cannot supply goods through an e commerce operator• Cannot be engaged in Interstate supplies (goods / services)• Does not have to collect tax on all the outward supply of

goods / services• Cannot claim Input tax credit on all inward supplies of

goods & / services.

| 45 |GST - Mitra

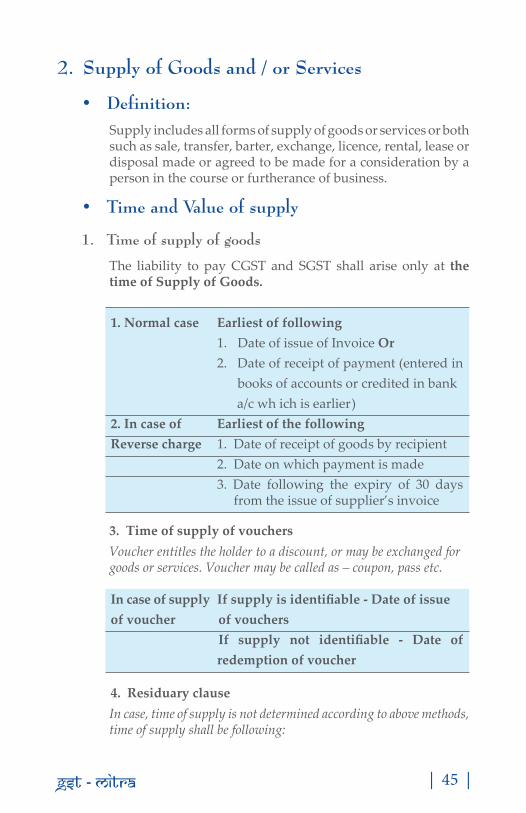

2. SupplyofGoodsand/orServices

• Definition: Supply includes all forms of supply of goods or services or both

such as sale, transfer, barter, exchange, licence, rental, lease or disposal made or agreed to be made for a consideration by a person in the course or furtherance of business.

• TimeandValueofsupply

1. Timeofsupplyofgoods

The liability to pay CGST and SGST shall arise only at the time of Supply of Goods.

1. Normal case Earliest of following 1. Date of issue of Invoice Or 2. Date of receipt of payment (entered in

books of accounts or credited in bank a/c wh ich is earlier)

2. In case of Earliest of the following Reverse charge 1. Date of receipt of goods by recipient 2. Date on which payment is made 3. Date following the expiry of 30 days

from the issue of supplier’s invoice

3. Time of supply of vouchers Voucher entitles the holder to a discount, or may be exchanged for

goods or services. Voucher may be called as – coupon, pass etc.

In case of supply Ifsupplyisidentifiable-Dateofissueof voucher of vouchers If supply not identifiable - Date of

redemption of voucher

4. Residuary clause In case, time of supply is not determined according to above methods,

time of supply shall be following:

| 46 | GST - Mitra

In residual cases Earliest of the following Date of filing of returns OR

Date of payment of tax

2. TimeofSupplyofServices

1. Normal cases Earliest of following 1. Date of Issue of Invoice (Prescribed

period is within 30 days of provision of services)

OR 2. Date of receipt of payment

Example:

Particulars Date of Date of Date of Time of Completion invoice receipt of supply of service payment i Invoice Issued July 1 July 20 Aug 10 July 20 Within Prescribed period

ii Invoice Issued July 1 July 28 July 25 July 25 within prescribed period

iii Invoice not Issued July 1 Aug 5 July 25 July 1 Within prescribed period

iv Invoice not Issued July 1 Aug 5 June 30 Jun 30 within prescribed period

2(a) In case of Earliest of the following reverse charge 1. Date on which payment is made (Debit

in books of accounts / credited in bank A/c) OR

2. Date following the expiry of 60 days from the issue of supplier’s invoice

| 47 |GST - Mitra

Example:

Particulars Date of Date of Date of 60 Days Time of Completion invoice receipt of from supply of service payment date of invoice i Invoice Issued July 1 July 20 Aug 10 Sept 20 Aug 10 Within Prescribed period

ii Invoice Issued July 1 July 28 July 25 Sept 28 July 25 Within Prescribed Period

iii Invoice not Issued July 1 Aug 5 July 25 Oct 5 July 25 Within Prescribed Period

iv Invoice not Issued July 1 Aug 5 June 30 Oct 5 Jun 30 Within Prescribed Period

2(b) In case of Earliest of the following Associated 1. Date of entry in recipients books enterprise OR

2. Date of Payment (Debit/Bank)

Example:

Particulars Date of Date of Date of Date of Time of Completion invoice receipt of entry of supply of service payment Bks of A/cs of recipient i Invoice Issued July 1 July 20 Aug 10 July27 July27 Within Prescribed period

ii Invoice Issued July 1 July 28 July 25 July27 July 25 Within Prescribed Period

iii Invoice not Issued July 1 Aug 5 July 25 July27 July 25 Within Prescribed Period

iv Invoice not Issued July 1 Aug 5 June 30 July27 Jun 30 Within Prescribed Period

| 48 | GST - Mitra

Before Change After Change Time of Supply

Service provided Invoice + payment receipt

Earliest of the follwing namely:1. Date of invoice2. Date of payment receipt

Service provided + invoice

Payment Date of invoice

Service provided +payment

Invoice Date of payment receipt

o 3.Timeofsupplyofvouchers

Incaseofsupply Ifsupplyisidentifiable- Date of issue of vouchers of voucher Ifsupplynotidentifiable-Date of

redemption of voucher

4.ResiduaryClause

In case, time of supply is not determined according to above methods, time of supply shall be following:

In residual cases Earliest of the following - Date of filing of returns Or

Date of payment of tax

5.ChangeinrateofTAX

Situation 1: Provision for taxable services prior to change in effective rate of tax (Good or services)

Ex: Services provided before change in rate of tax w.e.f 01.7.2017 (old rate 15%& new rate 18%)

| 49 |GST - Mitra

Cases Date of Date of Date of Time of Rate of Providing Invoice Payment supply Tax Service

CASE 1 12/05/2017 12/5/2017 15/7/2017 12/5/2017 15%

CASE 2 10/6/2017 15/6/2017 18/7/2017 15/6/2017 15%

CASE 3 21/6/2017 21/7/2017 12/6/2017 12/6/2017 15%

Situation 2 : Provision for taxable services after change in effective rate of tax

Ex: Services provided after the change in rate of tax

Cases Date of Date of Date of Time of Rate of Providing Invoice Payment supply Tax Service

CASE 1 20/7/17 12/6/17 26/7/17 26/7/17 18%

CASE 2 26/7/17 8/6/17 11/6/17 8/6/17 15%

CASE 3 28/7/17 28/7/17 12/6/17 28/7/17 18%

3. Valueoftaxablesupplyofgoodsand/orservices Ex. Super Cars Ltd, a car manufacturer sells spare parts to

R Ravindra Automobiles for Rs.6000/-. MRP of the spare parts is Rs.10, 000/- The invoice issued To Ravindra Automobiles is given below:

Before Change After Change Time of Supply

Invoice Service provided + payment

Date of paymentreceipt

Invoice + payment Service ProvidedEarliest of the following namely:1 . Date of invoice2 . Date of payment receipt

Payment Service Provided + Invoice

Date of Invoice

| 50 | GST - Mitra

In the GST Regime, The value of goods & / services is the transaction value i e the price paid/ payable which is Rs.6000, in the above example. Where the supplier (Super Cars) and recipient (Ravindra automobiles) are not related and the price is the sole consideration for supply.

• Effectofvariouscharges/expensesofsupplyon transaction value is as below

Charges/expensesrelated Effectontransactionvalue to supply Incidental expenses ex. Included in transaction value Commission, packing Interest / late fees / penalty charged Included in transaction ValueSubsidies excluding those Included in transaction Value provided By CG/SG Any tax other than GST Included in transaction valueAny amount payable by supplier Included in transaction value but incurred by receiver

GST Regime

Super Cars Limited Spare Parts Ravindra Automobiles

Invoice

Spare Parts

7,080

GST @ 18%

Total

1 1

1

6,000 No 6,000

S.No. Descriptionof goods

Quantity Rate Per Amount

MRP = Rs. 10,000Selling Price = Rs. 6,000

1,080

On Spare parts, GST is charged on the price payable, i.e.Rs. 6,000. On this value, GST @18% (Assuming GST of 18% on spare parts) is charged.

| 51 |GST - Mitra

• Asummaryoftheeffectofdiscountontransactionvalueis

Givenbelow:

Typeofdiscount Effectontransactionvalue

If the discount is given before or Can be claimed as deduction at the Time of supply and is from the transaction value recorded in the invoice

If the discount is given after Can be claimed as deduction supply, but agreed upon before from the transaction value or at the time of Supply

If the discount is given after Cannot be claimed as Deduction supply, and not known at the from the transaction value time of supply

3. JobworkProcedures

• Definition: Undertaking any treatment or process by a person (Job

worker) on goods belonging to another Registered taxable person (Principal)

• Normalprovisions

Case 1: To avail the input tax credit

• A principal (registered taxable person) may send inputs and/or capital goods without the payment of Tax to a job worker for job work and from there subsequently send to another Job work for further processing and bring back the goods after the completion of job work within one year and /or three years, respectively to any of his place of business without the payment of tax.

• Supply (sell) such inputs after completion of job work within one year and/or three years respectively from the place of business on payment of tax within India or with or without payment of tax for export as the case may be.

| 52 | GST - Mitra

Case 2: Cannot avail input tax credit

• Where the inputs and/ or capital goods sent to a job work are not received back by the principal after the completion of Job work or are not supplied from the place of Business within a period of one year / three years of their being sent out it shall be deemed that such input and / or capital goods had seen supplied by the principal to the job worker on the day when the said inputs / capital goods were sent out

• Jobwork-transitionalProvisions Case 1: In case, inputs/ semi finished / finished goods

received in the factory are removed to a job work premises for further processing prior to the appointed day, no tax shall be payable if in case goods are returned to the said factory premises within 6 months from the appointed day.

Case 2 : If in case, inputs /semi finished good/ finished goods received in factory are removed to a job work premises for further processing prior the appointed day, are not returned within the period of 6 months the input tax credit shall be liable tobe recovered. (ITC reversal). In case thefinishedgoods are sold directly from job work premises to the customer it would be liable to GST.

4. InputTaxCredit

• Definitions:• Input Tax is the tax charged on any supply of goods or services

or both made to the recipient• Input Tax Credit is the credit to be taken for tax paid on inputs.• Input Service: Any service used or intended to be used by

supplier in the course of business.• Output Tax means the tax chargeable on the taxable supply of

goods and/ or services made by Supplier or his agent. The output tax excludes the tax payable on reverse charge basis.

• Capital goods: Goods the value of which is capitalized in the books of accounts of the person claiming the credit and which are used in the course of business.

| 53 |GST - Mitra

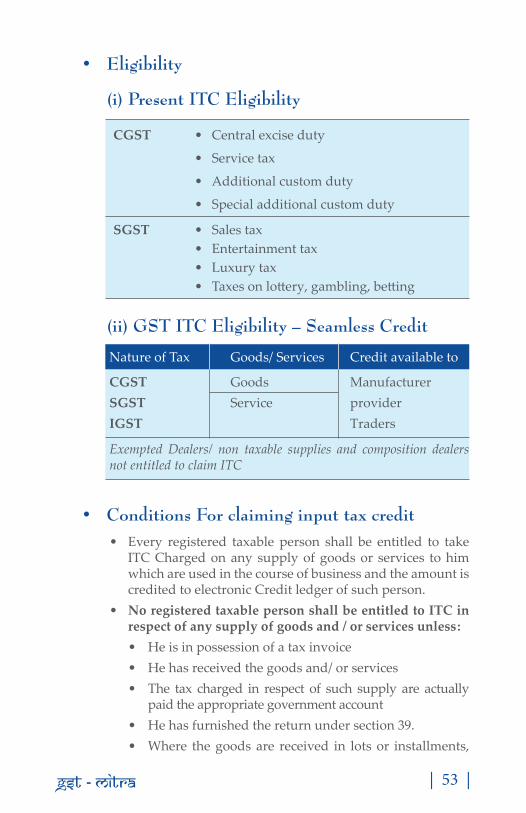

• Eligibility

(i)PresentITCEligibility

CGST • Central excise duty

• Service tax

• Additional custom duty

• Special additional custom duty

SGST • Sales tax • Entertainment tax • Luxury tax

• Taxes on lottery, gambling, betting

(ii)GSTITCEligibility–SeamlessCredit

Nature of Tax Goods/ Services Credit available to

CGST Goods ManufacturerSGST Service providerIGST Traders

Exempted Dealers/ non taxable supplies and composition dealers not entitled to claim ITC

• ConditionsForclaiminginputtaxcredit• Every registered taxable person shall be entitled to take

ITC Charged on any supply of goods or services to him which are used in the course of business and the amount is credited to electronic Credit ledger of such person.

• No registered taxable person shall be entitled to ITC in respect of any supply of goods and / or services unless:• He is in possession of a tax invoice• He has received the goods and/ or services• The tax charged in respect of such supply are actually

paid the appropriate government account• He has furnished the return under section 39.• Where the goods are received in lots or installments,

| 54 | GST - Mitra

taxable person shall be entitled to take credit upon receipt of last lot or installment.

• Where the recipient fails to pay to the supplier of services, the amount towards the value of supply of services along with tax payable within a period of 180 days from the date of issue of invoice by the supplier, then input tax credit availed by the recipient shall be added to his output tax liability along with interest.

• In case, Depreciation has been claimed on the capital goods, then ITC shall not be allowed on the said tax component. A registered person shall not be entitled to take input tax credit in respect of any invoice or debit note for supply of goods or services or both after the due date of furnishing of the return under section 39 for the month of September following the end of financial year to which such invoice or invoice relating to such debit note pertains or furnishing of the relevant annual return, whichever is earlier.

• SituationswhereITC(Inputtaxcredit)isnotavailable:NegativeListITC will not be available in respect of the following:• Motor vehicles and other conveyances except when they

are used–(i) For making the following taxable supplies, namely:—

(a) Further supply of such vehicles or conveyances ; or(b) Transportation of passengers; or(c) Imparting training on driving, flying, navigating such

vehicles or conveyances;(ii) For transportation of goods;• Food and beverages, outdoor catering, beauty treatment,

health services, cosmetic and plastic surgery except where an inward supply of goods or services or both of a particular category is used by a registered person for making an outward taxable supply of the same category of goods or services

• Membership of a club, health and fitness centre;• Rent-a-cab, life insurance and health insurance except

where – the Government notifies the services which are

| 55 |GST - Mitra

obligatory for an employer to provide to its employees under any law for the time being in force; or

• Travel benefits extended to employees on vacation such as leave or home travel concession;

• Works contract services when supplied for construction of an immovable property (other than plant and machinery) except where it is an input service for further supply of works contract service;

• Goods/services received by a person for construction of immovable property on his own account,other than P&M, even when used in course or furtherance of business.

The expression “construction” includes re-construction, renovation, additions or alterations or repairs, to the extent of capitalisation, to the said immovable property;

The expression “plant and machinery” means apparatus, equipment, and machinery fixed to earth by foundation or structural support that are used for making outward supply of goods or services or both and includes such foundation and structural supports but excludes—(i) land, building or any other civil structures;(ii) telecommunication towers; and(iii) pipelines laid outside the factory premises.

• Goods /services on which tax has been paid under composition schemes

• Goods or services or both used for personal consumption;• Goods lost, stolen, destroyed, written off or disposed of by

way of gift or free samples; and• Taxes paid under sections 74, 129 and 130 (fraud/seizure/

detention)

| 56 | GST - Mitra

• ApportionmentofCredit

Situations Effect on ITC

When the goods and / or services The amount of input tax credit are used by Registered Taxable shall be restricted to the taxperson partly for business and attributable to the purpose ofpartly for other purposes business, not for other Purposes.

In case the goods and /or services The amount of credit shall be are used partly for taxable restricted to the input taxsupplies (including zero rated attributable to taxable suppliessupplies) and partly for exempt including zero rated supplies supplies only

In case of banking company or An amount equal to 50% of the a financial institution eligible credit on inputs, capital goods and input services in that month. This option once exercised cannot be withdrawn during the remaining part of the year.

| 57 |GST - Mitra

• AvailabilityofCredit

Situations Effect on ITC

In case the person applied for He is entitled to take ITC inregistration within 30 days from respect of inputs held in stock,the date he becomes liable inputs contained in semi finishedfor registration, and registration goods, finished goods held inis granted stock on the date immediately preceding the date from which he becomes liable to pay tax.

If any of these below cases, Will be entitled to take ITC in • Voluntary registration respect of inputs held in stock,• Ceases to pay tax under and inputs contained in semi composition scheme finished or finished goods held • Exempt supply of goods or in stock on the day immediately services becomes a taxable preceding the date of grant supply of registration / date from which he becomes liable to pay/ date from which supply becomes taxable.

In case there is change in the The registered taxable person constitution on account of Sale shall be allowed to transfer theMerger, Demerger, ITC that remains unutilized inAmalgamation, Lease or transfer the books of accounts to of business such sold, merged demerged, amalgamated, leased or transferred business as the case may be

A taxable person shall not be entitled to take input tax credit in respect of goods and / or services after the expiry of one year from the date of issue of tax invoice relating to such supply.

| 58 | GST - Mitra

5.InputServiceDistributor-ISD

• Definition: An office of the supplier of goods/ services which receives tax

invoices towards receipt of input service and issues tax invoice or other prescribed document for the purpose of distributing the credit of CGST/SGST/UTGST paid on said services to a supplier of taxable goods/ services having the same PAN.

• ElementsofISD• It must be an office of a supplier.• ISD must be registered and having same PAN as of other

places of business.• It distributes credits of GST paid on services received among

the other place of business and establishment of the supplier.

• DistributionOfcredit

Distribution Of Credit

Location of ISD Credit of Credit of Credit of and recipient CGST SGST IGST of credit Indifferent state IGST IGST IGST In same state CGST SGST CGST SGST

• Conditionsfordistributionofcredit• Against the prescribed documents issued to each of the

recipient and such documents contains the details as prescribed.

• Credit distributed shall not exceed the amount of credit available for distribution.

• Credit of tax paid paid on input service attributable to recipient to be distributed to that recipient only.

• Credit of tax paid on input services attributable to more than one recipient to be distributed only amongst such recipients to whom the input service attributable pro rata on the basis of turnover in state of such recipient during

| 59 |GST - Mitra

relevant period to the total of the turnover of all such recipients and which are operational in the current year, during the said relevant period.

• Credit of tax paid on input services attributable to all recipients of credit shall be distributed amongst such recipients and such distribution shall be pro rata on the basis of the turnover in a State or turnover in a Union territory of such recipient, during the relevant period, to the aggregate of the turnover of all recipients and which are operational in the current year, during the said relevant period.

Relevant period shall be :• If the recipients of credit have turnover in their States in

the financial year preceding year during which credit is to be distributed, the said financial year; or

• If some or all recipient of credit do not have turnover in their states in the financial year preceding year during which credit is to be distributed, the last quarter for which details of the turnover of all the recipients are available, previous to the month during which credit is to be distributed,

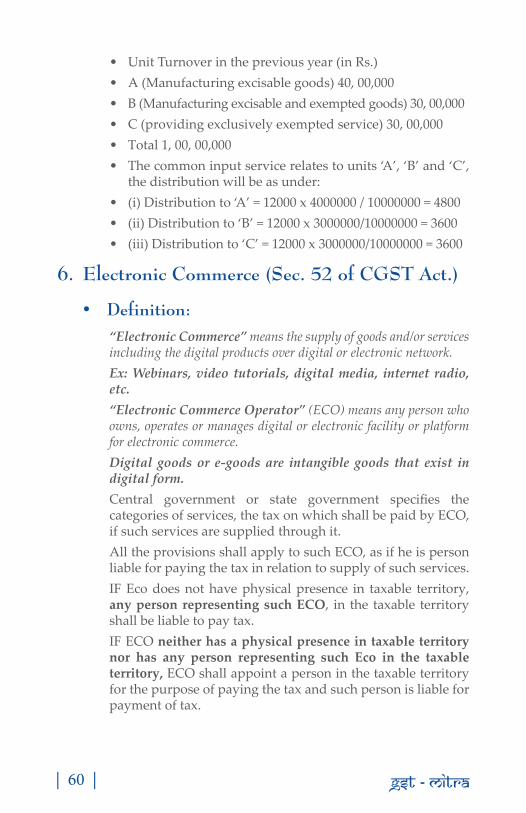

• PracticalIllustrationrelatedtodistributionofCreditbyISD• Input Service Distributor (ISD) has a total of 4 units namely

‘A’, ‘B’, ‘C’, and ‘D’ which are operational in the current year. The credit of input service pertaining to more than one unit shall be distributed as follows:

• Distribution to ‘A’ = Ta/Ts * Tc• Ta = Turnover of unit ‘A’ during the relevant period• Ts = Total turnover of all its unit i.e. ‘A’+’B’+’C’ during the

relevant period• Tc = Total credit of service tax attributable to services used

by more than one unit• Similarly the credit shall be distributed to the other units

‘B’, ‘C’ and ‘D’.• Illustration:• An ISD has a common input service credit of Rs. 12000

pertaining to more than one unit. The ISD has 3 units namely ‘A’, ‘B’, and ‘C’ which are operational in the current year.

| 60 | GST - Mitra

• Unit Turnover in the previous year (in Rs.)• A (Manufacturing excisable goods) 40, 00,000• B (Manufacturing excisable and exempted goods) 30, 00,000• C (providing exclusively exempted service) 30, 00,000• Total 1, 00, 00,000• The common input service relates to units ‘A’, ‘B’ and ‘C’,

the distribution will be as under:• (i) Distribution to ‘A’ = 12000 x 4000000 / 10000000 = 4800• (ii) Distribution to ‘B’ = 12000 x 3000000/10000000 = 3600• (iii) Distribution to ‘C’ = 12000 x 3000000/10000000 = 3600

6. ElectronicCommerce(Sec.52ofCGSTAct.)

• Definition: “Electronic Commerce” means the supply of goods and/or services

including the digital products over digital or electronic network. Ex: Webinars, video tutorials, digital media, internet radio,

etc. “Electronic Commerce Operator” (ECO) means any person who

owns, operates or manages digital or electronic facility or platform for electronic commerce.

Digital goods or e-goods are intangible goods that exist in digital form.

Central government or state government specifies the categories of services, the tax on which shall be paid by ECO, if such services are supplied through it.

All the provisions shall apply to such ECO, as if he is person liable for paying the tax in relation to supply of such services.

IF Eco does not have physical presence in taxable territory, any person representing such ECO, in the taxable territory shall be liable to pay tax.

IF ECO neither has a physical presence in taxable territory nor has any person representing such Eco in the taxable territory, ECO shall appoint a person in the taxable territory for the purpose of paying the tax and such person is liable for payment of tax.

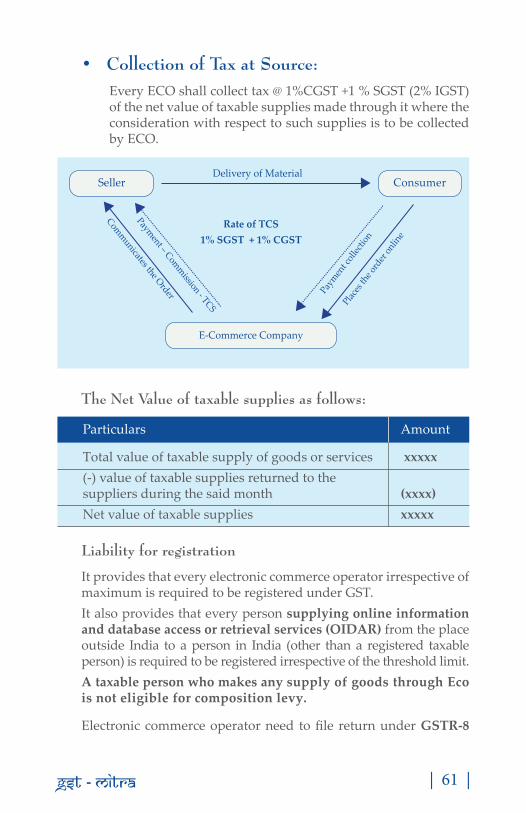

| 61 |GST - Mitra

• Collection of Tax at Source: Every ECO shall collect tax @ 1%CGST +1 % SGST (2% IGST)

of the net value of taxable supplies made through it where the consideration with respect to such supplies is to be collected by ECO.

TheNetValueoftaxablesuppliesasfollows:

Particulars Amount

Total value of taxable supply of goods or services xxxxx (-) value of taxable supplies returned to the suppliers during the said month (xxxx) Net value of taxable supplies xxxxx

Liabilityforregistration

It provides that every electronic commerce operator irrespective of maximum is required to be registered under GST.

It also provides that every person supplying online information and database access or retrieval services (OIDAR) from the place outside India to a person in India (other than a registered taxable person) is required to be registered irrespective of the threshold limit.

A taxable person who makes any supply of goods through Eco is not eligible for composition levy.

Electronic commerce operator need to file return under GSTR-8

SellerDelivery of Material

E-Commerce Company

Rate of TCS1% SGST + 1% CGST

Consumer

Payment – Commission - TCS