11_A Case for Governance Audit for Better Corporate Governance (1)

GOVERNANCE AND AUDIT COMMITTEE

Thursday, September 7, 2017

4:00 PM

Conference Room 157

County Government Center

70 West Hedding Street

San Jose, CA

AGENDA

CALL TO ORDER

1. ROLL CALL

2. PUBLIC PRESENTATIONS:

This portion of the agenda is reserved for persons desiring to address the Committee on any matter not on the agenda. Speakers are limited to 2 minutes. The law does not permit Committee action or extended discussion on any item not on the agenda except under special circumstances. If Committee action is requested, the matter can be placed on a subsequent agenda. All statements that require a response will be referred to staff for reply in writing.

3. ORDERS OF THE DAY

CONSENT AGENDA

4. ACTION ITEM - Approve Regular Meeting Minutes of June 1, 2017.

5. ACTION ITEM -Approve amending the FY 2018 Internal Audit Work Plan to define the specific purpose and scope of the “Transaction Monitoring Audit” placeholder project contained therein.

6. ACTION ITEM -Ratify the appointment to the Bicycle & Pedestrian Advisory Committee for the two-year term ending June 30, 2018 of Tom Granvold, representing the City of Santa Clara.

7. ACTION ITEM -Ratify the appointment to the Citizens Advisory Committee of Matthew Quevedo, representing the Silicon Valley Leadership Group, conditional on that organization’s current Citizens Advisory Committee representative being appointed to the 2016 Measure B Citizens’ Oversight Committee.

Santa Clara Valley Transportation Authority Governance and Audit Committee September 7, 2017

Page 2

8. ACTION ITEM -Approve the appointment to the Committee for Transportation Mobility & Accessibility for the four-year term ending December 31, 2020 of Tricia Kokes, representing Seniors/Individuals with Disabilities.

9. INFORMATION ITEM -Review and receive the Internal Audit Program's Audit Dashboard on the status of implementation of recommendations issued by the Office of the Auditor General.

10. INFORMATION ITEM -Receive and review the Auditor General's Ethics Hotline Quarterly Summary Report.

REGULAR AGENDA

11. ACTION ITEM -Recommend Board approval of individuals to serve on the 2016 Measure B Citizens' Oversight Committee, per the recommendation of the Evaluation Subcommittee.

12. ACTION ITEM -Review and receive the Auditor General's report on the Inventory Management and Costing Assessment.

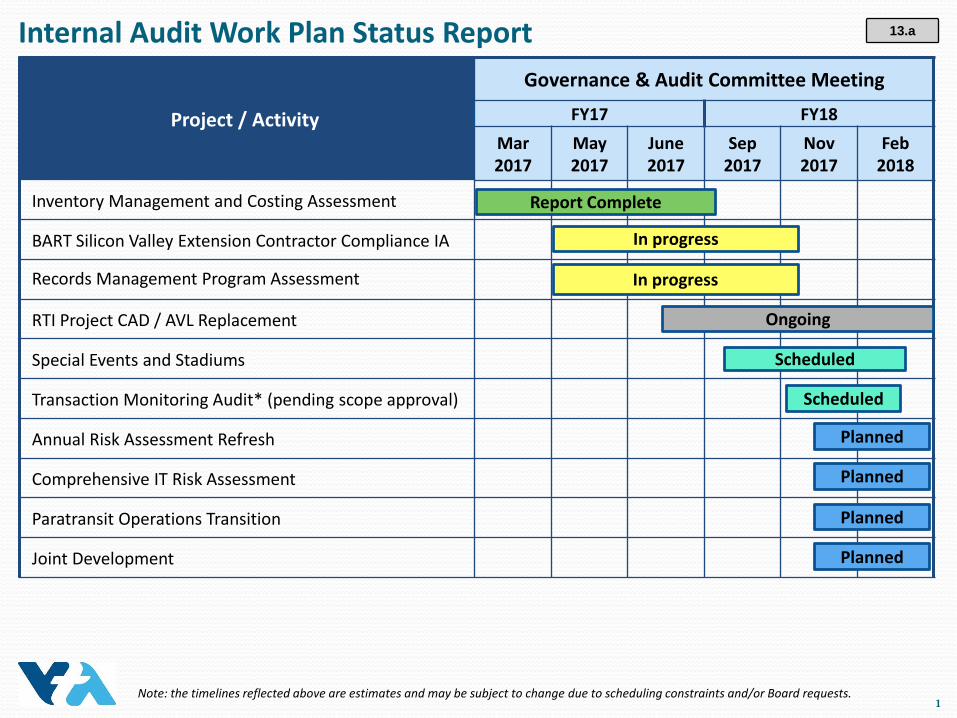

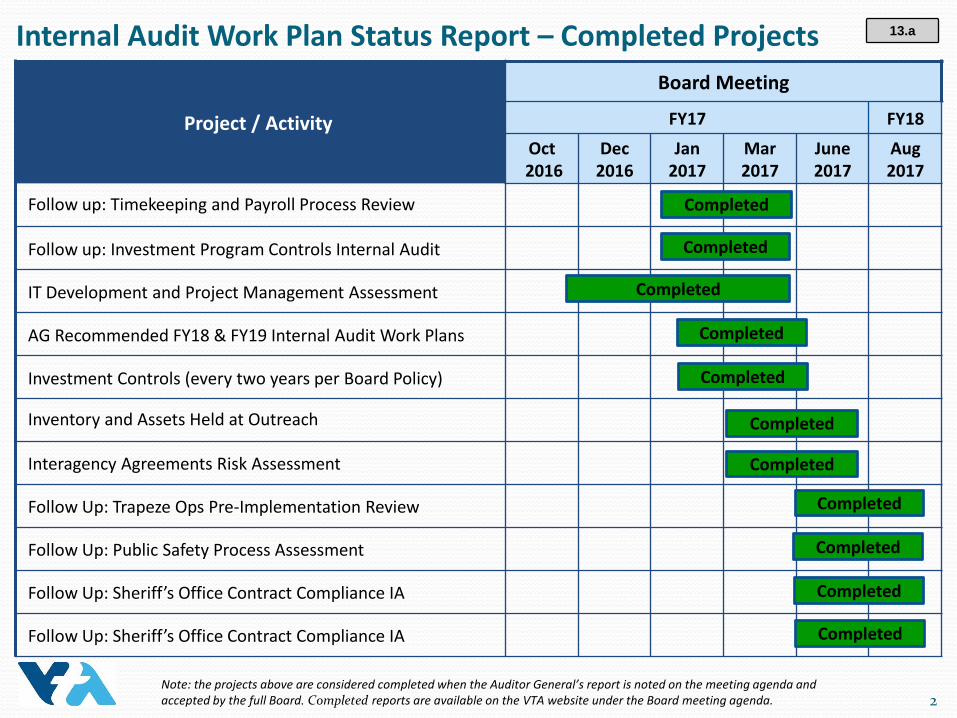

13. INFORMATION ITEM -Receive an update from Auditor General Office staff on the status of projects contained in the current Internal Audit Work Plan.

14. INFORMATION ITEM -Review and receive the scope of work for Annual Financial Audit Services for Fiscal Year 2017.

15. ACTION ITEM -Adopt the Interagency Agreements Policy.

16. INFORMATION ITEM - Review General Manager and General Counsel performance evaluation process. (Verbal Report)

OTHER ITEMS

17. Items of Concern and Referral to Administration.

18. Review Committee Work Plan. (Fernandez)

19. Committee Staff Report. (Fernandez)

20. Chairperson's Report. (Bruins)

21. Determine Items for the Consent Agenda for future VTA Board of Directors' meetings.

22. ANNOUNCEMENTS

23. ADJOURN

Santa Clara Valley Transportation Authority Governance and Audit Committee September 7, 2017

Page 3

In accordance with the Americans with Disabilities Act (ADA) and Title VI of the Civil Rights Act of 1964, VTA will make reasonable arrangements to ensure meaningful access to its meetings for persons who have disabilities and for persons with limited English proficiency who need translation and interpretation services. Individuals requiring ADA accommodations should notify the Board Secretary’s Office at least 48-hours prior to the meeting. Individuals requiring language assistance should notify the Board Secretary’s Office at least 72-hours prior to the meeting. The Board Secretary may be contacted at (408) 321-5680 or [email protected] or (408) 321-2330 (TTY only). VTA’s home page is www.vta.org or visit us on www.facebook.com/scvta. (408) 321-2300: 中文 / Español / 日本語 /

한국어 / tiếng Việt / Tagalog.

Disclosure of Campaign Contributions to Board Members (Government Code Section 84308) In accordance with Government Code Section 84308, no VTA Board Member shall accept, solicit, or direct a contribution of more than $250 from any party, or his or her agent, or from any participant, or his or her agent, while a proceeding involving a license, permit, or other entitlement for use is pending before the agency. Any Board Member who has received a contribution within the preceding 12 months in an amount of more than $250 from a party or from any agent or participant shall disclose that fact on the record of the proceeding and shall not make, participate in making, or in any way attempt to use his or her official position to influence the decision. A party to a proceeding before VTA shall disclose on the record of the proceeding any contribution in an amount of more than $250 made within the preceding 12 months by the party, or his or her agent, to any Board Member. No party, or his or her agent, shall make a contribution of more than $250 to any Board Member during the proceeding and for three months following the date a final decision is rendered by the agency in the proceeding. The foregoing statements are limited in their entirety by the provisions of Section 84308 and parties are urged to consult with their own legal counsel regarding the requirements of the law.

All reports for items on the open meeting agenda are available for review in the Board Secretary’s Office, 3331 North First Street, San Jose, California, (408) 321-5680, the Monday, Tuesday, and Wednesday prior to the meeting. This information is available on VTA’s website at http://www.vta.org and also at the meeting.

NOTE: THE BOARD OF DIRECTORS MAY ACCEPT, REJECT OR MODIFY

ANY ACTION RECOMMENDED ON THIS AGENDA.

Governance and Audit Committee

Thursday, June 1, 2017

MINUTES

CALL TO ORDER

The Regular Meeting of the Governance and Audit Committee (“Committee”) was called to order at 4:05 p.m. by Chairperson Bruins in Conference Room 157, County Government Center, 70 West Hedding, San José, California.

1. ROLL CALL

Attendee Name Title Status Jeannie Bruins Chairperson Present Cindy Chavez Member Present Glenn Hendricks Member Present Sam Liccardo Vice Chairperson Absent Teresa O’Neill Member Present

A quorum was present.

2. PUBLIC PRESENTATIONS

There were no Public Presentations.

3. ORDERS OF THE DAY

There were no Orders of the Day.

CONSENT AGENDA

4. Regular Meeting Minutes of May 4, 2017

M/S/C (Chavez/Hendricks) to approve the Regular Meeting Minutes of May 4, 2017. 5. Follow-Up on the Trapeze OPS Pre-Implementation Review

M/S/C (Chavez/Hendricks) to review and receive the Auditor General’s follow-up report on the implementation status of management’s action plans contained in the Trapeze OPS Pre-Implementation Review performed during Fiscal Year 2014.

NOTE: M/S/C MEANS MOTION SECONDED AND CARRIED AND, UNLESS OTHERWISE INDICATED, THE MOTION PASSED UNANIMOUSLY.

4

Governance and Audit Committee Minutes Page 2 of 5 June 1, 2017

6. Follow-Up on the Public Safety Process Assessment

M/S/C (Chavez/Hendricks) to review and receive the Auditor General’s follow-up report on the implementation status of management’s action plans contained in the Public Safety Process Assessment performed during Fiscal Year 2014.

RESULT: MOVER: SECONDER: AYES: NOES: ABSENT:

APPROVED – Consent Agenda Items #4 - #6 Cindy Chavez, Member Glenn Hendricks, Member Bruins, Chavez, Hendricks, O’Neill None Liccardo

REGULAR AGENDA

7. Inventory and Assets Held at Outreach

Pat Hagan, Auditor General’s Office, provided an overview, highlighting areas of concern and Auditor General’s recommendations for consideration.

Members of the Committee expressed concern about the security of data stored on computers which have been stored in an offsite storage facility by Outreach & Escort, Inc. (Outreach).

M/S/C (Chavez/Hendricks) to review and receive the Auditor General’s report on the Inventory and Assets held at Outreach.

RESULT: MOVER: SECONDER: AYES: NOES: ABSENT:

APPROVED – Agenda Item #7 Cindy Chavez, Member Glenn Hendricks, Member Bruins, Chavez, Hendricks, O’Neill None Liccardo

8. Interagency Agreements Risk Assessment

Mr. Hagan provided an overview of VTA’s interagency agreements and Auditor General’s recommendations.

Public Comment

Roland Lebrun, Interested Citizen, commented on the risks of these contracts to VTA.

Members of the Committee requested the following: 1) interagency agreements be made searchable; 2) future agreements have an executive summary; 3) the policy framework be brought to the Board; and 4) compile data on contract trends.

4

Governance and Audit Committee Minutes Page 3 of 5 June 1, 2017

M/S/C (Chavez/Hendricks) to review and receive the Auditor General’s report on the Interagency Agreements Risk Assessment. Further, the Committee requested that a policy framework and searchable interagency agreements be included in the action plan.

RESULT: MOVER: SECONDER: AYES: NOES: ABSENT:

APPROVED –Agenda Items #8 Cindy Chavez, Member Glenn Hendricks, Member Bruins, Chavez, Hendricks, O’Neill None Liccardo

Agenda Items #9 and #10 were heard together.

9. Follow-Up on the Sheriff’s Office Contract Compliance Internal Audit

10. Follow-Up on the Operator Scheduling Assessment

Bill Eggert, Auditor General, provided an overview of the Sheriff’s Office Contract Compliance Internal Audit and the Operator Scheduling Assessment.

M/S/C (Chavez/Hendricks) to review and receive the Auditor General’s follow-up report on the implementation status of management’s action plans contained in the Sheriff’s Office Contract Compliance Internal Audit performed during Fiscal Year 2013.

RESULT: MOVER: SECONDER: AYES: NOES: ABSENT:

APPROVED – Agenda Item #9 Cindy Chavez, Member Glenn Hendricks, Member Bruins, Chavez, Hendricks, O’Neill None Liccardo

M/S/C (Chavez/Hendricks) to review and receive the Auditor General’s follow-up report on the implementation status of management’s action plans contained in the Operator Scheduling Assessment performed during Fiscal Year 2015.

RESULT: MOVER: SECONDER: AYES: NOES: ABSENT:

APPROVED – Agenda Item #10 Cindy Chavez, Member Glenn Hendricks, Member Bruins, Chavez, Hendricks, O’Neill None Liccardo

11. Review Status of Internal Audit Work Plan

Mr. Eggert provided an overview, noting that some projects are in progress and an update will be provided at the September meeting.

4

Governance and Audit Committee Minutes Page 4 of 5 June 1, 2017

On order of Chairperson Bruins and there being no objection, the Committee received an update from Auditor General Office staff on the status of projects contained in the current Internal Audit Work Plan.

12. Applications to Serve on the 2016 Measure B Citizens’ Oversight Committee

Jim Lawson, Government Affairs Director & Executive Policy Advisor, provided an overview, highlighting the following: 1) 21 out of the 46 applications received to serve on the 2016 Measure B Citizens’ Oversight Committee were complete, noting no applications were received in the legal category; 2) members of the Evaluation Subcommittee are submitting their nominees for each position; and 3) it is anticipated that the Evaluation Subcommittee will provide a report at the Board meeting.

On order of Chairperson Bruins and there being no objection, the Committee reviewed and received the applications from individuals seeking to serve on the 2016 Measure B Citizens’ Oversight Committee evaluated by the Board subcommittee.

OTHER ITEMS

13. Items of Concern and Referral to Administration

There were no Items of Concern and Referral to Administration.

14. Review Committee Work Plan

Nuria I. Fernandez, General Manager and CEO, provided a brief overview of the work plan and noted the next Committee meeting is scheduled for September 7, 2017, highlighting key items scheduled for the meeting.

On order of Chairperson Bruins and there being no objection, the Committee reviewed the Committee Work Plan.

15. Committee Staff Report

There was no Committee Staff Report.

16. Chairperson’s Report

There was no Chairperson’s Report.

17. Determine Items for the Consent Agenda for future VTA Board of Directors’ Meetings

CONSENT:

Agenda Item #5., Review and receive the Auditor General’s follow-up report on the implementation status of management’s action plans contained in the Trapeze OPS Pre-Implementation Review performed during Fiscal Year 2014.

4

Governance and Audit Committee Minutes Page 5 of 5 June 1, 2017

Agenda Item #6., Review and receive the Auditor General’s follow-up report on the implementation status of management’s action plans contained in the Public Safety Process Assessment performed during Fiscal Year 2014.

Agenda Item #7., Review and receive the Auditor General’s report on the Inventory and Assets Held at Outreach.

Agenda Item #8., Review and receive the Auditor General’s report on the Interagency Agreement Risk Assessment.

Agenda Item #9., Review and receive the Auditor General’s follow-up report on the implementation status of management’s action plans contained in the Sheriff’s Office Contract Compliance Internal Audit performed during Fiscal Year 2013.

Agenda Item #10., Review and receive the Auditor General’s follow-up report on the implementation status of management’s action plans contained in the Operator Scheduling Assessment performed during Fiscal Year 2015.

REGULAR:

None

18. ANNOUNCEMENTS

Ms. Fernandez announced VTA will hold a Lesbian, Gay, Bisexual, Transgender, and Queer (LGBTQ) lunchtime event on June 22, 2017, at VTA’s headquarters.

19. ADJOURNMENT

On order of Chairperson Bruins and there being no objection, the Committee was adjourned at 5:00 p.m.

Respectfully submitted,

Thalia Young, Board Assistant VTA Office of the Board Secretary

4

Date: September 1, 2017 Current Meeting: September 7, 2017 Board Meeting: N/A

BOARD MEMORANDUM TO: Santa Clara Valley Transportation Authority Governance and Audit Committee

FROM: Auditor General, Bill Eggert SUBJECT: Amend FY 2018 Internal Audit Work Plan to Define a Placeholder Project

Policy-Related Action: No Government Code Section 84308 Applies: No

ACTION ITEM

RECOMMENDATION:

Approve amending the FY 2018 Internal Audit Work Plan to define the specific purpose and scope of the “Transaction Monitoring Audit” placeholder project contained therein.

BACKGROUND:

The Internal Audit Work Plan (“Work Plan”) specifies the projects that the Board of Directors has authorized the Auditor General’s Office to undertake during a given fiscal year. The Board of Directors has delegated certain specialized discretion to the Governance & Audit Committee in support of its responsibilities in overseeing the activities of the Auditor General (AG) function. This includes approving scope modifications and cost adjustments for Work Plan projects, subject to remaining within the overall budget for that Work Plan. It also includes defining the specific purpose and scope for Board-approved placeholder projects. The FY 2018 and FY 2019 Internal Audit Work Plans were approved by the Board in June 2017. The FY 2018 Work Plan contained a placeholder project for a “Transaction Monitoring Audit.” This project did not include a specific objective or scope. Instead, the scope of the project was to be determined at a future time upon further review and consideration by the AG’s Office of the relevant risks. Based on this analysis, the Auditor General would then recommend a specific

5

Page 2 of 3

objective and scope for this project for Governance & Audit Committee approval.

DISCUSSION:

Based on further evaluation of relevant risks to VTA, the Auditor General's Office recommends that the placeholder “Transaction Monitoring Audit” project be defined as the “AP Master File Transaction Analysis.” This project would examine risks and search for anomalies related to VTA’s Accounts Payable master file of vendor information. The scope could include, among other considerations: Vendor Demographic Anomalies

o Vendor Address is not mailable or deliverable (per U.S. Post Office records) o Duplicate business addresses o Vacant address

Procurement Anomalies o Multiple or recurring payments below sole-source threshold o Payments to vendors related by common ownership or as affiliates or subsidiaries o Payments to prime vendors who are also subcontractor vendors on separate contracts

Unexpected Relationships o Vendor officer or director name(s) matches employee name o Vendor address or phone number matches employee’s address or phone number o Multiple vendors with matching Tax ID or Federal Employer Identification Number

(FEIN) o Vendor FEIN matches employee Social Security Number

Legal Issues o Federal or State litigation o Liens and judgments o Bankruptcy filings o Uniform Commercial Code filings

Regulatory Filings / Media o Professional business licenses not in good standing o Regulatory or Security & Exchange Commission actions o OSHA actions o Adverse media coverage o Dun & Bradstreet credit ratings

The recommended project and scope can be accomplished within the existing placeholder project budget of 120 hours and $18,000. No additional funds will be required.

ALTERNATIVES:

The Committee could choose to modify the objective or scope of the recommended project, or could direct the Auditor General’s Office to undertake a different

5

Page 3 of 3

project.

FISCAL IMPACT:

There is no additional fiscal impact. The scope for the proposed project can be accomplished within the existing placeholder project budget of 120 hours and $18,000.

Prepared by: Lily Rogers, AG’s Office & Stephen Flynn, Advisory Committee Coordinator Memo No. 6208

5

Date: August 17, 2017 Current Meeting: September 7, 2017 Board Meeting: N/A

BOARD MEMORANDUM TO: Santa Clara Valley Transportation Authority Governance and Audit Committee THROUGH: General Manager, Nuria I. Fernandez

FROM: Board Secretary, Elaine Baltao SUBJECT: Ratification of Appointments to the Bicycle & Pedestrian Advisory Committee

Policy-Related Action: No Government Code Section 84308 Applies: No

ACTION ITEM

RECOMMENDATION:

Ratify the appointment to the Bicycle & Pedestrian Advisory Committee for the two-year term ending June 30, 2018 of Tom Granvold, representing the City of Santa Clara.

BACKGROUND:

The Bicycle & Pedestrian Advisory Committee (BPAC) advises the VTA Board of Directors on planning and funding for bicycle and pedestrian projects and issues. The BPAC consists of 16 voting members, one appointed by each of VTA’s Member Agencies (the 15 cities in the county and the County of Santa Clara), and one non-voting member and alternate appointed by the Silicon Valley Bicycle Coalition (SVBC). The BPAC also serves as the countywide bicycle and pedestrian advisory committee for the County of Santa Clara. The BPAC bylaws specify that the appointment term is two years and that members may be appointed to successive terms. Committee members must live, work or both in Santa Clara County during their term. Voting members of the Committee must also be a representative of the Member Agency’s local bicycle advisory committee or, for Member Agencies without a local bicycle advisory committee, their representative must be an individual who lives or works in the local jurisdiction and is interested in bicycle or pedestrian issues. BPAC members are precluded from representing a Member Agency that is their employer.

6

Page 2 of 2

The process to fill BPAC vacancies is that staff notifies the appointing authority of the vacancy or approaching term expiration and provides the current membership requirements. The appointing authority then appoints one member for the designated membership position. For vacancies occurring mid-term, the bylaws specify that they be filled for the remainder of the term by the appointing authority. In both cases, the Governance & Audit Committee must ratify the appointment.

DISCUSSION:

The City of Santa Clara has appointed Tom Granvold as its new representative on the BPAC, replacing Sarah Peters, who resigned due to relocating out-of-state. Mr. Granvold, a City of Santa Clara resident since 2008, has lived in California for over 50 years. He is now retired. During his professional career he held jobs with various technology firms, the last being Oracle, where he retired as a Senior Hardware Engineer. He attended the University of California at Berkeley. He is veteran, having served active duty in the U.S. Army. Mr. Granvold is a member of Santa Clara’s BPAC since 2008, and previously served on Sunnyvale's BPAC for a few years when he lived in that city prior to moving to Santa Clara. He has been an avid cyclist for many years, having commuted daily to work year round from the mid 1990s until he retired a few years ago. Over the years he has participated in a variety of group rides including the California Aids Ride, Cycle Oregon, and Waves to Wine. Since retiring, he does the vast majority of his shopping and errands on bicycle. Civic and community service includes as a volunteer Scout Master and as a judge for a local swim team. He is also a member of the Silicon Valley Bicycle Coalition. Based on his qualifications, expertise and community service, staff recommends that the Board ratify this appointment.

ALTERNATIVES:

The Board could choose to not ratify this appointment and instead request that the appointing authority appoint another representative.

FISCAL IMPACT:

There is no fiscal impact as a result of this action.

Prepared by: Stephen Flynn, Advisory Committee Coordinator Memo No. 6164

6

Date: August 23, 2017 Current Meeting: September 7, 2017 Board Meeting: N/A

BOARD MEMORANDUM TO: Santa Clara Valley Transportation Authority Governance and Audit Committee THROUGH: General Manager, Nuria I. Fernandez

FROM: Board Secretary, Elaine Baltao SUBJECT: Conditional Citizens Advisory Committee Appointment

Policy-Related Action: No Government Code Section 84308 Applies: No

ACTION ITEM

RECOMMENDATION:

Ratify the appointment to the Citizens Advisory Committee of Matthew Quevedo, representing the Silicon Valley Leadership Group, conditional on that organization’s current Citizens Advisory Committee representative being appointed to the 2016 Measure B Citizens’ Oversight Committee.

BACKGROUND:

The Citizens Advisory Committee (CAC) is a 17-member committee representing the residents of the various city/county groupings of the VTA Board of Directors, as well as specified community stakeholder groups with an interest in transportation. The CAC advises the Board and VTA administration on issues impacting the communities and organizations they represent. It also serves in two other functions: (1) as the ballot-specified Citizens Watchdog Committee for the 2000 Measure A Transit Improvement Program; and (2) as the 2008 Measure D ballot-specified advisory body that reviews and comments on VTA’s comprehensive transit program as part of the countywide transportation plan.

The CAC bylaws require that a committee member must be a resident of Santa Clara County while on the committee and cannot concurrently hold elected public office. Committee members cannot be VTA staff or employed by a city they represent. The committee membership term is indefinite, with CAC members serving until resignation or replacement by their appointing organization or the VTA Board.

7

Page 2 of 3

The process to fill CAC vacancies, as defined by the bylaws, is that member agencies, specified business and labor groups, and specified community interests positions nominate representatives for their respective membership positions. For select Community Interests positions, VTA’s Administration & Finance Committee appoints one member per position from nominations submitted by advocacy groups or received at-large. In all cases, the Governance & Audit Committee must ratify the appointment.

DISCUSSION:

The VTA Administrative Code establishes the membership of the CAC. One of the five positions in the Business & Labor section represents and is appointed by the Silicon Valley Leadership Group (SVLG). The SVLG’s current CAC representative, Chris O’Connor, is being recommended for appointment to the 2016 Measure B Citizens’ Oversight Committee (2016 MBCOC). This action is dependent on Mr. O’Connor resigning from the CAC, since the 2016 MBCOC bylaws do not allow members of that committee to concurrently serve on any other VTA board or committee. Mr. O’Connor has committed to resign from the CAC, conditional on being appointed to the 2016 MBCOC. Mr. O’Connor’s appointment will be considered by both the Governance & Audit Committee and the Board of Directors at their September 7, 2017 meetings. The SVLG has conditionally appointed Matthew Quevedo to serve as its representative on the CAC, subject to Mr. O’Connor being appointed to the 2016 MBCOC and therefore resigning from the CAC. Matthew Quevedo is the Senior Associate for Transportation and Housing Policy for the SVLG. In this role he works with both public and private stakeholders throughout the region to shape decision-making related to transportation infrastructure, housing development and related funding initiatives. As a member of the Santa Clara County Yes on Measure B campaign, Mr. Quevedo worked as an Outreach Coordinator to ensure voters were informed of the many benefits of the $6.3 billion transportation sales tax package. Mr. Quevedo's background is in local campaigns, neighborhood associations and non-profit organizations. Prior to joining the SVLG in 2016, he helped organize outreach efforts to residents throughout Santa Clara County on the many benefits provided by Rebuilding Together Silicon Valley and their home rehabilitation programs for low-income home owners. His work on political campaigns whose candidates were focused on mixed use growth, transportation and sustainable housing development. Matthew was born and raised in the City of San Jose and currently lives there. He graduated from San Jose State University (SJSU) with a Bachelor’s degree in Political Science and is in his final year of study at SJSU to earn his Master's Degree in Urban and Regional Planning. In his spare time he currently works with residents of downtown San Jose as the President of the San Jose Downtown Residents Association.

7

Page 3 of 3

Based on his qualifications, experience, knowledge of transportation issues and challenges, and extensive community involvement, staff recommends that the Committee ratify the appointment of Mr. Quevedo to the CAC.

ALTERNATIVES:

The Committee could choose to not ratify the conditional appointment, and instead ask the appointing authority to nominate another individual to represent it.

FISCAL IMPACT:

There is no fiscal impact as a result of this action.

Prepared by: Stephen Flynn, Advisory Committee Coordinator Memo No. 6160

7

Date: August 21, 2017 Current Meeting: September 7, 2017 Board Meeting: N/A

BOARD MEMORANDUM TO: Santa Clara Valley Transportation Authority Governance and Audit Committee THROUGH: General Manager, Nuria I. Fernandez

FROM: Board Secretary, Elaine Baltao SUBJECT: Appointment to the Committee for Transportation Mobility & Accessibility

Policy-Related Action: No Government Code Section 84308 Applies: No

ACTION ITEM

RECOMMENDATION:

Approve the appointment to the Committee for Transportation Mobility & Accessibility for the four-year term ending December 31, 2020 of Tricia Kokes, representing Seniors/Individuals with Disabilities.

BACKGROUND:

VTA’s five advisory committees provide input, perspective and technical expertise on proposed changes to VTA policy or priorities potentially impacting transit service and transportation projects throughout the county. The Committee for Transportation Mobility & Accessibility (CTMA) advises the Board of Directors on bus and rail system accessibility issues, paratransit service, and transportation accessibility matters in Santa Clara County. The committee has 17 voting and two ex-officio, non-voting members. The voting membership consists of seven seniors/individuals with disabilities, seven representatives of human service organizations serving older adults or persons with disabilities, and three representatives from either category. The CTMA bylaws define that appointments from either membership category are taken from applications received from the community at-large or nominations from the defined human service organizations. Members serve a four-year term that commences on January 1st and are eligible for reappointment to successive terms. Members from the seniors/individuals with disabilities category must reside within the county during their term.

8

Page 2 of 2

All CTMA membership applications are evaluated by a panel comprised of: (1) Committee Staff Liaison; (2) Advisory Committee Coordinator; and (3) CTMA Chairperson. The evaluation process includes a review of the candidate’s qualifications, evaluation of the organization’s ability to meaningfully represent and facilitate communication their constituencies, and an interview of the individual or a representative of the candidate organization. Effort are made to ensure all specific regional areas of the county and all major disabilities affecting mobility are represented. The panel then recommends the candidate that, in its collective estimation, would best serve the Committee, Board and community. All membership appointments to the CTMA require approval of the Governance & Audit Committee.

DISCUSSION:

Tricia Kokes has been nominated to represent seniors/individuals with disabilities on the CTMA. Ms. Kokes, who has been disabled since birth and uses a mobility device, is a San José native and life-long resident. She is a regular user of VTA fixed route services, primarily bus, but occasionally utilizes VTA Access Paratransit and light rail. During her work career, she was employed by Barton Security and Sun Micro Devices. Civic and community service includes long and extensive service with the Silicon Valley Independent Living Center (SVILC), a San José-based human services organization committed to self-advocacy, personal empowerment and independent living for individuals with disabilities. Ms. Kokes currently is the president of the SVILC Board of Directors, having served on the board since 2009. In addition, she has volunteered at that organization for over twenty years, lending her services to help other individuals with disabilities to have the knowledge and tools to be able to live independently in the community. Prior to that, many years ago she volunteered at the former Health Library located in downtown San José. To evaluate the candidate, in May 2017 the review panel assessed the candidate’s qualifications and, deeming her qualified, conducted an oral interview. Based on her qualifications, service to the community, ability to facilitate bi-directional communication with her stakeholder group, and interest in transit and transportation issues, it was the panel’s unanimous conclusion that Ms. Kokes would well-serve the CTMA and Board. As such, the panel recommends that she be appointed to the CTMA for the four-year term ending December 31, 2020.

ALTERNATIVES:

The Committee could choose to not ratify the appointment of this individual.

FISCAL IMPACT:

There is no fiscal impact as a result of this action.

Prepared by: Stephen Flynn, Advisory Committee Coordinator Memo No. 6147

8

Date: May 19, 2017 Current Meeting: September 7, 2017 Board Meeting: October 5, 2017

BOARD MEMORANDUM TO: Santa Clara Valley Transportation Authority Governance and Audit Committee THROUGH: General Manager, Nuria I. Fernandez

FROM: Chief Financial Officer, Raj Srinath SUBJECT: Update: Follow up on Audit Recommendations Issued by the Office of the

Auditor General as of March 31, 2017

FOR INFORMATION ONLY BACKGROUND:

In 2008, VTA established an independent audit function reporting to the audit committee by utilizing contract auditors to perform independent audit services and serve in the position of the Auditor-General. The Office of the Auditor-General has issued recommendations to strengthen compliance, improve internal control, and promote operational effectiveness and efficiency. In May 2016, VTA Internal Audit Program was established to follow up and report on the status of open audit recommendations and corrective action plans.

DISCUSSION:

The purpose of the audit dashboard report is to provide a status summary of implementation of recommendations. This is a control mechanism established by management to tract and provide reasonable assurance that appropriate and prompt action is provided by management in support of implementing the recommendations. The implementation status was based on compilation of information and documentary evidence from various departments. As of March 31, 2017, the total number of recommendations is 143; of this total, 48 or 34% are not yet due for implementation. Of these 48 not yet due, 37 are not due for implementation until June 2018.

9

Page 2 of 3

The status of implementation of the remaining 95 recommendations is summarized by area of responsibilities in the chart below.

Fully Implemented

Substantially Implemented

NotImplemented

Corrective actions are

complex; no further

actions necessary in

support of the

recommendation.

Major actions are complete;

critical elements of the

recommendations have been

implemented.

Only minor actions in

support of the

recommendations have

been performed; major

actions have yet to be

implemented.

Human Resources & Diversity Programs 1

Information Technology 9

Procurement and Contracts 8 1

ATU Pension Bd 3 1

Engineering & Transp Infra Development 14 1

Finance & Budget 14

General Manager 1

Operations 14 1

Paratransit 10

Grants Planning & Programming Dev 2

Public Relations - Community Outreach 4

System & Safety 11

Totals 91 2 2

Percentage 96% 2% 2%

Audit Area

The below graph shows all recommendations to date by area of responsibility, and their status as of March 31, 2017.

9

Page 3 of 3

Implementation Statusas of 3/31/17

Fully Sub-stantially

Not Implement Not Due

Fully

Implemented 91

Substantially Implemented 2

Not Implemented 2

Not yet Due 48

Exhibit A provides the detail of the 2 recommendations which are substantially complete. One pertains to the recommendation on the utilization of the SAP pension module or similar application to streamline manual process and simplify workflow. This is expected to be completed by June 2017. The other substantially implemented recommendation involves the use of SAP procurement and contracts module, which is on target to be completed by May 31, 2017.

Exhibit B provides the detail of the two recommendations not completed. The one recommendation not implemented relates to VTA’s effort to obtain written assurance from the City of Milpitas of its commitments under the Measure A agreement. Although VTA received $5.1 million out of the $17 million commitment, no written assurances on the remaining outstanding amount has been received. The other recommendation not completed had an original implementation date of January 2017. The recommendation relates to analyzing the cost-benefit of extending station platforms to accommodate three-car trains at the Vasona Branch line. A preliminary study was done which focused on speed and safety improvements throughout the system. A consulting firm has been retained for the cost-benefit analysis of the station expansion. This study is expected to be complete by September 2018. VTA Internal Audit Program will continue to follow up on these recommendations until they are fully implemented. Prepared By: Meeta Podar, Internal Audit Program Manager Memo No. 6114

9

Audit Recommendations that have not been Implemented

During the Period December 31 to March 31, 2017

Exhibit B

Audit Report

Governance &

Audit

Committee

review date

Risk Rating:

High, Medium Recommendation

or Low

Response by Department

Original Target Date

of Implementation

Revised Date of

Implementation

Progress Changes During the Period

Dec 2016 to Mar 2017

2016

Specific

Responsible

Individual

Actions Taken To Date

Other Comments

From To

Not

Implemented

Not

Implemented

Substantially Implemented

Substantially Implemented

Fully

Implemented

Fully Implemented

Operations Operator

Scheduling

Assessment

05/07/15 HIGH We recommend analyzing a cost-benefit of

extending station platforms to accommodate three-

car trains, consistent with the rest of the rail system

thus improving your ability to handle increased

ridership.

VTA management agrees that the current Vasona line infrastructure with two car platforms and two single track segments constrains event day operations as well as daily service. The VTA Planning and Project Development Division has a study underway, the Light Rail Enhancement Project, to review a variety of system design and operational strategies that would improve service, ridership and operating speed. Vasona line improvements are only one of many

enhancements being studied. The study will consider

the cost and benefits of each potential improvement.

Future decisions will be made on which improvements

to pursue for funding and implementation. The study is

targeted for completion by the end of 2016.

1/31/2017 9/30/2018 Not Due

Director of

Planning &

Programming

Per Jim Unites and his team their study done

in 2015 focused on speed and safety

improvements throughout the system, and

placed less focus on specific track and

platform improvements.

They have hired a consulting firm to do a

study on the platform improvements and a

cost-benefit analysis of the station

expansion.

This study is expected to be complete by September

2018.

Engineering and Transportation Infrastructure Development BART SV

Interagency

Agreement

Assessment

11/06/14 HIGH We recommend that VTA obtain written assurances

and clarifications from the City of Milpitas

regarding its commitments under the MA

considering the circumstances of the conflicting

agreement.

VTA agrees. VTA and the City of Milpitas management are coordinating resolution of this issue and are developing the pertinent clarifications regarding the City’s commitments under an amendment to the Master Agreement. Although a firm deadline cannot be established due to the complexity of this issue and because the two parties still need to reach an amended agreement and obtain City Council approval, VTA has already initiated the process of obtaining written assurances and clarifications from the City of Milpitas and anticipates the process will be completed by the end of February

2015.

02/28/15 Dependent on

city's collaborative

effort

Director of Engr &

Transp Infra Dev

(BART Silicon

Valley)

VTA met with the City of Milpitas on July 1,

2015 to coordinate the pertinent

clarifications regarding the City’s

commitments under an amendment to the

Master Agreement. On July 15, 2015, VTA

proposed amended terms for payment based

on the discussions at July 1 Meeting.

(Reference document P0728-C640-LTR-

000001)Although VTA and City staff

continue to meet and coordinate project

implementation matters, VTA has not

received a formal response to the proposed

amendment.

VTA continues to invoice the City for

reimbursement, and is preparing another

request for written assurances and

clarifications from the City of Milpitas

regarding its commitments under the Master

agreement.

This matter is now with the Office of the

General Counsel.

The City of Milpitas has been slow to respond to requests

for payment, or to requests for amended terms for

payment. As of April 30, 2017 VTA has invoiced the

City approximately $14.5 million of the total Authorized

Fund Agreement amount of $17M. VTA received two

payments totaling $5.1M, one in December 2016 for

$3.6M, and one in March 2017 for $1.5M. It is unclear if

further payments will be made.

Failure to properly comply with the agreement increases

the risk that the City may not have adequate funds to

reimburse VTA for the Eastern Segment. Without the

City and VTA reaching agreement, financial exposure to

VTA could potentially reach $11.9M.

9.a

Audit Recommendations that have been Substantially Implemented

During the Period December 31 to March 31, 2017

Exhibit A

Audit Report

Governance &

Audit

Committee

review date

Risk Rating:

High, Medium Recommendation

or Low

Response by Department

Original Target Date

of Implementation

Revised Date of

Implementation

Progress Changes During the Period

Dec 2016 to Mar 2017

2016

Specific

Responsible

Individual

Actions Taken To Date

Other

Comments

From To

Not

Implemented

Not

Implemented

Substantially Implemented

Substantially Implemented

Fully

Implemented

Fully Implemented

ATU Pension ATU Pension

Plan

Compliance

Audit

8/28/14 HIGH Management to explore fully implementing and

using the SAP Pension module or similar

application that fully integrates with SAP.

Utilizing the SAP system to its fullest capabilities

would streamline the manual processes, automate

controls, reduce paperwork and simplify workflow.

This would also allow all documents to be located

electronically in one place and easily accessed,

searched, tracked and reported upon. Additionally,

if VTA management elects to implement the SAP

Pension module, relevant training should be

provided to all users to help maximize system

usability, employee satisfaction with the new

process and return on investment.

VTA management concurs with the recommendation.

VTA will immediately begin evaluation to determine

the business needs of the VTA/ATU Pension Plan

administration process. Following completion of an

SAP enhancement (Pack 6) scheduled for completion

by December 2014 and depending on the results of the

business needs evaluation, VTA will implement either

SAP functionality or another available technology

solution, whichever best meets the business needs.

Although a firm date cannot be determined at this time,

implementation of the technology solution is estimated

for early 2015.

3/31/2015 6/30/2017

Chief Information

Officer

Following update provided by Gary Miskell on

09/06/16:After further analysis in the last week of

August 2016 with Maria Chavez and Jon Maier

the group needs information out of 4 different

data sources (pre 1995 Microfiche, BW data

warehouse, SAP 4.6, and the production SAP),

consolidated into a single data base and a few

custom reports written. To further refine the

requirement, build the data mart, extract the data

and build the reports, estimated completion date is

6/30/17

.While VTA has fully implemented the

digitization of Pension Records to a backed-up,

secure share file - IT is in the design phase of

automating employee records, including Pension

Records, in Sharepoint which is scheduled to be

deployed by 6/30/17

- Critical Pension Plan documents are stored onsite

with no backup of key data and/or documents.

Documents may be misplaced or damaged, and

confidential retiree personally identifiable

information (PII) may be more easily compromised.

- Due to current SAP limitations, necessary Pension

Plan information may not be captured accurately or

timely (i.e. contingent annuitant information).

Procurement & Contracting Process Assessment Procurement &

Contracting

Process

Assessment

05/01/2014 HIGH We strongly recommend Management explore fully

implementing and using the SAP procurement and

contracts module. This would allow all documents

to be online and easily accessible, tracked and

reported upon, which would help remediate current

communication gaps. Utilizing the system to its full

capabilities would streamline the process, reduce

paperwork, allow for online signatures/approvals,

simplify workflow and reduce procurement

turnaround time.

Management concurs. To implement this

recommendation, staff will take the following steps: (1)

Identify functions within the SAP procurement and

contracting modules that have not been implemented,

yet are necessary to completely automate the date

tracking and reporting functionality; (2) In support of

this, staff has initiated development of the prototype

workflow process and status reporting functionality in

SAP. The first reports using this process will be

produced by the close of April 2014; and (3) Initiate the

process to procure the services of a third-party

contractor to expedite the automation of the

procurement and contracting process. Staff will report

on the timeline for full implementation at the next

(August 28, 2014) Audit Committee meeting.

Workflow process: 4/28/2014 Report

on timeline for full implement- action:

8/28/14

05/30/17

Chief Information

Technology,

Manager of

Procurement,

Contracts & Matls,

Substantially completed with on-going process

improvements (based on AG report). Because of the

large undertaking involved with this

recommendation, the PCMM group divided this

into short and long term goals. To date, PCMM has

made substantial progress with the short term items.

The long-term item can be classified as ongoing

process improvement. Documented the

procurement business process from document

creation to PO / Contract approval. Developed an

SAP, K2 interactive forms and sharepoint record

center solution. SAP process, screens and workflow

are being tested with an early August 2016 release.

The interactive custom forms are 85% complete

with testing to start in August of 2016. Storage of

all electronic document will be done in Sharepoint

which is also in test.As of 9/23/2016 - VTA decided

that additional features and functionality be

included to the procurement solution. There are also

improvements to the integration between SAP, K2

interactive forms, and Sharepointe to allow for a

system that better supports the business processes.

The workflow project is on track and will be

completed by the end of this week.

Testing was completed early May 2017,training is

underway and will go live the last week of May

2017.

-The process is, at times, prohibitively delayed,

jeopardizing critical deadlines.- Project documents

are in several places & not organized; documents

may be misplaced or lost.- Buyer/Status of project is

unknown, or not readily available.- No formal

reporting of metrics; limited or no capability to

quickly gather needed data.

9.b

Date: August 31, 2017 Current Meeting: September 7, 2017 Board Meeting: N/A

BOARD MEMORANDUM TO: Santa Clara Valley Transportation Authority Governance and Audit Committee FROM: Auditor General, Bill Eggert SUBJECT: VTA Ethics Hotline Program Quarterly Report

FOR INFORMATION ONLY

BACKGROUND:

The VTA Ethics Hotline is a means for VTA staff and those doing business with VTA to anonymously report suspected unethical behavior such as fraud, waste, abuse, theft, misconduct or any violation of company policy, law or regulation. Launched in February 2015, this 24/7 hotline initially is available only to VTA staff, consultants, and vendors/suppliers. Individuals submitting reports are protected from any retribution by state law and VTA policy. The Ethics Hotline is hosted by a third-party provider, Ethical Advocate, to maintain independence and confidentiality to the extent provided by law. Reports are evaluated, investigated or referred by the Auditor General’s Office, an independent CPA firm reporting directly to the VTA Board of Directors. As part of its duties, the Auditor General’s Office provides high-level summary reports on Hotline usage and results. These reports are provided to the Governance & Audit Committee quarterly, coinciding with the meetings that focus primarily on audit activities, and a yearly report is provided to the Board following the close of the fiscal year.

DISCUSSION:

Attached is the summary report on Ethics Hotline usage from April through June 2017. It contains metrics on Hotline usage including the number of reports received, type of concerns reported, and disposition of the allegations during the subject period. It also includes fiscal year-to-date and trend information. Prepared By: Stephen Flynn, Advisory Committee Coordinator Memo No. 5475

10

VTA Ethics HotlineActivity Summary: 04/01/17 through 06/30/17

1

Method of

Submission

Number

of Reports

Website 1

Phone call 0

Other 0

Total 1

Current Period

ActivityNumber

Fraud 0

Waste or Inefficiency 0

Ethics/Policy Violation 0

Employee

Conduct/Abuse1

Theft 0

Customer Service 0

Non-VTA Issues 0

Total 1

One Year Report Submission 2016/2017

2 2

1 1 1

Jul-16 Aug-16 Sep-16 Oct-16 Nov-16 Dec-16 Jan-17 Feb-17 Mar-17 Apr-17 May-17 Jun-17

Total 1-30 days 31-60 days 60+ days

3

3 0 0

44 30 8 12

Total 50

Aging (Inception through

Current Period)

Preliminary Assessment

Investigation

Completed

10.a

Date: September 1, 2017 Current Meeting: September 7, 2017 Board Meeting: September 7, 2017

BOARD MEMORANDUM TO: Santa Clara Valley Transportation Authority Governance and Audit Committee THROUGH: General Manager, Nuria I. Fernandez

FROM: Board Secretary, Elaine Baltao SUBJECT: Appointment to the 2016 Measure B Citizens' Oversight Committee

Policy-Related Action: No Government Code Section 84308 Applies: No

ACTION ITEM

RECOMMENDATION:

Recommend Board approval of individuals to serve on the 2016 Measure B Citizens' Oversight Committee, per the recommendation of the Evaluation Subcommittee.

BACKGROUND:

On November 8, 2016 Santa Clara County voters approved Measure B that enacted a thirty year half-cent sales tax for transit and transportation improvements. The 2016 Measure B (“Measure B”) ballot specified that “an independent citizens’ oversight committee shall be appointed to ensure that the funds are being expended consistent with the approved Program.” The ballot also listed the specific duties and responsibilities of the citizens’ oversight committee. At its June 1, 2017 meeting, the Board amended the VTA Administrative Code to establish the 2016 Measure B Citizens’ Oversight Committee (“2016 MBCOC”) and approved the bylaws for that committee. The bylaws incorporated the membership criteria previously established by the Board to assist the Committee in its responsibility of evaluating 2016 Measure B revenues and project expenditures to determine compliance with the commitments made to voters in the ballot.

11

Page 2 of 6

The key membership provisions specified in the bylaws are: (A) Eight (8) voting positions from defined areas of expertise and with required experience:

1. A retired federal or state judge or administrative law judge or an individual with experience as a mediator or arbitrator.

2. A professional from the field of municipal/public finance with a minimum of four years relevant experience.

3. A professional with a minimum of four years of experience in management and administration of financial policies, performance measurement and reviews.

4. A professional with demonstrated experience of four years or more in the management of large scale construction projects.

5. A regional community organization representative with at least one year of decision making experience.

6. A regional business organization representative with at least one year of decision making experience.

7. A professional with four years of experience in organized labor. 8. A professional with a minimum of four years of experience in educational

administration at the high school or college level

(B) Members must be registered voters of Santa Clara County

(C) Members cannot hold elected or appointed office or be VTA or Member Agency staff.

(D) Term is four (4) years, and members are limited to two (2) consecutive terms. Half the initial terms will be for two (2) years to establish a staggered appointment cycle.

The 2016 MBCOC bylaws specify that a subcommittee of Board members appointed by the Board Chairperson is responsible for evaluating all applications to determine which applicants possess the required qualifications. After determining all eligible candidate, the subcommittee then recommends to the Governance & Audit Committee its top candidate for each of the eight membership positions. It is then the responsibility of the Governance & Audit Committee to the recommended a candidate for each position for Board approval. At the May 2017 Board meeting, Chairperson Jeannie Bruins announced that she had appointed Board members Larry Carr and Cindy Chavez, Board Vice Chairperson Sam Liccardo, and herself to the Evaluation Subcommittee.

DISCUSSION:

The Evaluation Subcommittee reviewed and evaluated the 46 application received to serve on the 2016 MBCOC. No applications had been received for the Retired Federal/State/ Administrative Law Judge or Mediator/Arbitrator position by then. The Subcommittee determined which candidates possessed the required expertise and experience necessary to be eligible for appointment to the committee. It then ranked the qualified candidates in each category to determine the candidate for each position to be recommended to the Governance & Audit Committee.

11

Page 3 of 6

The recommended candidates are:

1. Retired federal/state/administrative law judge or mediator/arbitrator

[No applications received when subcommittee evaluated applications] 2. Municipal/Public Finance Professional

Rose Herrera Rose Herrera has an extensive career in municipal/public finance. She served eight years on the San José City Council representing Council District 8 (Evergreen), including two years as vice mayor. She also served eight years on the VTA Board of Directors and its various committees, including the then Downtown/East Valley Policy Advisory Board and Ad Hoc Financial Recovery Committees. She is a past board member of the Housing and Community Development Advisory Committee and the Santa Clara Valley Habitat Agency. Furthermore, she served on and chaired the League of California Cities Statewide Transportation, Communication, and Public Works Committee. Civic and community service includes with the County Human Relations Commission, organizing community task forces as part of the Si Se Puede Project, and founding Involved Evergreen, a grass-roots organization formed to bring the Evergreen community together and share a sense of community. She has served on the Delinquency Prevention Commission, the California Association of Human Rights Organizations, and the Symphony San Jose Board of Directors. She founded the Norwood Creek Elementary School PTA and is a founding member of the Bay Area Military Women’s Collaborative. Ms. Herrera founded Cinnamon Software, a software manufacturing company, and served as its CEO for the 10 years prior to her election to the city council. Prior to that, she held positions in worldwide software sales and provided consulting services for other high-tech companies, including tech start-ups. In addition, she served in the United States Air Force where she was in the Security and Intelligence Service. Ms. Herrera is a native of San José and a long-time resident of Santa Clara County, having lived there for over 30 years. She earned both her Bachelors and Masters Degrees from Santa Clara University.

3. Professional in management and administration of financial policies, performance

measurement and reviews

Christine Pfendt Ms. Pfendt has an extensive career dealing with management and administration of financial policies, performance measurement and reviews. She currently is a management consultant for Stanford University where she handles high-profile technology, financial, and process improvement projects to resolve business challenges. Prior to that, she worked at Citigate Cunningham, a public relations firms located in Silicon Valley that specializes in Fortune 500 firms, primarily high-tech, where she held increasingly-responsible positions that included Controller, Chief Financial

11

Page 4 of 6

Officer, Vice President, and, finally, Chief Executive Officer. She also worked at Ziff Davis Events in various positions, the last being Assistant Worldwide Corporate Controller. In addition, she has worked as an Associate at Deloitte & Touche LLP and as the Accounting Manager for the Stanford Alumni Association. Civic and community service includes as a director on the YMCA of Silicon Valley Board of Directors, where she serves on multiple committees. She also volunteers her time as a student advisor at Stanford, and serves as a Community Services Commissioner for the Town of Los Gatos. She has also served as a volunteer at a large number of Olympic Games, including the most recent ones in Rio de Janeiro, Brazil. Ms. Pfendt, a Santa Clara resident, earned her Bachelor’s Degree from California Polytechnic State University, San Luis Obispo.

4. Large Scale Construction Project Manager

Ed Tewes Mr. Tewes, had an extensive career in public service that spanned over 45 years. He served as city manager for the cities of Morgan Hill (13 years), Modesto, and Clovis and as interim city manager for the cities of Gilroy and Guadalupe. He served as assistant city manager for Long Beach and also held various positions at the City of Pasadena. He has served as an adjunct faculty as Gavilan College. He currently is retired and consults part-time for CPS HR Consulting. His community involvement and charitable service is also extensive. Select examples include as a life member, board member and past board president of the International City/County Management Association (ICMA), a member of the Joint Task Force on State Government Reform, the Santa Clara County City and County Managers Association, and the American Society for Public Administration. He was also a member and past president of the California Redevelopment Association board of directors and a board member of the Fresno Economic Development Corporation, Public Policy Center for California State University Stanislaus, United Way of Stanislaus County, Workforce Investment Board of Stanislaus County, and Leadership Morgan Hill. Volunteer activities include as a band booster of Sobrato and Live Oak High Schools and Britton Middle School, the Taste of Morgan Hill street festival, and Morgan Hill Earth Day and Community Clean Up. Mr. Tewes, a Morgan Hill resident, earned his undergraduate degree in political science from Claremont Men’s College and his Master’s Degree in Public Administration from the University of Southern California.

11

Page 5 of 6

5. Regional Community Organization Representative

Bonnie Packer Ms. Packer has very extensive civic experience including on numerous City of Palo Alto committees such as the Comprehensive Plan Citizens Advisory Committee, Planning and Transportation Committee, and the Comprehensive Plan Housing Elements Update. Her vast service with community and charitable organizations in Palo Alto includes over two decades with the League of Women Voters, including on its board and multiple terms as board president. She has been a member and board chairperson of the Palo Alto Family YMCA and a board member of Palo Alto Housing. She has served on the board of several Palo Alto-area community non-profits, including the Women’s Club, the Kiwanis Club, the Palo Alto Art Center, Palo Alto Community Child Care, Chamber of Commerce, Palo Altans for Government Effectiveness, and the Palo Alto Council of PTAs. In addition, she founded the Palo Verde Neighborhood Association. Ms. Packer, who is retired and resides in Palo Alto, was a Senior Attorney at Pacific Bell. She earned her law degree from Santa Clara University and her undergraduate from Columbia University. Prior to earning her law degree, she worked as a book production editor and copy editor, as well as a teacher for the Peace Corps in Turkey.

6. Regional Business Organization Representative

Christopher O’Connor Mr. O’Connor is Senior Director for Transportation Policy for the Silicon Valley Leadership Group (SVLG). In this capacity he works with both public and private stakeholders throughout the region to shape decision-making related to transportation infrastructure, housing development and related funding initiatives. Has was a key member of the SVLG’s leadership effort on 2016 Measure B. Mr. O’Connor has extensive experience in community relations, intergovernmental affairs and public policy, including serving as a senior consultant for the U.S. State Department and on the staff of a California congressman. Mr. O’Connor, who lives in San José, is a native Northern Californian. He earned a Bachelors and Master’s degree in Government from CSU Sacramento

7. Organized Labor Representative

Edward Von Runnen Mr. Von Runnen, who is now retired, worked for VTA for over 36 years, holding four different positions during his career: Bus Operator, Light Rail Operator, Transit Radio Dispatcher, and Transit Bus Dispatcher. During 15 of those years, he served as an ATU Local 265 labor representative, first as a shop steward and later as an executive board member.

11

Page 6 of 6

8. Educational Administration Professional

Jaye Bailey Jaye Bailey has extensive educational administrative experience. She currently is the Vice President for Organizational Development/Chief of Staff at San José State University (SJSU) where she is a member of the SJSU president’s cabinet and serves as principal advisor. Prior to that, she served in the same capacity at Southern Connecticut State University (SCSU). While at SCJU, she held the positions of (1) Associate Vice President for Human Resources and (2) Chief Labor Relations and Employment Officer. Before joining SCSU, she served as both General Counsel and Assistant General Counsel at the Connecticut State Board of Labor Relations. Other professional experience includes as a professional arbitrator/mediator and working as a field attorney for the National Labor Relations Board. Her civic and professional service includes serving on the boards of several organizations, including: Connecticut ACE Women’s Network; Connecticut Labor and Employment Women; Labor and Employment Relations Association, where she also served as vice president; Association of Labor Relations Agencies, where she also served as president and vice president; New England Consortium of State Labor Relations Agencies, where she also served as executive director; and the Connecticut Bar Association, where she was a member and served as chair of its Labor and Employment Law section. Ms. Bailey, a San José resident, earned her law degree from the University of Connecticut and her Bachelor’s degree from the University of Rhode Island.

Consideration of the Governance & Audit Committee’s recommendation on individuals to be appointed to the 2016 MBCOC is scheduled for the Board’s September 7, 2017 meeting. Future applications for the Retired Federal/State/Administrative Law Judge or Mediator/ Arbitrator position will be processed and evaluated by the Evaluation Subcommittee per the established appointment process. The Evaluation Subcommittee’s recommended candidate will then be submitted for Governance & Audit Committee recommendation and Board approval.

ALTERNATIVES:

As defined in 2016 Measure B Citizens’ Oversight bylaws, it is the responsibility of the Governance & Audit Committee to recommend finalist candidates to the Board. Therefore, the Committee can recommend any of the candidates determined by the Subcommittee to possess the required qualifications and thus eligible for appointment.

FISCAL IMPACT:

There is no fiscal impact as a result of this action.

Prepared by: Stephen Flynn, Advisory Committee Coordinator Memo No. 6136

11

Date: September 1, 2017 Current Meeting: September 7, 2017 Board Meeting: October 5, 2017

BOARD MEMORANDUM TO: Santa Clara Valley Transportation Authority Governance and Audit Committee FROM: Auditor General, Bill Eggert SUBJECT: Inventory Management and Costing Assessment

Policy-Related Action: No Government Code Section 84308 Applies: No

ACTION ITEM

RECOMMENDATION:

Review and receive the Auditor General's report on the Inventory Management and Costing Assessment.

BACKGROUND:

The Auditor General’s (AG) Risk Assessment Refresh performed in late 2016 identified inventory management as high risk, in part due to the year-end inventory balance increase from $22 million at the end of Fiscal Year (FY) 2015 to $32 million at the close of FY 2016, an increase of 45%. As a result of the potential financial, strategic, and operational risks identified, the AG’s Office recommended, and the Board approved, that certain existing projects in the Board-approved FY17 Internal Audit Work Plan be deferred so an inventory management and costing assessment could be conducted. The AG’s Office completed this resulting project between December 2016 and May 2017 and the attached report is the result of that review. Inventory management is an ongoing, iterative sub-process of supply chain management focused on optimizing stock on hand to meet organizational demands, which include major transit operations and maintenance needs, while minimizing cost to VTA. It is the practice of overseeing and controlling the ordering, storage and disbursement of items that VTA uses to provide service and maintain its infrastructure and assets. The objective of inventory management is to provide uninterrupted service levels at the minimum cost.

12

Page 2 of 3

DISCUSSION:

The purpose of the Inventory Management and Costing Assessment was to provide independent outside analysis of VTA’s current inventory management processes, assess the design and operating effectiveness of supporting internal controls, and identify opportunities for process and control improvements, including efficiency gains and/or cost reductions. Based on the work performed, an overall report rating of High was assigned to help management understand our assessment of the overall design of VTA’s inventory management and costing processes. This was based on six primary observations categories, two of which were rated High and the other four rated Medium. We also issued 21 corresponding recommendations for corrective action or potential process improvements. Overall, based on our assessment there appears to be several significant opportunities for improvement relative to VTA’s inventory management processes and controls. Overall, our findings illustrate the opportunity for VTA management to: (1) enhance the strategic value of inventory management; (2) improve collaboration and consistency across divisions to enhance inventory related processes; and (3) implement and effectively promulgate controls to manage risk, measure performance, and promote continuous improvement. Specifically, we observed that VTA’s current inventory management process tends to operate more in a reactive mode that stresses fulfilling inventory requests, as opposed to the more optimal strategic and proactive planning and parts reordering process that focuses on continuous long-term strategic needs and continuous monitoring and evaluation. VTA’s current mode has, at times, resulted in critical parts shortages, inaccurate inventory records, operational inefficiency, and increased financial cost. For the inventory management and related supply chain processes reviewed, we observed that some key controls were in place. However, in a large percentage of cases critical inventory controls were either not established, not adequately documented, or not appropriately promulgated to staff to promote consistency and effectiveness. Management concurs with the risks identified and has committed to implement the recommended mitigation actions. Several have been completed, a large number will be completed by the end of 2017, with a few remaining ones by June 2018. Recommendations for improvement or efficiency opportunities contained in this report are presented for the consideration of VTA management, which is responsible for the effective implementation of any action plans.

12

Page 3 of 3

FISCAL IMPACT:

There is no financial impact associated with acceptance of this report.

Prepared by: Lily Rogers, AG's Office & Stephen Flynn, Advisory Committee Coordinator Memo No. 5980 ATTACHMENTS: A--Inventory Management and Costing Assessment (PDF)

12

Inventory Management and Costing Assessment

Auditor General Report No. 2017-05

May 17, 2017

12.a

Inventory Management and Costing Assessment Auditor General Report Issued: May 17, 2017

2

Overall Summary and Review Highlights

The findings identified in our report illustrate the opportunity for VTA management to enhance the strategic value of inventory management by establishing an agency-wide inventory management strategy, collaborating more effectively across divisions to enhance inventory related processes, and controls that manage risk, measure performance, and promote continuous improvement. For the inventory management and related supply chain processes reviewed, we observed that some key controls were in place. In some instances, however, critical inventory controls were either not established or were not adequately documented to promote consistency and effectiveness throughout VTA. This is primarily because VTA has not consistently effected strategic oversight of inventory management and promulgated policies and internal controls that mitigate financial, operational, and strategic risks that could adversely affect VTA achieving its objectives. At times, this has resulted in critical parts shortages, inaccurate inventory records, operational inefficiency, and increased financial risk.

Inventory management operates in a frequently reactive role within the agency that primarily emphasize fulfilling inventory requests, with limited formal proactive planning and parts reordering processes that focus on continuous operations, maintenance, and long-term strategic needs. An overall rating of High was assigned to help management understand our assessment of the overall design of VTA’s inventory management processes. We based our overall rating on our six observations: two rated as High risk and four rated as Medium risk, which are focused on:

Strategic inventory management and ongoing analysis

Proactive parts planning and replenishment

Perpetual inventory records and warehouse logistics

Segregation of duties and asset security

Maintenance work orders and costing

EXECUTIVE SUMMARY

AT

Overall Rating (See Appendix A for definitions)

Report Rating

Number of Observations by Risk Rating

High Medium Low

Inventory Management and Costing

High 2 4 0

Objective and Scope

The primary objectives of this review were to:

Obtain an understanding of VTA’s inventory management and costing processes and controls

Assess the design and operating effectiveness of supporting internal controls

Identify opportunities for process and control improvements, including efficiency gains and/or cost reductions

Additional detail around the scope and work steps completed can be found in Appendix B, with supplemental analyses in Appendices D and E.

Background

Inventory management is an ongoing, iterative sub-process of supply chain management focused on optimizing stock on hand to meet organizational demands, which include major transit operations and maintenance needs, while minimizing cost to VTA. As part of the Auditor General’s (AG) Risk Assessment, inventory management was identified as high risk, partially due to the year-end inventory balance increase from $22 million on June 30, 2015 to $32 million on June 30, 2016, an increase of 45%.

As a result of the potential financial, strategic, and operational risks identified, the AG recommended that certain existing projects in the Board-approved FY17 Internal Audit Work Plan be deferred so an Inventory Management and Costing Assessment could be conducted. The VTA Board approved the request, and the Auditor General’s Office completed this project between October 2016 and January 2017.

The review was performed in accordance with the Standards for Consulting Services issued by the American Institute of Certified Public Accountants. The report is prepared for use by VTA’s Board of Directors, Governance & Audit Committee, and management. Recommendations for improvement are presented for management’s consideration, and management is responsible for the effective implementation of corrective action plans.

We would like to thank those who assisted us throughout this review. Please address questions to Bill Eggert, Auditor General, at [email protected].

12.a

Inventory Management and Costing Assessment Auditor General Report Issued: May 17, 2017

3

OBSERVATIONS SUMMARY

The following is a summary of observations noted in the areas reviewed.

Definitions of the observation rating scale are included in Appendix A.

Ratings by Observation

Observation Title Rating

1. INVENTORY MANAGEMENT: STRATEGIC ORGANIZATIONAL OVERSIGHT AND ANALYSIS High

2. PARTS PLANNING, REPLENISHMENT, AND INVENTORY OPTIMIZATION High

3. PERPETUAL INVENTORY RECORDS AND WAREHOUSE LOGISTICS Medium

4. COMPONENT REBUILDS AND LABOR COSTING METHODOLOGY Medium

5. SAFEGUARDING OF ASSETS AND SEGREGATION OF DUTIES Medium

6. MAINTENANCE WORK ORDERS AND MONITORING Medium

12.a

Inventory Management and Costing Assessment Auditor General Report Issued: May 17, 2017

4

DETAILED OBSERVATIONS

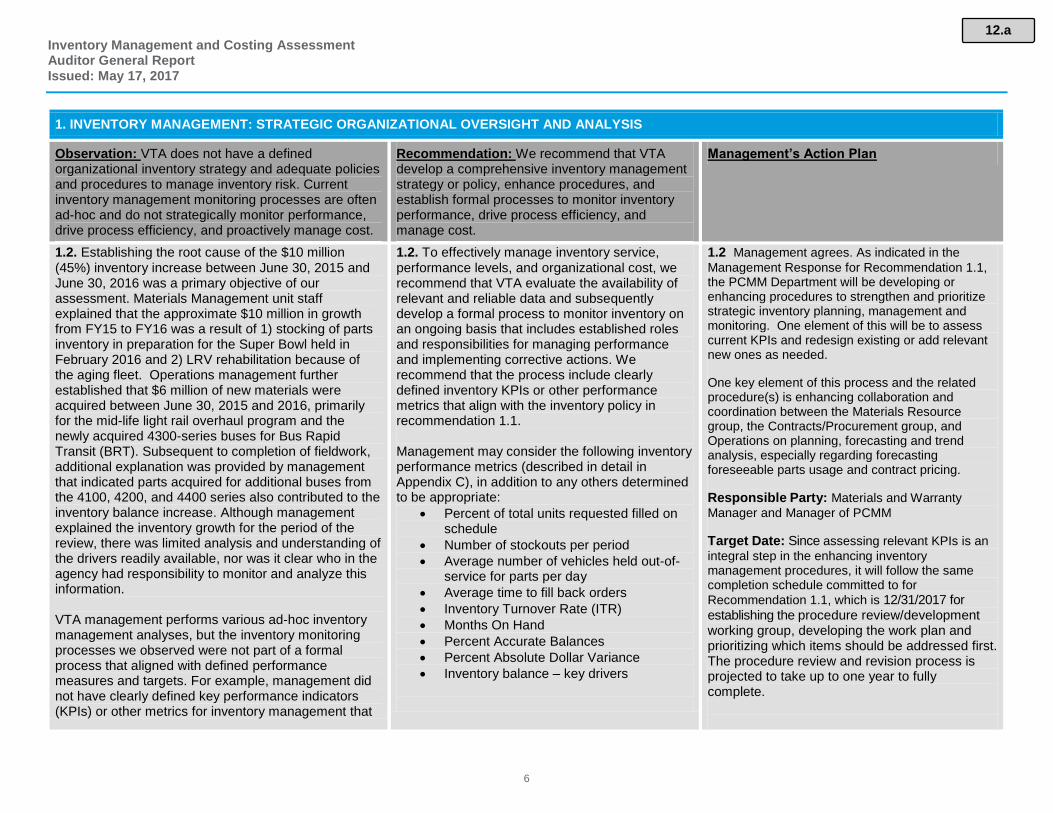

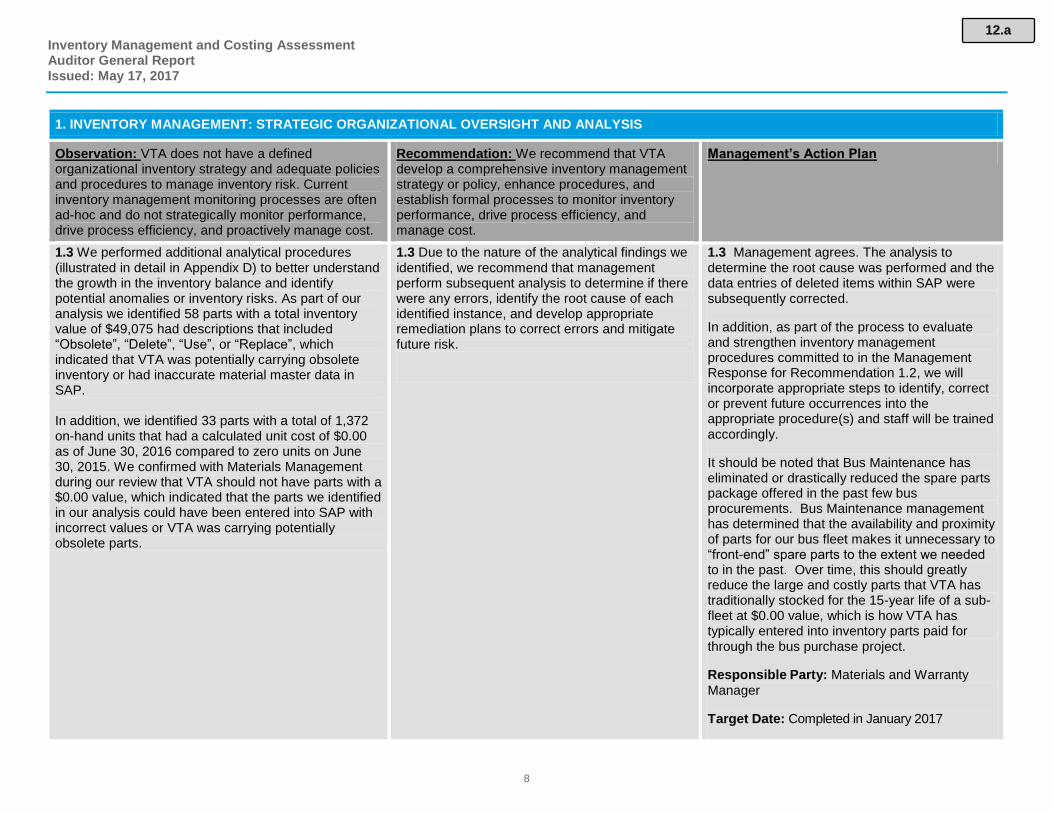

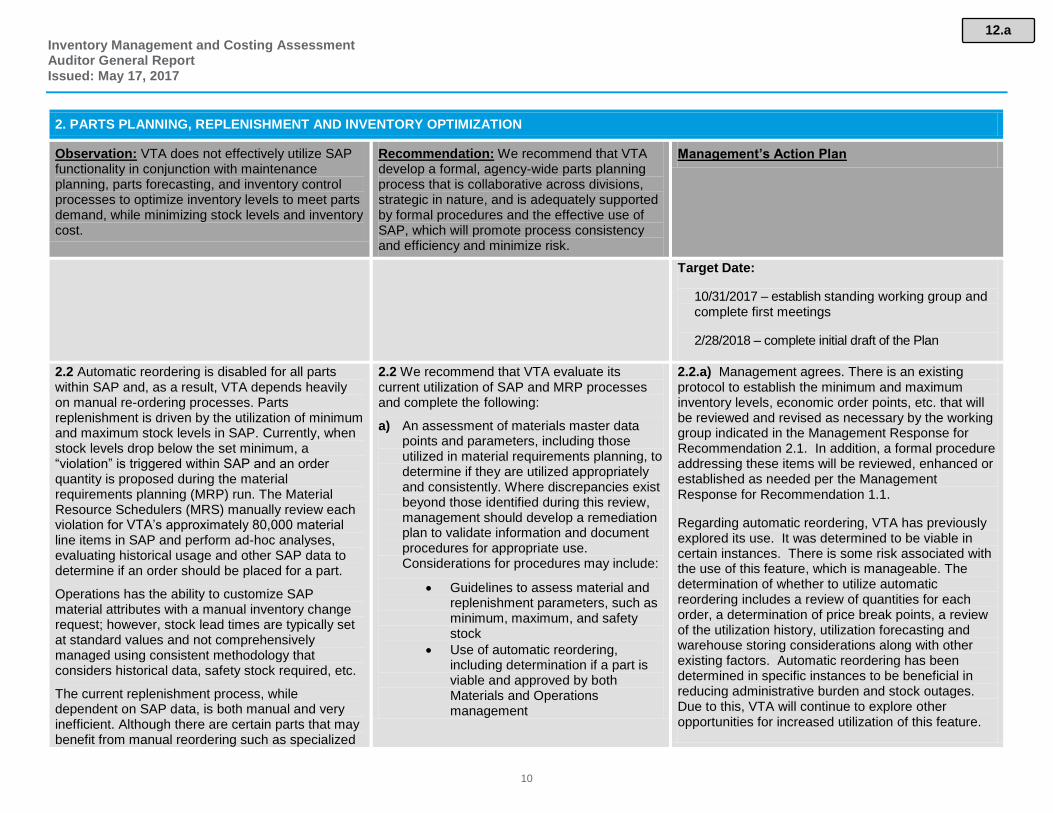

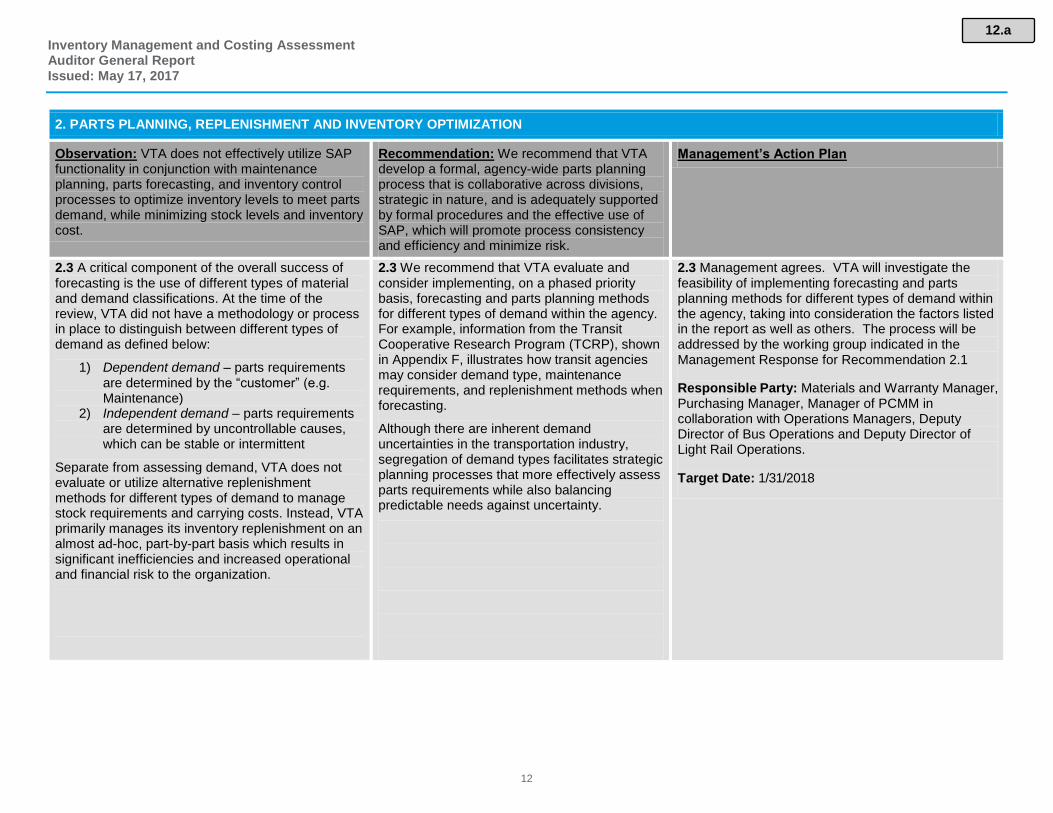

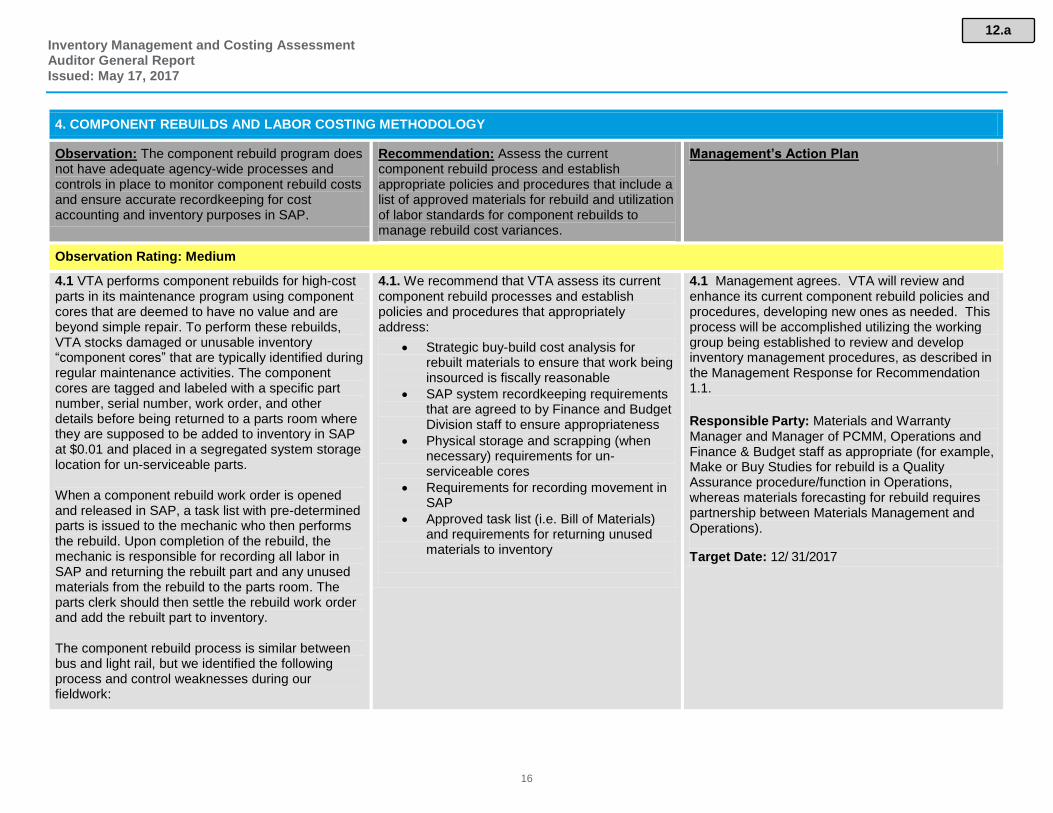

1. INVENTORY MANAGEMENT: STRATEGIC ORGANIZATIONAL OVERSIGHT AND ANALYSIS

Observation: VTA does not have a defined organizational inventory strategy and adequate policies and procedures to manage inventory risk. Current inventory management monitoring processes are often ad-hoc and do not strategically monitor performance, drive process efficiency, and proactively manage cost.

Recommendation: We recommend that VTA develop a comprehensive inventory management strategy or policy, enhance procedures, and establish formal processes to monitor inventory performance, drive process efficiency, and manage cost.

Management’s Action Plan

Observation Rating: High

1.1 Inventory management is a critical factor to VTA achieving its strategic objectives, and many of VTA’s core operations and maintenance activities are dependent on the availability of parts. However, we found that VTA does not have a formal inventory management strategy that clearly establishes organizational responsibility for inventory, including overall inventory management objectives and the inventory management methodology VTA uses to achieve those goals.

Although VTA has established various inventory management processes and procedures, relevant documentation for critical inventory sub-processes, including inventory accounting, excess and obsolescence, physical inventory verification (i.e. cycle counts), adjustments to inventory, etc., was not clearly defined and effectively communicated agency-wide. In some instances, process documentation provided by management did not reflect current business practices.

Without a comprehensive inventory management strategy and robust procedures that are implemented consistently agency-wide, VTA exposes itself to financial, operational, and strategic risks, including operational inefficiencies that could adversely affect the achievement of VTA objectives.

1.1. In order to enhance the inventory management function at VTA by maximizing value and minimizing risk, we recommend that VTA establish a comprehensive inventory management strategic policy that aligns with VTA’s strategic objectives and provides a framework for operational procedures. In addition, we recommend VTA either update or develop inventory procedures to enhance awareness, operational consistency and compliance across the Agency. Management may consider the following relevant areas when developing a comprehensive policy and supporting procedures:

Organizational responsibility

Inventory performance objectives

Inventory management model(s)

Inventory valuation methodology

Excess and obsolescence

Inventory disposal and write-off