Government Investigations and Enforcement Actions

32

Government Investigations and Enforcement Actions Presented by: Mitchell D. Raup, Noam B. Fischman, Jonathan N. Rosen

-

Upload

polsinelli-pc -

Category

Law

-

view

208 -

download

1

Transcript of Government Investigations and Enforcement Actions

Government Investigations and Enforcement Actions

Presented by:Mitchell D. Raup, Noam B. Fischman,

Jonathan N. Rosen

ANTITRUST RISKS IN M&A TRANSACTIONS

Mitchell Raup, vice-chair of Polsinelli’s Antitrust practice, has 30 years’ experience solving the most difficult antitrust problems. He has been lead antitrust counsel on dozens of health care M&A transactions involving hospitals, physician groups, provider networks, health insurers, pharmaceuticals, dialysis clinics, and group purchasing organizations. He regularly represents businesses and witnesses in antitrust investigations by the Federal Trade Commission, the Antitrust Division of the Department of Justice, and state attorneys general.

Mitchell D. RaupPractice Vice Chair

3

Introduction

A new transaction has just landed on your desk. Your company wants to acquire a competitor.

Your clients have negotiated the term sheet, and signed the letter of intent. Now, they want to close the deal as soon as possible.

Your assignment: spot all the issues, and get the deal done without surprises.

Because you are dealing with a competitor, antitrust should be at the top of your list of concerns.

Basic Antitrust Rules Governing Transactions

The transaction itself is governed by § 7 of the Clayton Act, which prohibits mergers and acquisitions that may substantially lessen competition.

The discussions leading up to the transaction are governed by § 1 of the Sherman Act, which prohibits agreements that unreasonably restrain competition.

• The merger agreement, and any related agreements, could violate § 1 even if the merger itself does not violate§ 7.

Hart-Scott-Rodino requires premerger notification to the antitrust enforcement agencies, and prohibits transfer of beneficial ownership or control before the 30-day waiting period has expired.

4

Hart-Scott-Rodino

If an HSR filing is required, both parties must file and wait 30 days after filing before closing. – The antitrust enforcement agencies can shorten or lengthen this

time. There are substantial penalties for closing a transaction without making

a required HSR filing, and for closing before the waiting period expires. HSR filing may be required for any transaction that transfers stock or

assets valued at over $78.2 million. There may be an exemption, but HSR rules are technical. If your deal is valued at over $78.2 million, call an HSR expert.

5

Due Diligence And Other Pre-closing Information Exchanges.

Every transaction requires exchanges of information. Competitors normally can’t share competitively-sensitive information

without antitrust risk.– The information exchange itself may be illegal. – The information exchange, if followed by coordination of the parties’

pricing and other business decisions, may be evidence of an illegal agreement.

Antitrust law allows the exchange of information that is reasonably related to the legitimate goal of closing a transaction. – But there are antitrust risks: merely knowing your competitor’s

confidential prices can support a charge of price-fixing.– There’s also a business risk: If the transaction does not close, your

client does not want its competitor to know the terms of its confidential contracts.

6

7

Due Diligence: Clean Team Agreements

Define the information that is confidential and competitively-sensitive, but must be exchanged.

Each party agrees to identify and segregate that information before delivering it.

Agreement on a “clean team” to review and analyze the information. – Clean team members normally can’t be decision-makers in the

business to which the information relates.– They can be executives in another line of business, or another

geographic area.– They can be outside consultants.

Clean team may report to business leaders on the results of their analysis, without revealing competitively-sensitive information.

Pre-closing Coordination and “Gun-Jumping”

Even if a merger is lawful, pre-closing coordination may be per se illegal.– Any agreement to coordinate business decisions before closing may

violate § 1 of the Sherman Act.– If a Hart-Scott-Rodino filing is required, the parties may not transfer

control of the target until the HSR waiting period expires. A trap for the unwary: terms of merger agreement that give the buyer

control over ordinary-course business decisions of the seller. Ordinary-course business decisions must be made independently until

closing. US v. Smithfield: $900,000 civil penalty for HSR violations.

– “Smithfield exercised operational control over a significant segment of Premium Standard’s business without observing the premerger waiting period requirement.”

8

Will the Antitrust Agencies Investigate?

Every deal with a competitor requires antitrust review. Red flags for a joint venture or other cooperation with a

competitor:– Per se illegal agreements.– Market power.

Red flags for an acquisition of a competitor:– 4-to-3, 3-to-2, or 2-to-1 merger.– Market share over 50%.– Market definition requires antitrust advice.

There is no safety “under the radar” for deals that don’t require HSR filings.

No market is too small for an antitrust investigation.

9

Getting the Deal Through

The ultimate issue in a merger investigation is: will the transaction create market power that can affect prices?

Many deals begin with a plan to increase prices. Most FTC and DOJ antitrust complaints begin with quotes

from the parties’ documents:– “Market share in primary care is a key success factor, critical to

sustaining a strong position relative to payer contracting.” (St. Luke’s/Saltzer).

– The acquisition will allow us to “regain control of industry pricing and avoid further price erosion” (H&R Block).

– The transaction “could stick it employers, . . . forcing high rates on employers and insurance companies” (Promedica).

10

11

Getting the Deal Through

Antitrust enforcers say deals like these are so obviously anticompetitive that they “never should have made it out of the boardroom.” (Bill Baer Senate testimony, March 9, 2016).

Good counsel early can help avoid these pitfalls. • Control your documents – especially 4(c) documents. • Educate your clients on what can and can’t be done, and

what reasons are and aren’t acceptable to antitrust enforcers.

Get antitrust help when you need it.

COMPLIANCE AND DUE DILIGENCE: FCPA

Noam Fischman serves as a guide leading clients through commercial litigation matters in federal and state courts, as well as government investigations and matters involving regulatory agencies. Noam has extensive experience advising clients about risk management and risk mitigation efforts in highly- regulated industries, including health care, the EB-5 foreign investor program, telecommunications, non-profit organizations, and higher education.

Noam B. FischmanShareholder

The Fact Pattern Widens

A new transaction has just landed on your desk. Your company wants to acquire a competitor that does business abroad.

Your clients have negotiated the term sheet, and signed the letter of intent. Now, they want to close the deal as soon as possible.

Your assignment: spot all the issues, and get the deal done without surprises.

Because the target company does business abroad, due diligence ought to include a compliance review of how that company conducts its business.

Why?

Certain areas of the world are known for having a higher risk of corruption. Transparency International Corruption Index– a good initial gut check for

whether your company does business, or the target company does business, in a location with a high risk of public corruption.

Foreign corruption is not just a theoretical risk based on the laws of a faraway land. It is a crime in the US to bribe foreign government officials someplace else.

Corruption concerns in the target company impact the value of what’s being bought.

Once the deal has been consummated, corruption risk is visited upon the acquirer.

Risk is a continuum. Know where you are (and the target company is) on that continuum.

Foreign Corrupt Practices Act (FCPA)

The FCPA makes it unlawful:– To make payments, or give anything of value, to foreign government officials, or their agents, to

obtain or retain business.

Key Concepts:– “Payments” or “Anything of value” is broadly defined to mean: gifts, entertainment, travel, and

hospitality; contractual payments; personal favors; donations to an official’s favorite charity; cash, stock/bonds; and much, much more.

– Governmental Official – once again, is very broadly defined and not restricted to high-level officials.– What does it mean to obtain or retain business (i.e., what is the business purpose test)?

• Obtaining tax-exempt status;• Winning a contract;• Altering or circumventing import rules;• Accessing non-public bid tender or RFP information;• Influence the adjudication of lawsuits; and, among other things,• Avoid contract termination.

– Intent – although “willful conduct” required, that standard is designed to require a minimal threshold: voluntary, purposeful, and with a bad purpose (specific knowledge of the FCPA is certainly not required).

Know Who Owns/Controls Whom

State-Owned (or Controlled) Enterprises: A “government official” includes employees of state-owned enterprises (e.g.,

utilities, health care, energy, transportation, etc.). It is fact specific whether an enterprise is state owned or controlled. Factors include,

for example:– Extent of ownership interest;– Degree of control;– Foreign state’s characterization of the relationship;– Circumstances surrounding the creation of the enterprise;– Level of financial support;– Purpose of the entity; and,– Power of the entity to control its own functioning.

Incentives to non-managerial employees (hospital nurses, for instance, in one well publicized case) can be the recipient of bribes under the FCPA!

You Cannot Accomplish Indirectly…

Vicarious Liability:– The Government holds you accountable for the conduct of your …

• Employees;• Agents;• Joint Venture Partners;• Consultants;• (Labels do not matter) …

– understand the business model and how key international benchmarks were achieved, who played a role, and what role they played.

– Follow the flow of money • Very few foreign nationals are actually named “uncle.”• Not many companies are named “Company A.” • Slush funds.

Measuring the Compliance Risk

Is this really an issue to concern business folks and/or corporate lawyers (“yes” if you ask the Government)?

November 2012 DOJ/SEC joint task force released a guide to FCPA issues. DOJ/SEC was clear: – (a) Successors/purchasers could be held (and are held) liable for the conduct of

predecessors in interest, – (b) but, companies that investigate and remediate and, if appropriate, “self report”

issues can significantly mitigate the risk of successor liability. • Self-disclosure is a complicated question based on a broad set of variables.• This sort of decision should be made only after a thorough investigation of the

relevant issues and significant consultation with experience FCPA counsel.

Two Recent Enforcement Examples

Alstom – example of how FCPA concerns can directly impact the timing and negotiation of a transaction.– Note: Antitrust issues here as well that resulted in the divestiture of

certain business units. Goodyear/Treadsetters – example of the benefit of hindsight!

– According to public papers, Goodyear purchased Treadsetters and let it continue to operate without much oversight.

– Led to divestiture of certain problematic subsidiaries.– Financial costs.

• Failure to detect case.• Profits attributable to bribes = approx. $14 million.• Bribes = $3.2 million. • Fines = $16 million. • Hard and soft costs of investigating, remediating, etc. = ???

How do I Mitigate Risk and Maximize Reward

5 Step Process Per DOJ and SEC: Playbook written by the Government:

1. Conduct a thorough risk-based FCPA and anti-corruption due diligence on potential new business acquisitions (i.e., conduct due diligence);

2. Ensure that the acquiring company’s code of conduct and compliance policies and procedures apply to the newly-acquired or merged entity(ies);

3. Training;4. Anti-corruption audit; and,5. (Remediate concerns: NOTE: Government’s guidance is to disclose. See slide 18!)

Concluding Thoughts

Upshot: 1. The scope, breadth, and depth of compliance due diligence is fact specific.

There is no “one size fits all” set of due diligence questions.• Picture layers of an onion rather than a box to be checked.

2. These concerns ought to (and, in fact, do) impact the substantive deal.• 2013 Deloitte Survey:

– 63% of respondents identified FCPA concerns as the basis for an aborted transaction during the prior 3 years.

3. For companies doing business abroad, the FCPA is critical to understanding what potential risk is being purchased as a matter and as a broader “tell” for the culture of the target company.

4. Culture is an intangible asset (or liability) of target companies.5. A “culture of compliance” very much matters if you or your company are

ever the subject of compliance inquiries by the Government.

EXPORT CONTROLS AND FALSE CLAIMS ACT: DUE DILIGENCE CONCERNS AND THE CULTURE OF COMPLIANCE

Jonathan Rosen is a highly regarded former federal and state prosecutor, having won more than 100 trials. He has argued numerous cases before the U.S. Court of Appeals for the District of Columbia. He focuses on health care fraud, consumer fraud, public corruption, the Foreign Corrupt Practices Act, corporate and securities fraud, export control violations, antitrust violations, money laundering, and government contracts. He has defended individuals in high-profile criminal cases and congressional investigations while also representing publicly traded companies in criminal cases, parallel civil and administrative matters, compliance issues, and internal investigations.

Jonathan N. RosenPractice Vice Chair

Fact Pattern Revisited

A new transaction has just landed on your desk. Your company wants to acquire a competitor that does business abroad in certain regulated industries.

Your clients have negotiated the term sheet, and signed the letter of intent. Now, they want to close the deal as soon as possible.

Your assignment: spot all the issues, and get the deal done without surprises.

Because the target company does business abroad, due diligence ought to include a compliance review of how the company conducts business.

US Export Control Regimes

Definitions– “Export” includes goods, services technology/technical data– “US person” includes US person in foreign country and foreign person in

foreign country or US Regulatory regimes

– OFAC Controls (Treasury Department)• Product neutral• Prohibited countries and individuals

– ITAR Controls (State Department)• Exports of USML items

– EAR Controls (Commerce Department)• Exports of dual use item

Export Control M&A Risks: Due Diligence

Examine export jurisdiction and classifications for accuracy. Review supplier contacts for certifications.

Screen all parties to trade transactions. Retain paperwork of screens performed.– denied persons list; debarred parties list; Specially designated nationals

Review systemic process to identify prohibited countries, prohibited buyers and end-users

Identify all dual/third country national personnel for information exports/deemed exports

Confirm consistency of end use with buyer’s business, standard practices

Export Control M&A Risks: Due Diligence (Cont.)

Foreign companies, Joint venture partners, distributors and subcontractors

Review for compliance with broker, munitions manufacturer registration requirements

Review for compliance with Technical Assistance & Manufacturing License Agreements

Review record keeping and computer system access, storage

Review for compliance with export clearance procedures Review export compliance program Export violations: evidence of violations

Export Control M&A Risks: Executing Transaction

Acquisition of U.S. target by Foreign Company Export licenses for transfers of certain assets to

foreign buyers Amendments of registration statement Transactions with prohibited parties Transactions with prohibited countries

Export Control M&A Risks:Post Transaction

Deemed exports: foreign target company Deemed exports: foreign company acquirer Termination of business with embargoed

countries Adoption of export compliance program Discovery of export control violation– ongoing or past violation

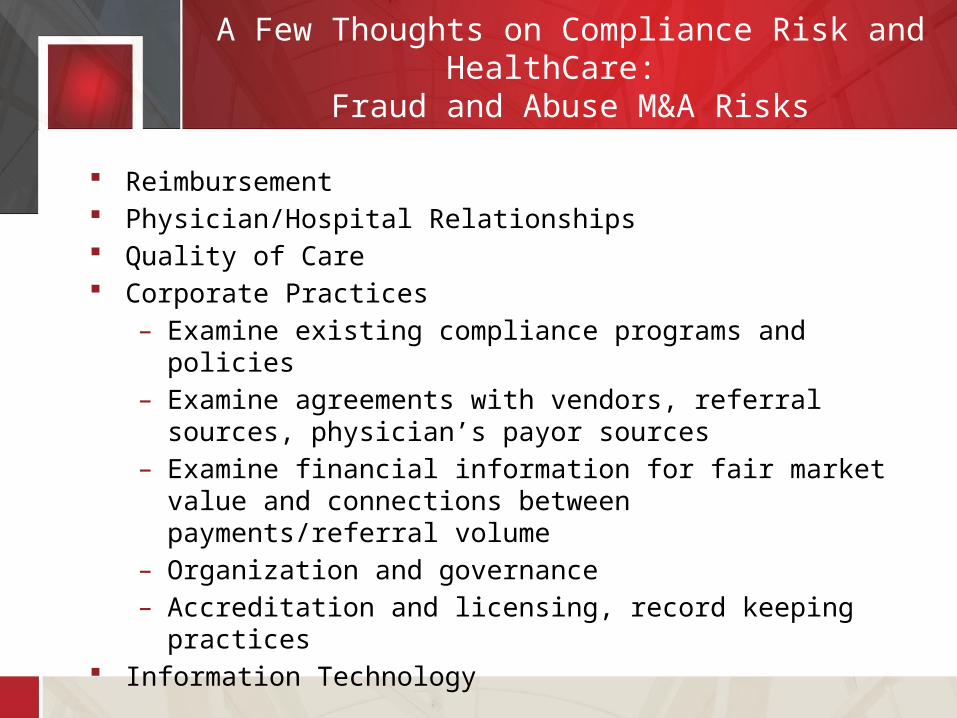

A Few Thoughts on Compliance Risk and HealthCare: Fraud and Abuse M&A Risks

Reimbursement Physician/Hospital Relationships Quality of Care Corporate Practices

– Examine existing compliance programs and policies– Examine agreements with vendors, referral sources, physician’s

payor sources– Examine financial information for fair market value and connections

between payments/referral volume– Organization and governance– Accreditation and licensing, record keeping practices

Information Technology

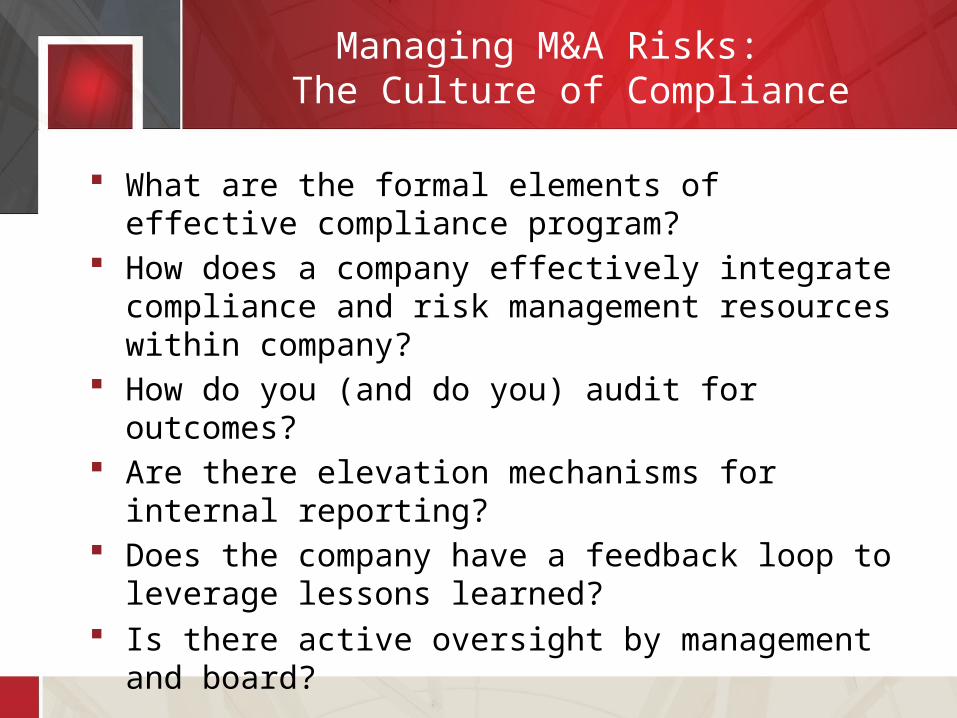

Managing M&A Risks: The Culture of Compliance

What are the formal elements of effective compliance program?

How does a company effectively integrate compliance and risk management resources within company?

How do you (and do you) audit for outcomes? Are there elevation mechanisms for internal reporting? Does the company have a feedback loop to leverage lessons

learned? Is there active oversight by management and board?

Government Investigations and Enforcement Actions

Thank you, and we hope that you will join us for our next webinar on June 28, 2016:

Claims and Related Issues Arising out of Bankruptcy or Receivership

Polsinelli provides this material for informational purposes only. The material provided herein is general and is not intended to be legal advice. Nothing herein should be relied upon or used without consulting a lawyer to consider your specific circumstances, possible changes to applicable laws, rules and regulations and other legal issues. Receipt of this material does not establish an attorney-client relationship.

Polsinelli is very proud of the results we obtain for our clients, but you should know that past results do not guarantee future results; that every case is different and must be judged on its own merits; and that the choice of a lawyer is an important decision and should not be based solely upon advertisements.

© 2016 Polsinelli PC. In California, Polsinelli LLP.Polsinelli is a registered mark of Polsinelli PC