Milton Johnson SVP and Controller Goldman Sachs 2004HCA Mark Kimbrough VP, Investor Relations.

1

GOLDMAN SACHS INVESTOR CONFERENCEEric Affeldt – President and CEO

Mark Burnett – COO

Frank Molina – VP, Investor Relations

June 1, 2015

2

CAUTIONARY STATEMENTS

Forward-Looking Statements

Certain statements in this presentation may be considered forward-looking statements. Forward-looking statements generally relate to future events or our future

financial or operating performance. In some cases, you can identify forward-looking statements by terminology such as “may”, “should”, “expect”, “intend”, “will”,

“estimate”, “anticipate”, “believe”, “predict”, “potential” or “continue”, or the negatives of these terms or variations of them or similar terminology or expressions

that relate to our expectations, strategy, plans or intentions. Such forward-looking statements are subject to risks, uncertainties, and other factors which could

cause actual results to differ materially from those expressed or implied by such forward looking statements.

These forward-looking statements are based upon estimates and assumptions that, while considered reasonable by the Company and its management, are

inherently uncertain. Factors that may cause actual results to differ materially from current expectations include, but are not limited to, various factors beyond

management's control adversely affecting discretionary spending, membership count and facility usage and the other risks, uncertainties and factors set forth in

the sections entitled “Risk Factors”, “Cautionary Statement Regarding Forward-Looking Statements” and “Management’s Discussion and Analysis of Financial

Condition and Results of Operations” in the Company's Annual Report on Form 10-K for the fiscal year ended December 30, 2014 and in its Quarterly Report on

Form 10-Q for the quarterly period ended March 24, 2015.

Nothing in this presentation should be regarded as a representation by any person that the forward-looking statements set forth herein will be achieved or that

any of the contemplated results of such forward-looking statements will be achieved. You should not place undue reliance on forward-looking statements, which

speak only as of the date they are made. The Company undertakes no duty to update these forward-looking statements.

Non-GAAP Financial Measures

In our presentation, we refer to certain non-GAAP financial measures. Please refer to the footnotes on each page of this presentation where non-GAAP financial

measures are presented or to the appendix found at the end of this presentation for a reconciliation of these measures to what we believe are the most directly

comparable GAAP measures.

3

Revenue Mix(3)

COMPANY OVERVIEW

Membership

Based

Business

46%

Dues

28%

Food &

Beverage

17%

Golf

Ops

9%

Other

(1) As of April 30, 2015

(2) As of March 24, 2015

(3) As of December 30, 2014; does not reflect a full year of Sequoia Golf

(4) Adjusted EBITDA is not calculated in accordance with accounting principles generally accepted in the U.S. (GAAP). See Appendix for a reconciliation to

the most comparable financial measure calculated in accordance with GAAP

(5) Free Cash Flow is a non-GAAP measure. See appendix for a reconciliation of Free Cash Flow to the most comparable financial measure calculated in

accordance with GAAP

Total Clubs(1)

209Clubs

160

49

Golf & Country

Clubs (GCC)

Business, Sports &

Alumni Clubs (BSA)

» Founded in 1957, ClubCorp has

grown from one club to a leading

owner-operator of private clubs

» 209 owned or operated locations

across 26 states, Washington D.C.,

Mexico and China(1)

» 180,000+ memberships, serving

over 430,000 members(2)

» 200 18-hole equivalents(1)

» Fiscal Year 2014 Results(3)

─ Revenue: $884.2 million

─ Adj. EBITDA: $196.5 million(4)

─ Free Cash Flow: $110.0 million(5)

1 Organic Growth

2 Reinvention

3 Acquisitions

Growth Strategies

3

4

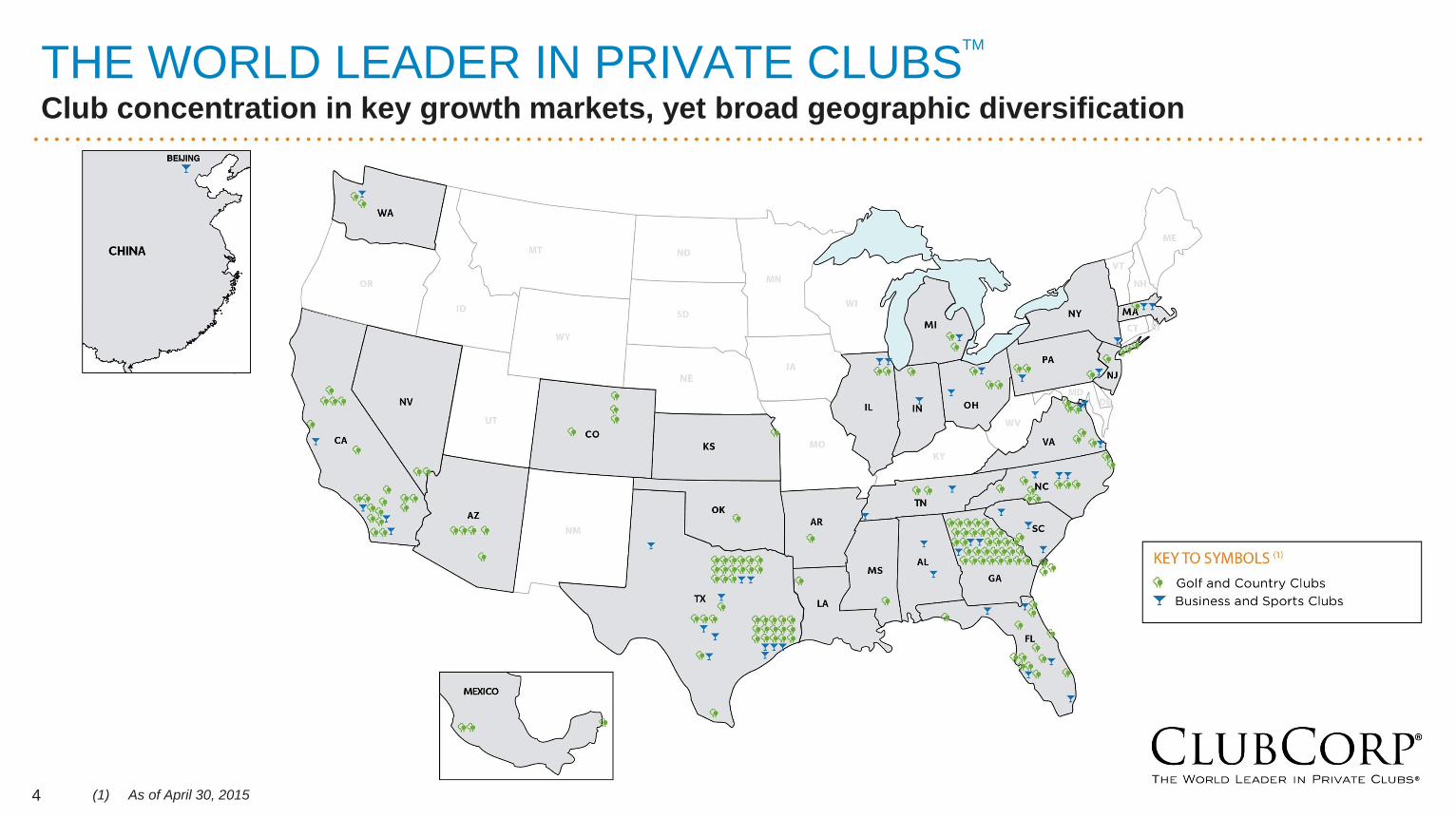

THE WORLD LEADER IN PRIVATE CLUBSClub concentration in key growth markets, yet broad geographic diversification

4 (1) As of April 30, 2015

TM

5

WE’RE IN THE MEMBERSHIP BUSINESSPredictable and stable dues-based membership business tied to mass affluent consumer

84,410 83,724 81,986 80,024 79,656 80,619 82,719 85,397

117,212

86% 86%

83% 83% 83%84% 84% 84% 84%

2006 2007 2008 2009 2010 2011 2012 2013 2014

GCC Membership Trends

Membership Counts Annual Retention Rate

79,383 73,160 67,032 63,967 62,953 62,046 61,405 63,474

77%73% 73%

76% 77% 77% 77% 77%

2007 2008 2009 2010 2011 2012 2013 2014

BSA Membership Trends

Membership Counts Annual Retention Rate

(1) Membership Count includes ~27,000 memberships added in the September 2014 acquisition of Sequoia Golf. Sequoia Golf excluded from Annual Retention Rate

(2) Source: Mosaic demographic analysis of 2014 GCC members within Buxton database

(1)

Resilient Membership Base(2)

» Targeting mass affluent demographic with

average annual household income in

excess of $150k with significant annual

discretionary income

─ Avg. Household income > $200k: 47%

─ Avg. Primary Home value > $750k: 49%

» Strong member retention plus meaningful

percentage of highly visible recurring

revenue makes our dues-based business

model resilient across economic cycles

» Additionally, proximity increases usage and

retention…these clubs are located in

Members’ communities

6

RESILIENT MEMBERSHIP BASETied to mass affluent consumer

A more resilient consumer…

» Targeting mass affluent demographic with average annual household income in excess of $150k with significant

annual discretionary income

» Strong member retention plus meaningful percentage of highly visible recurring revenue makes our dues-based

business model resilient across economic cycles

» Additionally, proximity increases usage and retention…these clubs are located in Members’ communities

21%

13%19%

47%

<$150k $150-175k $175-200k >$200

Average Household Income(1)

(GCC surrounding population demographics)

19% 16% 16%

49%

<$250k $250-500k $500-750k $750k+

Average Primary Home Value(1)

(GCC surrounding population demographics)

4%

30%

46%

20%

25-35 36-50 51-65 65+

Average Age(1)

(GCC surrounding population demographics)

(1) Source: Mosaic demographic analysis of 2014 GCC members within Buxton database.

7

EXECUTING OUR GROWTH STRATEGYUnderlying economics focused on increasing member spend and consolidating industry share

7

Superior Product &

Member Experience

Reinvention

O.N.E. offering

Increase Member Spend

Strategic Acquisitions

Local Market Cluster

Continued Consolidation of

the Industry

8

EXECUTING THREE PRONGED GROWTH STRATEGYUnderlying economics focused on increasing member spend and consolidating industry share

Organic

Growth

O.N.E. (Optimal Network Experiences) provides participating members 50% off á la carte dining at their home club(1),

access to and preferred rates at ClubCorp owned clubs within 50 mile radius, and 2 free rounds of golf per golf &

country club and 2 free meals per business club, per month(1) at ClubCorp owned clubs outside 50 mile radius

Participating members also receive access, special offerings or discounts to more than 300 private and public

facilities and over 1,000 alliance partner locations(2)

Reinvention

Fragmented nature and abundance of member-owned and individually-owned golf courses at compelling

valuations presents roll-up opportunities

Over $337 million spent to acquire 63 golf and country clubs in 2014 and 2015(4)

Our exceptional platform positions us to be a consolidator of the industry

Acquisitions

(1) Some restrictions apply

(2) As of April 30, 2015

(3) Does not include acquisitions and amount subject to change

(4) Includes Sequoia Golf properties owned or operated as of September 30, 2014. Purchase price of $265.0 million before adjustment for cash received of $5.6

million and customary closing adjustments

Significant ROI opportunities within our existing portfolio through modernizing clubs to be more relevant to today’s

members as well as appeal to broader target customers

Over $480 million total capital invested from fiscal year 2007 to fiscal year 2014

Expect to invest approximately $48-53 million of capital in 2015(3)

9

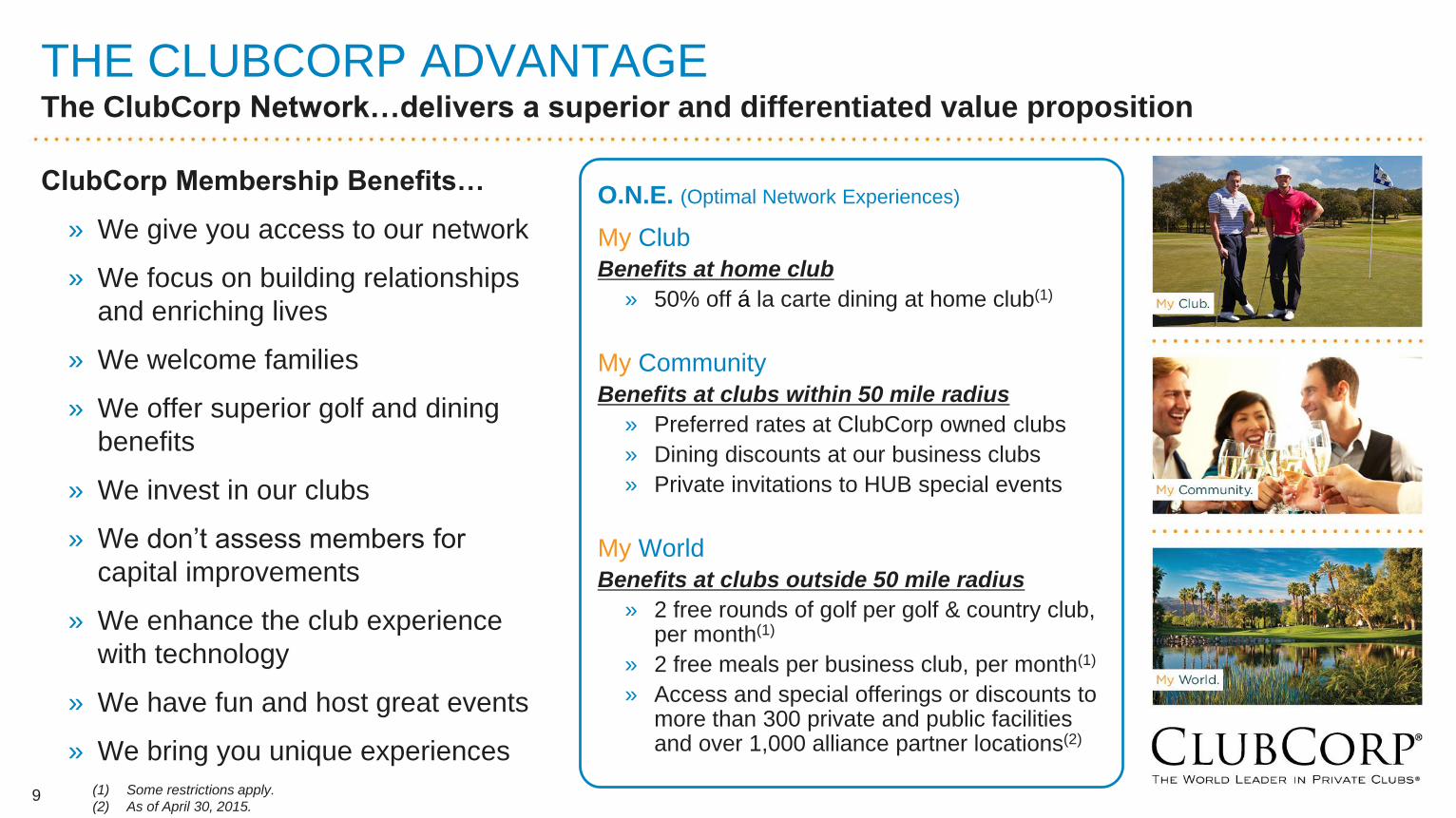

THE CLUBCORP ADVANTAGEThe ClubCorp Network…delivers a superior and differentiated value proposition

ClubCorp Membership Benefits…

» We give you access to our network

» We focus on building relationships

and enriching lives

» We welcome families

» We offer superior golf and dining

benefits

» We invest in our clubs

» We don’t assess members for

capital improvements

» We enhance the club experience

with technology

» We have fun and host great events

» We bring you unique experiences

9

O.N.E. (Optimal Network Experiences)

My Club

Benefits at home club

» 50% off á la carte dining at home club(1)

My Community

Benefits at clubs within 50 mile radius

» Preferred rates at ClubCorp owned clubs

» Dining discounts at our business clubs

» Private invitations to HUB special events

My World

Benefits at clubs outside 50 mile radius

» 2 free rounds of golf per golf & country club, per month(1)

» 2 free meals per business club, per month(1)

» Access and special offerings or discounts to more than 300 private and public facilities and over 1,000 alliance partner locations(2)

(1) Some restrictions apply.

(2) As of April 30, 2015.

10

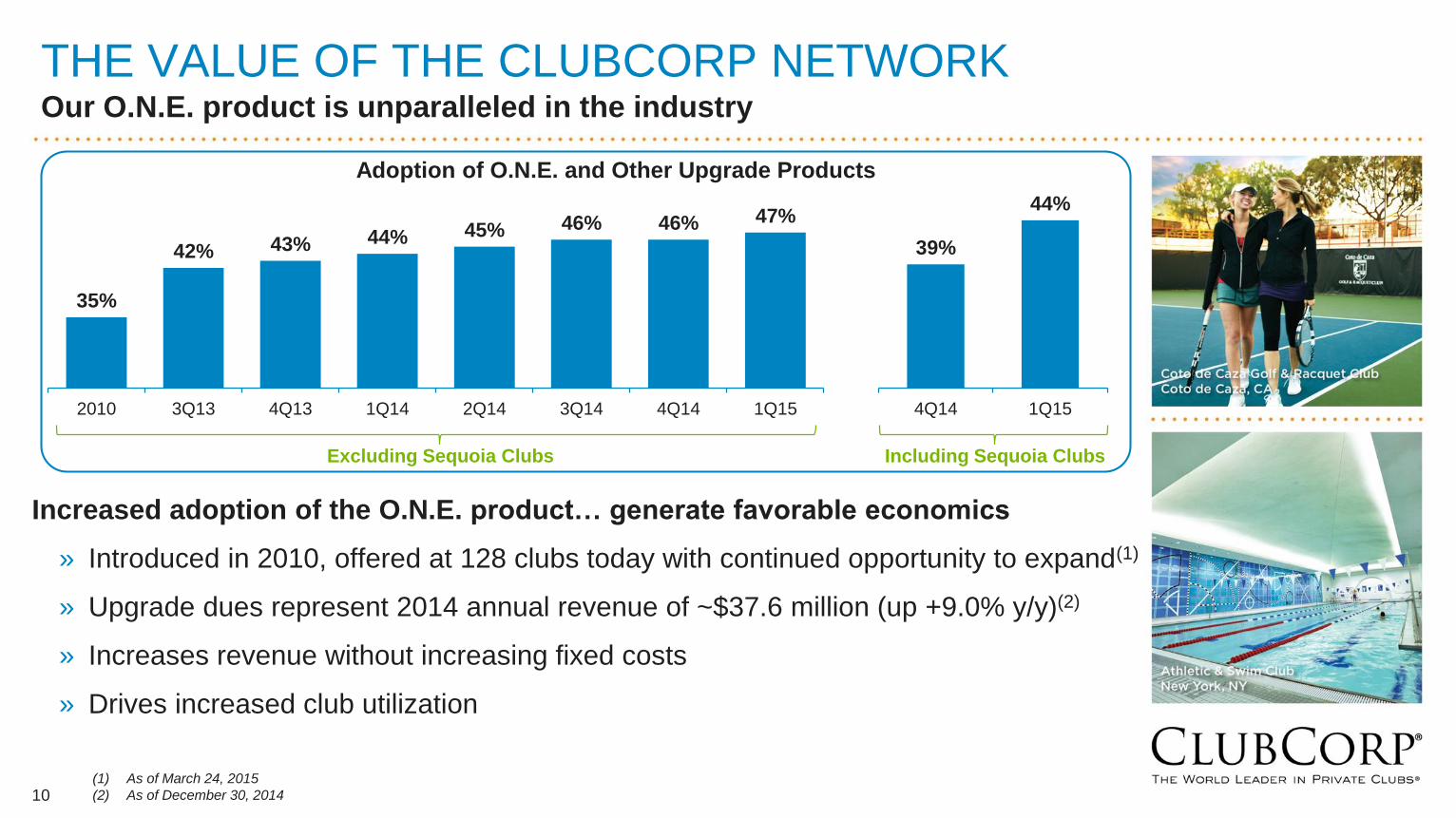

THE VALUE OF THE CLUBCORP NETWORKOur O.N.E. product is unparalleled in the industry

Increased adoption of the O.N.E. product… generate favorable economics

» Introduced in 2010, offered at 128 clubs today with continued opportunity to expand(1)

» Upgrade dues represent 2014 annual revenue of ~$37.6 million (up +9.0% y/y)(2)

» Increases revenue without increasing fixed costs

» Drives increased club utilization

10

35%

42% 43% 44% 45% 46% 46% 47%

2010 3Q13 4Q13 1Q14 2Q14 3Q14 4Q14 1Q15

(1) As of March 24, 2015

(2) As of December 30, 2014

39%

44%

4Q14 1Q15

Adoption of O.N.E. and Other Upgrade Products

Excluding Sequoia Clubs Including Sequoia Clubs

11

REINVENTION ELEMENTSReinventing and / or adding amenities that did not previously exist at the club

11

12

Invested ~$3.8M from mid-2012 to 2014.

Experienced +7.3% increased membership count, +14.6% increased revenue.(1)

GLENEAGLES COUNTRY CLUB (Plano, TX)

Dated, undersized bar

Integrated, modern, private experienceEnhanced fitness facilities

12 (1) Comparison reflects percentage change from pre-construction revenue and membership count in 2012 compared to fiscal year end 2014.

13

CITY CLUB LOS ANGELES (Los Angeles, CA)

Formal, stuffy, traditional

Modern dining, take advantage of viewWarm entry lobby

13 (1) Comparison reflects percentage change from pre-construction revenue and membership count in 2012 compared to fiscal year end 2014.

Invested ~$6.7M, net of landlord provided capital, from mid-2012 to 2014.

Experienced +17.8% increased membership count, +28.7% increased revenue.(1)

14

ACQUISITION OPPORTUNITIESClubCorp is the United States’ largest owner-operator in a highly fragmented industry

Private golf and country clubs in the U.S. …

» ~3,900 private clubs, of which ~16% have a corporate owner(1)

» ClubCorp is ~2-5x its next three largest private club competitors(1)

» In total, ClubCorp owns or operates 160 golf and country clubs(1)

» Acquisition pipeline remains robust

4618

3

MYCC1

135

189

109

MYCC122

1 Club 2 - 5 6 - 24 25 - 100 > 100

Owners of 1 or More Private Clubsand Number of Clubs They Represent(1)

Entities Clubs

3,300+

(1) Source: National Golf Foundation data for 2014. MYCC data as of April 30, 201514

15

CONTINUED CONSOLIDATION OF THE INDUSTRYScope, scale and expertise to acquire and consolidate fragmented industry

Single store additions…

» 16 single store acquisitions

since 2010

» ~$5.2 million average purchase

price per 18 hole equivalent

» ~$2 million additional one-time

reinvention capital per acquired

club

Portfolio additions…

» Sequoia Golf included 50

properties and 990 holes of

golf(3)

» Southeast portfolio added 6

clubs and 171 holes of golf

Date Club Name State Purchase Price (M)# of Clubs # of Holes

2010 Country Club of the South GA $7.61 18

2011 The Hamlet Golf & Country Club

Willow Creek Golf & Country Club

Wind Watch Golf & Country ClubNY $20.03 54

Canterwood Golf & Country Club WA $4.01 18

2012 Hartefeld National Golf Club PA $3.81 18

Chantilly National Golf & Country Club VA $4.61 18

TPC Piper Glen NC $3.81 18

TPC Michigan MI $3.01 18

Total Single Store $89.116 306

Prestonwood Country Club TX $11.222014 36

Oro Valley AZ $3.11 18Sequoia Golf Portfolio Various $260.050 990

Total Portfolio $303.856 1,161

2013 Oak Tree Country Club OK $10.01 36 (1)

Cherry Valley Country Club NJ $5.61 18(2)

(1) Includes purchase price of $5.0 million plus assumption of $5.0 million debt

(2) Purchase price of $6.9 million before adjustment for cash received of $1.3 million

(3) Properties owned or operated as of September 30, 2014. Purchase price of $265.0 million before adjustment for cash received of $5.6 million and customary

closing adjustments

Total ~$392.972 1,467

Ravinia Green Country Club IL $5.912015 18Rolling Green Country Club IL $6.51 18Southeast Portfolio Various $43.86 171

(3)

16

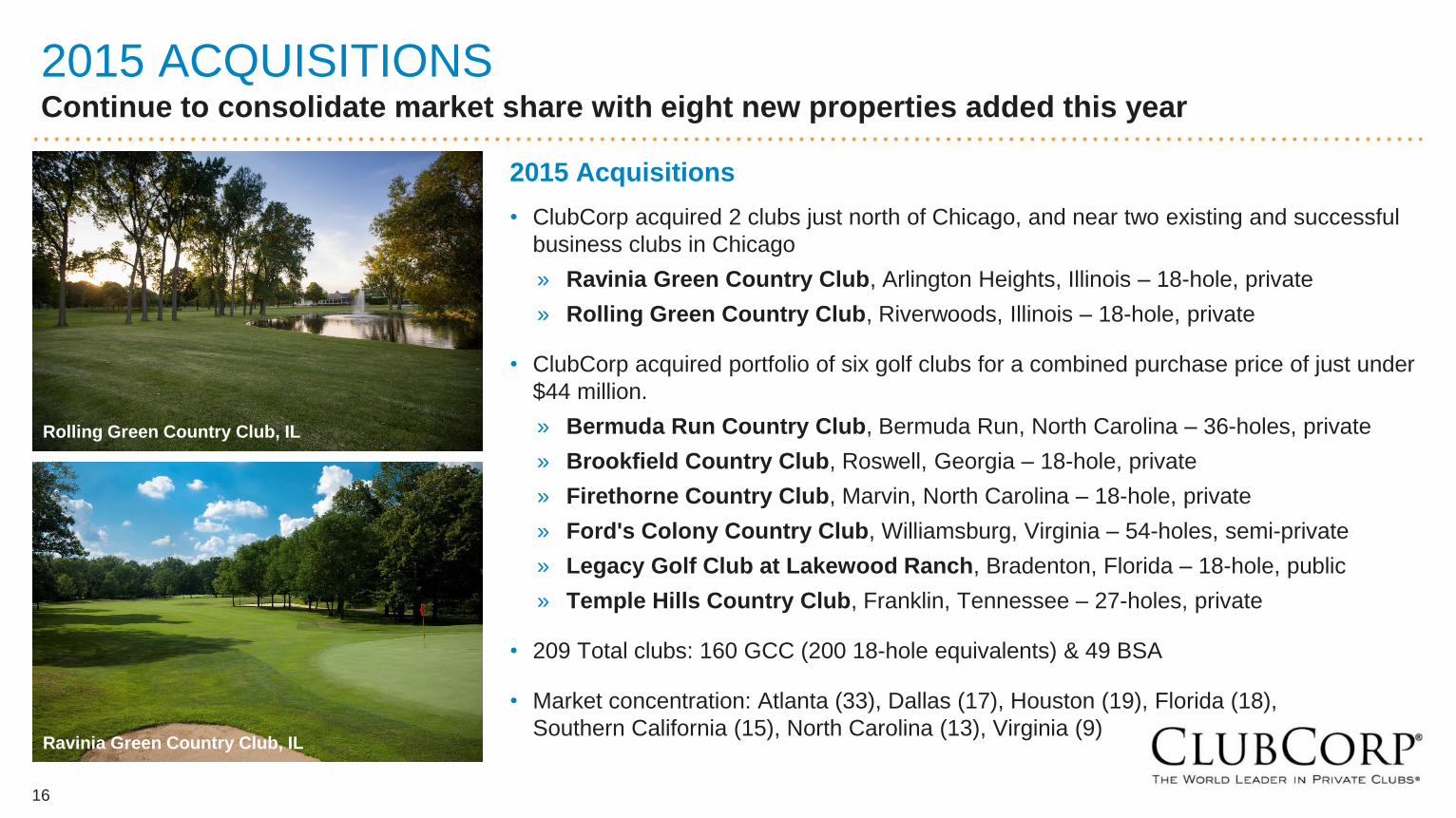

2015 ACQUISITIONS Continue to consolidate market share with eight new properties added this year

Rolling Green Country Club, IL

Ravinia Green Country Club, IL

2015 Acquisitions

• ClubCorp acquired 2 clubs just north of Chicago, and near two existing and successful

business clubs in Chicago

» Ravinia Green Country Club, Arlington Heights, Illinois – 18-hole, private

» Rolling Green Country Club, Riverwoods, Illinois – 18-hole, private

• ClubCorp acquired portfolio of six golf clubs for a combined purchase price of just under

$44 million.

» Bermuda Run Country Club, Bermuda Run, North Carolina – 36-holes, private

» Brookfield Country Club, Roswell, Georgia – 18-hole, private

» Firethorne Country Club, Marvin, North Carolina – 18-hole, private

» Ford's Colony Country Club, Williamsburg, Virginia – 54-holes, semi-private

» Legacy Golf Club at Lakewood Ranch, Bradenton, Florida – 18-hole, public

» Temple Hills Country Club, Franklin, Tennessee – 27-holes, private

• 209 Total clubs: 160 GCC (200 18-hole equivalents) & 49 BSA

• Market concentration: Atlanta (33), Dallas (17), Houston (19), Florida (18),

Southern California (15), North Carolina (13), Virginia (9)

17

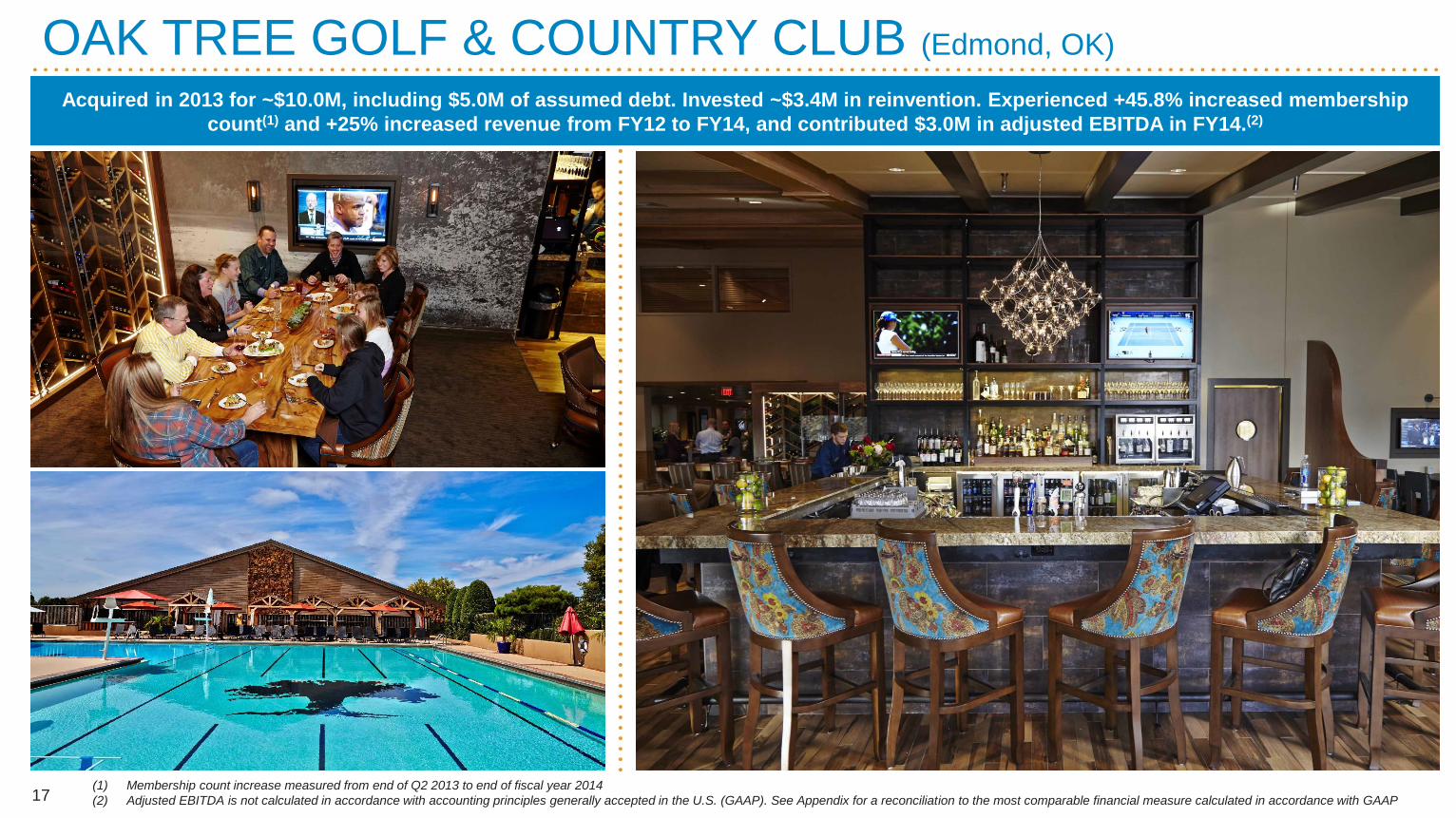

OAK TREE GOLF & COUNTRY CLUB (Edmond, OK)

(1) Membership count increase measured from end of Q2 2013 to end of fiscal year 2014

(2) Adjusted EBITDA is not calculated in accordance with accounting principles generally accepted in the U.S. (GAAP). See Appendix for a reconciliation to the most comparable financial measure calculated in accordance with GAAP

Acquired in 2013 for ~$10.0M, including $5.0M of assumed debt. Invested ~$3.4M in reinvention. Experienced +45.8% increased membership

count(1) and +25% increased revenue from FY12 to FY14, and contributed $3.0M in adjusted EBITDA in FY14.(2)

18

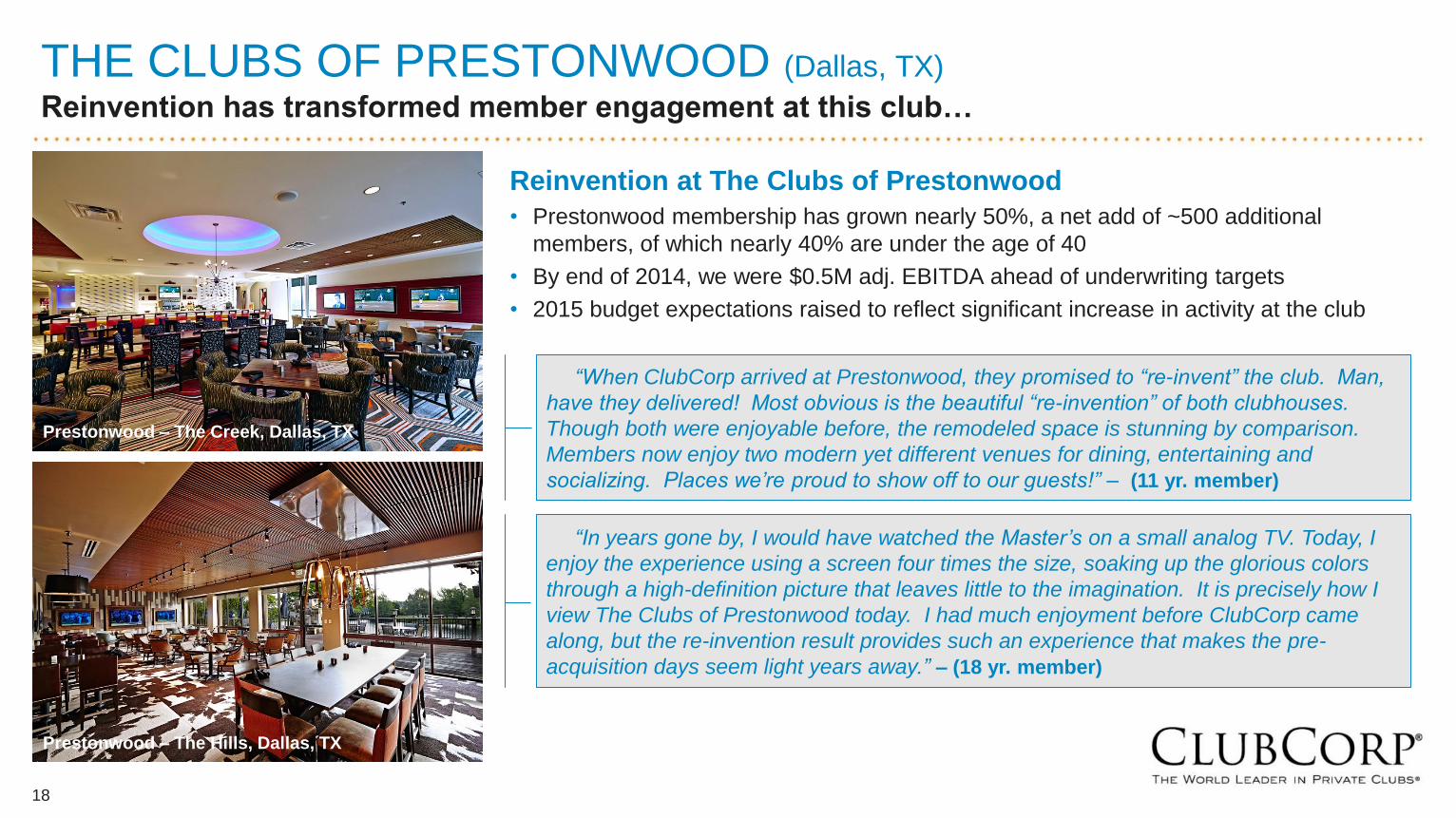

THE CLUBS OF PRESTONWOOD (Dallas, TX)

Reinvention has transformed member engagement at this club…

Prestonwood – The Creek, Dallas, TX

Prestonwood – The Hills, Dallas, TX

“When ClubCorp arrived at Prestonwood, they promised to “re-invent” the club. Man,

have they delivered! Most obvious is the beautiful “re-invention” of both clubhouses.

Though both were enjoyable before, the remodeled space is stunning by comparison.

Members now enjoy two modern yet different venues for dining, entertaining and

socializing. Places we’re proud to show off to our guests!” – (11 yr. member)

Reinvention at The Clubs of Prestonwood

• Prestonwood membership has grown nearly 50%, a net add of ~500 additional

members, of which nearly 40% are under the age of 40

• By end of 2014, we were $0.5M adj. EBITDA ahead of underwriting targets

• 2015 budget expectations raised to reflect significant increase in activity at the club

“In years gone by, I would have watched the Master’s on a small analog TV. Today, I

enjoy the experience using a screen four times the size, soaking up the glorious colors

through a high-definition picture that leaves little to the imagination. It is precisely how I

view The Clubs of Prestonwood today. I had much enjoyment before ClubCorp came

along, but the re-invention result provides such an experience that makes the pre-

acquisition days seem light years away.” – (18 yr. member)

19

1Q15 PERFORMANCEContinue to execute our three-pronged growth strategy

• By offering our members a superior product and exceptional member experience,

we consistently increase member spend, consolidate market share, and drive

long-term shareholder value

• We delivered record first quarter results:

» 1Q15 revenue +22% to $202 million

» 1Q15 adjusted EBITDA +21% to $39 million

• Positive membership growth at both same store clubs, and new or acquired clubs

• Controlled expenses delivering margin expansion across same store clubs

• At Sequoia, most of our projected cost synergies have been fully realized

• Members at recently acquired clubs have gravitated toward our O.N.E. offering, such

that ~44% of our members were enrolled in O.N.E. or similar upgrade offerings

• Added eight new clubs to our portfolio … we now operate 160 golf & country clubs

(GCC), or 200 18-hole equivalents, plus 49 business, sports & alumni clubs (BSA)

19

20

STRONG OPERATING PERFORMANCEProven operating track record with attractive FCF generation

$688 $720 $755$815

$884 $921

2010 2011 2012 2013(53wks)

2014 1Q15LTM

$150 $157 $166 $177$196 $203

21.8% 21.8%22.0%

21.7%

22.2% 22.1%

2010 2011 2012 2013(53wks)

2014 1Q15LTM

20

(1) Adjusted EBITDA is a non-GAAP measure. See Appendix for reconciliation to the most comparable financial measure calculated in accordance with GAAP. Orange line represents Adjusted EBITDA

margin, defined as Adjusted EBITDA divided by Revenue

(2) Same store memberships excludes managed clubs; total memberships includes same store and acquired clubs, but excludes memberships at managed clubs

(3) Free Cash Flow is not calculated in accordance with accounting principles generally accepted in the U.S. ("GAAP"). A reconciliation of Free Cash Flow to the most comparable financial measure

calculated in accordance with GAAP can be found in the appendix of this presentation

Revenue$ millions

CAGR +7.1% Adj. EBITDA(1)

$ millions

CAGR +7.4%

$83.0$87.5

$99.5

$110.0 $112.1

1Q14LTM

2Q14LTM

3Q14LTM

4Q14LTM

1Q15LTM

Levered FCF(3)

$ millions

138,664 139,863 139,664

169,601

1Q14Same-store

1Q15Same-store

1Q14Total

1Q15Total

Memberships(2)

21.4%

0.9%

21

GOLF & COUNTRY CLUBS (GCC)Solid growth across all key operating metrics

$532 $556$586

$628$695

$726

2010 2011 2012 2013(53wks)

2014 1Q15 LTM

48% Dues

23% F&B

22% Golf Ops

7% Other

$726M

Revenue(1)

$ millions

CAGR +7.6% LTM Revenue Mix(1)

$151 $156$168

$180$203 $212

28.4% 28.1%28.8% 28.7% 29.3% 29.2%

2010 2011 2012 2013(53wks)

2014 1Q15 LTM

Adj. EBITDA(1)(2)

$ millions

CAGR +8.3% Memberships(3)

1.2%

32.8%

(1) As of March 24, 2015.

(2) Adjusted EBITDA is a non-GAAP measure. See Appendix for a reconciliation to the most comparable financial measure calculated in accordance with GAAP.

Orange line represents Adjusted EBITDA margin, defined as Adjusted EBITDA divided by Revenue.

(3) Same store memberships excludes managed clubs; total memberships includes same store and acquired clubs, but excludes managed clubs as of March 24, 2015.

83,975 85,009 84,975

112,874

1Q14Same-store

1Q15Same-store

1Q14Total

1Q15Total

22

BUSINESS, SPORTS & ALUMNI CLUBS (BSA)Moderate revenue growth and improving profitability

$168$172

$174

$180$184

$186

2010 2011 2012 2013(53wks)

2014 1Q15 LTM

$30.3$32.5

$34.1 $34.4 $35.2 $36.318.0%18.9%

19.6%19.1% 19.2% 19.5%

2010 2011 2012 2013(53wks)

2014 1Q15 LTM

42% Dues

51% F&B

7% Other

$186M

Revenue(1)

$ millions

Adj. EBITDA(1)(2)

$ millions

LTM Revenue Mix(1)

Memberships(3)

0.3%

3.7%

CAGR +2.4%

CAGR +4.3%

(1) As of March 24, 2015.

(2) Adjusted EBITDA is a non-GAAP measure. See Appendix for a reconciliation to the most comparable financial measure calculated in accordance with GAAP.

Orange line represents Adjusted EBITDA margin, defined as Adjusted EBITDA divided by Revenue.

(3) Same store memberships excludes managed clubs; total memberships includes same store and acquired clubs, but excludes managed clubs as of March 24, 2015.

54,689 54,854 54,689

56,727

1Q14Same-store

1Q15Same-store

1Q14Total

1Q15Total

23

FY14 CAPEXContinued investment in business …

1Q15 Capital Expenditures

• 1Q15 maintenance capex $9.6 million

• 1Q15 expansion capital:

» ROI capital $11.3 million

» Acquisition capital $15.2 million

(i.e., $5.9M for Ravinia Green, $6.4M for Rolling Green, and $3M escrow for six-club portfolio acquisition)

2015 Capital Expenditures

• Remaining in 2015, we anticipate investing ~$38 million on maintenance capex

• Remaining in 2015, we anticipate investing ~$37-42 million on reinvention capital to reinvent and renovate approximately 30+ clubs, including 13 same-store clubs, several clubs from the Sequoia Golf acquisition, and many of our recently acquired single-store clubs

$24.9 $25.1 $16.7 $23.8 $29.1 $9.6

$18.0 $22.8 $37.5$35.7

$43.5

$11.3

2010 2011 2012 2013 2014 1Q15

Maintenance Capex ROI Capex

Capital Expenditures$ millions

24

FY14 FREE CASH FLOWAttractive FCF generation …

$76.8$83.0

$87.5

$99.5

$110.0 $112.1

4Q13LTM

1Q14LTM

2Q14LTM

3Q14LTM

4Q14LTM

1Q15LTM

Free Cash Flow

• +35% y/y increase in LTM levered FCF

• 1Q15 interest expense(2) was $10.3 million

• 1Q15 cash tax expense was $0.2 million

• Paid ~$8.4 million in dividends on January 15, 2015, and the Company currently pays annual dividends of $0.52/share

Liquidity & Capital Structure

• As of March 24, 2015, cash and cash equivalents and total liquidity of $175.3 million. Subsequent to Q1, the Company borrowed $41.0 million on the revolving credit facility, reducing total liquidity to ~$134 million

• As of March 24, 2015, ClubCorp had one term loan of approximately $900 million at L+350 basis points with a 1% LIBOR floor, and revolving credit borrowings of $6.0 million

• As of March 24, 2015, Sr. Secured Leverage Ratio was 4.3x

Levered FCF(1)

$ millions

(1) Free Cash Flow is not calculated in accordance with accounting principles generally accepted in the U.S. ("GAAP"). A reconciliation of Free Cash Flow to the most

comparable financial measure calculated in accordance with GAAP can be found in the appendix of this presentation.

(2) Interest on long-term debt excludes accretion of discount on member deposits, amortization of debt issuance costs, amortization of term loan discount and interest on

notes payable related to certain realty interests which we define as “Non-Core Development Entities”.

25

CAPITAL STRUCTUREStrong balance sheet

Capitalization ($ millions, except share price)

Capitalization March 24, 2015

Common Shares 64.6

Share Price @ 5/21/2015 $22.36

Total Equity Capitalization $1,444

Term Loan $901

Revolver 6

Mortgage Notes 37

Other Debt 2

Capital Leases 34

Total Funded Debt(1) $980

Less Cash Equivalents (73)

Net Debt $907

Total Capitalization $2,351

Non-controlling interest 10

Total Enterprise Value $2,361

Capital structure and liquidity…

» Term loan of ~$900 million priced at L+325 bps with 1% LIBOR floor(2); matures on July 24, 2020

» Senior Secured Leverage Ratio was 4.3x at the end of 1Q15

» Senior Secured Leverage Ratio Covenant of 5.00 : 1.00

» Ample liquidity for future acquisitions

─ Revolver of $135 million with ~$62 million of availability(3)

─ Cash: $72.5 million(4)

(1) Total Funded Debt excludes $12 million of notes payable related to certain non-core development entities and a $3 million discount on term loan

(2) As of May 28, 2015

(3) As of April 30, 2015

(4) As of March 24, 2015

26

INVESTMENT HIGHLIGHTS

Predictable dues-based membership business with growing base

Solid organic growth…tied to mass affluent consumer

Attractive returns on expansion capital, particularly from reinvention

Scope, scale and expertise to acquire and consolidate fragmented industry

Upside from recent acquisitions, including Sequoia Golf

Proven operating track record with attractive FCF generation(1)

26 (1) Free Cash Flow (FCF) is a non-GAAP measure. See appendix for a reconciliation of Free Cash Flow to the most comparable financial measure calculated in

accordance with GAAP.

27

APPENDIX

28

NET INCOME TO ADJUSTED EBITDARECONCILIATION OF NON-GAAP MEASURES TO CLOSEST GAAP MEASURE

(1) Includes non-cash impairment charges related to property and equipment and intangible assets, loss on disposals of assets (including property and equipment disposed of in connection with renovations) and net loss or income from discontinued operations and divested

clubs that do not quality as discontinued operations.(2) Includes (gain) loss on extinguishment of debt calculated in accordance with GAAP. (3) Includes non-cash items related to purchase accounting associated with the acquisition of ClubCorp, Inc. ("CCI") in 2006 by affiliates

of KSL and expense recognized for our long-term incentive plan related to fiscal years 2011 through 2013. (4) Represents adjustments permitted by the credit agreement governing ClubCorp's secured credit facilities including cash distributions from equity method investments

less equity in earnings recognized for said investments, income or loss attributable to non-controlling equity interests of continuing operations, franchise taxes, adjustments to accruals for unclaimed property settlements, acquisition costs, debt amendment costs, equity offering

costs, other charges incurred in connection with the ClubCorp Formation (as defined in our Annual Report on Form 10-K filed with the SEC on March 12, 2015) and management fees, termination fee and expenses paid to an affiliate of KSL. (5) Includes equity-based

compensation expense, calculated in accordance with GAAP, related to awards held by certain employees, executives and directors. (6) Represents estimated deferred revenue using current membership life estimates related to initiation payments that would have been

recognized in the applicable period but for the application of purchase accounting in connection with the acquisition of CCI in 2006 and the acquisition of Sequoia Golf on September 30, 2014.

LTM

FY10 FY11 FY12 FY13 FY14 1Q15

Net income (loss) 252,663$ (35,622)$ (26,992)$ (40,680)$ 13,329$ 12,841$

Interest expense 61,236 84,746 89,369 83,669 65,209 65,614

Income tax expense (benefit) 57,107 (16,421) (7,528) 1,681 (41,469) (45,521)

Interest and investment income (714) (138) (1,212) (345) (2,585) (2,587)

Depreciation and amortization 91,700 93,035 78,286 72,073 80,792 87,159

EBITDA 461,992$ 125,600$ 131,923$ 116,398$ 115,276$ 117,506$

Impairments, disposition of assets and income (loss) from discontinued

operations and divested clubs(1) 12,119 10,880 26,351 14,214 12,452 13,716

(Gain) loss on extinguishment of debt(2) (334,423) - - 16,856 31,498 31,498

Non-cash adjustments(3) (1,881) (37) 1,865 3,929 2,007 2,008

Other adjustments(4) 2,920 15,574 3,237 10,134 25,315 27,630

Equity-based compensation(5) - - - 14,217 4,303 4,573

Acquisition adjustment(6) 9,274 5,006 2,560 1,306 5,644 6,425

Adjusted EBITDA 150,001$ 157,023$ 165,936$ 177,054$ 196,495$ 203,356$

Adjusted EBITDA by Segment:

Golf and Country Clubs 151,148$ 156,001$ 168,491$ 180,208$ 203,415$ 212,065$

Business, Sports and Alumni Clubs 30,253 32,523 34,105 34,350 35,160 36,307

Other (31,400) (31,501) (36,660) (37,504) (42,080) (45,016)

Adjusted EBITDA 150,001$ 157,023$ 165,936$ 177,054$ 196,495$ 203,356$

29

CALCULATION OF FREE CASH FLOWRECONCILIATION OF NON-GAAP MEASURES TO CLOSEST GAAP MEASURE

(1) See the Adjusted EBITDA reconciliation in the preceding slide.

(2) Interest on long-term debt excludes accretion of discount on member deposits, amortization of debt issuance costs, amortization of term loan discount and interest on notes payable related to certain realty interests which we define as “Non-Core

Development Entities”.

4Q13 1Q14 2Q14 3Q14 4Q14 1Q15

LTM LTM LTM LTM LTM LTM

Adjusted EBITDA (1) 177,054$ 179,345$ 183,355$ 187,255$ 196,495$ 203,356$

LESS:

Interest expense and principal amortization on long-term debt (2) 61,317 56,660 51,776 44,370 40,912 41,142

Cash paid for income taxes 3,187 3,192 4,162 2,796 2,723 2,683

Maintenance capital expenditures 23,831 24,279 27,730 28,162 29,067 32,507

Capital lease principal & interest expense 11,885 12,190 12,197 12,436 13,799 14,938

Free Cash Flow 76,834$ 83,024$ 87,490$ 99,491$ 109,994$ 112,086$

(1)

30