GRAP Guideline 5 - Borrowing Costs

18

Accounting Guideline GRAP 5 Borrowing Costs All rights reserved. No part of this publication may be reproduced, stored in retrieval system, or transmitted, in any form or by any means, electronic mechanical, photocopying, recording, or otherwise, without the prior permission of the National Treasury of South Africa. Permission to reproduce limited extracts from the publication will not usually be withheld. Though National Treasury (NT) believes reasonable efforts have been made to ensure the accuracy of the information contained in the guideline, it may include inaccuracies or typographical errors and may be changed or updated without notice. NT may amend these guidelines at any time by posting the amended terms on NT's Web site. Note that this document is not part of the GRAP standard. The GRAP takes precedence while this guideline is used mainly to provide further explanations on the concepts already in the GRAP.

Transcript of GRAP Guideline 5 - Borrowing Costs

Accounting Guideline

GRAP 5

Borrowing Costs

All rights reserved. No part of this publication may be reproduced, stored in retrieval system, or transmitted, in any form or by any means, electronic

mechanical, photocopying, recording, or otherwise, without the prior permission of the National Treasury of South Africa.

Permission to reproduce limited extracts from the publication will not usually be withheld.

Though National Treasury (NT) believes reasonable efforts have been made to ensure the accuracy of the information contained in the guideline, it

may include inaccuracies or typographical errors and may be changed or updated without notice. NT may amend these guidelines at any time by

posting the amended terms on NT's Web site.

Note that this document is not part of the GRAP standard. The GRAP takes precedence while this guideline is used mainly to provide further

explanations on the concepts already in the GRAP.

GRAP 5 – Borrowing Costs

January 2014 Page 2 Page 2

Contents

1. INTRODUCTION ........................................................................................................... 3

2. SCOPE .......................................................................................................................... 4

3. BIG PICTURE ................................................................................................................ 5

4. IDENTIFICATION .......................................................................................................... 7

5. INITIAL RECOGNITION AND MEASUREMENT ............................................................ 8

5.1 Capitalising or expensing borrowing costs .................................................................. 8

5.2 Borrowing costs eligible for capitalisation ................................................................... 8

5.3 Specific borrowings .................................................................................................... 8

5.4 General borrowings .................................................................................................. 10

5.5 Deferred settlement terms ........................................................................................ 11

5.6 When to capitalise borrowing costs .......................................................................... 13

6. SUBSEQUENT MEASUREMENT ................................................................................ 15

6.1 Cessation of capitalisation of borrowing costs .......................................................... 15

6.2 Suspending capitalisation of borrowing costs ........................................................... 15

7. DISCLOSURE ............................................................................................................. 16

8. SUMMARY OF KEY PRINCIPLES............................................................................... 18

GRAP 5 – Borrowing Costs

January 2014 Page 3 Page 3

1. INTRODUCTION

This document provides guidance on the accounting treatment of borrowing costs.

The content should be read in conjunction with GRAP 5 (issued July 2007).

For purposes of this guide, “entities” refer to the following bodies to which the standards of GRAP relate to, unless specifically stated otherwise:

Public entities

Constitutional institutions

Municipalities and all other entities under their control

Parliament and the provincial legislatures

Explanation of images used in the manual:

Definition

Take note

Management process and decision making

Example

GRAP 5 – Borrowing Costs

January 2014 Page 4 Page 4

2. SCOPE

GRAP 5 is applicable to all entities preparing their financial statements on the accrual basis of accounting to account for borrowing costs.

The following falls outside the scope of GRAP 5:

Actual or imputed cost of net assets;

Borrowing cost incurred to acquire, construct or produce a qualifying asset measured at fair value; and

Inventories produced in large quantities on a repetitive basis.

GRAP 5 – Borrowing Costs

January 2014 Page 5 Page 5

3. BIG PICTURE

GRAP 5 – Borrowing Costs

January 2014 Page 6 Page 6

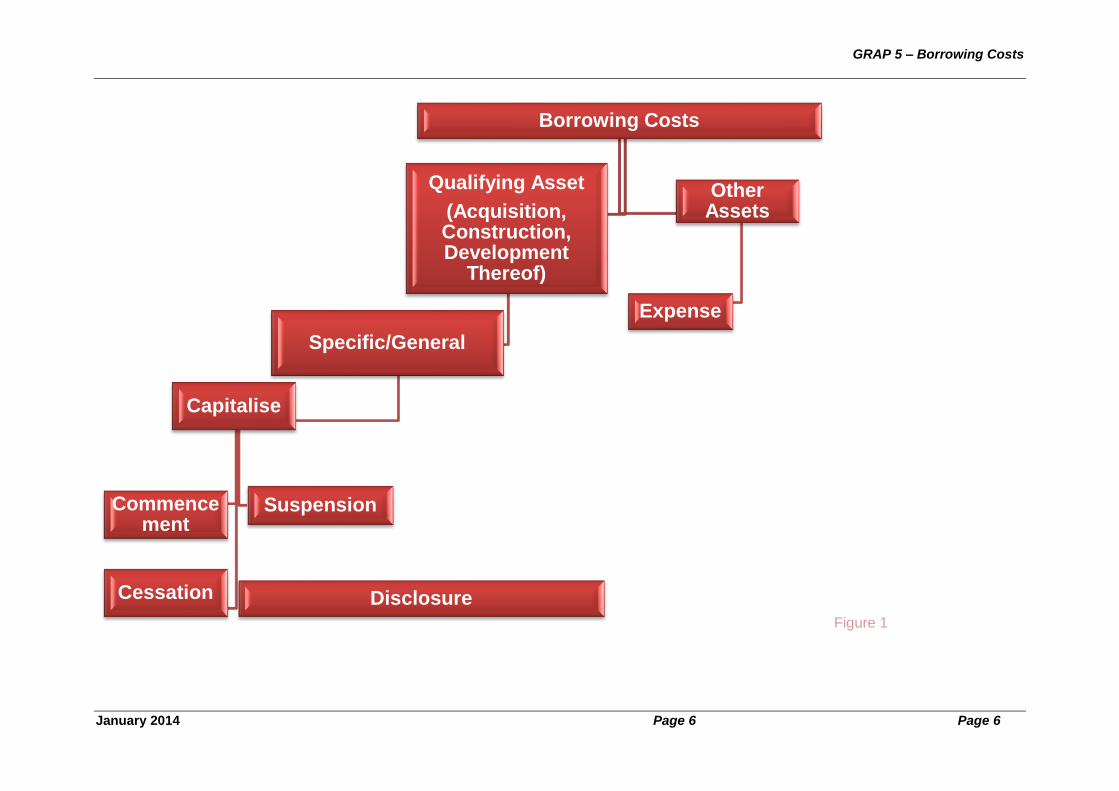

Figure 1

Borrowing Costs

Qualifying Asset

(Acquisition, Construction, Development

Thereof)

Specific/General

Capitalise

Commencement

Suspension

Cessation

Other Assets

Expense

Disclosure

GRAP 5 – Borrowing Costs

January 2014 Page 7

4. IDENTIFICATION

Borrowing costs are interest and other costs that an entity incurs in connection with the borrowing of funds.

Examples include, interest on bank overdrafts, short- and long-term borrowings, as well as finance charges in respect of finance leases recognised under GRAP 13 on Leases.

A qualifying asset in accordance with GRAP 5 is an asset that necessarily takes a substantial period of time to get ready for its intended use or sale.

Examples include property, plant and equipment that are manufactured or constructed, which can include buildings, infrastructure assets such as roads, bridges and power generation facilities, and inventories that takes a substantial period to complete.

The following are not qualifying assets:

Inventories produced in large quantities on a repetitive basis or inventories produced over a short period of time;

Investment property measured at fair value;

Biological assets;

Assets that is ready for their intended use or sale on acquisition date.

‘Substantial period’ is not defined in GRAP 5, therefore judgement needs to be exercised by management in order to determine if the period of acquisition, construction or production of a qualifying asset is substantial or not.

GRAP 5 – Borrowing Costs

January 2014 Page 8

5. INITIAL RECOGNITION AND MEASUREMENT

5.1 Capitalising or expensing borrowing costs

Borrowing costs that are directly attributable to the acquisition, construction or production of a qualifying asset should be capitalised to the cost of the asset. All other borrowing costs should be recognised as an expense in the period in which it is incurred.

Situations may arise where it is difficult to link the borrowing requirement of an entity directly to the nature of the expenditure to be funded. For example, an entity borrows funds for the construction of an office building and to incur maintenance on the buildings currently owned. In such a situation, the entity might be unable to distinguish whether the borrowings were incurred for capital or current expenditure.

Any borrowing cost incurred under such circumstances should be recognised as an expense.

5.2 Borrowing costs eligible for capitalisation

As stated earlier, only borrowing costs incurred that are directly attributable to the acquisition, construction of production of a qualifying asset can be capitalised to the cost of the asset.

GRAP 5 identifies two types of borrowings (i.e. specific and general) for which the amount of borrowing costs to be capitalised will differ depending on the type of borrowings. These are discussed in more detail below.

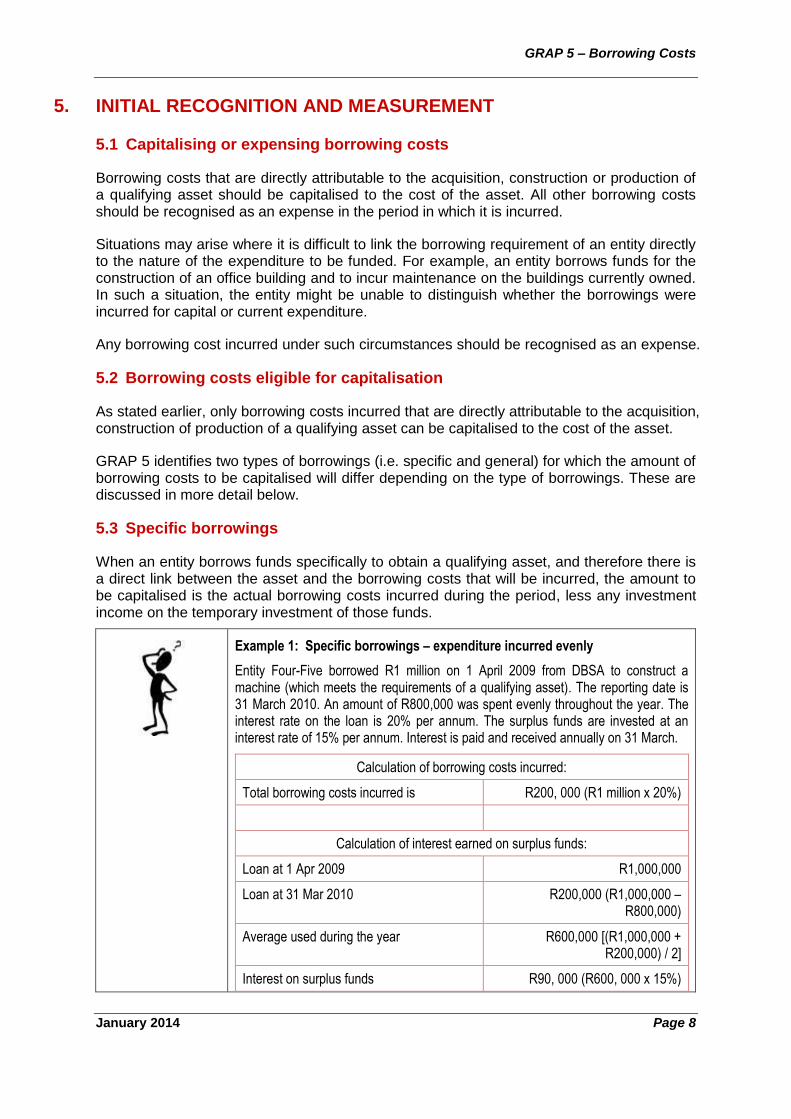

5.3 Specific borrowings

When an entity borrows funds specifically to obtain a qualifying asset, and therefore there is a direct link between the asset and the borrowing costs that will be incurred, the amount to be capitalised is the actual borrowing costs incurred during the period, less any investment income on the temporary investment of those funds.

Example 1: Specific borrowings – expenditure incurred evenly

Entity Four-Five borrowed R1 million on 1 April 2009 from DBSA to construct a machine (which meets the requirements of a qualifying asset). The reporting date is 31 March 2010. An amount of R800,000 was spent evenly throughout the year. The interest rate on the loan is 20% per annum. The surplus funds are invested at an interest rate of 15% per annum. Interest is paid and received annually on 31 March.

Calculation of borrowing costs incurred:

Total borrowing costs incurred is R200, 000 (R1 million x 20%)

Calculation of interest earned on surplus funds:

Loan at 1 Apr 2009 R1,000,000

Loan at 31 Mar 2010 R200,000 (R1,000,000 – R800,000)

Average used during the year R600,000 [(R1,000,000 + R200,000) / 2]

Interest on surplus funds R90, 000 (R600, 000 x 15%)

GRAP 5 – Borrowing Costs

January 2014 Page 9

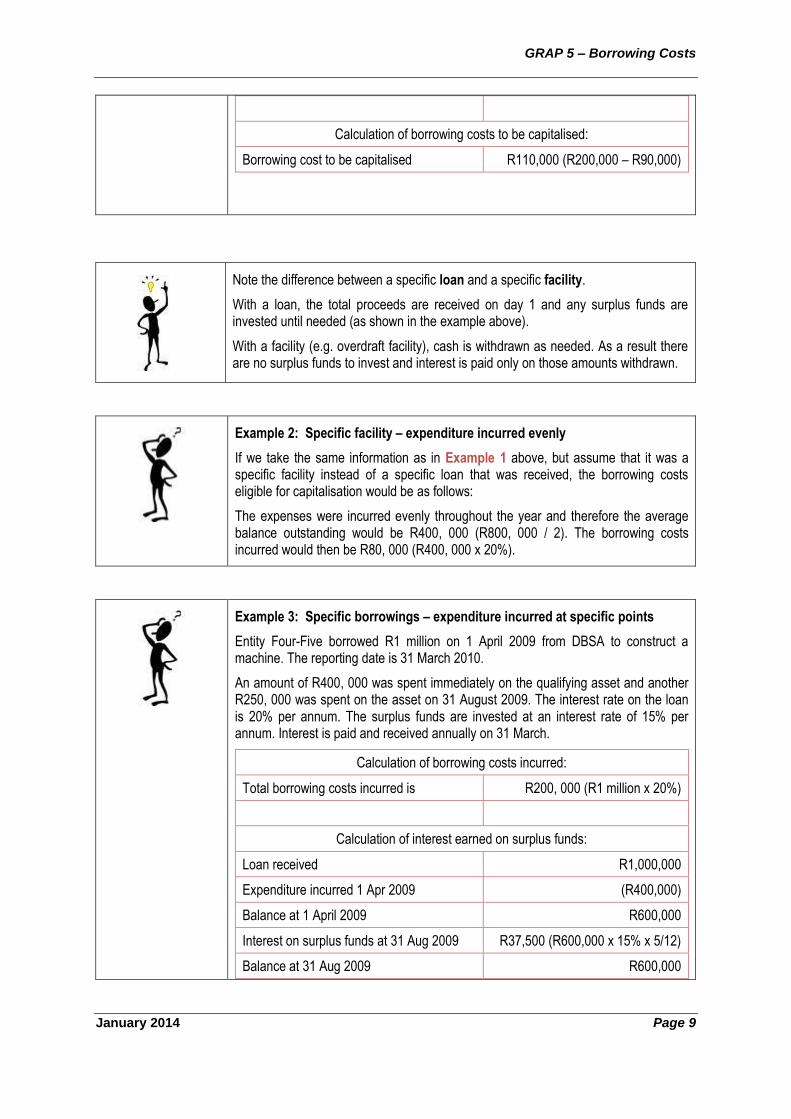

Calculation of borrowing costs to be capitalised:

Borrowing cost to be capitalised R110,000 (R200,000 – R90,000)

Example 2: Specific facility – expenditure incurred evenly

If we take the same information as in Example 1 above, but assume that it was a specific facility instead of a specific loan that was received, the borrowing costs eligible for capitalisation would be as follows:

The expenses were incurred evenly throughout the year and therefore the average balance outstanding would be R400, 000 (R800, 000 / 2). The borrowing costs incurred would then be R80, 000 (R400, 000 x 20%).

Example 3: Specific borrowings – expenditure incurred at specific points

Entity Four-Five borrowed R1 million on 1 April 2009 from DBSA to construct a machine. The reporting date is 31 March 2010.

An amount of R400, 000 was spent immediately on the qualifying asset and another R250, 000 was spent on the asset on 31 August 2009. The interest rate on the loan is 20% per annum. The surplus funds are invested at an interest rate of 15% per annum. Interest is paid and received annually on 31 March.

Calculation of borrowing costs incurred:

Total borrowing costs incurred is R200, 000 (R1 million x 20%)

Calculation of interest earned on surplus funds:

Loan received R1,000,000

Expenditure incurred 1 Apr 2009 (R400,000)

Balance at 1 April 2009 R600,000

Interest on surplus funds at 31 Aug 2009 R37,500 (R600,000 x 15% x 5/12)

Balance at 31 Aug 2009 R600,000

Note the difference between a specific loan and a specific facility.

With a loan, the total proceeds are received on day 1 and any surplus funds are invested until needed (as shown in the example above).

With a facility (e.g. overdraft facility), cash is withdrawn as needed. As a result there are no surplus funds to invest and interest is paid only on those amounts withdrawn.

GRAP 5 – Borrowing Costs

January 2014 Page 10

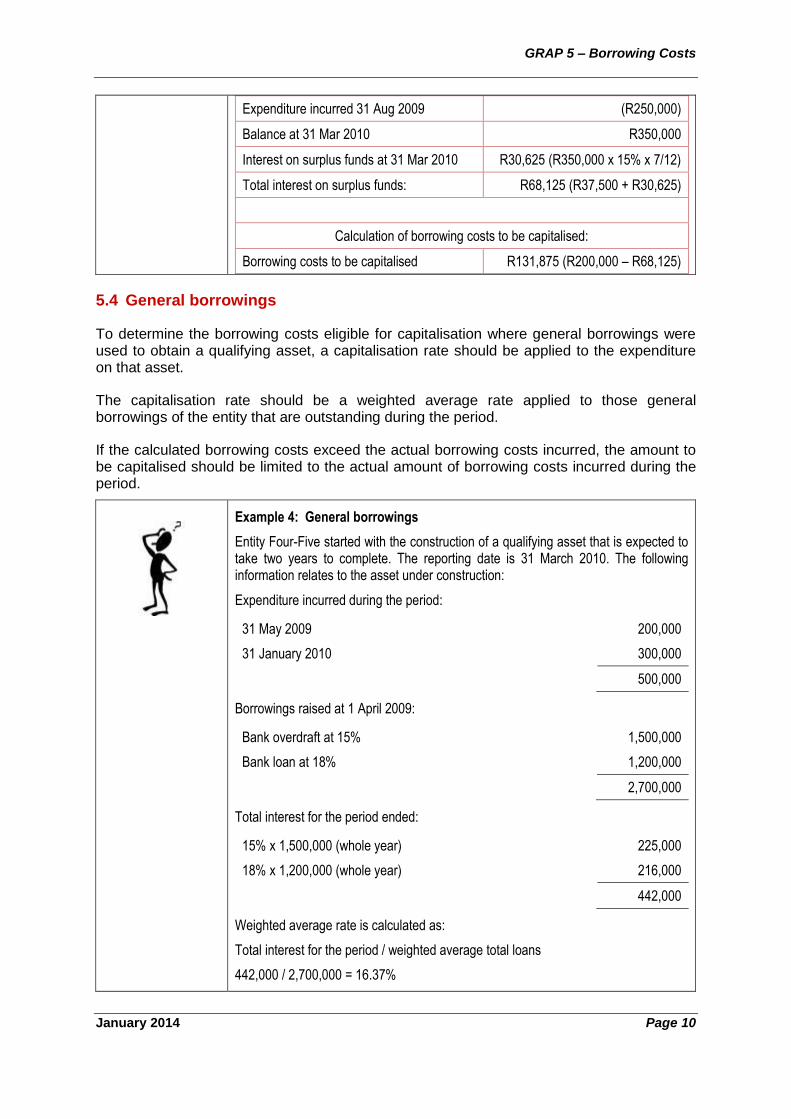

Expenditure incurred 31 Aug 2009 (R250,000)

Balance at 31 Mar 2010 R350,000

Interest on surplus funds at 31 Mar 2010 R30,625 (R350,000 x 15% x 7/12)

Total interest on surplus funds: R68,125 (R37,500 + R30,625)

Calculation of borrowing costs to be capitalised:

Borrowing costs to be capitalised R131,875 (R200,000 – R68,125)

5.4 General borrowings

To determine the borrowing costs eligible for capitalisation where general borrowings were used to obtain a qualifying asset, a capitalisation rate should be applied to the expenditure on that asset.

The capitalisation rate should be a weighted average rate applied to those general borrowings of the entity that are outstanding during the period.

If the calculated borrowing costs exceed the actual borrowing costs incurred, the amount to be capitalised should be limited to the actual amount of borrowing costs incurred during the period.

Example 4: General borrowings

Entity Four-Five started with the construction of a qualifying asset that is expected to take two years to complete. The reporting date is 31 March 2010. The following information relates to the asset under construction:

Expenditure incurred during the period:

31 May 2009 200,000

31 January 2010 300,000

500,000

Borrowings raised at 1 April 2009:

Bank overdraft at 15% 1,500,000

Bank loan at 18% 1,200,000

2,700,000

Total interest for the period ended:

15% x 1,500,000 (whole year) 225,000

18% x 1,200,000 (whole year) 216,000

442,000

Weighted average rate is calculated as:

Total interest for the period / weighted average total loans

442,000 / 2,700,000 = 16.37%

GRAP 5 – Borrowing Costs

January 2014 Page 11

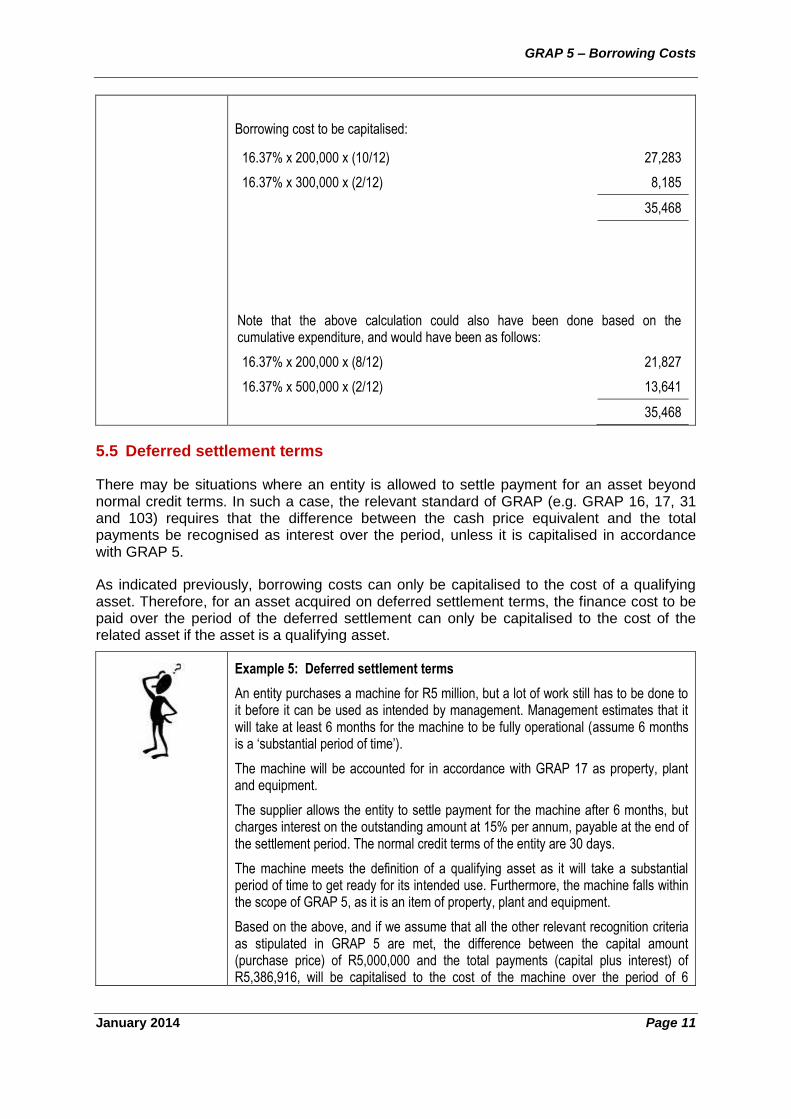

Borrowing cost to be capitalised:

16.37% x 200,000 x (10/12) 27,283

16.37% x 300,000 x (2/12) 8,185

35,468

Note that the above calculation could also have been done based on the cumulative expenditure, and would have been as follows:

16.37% x 200,000 x (8/12) 21,827

16.37% x 500,000 x (2/12) 13,641

35,468

5.5 Deferred settlement terms

There may be situations where an entity is allowed to settle payment for an asset beyond normal credit terms. In such a case, the relevant standard of GRAP (e.g. GRAP 16, 17, 31 and 103) requires that the difference between the cash price equivalent and the total payments be recognised as interest over the period, unless it is capitalised in accordance with GRAP 5.

As indicated previously, borrowing costs can only be capitalised to the cost of a qualifying asset. Therefore, for an asset acquired on deferred settlement terms, the finance cost to be paid over the period of the deferred settlement can only be capitalised to the cost of the related asset if the asset is a qualifying asset.

Example 5: Deferred settlement terms

An entity purchases a machine for R5 million, but a lot of work still has to be done to it before it can be used as intended by management. Management estimates that it will take at least 6 months for the machine to be fully operational (assume 6 months is a ‘substantial period of time’).

The machine will be accounted for in accordance with GRAP 17 as property, plant and equipment.

The supplier allows the entity to settle payment for the machine after 6 months, but charges interest on the outstanding amount at 15% per annum, payable at the end of the settlement period. The normal credit terms of the entity are 30 days.

The machine meets the definition of a qualifying asset as it will take a substantial period of time to get ready for its intended use. Furthermore, the machine falls within the scope of GRAP 5, as it is an item of property, plant and equipment.

Based on the above, and if we assume that all the other relevant recognition criteria as stipulated in GRAP 5 are met, the difference between the capital amount (purchase price) of R5,000,000 and the total payments (capital plus interest) of R5,386,916, will be capitalised to the cost of the machine over the period of 6

GRAP 5 – Borrowing Costs

January 2014 Page 12

months. The total payments (including interest) were calculated as follows:

PV = R5,000,000

I = 15%/12

N = 6

Comp FV = R5,386,916. This can be calculated by using MS Excel or a financial calculator.

Therefore the borrowing costs to be capitalised over 6 months is R386,916 (R5,386,916 - R5,000,000).

The journal entries will be as follows:

Acquisition date Debit Credit

R R

Machine 5,000,000

Creditor 5,000,000

Recognise machine purchased on acquisition date

At the end of 6 months Debit Credit

R R

Machine 386,916

Creditor 386,916

Capitalise interest accrued to the cost of the machine

Note that the interest over the six months has been aggregated for the purposes of this example. The actual monthly calculation of the interest will be as follows:

Period Interest Total

Month 1 (R5,000,000 x 15% / 12) R 62,500 5,062,500

Month 2 (R5,062,500 x 15% / 12) R 63,281 5,125,781

Month 3 (R5,125,781 x 15% / 12) R 64,073 5,189,854

Month 4 (R5,189,853 x 15% / 12) R 64,873 5,254,727

Month 5 (R5,254,726 x 15% / 12) R 65,684 5,320,411

Month 6 (R5,320,410 x 15% / 12) R 66,505 5,386,916

Total interest is therefore R386,916

At the end of 6 months Debit Credit

GRAP 5 – Borrowing Costs

January 2014 Page 13

R R

Creditor 5,386,916

Bank 5,386,916

The creditor paid

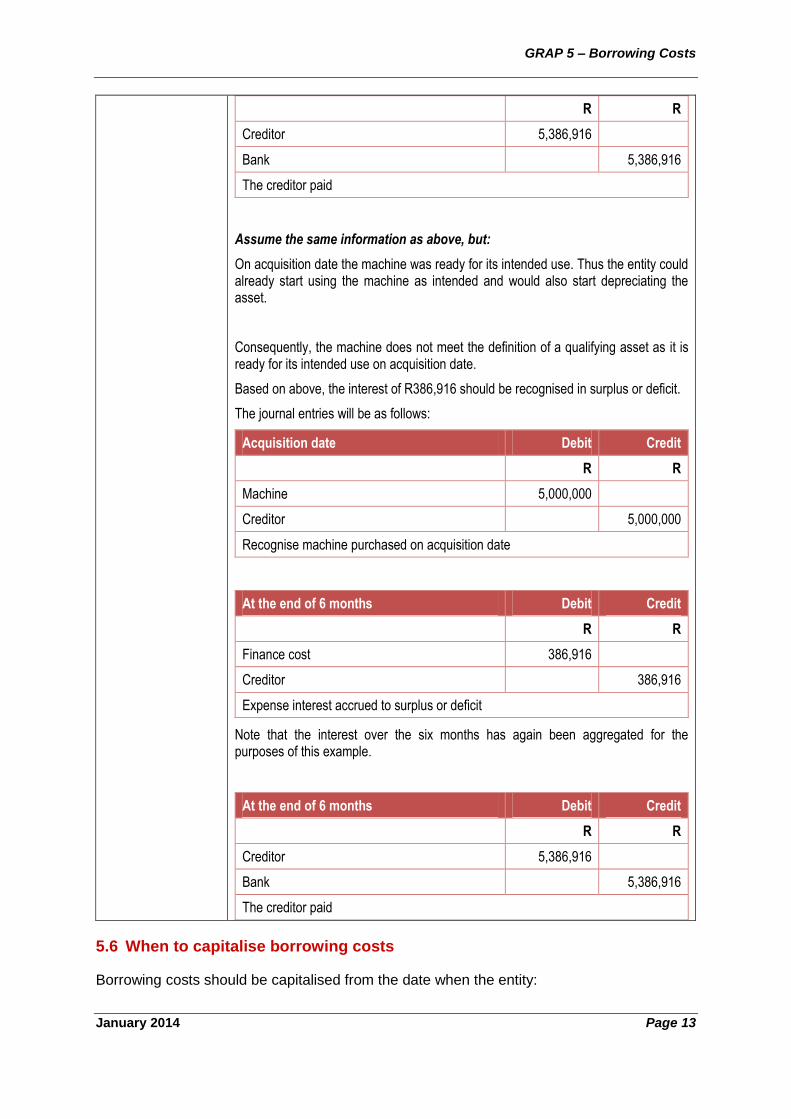

Assume the same information as above, but:

On acquisition date the machine was ready for its intended use. Thus the entity could already start using the machine as intended and would also start depreciating the asset.

Consequently, the machine does not meet the definition of a qualifying asset as it is ready for its intended use on acquisition date.

Based on above, the interest of R386,916 should be recognised in surplus or deficit.

The journal entries will be as follows:

Acquisition date Debit Credit

R R

Machine 5,000,000

Creditor 5,000,000

Recognise machine purchased on acquisition date

At the end of 6 months Debit Credit

R R

Finance cost 386,916

Creditor 386,916

Expense interest accrued to surplus or deficit

Note that the interest over the six months has again been aggregated for the purposes of this example.

At the end of 6 months Debit Credit

R R

Creditor 5,386,916

Bank 5,386,916

The creditor paid

5.6 When to capitalise borrowing costs

Borrowing costs should be capitalised from the date when the entity:

GRAP 5 – Borrowing Costs

January 2014 Page 14

Incurs expenditure on the qualifying asset;

Incurs borrowing costs; and

Commences activities that are necessary to get the asset ready for its intended use or sale.

GRAP 5 – Borrowing Costs

January 2014 Page 15

6. SUBSEQUENT MEASUREMENT

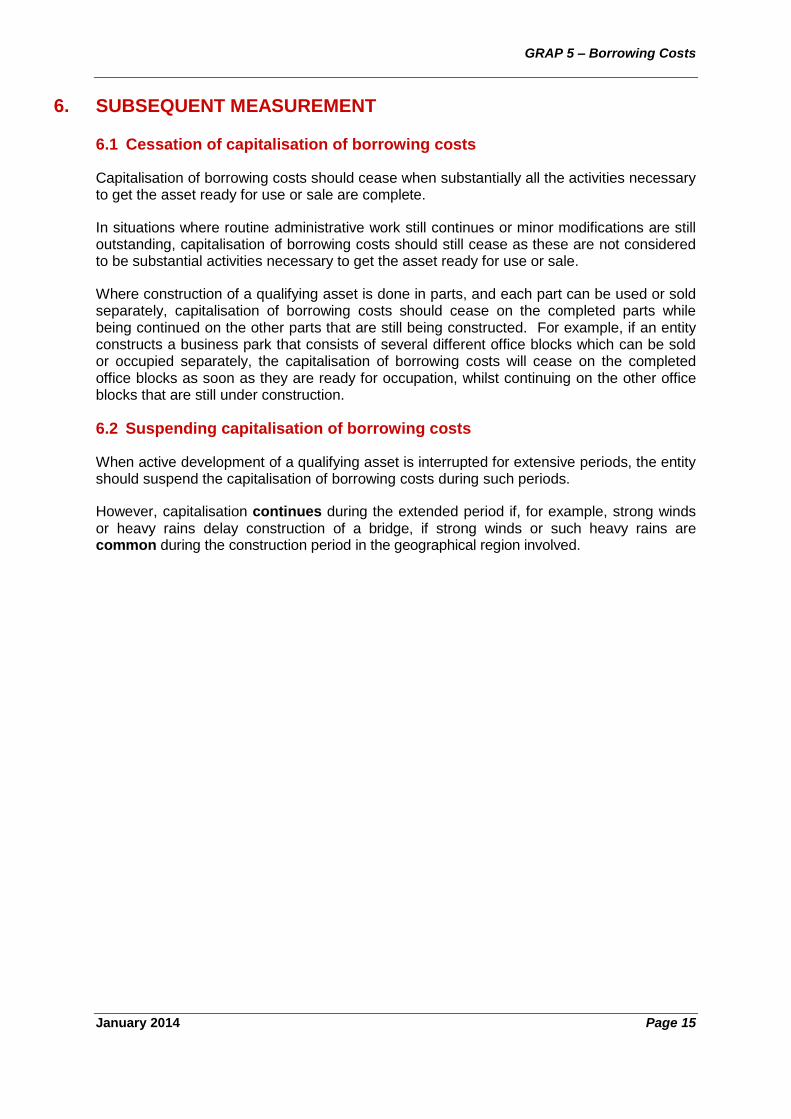

6.1 Cessation of capitalisation of borrowing costs

Capitalisation of borrowing costs should cease when substantially all the activities necessary to get the asset ready for use or sale are complete.

In situations where routine administrative work still continues or minor modifications are still outstanding, capitalisation of borrowing costs should still cease as these are not considered to be substantial activities necessary to get the asset ready for use or sale.

Where construction of a qualifying asset is done in parts, and each part can be used or sold separately, capitalisation of borrowing costs should cease on the completed parts while being continued on the other parts that are still being constructed. For example, if an entity constructs a business park that consists of several different office blocks which can be sold or occupied separately, the capitalisation of borrowing costs will cease on the completed office blocks as soon as they are ready for occupation, whilst continuing on the other office blocks that are still under construction.

6.2 Suspending capitalisation of borrowing costs

When active development of a qualifying asset is interrupted for extensive periods, the entity should suspend the capitalisation of borrowing costs during such periods.

However, capitalisation continues during the extended period if, for example, strong winds or heavy rains delay construction of a bridge, if strong winds or such heavy rains are common during the construction period in the geographical region involved.

GRAP 5 – Borrowing Costs

January 2014 Page 16

7. DISCLOSURE

An example illustrating the disclosure required for borrowing costs (refer to the standard for detail):

Extract from Statement Financial Position

Note 20x1 20x0

R R

Non-current assets

Property, plant and equipment 4 XX XX

Extract from Statement Financial Performance

Note 20x1 20x0

R R

Finance costs 5 XX XX

Extract from Notes to the financial statements

Accounting policies

1.5 Borrowing costs

For example, include as a minimum: Borrowing costs directly attributable to the acquisition, construction or production of a qualifying asset are capitalised to the cost of the asset. All other borrowing costs are recognised as an expense in the period in which it is incurred.

20x1 20x0

4. Property, plant and equipment

Opening balance XXX XXX

Cost / Revalued amount XX XX

Accumulated depreciation and impairment losses (XX) (XX)

Additions XX XX

Depreciation (XX) (XX)

Closing balance XXX XXX

Cost / Revalued amount XX XX

Accumulated depreciation and impairment losses (XX) (XX)

For borrowing costs capitalised: Included in the cost above is interest amounting to Rx

GRAP 5 – Borrowing Costs

January 2014 Page 17

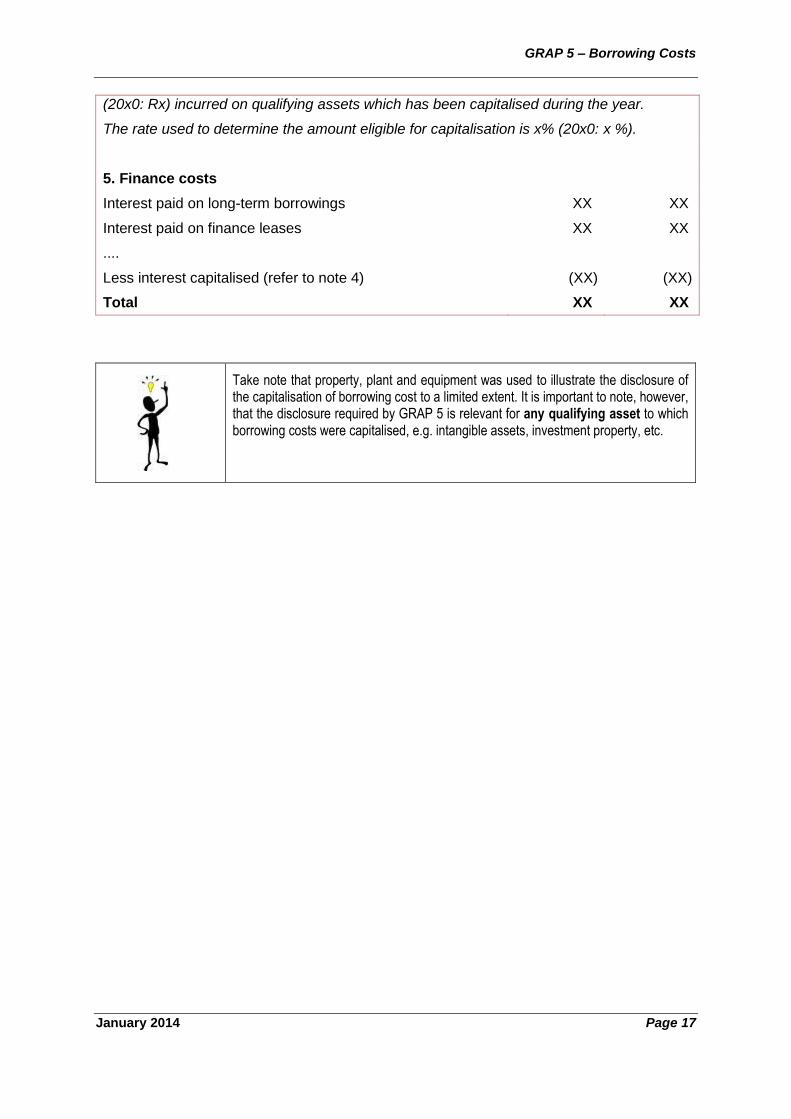

(20x0: Rx) incurred on qualifying assets which has been capitalised during the year.

The rate used to determine the amount eligible for capitalisation is x% (20x0: x %).

5. Finance costs

Interest paid on long-term borrowings XX XX

Interest paid on finance leases XX XX

....

Less interest capitalised (refer to note 4) (XX) (XX)

Total XX XX

Take note that property, plant and equipment was used to illustrate the disclosure of the capitalisation of borrowing cost to a limited extent. It is important to note, however, that the disclosure required by GRAP 5 is relevant for any qualifying asset to which borrowing costs were capitalised, e.g. intangible assets, investment property, etc.

GRAP 5 – Borrowing Costs

January 2014 Page 18

8. SUMMARY OF KEY PRINCIPLES

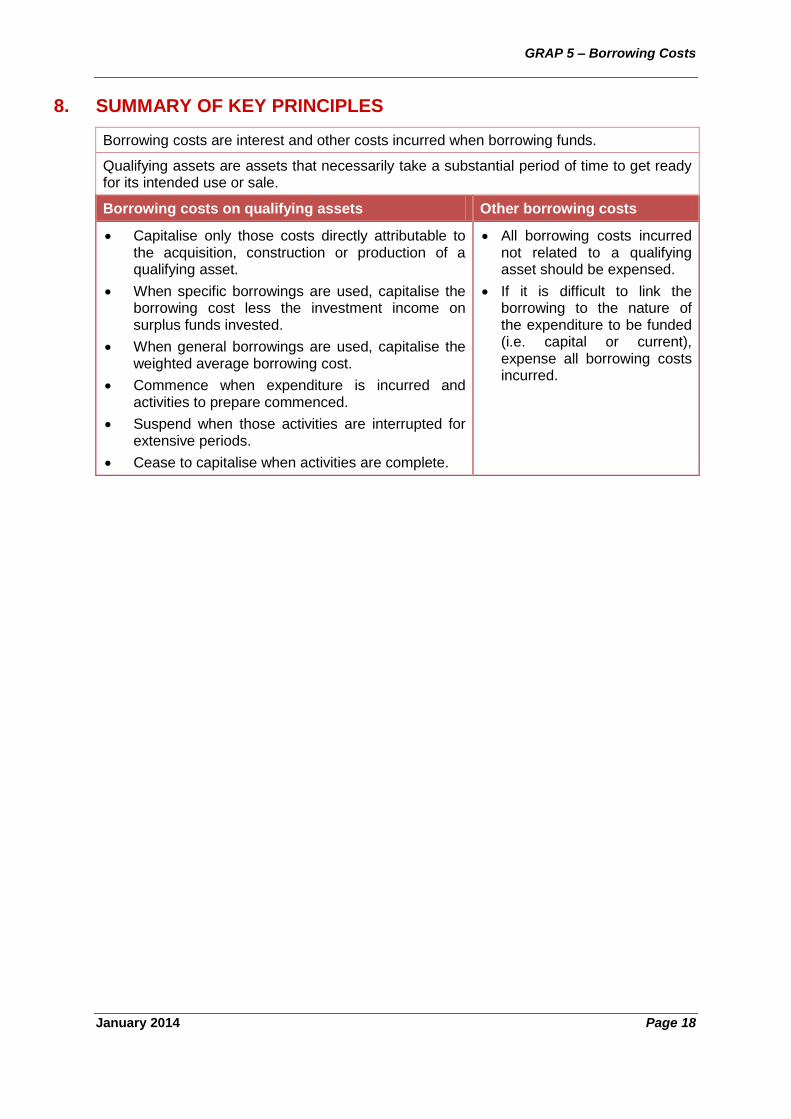

Borrowing costs are interest and other costs incurred when borrowing funds.

Qualifying assets are assets that necessarily take a substantial period of time to get ready for its intended use or sale.

Borrowing costs on qualifying assets Other borrowing costs

Capitalise only those costs directly attributable to the acquisition, construction or production of a qualifying asset.

When specific borrowings are used, capitalise the borrowing cost less the investment income on surplus funds invested.

When general borrowings are used, capitalise the weighted average borrowing cost.

Commence when expenditure is incurred and activities to prepare commenced.

Suspend when those activities are interrupted for extensive periods.

Cease to capitalise when activities are complete.

All borrowing costs incurred not related to a qualifying asset should be expensed.

If it is difficult to link the borrowing to the nature of the expenditure to be funded (i.e. capital or current), expense all borrowing costs incurred.