GAO-07-403 Natural Hazard Mitigation: Various Mitigation ...

1Power for All by 2012

India: Growing Energy Needs

and

Mitigation Options

Gireesh B. Pradhan, IASAdditional Secretary,

Ministry of Power, Government of India.5th May 2008

2Power for All by 2012

Eradicate extreme Poverty and Hunger.

Achieve universal primary education.

Promote gender equality and empower women.

Reduce child mortality.

Improve maternal health.

Combat HIV/ AIDS, malaria and other diseases.

Ensure environmental sustainability.

Develop a global partnership for development.

According to UN, all the MDGs, except for the last one, have links with

Energy Services (including electricity)

Millennium Development Goals (MDGs)

3Power for All by 2012

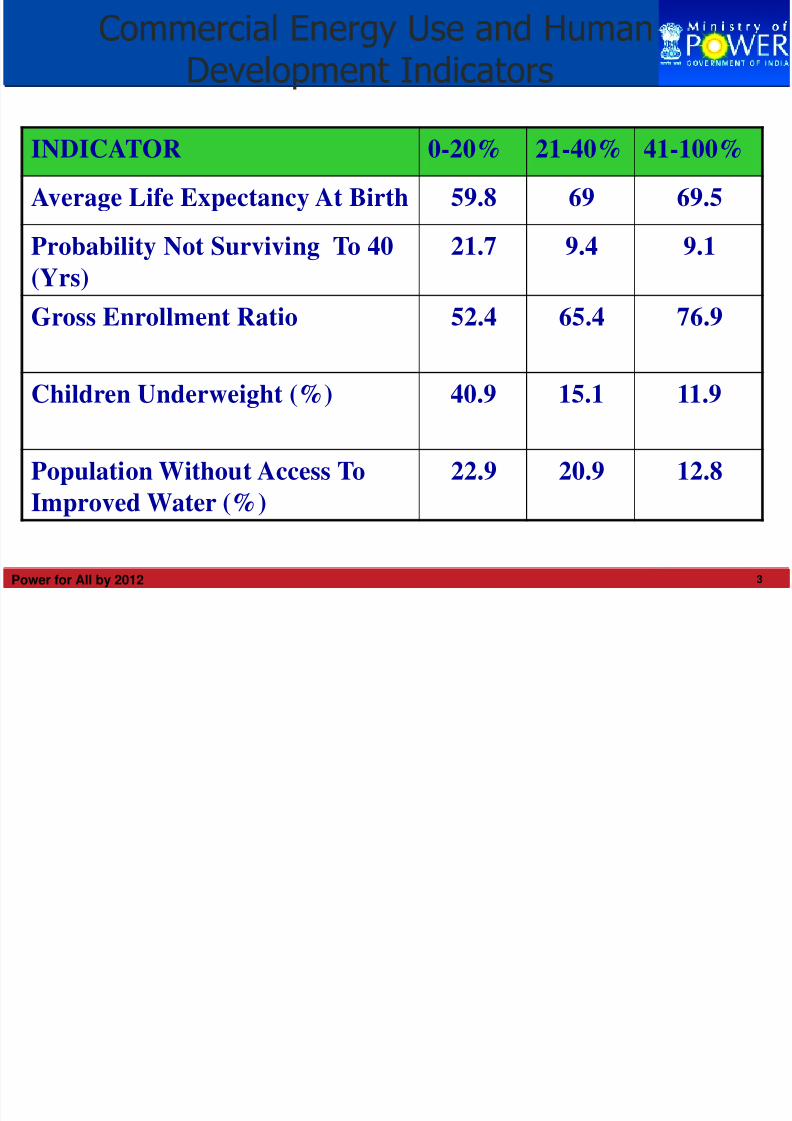

Commercial Energy Use and HumanDevelopment Indicators

INDICATOR 0-20% 21-40% 41-100%

Average Life Expectancy At Birth 59.8 69 69.5

Probability Not Surviving To 40

(Yrs)

21.7 9.4 9.1

Gross Enrollment Ratio 52.4 65.4 76.9

Children Underweight (%) 40.9 15.1 11.9

Population Without Access To

Improved Water (%)

22.9 20.9 12.8

4Power for All by 2012

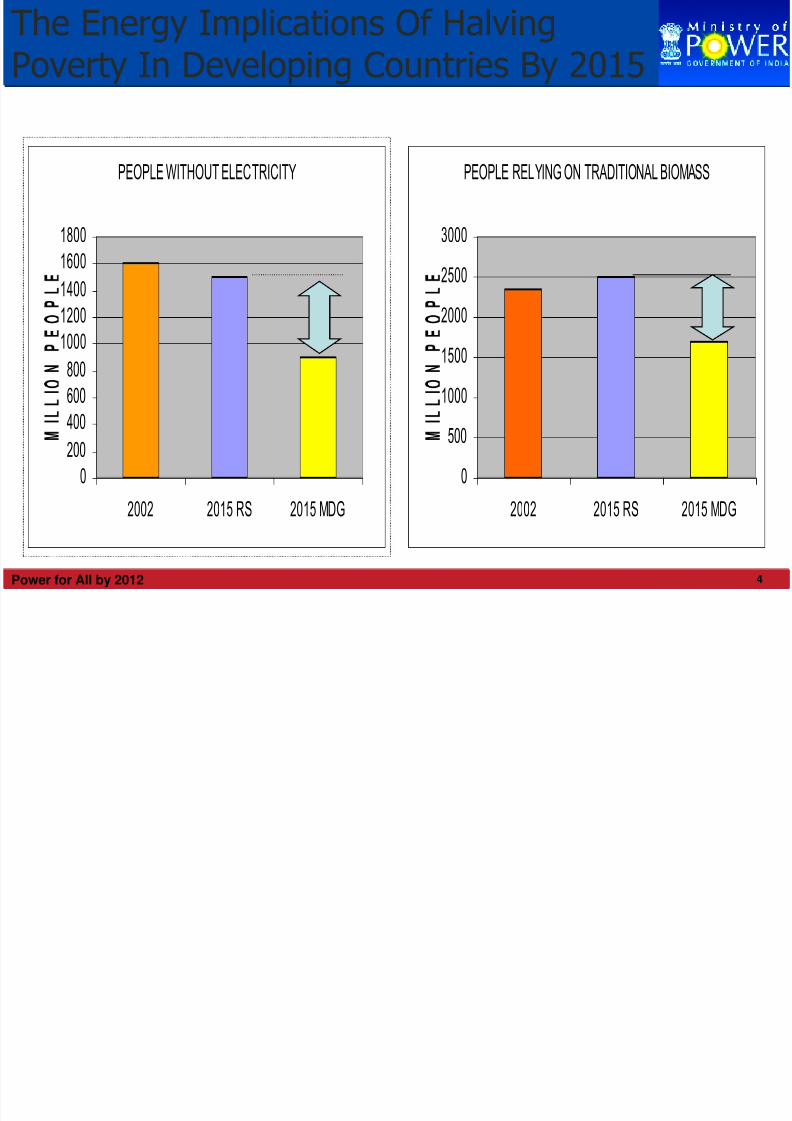

The Energy Implications Of HalvingPoverty In Developing Countries By 2015

PEOPLE WITHOUT ELECTRICITY

0

200

400

600

800

1000

1200

1400

1600

1800

2002 2015 RS 2015 MDG

PEOPLE RELYING ON TRADITIONAL BIOMASS

0

500

1000

1500

2000

2500

3000

2002 2015 RS 2015 MDG

5Power for All by 2012

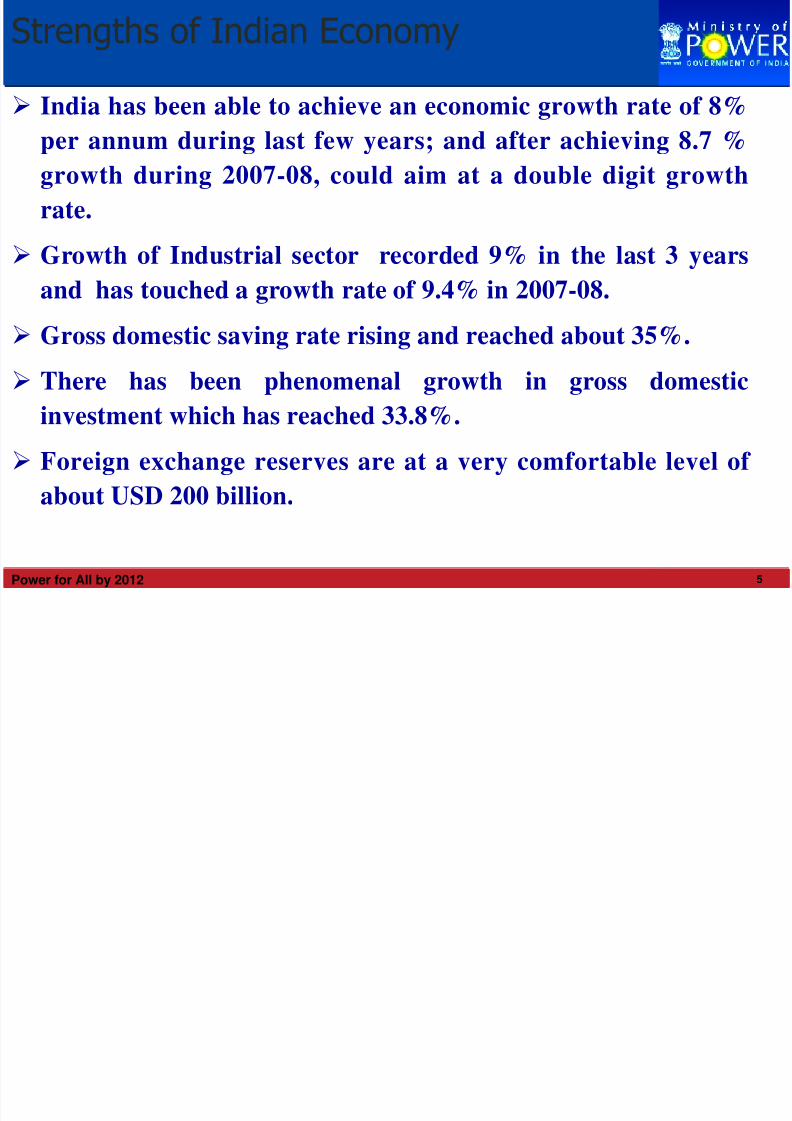

India has been able to achieve an economic growth rate of 8%

per annum during last few years; and after achieving 8.7 %

growth during 2007-08, could aim at a double digit growth

rate.

Growth of Industrial sector recorded 9% in the last 3 years

and has touched a growth rate of 9.4% in 2007-08.

Gross domestic saving rate rising and reached about 35%.

There has been phenomenal growth in gross domestic

investment which has reached 33.8%.

Foreign exchange reserves are at a very comfortable level of

about USD 200 billion.

Strengths of Indian Economy

6Power for All by 2012

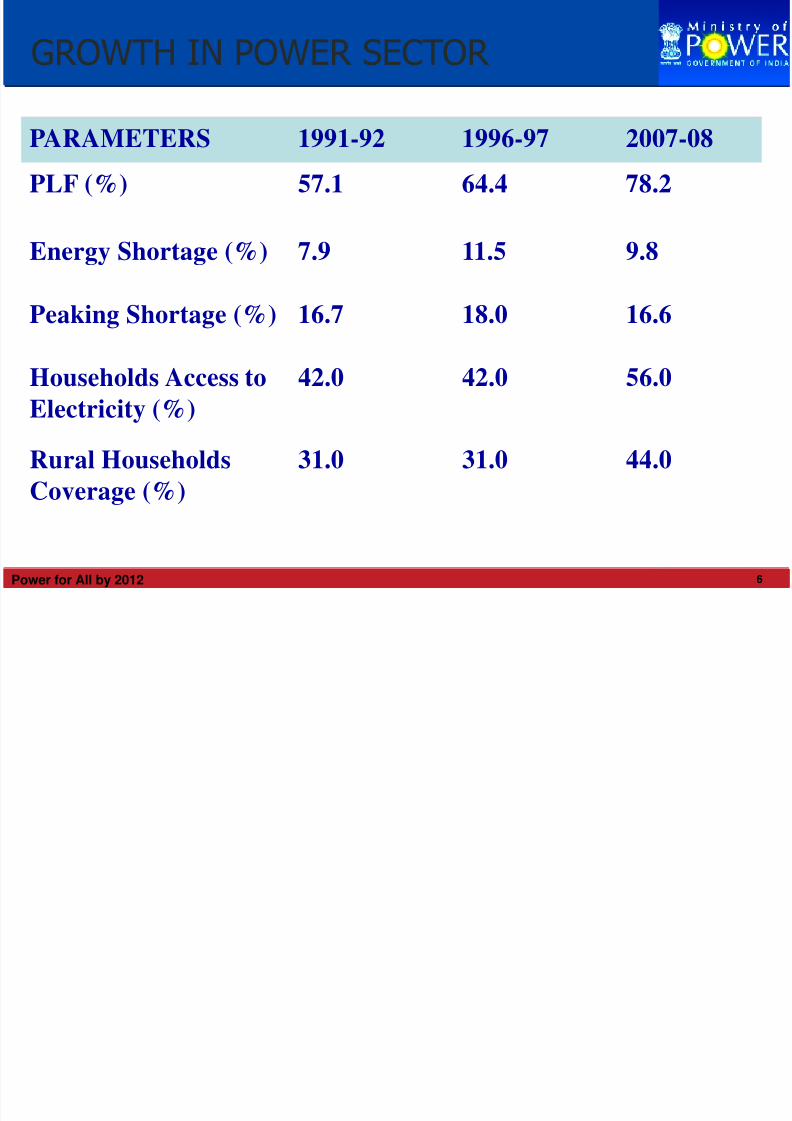

PARAMETERS 1991-92 1996-97 2007-08

PLF (%) 57.1 64.4 78.2

Energy Shortage (%) 7.9 11.5 9.8

Peaking Shortage (%) 16.7 18.0 16.6

Households Access to

Electricity (%)

42.0 42.0 56.0

Rural Households

Coverage (%)

31.0 31.0 44.0

GROWTH IN POWER SECTOR

7Power for All by 2012

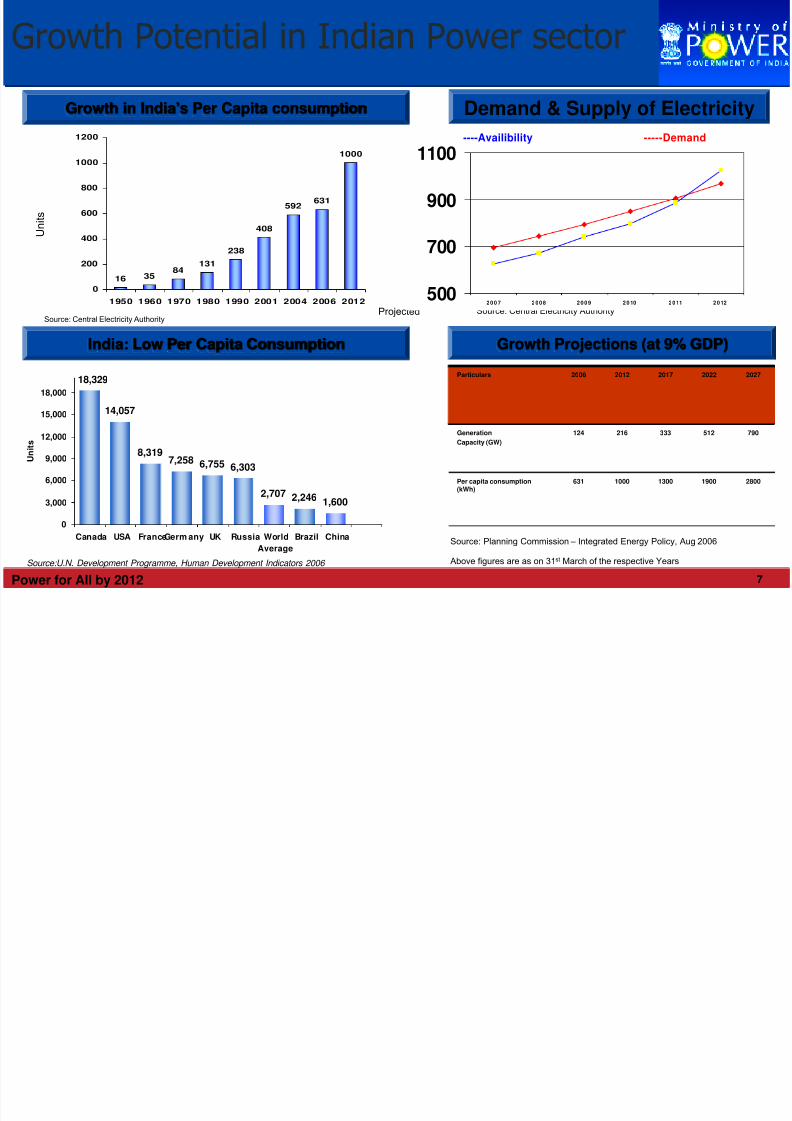

Growth Potential in Indian Power sector

16 3584

131

238

408

592631

1000

0

200

400

600

800

1000

1200

1 95 0 1 96 0 1 97 0 1 98 0 1 99 0 2 00 1 2 00 4 2 00 6 2 01 2

14,057

8,3197,258 6,755 6,303

2,246 1,6002,707

18,329

0

3,000

6,000

9,000

12,000

15,000

18,000

Canada USA FranceGerm any UK Russia World

Average

Brazil China

U n i t s

India: Low Per Capita Consumption

Growth in India’s Per Capita consumption

Projected

U n

i t s

Demand & Supply of Electricity

Growth Projections (at 9% GDP)

Particulars 2006 2012 2017 2022 2027

Generation

Capacity (GW)

124 216 333 512 790

Per capita consumption(kWh)

631 1000 1300 1900 2800

Source: Central Electricity Authority

Above figures are as on 31st March of the respective Years

Source: Planning Commission – Integrated Energy Policy, Aug 2006

Source:U.N. Development Programme, Human Development Indicators 2006

Source: Central Electricity Authority

500

700

900

1100

2007 2008 2009 2010 2011 2012

----Availibility -----Demand

8Power for All by 2012

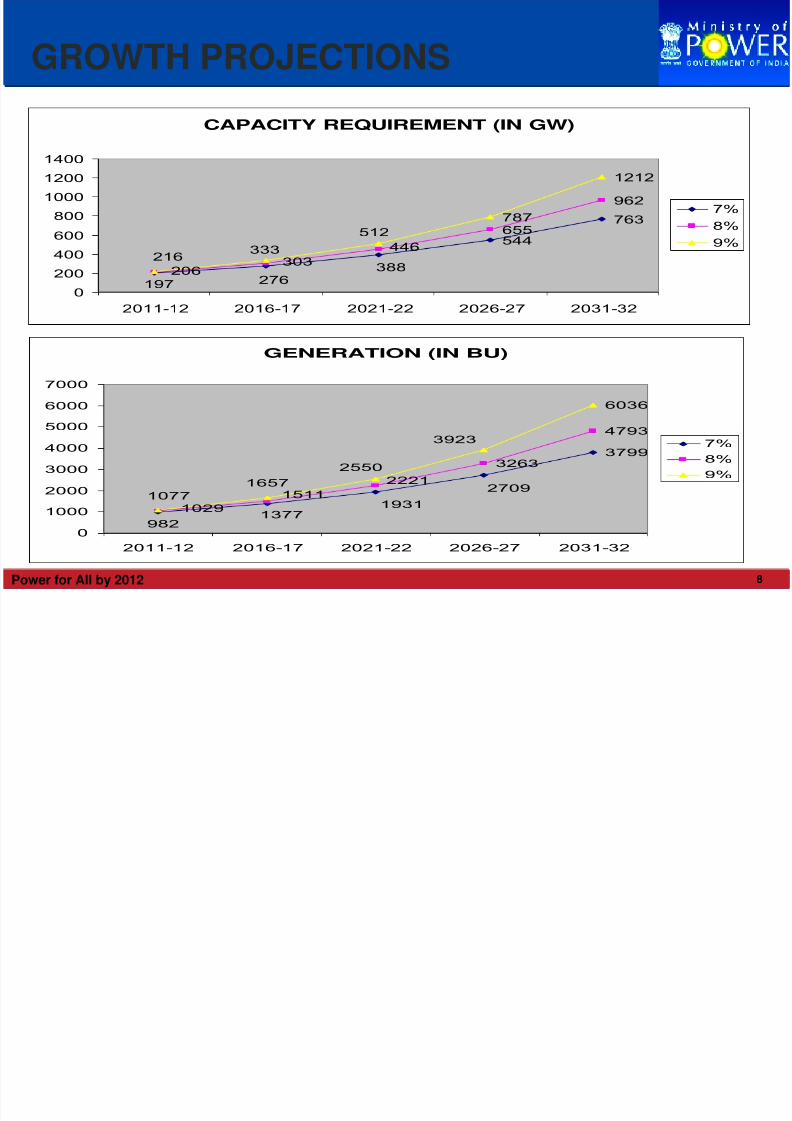

GROWTH PROJECTIONS

CAPACITY REQUIREMENT (IN GW)

544

763655

962

1212

388

276197

446

303206

512

787

333216

0

200

400

600

800

1000

1200

1400

2011-12 2016-17 2021-22 2026-27 2031-32

7%

8%

9%

GENERATION (IN BU)

3799

3263

4793

6036

1377

2709

1931

982

1511

2221

1029

1657

2550

3923

1077

0

1000

2000

3000

4000

5000

6000

7000

2011-12 2016-17 2021-22 2026-27 2031-32

7%

8%

9%

9Power for All by 2012

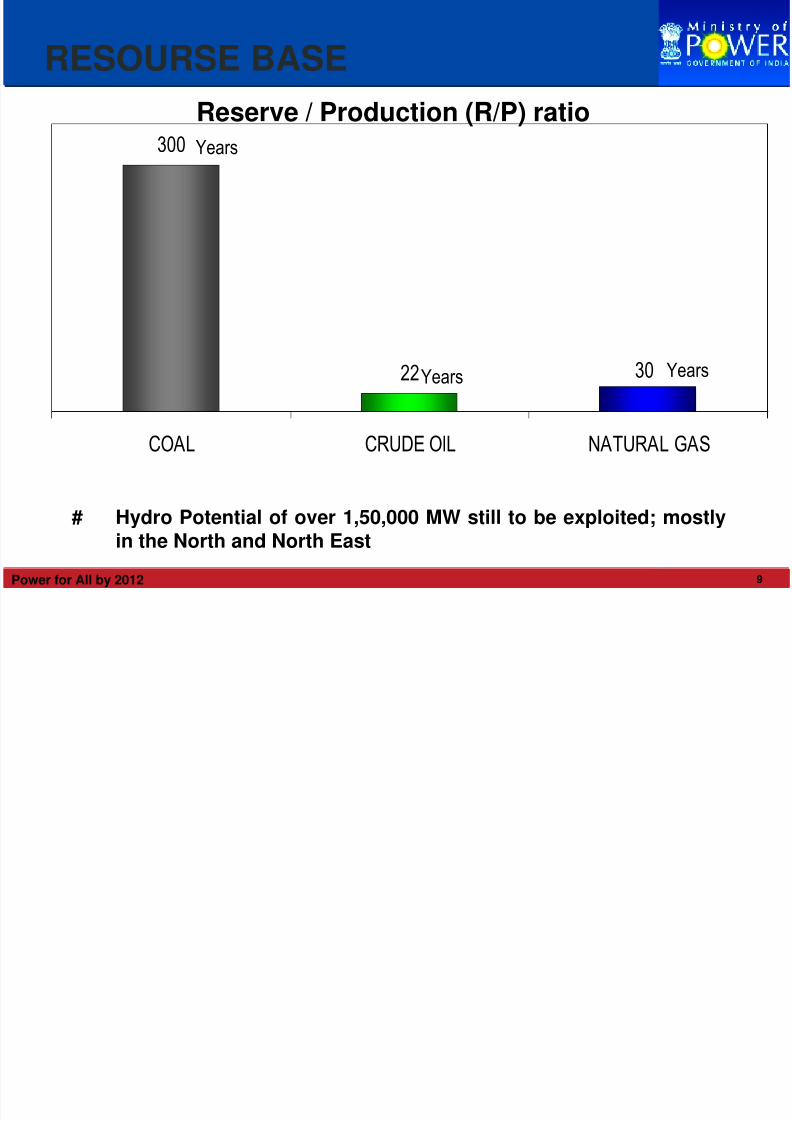

300

22 30

COAL CRUDE OIL NATURAL GAS

Years

Years Years

# Hydro Potential of over 1,50,000 MW still to be exploited; mostly

in the North and North East

Reserve / Production (R/P) ratio

RESOURSE BASE

10Power for All by 2012

INDIA AND THE REST OF THE WORLD

PARAMETERS INDIA OECD WORLD

Energy Supply

(Mtoe)

537.31 5548 11434

Energy Intensity

(Kgoe/$PPP GDP)

0.16 0.20 0.32

Per Capita Electricity

Consumption (kWh)

672 8365 2596

Per Capita CO2

Emissions (Tonnes)

1.05 11.02 4.22

Mtoe : Million tons of oil equivalent, Kgoe : Kilo gram oil equivalent

11Power for All by 2012

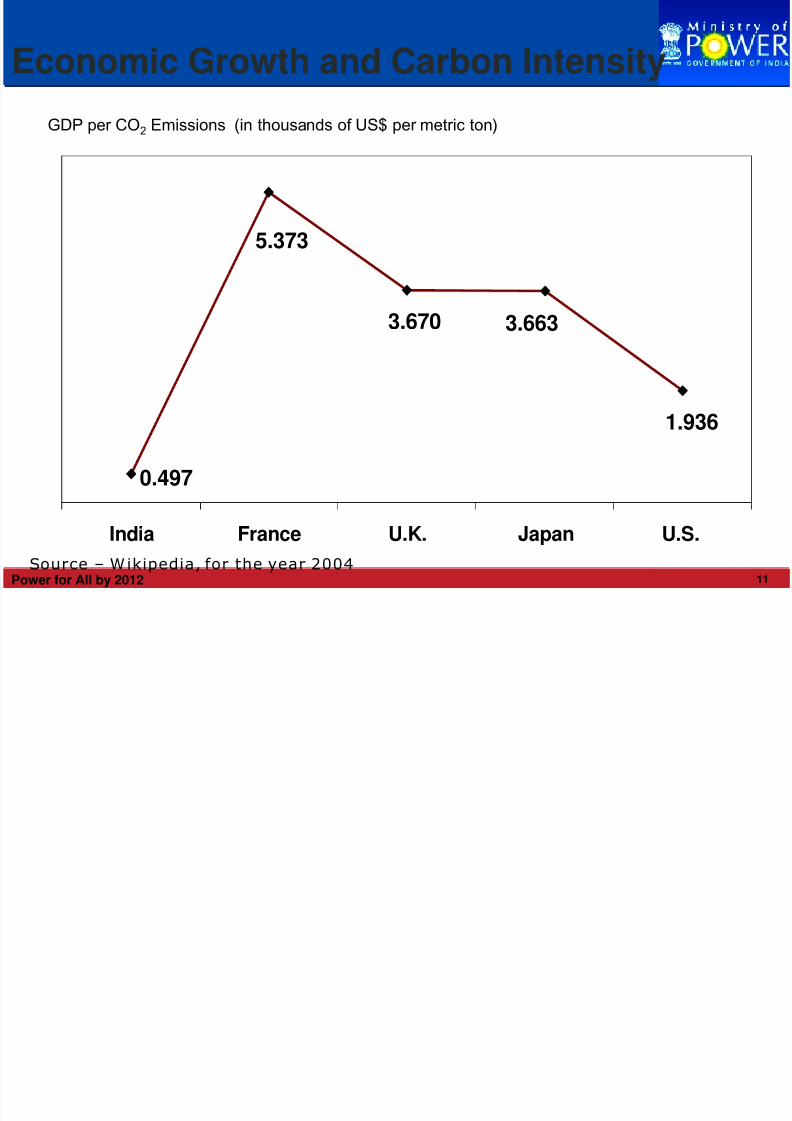

Economic Growth and Carbon Intensity

Source – Wikipedia, for the year 2004

GDP per CO2 Emissions (in thousands of US$ per metric ton)

1.936

0.497

5.373

3.670 3.663

India France U.K. Japan U.S.

12Power for All by 2012

Currently, India’s per-capita GHG emissions are 24% of global

average, 5% of the US, 12% of EU, 11% of Japan.

In cumulative terms,, India has 2% of global GHG emissions.

According to World Energy Outlook’s projections, China’s

share in cumulative emissions between 1900 to 2030 would rise

to 16% approaching that of the US (25%) and the EU (18%).

India’s cumulative emissions are projected to reach 4% which

would be comparable to those of Japan.

Our GHG emissions now, and for many decades to come will

remain within any reasonable measure of our legitimate

environmental space.

India’s Overall Perspective

13Power for All by 2012

Overarching Principles of the UNFCCC:

Article 4.7 of the UNFCCC recognizes that economic and social

development and poverty eradication are the first and

overriding priorities of the developing country Parties.

The Preamble also recognizes that the share of global emissions

originating in developing countries will grow to meet their social

and development needs, and that their per-capita emissions are

still relatively low.

Non-negotiated initiatives outside the UNFCCC process in

which all Parties are not necessarily represented cannot furnish

inputs to the UNFCCC process : Reference is to “Renewables

Initiative” (Germany), “Energy Initiative” (UK), etc.

India’s Overall Perspective: Cont..

14Power for All by 2012

India’s per-capita consumption of electricity and per capita CO2

emissions amongst the lowest in the world.

A large proportion of the country’s population lives below

poverty line (BPL).

Over 50% of population without access to electricity. Some 70

households use traditional biomass for cooking.

India is at the early stages of industrialization and the economic

development – Convergence in per capita income level, energy

consumption and CO2 emission would happen as development

reaches the level of OECD countries.

India’s Overall Perspective: Cont..

Contd…

15Power for All by 2012

Feasible hydro potential shall be fully developed. All hydro

irrespective of size is renewable. We have negotiated hard

against narrower definition which excludes large hydro.

Strong programme for development of other renewable and

non- conventional sources also. Good achievement in exploiting

wind energy potential – Fourth largest in the world.

Electricity Act gives preferential treatment to energy from non-

conventional resources.

Access to fuel remains the key issue for development of nuclear

India’s Overall Perspective: Cont..

Contd…

16Power for All by 2012

Dependence on fossil fuels would remain in the short and

medium term - IEA also projects this.

Availability and pricing issues for usage of gas.

Abundant coal reserves, future electricity needs to be met

primarily from coal.

Usage of clean coal technologies if cost effective. (IGCC)

Energy efficiency is being promoted vigorously.

Super Critical Technology : NTPC, UMPP.

Tariff Policy lays down road - map for reduction of cross

subsidies.

India’s Overall Perspective: Cont..

17Power for All by 2012

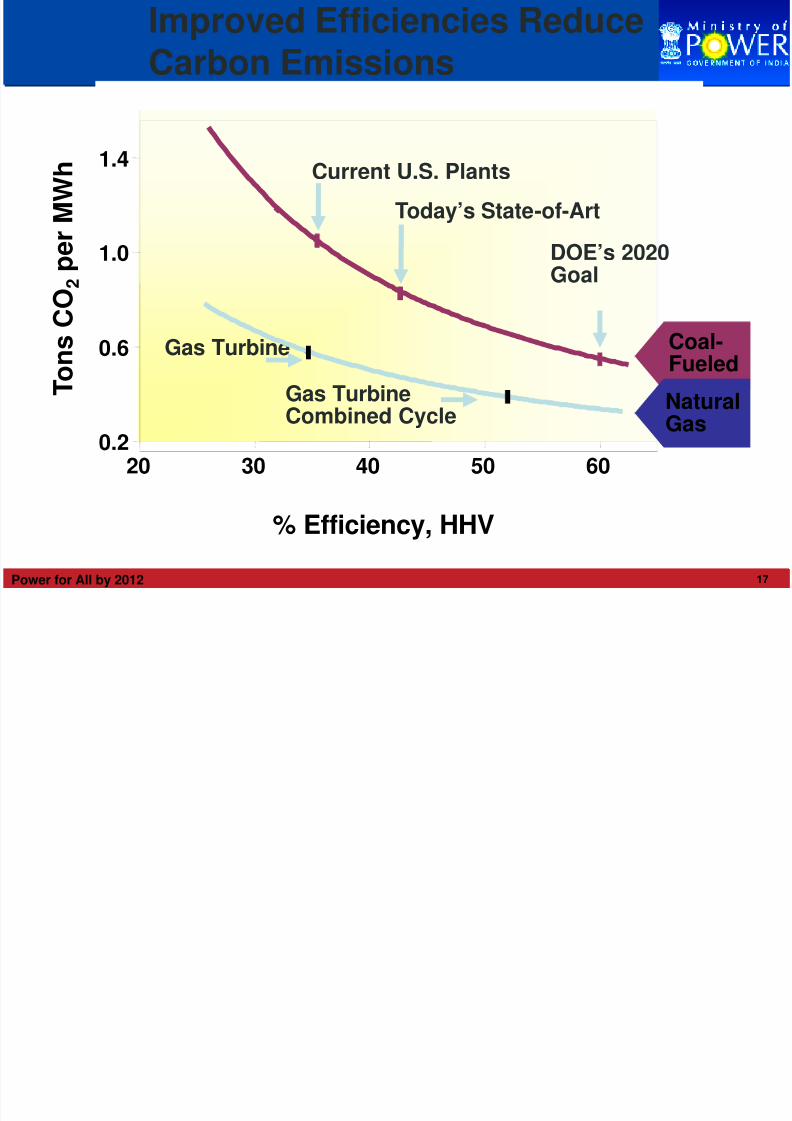

Improved Efficiencies ReduceCarbon Emissions

Current U.S. Plants

Today’s State-of-Art

DOE’s 2020Goal

Gas Turbine

Gas TurbineCombined Cycle

% Efficiency, HHV

T o n s C O

2 p e r M W h

0.2

0.6

1.0

1.4

20 30 40 50 60

Coal-Fueled

NaturalGas

18Power for All by 2012

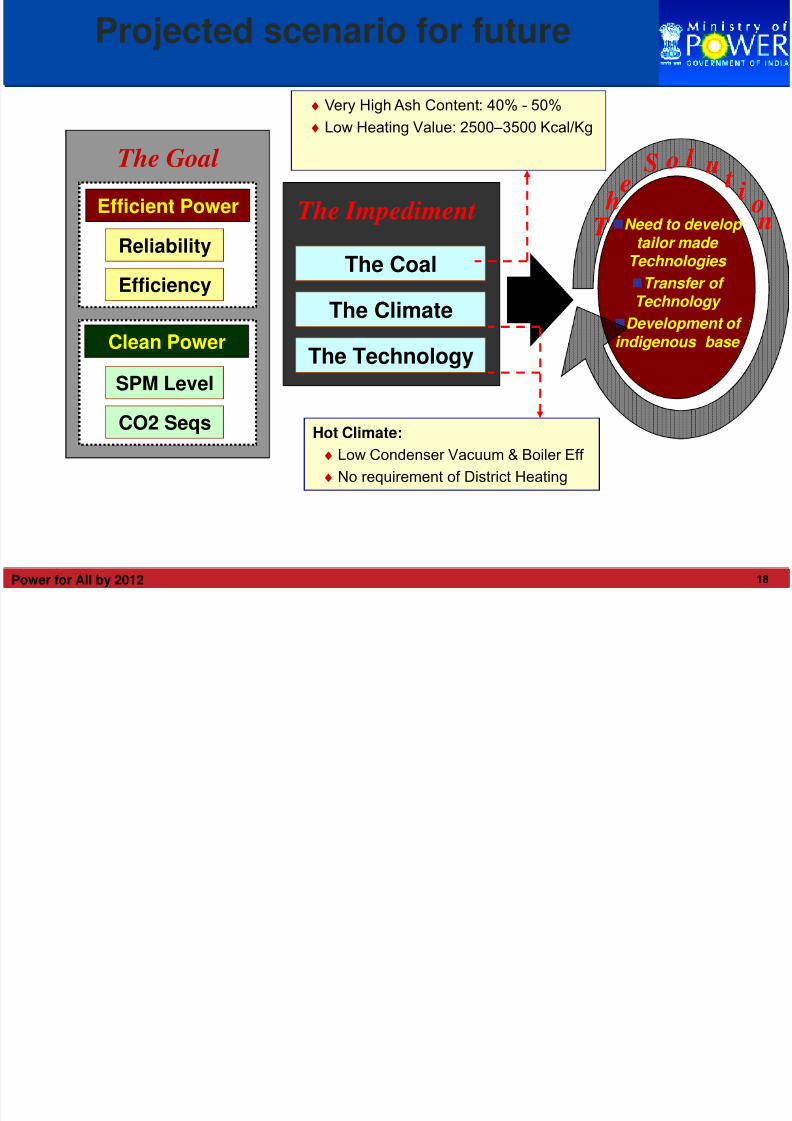

The Goal

Need to develop

tailor made Technologies

Transfer of Technology

Development of

indigenous base

Efficient Power

Reliability

Efficiency

Clean Power

SPM Level

CO2 Seqs

The Impediment

The Coal

The Climate

The Technology

Hot Climate:

♦ Low Condenser Vacuum & Boiler Eff

♦ No requirement of District Heating

♦ Very High Ash Content: 40% - 50%

♦ Low Heating Value: 2500–3500 Kcal/Kg

T h

eS o l u

ti o n

Projected scenario for future

19Power for All by 2012

Deployment of CCS ??

Discussions in the context of Clean Coal Technologies

Wide spectrum – supercritical, IGCC ,CCS

Different levels of commercialization and development

Our stand –we will deploy what is cost effective and safe

We are using Supercritical –NTPC, UMPP

IGCC -- yet to become commercial, 30% extra cost

CCS – will double the cost of power generation, concerns about safety

of storage

Demonstration Plants not to be located in densely populated

developing countries.

The difference between greener technologies and existing technologies

to be funded by developed countries as part of ‘Differentiated

Responsibilities’

20Power for All by 2012

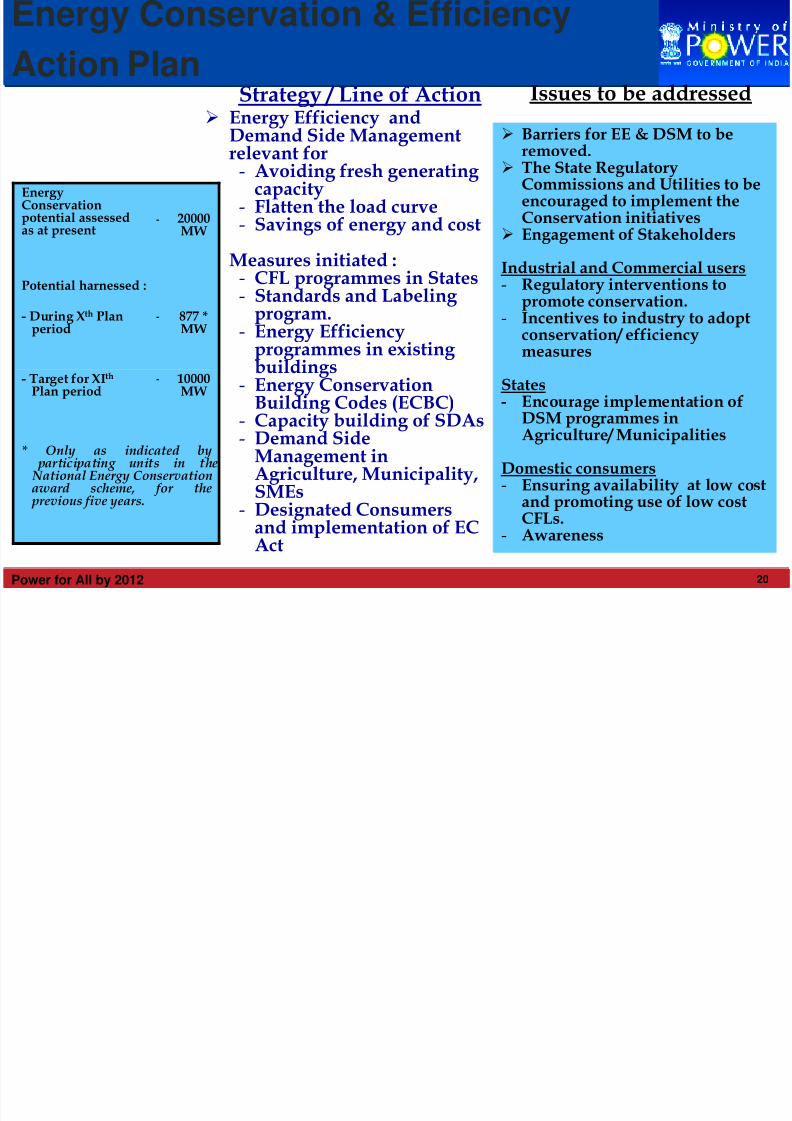

Energy Efficiency andDemand Side Managementrelevant for

- Avoiding fresh generating capacity

- Flatten the load curve- Savings of energy and cost

Measures initiated :- CFL programmes in States- Standards and Labeling

program.- Energy Efficiency

programmes in existing buildings

- Energy ConservationBuilding Codes (ECBC)

- Capacity building of SDAs- Demand Side

Management inAgriculture, Municipality,SMEs

- Designated Consumersand implementation of ECAct

Barriers for EE & DSM to beremoved.

The State RegulatoryCommissions and Utilities to beencouraged to implement theConservation initiatives

Engagement of Stakeholders

Industrial and Commercial users- Regulatory interventions to

promote conservation.- Incentives to industry to adopt

conservation/ efficiencymeasures

States- Encourage implementation of

DSM programmes inAgriculture/ Municipalities

Domestic consumers- Ensuring availability at low cost

and promoting use of low costCFLs.

- Awareness

Strategy / Line of Action Issues to be addressed

EnergyConservationpotential assessedas at present

- 20000MW

Potential harnessed :

- During Xth Planperiod

- 877 *MW

- Target for XIth

Plan period- 10000

MW

* Only as indicated by participating units in the National Energy Conservationaward scheme, for the previous five years.

Energy Conservation & Efficiency

Action Plan

21Power for All by 2012

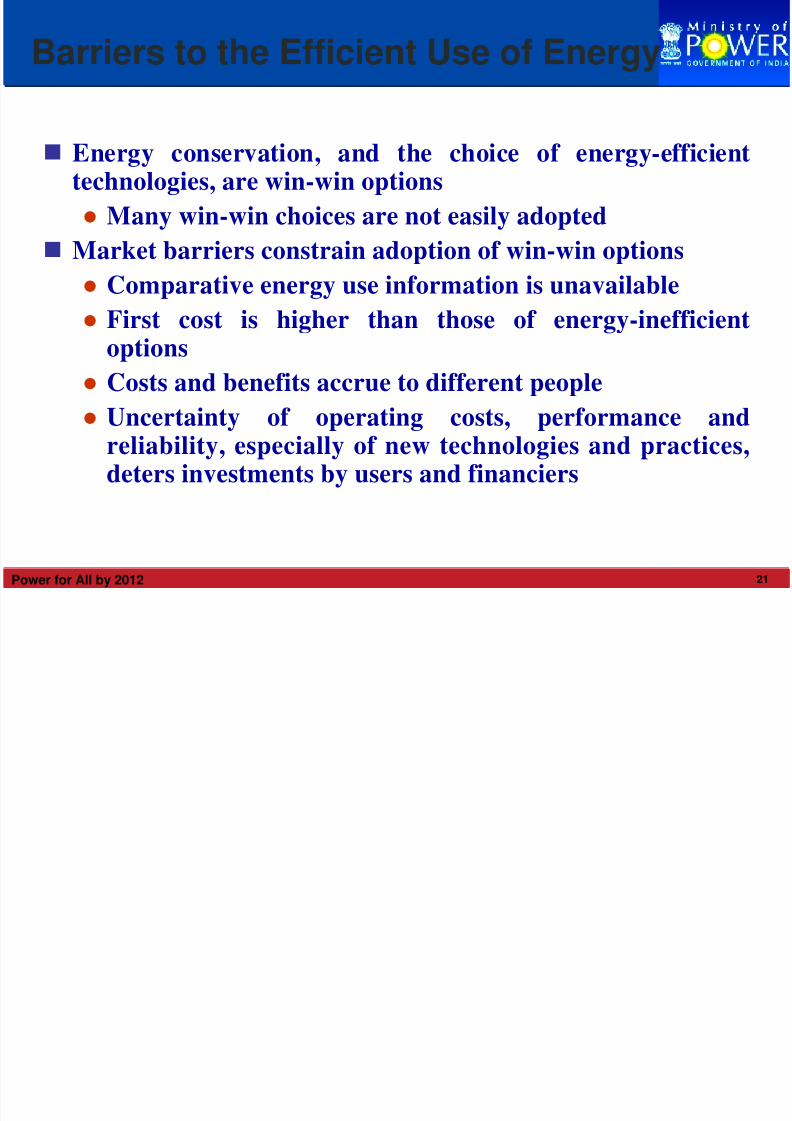

Barriers to the Efficient Use of Energy

Energy conservation, and the choice of energy-efficienttechnologies, are win-win options

● Many win-win choices are not easily adopted

Market barriers constrain adoption of win-win options

● Comparative energy use information is unavailable

● First cost is higher than those of energy-inefficientoptions

● Costs and benefits accrue to different people

● Uncertainty of operating costs, performance andreliability, especially of new technologies and practices,deters investments by users and financiers

22Power for All by 2012

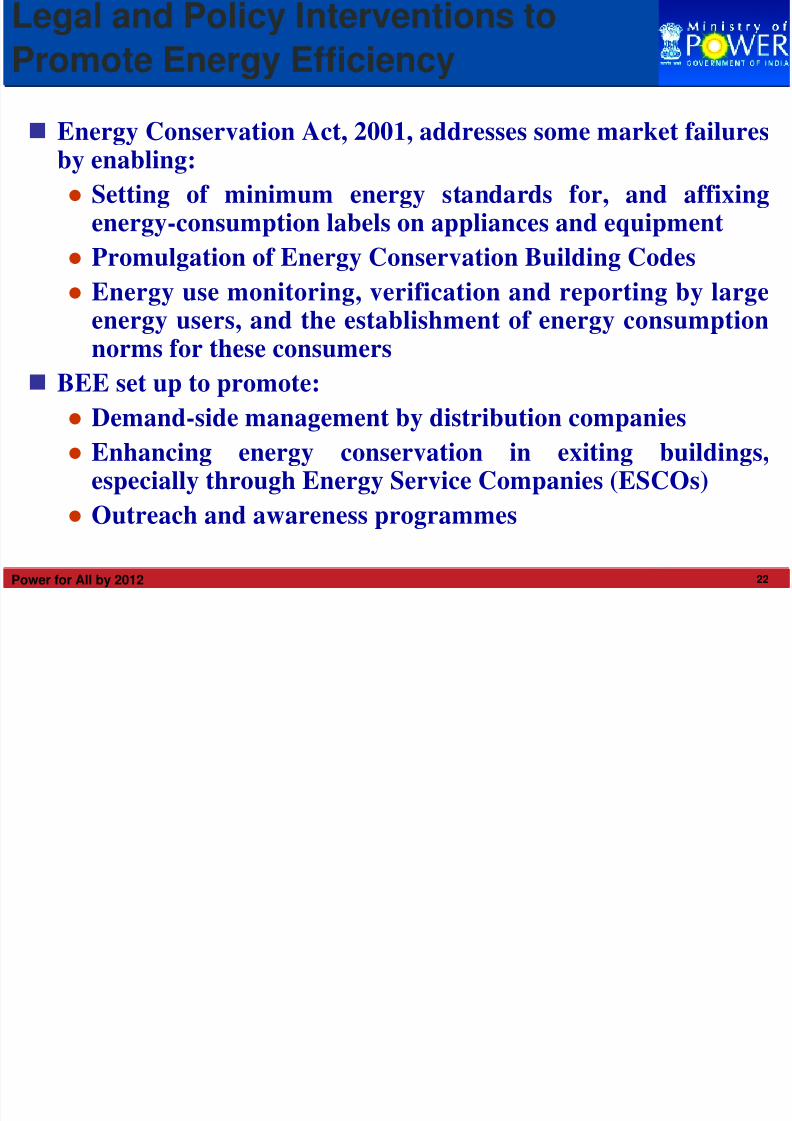

Energy Conservation Act, 2001, addresses some market failuresby enabling:

● Setting of minimum energy standards for, and affixingenergy-consumption labels on appliances and equipment

● Promulgation of Energy Conservation Building Codes

● Energy use monitoring, verification and reporting by largeenergy users, and the establishment of energy consumptionnorms for these consumers

BEE set up to promote:

● Demand-side management by distribution companies

● Enhancing energy conservation in exiting buildings,especially through Energy Service Companies (ESCOs)

● Outreach and awareness programmes

Legal and Policy Interventions to

Promote Energy Efficiency

23Power for All by 2012

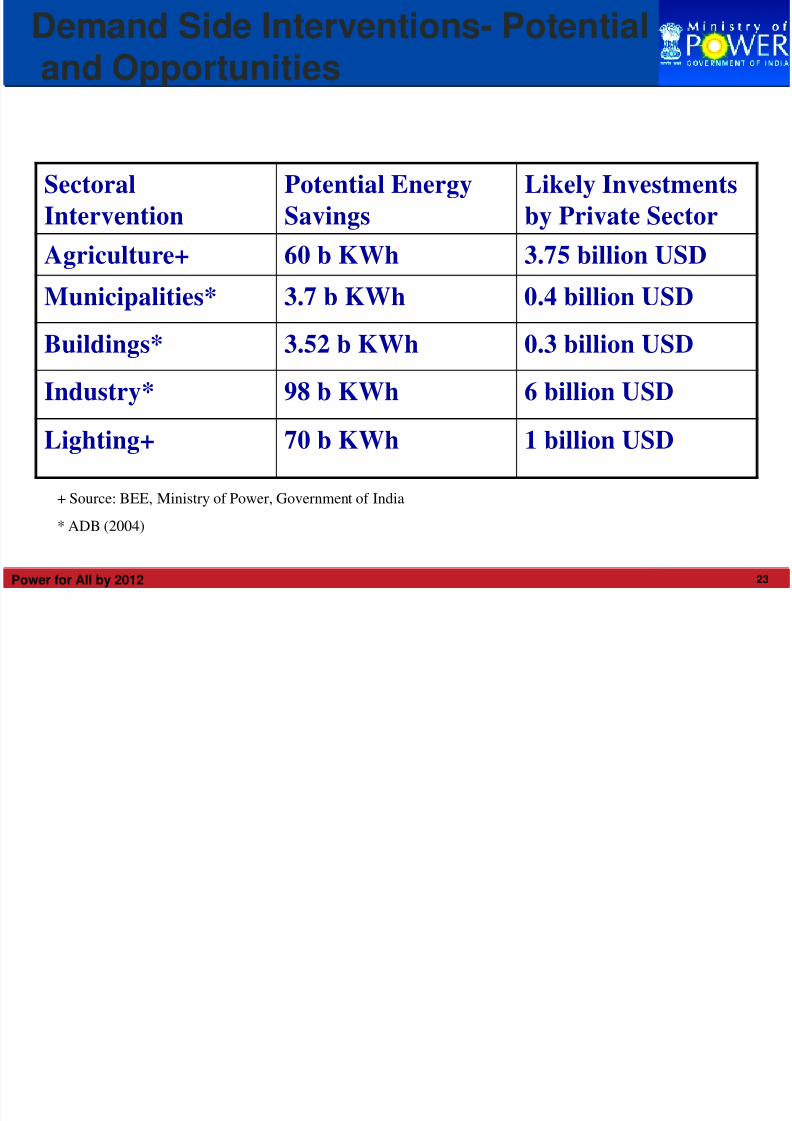

Demand Side Interventions- Potentialand Opportunities

Sectoral

Intervention

Potential Energy

Savings

Likely Investments

by Private Sector

Agriculture+ 60 b KWh 3.75 billion USD

Municipalities* 3.7 b KWh 0.4 billion USD

Buildings* 3.52 b KWh 0.3 billion USD

Industry* 98 b KWh 6 billion USD

Lighting+ 70 b KWh 1 billion USD

+ Source: BEE, Ministry of Power, Government of India

* ADB (2004)

24Power for All by 2012

Approach and Methodology- EnergyEfficiency Action Plan

Sector specific approach- barriers being addressed separately

in each sector- e.g.. Use of CDM to reduce cost of CFL under

BLY, creation of DPRs and provision of financing for

agriculture/ municipal and buildings, capacity building for use

of ECBC for commercial sector.

Adopting sectoral approach by facilitating creation of markets

for energy efficiency

Emphasis on conducive environment, handholding of early

movers

8 Different sector specific schemes being implemented to take

note of this requirement

25Power for All by 2012

CDM Based CFL Scheme

26Power for All by 2012

CDM Based CFL Scheme- BachatLamp Yojana (BLY)

Scheme seeks to replace estimated 400 million incandescentbulbs by CFLs- could save 6000 MW by 2012

BEE has prepared a Programme of Activities (PoA) as avoluntary coordinated effort to facilitate the scheme in theentire country and reduce transaction costs

18 CFL manufacturers/ suppliers have agreed to participate-14 states have initiated the scheme

Monitoring Plan finalised

2 pilot projects in Haryana and Andhra Pradesh submitted toCDM Executive Board for registration

Leveraging of CDM revenues to remove the high first costbarrier- market transformation in favour of efficient lighting

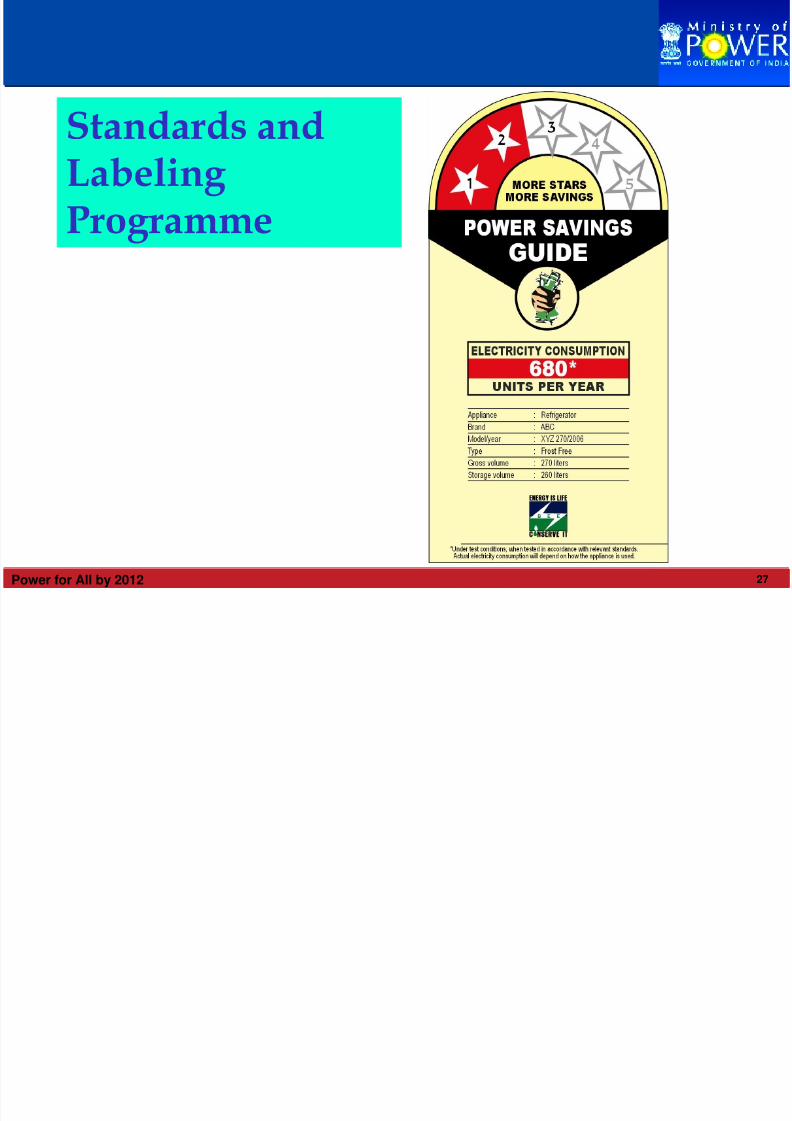

27Power for All by 2012

Standards andLabeling Programme

28Power for All by 2012

Standards & Labeling Programme

The National Energy Labeling Programme launched byHon’ble Union Minister of Power on 18th May, 2006.

• To create appropriate legal and regulatory environment forenergy efficient end use products

• To provide the consumer an informed choice about energysaving by using efficient devices

• To gear up Indian industry to compete in markets that havemade/ are making such standards mandatory e.g.. US or EU

• To stimulate market transformation in favour of energyefficient equipments and appliances- both from supply anddemand side

• To reduce overall energy consumption by use of suchequipments/ appliances- 18 BU by 2012 (~3000 MW)

• To provide assistance/ support to Small & MediumManufacturers

29Power for All by 2012

• Voluntary labeling for ACs, Refrigerators, Tube lights (TL),

motors and Distribution Transformers already in place

• 90% of TL, 80% of Refrigeration and 75% of AC industry

on board

• Consumer awareness campaign launched

• Independent institutional mechanism for check and

challenge testing on random basis for labeled equipments

being conducted.

• Regulation for mandatory labeling under section 14 of the

Energy Conservation Act to be notified

• Preliminary results for 2007-08 indicate energy savings by

use of these equipments equivalent to about 300 MW of

capacity

Standards & Labeling Programme…

30Power for All by 2012

Statutory agencies at state level to implement EC Act- key to

implement EC Act at State level

Capacity building necessary to enable them to discharge

regulatory, facilitative and enforcement functions under the

Act

Institutional capacity limited- both in terms of human and

infrastructure resources

Most states have notified SDAs in the last 2 years

Hand holding necessary to ensure balanced implementation of

Act

30 States have designated their agencies so far

State Designated Agency (SDA)Program

31Power for All by 2012

Energy Conservation Building Code(ECBC)

32Power for All by 2012

Energy Conservation Building Code(ECBC)

Covers new commercial buildings

Building components included

● Building Envelope (Walls, Roofs, Windows)

● Lighting (Indoor and Outdoor)

● Heating Ventilation and Air Conditioning (HVAC) System

● Solar Water Heating and Pumping

● Electrical Systems (Power Factor, Transformers)

● Potential to save 1.7 billion units annually on mandatoryapplication

● Expected reduction in XI plan 500 MW

ECBC launched by MOP on 27.5.2007 for five climatic zones

33Power for All by 2012

Easy to use guides, tip sheets launched

Panel of architects prepared to help dissemination of ECBC

Curriculum enhancement in architectural institutions taken up

CPWD and some other Government agencies taking the lead in ECBC

implementation

Survey indicates about 306 buildings being constructed in the country

which are ECBC complaint- will result is an estimated avoided capacity

addition of 300 MW on completion

Existing Buildings Energy Efficiency (EE)

Over 500 government buildings being taken up for EE

ESCOs being short listed- accreditation of ESCOs by CRISIL/ ICRA

being initiated to improve credibility

Standardised performance contract documents developed

Innovative financial instruments being developed to mainstream ESCO

based EE

ECBC Programme…

34Power for All by 2012

Agriculture and Municipal DSM

35Power for All by 2012

Agricultural & Municipal DSM

• Over 35% of electricity consumed by Agriculture and

Municipal sector

• High inefficiencies in pumping system- targeted through a

subsidy reduction approach

• Business model linked to subsidy reduction being evolved

• Shelf of bankable DPRs to be prepared- 10 in each states (total

350) to stimulate the market

• Baseline development, conducive regulatory regime and

payment security mechanism being worked out.

• Awareness and outreach to local and municipal bodies

• Manual for Mu DSM being developed with standard contract

documents to enable easier implementation

• Risk mitigation measures for encouraging PPP being evolved

CDM benefits for the scheme being put in.

36Power for All by 2012

Visit us at www.powermin.nic.in