Group Presentation

39

Background Presentation Vodafone Group Plc

-

Upload

rohit-mittal -

Category

Documents

-

view

18 -

download

0

description

Strategy analyisis

Transcript of Group Presentation

Background

Presentation

Vodafone Group Plc

Disclaimer

2

Information in the following presentation relating to the price at which relevant investments have been bought or sold in the past or

the yield on such investments cannot be relied upon as a guide to the future performance of such investments. This presentation

does not constitute an offering of securities or otherwise constitute an invitation or inducement to any person to underwrite,

subscribe for or otherwise acquire or dispose of securities in any company within the Group.

The presentation contains forward-looking statements within the meaning of the US Private Securities Litigation Reform Act of 1995

which are subject to risks and uncertainties because they relate to future events. Some of the factors which may cause actual results

to differ from these forward-looking statements are discussed on the final slide of the presentation.

The presentation also contains non-GAAP financial information which the Group’s management believes is valuable in understanding

the performance of the Group or the Group’s businesses. However, non-GAAP information is not uniformly defined by all companies

and therefore it may not be comparable with similarly titled measures disclosed by other companies, including those in the Group’s

industry. Although these measures are important in the assessment and management of the business, they should not be viewed in

isolation or as replacements for, but rather as complementary to, the comparable GAAP measures.

Vodafone, the Vodafone Speech Mark, the Vodafone Portrait, Vodacom and M-Pesa are trademarks of the Vodafone Group. The

Vodafone Rhombus is a registered design of the Vodafone Group. Other product and company names mentioned herein may be the

trademarks of their respective owners.

• Vodafone Group Plc is one of the world’s largest

telecommunications companies providing a wide range of

services, including voice, messaging, data across mobile

and fixed networks

• We have 438m mobile customers and 11 million fixed

broadband customers

• We have mobile operations in 26 countries and partner

with mobile networks in over 50 more

• Our operations are spread across two geographic regions -

Europe and Africa, Middle East and Asia Pacific (AMAP)

• The Group is listed on the London and NASDAQ (ADR

listing) stock exchanges and is headquartered in London

• We have over 275,000 base station sites across our

markets (as of December 2014)

A brief introduction to the Group

3

Financial highlights FY 13/14

Revenue £43.6bn

EBITDA £12.8bn

Adjusted operating profit £7.9bn

Capex £7.1bn

Free cash flow £4.4bn

Adjusted EPS 17.54p

Dividend per share 11.00p

8%

15%

4%

42%

31%

• Mobile accounts for the majority (81%)

of our business

• Fixed (15%) is becoming an increasing

part of what we do

• A quarter of our business comes from

Enterprise customers

• Revenue and profits are spread across

our geographical footprint

Revenue and profit mix of the Group

4

Mobile

out-of-

bundle

Mobile

incoming

Group service revenue FY 13/14

8%

27%

19% 15%

11%

10%

10%

Spain

Other

Germany

UK

Italy

Vodacom

India

Group service revenue FY 13/14

21%

13%

12% 11%

11%

6%

26%

Germany

Vodacom

Italy

UK

India

Spain

Group EBITDA FY 13/14

37%

29%

27%

7% Consumer

contract

Consumer prepaid

Other

Enterprise

Group service revenue FY 13/14

Other

Fixed

Other

Mobile in-bundle

• Over 60% of our customers are

from emerging markets

• The majority of our customers are

prepaid customers

• Consumer contract customers are

12% of the base and contribute

over a third of service revenue

• Enterprise contributes over a

quarter of our service revenue

Mobile customer mix of the Group

5

Customers by country (%) FY 13/14

38

15 7

10

6

4 3

17 India

Vodacom Germany

Egypt

Italy

UK

Spain

Other

Customers by segment (%) FY 13/14

12 81

7

Consumer contract

Enterprise

Consumer

prepaid

History of the Group

6

1984 1991 1999 2000 2006 2007 2009 2010 2011 2013 2014

Incorporated as Racal

Strategic Radio Limited

Demerger from

Racal and full listing

on the LSE

Merger with AirTouch

Communications,

formation of Verizon

Wireless (Vodafone

held a 45% stake)

Acquisition of

Mannesmann AG,

acquiring further

businesses in Europe

Acquisition of Telsim

(now Vodafone Turkey)

Disposal of

Vodafone Japan

Acquisition of

controlling stake in

Vodafone Essar (now

Vodafone India)

Vodacom Group

became a subsidiary

Vodafone Australia

merged with

Hutchinson 3G Australia

Disposal of our interest

in China Mobile

Sale of interest

in SFR

2012

Acquisition of

Cable and Wireless

Worldwide

Acquisition of

Kabel Deutschland

in Germany

Sale of 45%

interest in

Verizon

Wireless

Acquisition of

Ono in Spain

Ownership of

Vodafone India

and Italy

increased

to 100%

Where we operate

7

Subsidiaries (% ownership)

Joint ventures/associates

Indus Towers (42%), part of Vodafone India

Australia (50%)

Safaricom (Kenya) (40%)

Partner markets

Portugal (100%)

Qatar (22.95%)

Romania (100%)

Spain (100%)

Turkey (100%)

UK (100%)

Vodacom Group (65%)

Consists of

South Africa

Tanzania

Mozambique

DRC

Lesotho

Albania (100%)

Czech Rep (100%)

Egypt (54.9%)

Germany (100%)

Ghana (70%)

Greece (99.9%)

Hungary (100%)

India (100%)

Ireland (100%)

Italy (100%)

Malta (100%)

Netherlands (100%)

New Zealand (100%)

See page 37 for details

Our people

8

Gerard Kleisterlee (Chairman) Appointed July 2011

He retired as President/CEO and Chairman of Philips on 31 March

2011 after spending three decades with the company. He is also a

Board member of Daimler AG, Royal Dutch Shell and Dell Inc.

Vittorio Colao (CEO) Appointed July 2008

CEO before joining the Board in 2002. He left Vodafone in 2004 for

RCS MediaGroup before re-joining the Board in October 2006 as CEO,

Europe and Deputy CEO.

Nick Read (CFO) Appointed April 2014

He joined Vodafone in 2001 and has held a variety of roles including

CFO, CCO and CEO of Vodafone UK. Before becoming Group CFO, he

was the regional CEO for our AMAP region and a Board member of our

listed companies Vodacom Group, Safaricom and Vodafone Qatar.

Steve Pusey* (CTO) Appointed June 2009

He joined Vodafone in 2006 having previously served as Executive

Vice President and President for Nortel, EMEA having joined the

company in 1982. Before then he worked for British Telecom.

Non-executive board members: Luc Vandevelde (Senior Independent Director), Sir Crispin Davies, Dame Clara Furse DBE, Val Gooding, Renee James, Samuel Jonah,

Nick Land and Philip Yea

Executive committee: Vittorio Colao (CEO), Nick Read (CFO), Stephen Pusey (CTO), Philipp Humm (CEO Europe), Serpil Timuray (CEO AMAP), Paolo Bertoluzzo (Group

Chief Commercial and Operations Officer), Warren Finegold (Strategy & Business Development Director), Matthew Kirk (External Affairs Director), Rosemary Martin

(General Counsel and Company Secretary), Ronald Schellekens (Group HR Director), Nick Jeffery (Group Enterprise Director)

Over

97,000 employees1

24 nationalities 22% women in top senior management roles

1. As of March 2014

* Steve Pusey will retire on 31 July 2014

The services we provide

81%

15%

4%

Mobile

Fixed

Other

We also provide financial services

We have 18.5m M-Pesa users across 9 markets.

M-Pesa enables customers to send and receive money via

their mobile phones without the need for a bank account.

M-Pesa also includes the ability to save and receive

short-term loans in some markets

Split of Group service revenue FY 13/14 Voice

Over 1.2 trillion minutes of calls were carried over our networks last year

That’s the equivalent of everyone around the world talking for two and a half hours

Messaging We sent over 337 billion text, picture, music and video messages last year

Data Over 544 petabytes of data were sent across our networks last year

That’s enough data for over 100 billion one minute video clips

Fixed We serve over 11 million customers, mainly in Germany, Spain and Italy

Other services We earn revenue from letting other ‘virtual’ operators use our network and from partners outside our footprint using our products and services

9

Our technology

10 Data shown here correct as of 31 December 2014 unless otherwise stated

1. Next Generation Network technology: includes fibre-to-the-home, cable and fibre/VDSL to the cabinet or central office

We have over

Mobile

275,000 base station

sites

Europe

India

AMAP

37%

46%

17% (excl. India)

10

18 markets with 4G services

65% 4G coverage in Europe 77% European sites fully

modernised

90% 3G coverage in India (targeted urban areas)

80% 3G coverage in AMAP (excluding India)

£17.2bn net book value of owned licences and spectrum (as of March 2014)

Fixed

An excellent network experience is key to our strategy and Project Spring accelerates our progress

26m households passed with NGN

48m households passed with NGN

(incl. wholesale)

• Our fixed access comes from a range of sources:

– Acquisitions (e.g. KDG, Ono)

– Self or co-building (e.g. Italy, Spain, Portugal)

– Wholesale (e.g. Netherlands)

79% European sites with high capacity backhaul

Project Spring is our investment programme that increases our capital expenditure over two years

to £19 billion – to accelerate and extend our strategy and strengthen our differentiation

Project Spring: investing £19 billion over two years

11

European

mobile

• Extend network coverage and density with 36k new 4G sites and 98% of sites with high capacity backhaul

• Provide a ‘perfect voice’ experience (call success rates over 99%)

• Deliver the best 4G data experience with over 90% outdoor population 4G coverage and 90% of sessions > 3Mbps

AMAP

mobile • Extend network coverage and density with 22k new 3G sites

• Grow 3G coverage to 95% in targeted urban areas in India

Unified

comms

• Build fibre in Italy and Spain

• Extend our existing fibre build programme in Portugal

• Expand xDSL coverage in selected markets

Enterprise • Invest in growth areas: IP-VPN, Hosting & Cloud, M2M

• Leverage carrier services platform

• International expansion

Customer

experience

• Accelerate retail redesign and selectively increase direct distribution

• Enhance online/mCare capabilities and create consistently strong contact centre experience

• Faster deployment of mobile payment services

Our strategy

12

Our strategy is focused on four key growth areas and targets:

Unified

Communications

A leading mobile data provider Converged services in all key

European markets

A stronger leader and first

choice for data

Major enterprise provider with

full service offering

Consumer Europe Enterprise Consumer Emerging

Markets

Supported by:

An excellent network experience A simplified and cost-efficient business model

and operations

Project Spring accelerates and extends our strategic priorities through investment in mobile and fixed networks,

products and services, and our retail platform, to strengthen further our network and service differentiation

What we want to achieve for our customers:

Always best connected

• Best mobile voice and data

(coverage and quality) - 4G/3G

• Competitive in fixed and best converged

experience

Unmatched customer experience

• Number one in customer experience

- in store, online, on the phone

• Consistent execution across markets

Integrated worry-free solutions

• Simplest connectivity and price plans

• Converged enterprise product suite

• Innovator in new services, such as

mobile payments

390 430

473

527

627

Q2 13/14 Q3 13/14 Q4 13/14 Q1 14/15 Q2 14/15

Our strategy: Consumer Europe

13

• More and more of our customers are using data with increases in smartphone users,

4G customers and average data usage

• This is helped by bundling content with 4G price plans, for example UK consumers

can choose between Netflix, Spotify, Sky Sports and Now TV

Acceleration in average smartphone

usage growth Europe (MB)1

+10%

+11%

+19%

1. Android and iOS

33.0

41.0

48.0

Q2 12/13 Q2 13/14 Q2 14/15

Smartphone penetration

continues to increase European smartphone penetration (%)

+10%

4G penetration growing rapidly

2.0

4.7 6.7

9.7

5.4

11.0

13.6

16.2

Q3 13/14 Q4 13/14 Q1 14/15 Q2 14/15

4G smartphone customers (m)

4G smartphones (m)

Our strategy: unified communications

1. FY 14/15 includes Ono on a pro forma basis

2012 2013 2014

Acquired TelstraClear in

New Zealand to become

an unified comms operator

Acquired CWW in the UK, making

us an integrated fixed/mobile

operator for enterprise customers

Acquired Kabel

Deutschland, the

leading cable operator

in Germany

Acquired Ono,

the leading cable

operator in Spain

We increasingly offer more than mobile

Our recent acquisitions

Fixed as a % of European service revenue

FY 11/12 FY 14/15

(Pro forma)1 11%

25%

We are building out fibre in

Italy, Spain, Portugal and

Ireland

11.2m broadband customers

9.6m TV customers

14

Acquired Hellas Online

in Greece, a leading

broadband provider

Our strategy: Emerging markets

15

• Our emerging markets are DRC, Egypt, Ghana, India, Lesotho, Mozambique, Qatar,

South Africa, Tanzania and Turkey

• Customer growth remains strong and customers are increasingly moving to data

• Our money transfer service, M-Pesa, is now available in 9 markets

Growth in customers, AMAP (m)1

286.2

294.5

303.7

310.5 312.5

Q2 13/14 Q3 13/14 Q4 13/14 Q1 14/15 Q2 14/15

Growth in data users (m) Growth in M-Pesa users (m)

1. AMAP region also includes Australia and New Zealand

15.9

16.8 16.8

17.7

18.5

Q2

13/14

Q3

13/14

Q4

13/14

Q1

14/15

Q2

14/15

44.0

21.1

7.1 5.8

57.2

25.9

9.3 7.7

India Vodacom Turkey Egypt

Sept 2013

Sept 2014

Group strategy: Enterprise

1. Market leader in Gartner Magic Quadrant for managed M2M services

Group service revenue

Vodafone Global Enterprise serves around 1,700

multinational companies in over 100 countries

Expanding in key growth areas

Global leader in M2M1, position strengthened with

acquisition of Cobra Automotive

Our Cloud & Hosting services help organisations

bring their data and applications to the cloud

Carrier services – we are the largest international

voice carrier in the world

+1.2%

+23.5%

+2.0%

+9.1%

How we differentiate

• Scale - #1 or #2 position in most of our markets

• Strength in fixed and mobile- historically strong in mobile, successful in

building capability in fixed (now a quarter of enterprise revenues)

• Range of services - able to provide a full range of other services including

M2M, cloud & hosting and IP-VPN

• Geographic reach - presence in over 100 countries

• Network- leveraging the Vodafone mobile and fixed networks

We provide a range of mobile, fixed, hosting, cloud and other business

services for business across the world, whether large or small

Enterprise is

around a

quarter of the

Group

Q2 14/15 growth

16

Our financials

17

Guidance

Assumptions

Excludes Ono. Assumes FX rates of £1: €1.21, £1:INR 105.8 £1:ZAR 18.4. Also excludes the impact of license

and spectrum purchases, material one-off tax related payments, restructuring costs and any fundamental

structural change to the eurozone. It also assumes no material change to the current structure of the Group.

Net debt of £21.8bn at 30 September 2014 The Group has a range of debt instruments including bonds, commercial paper

and bank loans. The currency profile of the Group’s debt is broadly in line with

the value of the Group’s underlying assets.

Moody’s Fitch Standard & Poor’s Baa1 BBB+ A-

Long term credit ratings:

Key financials FY 13/14 FY 12/13 FY 11/12 FY 10/11 FY 09/10

Revenue (£bn) 43.6 44.4 46.4 45.9 44.5

EBITDA (£bn) 12.8 13.6 14.5 14.7 14.7

Adjusted operating

profit (£bn) 7.9 12.0 11.5 11.8 11.5

Capex (£bn) 7.1 6.3 6.4 6.2 6.2

Free cash flow (£bn) 4.2 5.5 6.1 7.0 7.2

Adjusted EPS (p) 17.54 15.65 14.91 16.75 16.11

Dividend per share (p) 11.00 10.19 13.52 8.90 8.31

For the year ended 31 March 2015

EBITDA: £11.6bn - £11.9bn

Positive free cash flow after all capex, before M&A, spectrum and restructuring costs

1.5

(1.9)

(4.3)

3.7

0.2

(2.0)

FY 11/12 FY 12/13 FY 13/14

Organic service revenue growth (%)

Reported

Excluding MTRs1

1. Mobile termination rates

35

12 10

43

Our shareholders and shareholder returns

18

Dividend policy

Intention to grow dividend per share annually

Year ended 31 March Interim Final Total

2008 2.49 5.02 7.51

2009 2.57 5.20 7.77

2010 2.66 5.65 8.31

2011 2.85 6.05 8.90

20122 3.05 6.47 9.52

2013 3.27 6,92 10.19

2014 3.53 7.47 11.00

2015 3.60 TBC TBC

Dividend history (pence per ordinary share)

Our shareholders (%) Share price history Price rebased to Vodafone (pence)

260

220

180

140

100 Oct 2011 Oct 2012 Oct 2013

UK North

America

Europe Rest of World

Listing - - -

Ticker - - -

Types - - -

Market Cap - - -

Shares in issue - - -

London, NASDAQ

VOD:LN, VOD:AR

Ordinary, ADR

Approx. £54bn

as of 30 Sept 2014

26,504m1

Vodafone DJ Global Telcos, rebased to Vodafone

Shareholder returns (£bn)

1. Excludes 2,309m treasury shares. Total of 28,813m shares in issue as of 30 Sept 2014

2. The group also paid a special dividend of 4.00p in February 2012

Over £80 billion returned to shareholders from

FY 10/11 to FY 13/14, consisting of £21 billion

in dividends, £8 billion of share buybacks and a

£51 billion return to shareholders following the

sale of our stake in Verizon Wireless (February

2014)

Sept 2014

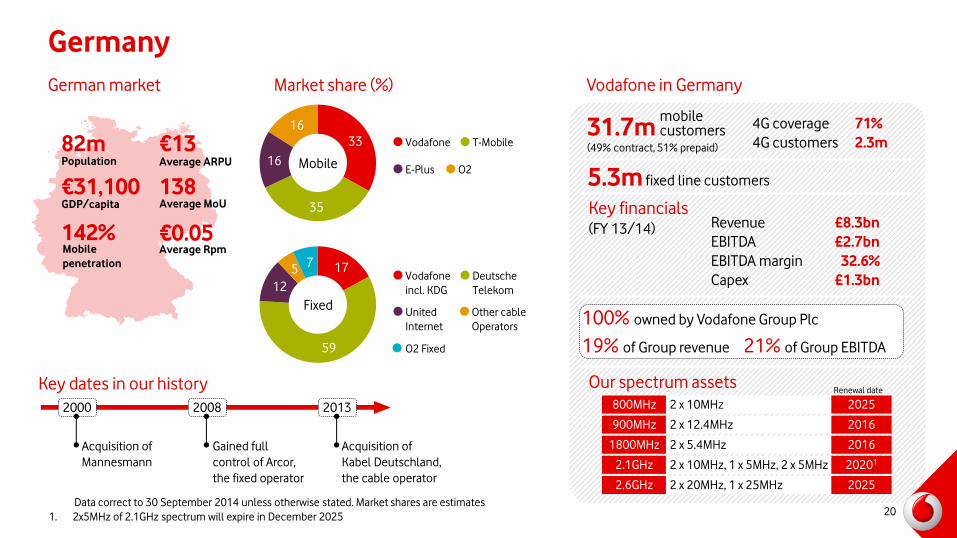

Our markets: Europe

17

59

12

5 7

Germany

20

82m Population

€13 Average ARPU

€31,100 GDP/capita Average MoU

142% Mobile

penetration

138

€0.05 Average Rpm

Key dates in our history

German market

33

35

16

16

Mobile

Fixed

Vodafone T-Mobile

E-Plus O2

2000 2008 2013

Acquisition of

Mannesmann

Gained full

control of Arcor,

the fixed operator

Acquisition of

Kabel Deutschland,

the cable operator

900MHz

1800MHz

2.6GHz

800MHz

2.1GHz

2 x 12.4MHz

2 x 5.4MHz

2 x 20MHz, 1 x 25MHz

2 x 10MHz

2 x 10MHz, 1 x 5MHz, 2 x 5MHz

2016

2016

2025

2025

20201

Renewal date

Data correct to 30 September 2014 unless otherwise stated. Market shares are estimates

1. 2x5MHz of 2.1GHz spectrum will expire in December 2025

Market share (%) Vodafone in Germany

31.7m mobile customers

(49% contract, 51% prepaid)

5.3m fixed line customers

4G coverage 71%

4G customers 2.3m

Key financials (FY 13/14) Revenue £8.3bn

EBITDA £2.7bn

EBITDA margin 32.6%

Capex £1.3bn

100% owned by Vodafone Group Plc

19% of Group revenue 21% of Group EBITDA

Our spectrum assets

Vodafone

incl. KDG

Deutsche

Telekom

United

Internet

Other cable

Operators

O2 Fixed

9

72

4 7

8

UK

21

65m Population

£17 Average ARPU

£24,400 GDP/capita Average MoU

122% Mobile

penetration

186

£0.04 Average Rpm

Key dates in our history

UK market

25

24 31

11 9

Mobile

Fixed

Enterprise

Vodafone O2 EE

3

900MHz

1800MHz

2.6GHz

800MHz

2.1GHz

2 x 17.4MHz

2 x 5.8MHz

2 x 20MHz, 1 x 25MHz

2 x 10MHz

2 x 14.8MHz

n/a1

n/a1

2033

2033

n/a1

Renewal date

Data correct to 30 September 2014 unless otherwise stated. Market shares are estimates

1. Indefinite license with a five year notice of revocation

Market share (%) Vodafone in the UK

19.7m mobile customers

(60% contract, 40% prepaid)

Consumer fixed line services to launch 2015

4G coverage 48%

4G customers 1.4m

Key financials (FY 13/14) Revenue £6.4bn

EBITDA £1.4bn

EBITDA margin 22.1%

Capex £0.9bn

100% owned by Vodafone Group Plc

15% of Group revenue 11% of Group EBITDA

Our spectrum assets

Vodafone BT

Virgin

Media

Colt

MVNOs

1985 2004 2012

Vodafone launched

the first mobile

network in the UK

3G services

launched

Acquisition of

Cable and Wireless,

the fixed operator

Others

Fixed

6

73

8

12 1

Italy

22

61m Population

€12 Average ARPU

€22,700 GDP/capita Average MoU

146% Mobile

penetration

230

€0.03 Average Rpm

Key dates in our history

Italian market

33

33

21

9 3

Mobile

Fixed

Vodafone Telecom Italia

Wind 3

900MHz

1800MHz

2.6GHz

800MHz

2.1GHz

2 x 10MHz

2 x 15MHz, 2 x 5MHz

2 x 15MHz

2 x 10MHz

2 x 15MHz, 1 x 5MHz

2015

20151

2029

2029

2021

Renewal date

Data correct to 30 September 2014 unless otherwise stated. Market shares are estimates

1. 2 x 5MHz of 1800MHz spectrum will expire in 2029

Market share (%) Vodafone in Italy

26.0m mobile customers

(19% contract, 81% prepaid)

4G coverage 64%

4G customers 1.0m

Key financials (FY 13/14) Revenue £4.3bn

EBITDA £1.5bn

EBITDA margin 35.6%

Capex £0.6bn

100% owned by Vodafone Group Plc

10% of Group revenue 12% of Group EBITDA

Our spectrum assets

MVNOs

2000 2007 2014

Acquisition of

Mannesmann included

Italian operations

Acquisition of TeleTu,

the fixed operator

Took ownership to 100%

1.8m fixed line customers

Vodafone

Wind Fastweb Tiscali

Telecom Italia

12

69

7 8

5

Spain

23

46m Population

€16 Average ARPU

€22,100 GDP/capita Average MoU

109% Mobile

penetration

174

€0.06 Average Rpm

Key dates in our history

Spanish market

30

34

22

5 9

Mobile

Fixed

Vodafone

incl. Ono

Telefonica

Orange Yoigo

900MHz

1800MHz

2.6GHz

800MHz

2.1GHz

2 x 11MHz

2 x 20MHz

2 x20MHz. 1 x 20MHz

2 x 10MHz1

2 x 15MHz, 1 x 5MHz

2028

2030

2030

2030

2030

Renewal date

Market share (%) Vodafone in Spain

14.8m mobile customers

(74% contract, 26% prepaid)

4G coverage 64%

4G customers 1.6m

Key financials1 (FY 13/14) Revenue £3.5bn

EBITDA £0.8bn

EBITDA margin 22.4%

Capex £0.5bn

100% owned by Vodafone Group Plc

8% of Group revenue 6% of Group EBITDA

Our spectrum assets

MVNOs

1999 2007 2014

Acquisition of AirTouch

included Spanish

operations

Acquisition of Tele2,

the fixed operator

Acquisition of Ono,

a cable operator

2.7m fixed line customers

Vodafone

incl. Ono

Telefonica

Jazztel Orange Others

Data correct to 30 September 2014 unless otherwise stated. Market shares are estimates

1. Not yet available for use

Netherlands

24

17m Population

€24 Average ARPU

€37,400 GDP/capita Average MoU

101% Mobile

penetration

159

€0.09 Average Rpm

Key dates in our history

Dutch market

31

39

23

7

Mobile

Fixed

Vodafone KPN

T Mobile MVNOs

900MHz

1800MHz

2.6GHz

800MHz

2.1GHz

2 x 10MHz

2 x 20MHz

2 x 10MHz

2 x 10MHz

2 x 20MHz, 1 x 5MHz

2030

2030

2030

2029

2030

Renewal date

Market share (%) Vodafone in the Netherlands

5.2m mobile customers

74% contract, 26% prepaid)

Key financials (FY 13/14) Revenue £1.6bn

EBITDA £0.5bn

EBITDA margin 34.1%

Capex £0.2bn

100% owned by Vodafone Group Plc

4% of Group revenue 4% of Group EBITDA

Our spectrum assets

1995 2003

Libertel launched

services

Vodafone acquires

full ownership of

Vodafone Libertel

Consumer fixed line services launched Sept 2014

1

45 54

Vodafone KPN

Others

Data correct to 30 September 2014 unless otherwise stated. Market shares are estimates

Portugal

25

10m Population

€10 Average ARPU

€14,800 GDP/capita Average MoU

159% Mobile

penetration

148

€0.05 Average Rpm

Key dates in our history

Portuguese market

38

40

21 1

Mobile

900MHz

1800MHz

2.6GHz

800MHz

2.1GHz

2 x 10MHz, 2 x 3MHz

2 x 6MHz, 2 x 14MHz

2 x 20MHz, 25MHz TDD

2 x 10MHz

2 x 20MHz

20211

20272

2027

2027

2016

Renewal date

Data correct to 30 September 2014 unless otherwise stated. Market shares are estimates

1. 2 x 3MHz of 900MHz spectrum will expire in 2015

2. 2 x 6MHz of 1800MHz spectrum will expire in 2021

Market share (%) Vodafone in Portugal

5.4m mobile customers

(26% contract, 74% prepaid)

Key financials (FY 13/14) Revenue £0.9bn

EBITDA £0.3bn

EBITDA margin 34.8%

Capex £0.2bn

100% owned by Vodafone Group Plc

2% of Group revenue 2% of Group EBITDA

Our spectrum assets

1992 2001 2003

Telecel launched

services

Rebranded to

Vodafone

Vodafone acquired full

ownership

0.3m fixed line customers

Vodafone Portugal Telecom

Optimus MVNOs

4

55

33

9

Vodafone Portugal Telecom

Optimus Others

Fixed

Greece

26

11m Population

€11 Average ARPU

€14,700 GDP/capita Average MoU

133% Mobile

penetration

231

€0.04 Average Rpm

Key dates in our history

Greek market

31

51

18

Mobile

1800MHz

2.1GHz

900MHz

2 x 15MHz, 2 x 10MHz

2 x 20MHz, 1 x 5MHz

2 x 15MHz

20261

2021

20271

Renewal date

Data correct to 30 September 2014 unless otherwise stated. Market shares are estimates

1. 2 x 15MHz of the 1800MHz spectrum will expire in August 2016

2. As of 31. December 2014, including Hellas Online

Market share (%) Vodafone in Greece

5.0m (32% contract, 68% prepaid)

Key financials (FY 13/14) Revenue £0.6bn

EBITDA £0.2bn

EBITDA margin 27.6%

Capex £0.1bn

99.9% owned by Vodafone Group Plc

1% of Group revenue 1% of Group EBITDA

Our spectrum assets

1992 2004 2014

Creation of Panafon

between four partners,

including Vodafone

Final increase in

Vodafone’s share of

the business

Acquisition of

Hellas Online

0.5m fixed line customers2

Vodafone Cosmote

Wind

10

64

16

6 4

Vodafone

(incl. HOL)

OTE

Forthnet Tellas

Fixed

CYTA

mobile customers

Romania

27

20m Population

$10,200 GDP/capita

106% Mobile

penetration

Key dates in our history

Romanian market1

38

19

43 Mobile

Data correct to 30 September 2014 unless otherwise stated. Market shares are estimates

1. IMF Database and World Bank estimates

Market share (%) Vodafone in Romania

7.9m (42% contract, 58% prepaid)

Key financials (FY 13/14)

Revenue £0.6bn

EBITDA £0.2bn

EBITDA margin 33.2%

Capex £0.1bn

100% owned by Vodafone Group Plc

1% of Group revenue 2% of Group EBITDA

2005 2006

Acquisition of Connex Rebranded to

Vodafone

Vodafone Cosmote

Orange

900MHz

1800MHz

2.6GHz

800MHz

2.1GHz

2 x 10MHz

2 x 30MHz

1 x 15MHz

2 x 10MHz

2 x 15MHz, 1 x 5MHz

2029

2029

2029

2029

2020

Renewal date Our spectrum assets

3

53 33

11

Vodafone Romtelecom

RCS & RDS UPC Fixed

mobile customers

Other Europe

Albania 2.0m mobile customers (5% contract, 95% prepaid)

Data correct to 30 September 2014 unless otherwise stated. Market shares are estimates

1. World Bank, 2013 estimates

2. IMF, 2011 estimates

Czech Republic 3.2m mobile customers (62% contract, 38% prepaid)

Hungary 2.6m mobile customers (55% contract, 45% prepaid)

Ireland 2.1m mobile customers (45% contract, 55% prepaid)

Malta 0.3m mobile customers (18% contract, 82% prepaid)

0.2m fixed line customers

Population GDP/capita Mobile

penetration1

Mobile market share

Fixed market

share

2.9m

11.0m

9.9m

4.8m

0.4m

$4,900

$19,000

$13,200

€37,300

$24,300

116%

131%

116%

103%

n/a

n/a

n/a

43%

n/a

16%

99.9% ownership

<1% of Group revenue

<1% of Group EBITDA

100% ownership

1% of Group revenue

1% of Group EBITDA

100% ownership

<1% of Group revenue

<1% of Group EBITDA

100% ownership

2% of Group revenue

2% of Group EBITDA

100% ownership

<1% of Group revenue

<1% of Group EBITDA

130%

n/a

n/a

n/a

n/a

28

Our markets: AMAP

India

30

1,243m Population

$1,500 GDP/capita

74% Mobile

penetration

Indian market

22

29 16

10

6

7 10

Mobile

Market share (%) Vodafone in India

173.8m mobile customers

(7% contract, 93% prepaid)

3G coverage 90%1

Data users 57.1m

Key financials (FY 13/14)

Revenue £4.4bn

EBITDA £1.4bn

EBITDA margin 31.8%

Capex £0.7bn

100% owned by Vodafone Group Plc

10% of Group revenue 11% of Group EBITDA

1800MHz

2.1GHz

900MHz

Varies by circle

Varies by circle

Varies by circle

2014-27

2030

2014-24

Renewal date Our spectrum assets

INR185

379

INR0.40 Average Rpm

Average ARPU

Average MoU

Key dates in our history

Data correct to 30 September 2014 unless otherwise stated. Market shares are estimates

1. Targeted urban areas only

2. 2 x 15MHz of the 1800MHz spectrum will expire in August 2016

2007 2011 2014

Acquisition of controlling

stake in Vodafone Essar

Renamed Vodafone

India Limited

Took ownership to 100%

Vodafone Airtel India IDEA Cellular

BSNL / MTNL

Reliance Tata

Others

Vodacom Group: South Africa

31

53m Population

$6,400 GDP/capita

147% Mobile

penetration

South African market

53

31

15 2

Mobile

Mobile market share (%) Vodacom in South Africa

39.9m mobile customers

(9% contract, 91% prepaid)

3G coverage 97%

Data users 16.7m

Vodacom Group* - Key financials (FY 13/14)

Revenue £4.7bn

EBITDA £1.7bn

EBITDA margin 36.4%

Capex £0.7bn

Vodacom Group 65% owned by Vodafone Group

Vodacom South Africa 94% owned by Vodacom Group

11% of Group revenue 13% of Group EBITDA

1800MHz

2.1GHz

900MHz

2 x 12MHz

2 x 15MHz, 1 x 5MHz

2 x 11MHz

n/a1

n/a1

n/a1

Renewal date Our spectrum assets

ZAR93

108

ZAR0.66 Average Rpm

Average ARPU

Average MoU

Key dates in our history

Data correct to 30 September 2014 unless otherwise stated. Market shares are estimates

1. Spectrum licenses renewed annually

1994 2009 2011

Launched its first

services

Became a subsidiary Rebranded to align with

Vodafone global brand

Vodafone MTN

CellC TelkomMobile *82% of FY 13/14 revenue was from Vodacom South Africa

Vodacom Group: Internationals

32

Data correct to 30 September 2014 unless otherwise stated. Market shares are estimates

1. Vodacom, 2014 estimates

2. Owned through Vodacom Group, which is 65% owned by Vodafone Group

Tanzania 11.3m mobile customers

Mozambique 4.9m mobile customers

DRC 11.0m mobile customers

Lesotho 1.1m mobile customers

Population GDP/capita Mobile

penetration1

Mobile market share

50.8m

26m

69m

2.1m

$770

$630

$410

$1,300

60%

45%

40%

70%

44%

36%

73%

82% ownership

85% ownership

51% ownership

80% ownership

46%

Vodacom % ownership2

Turkey

33

77m Population

$10,500 GDP/capita

92% Mobile

penetration

Turkish market

28

50

22

Mobile market share (%) Vodafone in Turkey

20.6m mobile customers

(39% contract, 61% prepaid)

3G coverage 83%

Data users 9.3m

Key financials (FY 13/14)

Revenue £2.0bn

EBITDA £0.4bn

EBITDA margin 17.7%

Capex £0.3bn

100% owned by Vodafone Group Plc

5% of Group revenue 3% of Group EBITDA

2.1GHz

900MHz

2 x 15MHz, 1 x 5MHz

2 x 11MHz

2029

2023

Renewal date Our spectrum assets

TRL22

348

TRL0.06 Average Rpm

Average ARPU

Average MoU

Key dates in our history

2005 2006 2009

Acquisition of Telsim Rebranded to

Vodafone

Vodafone Turkcell

Avea

3G services launched

Mobile

1

74

13

12

Fixed Vodafone

Super

Online

Others

Turk Telecom

Data correct to 30 September 2014 unless otherwise stated. Market shares are estimates

Egypt

34

84m Population

$3,300 GDP/capita

120% Mobile

penetration

Egyptian market

39

33

28

Mobile market share (%) Vodafone in Egypt

39.4m mobile customers

(6% contract, 94% prepaid)

3G coverage 92%

Data users 7.7m

Key financials (FY 13/14)

Revenue £1.2bn

EBITDA £0.5bn

EBITDA margin 44.4%

Capex £0.2bn

54.9% owned by Vodafone Group Plc

3% of Group revenue 4% of Group EBITDA

1800MHz

900MHz

2 x 10MHz

2 x 12.5MHz

2020

2020

Renewal date Our spectrum assets

EGP26

195

EGP0.11 Average Rpm

Average ARPU

Average MoU

Key dates in our history

1998 2006

Part Vodafone-owned

consortium started

services in Egypt

Increased ownership

to 54.9%

Vodafone Mobinil

Etisalat

2.1GHz 2 x 15MHz 2020

Mobile

Data correct to 30 September 2014 unless otherwise stated. Market shares are estimates

Our markets: other AMAP

Ghana 6.8m mobile customers (1% contract, 99% prepaid)

New Zealand 2.3m mobile customers (37% contract, 63% prepaid)

Qatar 1.4m mobile customers (9% contract, 91% prepaid)

Population GDP/capita Mobile

penetration Mobile

market share Fixed market

share

26m

4.5m

2.3m

$1,400

$44,300

$94,700

108%

124%

153%

19%1

47%

32%

70% ownership

<1% of Group revenue

<1% of Group EBITDA

100% ownership

2% of Group revenue

2% of Group EBITDA

22.95% ownership

<1% of Group revenue

<1% of Group EBITDA

0.4m fixed line customers

27%

n/a

n/a

Data correct to 30 September 2014 unless otherwise stated. Market shares are estimates

1. As of 30 June 2014 35

Our joint ventures and associates

Australia (joint venture)

4.9m mobile customers

Indus Towers (joint venture)

50% ownership

42% ownership (through Vodafone India)

• Incorporated in November 2007

• Builds infrastructure for the three shareholders and rents to 3rd parties

• Largest telecom tower company in the world

18

53

29

Mobile market share (%)

Vodafone

Telstra

Optus

• Merged with Hutchison in 2009 to form joint venture

• Number three operator

Safaricom (associate) 21.9m mobile customers (3% contract, 97% prepaid)

40% ownership

• Market leader in Kenya

• 12.8m M-Pesa users generating over 20% of total revenue

• 3,140 base stations (as of March 2014)

36 1. Data correct to 30 September 2014 unless otherwise stated. Market shares are estimates

Partner markets

37

Europe

The Group has partnership agreements with local mobile operators

in over 50 countries extending our reach beyond our equity investments

by enabling a range of our products and services to be marketed in

partnership territories

These partnerships create additional revenue through fees paid by the

partners for access to the Vodafone brand. Results are included within

‘Common Functions’ in our results

Austria

Armenia

Belgium

Bulgaria

Channel Islands

Croatia

Cyprus

Denmark

Estonia

Faroe Islands

Finland

Americas

Brazil

Canada

Chile

AMAP

Afghanistan

Bahrain

Fiji

French Polynesia

Guam

Hong Kong

Iraq

Japan

Jordan

Kuwait

Malaysia

Papua New Guinea & Solomon Islands

Philippines

Saudi Arabia

Singapore

South Korea

Sri Lanka

Taiwan

Thailand

Uganda

United Arab Emirates

Vietnam

France

Iceland

Latvia

Lithuania

Luxemburg

Macedonia/FYROM

Norway

Poland

Russia

Serbia

Slovenia

Sweden

Switzerland

Turkmenistan

Ukraine

More information

38 www.vodafone.com/investor

Visit our website for more information

For definitions of terms please see www.vodafone.com/content/index/investors/glossary

References

All data correct as of 30 September 2014 unless otherwise stated

All market share figures are internal estimates as of 30 September 2014

General market data from Bank of America Merrill Lynch Global Wireless Matrix, 31 October 2014 unless otherwise stated

GDP data from IMF, “World Economic Outlook Database”, October 2014

Follow us

on Twitter

Download our

iPad app

@VodafoneIR

Forward-looking statements

39

This presentation contains “forward-looking statements” within the meaning of the US Private Securities Litigation Reform Act of 1995 with respect to the

Group’s financial condition, results of operations and businesses and certain of the Group’s plans and objectives.

In particular, such forward-looking statements include, but are not limited to, statements with respect to: expectations regarding the Group’s financial

condition or results of operations, including the outlook for the 2015 financial year, or dividends; expectations for the Group’s future performance

generally, including EBITDA growth, free cash flow and capital expenditure; statements relating to the Group’s Project Spring investment programme;

expectations regarding the operating environment and market conditions and trends, including customer usage, competitive and macroeconomic

pressures, price trends and opportunities in specific geographic markets; growth in customers and usage; expectations regarding spectrum licences; and

expectations regarding adjusted operating profit, EBITDA margins, capital expenditure, free cash flow, and foreign exchange rate movements.

Forward-looking statements are sometimes, but not always, identified by their use of a date in the future or such words as “will”, “anticipates”, “aims”,

“could”, “may”, “should”, “expects”, “believes”, “intends”, “plans” or “targets” (including in their negative form). By their nature, forward-looking

statements are inherently predictive, speculative and involve risk and uncertainty because they relate to events and depend on circumstances that may or

may not occur in the future. There are a number of factors that could cause actual results and developments to differ materially from those expressed or

implied by these forward-looking statements.

A review of the reasons why actual results and developments may differ materially from the expectations disclosed or implied within forward-looking

statements can be found under the headings “Risk Factors” and “Other Information – Forward-looking statements” in our half year financial report for the

six months ended 30 September 2014 which can be found on the Group’s website (vodafone.com/investor). All subsequent written or oral forward-

looking statements attributable to the Company, to any member of the Group or to any persons acting on their behalf are expressly qualified in their

entirety by the factors referred to above. No assurances can be given that the forward-looking statements in or made in connection with this presentation

will be realised. Subject to compliance with applicable law and regulations, Vodafone does not intend to update these forward-looking statements and

does not undertake any obligation to do so.