Growing global ventures by effective seed acceleration – The opportunities and barriers of...

86

Growing global ventures by effective seed acceleration The opportunities and barriers of business acceleration Supervisors: Gyorgy Drotos PhD (Corvinus University of Budapest, Research Centre of Information Resources Management) Peter Kadas MD (serial entrepreneur, founder of Brandvocat, blogger at startupdate.hu). 14. 05. 2013

-

Upload

balazs-szabo -

Category

Business

-

view

6.667 -

download

0

Transcript of Growing global ventures by effective seed acceleration – The opportunities and barriers of...

Growing global ventures by effective seed acceleration

The opportunities and barriers of business acceleration

Supervisors:

Gyorgy Drotos PhD (Corvinus University of Budapest, Research Centre of Information Resources

Management)

Peter Kadas MD (serial entrepreneur, founder of Brandvocat, blogger at startupdate.hu).

14. 05. 2013

2

About the author

Balazs Szabo is head of Business Development at InVendor and the Advisor of the Global Executive

Team at Kairos Society. Balazs Szabo was attended to the CEMS Masters’ in International Management

program which is one of the best management master according the Financial Times’ ranking and he

also attended Management and Leadership and Sociology at the Corvinus University of Budapest

beside studying in Université Catholique de Louvain in Belgium. He is an entrepreneur, strategic and

investment advisor for early stage startup companies. He is the main organizer of inveAst - Investors

Meet Startups from CEEMEA co-organized by InVendor and Bloomberg in London. He was the

organizer of the first Hungarian Innovation Day, that was held on the 16th October, 2012 in London in

order to connect the Hungarian startups with high growing potentials with London based Venture

Capitalists and Seed Investors. The patrons of the event were the British Ambassador to Hungary, the

Hungarian Ambassador to Great Britain and the Chairman of the Hungarian Private Equity and Venture

Capital Association. The event was supported by the British Private Equity and Venture Capital

Association and the EBRD.

Balazs is also a member of the education committee at Hungarian Venture Capital and Private Equity

Association. He has been elected four times as a Future Leader, by The Ambrosetti Forum (IT), by the

World Foresight Forum (NL) by the St. Petersburg International Economic Forum (RU), Youth

International Economic Forum (RU) and Open Innovations Forum (RU).

Balazs is a TEDx speaker and the author of startup/investment articles in business magazines, NEXT

Mentor, Startup Sauna Pioneers Festival and Startup Tour Ambassador. Balazs is the founder and

editor of www.cee-startups.com

You can find Balazs on LinkedIn.

www.balazsszabo.com

3

Table of Contents About the author .................................................................................................................................. 2

1 Introduction ..................................................................................................................................... 7

1.1 Problem statement .................................................................................................................. 9

1.2 The scope of the thesis .......................................................................................................... 10

1.3 Relevance .............................................................................................................................. 11

2 Methodology ................................................................................................................................. 14

3 Theoretical framework .................................................................................................................. 15

3.1 Describing the concepts ........................................................................................................ 15

3.1.1 Entrepreneurship........................................................................................................... 15

3.1.2 Startup ........................................................................................................................... 15

3.2 The actors of the entrepreneurial ecosystem ....................................................................... 17

3.2.1 Entrepreneurs ................................................................................................................ 18

3.2.2 Investors ........................................................................................................................ 18

3.2.3 Mentors/advisors .......................................................................................................... 19

4 The new economics of startups .................................................................................................... 21

4.1 How companies grow? .......................................................................................................... 21

4.2 The early stage startup challenges ........................................................................................ 23

4.3 Changes in the business environment .................................................................................. 24

4.4 The background of the shift between business incubators and business accelerators ........ 29

4.5 Business accelerators ............................................................................................................ 32

5 Key elements of the business accelerator programs .................................................................... 34

5.1 Easily accessable open application process .......................................................................... 35

5.2 Intensive competition ........................................................................................................... 35

5.3 Offered pre-seed/seed investment ....................................................................................... 35

5.4 Focus on teams ...................................................................................................................... 35

5.5 Time-limited support, intensive mentoring .......................................................................... 36

5.6 Batch of startups and alumni network .................................................................................. 37

6 Introduction of international best practices of seed acceleration ................................................ 39

6.1 Y Combinator ......................................................................................................................... 39

6.2 Techstars ............................................................................................................................... 40

6.3 500 Startups .......................................................................................................................... 42

4

6.4 Seedcamp .............................................................................................................................. 43

6.5 Startup Sauna ........................................................................................................................ 44

6.6 Startup Wise Guys ................................................................................................................. 45

6.7 StartupBootcamp .................................................................................................................. 46

6.8 Startup Highway .................................................................................................................... 46

7 Qualitative and quantitative research ........................................................................................... 48

7.1 Interviews .............................................................................................................................. 48

7.1.1 The importance of accelerators .................................................................................... 48

7.1.2 The birth of accelerators ............................................................................................... 48

7.1.3 Creating entrepreneurial ecosystem by using best practices ....................................... 49

7.1.4 Criteria of selecting teams ............................................................................................. 50

7.1.5 Value proposition for startups ...................................................................................... 50

7.1.6 Mentors/coaches........................................................................................................... 50

7.1.7 The core program .......................................................................................................... 51

7.1.8 The geographic areas covered....................................................................................... 52

7.1.9 Success and metrics ....................................................................................................... 52

7.1.10 Skills ............................................................................................................................... 53

7.2 Survey .................................................................................................................................... 54

7.2.1 Demographic limitations ............................................................................................... 54

7.2.2 The surveyed sectors ..................................................................................................... 56

7.3 Analysis of the survey results ................................................................................................ 56

7.4 Summary of the survey results .............................................................................................. 61

7.4.1 Accelerators and their location ..................................................................................... 61

7.4.2 The most important decisive factors of selecting accelerator ...................................... 61

7.4.3 The key added values of an accelerator program ......................................................... 61

7.4.4 Other preferences of entrepreneurs regarding the length and program elements ..... 61

8 Conclusion ..................................................................................................................................... 62

9 The findings of the research .......................................................................................................... 63

10 Recommendation for further research ..................................................................................... 65

References ............................................................................................................................................. 66

Appendix ................................................................................................................................................ 70

1. E-mail Interview Questions for StartupHighway – Agnė Adomaitytė 02. 04. 2013 .................. 70

2. E-mail Interview with Antti Ylimutka Startup Sauna CEO 17. 04. 2013 .................................... 72

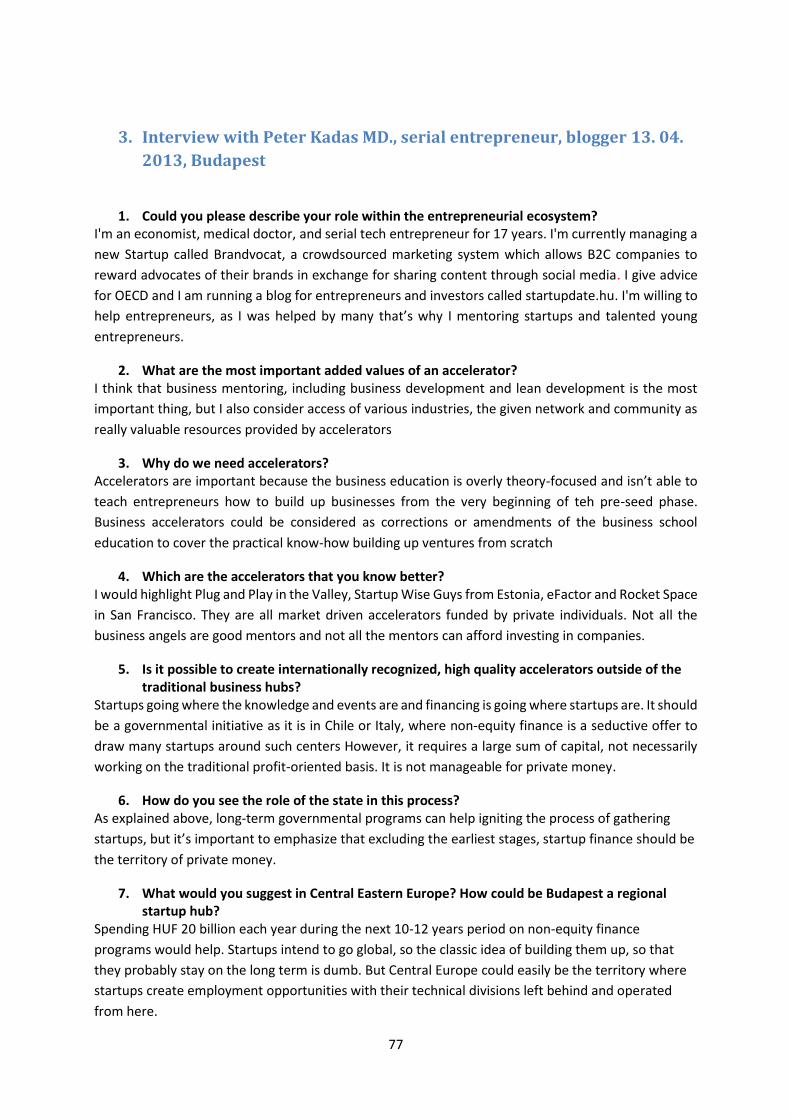

3. Interview with Peter Kadas MD., serial entrepreneur, blogger 13. 04. 2013, Budapest .......... 77

5

4. E-mail Interview with Mike Reiner, Startup Wise Guys 23. 04. 2013........................................ 78

5. The questionnaire...................................................................................................................... 81

6

Graphs 1. Graph The process of the deaflow ................................................................................................... 12

2. Graph The entrepreneurial ecosystem ............................................................................................. 17

3. Graph How companies grow? ........................................................................................................... 21

4. Graph The transition from a startup to a company .......................................................................... 22

5. Graph The investment need and lifecycles ...................................................................................... 23

6. Graph Equity gap vs. competence gap ............................................................................................. 24

7. Graph Seed deals by vintage quarter ............................................................................................... 27

9. Graph The Role of Business Incubators ............................................................................................ 30

10. Graph Continuum of added value services provided by incubators and accelerators .................. 31

11. Graph Different types of accelerators ............................................................................................. 33

12. Graph The intersection of accelerators and incubators ................................................................. 34

13. Graph The Accelerator Cycle ........................................................................................................... 37

14. Graph Key elements of the accelerator program ............................................................................ 38

15. Graph The vicious circle of the accelerators ................................................................................... 38

16. Graph The age distribution of the surveyed entrepreneurs ........................................................... 54

17. Graph Nationality of the surveyed entrepreneurs ......................................................................... 55

18. Graph Number of entrepreneurs by their sector ............................................................................ 56

19. Graph The proportion of the surveyed entrepreneurs regarding their current stay ...................... 57

20. Graph Have you ever participated in a startup accelerator program? .......................................... 57

21. Graph Types of funding .................................................................................................................. 58

22. Graph The most important decisive points of choosing an accelerator ......................................... 58

23. Graph Please evaluate the most important added valua of an accelerator ................................... 59

24. Graph Please evaluate the following educational elements of the accelerator program .............. 60

25. Graph How to measure accelerators .............................................................................................. 63

7

1 Introduction

„Entrepreneurs embody the promise of America: the idea that if you have a good idea and are willing

to work hard and see it through, you can succeed in this country. And in fulfilling this promise,

entrepreneurs also play a critical role in expanding our economy and creating jobs.”

President Barack Obama

After Barack Obama acknowledged the importance of entrepreneurship through the launch of Startup

America, the phenomenon was at the forefront of the discussions. Entrepreneurship and startups

became a global theme that impacted every geography, industry, market and demographic throughout

the world. (Feld, 2012) We are living in the age of entrepreneurship and fast growing ventures

according to Janos Vecsenyi (Vecsenyi, 2011)

Building a sustainable startup ecosystem is a key factor towards eliminating the market risks of seed

funding as this is the stage where most companies fail. There are different models of seed acceleration

throughout the world in order to minimize the risks of seed investors that is a common bottleneck of

growing global ventures.

In certain countries where the investment culture is more developed market actors do the acceleration

phase (USA), in other parts of the world governmental interventions and support is needed to get

private investors involved in one of the riskiest part of the investment lifecycle (Israel, Finland etc.)

Business accelerator is a new approach of helping and funding startup companies at the seed stage.

Instead of filtering out only one startup at a time these programs filter out cohorts and mentoring

them in batches to make it more efficient and less risky. The business accelerator model differs from

the traditional seed-stage investing and business incubators (Cristiansen, 2009)

Over the past eight years, a new methods of incubating technology startups have emerged, driven by

business angel investors, serial entrepreneurs and venture capitalists: the accelerator program.

In the global innovation hubs like the Silicon Valley, New York, Boston, Berlin or London all the needed

elements of the entrepreneurial ecosystem are present, including (serial) entrepreneurs, angel

investors, venture capitalists, incubators, accelerators etc. There other countries that were not

identified as flagship nations of the innovation a few decades ago, but there is significant improvement

as the results of the well organized and executed strategies and subsidies coming from the state or

wealthy private individuals. Countries as Israel, Chile or even Estonia are on their track to be among

the innovation hub of their geographical region or even broaden territories.

The thesis sheds light on the global best practices of seed funding and business acceleration. The goal

of the paper is to identify suitable and adaptable models of seed funding that could contribute to the

8

birth of new venture success stories and entrepreneurial growth in those regions that can not be

considered as traditional business hubs.

I have been involved personally in building an entrepreneurial ecosystem in Hungary and in Central

Eastern Europe since 2010. I was the president of Kairos Society, a student run global not for profit

organization in the past two years in Hungary and I was working on the Central Eastern European

expansion where I met really promising early stage companies building an innovative globally scalable

product of service. Currently I am an investment advisor for startup companies at InVendor Investment

and Innovation Ltd. and I am working with scalable businesses on their international expansion. I was

the local organizer of the first international seed accelerator program’s Warmup in Budapest (Startup

Sauna Warmup in 1st October 2012) and I have organized the Startup Sauna Zagreb Warmup event in

March 2013.

I was also the main organizer of the first Hungarian Innovation Day, that was held on the 16th October,

2012 in London in order to connect the Hungarian startups with high growing potentials with London

based Venture Capitalists and Seed Investors. The event was supported by the British Private Equity

and Venture Capital Association and the EBRD. I am also a TEDx speaker and the author of

startup/investment articles in business magazines.

By regularly working with startups I have realized that there is a lack of publication and primary

research on the topic not just in the local level but on the global scale as well. I have started to work

on my research at the autumn of 2012. In the meantime a few really valuable contribution had been

published including Frimodig, Barrehag et al, and Bollingtoft’s research on the topic (Frimodig, 2012,

Barrehag et al 2012, Bollingtoft, 2012). Therefore I have decided to focus on the empirical added value

expecially by measuring the preferences quantitatively.

The effective acceleration of businesses at the early stage is a new management challenge that is

solved by top tier accelerator programs and their mentorship based educational elements. This way of

education is considered as an alternative of an MBA course, mostly for entrepreneurs as the startup

stage needs different skills and approaches (searching for the working business model) as the

transition stage of becoming a successful company (executing a business model). I thought the

phenomenon of business accelerators is an interesting research topic of my Management and

Leadership thesis in order to know their best practices and added values better that helps their

positioning within the management science. Because of the lack of Hungarian sources and the low

number of global scientific literature in this topic I have asked for the opportunity to write a reference

work in English in order to have a small contribution to the business accelerators literature within the

science of management.

The cradle of business acccelerators is in the US, as a result of the growing popularity of Y combinator

(located in Mountain View) and Techstars (started in Boulder, Colorado). The number of accelerator

programmes has grown fastly in the US over the past few years and apparently the trend is being

replicated in Europe. From one accelerator programme, Y Combinator in 2005, there are now hundreds

just in the US that are funding hundreds of startups per year. There are also a number of high profle

startup that succeeded from accelerator programmes. (Miller, Bound, 2011)

9

Despite the short track record it is obvious that business accelerator programs have positive impact on

entrepreneurs, helping them to develop rapidly, create a powerful network that helps business

development and follow-on fundings within a short timeframe.

In order to get primary information on the actors during this research I have conducted interviews with

global investors as the founders and executives of Startup Sauna, Startup Wise Guys, Startup Highway

and a serial entrepreneur. I have also asked entrepreneurs on their experiences and expectations on

business accelerator programs by conducting a survey.

After the analysis of the results provided by the secondary research and the primary sources

(interviews, survey) we are getting to the conclusion and try to give recommendations for global and

national actors involved in this ecosystem both in the world and in my home country Hungary.

1.1 Problem statement

Business accelerators and their predecessors have proven to be an economic development tool for the

communities they serve. (van Huijgevoort, 2012 p. 4) Growing new ventures is considered as an

essential way of creating new workplaces and boosting economy. At the beginning of a company

lifecycle there are significant obstacles (lack of business experience, lack of capital, validation) and as

a result of that the initial phase of starting a venture could be considered the most critical period of

the venture lifecycle. Accelerator programs are pushing start-ups through their earliest life cycle at an

accelerated pace by helping to learn the basics of business, giving the participants mentoring,

networking, peer support, validation of the business idea and also access to follow-on funding.

Accelerators provide entrepreneurs with the support and funding they need to bridge the path

between ideas and developing working prototypes. (Miller and Bound, 2011)

Business accelerators usually offer seed money and guidance for a small stake, usually between 4 and

10 percent, of the start up company. These programs combine services offered by business incubators

with additional resources and benefits to help start-ups quickly secure funding and receive validation.

Unlike business incubators, accelerators are more selective, often accepting only maximum 10-15

startups per batch. The reduced number of companies offers a more tailored business development

process. (launchause.com, 2012)

The growing number of accelerator programs is the result of the changing economics of starting up.

Costs associated with early-stage tech startups have dropped signifcantly in the past years, making

possible to start a business with small initial money (USD 10 000-USD 50 000) compared to previous

eras of investment in digital businesses.

There is little scientific literature available about seed accelerator programs (eg. Cristiansen, 2009, van

Huijgevoort, 2012, Frimodig, 2012, Barrehag et al, 2012,) despite its significance presence in

technology blogs (eg. Techcrunch) and online business magazines (eg. Forbes). According to

Cristiansen „While significant literature exists on startups and entrepreneurship, these accelerator

programmes are so new that they still consider their own success an open question.”(Cristiansen, 2009

p.5)

In this thesis we are using the following definiton for business accelerators:

10

„Accelerators are organizations that provide cohorts of selected nascent ventures seed-investment,

usually in exchange for equity, and limited-duration educational programming, including extensive

mentorship and structured educational components. These programs typically culminate in “demo

days” where the ventures make pitches to an audience of qualified investors.” (Cohen, 2012 in Forbes

2013)

Business accelerator programs and their effects are changing the pre-seed phase of venture

development lifecycle that needs more research focus from the seed financing and also from the

management perspective of the accelerator program.

1.2 The scope of the thesis

Starting from the fact that there is little academic research on accelerators, there is a wide range of

possible research angles available for this thesis. In order to create the context this chapter outlines a

purpose and aim of the thesis, as well as a research question. Furthermore, the scope of the study is

described as well as how sustainability fits into the investigation.

This goal of the research is to identify the criteria of success for business accelerator from different

point of view. The stakeholders are the startup founders, entrepreneurs programme founders and

external investors. We are not examining other stakeholders as governmental institutions and other

NGO-s because they are out of scope of the study. The track record of the accelerators is too early to

evaluate programs and their effect. On the long run we can evaluate by measuring success factors as

survival rate of the participating ventures and follow-on investment rounds. There are also soft factors

that can be considered as the perceived added value by the participating entrepreneurs.

The main question of the research: What are the key success factors of a business accelerator?

Sub-questions of the research are:

How can we define success in case of the business accelerators?

How do entrepreneurs select business accelerator programs?

What are the expected outcomes of the accelerator programs by the founders, mentors,

investors and by the participating startups?

Is that possible to create a successful business accelerator outside of the major investment

hubs?

The hypothesis of the research is that the success of a business accelerator program is not determined

by the geographical location and the local investment environment where it exists.

By using this hypothesis the goal is to find out whether Hungary could be an entrepreneurial hub by

offering internationally competitive accelerator program for companies at the seed level. We will have

the final conclusion after answering the main- and sub-research questions.

11

1.3 Relevance

At the time of the slow economic recovery there is growing interest in helping startups launch and

succeed that has a positive effect on the whole society by creating new jobs. There are an increasing

number of initiatives seeking to support entrepreneurs as they launch their businesses. (Forbes.com,

2012a)1

The currently available data on accelerators is lacking, and not sufficient therefore at this stage we are

unable to measure the real macroeconomic effects of these initiatives. What can be seen is the

immediate effects on the labour market. 151 registered accelerator programs accelerated 2416

companies that has created 6408 jobs so far according to seed-db.com that is an online repository of

seed accelerators based on Cristiansen’s research (Cristiansen, 2009, seed-db.com, 2013)

Number of registered programs worldwide

151

Companies accelerated 2416

Number of successful exits 124

Sum of exit value $ 1 130 258 600

Total funding $ 1 793 109 821

Jobs created 6408

1. Table The macroeconomic effects of business accelerators

Source: Own edition based on http://www.seed-db.com Date: 03.03.2013.

The database has significant limitation as it has been updated by the accelerators manually and some

of them not consider their presence here a priority therefore in certain cases the data are missing or

out of date. Despite the macroeconomic effects that are visible by seed accelerators it is important to

higlight the fact that because of the lack of data and the short time span we can not evaluate the social

impact made by the accelerators in this early phase. Y Combinator, the flagship accelerator program

operating since 2005, that is why it has provided more funding alone than the other 152 accelerators

together.

1 http://www.forbes.com/sites/kauffman/2012/08/08/evaluating-the-effects-of-accelerators-not-so-fast/

12

All Accelerator without Y

Combinator (N=152)

Y Combinator

Companies accelerated 1937 479

Jobs created 4892 1548

Number of exits 68 57

Funding (USD) 801 695 421 USD 1 009 779 400 USD

2. Table The macroeconomic effects of accelerators without Y Combinator

Source: Own edition based on http://www.seed-db.com 2 Date: 10.03.2013.

Accelerators could be funded by entrepreneurs, wealthy individuals, VCs, business angels or

governmental institutions. Beside the positive macroeconomic effect by job creation business

accelerators are providing the pipeline and the dealflow for Venture Capital investors giving them the

opportunity of identifying the next success stories. Sourcing is a crucial element of the VC investment

process. According to Mahendra Ramsinghani 7% of the investment opportunities are screened, 5%

of them are getting to meetings with VCs, 3% will reach the due diligence and only 1% of the

opportunities end up with investment. (Ramsinghani, 2011)

1. Graph The process of the deaflow

Source: Mahendra Rasmsinghani, The Business of Venture Capital, 2011 Figure 6.2

2 You can find a detailed article on the methodological bias by evaluating seed accelerators: http://www.forbes.com/sites/kauffman/2012/08/08/evaluating-the-effects-of-accelerators-not-so-fast/2/

13

As it can be seen above only 1% of the new investment opportunities ends up with successful

investment from the Venture Capital perspective (Ramsinghani, 2011). Accelerators could help the

newly established companies to get the needed knowledge, network, mentoring and attitude towards

creating successful businesses giving value to the VCs by offering pre-filtered and validated projects

and valuable dealflow.

14

2 Methodology

During the research it was a real challenge to find proven and curated academic literature on the topic.

The thesis built on the knowledge conveyed by the accelerator research of Cristiansen, Van

Huijgevoort, Miller and Bound, Frimodig, Barrehag et al. (Cristiansen, 2009, Van Huijgevoort, Miller

and Bound 2011, Frimodig, 2012, Barrehag et al, 2012) I have also used accredited online newspapers

as New York Times, Financial Times, Forbes, TechCrunch, Wall Street Journal, Inc etc. as secondary

sources.

The study combines quantitative (surveying entrepreneurs as prospective accelerator applicants and

alumni) and qualitative approach (exploratory interviews). The qualitative approach was needed

because of the lack of previous studies on the topic. According to Hirsjärvi et al. the aim of qualitative

research is to create the description of real situations, including the aspect of the manifold view of the

reality. The aim of qualitative research is to explore the topic as comprehensively as possible.

Moreover, the objective is rather to find or reveal the new facts than verify existing propositions.

(Hirsjärvi et al., 2009, Frimodig, 2012).

Because of the limited numbers of scientific literature and research on the topic it was essential to

have primary sources of information about the perception and preferences of entrepreneurs. I have

conducted a survey and asked 94 entrepreneurs including alumni and perspective seed accelerator

participants. A variety of international entrepreneurs were surveyed and in order to have first hand

experiences I have conducted interviews with the founders of the accelerators, key employees and

serial entrepreneurs. This paper is not providing detailed insight into the different sources of

investments because these are considered out of the research scope. The research only deals with

those actors (seed investors, business angels, venture capitalists) that are connected with the business

accelerators either as founders or partners providing follow on investments. I am not evaluating the

effectiveness of involving seed investors and angel investors instead of applying to an accelerator as it

has been considered out of scope.

15

3 Theoretical framework

In order to have a better understanding of the framework and the ecosystem the goal of this section

is to shed light on the concepts and the actors around business accelerators. Therefore this section

defines entrepreneurship and startup as the basic concepts of the study. Both phenomenon has many

definitions in use and there is no single definition and the terms are not consistent that are being used.

This section also describes how we define an entrepreneur, what are the types of the investors and

how the mentors are involved in the processes of growing successful ventures from scratch.

3.1 Describing the concepts

3.1.1 Entrepreneurship

Solving a real existing problem is one of the fundamentals of starting a successful company. Identifying

„pain points” and offer solutions for them by starting up new ventures is a creative process that is

called entrepreneurship.

Entrepreneurship can be defined as the pursuit of opportunity beyond resources controlled3.

According to Steve Blank’s thoughts entrepreneurs could be everywhere. Inside the corporation,

within the government or the leader of a non profit initiative could be named as an entrepreneur. Real

entrepreneurs should do something in a radically new way and solve problems by doing that. Startups

are led sometimes by managers, engineers or scientists but not real entrepreneurs. (Blank, 2012) Brad

Feld define entrepreneur as someone who has co-founded a company. He makes a differentiation

between „high-growth entrepreneurial companies” and „small businesses” He consider both

important but entrepreneurial companies have the potential to be or are high growth businesses

whereas small businesses tend to be local, profitable, but slow-growth organization (Feld, 2012)

In this research we are using the narrower approach that is supported by Brad Feld. He makes a

difference between entrepreneurs and small business owners that are running traditional businesses

(Feld, 2012)

3.1.2 Startup

Defining startup is a big challenge. We often think about two programmers in a garage if we hear this

term. Starting a new company is getting more and more popular, becoming a trend. As a result of the

recent hype around entrepreneurship there are some books, studies, papers on the topic but there is

no widely accepted terminology at all. Definitions vary in terms of the maturity of the company,

commercial track record, etc. In this paper I am taking a look at the potential ways of defining a startup

company and finally create an own terminus technicus for that phenomenon.

3 http://blogs.hbr.org/hbsfaculty/2013/01/what-is-entrepreneurship.html

16

The pre-startup phase, the process from the idea to actual startup phase can be divided into five steps:

intention, product/market fit validation, organization creation, business concept alignment and

market entry. At the beginning of this process, entrepreneurs can be identified as nascent

entrepreneurs (potential entrepreneurs) and later at the final part starting entrepreneurs, firstly

novice entrepreneurs. (Geldren et al., 2005, Frimodig, 2012) If they are running their businesses

successfully and get to exit by an acquisition or an IPO they often start their next businesses becoming

’serial entrepreneurs’.

According to Eric Ries, the father of lean startup concept startup is a melting pot term. „Entrepreneurs

are everywhere. (…) concept of entrepreneurship includes anyone who works within my definition of

a startup: a human institution designed to create new products and services under conditions of

extreme uncertainty. Entrepreneurship is management. A startup is an institution, not just a product,

and so it requires a new kind of management specifically geared to its context of extreme uncertainty.

In fact, as I will argue later, I believe “entrepreneur” should be considered a job title in all modern

companies that depend on innovation for their future growth. (Ries, 2011 p.17)

Steve Blank, the professor of Entrepreneurship at Stanford and a serial entrepreneur using the

following definition "A startup is an organization formed to search for a repeatable and scalable

business model."

According to Steve Blank the keyword of the definition is the search as startups have to adapt to the

needs of the customers and challenge the initial assumptions by testing all their hypothesis. Therefore

the goal of the startup is to search and to find the scalable business model that serves the market

needs and solve the customers’s pain points while enables profitable operation and growth.

Dave McClure the Founder of 500 Startups, a leading accelerator has identified the following formula

STARTUP = Hacker + Hustler + Designer4

According to the European Venture Capital Association startup could be defined as „Companies that

are in the process of being set up or may have been in business for a short time, but have not sold their

product commercially.” (evca.eu, 2012)

Based on the definitions provided above this paper using the term startup as the following:

Start-up companies are businesses with high growing potential and global scalability by solving a real

customer need and continously looking for the most successful business model.

4 Based on TechCrunch interview with Dave McClure, the Founder of 500 Startups: http://techcrunch.com/2011/04/10/dave-mcclure-on-500-startups-if-sequoia-is-the-yankees-were-the-oakland-as/ Dowloaded: 29.04. 2013.

17

3.2 The actors of the entrepreneurial ecosystem

Entrepreneurs running startups, are existing within the entrepreneurial ecosystem that contains

investors, mentors, accelerators, governmental institutions, educational institutions and other actors

of the society. In this paper I put the accelerator in the middle of the ecosystem as you can see below.

The graph shows that all the actors are interconnected. The accelerators provides networking access

to entrepreneurs as they are supported by mentors during their program. The mentors get access to

promising startups and up-to-date knowledge in their industry. On the other hand they provide

branding support for the accelerators by let them use their name for promotions in order to attract

the best startups. Having the most promising companies provide a dealflow for investors that could

result in capital raise and follow on investment after the core accelerator program.

2. Graph The entrepreneurial ecosystem, Own edition based on Barrehag et al, 2012

18

3.2.1 Entrepreneurs

Accoding to Merriam-Webster dictionary entrepreneur is the “one who organizes, manages and

assumes the risks of a business or enterprise (Forbes, 2012)5. In this research we are using the term

entrepreneur according to Brad Feld’s definition found in the book called Startup Communities:

Building an Entrepreneurial Ecosystem in Your City (Feld, 2012) According to the founder of TechStars

entrepreneurs are running globally scalable startups. We consider small business owners out of scope

in this paper, therefore we are focusing on entrepreneurs running their business that has real added

value and the business can be scalable. According to Hemingway and Balint, the idea of a startup is

based 47% on the previous experience of the entrepreneurs as they are tend to choose a problem to

be solved within they feel themselves comfortable (Hemingway-Bálint, 2004)

3.2.2 Investors

Running a startup is associated with high risk and often requires more funding than the founders can

provide themselves by boostrapping. Therefore they have to find investors that can provide them

capital in exchange for equity (Arundale, 2007). According to the glossary of the Princeton University

investor is someone who commits capital in order to gain financial returns6. We can make a distinctions

among the investors based on the maturity of the company where they invest and they can be also

categorized whether they are establishing legal entities like venture funds or angel funds by becoming

formal investors or staying informal and investing their own money in companies. Angel investors,

seed funds and venture capitalists are the most associated types of investors with business

accelerators. In this reseach we are using the following categories:

Seed investor

Seed investor is providing the money that is used to move on with the idea and start a business – to

provide the first set of premises or to patent a piece of intellectual property or develop a prototype. It

is often the financial contribution of the entrepreneur or his family or friends to getting the enterprise

off the ground (3F financing). It can also be provided by specialized funds (frequently affiliated to a

university or a government ‘enterprise’ initiative) or from private individuals or philanthropic trusts. It

will usually require continuing equity participation in the business, but on vastly diluted terms; if it

doesn’t, because for instance it comes in the form of a government grant, then in consequence the

term ‘capital’ is sometimes misleading. (Bloomfield, 2005)

5 Source: http://www.forbes.com/sites/brettnelson/2012/06/05/the-real-definition-of-entrepreneur-and-why-it-matters/ Dowloaded: 29.04. 2013. 6Source: http://wordnetweb.princeton.edu/perl/webwn?s=investor Dowloaded: 29.04. 2013.

19

Business Angel

Angel investors, angel funds and affiliated forms of seed capital provide an early access to investment

opportunities for ventures. An angel investor or a business angel is an affluent individual or a group of

individuals that provides capital for a business start-up usually in exchange for convertible debt or

ownership equity. (Forbes.com, 2012b) Angel investor groups are composed of wealthy individuals or

hign-net-worth individuals (HNWIs) who pool resources and investment expertise. The number of

active angels in the United States is reported to be about 125 000, between 10 000 and 15 000 angels

are belong to angel groups (Ramshinghani, 2011). According to Ramshinghani, over 550 angel groups

exist worldwide and nearly 300 of which are based in the United States.

Boosting business angel investments is really important especially in Europe where seed accelerator

programs help to fill in the gap in start-up financing between friends and family and formal venture

capital.

Business angel investments can range from USD 5 000 to USD 500 000 or more. At the early stage of

the business, angels become very real and serious investors and owners with high expectations looking

for solid results and willing to actively involve themself in setting up the company.

Venture Capital

Most business people know something about venture capital or more likely some of the myths about

venture capital. This invaluable actors are often the currency of business conversation, but much of

the details what happens during an investment is unknown by most of the people. Since nature abhors

a vacuum, myth rushes in to fill the gap left by the absence of knowledge according to Bloomfield

(Bloomfield, 2005)

Venture capital is the originated from the United States in the 1960s and 1970s, when individuals put

money behind bright ideas – that later grew into disruptive businesses like Apple Computers, Cisco

Systems, Netscape, – without any certainty of return. It is closer to seed capital than other forms of

funding. Venture Capital is the sub-section of private equity. The portfolios of venture capital investors

typically involve risk taking with a potentially expected high return. They are often organized as limited

liability companies with the investors as partners of the corporation (Privco, 2012). VCs invest in

companies in exchange for equity and provides the startup with access to a wider network of

specialists. (Barrehag et al, 2012) According to Berglund (2011), VCs try to get to know the startups as

a part of their due diligence process. The reasoning is that they want to be able to say no to potentially

poor deals as soon as possible. In addition, the purely technical skill of the teams is evaluated and their

previous accomplishments are assessed (Privco 2012). Venture money is the supposed plug for the

equity gap. (Ramsinghani, 2011) Accelerators can provide validated and pre-screened dealflow for VCs

as Venture capital industry has high administrative and management costs and high risks.

As a result of these trends VCs are having crucial part of the success of the accelerators by providing

follow-on funding after the accelerator program.

3.2.3 Mentors/advisors

20

Mentors are experienced entrepreneurs or investors who contribute time, energy and knowledge to

startups and can be a key part of a startup community. (Feld, 2012) There is a difference between

mentor and advisor as the advisor has an economic relationship with the company he is advising. The

mentor is helping startups without a clear set of outcome goals or economic rewards. Mentors play a

crucial role in accelerators by providing guidance and ongoing support for the teams.

Well known mentors can bring value to an accelerator besides working with startups by marketing and

exposure that can result in attracting the most appropriate startups. As a consequence, by helping to

recruit the best startups the mentors will eventually promote the ambition of the accelerator to meet

the investor expectations, namely well prepared startups (Barrehag, 2012 p45)

21

4 The new economics of startups

4.1 How companies grow?

Before explaining what the phenomenons are behind the growing numbers and importance of startups

it is worth to define the phases that organizations go through as they grow. All kinds of organizations

experience these challenges for a certain extent. Each growth phase is made up of a period of relatively

stable growth, followed by a "crisis" when major organizational change is needed if the company is to

carry on growing. (Greiner, 1988)

This is not a negative phenomenon rather the needed structural change in order to further develop

the company. It is more like a ’turning point’ when the company needs transition. We consider Phase

1 and Phase 2 in the scope of the study as they are the typical startup lifecycles.

3. Graph How companies grow? Based on Greiner 1988 Source: www.exponentialtraining.com

Phase 1 is the stage when entrepreneurs who founded the firm are heavily involved in creating

products and opening up markets. There aren't many staff, so informal communication works fine,

and rewards for long hours are probably through profit share or stock options. However, as capital is

injected production expands and more staff join, there's a need for more formal communication. This

phase ends with a Leadership Crisis, where professional management is needed. The founders may

change their style and take on this role, but often someone new will be brought in. (Frimodig, 2012)

22

At the Phase 2 growth continues in an environment of more formal communications, budgets and

focus on separate activities like marketing and production. Incentive schemes replace stock as a

financial reward. However, there comes a point when the products and processes become so

numerous that there are not enough hours in the day for one person to manage them all, and he or

she can't possibly know as much about all these products or services as those lower down the

hierarchy. (Frimodig, 2012)

This phase ends with an Autonomy Crisis: New structures based on delegation are called for.

At the seed stage focus is on the business conception and idea development. The startup phase

emphasizes product or prototype development, whereas early growth consists of small-scale

commercialization and focus is on scalability. (Kubiš, 2009, Frimodig, 2012)

4. Graph The transition from a startup to a company, Source: Blank, 20137

There is also a transformation from the scalable startup that is looking for the right business model to

a company that executes the suitable business model at this stage as you can see on the 4. Graph.

Seed and startup stages are usually funded by informal investors. “Traditionally, informal seed money

has been gathered from 3Fs (founders, family and friends or fools) or 4Fs (founders, family, friends and

foolhardy investors) that have close relationships with founders and they believe that the company can

progress well based on the founders’ experience and capabilities.” (Frimodig, 2012 p42.) Moreover, at

the startup phase investors are still informal and are defined as informal venture capitalists. The main

difference compared to informal seed money is that formal venture capital investors invest in unknown

companies without close personal involvement. (Frimodig, 2012)

Generally, informal venture capitalists are angel investors; micro angels, business angels and super

angels. At later growth phases funding is raised from formal investors such as venture capital

companies. (Rasila, 2004). Development stages of growth, cash flow and sources of finance are

visualized below (Frimodig, 2012)

7 Source: http://blogs.wsj.com/accelerators/2013/04/01/steve-blank-should-i-get-an-m-b-a/ Dowloaded: 29.04. 2013.

23

5. Graph The investment need and lifecycles in Frimodig, 2012

4.2 The early stage startup challenges

Throughout the stages of the development the basic needs of the company are also differ. The startups

have a lack of knowledge and there are difficulties in finding the working business model, have access

to the market and raise funding after their launch. (Harding, 2002; Rasila, 2004.) Filling the gaps

demands that information and knowledge flow between startups and investors. Business angels can

fill the gap through a supportive approach, including mentoring, providing expertise, and also mental

and financial support. (Harding, 2002, Frimodig, 2012) Business accelerator also can contribute by

helping founders to bridging the gap between starting up and the market reach.

Startups have knowledge and an equity gap in the early stage of their existence. At the beginning the

founders usually need help on product and customer development when they are looking for the

suitable and sustainable business model. Obviously the more knowledge and experience they have,

the less support is needed. Parallelly with that, the need for capital is arising as the company is

developing and reaching the milestones step by step. In this development process the emerging need

of seperating different functions as IT, product management, marketing, sales, business development,

etc is appearing.

24

6. Graph Equity gap vs. competence gap (Rasila, 2004; Ala-Mutka 2005) in Frimodig, 2012

4.3 Changes in the business environment

As a result of the globalization and market- oriented business thinking, domestic markets have lost

significance and businesses going to global markets from day one. Operating in an extremely complex

environment makes the starting up process even more challenging as a result of different cultures,

politics and technological solutions. (Hisrich, 2010, Frimodig, 2012)

Globalization is a natural process that could be defined as “universal mechanism that grew out of the

naturally occurring order-exchange process”. Globalization has roots deep in history, but nowadays its

pace has been accelerated. (Beer, 2011 in Frimodig, 2012 p13). The global business environment has

changed according to Frimodig (Frimodig, 2012) during the last few decades and therefore has affected

the internationalization process of companies leading to the emergence of born globals in the 1990s.

(Laanti et al., 2007. in Frimodig, 2012)

The global aspiration of the startups is demanding management challenge because of the unbalance

between goals and resources. Usually the relatively young and inexperienced founders’ lack of relevant

knowledge, which is needed to gain high- growth in the global market. (Knight and Cavusgil, 2004;

Gabrielsson, 2007, in Frimodig, 2012). However, enthusiasm and vision can give limited compensation

in filling the knowledge gap (competence gap). The startup should seek appropriate resources and

knowledge outside the company to cover the knowledge gap. (Frimodig, 2012)

According to P. Miller and K. Bound (Miller, Bound, 2011) the changes in the environment had

significant effect both on the startup side and on the investor side as well. Those are decraising startup

costs, better access to customers and more efficient monetisation by using different online channels.

According to P. Miller and K. Bound „the falling costs of hardware and software (are) one of the main

25

drivers in the proliferation of startups over the last five years and an important factor in the growth of

accelerator programs” (Miller, Bound, 2011 P. 21.)

The cost of launching a start-up is decreasing

As a result of the technological developments, the new ICT business models and the decreasing service

costs startups can start their operation with rented resources instead of having significant initial costs

by hardwares for example cloud services could be a cost effective solution instead of buying a server

and paying for the maintenance in-house. These alternatives are affordable compared with the solid

hardware infrastructure needed before the dot com bubble to start a new company.

Dot-com Era Lean startup era

Buy own servers and drive them to the

datacenter

Using services from the cloud

Buying software licenses for all the employee Activate Google Apps for your domain

Agree and sign an office lease Working from/meeting at a coworking space

Launch a billboard campaign Google Adwords or Facebook advertisments

Take years to build software and then release Iterative agile software development with

daily updates

3. Table Starting up in the dot-com era versus the lean startup era (Based on Miller, Bound, 2011)

The trend turning towards open source softwares also helped a lot by making the startup more „lean”.

Licenses for software used to cost a lot, now there are alternative tools in most cases for free or very

reasonable prices.

Another favourable trend is the pay as you go business model or monthly subscriptions for online

services like online CRM, project management, workflow, cloud ERP and other related softwares and

services.8 Small companies should not have to pay significant money on upfront. Certain sofwares are

available in the cloud for them that would not be affordable otherwise. Startups can start using

services for free and if they decide to use the premium functions they can pay a monthly fee.

Leased offices could be replaced by working in coffee houses or paying daily or hourly fees at co-

working spaces that gives extra flexibility for startups especially at the very beginning of their customer

validation and development process. Meeting room rental services are also available at the co-working

offices.

The initial costs of setting up a business has changed dramatically in the last couple of years. The major

cost of early-stage companies are not related to technology nowadays but more like human resource

expenses. One of the initial problems for founders how to cover their daily expenses while they are

8 You can find cost effective tools for startups in the following article: http://www.inc.com/tom-searcy/start-up-on-a-budget-14-cheap-tools.html Dowloaded: 29.04. 2013.

26

developing the first product, trying to acquire new customers or working on finding investors. (Miller,

Bound, 2011)

Easier to find and address new customers

Not just the decreasing cost of the starting up process that has changed in the last decade but the

customer acquisition methods and costs too. There are new online channels of reaching the target

audience and these channels also give better results based on the better measurability and more

effective targeting. By using Google Adwords, Facebook or LinkedIn advertisements it is possible to pre

validate products, services on low budget and continuing spending just on the effective channels,

campaigns. There is another reason starting up is cheaper as competitive analysis is getting easier and

cheaper now by using online channels like LinkedIn, AngelList or Crunchbase on the competititors

funding, employee count, and sales.9

Getting the revenue inflow is easier

Beside the growing number of potential customers by the result of the easier starting up, reach and

targeting there are effective ways on getting paid for products and services via direct payment

transactions through e-commerce channels, app stores or subscription based models. Based on these

facts online channels that makes a much more cost effective alternative than traditional commercial

channels.

Changes in the investment market

The economics of startup companies changed dramatically and the entry barriers to the technology

intensive markets have decreased significantly during the past decade that can be considered as one

of the main factor behind the growth of the business accelerator programmes.

Beside the lower costs of starting up a venture, the venture capital industry is having hard time to

adapt and find their place in the ecosystem. VC has retreated from early-stage investments,

particularly in Europe, and the way of early-stage investment is changing. In the US a number of multi-

stage investment funds have emerged, but in Europe, bar a few newly developed ‘feeder funds,’ like

Index Seed and Atomico, an investment gap is growing both the US and Europe, business angels have

stepped in to fll this gap since 2000. (Miller, Bound, 2011)

Yet despite positive signs that the gap in venture performance between the US and Europe is

narrowing, it is likely that the gap will widen again as US investors are set to reap the social media

boom. “The problem with the European investment market is not that European investors aren’t as

good at growing companies, but that the environmental conditions, and particularly the pipeline of

companies is inadequate. This is proved by venture performance data – UK VCs perform better than

average when they invest in the US and US VCs perform worse than average when they invest in the

UK.” (Miller, Bound, 2011 p23.)

9 Source: http://davidquail.com/2012/05/11/another-reason-starting-up-is-cheaper-now/ Downloaded: 29. 04. 2013

27

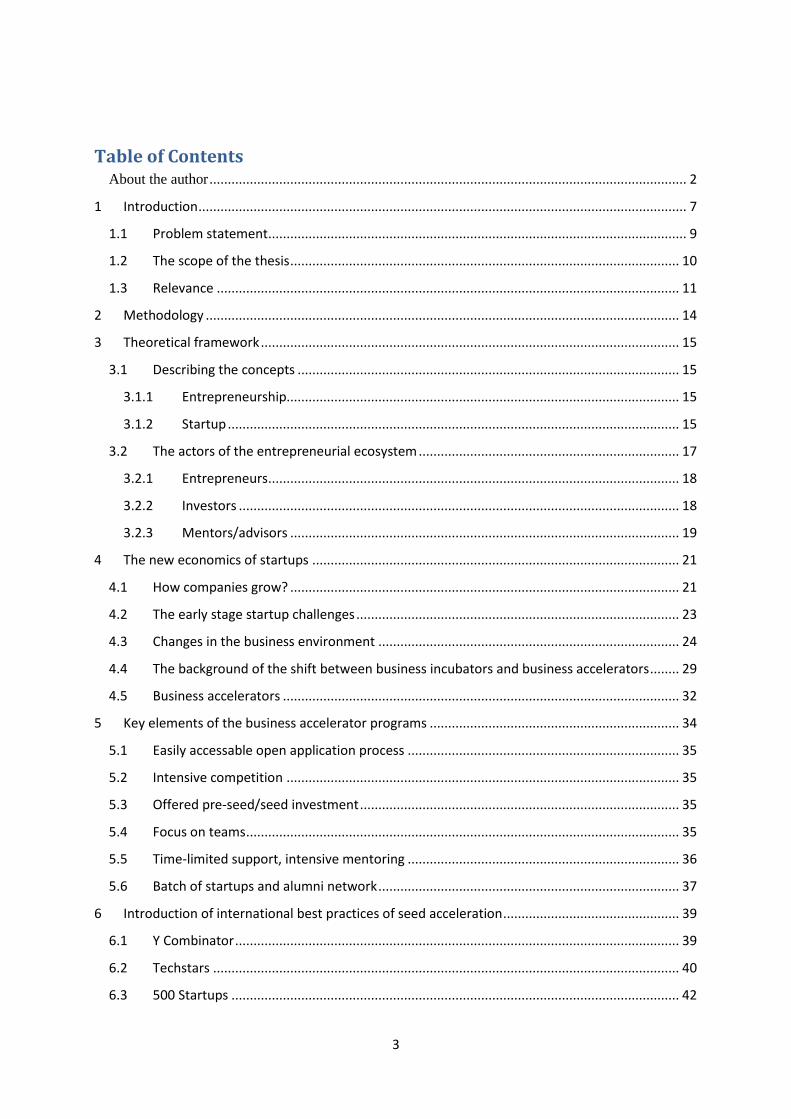

The fundraising is critical for the growth of a born global company. Generally the companies that have

gained external funding grow faster. On the other hand, investors and venture capitalists search

founders that are able to create global visions, have international business experience and global

networks, and therefore competence, knowledge and experience are all important. (Laanti, et al.,

2007) (Frimodig, 2012)

Technically, in the early phases of a born global company, the product development has a significant

role. It is crucial to have a clearly focused product portfolio and keep the customer focus. (Barringer et

al., 2005, Gabrielsson, 2007, Frimodig, 2012) The right combination of engineers, designers, marketing

and sales makes a team an interesting investment targets.

As a result of the costs of starting a new venture coming down, venture capitalists increasingly making

smaller seed investments and seed investments in internet companies are becoming more prevalent

when it comes to early stage investing.10

7. Graph Seed deals by vintage quarter Source: www.cbinsights.com

On the other hand, regarding the follow-on investments for seed funded companies there is also an

interesting trend. The next investment level after the seed funding called Series A that remains

relatively steady in the past few years despite the boom of the seed investments. The gap between

the two funding round called the Series A Crunch that is an excessive demand for a limited supply of

10 Source: http://www.cbinsights.com/blog/trends/seed-investing-report Dowloaded: 29.04. 2013.

28

Series A financings. This trend would mean that “many startups will be orphaned and that some

investors will lose their money”. (cbinsights.com, 201311)

8. Graph Series A Deals by Vintage Quarter Source: www.cbinsights.com

The Series A crunch is one of the biggest challenge that the early stage VCs and business accelerators and their portfolio companies are facing with in the next few years.

11 Source: http://www.cbinsights.com/blog/trends/seed-investing-report Dowloaded: 29.04. 2013.

29

4.4 The background of the shift between business incubators and business

accelerators

The seed accelerator (or business accelerator) derives many of its characteristics from the business

incubator. Therefore it is recommended to start the description by introducing the concept of

incubation.

Incubators, the predecessors of the business accelerators have proven to be an economic development

tool for the communities they serve since 1959. The general idea behind the incubation concept to

create an institutionalized environment that assists and enables startup companies and business ideas

to grow. (Barrehag et al, 2012) Incubated companies have created numerous jobs, thereby increasing

the tax base, occupying additional commercial real estate space, contributing to local business

infrastructures and creating even more jobs in other industry sectors (van Huijgevoort, 2012 p4.

Wiggins & Gibson, 2003)

Business incubators are institutions that support entrepreneurs and the process of starting a venture,

helping to increase survival rates for innovative companies and also for small and medium enterprises.

The process of developing a startup company within an incubator can be extensive and could take

several years. (Barrehag et al, 2012)

There is no widely accepted standard definition of business incubation. There are several definitions

available in the academic literature and just as many have been adopted by industry associations and

policymakers in different countries, reflecting local cultures and national policies. According to

Hamdani, Germany targets innovative start-ups, while France and the Netherlands promote the

university-incubator model. (Hamdani, 2006)

The American National Business Incubation Association defines a business incubator as “an economic

development tool designed to accelerate the growth and success of entrepreneurial companies through

an array of business support resources and services. (Bollingtoft, 2012) According to Sherman &

Chappell (Sherman & Chappell, 1998), these support services include assistance in developing business

and marketing plans, building management teams, and obtaining capital and access to a range of other,

more specialized, professional services. They also provide flexible space, shared equipment and

administrative services

The main purpose of a business incubator, is to create a favorable business environment for start-up

firms to compensate for the lack of financial, knowledge and networking resources they generally have

(Commission, 2002). The start-up firms in an incubator are provided offices for moderate price, shared

equipment, administrative services (legal advisory, accounting etc.) and other business related

services. (Bollingtoft, 2012).

30

9. Graph The Role of Business Incubators Based on: Sahay, 2004,

According to Sahay the author of the Role of Technology Business Incubator, Angel Investor and

Venture Capital Fund in Industrial Development ’Business incubators accelerate the successful

development of entrepreneurial companies through an array of business support resources and

services, developed or orchestrated by incubator management, and offered both in the incubator and

through its network of contacts. A business incubator’s main goal is to produce successful firms that

will leave the program financially viable and freestanding. These incubator graduates have the

potential to create jobs, revitalize neighborhoods, commercialize critical technologies and strengthen

local and national economies.’ (Sahay, 2004 p5.)

The US Small Business Administration defines incubators as: physical facilities that provide new firms

with the supportive network necessary to increase their probability of survival during the early years

when they are most vulnerable. (Cornelius, 2003)

Business incubators are institutions founded to be the catalysts of the entrepreneurial process, by

helping to increase survival rates for innovative startup companies. Entrepreneurs with feasible

projects are selected and admitted into the incubators, where they are offered specialized resources

and servicesthat might include such elements as (Sahay, 2004):

Providing available spaces (office, production space, laboratories for discounted renting fee)

Consulting and Management services (consulting for business planning, financial

management, taxes, marketing, advertising, advice on intellectual property, access to funding)

Administrative services (juridical assistance, accounting, shared bookkeeping)

31

Logistic support (office services, utilities, usage of equipments, IT services)

Technical assistance (laboratory services, instruments, research services, assistance with early

engineering & prototype, quality management services, technological services)

Business networking (access to different actors, institutions, universities, corporates, chamber

of commerces, investors)

Training and education (professional business training courses, fine tuning business

management skills (planning, organizing, directing & controlling), coaching, mentorship and

personnel training services, entrepreneurial training programs)

(Based on Sahay, 2004, Van Huijgeevort, 2012, Vasilescu, 2008)

Efforts to determine how incubators assisted firm development quickly became an examination of

incubator categories. Based on the extent of value added services there is a continuum from real estate

incubators to purely business development focused programs. (Cornelius, 2003, van Huijgevoort, 2012,

Bøllingtoft & Ulhøi, 2005; Christiansen, 2009; Commission, 2002; Grimaldi & Grandi, 2005; Hansen,

Chesbrough, Nohria, & Sull, 2000.)

10. Graph Continuum of added value services provided by incubators and accelerators (Price, 2004 in Frimodig, 2012)

In short, there has been a shift from real estate provision and appreciation to for-profit enterprise

development, as the main starting point of business incubators (Aerts et al., 2007 in van Huijgevoort,

2012).

At the time before the dot-com bubble in 2000, a lot of networked incubators12 started with a focus

on IT-based startups. These very specialized and received significant funding from investors at a rapid

12 Networked incubator: A networked incubator is a type of business incubator model which is a suited model of the Internet economy. The ‘Networked Incubator’ model emphasizes the dynamic working environment, with start-up firms constantly working together,and informal interactions of co-founders and participants (van Huijgevoort, 2012)

32

pace. The model was based on large investments in single projects, which suited venture capital and

had previously been successful (Miller, Bound 2011).

As the dot-com bubble inflated, many promising IT-based were unable to generate revenue and

collapsed (Blank 2005). Within two years starting from 2000 to 2002 NASDAQ lost 80% of its former

value because of the dot-com bubble. This collapse in valuation meant that many investors lost their

capital in companies that had only succeeded in burning through their money without creating anything

of value. (Barrehag et al, 2012) Critics of the networked incubator investment model coined the term

“incinerator” to emphasize the problems of investing large amounts of capital at once without

demanding measurable results (Miller, Bound 2011), (Barrehag et al, 2012).

As the investment climate began to recover a few years later, the new frameworks and approaches

initiated by entrepreneurs such as Paul Graham started to gain the attention of the investors. Key

changes in the model were shorter incubation cycles, as most IT based products can be developed

faster than physical products. (Miller, Bound 2011)

5 years after the peak of the dot-com bubble Paul Graham launched Y Combinator in Silicon Valley.

This represented a business idea that had a lot of common characteristics with traditional incubator

but there were also significant process innovations. Most importantly, the acceleration period is

usually no longer than three months that is suitable for ICT related applications. In addition, the cost

and structure of investments differ in that they are much smaller in each individual startup. (Barrehag

et al, 2012). Y Combinator for instance offers twice a year 40 companies 11-20 000 USD investments

for 6-7 percentage of its stake.

4.5 Business accelerators

The traction of business accelerators is much shorter, originating from 2005 (Christiansen, 2009; Miller

& Bound, 2011). A very small amount of scientific literature exists on business accelerators, however

the growth in the number these programs is significant. According to Bloomberg Businessweek, in

2011 around 110 business accelerator programs were operating around the world (Van Huijgevoort,

2012) and for 2013 it has grown to 153 (seed-db.com, 2013).

According to Susan Cohen who is a researcher at the University of North Carolina at Chapel Hill:

Accelerators are organizations that provide cohorts of selected nascent ventures seed-investment,

usually in exchange for equity, and limited-duration educational programming, including extensive

mentorship and structured educational components. These programs typically culminate in “demo

days” where the ventures make pitches to an audience of qualified investors. (Forbes.com, 2012)

33

11. Graph Different types of accelerators, Source: Frimodig, 2012

34

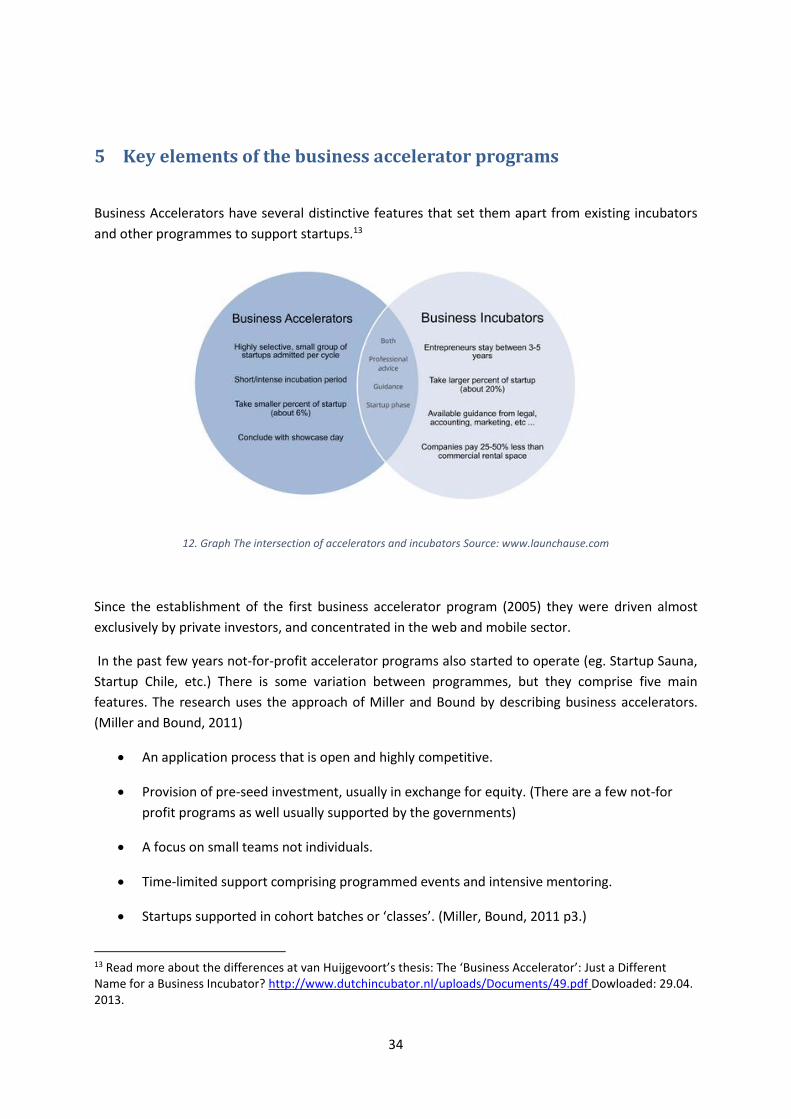

5 Key elements of the business accelerator programs

Business Accelerators have several distinctive features that set them apart from existing incubators

and other programmes to support startups.13

12. Graph The intersection of accelerators and incubators Source: www.launchause.com

Since the establishment of the first business accelerator program (2005) they were driven almost

exclusively by private investors, and concentrated in the web and mobile sector.

In the past few years not-for-profit accelerator programs also started to operate (eg. Startup Sauna,

Startup Chile, etc.) There is some variation between programmes, but they comprise five main

features. The research uses the approach of Miller and Bound by describing business accelerators.

(Miller and Bound, 2011)

An application process that is open and highly competitive.

Provision of pre-seed investment, usually in exchange for equity. (There are a few not-for

profit programs as well usually supported by the governments)

A focus on small teams not individuals.

Time-limited support comprising programmed events and intensive mentoring.

Startups supported in cohort batches or ‘classes’. (Miller, Bound, 2011 p3.)

13 Read more about the differences at van Huijgevoort’s thesis: The ‘Business Accelerator’: Just a Different Name for a Business Incubator? http://www.dutchincubator.nl/uploads/Documents/49.pdf Dowloaded: 29.04. 2013.

35

5.1 Easily accessable open application process

Accelerator programmes have web-based application processes and they are expecting applications

from teams coming from anywhere in the world. The application process is simple, by keeping minimal

paperwork needed. The form often focuses more attention to the founders and the team rather than

the business idea and concept. If the team managed to get through the pre-selection, they are invited

to an interview that are pretty short (10-20 minutes in most cases). The process of selection from the

application deadline through to a decision is often very short compared to many routes to funding or

business education programmes. (Miller, Bound, 2011)

5.2 Intensive competition

Programmes are highly selective and exclusive, involving serial entrepreneurs, investors, experts to

choose the most talented teams that worth to participate in the accelerator program. Most of the

accelerators are having applicant success ratio of less than one in ten. Accelerator programmes often

invest considerable time in speaking and running events internationally to reach out to potential

applicants to maintain the quality of the applicant pool (eg. Startup Sauna, Seedcamp). For high profile

accelerators, less than 1 per cent of applicants will be successful.

Accelerators usually decide on a limit on the number of startups they can support in each cohort based

on the amount of office space they have available or the number of mentors and operational staff

needed to handle larger numbers. One of the most successful one, Techstars has decided to work with

ten companies per batch whereas Y Combinator has been less constrained. They now fund over 60

companies per cohort.

5.3 Offered pre-seed/seed investment

The investment provided by accelerator programmes is different, in most cases it depends on how

much it costs per co-founder to live during the period of the programme and for a short period

afterwards. Programmes usually provide a minimum of USD 20 000 and a maximum of USD 50 000

investment during the first three months. This can be in the form of a non refundable grant, convertible

note or an equity investment. (Miller, Bound, 2011)

5.4 Focus on teams

Accelerator programs are focusing on teams not individuals. They usually prefer teams not larger than

three or four person. Larger teams needs more initial investment to cover the living expenses and

make the co-founders ready to work on solely on the startup.

36

5.5 Time-limited support, intensive mentoring

Accelerator programmes provide support for a set period of time – usually between three and six

months. According to Miller and Bound this is linked to the decreasing length of time it takes to launch

a web startup, but it’s also about creating a high pressure environment that will drive rapid progress.

(Miller and Bound, 2011)

While a number of programmes do offer ongoing support for graduated companies there is always a