GST and Textiles Sector - taxguru.in · GST and Textiles Sector Page 3 of 35 PRESENT INDIRECT TAXES...

35

GST and Textiles Sector Page 1 of 35 A compilation by: B. Venkateswaran , IRS Asst. Director DG Systems Chennai GST and Textile Sector Download Source- www.taxguru.in

Transcript of GST and Textiles Sector - taxguru.in · GST and Textiles Sector Page 3 of 35 PRESENT INDIRECT TAXES...

GST and Textiles Sector

Page 1 of 35

A compilation by:

B. Venkateswaran , IRS

Asst. Director DG Systems Chennai

GST and Textile Sector

Download Source- www.taxguru.in

GST and Textiles Sector

Page 2 of 35

INDEX

1. Present Indirect Taxes

2. Goods and Services Tax

3. Registration

4. Rate Of GST

5. Valuation

6. Input Tax Credit

7. Refund

8. Job Work & Textile Sector

9. Export Of Textile Products

10. Duty Drawback

11. Annexure I

12. Annexure II (CGST, SGST and IGST Rate For Textile Sector)

13. Annexure III (GST, SGST and IGT Rates for some inputs and capital

goods)

Download Source- www.taxguru.in

GST and Textiles Sector

Page 3 of 35

PRESENT INDIRECT TAXES

The textile industry has historically enjoyed tax exemptions on the cotton value

chain. Currently, attracts zero Central excise duty (under optional route).VAT is

not applicable on fabrics, but yarn and garments attract VAT according to state

rates. On an average, the items used by the textile industry such as machinery

and chemical agents have been taxed at around 20% throughout the country.

After GST, the average tax rate will be lowered to around 18%.

Central Excise duty

Central excise duty was first introduced on woven garments in year 2001 which

was subsequently extended to entire textile industry by 2003. The excise duty

exemption option was also provided vide notification no.30/2004 with condition

of non-availment of Cenvat credit. There was also an option to pay concessional

rate of excise duty with Cenvat credit benefit. However, almost all assesses opted

for exemption.

In 2011, mandatory excise duty was reintroduced on branded garments with

Cenvat credit benefit and abatement of 55% for duty payment. This mandatory

levy was again removed in 2013 and optional scheme of paying duty with Cenvat

credit benefit was continued.

In 2016, mandatory excise duty has been introduced again on branded

readymade garments made up of textiles falling under Central excise tariff

heading 61, 62 and 63. The levy is attracted only when retail sale rice (RSP) is

Rs.1000/- or more and levy is only on 60% value after standard abatement of 40%.

For payment of duty, rate of 2% without Cenvat credit or 12.5% with Cenvat credit

option is applicable. Non-branded goods continue with “Nil” levy without Cenvat

credit benefit. Otherwise, option of paying 6% with Cenvat credit in case of

garments / articles of cotton, not containing any other textile material is available.

For garments of other composition, “Nil” rate without Cenvat credit or 12.5% with

Cenvat credit is available.

VAT / Sales tax

Most of the states in India have exempted textiles and fabrics from levy of VAT /

Sales tax. Garments including textiles are being subject to lower rate of VAT / Sales

Download Source- www.taxguru.in

GST and Textiles Sector

Page 4 of 35

tax in many states. For small players, the option of paying taxes at concessional

rates is also provided under composition scheme in many states.

Entry tax

Entry tax is levied on specified goods when goods enter local area, many states.

Even textiles such as cotton, woolen or silk or artificial silks are liable to entry tax in

states like Karnataka at the rate of 1% which is adding to purchase cost.

Download Source- www.taxguru.in

GST and Textiles Sector

Page 5 of 35

GOODS AND SERVICES TAX

In GST regime, most of the indirect taxes such as Central excise duty, service tax,

and VAT / Sales tax and entry tax were subsumed and seamless input tax credit is

allowed for the entire supply chain.

The major taxes/levies which were subsumed in the GST regime are:

CENTRE TAXES

― Central Excise duty

― Additional duties of Excise

― Excise duty levied under Medicinal & Toilets Preparation Act

― Additional duties of customs (CVD & SAD)

― Service Tax

― Surcharges & Cesses

STATE TAXES

― State VAT/Sales Tax

― Central Sales Tax

― Purchase Tax

― Entertainment Tax (other than those levied by local bodies)

― Luxury Tax

― Entry Tax (All forms)

― Taxes on lottery, betting & gambling

― Surcharges & Cesses

GST comprises of the following levies:

a. Central Goods and Services Tax (CGST) [also known as Central Tax] on intra-

state or intra-union territory of goods or services or both.

b. State Goods and Services Tax (SGST) [also known as State Tax] on intra-state

supply of goods or services or both.

c. Union Territory Goods and Services Tax (UTGST) [also known as Union territory

Tax] on intra-union territory supply of goods or services or both.

d. Integrated Goods and Services Tax (IGST) [also known as Integrated Tax]

on inter-state supply of goods or services or both. In case of import of goods

also, the present levy of Countervailing Duty (CVD) and Special Additional

Duty (SAD) were replaced by integrated tax.

Download Source- www.taxguru.in

GST and Textiles Sector

Page 6 of 35

The taxable event in GST:

The taxable event in GST is supply of goods or services or both. Various taxable

events like manufacture, sale, rendering of service, purchase, entry into a territory

of state etc. have been done away with in favour of just one event i.e. supply.

The constitution defines “Goods and Services Tax” as any tax on supply of goods,

or services or both, except for taxes on the supply of the alcoholic liquor for

human consumption.

Supply of Goods or Services or Both Goods as well as services have been defined

in the CGST, Act, 2017.

(52) “goods” means every kind of movable property other than money and

securities but includes actionable claim, growing crops, grass and things

attached to or forming part of the land which are agreed to be severed before

supply or under a contract of supply;

(102) “services” means anything other than goods, money and securities but

includes activities relating to the use of money or its conversion by cash or by

any other mode, from one form, currency or denomination, to another form,

currency or denomination for which a separate consideration is charged;

Schedule II to the CGST Act, 2017 lists a few activities which are to be treated as

supply of goods or supply of services.

For example, any transfer of title in goods would be a supply of goods, whereas

any transfer of right in goods without transfer of title would be considered as

services. Also any treatment or process which is applied to another person's goods

is a supply of services.

Further Schedule III to the CGST Act, 2017 spells out activities which shall be

treated as neither supply of goods nor supply of services or outside the scope of

GST.

Under the above legal provisions the impact of GST on Textile Sector is

summarized as under.

The textile sector consisting of the following major sub-sectors.

Download Source- www.taxguru.in

GST and Textiles Sector

Page 7 of 35

1. Fibres to Yarn

2. Fabric and

3. Garments

Various supply chains in Textile Sector

1. Fibres- Cotton to Yarn

Sl No Supply type Levy of GST

1 Unprocessed Cotton supplied to Ginning mill GST Exempted

2 Ginning Mill to Spinning Mill- GST Exempted

3 Spinning Mill to yarn trader/ Weavers etc., Attract GST as supply of

Goods

4 Spinning Mill to Job work ( Cop stage to Reeling,

Cone winding, Doubling Etc.,)

Attract GST as supply of

Service

2.Yarn to Grey /Processed Fabric (Woven/Knitted etc.,)

Sl No Supply type Levy of GST

1 Yarn from Weavers/ Mills to Sizing Mill

on Job work basis

Attract GST as supply of Service

2 Yarn Weavers/ Mills on to Weaving /

Knitting on Job work basis

Attract GST as supply of Service

3 Sale of gray fabric to

Manufacturers/Trader

Attract GST as supply of Good

Download Source- www.taxguru.in

GST and Textiles Sector

Page 8 of 35

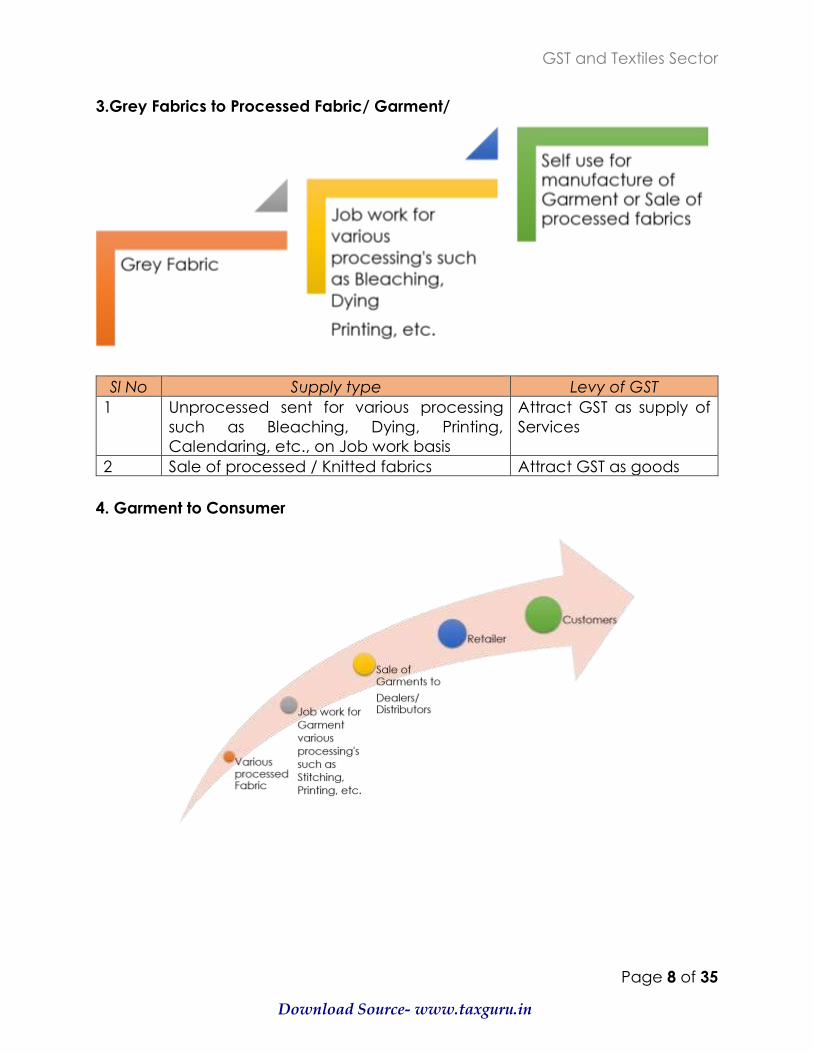

3.Grey Fabrics to Processed Fabric/ Garment/

Sl No Supply type Levy of GST

1 Unprocessed sent for various processing

such as Bleaching, Dying, Printing,

Calendaring, etc., on Job work basis

Attract GST as supply of

Services

2 Sale of processed / Knitted fabrics Attract GST as goods

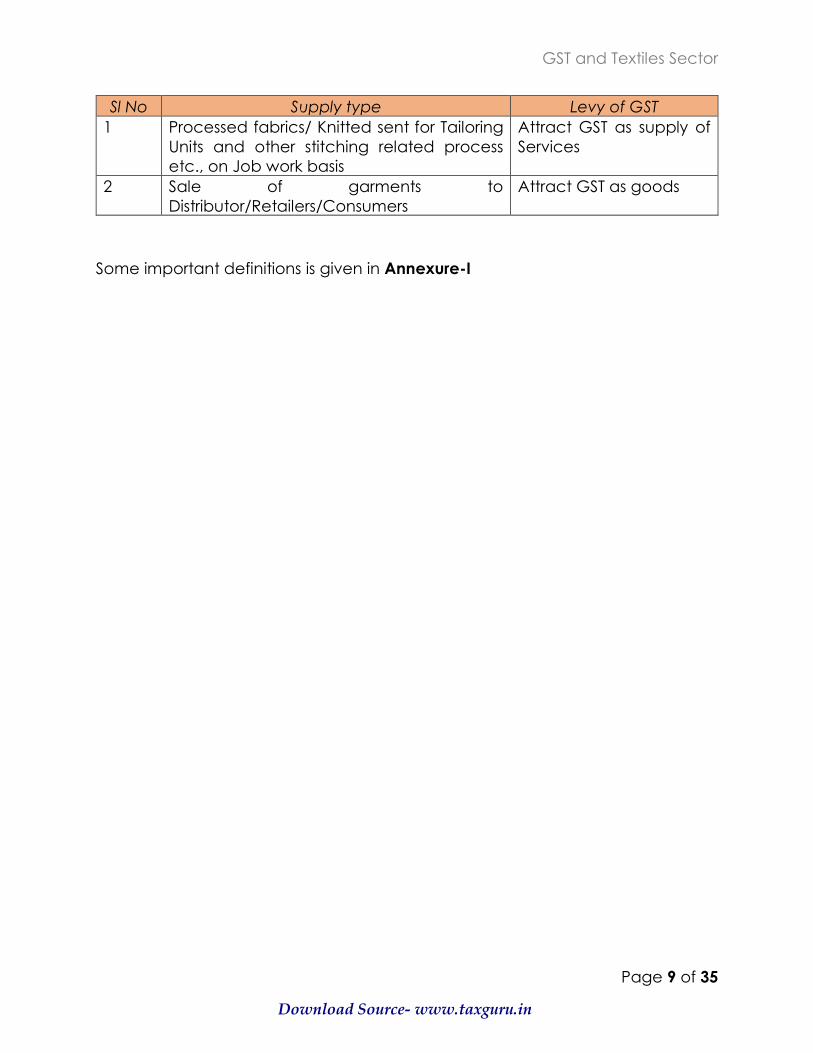

4. Garment to Consumer

Download Source- www.taxguru.in

GST and Textiles Sector

Page 9 of 35

Sl No Supply type Levy of GST

1 Processed fabrics/ Knitted sent for Tailoring

Units and other stitching related process

etc., on Job work basis

Attract GST as supply of

Services

2 Sale of garments to

Distributor/Retailers/Consumers

Attract GST as goods

Some important definitions is given in Annexure-I

Download Source- www.taxguru.in

GST and Textiles Sector

Page 10 of 35

REGISTRATION

GST being a tax on the event of “supply”, every supplier needs to get registered.

However, small businesses having all India aggregate turnover below Rupees 20

lakh (10 lakh if business is in Assam, Arunachal Pradesh, J&K, Himachal Pradesh,

Uttarakhand, Manipur, Mizoram, Sikkim, Meghalaya, Nagaland or Tripura) need

not register. The small businesses, having turnover below the threshold limit can,

however, voluntarily opt to register.

The aggregate turnover includes supplies made by him on behalf of his principals,

but excludes the value of job-worked goods if he is a job worker. But persons who

are engaged exclusively in the business of supplying goods or services or both

that are not liable to tax or wholly exempt from tax or an agriculturist, to the extent

of supply of produce out of cultivation of land are not liable to register under GST.

It should be noted that GST in India is State-centric. Hence, a person making

supplies from different States needs to take separate registration in each State.

Further, the person may take more than one registration within a State if the

person has multiple business verticals. A person who has obtained or is required

to obtain more than one registration, whether in one State or Union territory or

more than one State or Union territory shall, in respect of each such registration,

be treated as distinct persons for the purposes of GST. Hence, a supply between

these entities constitutes supply under GST.

The supply chain in the Textile Sector is as under:

Download Source- www.taxguru.in

GST and Textiles Sector

Page 11 of 35

Supply through Branch Transfer under GST

A Branch in common sense is a location, other than the main office, where

business is conducted. In VAT Regime, Branch Transfer against F Form. No such

form in GST Regime and the supply is regulated under the concept concept of

Distinct Person

As per Schedule I – Branch Transfer even if without consideration to be treated as

Supply of goods or services or both between related persons or between distinct

persons as specified in section 25, when made in the course or furtherance of

business:

As per Section 25(4) A person who has obtained or is required to obtain more than

one registration, whether in one State or Union territory or more than one State or

Union territory shall, in respect of each such registration, be treated as distinct

persons for the purposes of this Act.

Supply of goods made through an agent

As per Schedule I supply of goods to Agent without consideration is treated as

Supply

3. Supply of goods—

(a) by a principal to his agent where the agent undertakes to supply such

goods on behalf of the principal; or

(b) by an agent to his principal where the agent undertakes to receive such

goods on behalf of the principal.

As per Section 24 persons who make taxable supply of goods or services or both

on behalf of other taxable persons whether as an agent or otherwise is required

to take registration.

In view of the above GST has to be payable for the supply though Branch and

Consignment Agent even though no consideration is received. Since one state

one registration, GST is not payable if supply to Intra-State Brach.

Download Source- www.taxguru.in

GST and Textiles Sector

Page 12 of 35

RATE OF GST

After GST, the average tax rate for Textile Sector is around 5 %. Minimum is Zero

and maximum rate is 18%. The rates for various chapter is given in the Annexure-

II

Sl.No Goods / Service GST Rate

1 Cotton yarn, cotton fabrics, Knitted or

crocheted fabrics

5% (2.5%+2.5%)

2 Articles of apparel and clothing accessories,

knitted or crocheted, of sale value not

exceeding Rs. 1000 per piece

5% (2.5%+2.5%)

3 Articles of apparel and clothing accessories,

knitted or crocheted, of sale value exceeding

Rs. 1000 per piece

12% (6 %+6%)

4 Yarn of manmade staple fibres 18% (9%+9%)

5 Job work 5% (2.5%+2.5%)

Composition levy under GST

The composition levy is an alternative method of levy of tax designed for

small taxpayers whose turnover is up to Rs. 75 lakhs ( Rs. 50 lakhs in case of

few States) The objective of composition scheme is to bring simplicity and

to reduce the compliance cost for the small taxpayers. Moreover, it is optional

and the eligible person opting to pay tax under this scheme can pay tax at a

prescribed percentage of his turnover every quarter, instead of paying tax at

normal rate.

S. No. Category of Registered person Rate of Tax

1 Manufacturers, other than manufacturers of

such goods as may be notified by the

Government (Ice cream, Pan Masala,

Tobacco products etc.)

2% ( 1% Central tax Plus 1% State

tax) of the turnover

2 Restaurant Services 5% ( 2.5% Central tax plus 2.5%

SGST) of the turnover

3 Traders or any other supplier eligible for

composition levy

1% ( 0.5% Central tax plus 0.50%

State tax ) of the turnover

Download Source- www.taxguru.in

GST and Textiles Sector

Page 13 of 35

VALUATION

Under GST law, taxable value is the transaction value i.e. price actually paid or

payable, provided the supplier & the recipient are not related and price is the

sole consideration. In most of the cases of regular normal trade, the invoice value

will be the taxable value. However, to determine value of certain specific

transactions, Determination of Value of Supply rules have been prescribed in

CGST Rules, 2017.

Compulsory Inclusions

Any taxes, fees, charges levied under any law other than GST law, expenses

incurred by the recipient on behalf of the supplier, incidental expenses like

commission & packing incurred by the supplier, interest or late fees or penalty for

delayed payment and direct subsidies (except government subsidies) are

required to be added to the price (if not already added) to arrive at the taxable

value.

Exclusion of discounts

Discounts like trade discount, quantity discount etc. are part of the normal trade

and commerce. Therefore, pre-supply discounts i.e. discounts recorded in the

invoice have been allowed to be excluded while determining the taxable value.

Discounts provided after the supply can also be excluded while determining the

taxable value, provided two conditions are met, namely:

(a) Discount is established in terms of a pre supply agreement between the

supplier & the recipient and such discount is linked to relevant invoices

(b) Input tax credit attributable to the discounts is reversed by the recipient

Download Source- www.taxguru.in

GST and Textiles Sector

Page 14 of 35

INPUT TAX CREDIT

Input tax credit on inputs and input services and Capital goods are provided for

the complete supply chain. It is to be noted that materials such as chemicals,

dyes, accessories and packing materials which constitutes major material cost is

eligible as input tax credit when output GST is paid. The availability of seamless

credit could also result in lower price of goods which could boost demand for

Textile Sector. The rates for certain Inputs and Capital goods is Given in Annexure

III

Some of the technical aspects of the scheme of Input Tax Credit are as under:

A. Any registered person can avail credit of tax paid on the inward supply

of goods or services or both, which is used or intended to be used in the

course or furtherance of business.

B. The pre-requisites for availing credit by registered person are:

i. He is in possession of tax invoice or any other specified tax

paying document.

ii. He has received the goods or services. “Bill to ship” scenarios

also included.

iii. Tax is actually paid by the supplier.

iv. He has furnished the return.

v. If the inputs are received in lots, he will be eligible to avail the

credit only when the last lot of the inputs is received.

vi. He should pay the supplier, the value of the goods or services

along with the tax within 180 days from the date of issue of

invoice, failing which the amount of credit availed by the

recipient would be added to his output tax liability, with interest

[rule 2(1) & (2) of ITC Rules]. However, once the amount is paid,

the recipient will be entitled to avail the credit again. Incase

part payment has been made, proportionate credit would be

allowed.

C. Documents on the basis of which credit can be availed are:

i. Invoice issued by a supplier of goods or services or both

ii. Invoice issued by recipient along with proof of payment of

tax

iii. A debit note issued by supplier

Download Source- www.taxguru.in

GST and Textiles Sector

Page 15 of 35

iv. Bill of entry or similar document prescribed under Customs Act

v. Revised invoice

vi. Document issued by Input Service Distributor

D. The Input Service Distributor (ISD) may distribute the credit available for

distribution in the same month in which, it is availed. The credit of CGST,

SGST, UTGST and IGST shall be distributed as per the provisions of Rule 4(1)

(d) of ITC Rules. ISD shall issue invoice in accordance with the provisions

made under Rule 9(1) of Invoice Rules.

E. ITC is not available in some cases as mentioned in section17 (5) of CGST

Act, 2017. Some of them are as follows:

a. motor vehicles and other conveyances except under specified

circumstances.

b. goods and/or services provided in relation to:

i. Food and beverages, outdoor catering, beauty treatment,

health services, cosmetic and plastic surgery, except under

specified circumstances;

ii. Membership of a club, health and fitness center;

iii. Rent-a-cab, life insurance, health insurance except where it is

obligatory for an employer under any law;

iv. Travel benefits extended to employees on vacation such as

leave or home travel concession

How is Input Tax Credit Used?

ITC on account of CGST

It should first be used to pay CGST.

Then, any remaining amount should be used to pay IGST.

Note that you cannot use ITC of CGST to pay SGST.

ITC on account of SGST

It should be used to pay SGST first.

Then, any remaining amount should be used to pay IGST.

Note that you cannot use ITC of SGST to pay CGST.

ITC on account of IGST

It should be used to pay IGST first.

Then, any remaining amount should be used to pay CGST.

The last priority should be given to payment of SGST.

Download Source- www.taxguru.in

GST and Textiles Sector

Page 16 of 35

REFUND

The provisions pertaining to refund contained in the GST law aim to streamline and

standardize the refund procedures under GST regime. Thus, under the GST regime,

there will be a standardized form for making any claim for refunds. The claim and

sanctioning procedure will be completely online and time bound, which is a

marked departure from the existing time consuming and cumbersome

procedure.

Situations Leading to Refund Claims:

A claim for refund may arise on account of:

i. Export of goods or services

ii. Supplies to SEZs units and developers

iii. Deemed exports

iv. Refund of taxes on purchase made by UN or embassies etc.

v. Refund arising on account of judgment, decree, order or direction of the

Appellate Authority, Appellate Tribunal or any court

vi. Refund of accumulated Input Tax Credit on account of inverted duty

structure

vii. Finalisation of provisional assessment

viii. Refund of pre-deposit

ix. Excess payment due to mistake

x. Refunds to International tourists of GST paid on goods in India and carried

abroad at the time of their departure from India

xi. Refund on account of issuance of refund vouchers for taxes paid on

advances against which, goods or services have not been supplied

xii. Refund of CGST & SGST paid by treating the supply as intra- State supply

which is subsequently held as inter-State supply and vice versa

Thus, practically every situation is covered.

Payment of Wrong Tax

Under GST it might happen that the taxable person may pay integrated tax

instead of Central tax plus State Tax and vice versa because of incorrect

application of the place of supply provisions. In such cases, while making the

appropriate payment of tax, interest will not be charged and the refund claim of

the wrong tax paid earlier will be entertained without subjecting it to the provision

of unjust enrichment.

Download Source- www.taxguru.in

GST and Textiles Sector

Page 17 of 35

The refund claim, wherever due, will be directly credited to the bank account of

the applicant. The applicant need not come to the authorities to collect the

cheque or for any other issues relating to the refund claim.

Download Source- www.taxguru.in

GST and Textiles Sector

Page 18 of 35

JOB WORK & TEXTILE SECTOR

Major production process in the Textile sector is through job work only.

― Yarn to Reeling, Doubling, Yarn dying, bleaching, mercerizing etc.,

― Gray fabric to Processed fabric dying, bleaching, mercerizing, printing etc.,

― Woven /Knitted fabrics to Garment

During the excise regime certain above processes were treated as manufacture

and levy is made on the entire value including the material value.

Now in the GST, the treatment of Job-work is completely changed. As per Section

2(68) of the CGST Act, 2017 defines job-work as under:

(68) “job work” means any treatment or process undertaken by a person

on goods belonging to another registered person and the expression “job

worker” shall be construed accordingly;

As per Section 7 of the Act, supply” includes

(a) all forms of supply of goods or services or both such as sale, transfer, barter,

exchange, licence, rental, lease or disposal made or agreed to be made for a

consideration by a person in the course or furtherance of business;

(b) Import of services for a consideration whether or not in the course or

furtherance of business;

(c) The activities specified in Schedule I, made or agreed to be made

without a consideration; and

(d) The activities to be treated as supply of goods or supply of services

as referred to in Schedule II.

As per Schedule II of CGST Act, 2017, Treatment or process any treatment or

process which is applied to another person's goods is a supply of services. The

ownership of the goods does not transfer to the job-worker but it rests with the

principal. Thus Job work is a service.

In view of the above facts the “job worker is required to obtain registration”, if his

aggregate turnover exceeds the prescribed threshold and follow the various

procedure as per the provisions of CGST Act, 2017 and rules made thereunder:

Download Source- www.taxguru.in

GST and Textiles Sector

Page 19 of 35

Value for the purpose of payment of GST on Job work:

As per the provisions of Section 15 of CGST Act, 2017, the value of a supply of

goods or services or both shall be the transaction value, which is the price actually

paid or payable for the said supply of goods or services or both where the supplier

and the recipient of the supply are not related and the price is the sole

consideration for the supply.

As per Explanation (ii) to Section 22, of CGST, Act, 2017 the supply of goods, after

completion of job work, by a registered job worker shall be treated as the supply

of goods by the principal referred to in section 143, and the value of such goods

shall not be included in the aggregate turnover of the registered job worker;

Explanation.––For the purposes of this section,––

(i) The expression “aggregate turnover” shall include all supplies made by the

taxable person, whether on his own account or made on behalf of all his

principals;

(ii) the supply of goods, after completion of job work, by a registered job worker

shall be treated as the supply of goods by the principal referred to in section 143,

and the value of such goods shall not be included in the aggregate turnover of

the registered job worker;

The value of goods after completion of job work is not includible in the turnover of

the job-worker. It will be treated as supply of goods by the principal and will

accordingly be includible in the turnover of the Principal.

Rate of GST for Job work:

Notification No: 11/2017 Central (Rate) dated 28/06/2017 prescribes the rate of

CGST for various services. As per this notification rate prescribed for job work for

the textile sectors is as under:

Chapter, Section or Heading Description of Service Rate of CGST

Heading 9988

(Manufacturing services on

physical inputs (goods) owned

by others)

(i) Services by way of job work in

relation to-

(b) Textile yarns (other than of

man-made fibres) and textile

fabrics;

2.5 %

Download Source- www.taxguru.in

GST and Textiles Sector

Page 20 of 35

Procedural aspects for the movement of goods from Principal to Job-worker:

In GST regime, the principal would get the option of sending inputs or capital

goods for job work. Raw materials sent to be received back within 1 year and

capital goods to be received back within 3 years. If the goods are not received

within this time limit, then supply of goods would be treated as supply for levy of

GST. The processed goods could also be sent directly to customers of principal,

provided job workers are registered or the details of job workers place are added

as additional place of business in principal’s registration certificate.

a. A registered person (Principal) can send inputs/ capital goods under

intimation and subject to certain conditions without payment of tax to a job-

worker and from there to another job-worker and after completion of job-work

bring back such goods without payment of tax. The principal is not required to

reverse the ITC availed on inputs or capital goods dispatched to job-worker.

b. Principal can send inputs or capital goods directly to the job-worker without

bringing them to his premises and can still avail the credit of tax paid on such

inputs or capital goods.

c. However, inputs and/or capital goods sent to a job-worker are required to

be returned to the principal within 1 year and 3 years, respectively, from the date

of sending such goods to the job-worker.

d. After processing of goods, the job-worker may clear the goods to-

i. Another job-worker for further processing

ii. Dispatch the goods to any of the place of business of the principal

without payment of tax

iii. Remove the goods on payment of tax within India or without

payment of tax for export outside India on fulfilment of conditions.

(e) The facility of supply of goods by the principal to the third party directly from

the premises of the job-worker on payment of tax in India and likewise with or

without payment of tax for export may be availed by the principal on declaring

premise of the job-worker as his additional place of business in registration. In case

the job-worker is a registered person under GST, even declaring the premises of

the job-worker as additional place of business is not required.

Download Source- www.taxguru.in

GST and Textiles Sector

Page 21 of 35

(f) Before supply of goods to the job-worker, the principal would be required

to intimate the Jurisdictional Officer containing the details of the description of

inputs intended to be sent by the principal and the nature of processing to be

carried out by the job-worker. The said intimation shall also contain the details of

the other job-workers, if any.

(g) The inputs or capital goods shall be sent to the job-worker under the cover

of a challan issued by the principal. The challan shall be issued even for the inputs

or capital goods sent directly to the job-worker. The challan shall contain the

details specified in Rule 10 of the Invoice Rules.

(h) The responsibility for keeping proper accounts for the inputs or capital

goods shall lie with the principal.

(i) The waste and scrap generated during the job work can be supplied by

the job worker directly from his place of business, on payment of tax, if he is

registered. If he is not registered, the same would be supplied by the principal on

payment of tax.

Download Source- www.taxguru.in

GST and Textiles Sector

Page 22 of 35

EXPORT OF TEXTILE PRODUCTS

In the GST regime, the governing provisions related to exports are contained

in section 16 of the Integrated Goods and Service Tax Act, 2017 (IGST Act).

Supplies of goods and services for exports have been categorized as 'Zero

Rated Supply' implying that goods could be exported under bond or Letter

of Undertaking without payment of integrated tax followed by claim of

refund of unutilized input tax credit or on payment of integrated tax with

provision for refund of the tax paid.

A. Procedure of Export

1. Any person making zero rated supply (i.e. any exporter) shall be eligible

to claim refund under either of the following options, namely: -

(a) he may supply goods or services or both under bond or Letter of

Undertaking, subject to such conditions, safeguards and procedure as may

be prescribed, without payment of integrated tax and claim refund of

unutilized input tax credit; or

(b) he may supply goods or services or both, subject to such conditions,

safeguards and procedure as may be prescribed, on payment of integrated

tax and claim refund of such tax paid on goods or services or both supplied,

in accordance with the provisions of section 54 (Refunds) of the Central

Goods and Services Tax Act or the rules made there under (i.e.) the Central

Goods and Service Tax Rules, 2017).

2. For the option (a) above, procedure to file refund has been outlined

in the Central Goods and Service Tax Rules, 2017. The exporter claiming

refund of unutilized input tax credit will file an application electronically

through the Common Portal, either directly or through a Facilitation Centre

notified by the GST Commissioner. The application shall be accompanied

by documents as prescribed in the said rules. Application for refund shall

be filed only after the export manifest or an export report, as the case

may be, is delivered under section 41 of the Customs Act, 1962 in respect

of such goods. The formats for furnishing bond or LUT for export of goods

have been separately notified under COST Rules, 2017.

3. For the option (b), broadly the procedure is that a registered person

shall not be required to file any application for refund of integrated goods

and services tax paid on supply of goods for exports. The shipping bill,

Download Source- www.taxguru.in

GST and Textiles Sector

Page 23 of 35

having inter-alia GST invoice details, filed by an exporter shall be deemed

to be an application for refund of integrated tax paid on the goods

exported out of India and such application shall be deemed to have been

filed only when the person in charge of the conveyance carrying the export

goods duly files an export manifest or an export report covering the number

and the date of shipping bills or bills of export and the applicant has

furnished a valid return in FORM GSTR-3. The details of the relevant export

invoices contained in FORM GSTR-1 shall be transmitted electronically by the

common portal to the Customs system and the said system shall in turn

electronically transmit back to the common portal a confirmation that the

goods covered by the said invoices have been exported out of India. Upon

receipt of information regarding furnishing of valid return in FORM GSTR-3

from the common portal, the Customs system shall process the claim for

refund and an amount equal to the integrated tax paid in respect of each

shipping bill or bill of export shall be electronically credited to the bank

account of the applicant mentioned in his registration particulars.

Government has allowed a grace period to the registrants to file returns

under the new GST Law. Therefore, this refund procedure shall as a

consequence come into operation only when the registrants file the above

mentioned returns. Further, the exporters are free to avail option (a) or

option (b). The refund shall be governed by the provisions of the section

16 of the IGST Act. , 2017

Download Source- www.taxguru.in

GST and Textiles Sector

Page 24 of 35

DUTY DRAWBACK

In GST regime, duty drawback may lose relevance as there would be seamless

credit at each stage of value addition and better transparency. Even if duty

drawback is continued to offset the impact of basic customs duty component,

which is non-creditable tax, the drawback rate could be very less. This could

impact largely, those assesses who are dependent on duty drawbacks for

achieving good margin / profit.

No amendments have been made to the drawback provisions (Section 74 or

Section 75) under Customs Act 1962 in the GST regime. Hence, the drawback

scheme will continue in terms of both section 74 and section 75. Option of All

Industry Rate (AIR) as well as Brand Rate under Section 75 shall also continue.

Drawback under Section 74 will refund Customs duties as well as Integrated Tax

and Compensation Cess paid on imported goods which are re-exported.

At present Duty Drawback Scheme under Section 75 neutralises Customs duty,

Central excise duty and Service Tax chargeable on any imported materials or

excisable materials used or taxable services used as input services in the

manufacture of export goods. Under GST regime, Drawback under Section 75

shall be limited to Customs duties on imported inputs and Central Excise duty on

items specified in Fourth Schedule to Central Excise Act 1944 (specified petroleum

products, tobacco etc.) used as inputs or fuel for captive power generation.

A transition period of three months is also being provided from date of

implementation of GST i.e. 1.7.2017. During this period, existing duty drawback

scheme under Section 75 shall continue. For exports during this period, exporters

can claim higher rate of duty drawback (composite AIR) subject to conditions

that no input tax credit of CGST/IGST is claimed, no refund of IGST paid on export

goods is claimed and no CENVAT credit is carried forward. A declaration from

exporter and certificate from jurisdictional GST officer in this regard has been

prescribed in the notification related to AIRs. This will prevent double availment of

neutralization of input taxes. Similarly, the exporter can claim brand rate for

Customs, Central Excise duties and Service Tax during this period.

Exporters also have the option of claiming only the Customs portion of AIR and

claim refund/ITC under GST laws. All Industry Rates for the transition period shall

be notified in due course of time.

Download Source- www.taxguru.in

GST and Textiles Sector

Page 25 of 35

ANNEXURE I

Some important definitions:

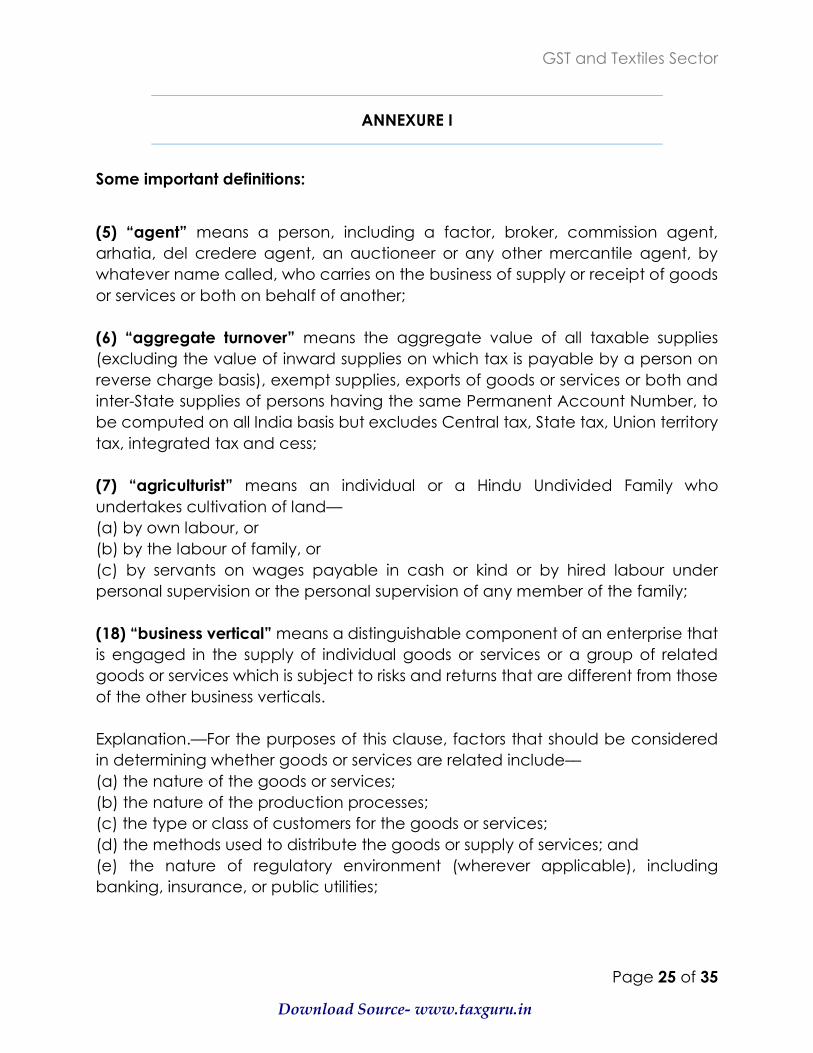

(5) “agent” means a person, including a factor, broker, commission agent,

arhatia, del credere agent, an auctioneer or any other mercantile agent, by

whatever name called, who carries on the business of supply or receipt of goods

or services or both on behalf of another;

(6) “aggregate turnover” means the aggregate value of all taxable supplies

(excluding the value of inward supplies on which tax is payable by a person on

reverse charge basis), exempt supplies, exports of goods or services or both and

inter-State supplies of persons having the same Permanent Account Number, to

be computed on all India basis but excludes Central tax, State tax, Union territory

tax, integrated tax and cess;

(7) “agriculturist” means an individual or a Hindu Undivided Family who

undertakes cultivation of land—

(a) by own labour, or

(b) by the labour of family, or

(c) by servants on wages payable in cash or kind or by hired labour under

personal supervision or the personal supervision of any member of the family;

(18) “business vertical” means a distinguishable component of an enterprise that

is engaged in the supply of individual goods or services or a group of related

goods or services which is subject to risks and returns that are different from those

of the other business verticals.

Explanation.––For the purposes of this clause, factors that should be considered

in determining whether goods or services are related include––

(a) the nature of the goods or services;

(b) the nature of the production processes;

(c) the type or class of customers for the goods or services;

(d) the methods used to distribute the goods or supply of services; and

(e) the nature of regulatory environment (wherever applicable), including

banking, insurance, or public utilities;

Download Source- www.taxguru.in

GST and Textiles Sector

Page 26 of 35

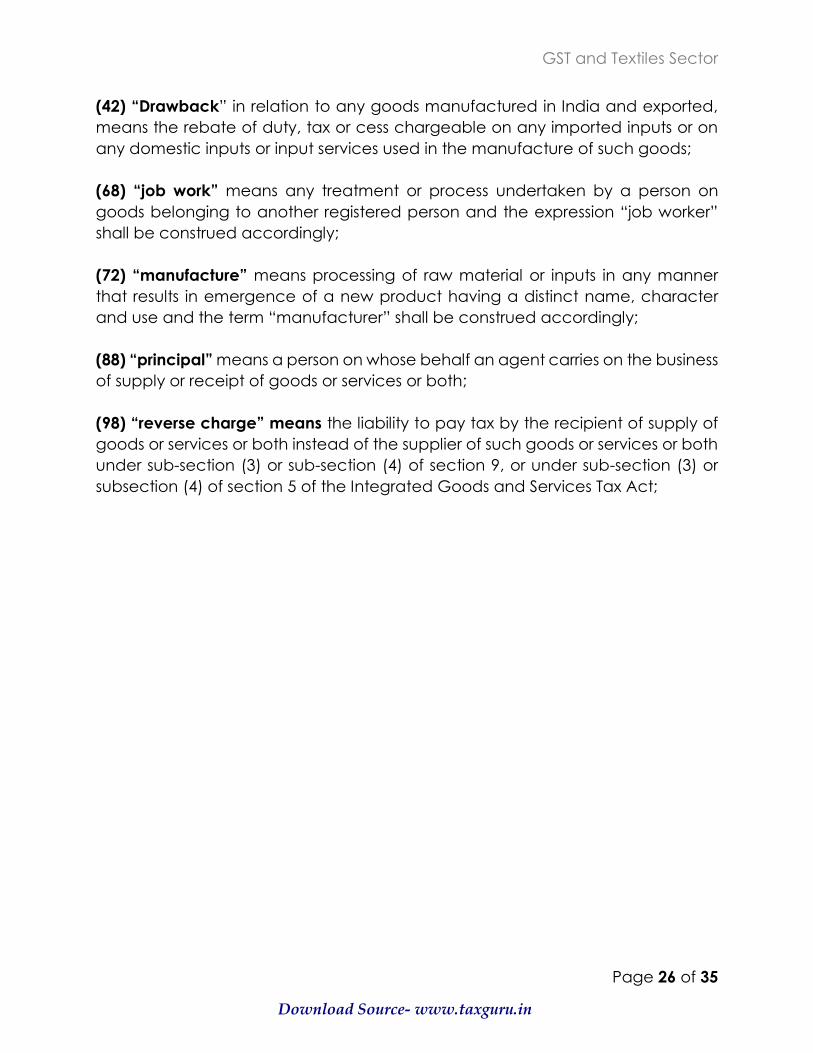

(42) “Drawback” in relation to any goods manufactured in India and exported,

means the rebate of duty, tax or cess chargeable on any imported inputs or on

any domestic inputs or input services used in the manufacture of such goods;

(68) “job work” means any treatment or process undertaken by a person on

goods belonging to another registered person and the expression “job worker”

shall be construed accordingly;

(72) “manufacture” means processing of raw material or inputs in any manner

that results in emergence of a new product having a distinct name, character

and use and the term “manufacturer” shall be construed accordingly;

(88) “principal” means a person on whose behalf an agent carries on the business

of supply or receipt of goods or services or both;

(98) “reverse charge” means the liability to pay tax by the recipient of supply of

goods or services or both instead of the supplier of such goods or services or both

under sub-section (3) or sub-section (4) of section 9, or under sub-section (3) or

subsection (4) of section 5 of the Integrated Goods and Services Tax Act;

Download Source- www.taxguru.in

GST and Textiles Sector

Page 27 of 35

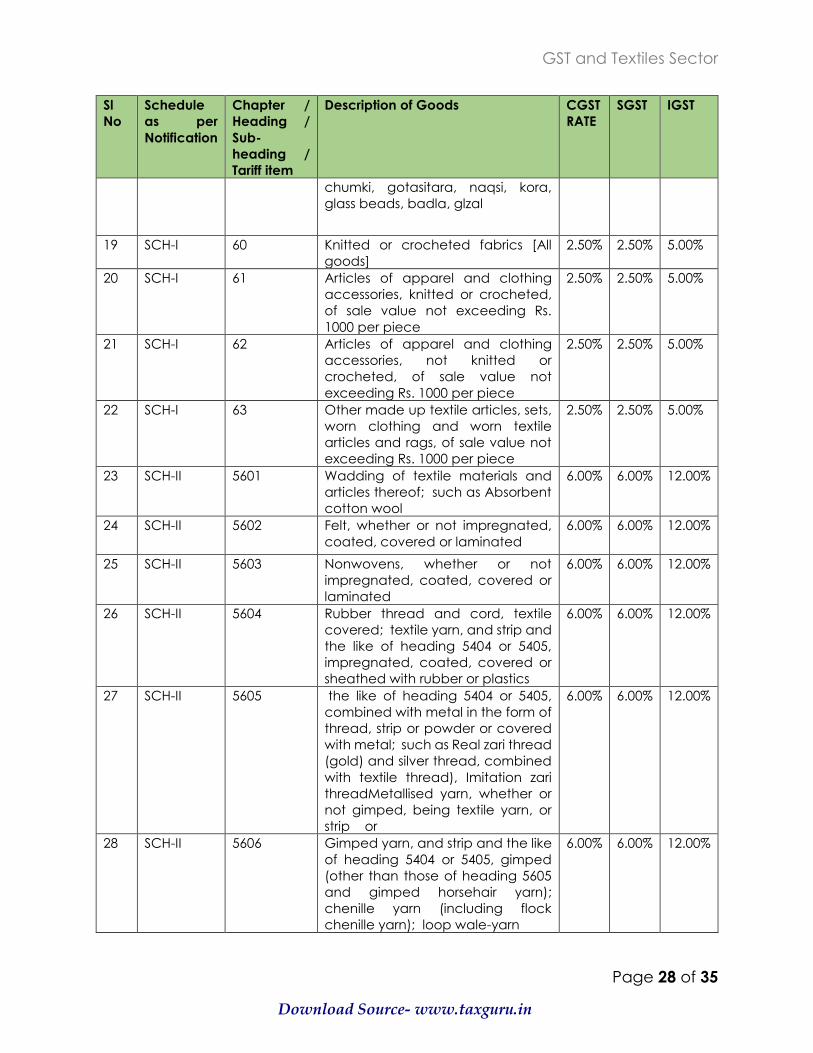

ANNEXURE II

CGST, SGST and IGST Rate for Textile Sector

Sl

No

Schedule

as per

Notification

Chapter /

Heading /

Sub-

heading /

Tariff item

Description of Goods CGST

RATE

SGST IGST

1 SCH 52 Gandhi Topi 0.00% 0.00% 0.00%

2 SCH 52 Khadi yarn 0.00% 0.00% 0.00%

3 SCH 5303 Jute fibres, raw or processed but

not spun

0.00% 0.00% 0.00%

4 SCH 5305 Coconut, coir fibre 0.00% 0.00% 0.00%

5 SCH 63 Indian National Flag 0.00% 0.00% 0.00%

6 SCH-I 5201 to 5203 Cotton and Cotton waste 2.50% 2.50% 5.00%

7 SCH-I 5204 Cotton sewing thread, whether or

not put up for retail sale

2.50% 2.50% 5.00%

8 SCH-I 5205 to 5207 Cotton yarn [other than khadi yarn] 2.50% 2.50% 5.00%

9 SCH-I 5208 to 5212 Woven fabrics of cotton 2.50% 2.50% 5.00%

10 SCH-I 5301 All goods i.e. flax, raw or processed

but not spun; flax tow and waste

(including yarn waste and

garneted stock)

2.50% 2.50% 5.00%

11 SCH-I 5302 True hemp (Cannabis sativa L), raw

or processed but not spun; tow and

waste of true hemp (including yarn

waste and garneted stock)

2.50% 2.50% 5.00%

12 SCH-I 5303 All goods i.e. textile bast fibres

[other than jute fibres, raw or

processed but not spun]; tow and

waste of these fibres (including yarn

waste and garneted stock)

2.50% 2.50% 5.00%

13 SCH-I 5305 to 5308 All goods [other than coconut coir

fibre] including yarn of flax, jute,

other textile bast fibres, other

vegetable textile fibres; paper yarn

2.50% 2.50% 5.00%

14 SCH-I 5309 to 5311 Woven fabrics of other vegetable

textile fibres, paper yarn

2.50% 2.50% 5.00%

15 SCH-I 5407, 5408 Woven fabrics of manmade textile

materials

2.50% 2.50% 5.00%

16 SCH-I 5512 to 5516 Woven fabrics of manmade staple

fibres

2.50% 2.50% 5.00%

17 SCH-I 5705 Coir mats, matting and floor

covering

2.50% 2.50% 5.00%

18 SCH-I 5809, 5810 Embroidery or zari articles, that is to

say,- imi, zari, kasab, saima, dabka,

2.50% 2.50% 5.00%

Download Source- www.taxguru.in

GST and Textiles Sector

Page 28 of 35

Sl

No

Schedule

as per

Notification

Chapter /

Heading /

Sub-

heading /

Tariff item

Description of Goods CGST

RATE

SGST IGST

chumki, gotasitara, naqsi, kora,

glass beads, badla, glzal

19 SCH-I 60 Knitted or crocheted fabrics [All

goods]

2.50% 2.50% 5.00%

20 SCH-I 61 Articles of apparel and clothing

accessories, knitted or crocheted,

of sale value not exceeding Rs.

1000 per piece

2.50% 2.50% 5.00%

21 SCH-I 62 Articles of apparel and clothing

accessories, not knitted or

crocheted, of sale value not

exceeding Rs. 1000 per piece

2.50% 2.50% 5.00%

22 SCH-I 63 Other made up textile articles, sets,

worn clothing and worn textile

articles and rags, of sale value not

exceeding Rs. 1000 per piece

2.50% 2.50% 5.00%

23 SCH-II 5601 Wadding of textile materials and

articles thereof; such as Absorbent

cotton wool

6.00% 6.00% 12.00%

24 SCH-II 5602 Felt, whether or not impregnated,

coated, covered or laminated

6.00% 6.00% 12.00%

25 SCH-II 5603 Nonwovens, whether or not

impregnated, coated, covered or

laminated

6.00% 6.00% 12.00%

26 SCH-II 5604 Rubber thread and cord, textile

covered; textile yarn, and strip and

the like of heading 5404 or 5405,

impregnated, coated, covered or

sheathed with rubber or plastics

6.00% 6.00% 12.00%

27 SCH-II 5605 the like of heading 5404 or 5405,

combined with metal in the form of

thread, strip or powder or covered

with metal; such as Real zari thread

(gold) and silver thread, combined

with textile thread), Imitation zari

threadMetallised yarn, whether or

not gimped, being textile yarn, or

strip or

6.00% 6.00% 12.00%

28 SCH-II 5606 Gimped yarn, and strip and the like

of heading 5404 or 5405, gimped

(other than those of heading 5605

and gimped horsehair yarn);

chenille yarn (including flock

chenille yarn); loop wale-yarn

6.00% 6.00% 12.00%

Download Source- www.taxguru.in

GST and Textiles Sector

Page 29 of 35

Sl

No

Schedule

as per

Notification

Chapter /

Heading /

Sub-

heading /

Tariff item

Description of Goods CGST

RATE

SGST IGST

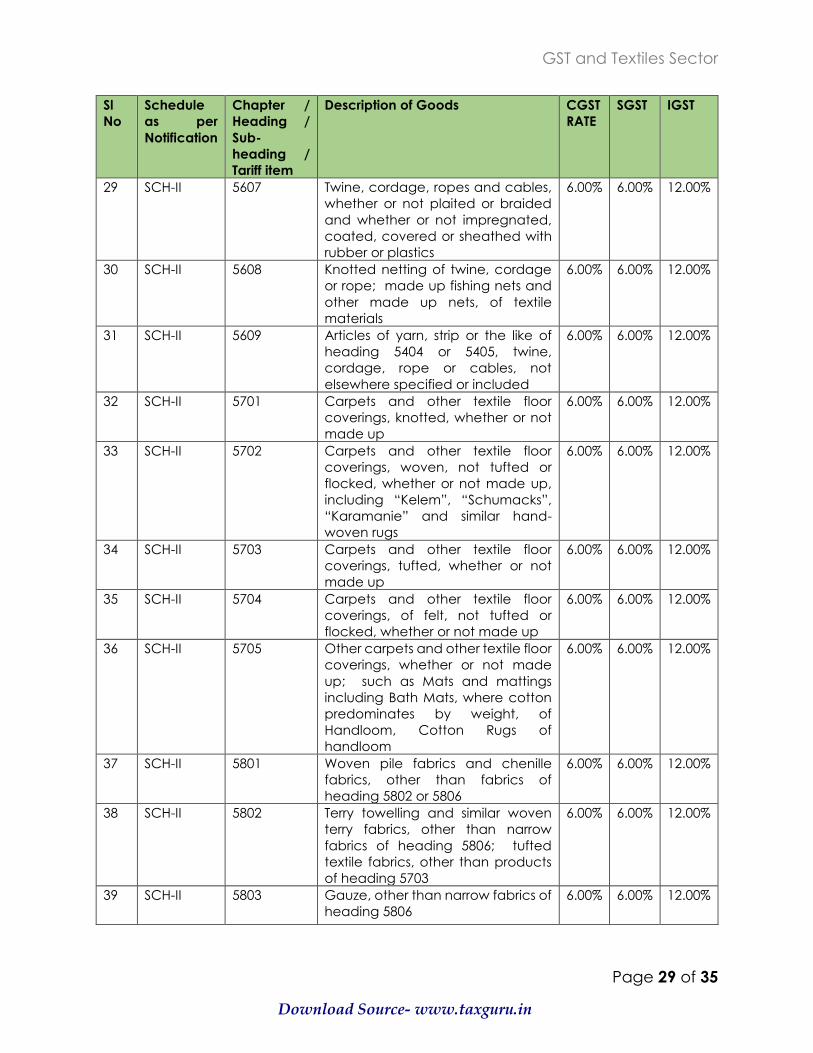

29 SCH-II 5607 Twine, cordage, ropes and cables,

whether or not plaited or braided

and whether or not impregnated,

coated, covered or sheathed with

rubber or plastics

6.00% 6.00% 12.00%

30 SCH-II 5608 Knotted netting of twine, cordage

or rope; made up fishing nets and

other made up nets, of textile

materials

6.00% 6.00% 12.00%

31 SCH-II 5609 Articles of yarn, strip or the like of

heading 5404 or 5405, twine,

cordage, rope or cables, not

elsewhere specified or included

6.00% 6.00% 12.00%

32 SCH-II 5701 Carpets and other textile floor

coverings, knotted, whether or not

made up

6.00% 6.00% 12.00%

33 SCH-II 5702 Carpets and other textile floor

coverings, woven, not tufted or

flocked, whether or not made up,

including “Kelem”, “Schumacks”,

“Karamanie” and similar hand-

woven rugs

6.00% 6.00% 12.00%

34 SCH-II 5703 Carpets and other textile floor

coverings, tufted, whether or not

made up

6.00% 6.00% 12.00%

35 SCH-II 5704 Carpets and other textile floor

coverings, of felt, not tufted or

flocked, whether or not made up

6.00% 6.00% 12.00%

36 SCH-II 5705 Other carpets and other textile floor

coverings, whether or not made

up; such as Mats and mattings

including Bath Mats, where cotton

predominates by weight, of

Handloom, Cotton Rugs of

handloom

6.00% 6.00% 12.00%

37 SCH-II 5801 Woven pile fabrics and chenille

fabrics, other than fabrics of

heading 5802 or 5806

6.00% 6.00% 12.00%

38 SCH-II 5802 Terry towelling and similar woven

terry fabrics, other than narrow

fabrics of heading 5806; tufted

textile fabrics, other than products

of heading 5703

6.00% 6.00% 12.00%

39 SCH-II 5803 Gauze, other than narrow fabrics of

heading 5806

6.00% 6.00% 12.00%

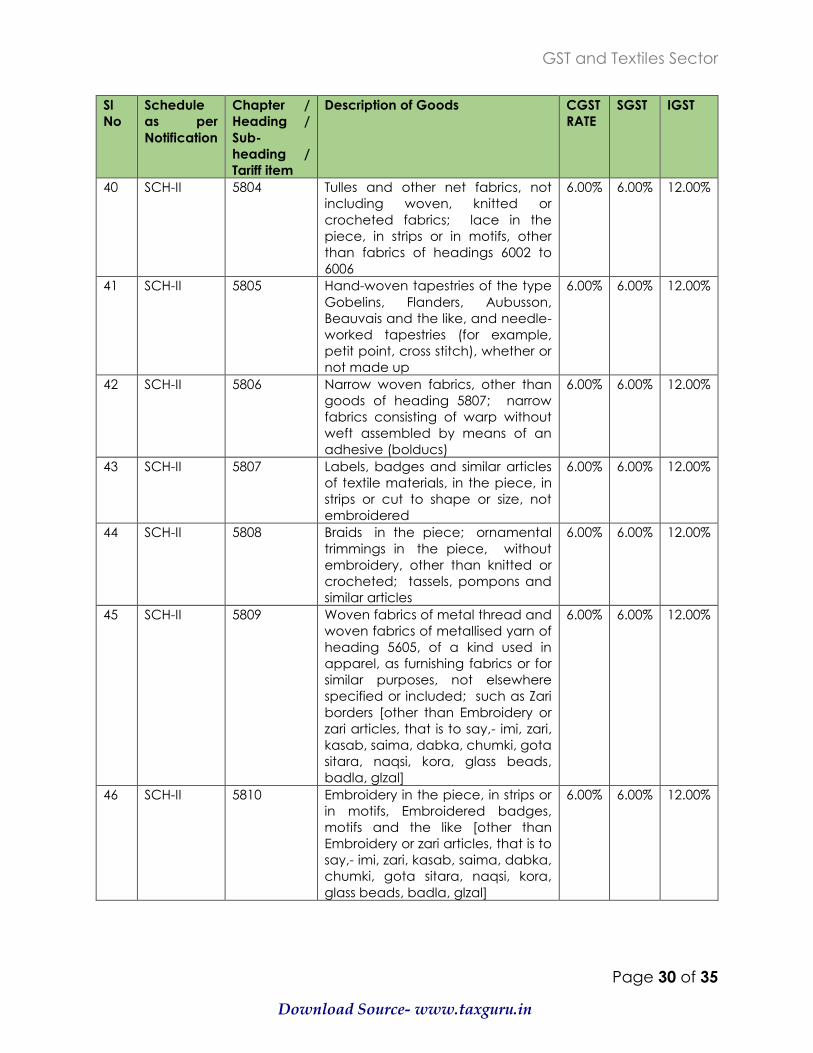

Download Source- www.taxguru.in

GST and Textiles Sector

Page 30 of 35

Sl

No

Schedule

as per

Notification

Chapter /

Heading /

Sub-

heading /

Tariff item

Description of Goods CGST

RATE

SGST IGST

40 SCH-II 5804 Tulles and other net fabrics, not

including woven, knitted or

crocheted fabrics; lace in the

piece, in strips or in motifs, other

than fabrics of headings 6002 to

6006

6.00% 6.00% 12.00%

41 SCH-II 5805 Hand-woven tapestries of the type

Gobelins, Flanders, Aubusson,

Beauvais and the like, and needle-

worked tapestries (for example,

petit point, cross stitch), whether or

not made up

6.00% 6.00% 12.00%

42 SCH-II 5806 Narrow woven fabrics, other than

goods of heading 5807; narrow

fabrics consisting of warp without

weft assembled by means of an

adhesive (bolducs)

6.00% 6.00% 12.00%

43 SCH-II 5807 Labels, badges and similar articles

of textile materials, in the piece, in

strips or cut to shape or size, not

embroidered

6.00% 6.00% 12.00%

44 SCH-II 5808 Braids in the piece; ornamental

trimmings in the piece, without

embroidery, other than knitted or

crocheted; tassels, pompons and

similar articles

6.00% 6.00% 12.00%

45 SCH-II 5809 Woven fabrics of metal thread and

woven fabrics of metallised yarn of

heading 5605, of a kind used in

apparel, as furnishing fabrics or for

similar purposes, not elsewhere

specified or included; such as Zari

borders [other than Embroidery or

zari articles, that is to say,- imi, zari,

kasab, saima, dabka, chumki, gota

sitara, naqsi, kora, glass beads,

badla, glzal]

6.00% 6.00% 12.00%

46 SCH-II 5810 Embroidery in the piece, in strips or

in motifs, Embroidered badges,

motifs and the like [other than

Embroidery or zari articles, that is to

say,- imi, zari, kasab, saima, dabka,

chumki, gota sitara, naqsi, kora,

glass beads, badla, glzal]

6.00% 6.00% 12.00%

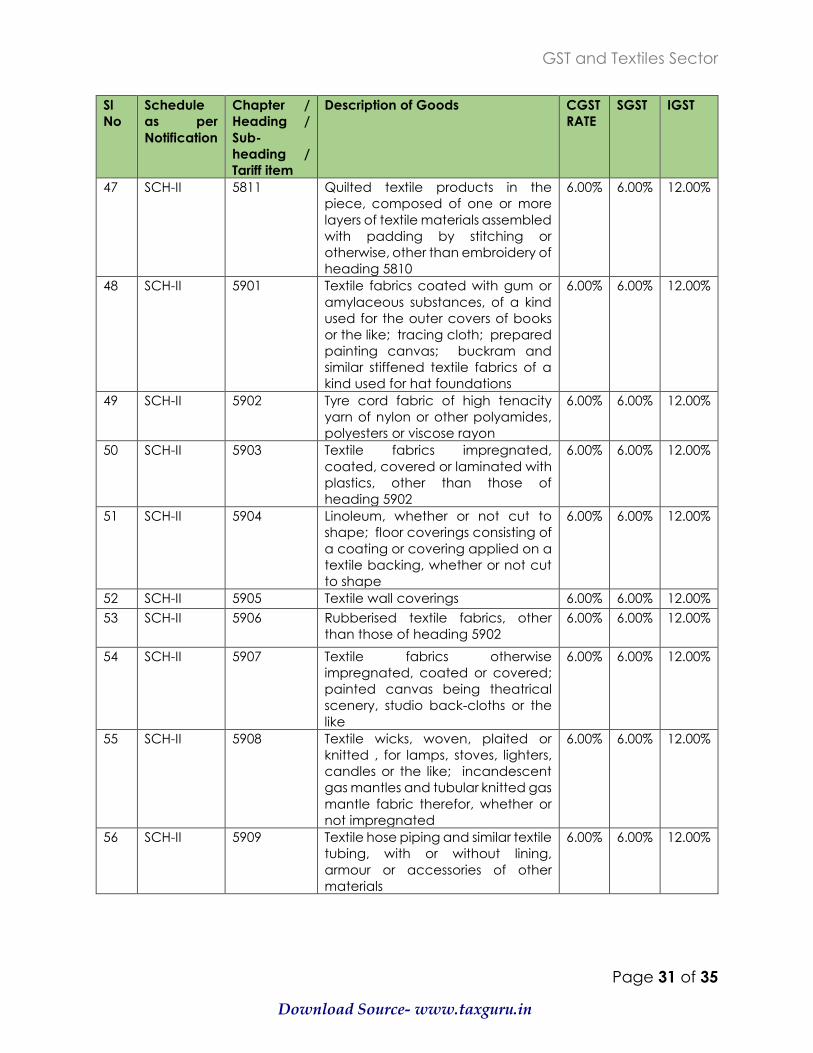

Download Source- www.taxguru.in

GST and Textiles Sector

Page 31 of 35

Sl

No

Schedule

as per

Notification

Chapter /

Heading /

Sub-

heading /

Tariff item

Description of Goods CGST

RATE

SGST IGST

47 SCH-II 5811 Quilted textile products in the

piece, composed of one or more

layers of textile materials assembled

with padding by stitching or

otherwise, other than embroidery of

heading 5810

6.00% 6.00% 12.00%

48 SCH-II 5901 Textile fabrics coated with gum or

amylaceous substances, of a kind

used for the outer covers of books

or the like; tracing cloth; prepared

painting canvas; buckram and

similar stiffened textile fabrics of a

kind used for hat foundations

6.00% 6.00% 12.00%

49 SCH-II 5902 Tyre cord fabric of high tenacity

yarn of nylon or other polyamides,

polyesters or viscose rayon

6.00% 6.00% 12.00%

50 SCH-II 5903 Textile fabrics impregnated,

coated, covered or laminated with

plastics, other than those of

heading 5902

6.00% 6.00% 12.00%

51 SCH-II 5904 Linoleum, whether or not cut to

shape; floor coverings consisting of

a coating or covering applied on a

textile backing, whether or not cut

to shape

6.00% 6.00% 12.00%

52 SCH-II 5905 Textile wall coverings 6.00% 6.00% 12.00%

53 SCH-II 5906 Rubberised textile fabrics, other

than those of heading 5902

6.00% 6.00% 12.00%

54 SCH-II 5907 Textile fabrics otherwise

impregnated, coated or covered;

painted canvas being theatrical

scenery, studio back-cloths or the

like

6.00% 6.00% 12.00%

55 SCH-II 5908 Textile wicks, woven, plaited or

knitted , for lamps, stoves, lighters,

candles or the like; incandescent

gas mantles and tubular knitted gas

mantle fabric therefor, whether or

not impregnated

6.00% 6.00% 12.00%

56 SCH-II 5909 Textile hose piping and similar textile

tubing, with or without lining,

armour or accessories of other

materials

6.00% 6.00% 12.00%

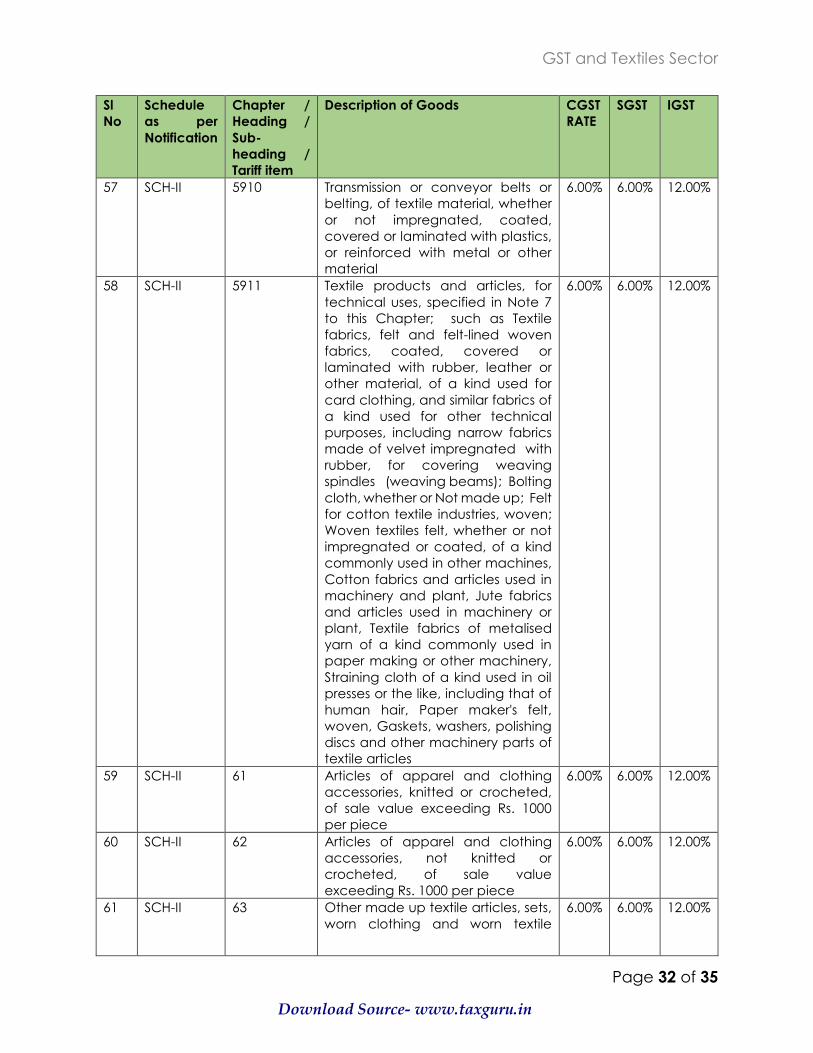

Download Source- www.taxguru.in

GST and Textiles Sector

Page 32 of 35

Sl

No

Schedule

as per

Notification

Chapter /

Heading /

Sub-

heading /

Tariff item

Description of Goods CGST

RATE

SGST IGST

57 SCH-II 5910 Transmission or conveyor belts or

belting, of textile material, whether

or not impregnated, coated,

covered or laminated with plastics,

or reinforced with metal or other

material

6.00% 6.00% 12.00%

58 SCH-II 5911 Textile products and articles, for

technical uses, specified in Note 7

to this Chapter; such as Textile

fabrics, felt and felt-lined woven

fabrics, coated, covered or

laminated with rubber, leather or

other material, of a kind used for

card clothing, and similar fabrics of

a kind used for other technical

purposes, including narrow fabrics

made of velvet impregnated with

rubber, for covering weaving

spindles (weaving beams); Bolting

cloth, whether or Not made up; Felt

for cotton textile industries, woven;

Woven textiles felt, whether or not

impregnated or coated, of a kind

commonly used in other machines,

Cotton fabrics and articles used in

machinery and plant, Jute fabrics

and articles used in machinery or

plant, Textile fabrics of metalised

yarn of a kind commonly used in

paper making or other machinery,

Straining cloth of a kind used in oil

presses or the like, including that of

human hair, Paper maker's felt,

woven, Gaskets, washers, polishing

discs and other machinery parts of

textile articles

6.00% 6.00% 12.00%

59 SCH-II 61 Articles of apparel and clothing

accessories, knitted or crocheted,

of sale value exceeding Rs. 1000

per piece

6.00% 6.00% 12.00%

60 SCH-II 62 Articles of apparel and clothing

accessories, not knitted or

crocheted, of sale value

exceeding Rs. 1000 per piece

6.00% 6.00% 12.00%

61 SCH-II 63 Other made up textile articles, sets,

worn clothing and worn textile

6.00% 6.00% 12.00%

Download Source- www.taxguru.in

GST and Textiles Sector

Page 33 of 35

Sl

No

Schedule

as per

Notification

Chapter /

Heading /

Sub-

heading /

Tariff item

Description of Goods CGST

RATE

SGST IGST

articles and rags, of sale value

exceeding Rs. 1000 per piece

62 SCH-III 5401 Sewing thread of manmade

filaments, whether or not put up for

retail sale

9.00% 9.00% 18.00%

63 SCH-III 5402, 5404,

5406

All synthetic filament yarn such as

nylon, polyester, acrylic, etc.

9.00% 9.00% 18.00%

64 SCH-III 5403, 5405,

5406

All artificial filament yarn such as

viscose rayon, Cuprammonium,

etc.

9.00% 9.00% 18.00%

65 SCH-III 5501, 5502 Synthetic or artificial filament tow 9.00% 9.00% 18.00%

66 SCH-III 5503,

5504,5506,

5507

Synthetic or artificial staple fibres 9.00% 9.00% 18.00%

67 SCH-III 5505 Waste of manmade fibres 9.00% 9.00% 18.00%

68 SCH-III 5508 Sewing thread of manmade staple

fibres

9.00% 9.00% 18.00%

69 SCH-III 5509, 5510,

5511

Yarn of manmade staple fibres 9.00% 9.00% 18.00%

Download Source- www.taxguru.in

GST and Textiles Sector

Page 34 of 35

ANNEXURE III

GST, SGST AND IGT RATES FOR SOME INPUTS AND CAPITAL GOODS

Sl.

No

SCH Chapter /

Heading /

Sub-

heading /

Tariff item

Description of Goods CGST

RATE

SGST

RATE

CGST

RATE

1 SCH-III 3203 Colouring matter of vegetable or

animal origin (including dyeing

extracts but excluding animal

black), whether or not chemically

defined; preparations as specified

in Note 3 to this Chapter based on

colouring matter of vegetable or

animal origin

9.00% 9.00% 18%

2 SCH-III 3204 Synthetic organic colouring

matter, whether or not chemically

defined; preparations as specified

in Note 3 to this Chapter based on

synthetic organic colouring

matter; synthetic organic

products of a kind used as

fluorescent brightening agents or

as luminophores, whether or not

chemically defined

9.00% 9.00% 18%

3 SCH-III 3205 Colour lakes; preparations as

specified in Note 3 to this Chapter

based on colour lakes

9.00% 9.00% 18%

4 SCH-III 3206 Other colouring matter;

preparations as specified in Note 3

to this Chapter, other than those

of heading 32.03, 32.04 or 32.05;

inorganic products of a kind used

as luminophores, whether or not

chemically defined

9.00% 9.00% 9.00%

5 SCH-II 8452 Sewing machines 6.00% 6.00% 6.00%

6 SCH-III 8445 Machines for preparing textile

fibres; spinning, doubling or

twisting machines and other

machinery for producing textile

yarns; textile reeling or winding

(including weft-winding) machines

and machines for preparing textile

yarns for use on the machines of

heading 8446 or 8447

9.00% 9.00% 18%

7 SCH-III 8446 Weaving machines (looms) 9.00% 9.00% 18%

Download Source- www.taxguru.in

GST and Textiles Sector

Page 35 of 35

Sl.

No

SCH Chapter /

Heading /

Sub-

heading /

Tariff item

Description of Goods CGST

RATE

SGST

RATE

CGST

RATE

8 SCH-III 8447 Knitting machines, stitch-bonding

machines and machines for

making gimped yarn, tulle, lace,

embroidery, trimmings, braid or

net and machines for tufting

9.00% 9.00% 18%

9 SCH-III 8448 Auxiliary machinery for use with

machines of heading 84.44,

84.45,84.46 or 84.47 (for example,

dobbies, Jacquards, automatic

stop motions, shuttle changing

mechanisms); parts and

accessories suitable for use solely

or principally with the machines of

this heading or of heading 8444,

8445,8446 or 8447 (for example,

spindles and spindles flyers, card

clothing, combs, extruding nipples,

shuttles, healds and heald frames,

hosiery needles)

9.00% 9.00% 18%

10 SCH-III 8449 Machinery for the manufacture or

finishing of felt or nonwovens in the

piece or in shapes, including

machinery for making felt hats;

blocks for making hats

9.00% 9.00% 18%

11 SCH-III 8451 Machinery (other than machines

of heading 8450) for washing,

cleaning, wringing, drying, ironing,

pressing (including fusing presses),

bleaching, dyeing, dressing,

finishing, coating or impregnating

textile yarns, fabrics or made up

textile articles and machines for

applying the paste to the base

fabric or other support used in the

manufacture of floor covering

such as linoleum; machines for

reeling, unreeling, folding, cutting

or pinking textile fabrics

9.00% 9.00% 18%

12 SCH-III 8482 Ball bearing, Roller Bearings 9.00% 9.00% 18%

References

― E-filers of the CBEC on various legal provisions of GST

― Goods and Services Act, 2017

― Goods and Services Rules, 2017

― Notification No:1/2017 Central (Rate) dated as amended

― Notification No:2/2017 Central (Rate) dated as amended

Download Source- www.taxguru.in