Greece’s need of durable rebalancing...ees. However, the high drama should not de-tract from the...

12

ECONOMIC POLICY NOTE 27/4/2015 Greece’s need of durable rebalancing AGNIESZKA GEHRINGER The discussion about Greece has intensified in recent months. Greece is running out of time in its search for fresh cash to serve its external debt and to pay wages to public sector employ- ees. However, the high drama should not de- tract from the fundamental problem of the Greek economy. In the present paper, we have a closer look at the development of the country’s current ac- count. The key findings are: (i) The deterioration of the current account before the debt crisis was largely due to excess demand. Thanks to productivity growth, exports were stable or even in- creased. (ii) The subsequent decline of the current ac- count deficit was primarily achieved by ag- gregate demand contraction. Only more recently, the real exchange rate fell owing to a decline in nominal wages and prices. (iii) To support growth, expenditure reducing policies should be supplemented with ex- penditure switching policies. Generally, this is best achieved through a nominal devalu- ation. As this is not possible in EMU, intro- duction of a parallel currency for domestic use might help. 1 (iv) To make the gain in competitiveness per- manent, the Greek economy needs more investment in new capacities and technol- ogies. In order to enable such investment, the business environment must be im- proved. The nature of the Greek current account defi- cits Starting in 1994, the Greek economy entered a period of high and persistent current account deficits. Easy credit conditions after the intro- duction of the euro in 2001 induced ever higher deficits (Fig. 1 and 2). 1 See Thomas Mayer (2015), A Parallel Currency for Greece, Flossbach von Storch AG Research Institute, Eco- nomic policy note 4/2015.

Transcript of Greece’s need of durable rebalancing...ees. However, the high drama should not de-tract from the...

ECONOMIC POLICY NOTE 27/4/2015

Greece’s need of durable rebalancing

AGNIESZKA GEHRINGER

The discussion about Greece has intensified in

recent months. Greece is running out of time in

its search for fresh cash to serve its external

debt and to pay wages to public sector employ-

ees. However, the high drama should not de-

tract from the fundamental problem of the

Greek economy.

In the present paper, we have a closer look at

the development of the country’s current ac-

count. The key findings are:

(i) The deterioration of the current account

before the debt crisis was largely due to

excess demand. Thanks to productivity

growth, exports were stable or even in-

creased.

(ii) The subsequent decline of the current ac-

count deficit was primarily achieved by ag-

gregate demand contraction. Only more

recently, the real exchange rate fell owing

to a decline in nominal wages and prices.

(iii) To support growth, expenditure reducing

policies should be supplemented with ex-

penditure switching policies. Generally, this

is best achieved through a nominal devalu-

ation. As this is not possible in EMU, intro-

duction of a parallel currency for domestic

use might help. 1

(iv) To make the gain in competitiveness per-

manent, the Greek economy needs more

investment in new capacities and technol-

ogies. In order to enable such investment,

the business environment must be im-

proved.

The nature of the Greek current account defi-

cits

Starting in 1994, the Greek economy entered a

period of high and persistent current account

deficits. Easy credit conditions after the intro-

duction of the euro in 2001 induced ever higher

deficits (Fig. 1 and 2).

1 See Thomas Mayer (2015), A Parallel Currency for

Greece, Flossbach von Storch AG Research Institute, Eco-

nomic policy note 4/2015.

2

Easy credit permitted Greek households, firms

and the government to finance consumption

and all kinds of investment, not all of it produc-

tive. As a result, domestic demand rose dispro-

portionally faster than supply.

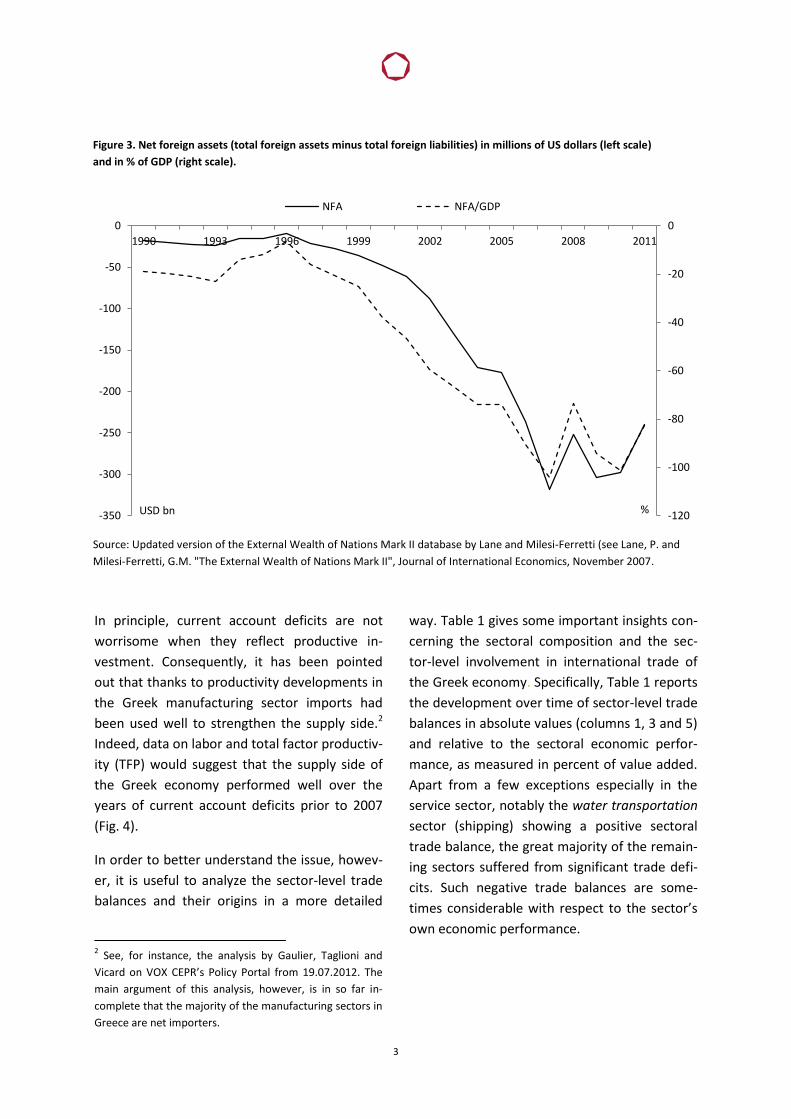

As this excess of demand was covered by net

inflows of financial capital from abroad year

after year, Greece saw its external debt worsen-

ing substantially over time (Fig. 3).

Figure 1. Ten years bond yields (right scale) and current account balance (left scale) in Greece.

Source: IMF World Economic Outlook and Eurostat.

Figure 2. MFI lending to the private sector in Greece.

Source: Haver.

0

5

10

15

20

25

30

-15

-13

-11

-9

-7

-5

-3

-1

1

3

1990 1994 1998 2002 2006 2010 2014

% % of GDP Current account balance bond yields

0

50

100

150

200

250

300

1990 1993 1996 1999 2002 2005 2008 2011 2014

EUR bn

3

In principle, current account deficits are not

worrisome when they reflect productive in-

vestment. Consequently, it has been pointed

out that thanks to productivity developments in

the Greek manufacturing sector imports had

been used well to strengthen the supply side.2

Indeed, data on labor and total factor productiv-

ity (TFP) would suggest that the supply side of

the Greek economy performed well over the

years of current account deficits prior to 2007

(Fig. 4).

In order to better understand the issue, howev-

er, it is useful to analyze the sector-level trade

balances and their origins in a more detailed

2 See, for instance, the analysis by Gaulier, Taglioni and

Vicard on VOX CEPR’s Policy Portal from 19.07.2012. The

main argument of this analysis, however, is in so far in-

complete that the majority of the manufacturing sectors in

Greece are net importers.

way. Table 1 gives some important insights con-

cerning the sectoral composition and the sec-

tor-level involvement in international trade of

the Greek economy. Specifically, Table 1 reports

the development over time of sector-level trade

balances in absolute values (columns 1, 3 and 5)

and relative to the sectoral economic perfor-

mance, as measured in percent of value added.

Apart from a few exceptions especially in the

service sector, notably the water transportation

sector (shipping) showing a positive sectoral

trade balance, the great majority of the remain-

ing sectors suffered from significant trade defi-

cits. Such negative trade balances are some-

times considerable with respect to the sector’s

own economic performance.

Figure 3. Net foreign assets (total foreign assets minus total foreign liabilities) in millions of US dollars (left scale)

and in % of GDP (right scale).

Source: Updated version of the External Wealth of Nations Mark II database by Lane and Milesi-Ferretti (see Lane, P. and

Milesi-Ferretti, G.M. "The External Wealth of Nations Mark II", Journal of International Economics, November 2007.

-120

-100

-80

-60

-40

-20

0

-350

-300

-250

-200

-150

-100

-50

0

1990 1993 1996 1999 2002 2005 2008 2011

% USD bn

NFA NFA/GDP

4

This is shown in the second, fourth and sixth

column of Table 1, where the sectoral trade

balance is reported in percentage of sectoral

value added. Finally and most importantly, for

many sectors the situation deteriorated be-

tween 1995 and 2007. This was especially the

case for both chronic deficit sectors, like coke &

petroleum, construction, hotels & restaurants3,

public administration and health, as well as ear-

lier surplus sectors, like agriculture – all of

which weigh considerably in the economy-wide

trade balance. These data show that prior to the

financial crisis most sectors of the economy

were running current account deficits. In princi- 3 The strongly negative numbers for this sector, which

constitutes a large part of the tourism activities, are quite

surprising. They imply that much more Greek citizens

abroad than foreigners in Greece bought hotel and restau-

rant services.

ple, three different forces could play a role

here: diminishing exports but stable imports, in-

creasing imports but stable exports, or imports

increasing faster than exports. The data suggest

that for the majority of sectors, the fast growing

imports were accompanied by stable or even

increasing exports (Fig. 5). Imports thus clearly

reflected growing domestic expenditures driven

by easy credit conditions. For exports, the pic-

ture is in line with the growing aggregate

productivity shown in Figure 4. Export sectors

were overall able to compete internationally

and offer stable or growing amounts of goods

and services abroad.

Figure 4. Productivity developments in Greece.

Note: Total factor productivity (TFP) and labor productivity are indexes with 2010=100 for TFP and 2005=100 for labor

productivity. TFP is calculated as a Solow residual and expresses the part of output growth that cannot be explained by

growth in standard inputs (labor and capital). Labor productivity is expressed in terms of output per employed person.

Source: TFP is taken from AMECO Macroeconomic Database; labor productivity is taken from Haver.

70

75

80

85

90

95

100

105

110

115

1990 1993 1996 1999 2002 2005 2008 2011 2014

Index values

TFP Labor productivity

5

Table 1. Sectoral trade balance (exports – imports).

1995 2007 2011

Mio. € % VA Mio. € % VA Mio. € % VA

Agriculture 438 4.1 -65 -0.7 -52 -0.6

Mining 79 11.8 -1.424 -115.0 -38 -3.5

Food 77 2.0 -869 -12.5 -741 -7.8

Textiles -3 -0.1 326 17.7 -74 -3.0

Leather -57 -30.9 -29 -11.0 12 5.6

Wood -74 -16.4 -157 -31.7 -67 -16.7

Pulp & Paper -420 -45.3 -476 -26.2 -475 -22.3

Coke & Petroleum -1.123 -281.9 -7.958 -487.1 -6.088 -293.8

Chemicals -445 -42.4 540 35.3 439 27.1

Rubber & Plastics -168 -35.1 -59 -5.8 -10 -1.1

Other Non-minerals 55 6.1 -132 -7.1 33 2.3

Metals -134 -10.9 -1.377 -41.8 -141 -4.4

Machinery -102 -20.3 -68 -5.8 188 21.2

Electrical & Optical Eq. -440 -100.9 -157 -11.8 112 13.4

Transport Eq. -295 -53.0 -369 -36.9 22 2.2

Other Manufact. -57 -6.7 182 18.4 -337 -25.9

Electricity, Gas & Water Supply -227 -6.6 -583 -8.1 -391 -5.5

Construction -1.661 -23.2 -4.458 -25.0 -3.118 -25.7

Sale, Maintenance & Repair 16 0.5 99 1.3 102 1.5

Wholesale Trade 4 0.0 -104 -0.5 -107 -0.5

Retail Trade 122 2.0 348 2.2 312 2.0

Hotels & Restaurants -562 -7.2 -2.022 -10.5 -1.654 -8.4

Inland Transport -356 -16.9 -836 -24.5 -797 -22.0

Water Transport 1.197 273.6 18.329 129.7 13.614 121.1

Air Transport -61 -4.9 963 59.8 453 35.0

Other Transport 77 16.6 152 6.0 1.659 78.0

Post & Telecommunications 49 1.7 230 2.8 205 2.7

Financial Interm. -7 -0.1 2 0.0 -113 -0.8

Real Estate -86 -0.6 -264 -0.9 -316 -1.1

Renting & Business Activities -154 -3.5 -51 -0.6 99 1.1

Public Administration -1.331 -13.1 -3.123 -13.4 -2.830 -10.8

Education -12 -0.2 -190 -1.1 -161 -0.9

Health -563 -12.8 -2.936 -24.1 -3.427 -27.8

Other Services -180 -4.0 -917 -8.7 -810 -6.9

Note: See Appendix for a detailed list of sectoral full names.

6

Figure 5. Sectoral trade balances (solid line), imports (dotted line) and exports (dashed line), in

millions of euro.

-400

0

400

800

1200

1600

2000

1995 1998 2001 2004 2007 2010

Agriculture

trade balance exports imports

-2000

-1000

0

1000

2000

3000

4000

1995 1998 2001 2004 2007 2010

Food

-500

0

500

1000

1500

2000

1995 1998 2001 2004 2007 2010

Textiles

-1000

-500

0

500

1000

1995 1998 2001 2004 2007 2010

Pulp & Paper

-15000

-10000

-5000

0

5000

10000

15000

1995 1998 2001 2004 2007 2010

Coke & Petroleum

-1000

-500

0

500

1000

1500

2000

2500

3000

1995 1998 2001 2004 2007 2010

Chemicals

-400

-200

0

200

400

600

1995 1998 2001 2004 2007 2010

Other Non-minerals

-2000

-1000

0

1000

2000

3000

4000

5000

6000

1995 1998 2001 2004 2007 2010

Metals

7

Figure 5. Cont.

-1000

-500

0

500

1000

1995 1998 2001 2004 2007 2010

Electricity, Gas & Water Suppl.

-6000

-4000

-2000

0

2000

4000

6000

8000

1995 1998 2001 2004 2007 2010

Construction

-100

0

100

200

300

400

500

600

1995 1998 2001 2004 2007 2010

Sales, Maintenance & Repair

-500

0

500

1000

1500

2000

2500

3000

3500

1995 1998 2001 2004 2007 2010

Wholesale Trade

-500

0

500

1000

1500

2000

1995 1998 2001 2004 2007 2010

Retail Trade

-3000

-2000

-1000

0

1000

2000

3000

1995 1998 2001 2004 2007 2010

Hotels & Restaurants

-1500

-1000

-500

0

500

1000

1500

2000

1995 1998 2001 2004 2007 2010

Inland Trasport

-500

0

500

1.000

1.500

2.000

2.500

1995 1998 2001 2004 2007 2010

Air Trasport

8

Figure 5. Cont.

Note: The Figure shows data relative to the sectors which produce more than one percent of the economy-wide output (as for 1995; the relative importance of the sectors remains almost invariant over time). Source: Own elaborations based on World Input Output Database.

-100

0

100

200

300

400

500

600

700

1995 1998 2001 2004 2007 2010

Post & Telecommunications

-400

-200

0

200

400

600

800

1000

1995 1998 2001 2004 2007 2010

Financial Interm.

-400

-300

-200

-100

0

100

200

300

400

1995 1998 2001 2004 2007 2010

Real Estate

-500

0

500

1000

1500

2000

1995 1998 2001 2004 2007 2010

Renting and Business Activities

-6000

-4000

-2000

0

2000

4000

6000

1995 1998 2001 2004 2007 2010

Public Administration

-300

-200

-100

0

100

200

300

400

1995 1998 2001 2004 2007 2010

Education

-6000

-4000

-2000

0

2000

4000

6000

1995 1998 2001 2004 2007 2010

Health

-1500

-1000

-500

0

500

1000

1500

1995 1998 2001 2004 2007 2010

Other Services

9

There are, however, a few important excep-

tions from this general pattern. In the case of

coke & petroleum, electricity, gas & water

supply, construction, hotels & restaurants, and

public administration imports were much

stronger and outperforming exports substan-

tially. This suggests that a quite considerable

part of imports flew towards sectors not able to

contribute to a future rebalancing of the

economy-wide current account.

The way ahead for Greece

The analysis of the sectoral trade balances and

their origins confirm that the past current

account deficits in Greece were strongly driven

by excessive demand dynamics, which reflected

the artificially low interest rates in the wake of

accession to EMU and loose fiscal policies.

Exports, by contrast, followed an overall stable

development, which reflected the positive

productivity dynamics of the Greek economy.

Although the current account deficits

disappeared in the recent crisis period, the risk

of reversal is still present, once the economy

recovers. A rebalancing of the Greek current

account is therefore strongly required.

How can such a rebalancing be achieved? There

are not many options left for Greece.

If Greece remains in EMU, the only possibility is

an internal devaluation accompanied by

decisive austerity.

The only alternative to painful internal

devaluation is complete or partial (i.e., through

the introduction of a parallel currency for

domestic use) EMU exit and external

devaluation. In the end, the new Greek

government will have to make a choice between

these two options.

Durably rebalancing the current account

While external devaluation would help in the

indispensable transformation process, it is at

the same time insufficient for a durable

rebalancing of the Greek current account and

long-lasting growth. The rebalancing

immediately following the external devaluation

can only be seen as a first and temporary effect

due to changing relative prices. A durable

rebalancing requires a long-term perspective

and dedicated entrepreneurial efforts to search,

select and undertake profitable investments for

the creation of an economic structure, able to

compete internationally. The crucial ingredient

of such a dynamic process should be the

continuous involvement in innovation activities,

according to the highest international

standards.

In this respect, Greece is much lagging behind

the EU average. The recent results of the EU

Innovation Union Scoreboard 2014 show that in

terms of a composite indicator, the Summary

Innovation Index, Greece scores at around 70%

of the EU average and belongs to the group of

the so called “moderate innovators”, behind

Portugal, Spain, Czech Republic and Italy.

Although in absolute terms of the innovation

index Greece has been improving over time, the

performance relative to the EU average has

declined in the crisis years. Similarly, R&D

expenditures by business are among the lowest

in the EU. Finally, in terms of knowledge-

intensive exports, Greece remains among the

worst performing member states.

Since innovative ventures are characterized by a

high degree of uncertainty over the final

outcome of entrepreneurial activity and

additionally are connected with high costs,

there is a need for the creation and

maintenance of a stable and friendly business

environment. In this respect, efforts should be

10

directed towards the removal of the residual

barriers to business activities in Greece. These

barriers are of different nature. Specifically,

firms in Greece have problems getting financing,

face difficulties in establishing collaborations,

struggle with barriers to commercialization, pay

high costs of accessing new markets etc. The

results of the most recent issue of Community

Innovation Survey reports that 37% of

innovative firms in industrial sectors, 38% in

core innovative activities and 39% in core in-

novative service activities consider the lack of

adequate finance as a highly important barrier

to innovation. In contrast, only around 13% of

innovative firms from across all sectors

considered the access to adequate finance as

not being relevant. Similarly, high costs of

access to new markets were a highly important

barrier to innovation for 32% of innovative firms

in the industrial sectors, for 25% in core

innovation activities and for 20% in core

innovation service activities.

Substantial improvements in microeconomic

structure are required also elsewhere.

Regarding the ease of doing business Greece

ranks 61 in the total of 189 countries

worldwide.

Among the different categories of difficulties

that firms face, enforcing contracts (rank 155)

and registering property (rank 116) constitute

the most serious ones. Other important

adjustments should be directed towards the

improvement in country’s governance

landscape. According to the World Bank’s

estimates, Greece scores poorly in terms of

almost all dimensions: control of corruption (in

2013 the country ranked in the 55.5 percentile),

political stability and no violence (39.3), rule of

law (63.5), government effectiveness (67.0) and

regulatory quality (72.7). Finally, closed

professions, low labor force participation and

corruption open further fields of necessary

interventions.

Conclusion

In our view, Greece needs a two-pronged

strategy: a reduction of excess demand (which

has been largely achieved) and an improvement

of economic efficiency and competitiveness

(which so far has proven elusive). Exchange rate

depreciation, through full or partial EMU exit,

could bring necessary relief. But comprehensive

reform of the supply side is needed to achieve

lasting economic growth.

11

Appendix

Full names of industrial sectors

Abbreviated names Full names

Agriculture Agriculture, Hunting, Forestry and Fishing

Mining Mining and Quarrying

Food Food, Beverages and Tobacco

Textiles Textiles and Textile Products

Leather Leather, Leather and Footwear

Wood Wood and Products of Wood and Cork

Pulp & Paper Pulp, Paper, Paper , Printing and Publishing

Coke & Petroleum Coke, Refined Petroleum and Nuclear Fuel

Chemicals Chemicals and Chemical Products

Rubber & Plastic Rubber and Plastics

Other Non-minerals Other Non-Metallic Mineral

Metals Basic Metals and Fabricated Metal

Machinery Machinery, Nec

Electrical & Optical Eq. Electrical and Optical Equipment

Transport Eq. Transport Equipment

Other Manufact. Manufacturing, Nec; Recycling

Electricity, Gas & Water Supply Electricity, Gas and Water Supply

Construction Construction

Sales, Maintenance & Repair Sale, Maintenance and Repair of Motor Vehicles and Motorcycles; Retail Sale of Fuel

Wholesale Trade Wholesale Trade and Commission Trade, Except of Motor Vehicles and Motorcycles

Retail Trade Retail Trade, Except of Motor Vehicles and Motorcycles; Repair of Household Goods

Hotels & Restaurants Hotels and Restaurants

Inland Transport Inland Transport

Water Transport Water Transport

Air Transport Air Transport

Other Transport Other Supporting and Auxiliary Transport Activities; Activities of Travel Agencies

Post & Telecommunications Post and Telecommunications

Finance Financial Intermediation

Real Estate Real Estate Activities

Renting & Business Activities Renting of M&Eq and Other Business Activities

Public Administration Public Admin and Defence; Compulsory Social Security

Education Education

Health Health and Social Work

Other Services Other Community, Social and Personal Services

12

Reprinting or making the content publicly available – in particular by including it in third-party websites – together with

reproduction on data storage devices of any kind requires the prior written consent of Flossbach von Storch AG.

Legal notice

The information contained and opinions expressed in this document reflect the views of the author at the time of publica-

tion and are subject to change without prior notice. Forward-looking statements reflect the judgement and future expecta-

tions of the author. The opinions and expectations found in this document may differ from estimations found in other

documents of Flossbach von Storch AG. The above information is provided for informational purposes only and without any

obligation, whether contractual or otherwise. This document does not constitute an offer to sell, purchase or subscribe to

securities or other assets. The information and estimates contained herein do not constitute investment advice or any

other form of recommendation. All information has been compiled with care. However, no guarantee is given as to the

accuracy and completeness of information and no liability is accepted. Past performance is not a reliable indicator of fu-

ture performance.

All authorial rights and other rights, titles and claims (including copyrights, brands, patents, intellectual property rights and

other rights) to, for and from all the information in this publication are subject, without restriction, to the applicable provi-

sions and property rights of the registered owners. You do not acquire any rights to the contents. Copyright for contents

created and published by Flossbach von Storch AG remains solely with Flossbach von Storch AG. Such content may not be

reproduced or used in full or in part without the written approval of Flossbach von Storch AG.

© 2015 Flossbach von Storch. All rights reserved.

Site information

Publisher: Flossbach von Storch AG, Research Institute, Ottoplatz 1, 50679 Cologne, Germany; Phone +49 221 33 88-291,

[email protected], Directors: Dr. Bert Flossbach, Kurt von Storch, Dirk von Velsen; Registration: No. 30 768 in the Com-

mercial and Companies Register held at Cologne District Court; VAT-No. DE200075205; Supervisory authority: German

Federal Financial Services Supervisory Authority, Marie-Curie-Straße 24 – 28, 60439 Frankfurt / Graurheindorfer Straße 108,

53117 Bonn, www.bafin.de; Authors: Agnieszka Gehringer, PhD; Editorial deadline: 27/4/2015