Greenhouse Business Management Ben Beale Extension Educator-MCE St. Mary’s County Some slides...

83

Greenhouse Business Management Ben Beale Extension Educator-MCE St. Mary’s County Some slides adapted from Wei- Fe Uva; Cornell Extension

-

date post

21-Dec-2015 -

Category

Documents

-

view

217 -

download

3

Transcript of Greenhouse Business Management Ben Beale Extension Educator-MCE St. Mary’s County Some slides...

Greenhouse Business Management

Ben Beale

Extension Educator-MCE

St. Mary’s County

Some slides adapted from Wei-Fe Uva; Cornell Extension

Objectives

• Trends in Maryland Greenhouse Businesses

• Marketing Strategies for Greenhouse Businesses

• Financials-Enterprise Budgeting

Why do we care?

• Rising population base of affluent suburbanites in reach of Maryland growers

Source: Census 2000 analyzed by the Social Science Data Analysis Network (SSDAN).

1953-Agricultural land

1982

1992

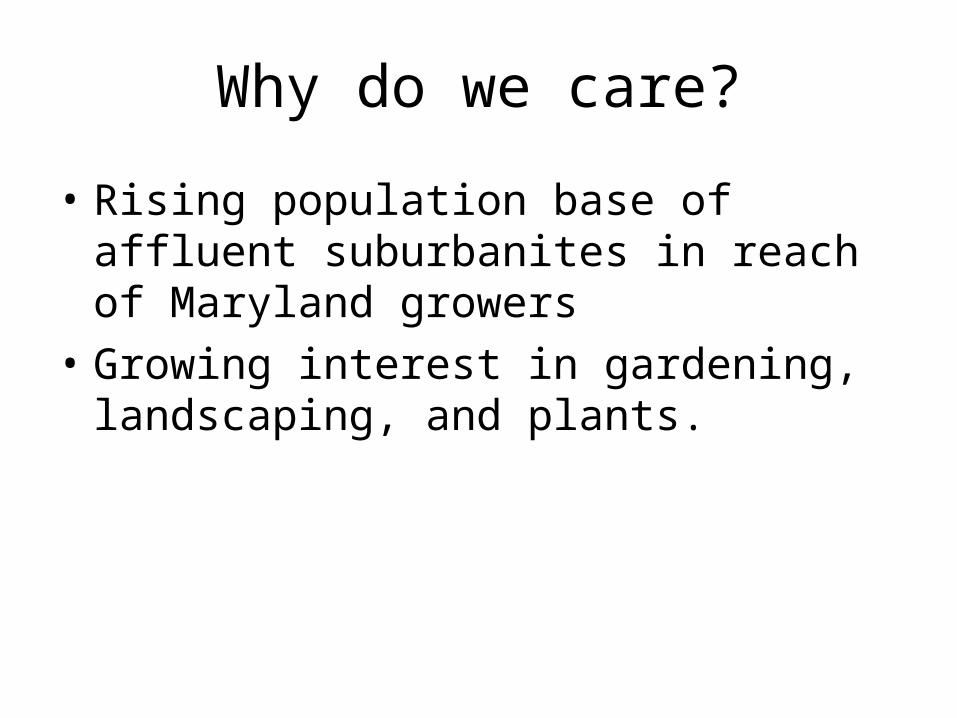

Why do we care?

• Rising population base of affluent suburbanites in reach of Maryland growers

• Growing interest in gardening, landscaping, and plants.

Why do we care?

• Rising population base of affluent suburbanites in reach of Maryland growers

• Growing interest in gardening, landscaping, and plants.

• Horticulture industry is the fastest growing sector in American Agriculture.

Greenhouse and nursery crops: Wholesale cash receipts

0.0 5.0 10.0 15.0 20.0

1992

1994

1996

1998

2000

2002

Billion dollars

Nursery and other greenhouse Floriculture

Production trends of floriculture crops

0

1,000

2,000

3,000

4,000

5,000

6,000

1994 1995 1996 1997 1998 1999 2000 2001 2002 2003

Mill

ion

$

bedding and garden plants potted flowering plants

foliage plants cut flowers

propagative material and cut greens

Floriculture crops: Average sales per grower

0

200,000

400,000

600,000

800,000

1,000,000

1,200,000

1,400,000

1,600,000

1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003

Do

llar

s

West South Midwest Northeast

Maryland

0

50,000

100,000

150,000

200,000

250,000

300,000

350,000

1994 1995 1996 1997 1998 1999 2000 2001 2002 2003

Maryland

ERS Data. $ in 1000. Greenhouse and Nursery Crops

Now for the Bad News!

• The majority of small businesses fail within the first 2 years.

• Most folks starting a greenhouse do so because they enjoy growing, not the business side.

The Importance of Management

SWOT analysis:

The SWOT analysis is simply a tool for organizing your thoughts and determining areas of competitive advantage.

Looks internally at:

•Strength

•Weaknesses

Looks externally at:

•Threats

•Opportunities

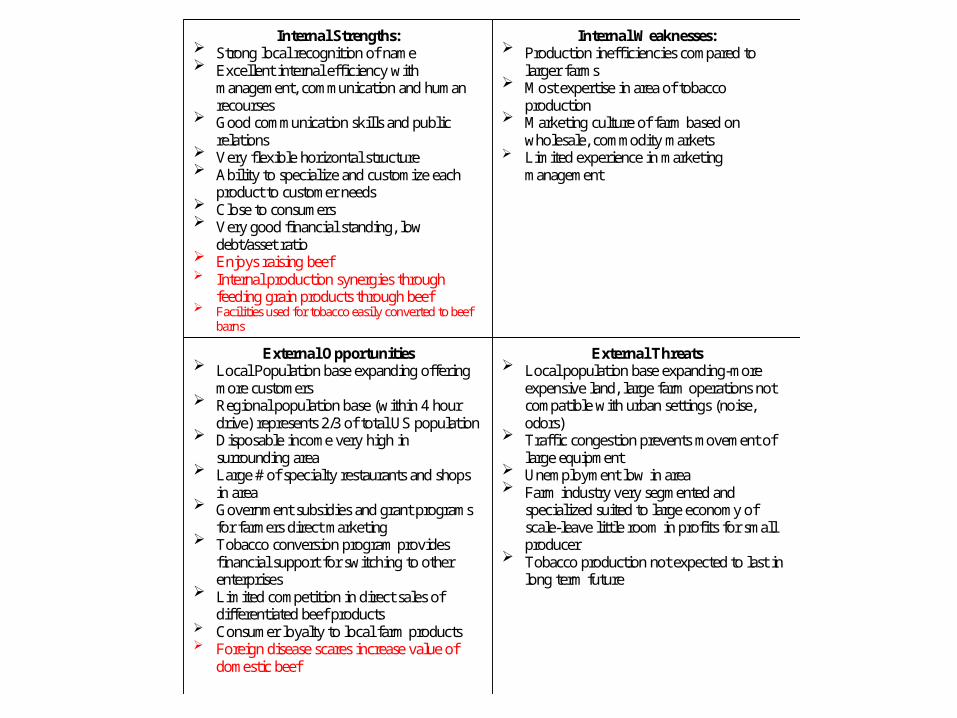

Internal Strengths: Strong local recognition of name Excellent internal efficiency with

management, communication and humanrecourses

Good communication skills and publicrelations

Very flexible horizontal structure Ability to specialize and customize each

product to customer needs Close to consumers Very good financial standing, low

debt/asset ratio Enjoys raising beef Internal production synergies through

feeding grain products through beef Facilities used for tobacco easily converted to beef

barns

External Opportunities Local Population base expanding offering

more customers Regional population base (within 4 hour

drive) represents 2/3 of total US population Disposable income very high in

surrounding area Large # of specialty restaurants and shops

in area Government subsidies and grant programs

for farmers direct marketing Tobacco conversion program provides

financial support for switching to otherenterprises

Limited competition in direct sales ofdifferentiated beef products

Consumer loyalty to local farm products Foreign disease scares increase value of

domestic beef

External Threats Local population base expanding-more

expensive land, large farm operations notcompatible with urban settings (noise,odors)

Traffic congestion prevents movement oflarge equipment

Unemployment low in area Farm industry very segmented and

specialized suited to large economy ofscale-leave little room in profits for smallproducer

Tobacco production not expected to last inlong term future

Internal Weaknesses: Production inefficiencies compared to

larger farms Most expertise in area of tobacco

production Marketing culture of farm based on

wholesale, commodity markets Limited experience in marketing

management

Overall objective-profit

Strength of SMP

Success of Execution

SMP not good

Execution not goodFigure 1

Cornell Greenhouse Cornell Greenhouse Business Summary, 2000 Business Summary, 2000

- Growing Greenbacks in Your - Growing Greenbacks in Your GreenhouseGreenhouse

Wen-fei Uva and Steve RichardsDepartment of Applied Economics and Management

Cornell University

http://hortmgt.aem.cornell.edu/resources/presentations.htm

2000 Greenhouse Businesses Profile2000 Greenhouse Businesses Profile• 29 New York Greenhouses

– 12 Eastern NY– 11 Central NY– 6 Western NY

• Marketing Channel: – 14 mainly wholesale, 15 mainly retail

• Major Crops:– 21 produced mainly bedding/garden plants– 5 produced mainly potted flowers– 1 greenhouse vegetables & herbs– 1 propagative material, 1 cut flowers

Size of Greenhouses Surveyed

01234567

1,440 15,580 29,720 43,860 More

Size (sq ft)

fre

qu

en

cy

Wen-fei Uva and Steve RichardsDepartment of Applied Economics and ManagementCornell University

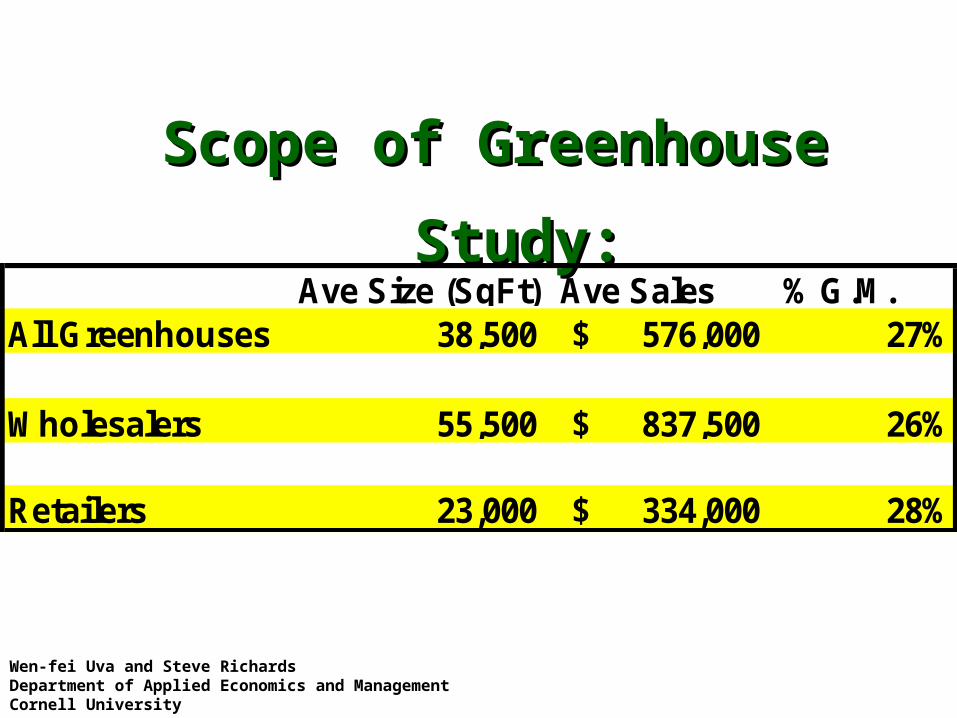

Scope of Greenhouse Study:Scope of Greenhouse Study:

Ave Size (SqFt) Ave Sales % G.M.All Greenhouses 38,500 576,000$ 27%

Wholesalers 55,500 837,500$ 26%

Retailers 23,000 334,000$ 28%

Wen-fei Uva and Steve RichardsDepartment of Applied Economics and ManagementCornell University

Wholesale Greenhouse 2000 Income Statement

WHOLESALE FIRMS >50% Amount Per Sq Foot % of SalesSales 843,403 14.67$ 100%Less: Cost of Goods Sold 664,711 11.10$ 74%Accrual Gross Margin 178,693 3.58$ 26%

Less: Overhead Expenses 162,473 2.98$ 20%Accrual Net Income 16,219 0.60$ 6%

Wen-fei Uva and Steve RichardsDepartment of Applied Economics and ManagementCornell University

Cost of Goods Sold: Wholesale

• Labor 44%

• Plant Material 23%

• Packaging Materials 11%

• Heating 6%

• All Other COGS 16%

Wen-fei Uva and Steve RichardsDepartment of Applied Economics and ManagementCornell University

Overhead Expenses: Wholesale

• Land Rent 18%

• Repairs 18%

• Depreciation 17%

• Insurance 12%

• Interest 12%

• Other Overhead 23%

Wen-fei Uva and Steve RichardsDepartment of Applied Economics and ManagementCornell University

Retail Greenhouse 2000 Income Statement

RETAIL GREENHOUSES Amount Per Sq Foot % of SalesIncome 304,510 13.90$ 100%Less: Cost of Goods Sold 219,612 10.56$ 73%Accrual Gross Margin 84,898 3.35$ 27%

Overhead Expenses 49,564 2.64$ 23%Accrual Net Income 35,334 0.71$ 3%

Wen-fei Uva and Steve RichardsDepartment of Applied Economics and ManagementCornell University

Cost of Goods Sold: Retail

• Labor 37%

• Plant Material 27%

• Hard Goods 7%

• Heating 6%

• All Other COGS 23%

Wen-fei UvaDepartment of Applied Economics and ManagementCornell University

Overhead Expenses: Retail

• Depreciation 20%

• Insurance 18%

• Miscellaneous 15%

• Interest 13%

• Repairs 11%

• Other Overhead 23%

Wen-fei Uva and Steve RichardsDepartment of Applied Economics and ManagementCornell University

Average Balance Sheet

ALL GREENHOUSES Year Start Year EndASSETS

Current Assets 176,429 187,411 Intermediate Assets 72,846 65,269 Long Term Assets 191,999 187,694

Total Assets 441,274 440,374

LIABILITIESCurrent Liabilities 54,895 53,404 Intermediate Liabilities 23,660 13,872 Long Term Liabilities 110,718 131,115

Total Liabilities 189,274 198,391

Net Worth (Assets-Liabilities) 252,000 241,983

Average Cash Flow Statement

Cash Flow From Operating ActivitiesCash Farm Income 56,127 Less: Cash Withdrawals 44,747

Net Provided From Operations 11,380 Cash Flow From Investing ActivitiesSale of Assets 5,167 Less: Capital Purchases 18,657

Net Provided From Investing (13,491) Cash Flow From Financing ActivitiesCash Inflow From Financing 35,890 Less: Cash Outflow From Financing 27,587

Net Provided From Financing 8,304 Cash Flow From Reserves

Beginning Cash/Checking/Savings 46,733

Less: Ending Cash/Check/Savings 47,515

Net Provided From Reserves (782)

IMBALANCE 5,411

First Question-What is marketing?

• Marketing is:– Organizing the resources of the firm toward understanding

customers needs and wants and offering products and/or services that meet those needs. (Russell Winer-Marketing Management)

– The purpose of a business is to create and keep a customer. To do that you have to produce and deliver goods and services that people value and want at prices and under conditions that are reasonably attractive relative to those offered by others to a proportion of customers large enough to make those prices and conditions possible. (Theodore Levitt-Marketing Theorist)

– Doing something for someone(s) better than another can in order to make a profit. (Ben’s farm guess)

Marketing Functions:

•Price

•Product

•Promotion

•Distribution

Products

PricePlace

Promotion

TargetMarket

Marketing is finding, developing, and profiting from opportunities

Your target markets will determine your production and marketing practices, Not vise versa.

Slide From: Wen-fei UvaDepartment of Applied Economics and ManagementCornell University

Low- Cost leadership Focus-Niche Strategy based on low cost

Best-Cost provider

Focus strategy based on differentiation

Broad differentiation

Low Cost/Low Price

Differentiation

Broad Narrow / Focused

What Opportunities Exist?

• Low-Cost Provider Strategy– Target Market: Chain Super Market and Box

Stores– Large Operations with market partnering

agreements– Mass market with commodity type pricing– Efficiency based

Wholesale Production-Contract Production

• Agreement with landscape and retail operations for production of particular or specialized cultivars– Contractors/builders– Smaller individual retail centers– On-site location advantages

Service Oriented Opportunities

• Production of material plus installation or service agreement– Landscaping-Production of “landscape

pillows” for high end market– Pick your own/ Plant a tree service– Rentals items -Parties, special occasions,

seasonal items, interior-scaping. Mostly container production.

– Interior-scapes

Wholesale Production-Specialty Items (differentiated strategy)

• Competitive advantage in being able to produce a product of substantial attributes that outside, larger producers can not.

• Such attributes include:– Quality– Delivery flexibility– Specialized cultivars branded for specific area– Value added features

• Ability to predict future trends and customer desires

Finding your niche-Getting things in the right place.

Name of the Game:Name of the Game:Niche MarketingNiche Marketing

• Identify marketsIdentify markets

• Determine special needsDetermine special needs

• Position yourself to serve those marketsPosition yourself to serve those markets

• Find out what the larger producers can’t Find out what the larger producers can’t supply: What is too small for them?supply: What is too small for them?

• Look for ways to differentiate your product, Look for ways to differentiate your product, not only from what you grow, but how you not only from what you grow, but how you grow it, what you do with it, or how you grow it, what you do with it, or how you package it, or market it.package it, or market it.

Some Examples of Current Some Examples of Current Niche Market TrendsNiche Market Trends

• Fresh, in-season local produceFresh, in-season local produce

• Color, (white eggplants, blue potatoes)Color, (white eggplants, blue potatoes)

• Nostalgia, (traditional American comfort Nostalgia, (traditional American comfort foods, i.e. corn-on-cob, corn bread, foods, i.e. corn-on-cob, corn bread, vegetable varieties from several years vegetable varieties from several years ago)ago)

• Organic foods, people believe it is saferOrganic foods, people believe it is safer

• Edible and cut flowersEdible and cut flowers

Where are folks selling?

• Farmer Owned farmers market

• Community farmers markets

• Direct sales to local stores

• Sales to supermarket chains

• Sales to wholesalers and brokers

• On-farm sales• Contract growers

Developing an Enterprise Budget

GREENHOUSE BEDDING PLANTS (24'X100' DOUBLE LAYER PLASTIC) PER ACRE FOR YEAR 2006ITEM UNIT QUANTITY PRICE TOTAL

GROSS INCOMEBEDDING PLANTS FLATS 2100 $7.00 ######### -$ TOTAL GROSS INCOME #########VARIABLE COSTSSOIL MIX CUBIC FEET 500 $3.60 1,800.00$ CUTTINGS FLATS 2100 $1.00 2,100.00$ FLATS FLATS 2100 $0.33 693.00$ INSERTS FLATS 2100 $0.30 630.00$ PLASTIC COLOR TAGS PACK 20000 $0.02 400.00$ NITROGEN POUND 50 $0.34 17.00$ LIQUID FEED NUTRIENTS POUND 50 $1.00 50.00$ PLASTIC COVER (40'X100'-2LAYERS-$600/3YRS/0.5YR) ROLL 2 $300.00 100.00$

BANROT POUND 4 $31.00 124.00$ INSECTICIDES, MITICIDES 1 $60.00 $60.00UTILITIES (ELEC. FUEL-OIL) 100 $19.00 $1,900.00HAULING FLATS 2100 $0.20 $420.00LABOR HOURS 600 $7.00 4,200.00$

-$

Department of Applied Economics and ManagementCornell UniversityIthaca, NY 14853

Dr. Wen-fei UvaSenior Extension Associate

What is Your Profitability? What is Your Profitability?

- - Using Financial Records to Using Financial Records to Improve Business PerformanceImprove Business Performance

What Is Financial What Is Financial Management?Management?

• The ability to allocate financial resources in the areas which generate the greatest returnsgreatest returns.

• Financial Management DecisionsYou Need to Make:

* Pricing Your Product* Pricing Your Product

• One of the most critical components of marketing. A common concern!

• Critical in achieving sales and profitability

• Need to know your COSTS

* Making Business * Making Business DecisionsDecisions

• Are your sales covering your costs?

• Which product lines generate the most income?

• Should you operate year-round or shut down in the winter?

• Contributions to fixed costs

• Optimum mix of product lines

• Goal setting and increased efficiency

* Making Investment * Making Investment DecisionsDecisions

• Input substitution

Capital for labor: installing automated irrigation system or not?

Buying vs. raising your own bedding plants

• Enterprise changes

Whether or not to sell a particular product

Adding another operation to your business

• What is the best investment for my money

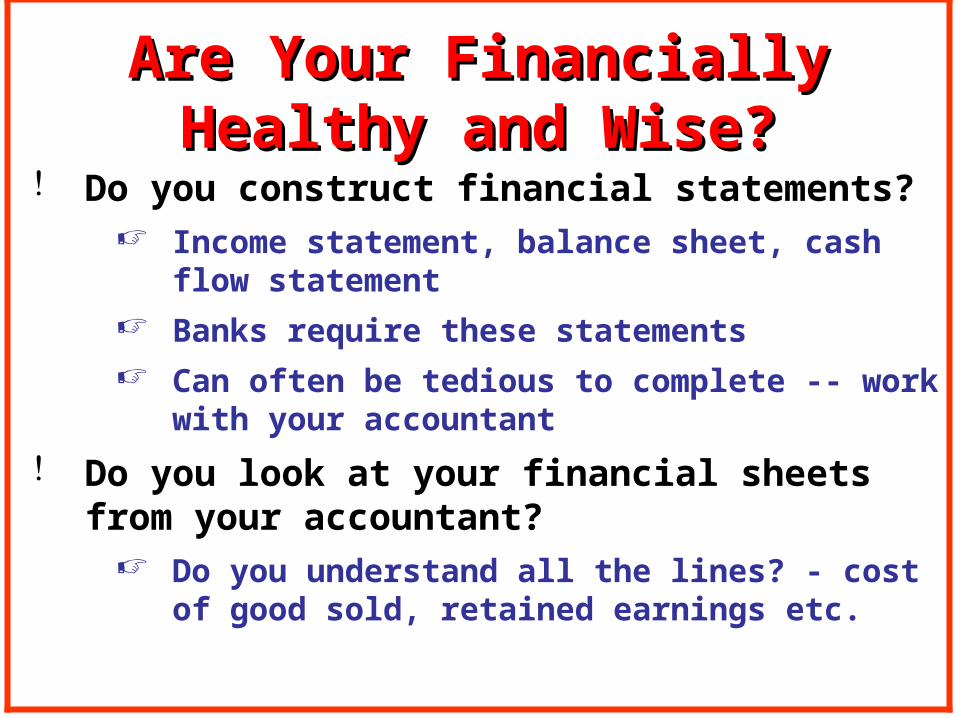

Are Your Financially Healthy Are Your Financially Healthy and Wise?and Wise?

Do you keep good financial records?

Keep records for more than just taxes!

Use a computer program!

Financial information should be at your fingertips at all times

Are Your Financially Healthy Are Your Financially Healthy and Wise?and Wise?

Do you construct financial statements? Income statement, balance sheet, cash

flow statement

Banks require these statements

Can often be tedious to complete -- work with your accountant

Do you look at your financial sheets from your accountant?

Do you understand all the lines? - cost of good sold, retained earnings etc.

Do You Perform Financial Analysis?

Cost analysis - costs to operate the business and profitability

Ratio analysis - Gross Margin Return On Investment, Return on Asset, Inventory Turns

Enterprise analysis - What is your most profitability product line?

Are Your Financially Healthy Are Your Financially Healthy and Wise?and Wise?

Do you know how your business compare with industry benchmarks How do you compare to other firms in the

industry? - Gross Margin, Inventory Turns, Profit Margin

Set performance goals Track your performance over time (trend

analysis)

Repeat process annually

Are Your Financially Healthy Are Your Financially Healthy and Wise?and Wise?

Calculating Calculating Production CostsProduction Costs

• A Record Keeping System for You

• Pricing for Profit

Expenses Records Variable costsVariable costs: cost items that vary with production volume

(Direct and Indirect).

Costs of plant materials, pots, soil, hourly labor, advertising.

Fixed costsFixed costs: cost items that do not vary with production volume (Overhead costs).

Costs of rent, property taxes, management salary and family living expenses.

Allocate these costs to each product could be tricky (by floor space, time in store, etc.)

25 to 50% of total costs.

Expenses Records - cont. Marketing costsMarketing costs:

Advertising, packaging, shipping, billing, and special promotion, display, etc.

It could also be assigned to variable and fixed costs, but why look at it separately?

Production efficiency vs. marketing efficiency

5 to 15% of total costs

ProfitProfit

Pricing for ProfitPricing for Profit

Variable CostsVariable Costs

Fixed CostsFixed Costs

Price Price (Revenue)(Revenue)

Contribution

Break-even

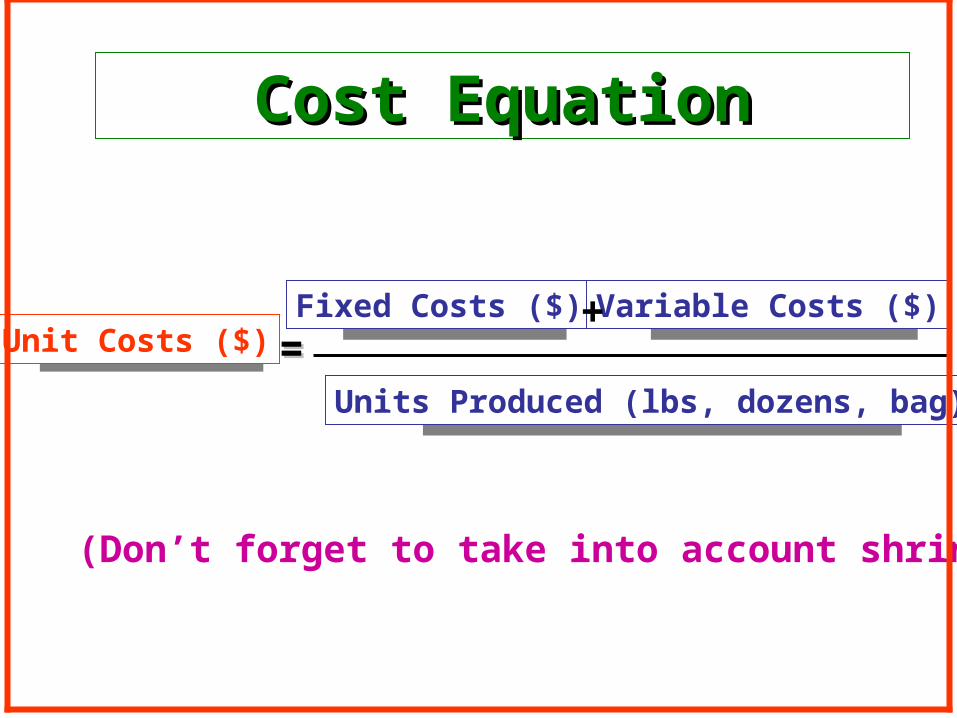

Cost EquationCost Equation

Unit Costs ($) ==Fixed Costs ($) Variable Costs ($)+

Units Produced (lbs, dozens, bag)

(Don’t forget to take into account shrinkage)

Analyze Enterprise ProfitabilityAnalyze Enterprise Profitability

Step 1: Determine How You Want to Allocate the Fixed Costs

# total sq.ft. Weeks inoperation

Total square ft. weeksin operation

Greenhouse 18,000 25 450,000

Outdoor display 50,000 28 1,400,000

Gift shop 5,000 45 225,000

4 0

5 0

Totals 68,500 2,075,000

By Area & Length of Operation

Step 2: Calculate SFW Needed for a Enterprise

(ex. 5,000 pots of 4” Geraniums)

Product Location SquareFeet

Weeks SFW

Geranium Greenhousespacing A

5,000 4 20,000

Geranium Greenhousespacing B

10,000 4 40,000

Geranium OutdoorDisplay

10,000 4 40,000

TOTAL 100,000

Step 3: Calculate Costs - Direct Variable Costs

Direct Variable Costs $ Amount

Seeds or plants $ 750

Potted soil 100

Fertilizer and Chemicals 50

Packaging material 150

Direct labor 2,000

TOTAL FOR THIS PRODUCT LINE $ 3,050

Step 3: Calculate Costs - Indirect Variable Costs

Indirect Variable Costs $ Amount Total Sq. Ft. Week $/Sq. Ft. Week

Electricity $ 8,000 2,075,000 $ 0.00386

Trucking 2,400 2,075,000 0.00116

Telephone 1,000 2,075,000 0.00048

Water 500 2,075,000 0.00024

Fuel 1,000 2,075,000 0.00048

Heating for Greenhouse 2,000 450,000 0.00444

Hourly Labor 65,000 2,075,000 0.03133

Advertising 2,000 Annually orspecial event?

2,075,0000.0096

TOTAL 0.05159

Step 3: Calculate Costs - Fixed Costs

Fixed Costs $ Amount Total Sq. Ft. Week $/Sq. Ft. Week

Management Salary 50,000 2,075,000 0.02410

Interest 15,616 2,075,000 0.00753

Depreciation 5,497 2,075,000 0.00265

Insurance 5,102 2,075,000 0.00246

Building and Equipment M/R 2,779 2,075,000 0.00134

Property Taxes 8,025 2,075,000 0.00387

Leases and Rental 10,879 2,075,000 0.00524

Office Supplies 2,991 2,075,000 0.00144

Professional Fee 2,123 2,075,000 0.00102

Misc. 4,000 2,075,000 0.00193

Family Expenses & BankPrincipal Payments

20,000

TOTAL 0.05157

Step 4: Calculate Enterprise Profitability

Revenue

Price per Unit $ 3.25

Units Sold (Take into consideration shrinkage) 4,800

TOTAL REVENUE $ 15.600

Expenses

Direct Variable Costs (COGS) $ 3,050

Indirect Variable Costs (100,000 SFW * $0.05159/SFW) = $ 5,159

Fixed (Overhead) Costs (100,000 SFW * $0.05157/SFW) = $ 5,157

TOTAL EXPENSES $ 13,366

ENTERPRISE PROFIT 2,134

Step 5: Breakeven Analysis

Variable Costs per UnitSold

($3,050 + $5,159) / 4,800= $1.71

Consider discontinueif below thisnumber

Overhead Costs per UnitSold

$5,157 / 4,800 = $1.07 Need to cover thisnumber

Total Cost per Unit $1.71 + $1.07 = $2.78 Breakeven price

Profit per Unit Sold (4,800pots)

$1.01

Profit per Unit Grown(5,000 pots)

$0.97

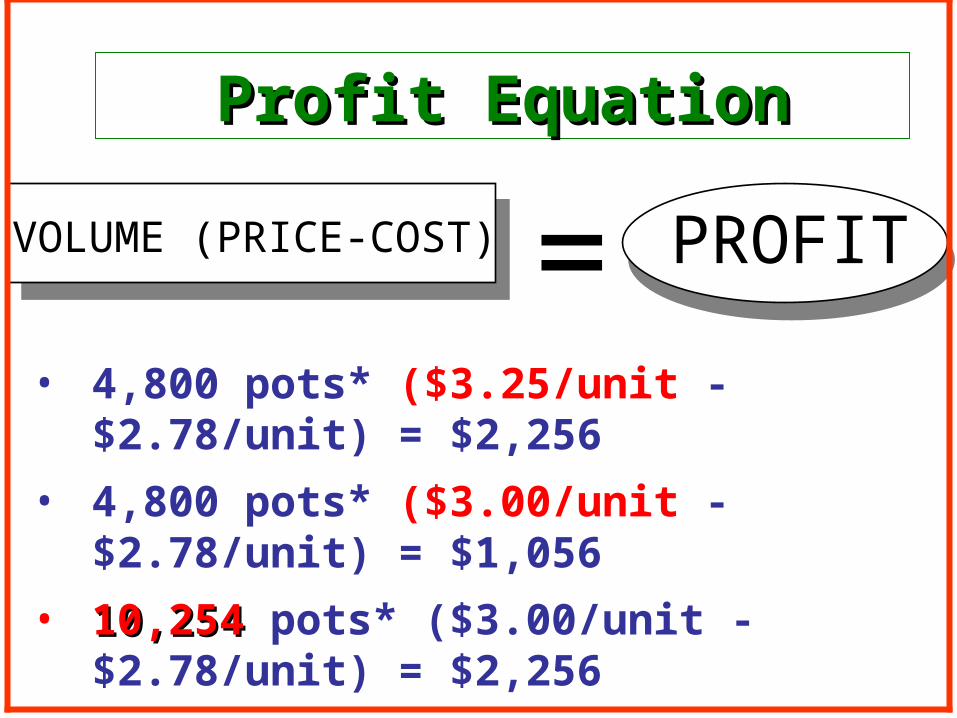

=VOLUME (PRICE-COST) PROFIT

Profit EquationProfit Equation

• 4,800 pots* ($3.25/unit - $2.78/unit) = $2,256

• 4,800 pots* ($3.00/unit - $2.78/unit) = $1,056

• 10,25410,254 pots* ($3.00/unit - $2.78/unit) = $2,256

• For $250,000 in sales, a 4% price increase (4 cent increase for every dollar) give you $10,000 more profit.

Evaluating Business Evaluating Business ProfitabilityProfitability

• Financial Ratios

• Efficiency Measures

Financial RatiosFinancial Ratios

• Profitability Ratios

• Gross Margin: (Revenue - Variable Costs) Revenue -- (around 50%)

• Profit Margin: (Revenue - Total Costs) Revenue -- (around 10-15%)

• Return on Assets

• Net Business Income Average Total Assets

• How efficient are you using your resources to produce income.

Financial RatiosFinancial Ratios• Inventory Ratio (3.5)

• Cost of Good Sold Average Inventory• How fast are you turnover your inventory

• Liquidity• Current Ratio: Current Liability Current

Assets• Your ability to cover current debt (liability)

• Solvency• Debt-to Asset Ratio: Total Liability Total

Assets• The percentage of the business’s assets to which

creditors have claim.

Efficiency MeasuresEfficiency Measures• Operating Efficiency

• Sales per Full Time Worker Equivalent• Net Income pre FT Worker Equivalent• Sales per Square Foot

• Cost Efficiency• Labor as percent of sales• Operating expenses as percent of sales• Costs per square foot (or square foot week)

• Profitability• Net Income per Owner• Net Income per Owner Hour• Net Income per Square Foot

http://aede.ag.ohio-state.edu/people/moore.301/index.htm

So get ready, hold on and enjoy the ride. The trying is half the fun.

And after all the hard work, you get to reap the benefit of your efforts!

The End