Going digital Payments in the post-Covid world

15

A report by The Economist Intelligence Unit Going digital Payments in the post-Covid world

Transcript of Going digital Payments in the post-Covid world

A report by The Economist Intelligence Unit

Going digital Payments in the post-Covid world

The world leader in global business intelligence

The Economist Intelligence Unit (The EIU) offers deep insight and analysis of the economic and political developments in the increasingly complex global environment; identifying opportunities, trends, and risks on a global and national scale.

Formed in 1946 with more than 70 year’s experience, it is ideally positioned to be commentator, interpreter and forecaster on the phenomenon of globalisation as it gathers pace, enabling businesses, financial firms, educational institutions and governments to plan effectively for uncertain futures.

Actionable insight to win in the world’s markets

The world’s leading organisations rely on our subscription services for data, analysis and forecasts that keep them informed about emerging issues around the world.

We specialise in:

• Country analysis—access detailed country-specific economic and political forecasts, as well as assessments of the business environments in different markets with EIU Viewpoint

• Risk analysis—our risk services identify actual and potential threats around the world and help our clients understand the implications for their organisations. Available products: Country Risk Service and Risk Briefing

• Industry analysis—five-year forecasts, analysis of key themes and news analysis for six key industries in 60 major economies. These forecasts are based on the latest data and in-depth analysis of industry trends, available via EIU Viewpoint

• Speaker Bureau—book the experts behind the award-winning economic and political forecasts. Our team is available for presentations and panel moderation as well as boardroom briefings covering their specialisms. Explore Custom Briefing for more speaker information

LONDON

The Economist Intelligence Unit20 Cabot Square, LondonE14 4QW, United Kingdom

Tel: +44 (0)20 7576 8000e-mail: [email protected]

GURGAON

The Economist Intelligence UnitSkootr Spaces, Unit No. 112th Floor, Tower B, Building No. 9DLF Cyber City, Phase - IIIGurgaon - 122002Haryana, India

Tel: +91 124 6409486e-mail: [email protected]

NEW YORK

The Economist Intelligence Unit750 Third Ave, 5th Floor, New YorkNY 10017, United States

Tel: +1 212 541 0500e-mail: [email protected]

DUBAI

The Economist Intelligence UnitPO Box No - 450056, Office No - 1301AAurora TowerDubai Media CityDubai, United Arab Emirates

Tel: +971 4 4463 147e-mail: [email protected]

HONG KONG

The Economist Intelligence Unit1301 Cityplaza Four12 Taikoo Wan RoadTaikoo Shing, Hong Kong

Tel: + 852 2585 3888e-mail: [email protected]

Contact us

GOING DIGITAL: PAYMENTS IN THE POST-COVID WORLD

© The Economist Intelligence Unit Limited 20211

Contents

Introduction 2

Pandemic gives regulators a unique opportunity to spur digital payments 4

Card-backed payment systems hold sway in the developed world 5

China’s super app model to dominate emerging Asia 6

In Africa, mobile network operators give way to super apps 7

Fast-payment systems are transforming developing countries 8

New frontiers: central bank digital currencies 9

Transform or perish 11

GOING DIGITAL: PAYMENTS IN THE POST-COVID WORLD

© The Economist Intelligence Unit Limited 20212

Across the world, digital payments are now synonymous with mobile payments, with the rate of adoption directly linked to access to smartphones and telecoms networks. The furious

growth in digital payments in developing countries, especially in Asia, demonstrates the impact of the coronavirus (Covid-19) pandemic in advancing online retail sales, as well as the role that governments and regulators play in facilitating the spread of new payments systems.

Our research shows how the digital-payment revolution is transforming business in different parts of the world. Governments have a crucial role to play in formulating policies that guarantee equitable access to these systems while encouraging innovation. However, regulators’ responsibilities will increase further with the spread of digital currencies and super apps, which will allow for more cross-selling while also exacerbating the risks to data security, privacy and sustainable credit terms. Both payments services providers and conventional financial services companies need to be ready for regulatory shifts as they seek to take advantage of new opportunities.

Key implications:

• Governments in countries with a low level of digitalisation and unsatisfactory financial inclusion must recognise that an enabling policy framework and public investment are keys to the successful widespread adoption of digital-payment systems.

• Payment-platform providers must create additional capacity to prepare for greater demand for digital-payment services, as well as opportunities to migrate customers to financial services that yield higher margins. They must also prepare for the rising costs and complexities of compliance with regulatory requirements.

• Firms and service providers in adjacent areas must rapidly transform their businesses to benefit from these developments. Their strategies should include improving the interoperability of their digital platforms and deploying application programming interfaces (APIs) to allow the use of embedded-payment systems.

• Regulators must adopt a proactive, multi-level approach to technological changes when formulating new standards, as well as closely monitoring any financial risks within payments systems.

Going digital: payments in the post-Covid world

GOING DIGITAL: PAYMENTS IN THE POST-COVID WORLD

© The Economist Intelligence Unit Limited 20213

China leads global mobile-payment market

Sources: Business of Apps; eMarketer; The Economist Intelligence Unit. *As at end-2020

Global mobile payments market Adoption of mobile payments (as % of smartphone users)†

Mobile-payment users (m)*

2015 16 17 18 19 20

400

600

800

1,000

1,200

1,400

1,600Revenue (US$ bn)

0.4

0.6

0.8

1.0

1.2

1.4

1.6Users (bn)

0 20 40 60 80 100

China

India

United States

Japan

Italy

United Kingdom

Russia

France

Germany

AliPay WeChatPay

ApplePay

GooglePay

SamsungPay

Venmo CashApp

PayPal

0

200

400

600

800

†as of end-2019.

GOING DIGITAL: PAYMENTS IN THE POST-COVID WORLD

© The Economist Intelligence Unit Limited 20214

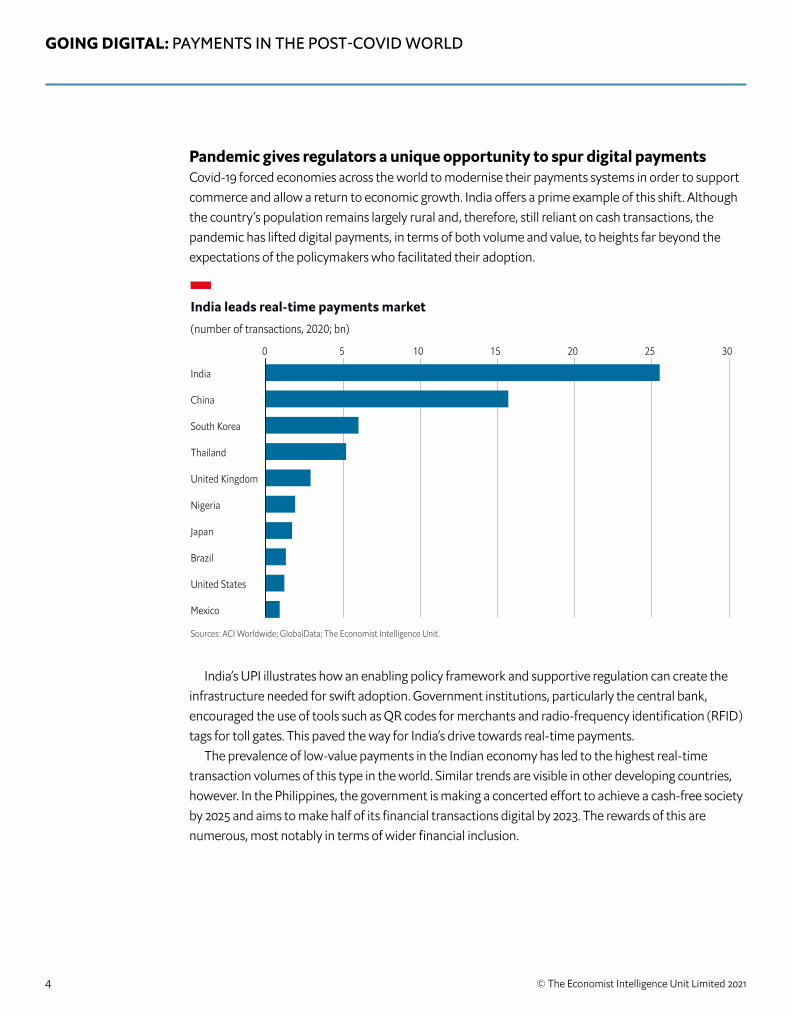

Pandemic gives regulators a unique opportunity to spur digital paymentsCovid-19 forced economies across the world to modernise their payments systems in order to support commerce and allow a return to economic growth. India offers a prime example of this shift. Although the country’s population remains largely rural and, therefore, still reliant on cash transactions, the pandemic has lifted digital payments, in terms of both volume and value, to heights far beyond the expectations of the policymakers who facilitated their adoption.

India’s UPI illustrates how an enabling policy framework and supportive regulation can create the infrastructure needed for swift adoption. Government institutions, particularly the central bank, encouraged the use of tools such as QR codes for merchants and radio-frequency identification (RFID) tags for toll gates. This paved the way for India’s drive towards real-time payments.

The prevalence of low-value payments in the Indian economy has led to the highest real-time transaction volumes of this type in the world. Similar trends are visible in other developing countries, however. In the Philippines, the government is making a concerted effort to achieve a cash-free society by 2025 and aims to make half of its financial transactions digital by 2023. The rewards of this are numerous, most notably in terms of wider financial inclusion.

India leads real-time payments market(number of transactions, 2020; bn)

Sources: ACI Worldwide; GlobalData; The Economist Intelligence Unit.

0 5 10 15 20 25 30

India

China

South Korea

Thailand

United Kingdom

Nigeria

Japan

Brazil

United States

Mexico

GOING DIGITAL: PAYMENTS IN THE POST-COVID WORLD

© The Economist Intelligence Unit Limited 20215

Card-backed payment systems hold sway in the developed worldThe most familiar—and least revolutionary—change is occurring in developed countries where the existing card-payment infrastructure has been extended to mobile phones and contactless cards. For example, the widely adopted systems of Apple Pay, Google Pay and Samsung Pay use traditional branded cards embedded in mobile apps to make transfers at improved point-of-sale (POS) terminals. They use the existing infrastructure to move money from payer to recipient while allowing card networks and issuers to continue to collect fees. Contactless payment, adoption of which was sluggish prior to the pandemic, has taken off amid fears that the virus is being spread by handling currency notes.

Card-driven contactless payments will take off at a rapid pace in the Americas and Western Europe, where consumer wearables (smartwatches, for example) will also emerge as a key medium for payments. In contrast to chip and pin-based cards, contactless cards reduce transaction time and provide a seamless experience for both merchants and customers. Mobile apps such as Apple Pay and Samsung Pay will continue to lift the engagement levels of their users, incentivising them to use their platforms for a host of other digital transactions, including utility-bill payments, personalised savings and credit products and online shopping. Meanwhile, players in Europe, such as Sweden’s Swish, will continue to evolve to provide services enabled by real-time payment infrastructure and other innovations that the regulators are pursuing in the region, such as QR codes.

Apple Pay leads proximity mobile payments in US

(m users; as at March 2021)*

Sources: eMarketer; The Economist Intelligence Unit.

Apple Pay Starbucks Google Pay Samsung Pay

0

10

20

30

40

50

14+ aged mobile users that have made at least one transaction in the past six months; excludes transactions made via tablets.

Key geographies: North America | Western Europe

GOING DIGITAL: PAYMENTS IN THE POST-COVID WORLD

© The Economist Intelligence Unit Limited 20216

China’s super app model to dominate emerging AsiaA more radical approach has upended payments in China and is increasingly doing so in other parts of Asia. AliPay and WeChat, whose apps link users’ mobile phones to existing bank accounts, emerged with the spectacular increase in Chinese e-commerce at their parent firms, Alibaba and Tencent, in the 2000s. Originally used for online purchases and messaging, they expanded to become “super apps”—all-in-one platforms that offer ride-hailing, food delivery, entertainment services and a full range of financial products, including credit and insurance. Singapore’s Grab, Indonesia’s Gojek, South Korea’s KakaoPay and India’s Flipkart and PayTM are aiming to build their own super apps.

In China, the birthplace of the super app, regulators are now cracking down on platforms that have previously benefited from loose regulatory oversight to gain a monopolistic advantage in financial services and vertically integrated e-commerce. After allowing simple payments providers to grow into major distributors of financial products, even offering interest-yielding deposits, regulators now want to make them subject to the same supervision that is applied to banks. This is likely to include capital adequacy requirements.

By contrast, South-east Asia lacks the cautious approach of Chinese regulators, with governments largely supportive of indigenous super apps, at least at present. Most of the region’s economies have large informal sectors, which means that significant sections of the population have limited access to banking and other savings products. Governments in emerging Asia will maintain a benign attitude to regulating super apps, looking to leverage such platforms to attain financial-inclusion targets.

Next wave of super apps in Asia

Sources: Tracxn; Briter Bridges; Business of Apps; The Economist Intelligence Unit

INDONESIAINDONESIASINGAPORE

INDIA

JAPANSOUTH KOREA

VIETNAM

INDONESIA

Promising candidates

Announced an US$18bn merger with Tokopedia in May 2021

Proposed to pursue a US$40bn SPAC IPO in 2021

Filed papers for a US$2.2bn IPO in July 2021

Acquired by Walmart for US$16bn in 2018

167m monthly active users across Japan, Thailand, Taiwan and Indonesia (Q3 2020)

Registered US$58.2bn transactions in 2020

Part of VNG Corp, Vietnam's first-ever unicorn

Notes: Unicorns are private-sector start-ups valued more than US$1bn. IPO - initial public o�ering. SPAC - special purpose acquisition company.

GOING DIGITAL: PAYMENTS IN THE POST-COVID WORLD

© The Economist Intelligence Unit Limited 20217

In Africa, mobile network operators give way to super appsA third distinct path has emerged, primarily in less-developed economies where the use of mobile phones has become widespread but few citizens have formal financial accounts. For example, Kenya’s telecoms firm, Safaricom, and the UK-based Vodafone created M-Pesa in 2007 to allow users to transfer funds domestically to friends and family using mobile-phone credits. The success of the system led to its extension to regular retail payments and to it being linked to users’ bank accounts. The mobile-money revolution has since caught on in Nigeria, which has Africa’s largest unbanked population. However, in contrast with Kenya, the mobile-money industry in Nigeria is dominated by banks and technology firms, as telecoms operators cannot apply directly for mobile-money licences.

Over the medium term, mobile-money operators will scale up their value-added financial services, such as interest-yielding deposits and insurance, supported by the growing number of people joining the ranks of the middle- and high-income groups. Incumbent mobile-money players will emerge as major fintech players in the region, alluring capital and partnership opportunities from major global payment-platform and technology firms. The bigger players will shift focus to create platform-like structures, adding new verticals and creating a suite of products and services, such as ride-hailing, food delivery, and entertainment for their users. In other words, they will evolve to become more like Asia-style super apps.

Key geographies: China | India | South-east Asia

Payments are the core element of the super-app value proposition in South-east Asia First functionality Expansion Not yet present

Payments E-commerce

Financial Services

Mobility/delivery Deals Chat

Fave (Singapore)

Grab (Singapore)

Gojek (Indonesia)

Line ( Japan)

Lazada (Singapore)

Shopee (Singapore)

Tokopedia (Indonesia)

Note. Mobility / delivery also includes food delivery, ride-hailing and logistics services. Financial services include banking, insurance and investment services. Deals include coupons or discounts on dining, staycation, travel, movies and other lifestyle products.

Sources: Tech in Asia; The Economist Intelligence Unit.

GOING DIGITAL: PAYMENTS IN THE POST-COVID WORLD

© The Economist Intelligence Unit Limited 20218

Fast-payment systems are transforming developing countries Governments championing fast-payment systems indicate that they expand financial inclusion while reducing the leakage of subsidies. Following the success of India’s UPI, several countries are currently in the process of building instant real-time payment platforms. Brazil, for example, debuted its fast-payment platform, Pix, in late 2020, while, in early 2021, Saudi Arabia unveiled its new version of the instant-payments platform, Sarie, which facilitates quick transfer of funds using various methods of identification, including mobile number and email address.

Key geographies: Sub-Saharan Africa

Kenya and Nigeria drive mobile money in Africa

Sources: Central Bank of Kenya; Central Bank of Nigeria; company reports; The Economist Intelligence Unit.

*Data for 2020 is from Jan-Aug.

Leading players in Africa (m users)†

M-Pesa Airtel Money MTN MoMo

FY 2018/19 2019/20 2020/21

Registered accounts in Kenya (m)

2014 15 16 17 18 19 20

20

30

40

50

60

70

†Fiscal years: Apr-Mar (M-Pesa, Airtel Money); Jan-Dec (MTN MoMo).

0

10

20

30

40

50

Transactions volume in Nigeria (m)*

0

100

200

300

400

500

2014 16 18 2015 17 19

GOING DIGITAL: PAYMENTS IN THE POST-COVID WORLD

© The Economist Intelligence Unit Limited 20219

In the second half of the present decade, adoption of digital payments will mature in most countries as platforms emerge as major distribution channels for savings and credit products. Players with diverse verticals and enjoying a presence across geographies will then stand to benefit, generating robust fees for their platforms from both customers and businesses. Payments operators, especially in emerging markets, will shift their focus towards improving their profitability, moving on from their current preoccupation with expanding their customer bases.

New frontiers: central bank digital currenciesThe rapid adoption of digital payments has also accelerated the launch of digital currencies, as governments try to wrest back some control over money supplies, as well as further facilitating the digitalisation of payment systems. Central banks around the world are advocating that these currencies be built around a digital identity, thereby safeguarding data security and privacy—lack of which is a major criticism of cryptocurrencies.

India's UPI leads retail fast-payment systems

United Payment Interface (UPI) Brazil’s Pix

Saudi Arabia’s Sarie Thailand’s PromptPay

2017 18 19 20

0

5,000

10,000

15,000

20,000Volume (m)

0

15,000

30,000

45,000

60,000Value (US$ bn)

N D J F M A M J

2020 2021

0

200

400

600

800Volume (m)

0

25

50

75

100Value (US$ bn)

2016 17 18 19 20

0

50

100

150

200

250Volume (m)

0

500

1,000

1,500

2,000

2,500Value (US$ bn)

2017 18 19 20

0

1,500

3,000

4,500

6,000Volume (m)

0

200

400

600

800Value (US$ bn)

Sources: National Payment Corp of India; Banco Central do Brasil; Saudi Central Bank; Bank of Thailand; The Economist Intelligence Unit.

Key geographies: Asia | Middle East | Latin America

GOING DIGITAL: PAYMENTS IN THE POST-COVID WORLD

© The Economist Intelligence Unit Limited 202110

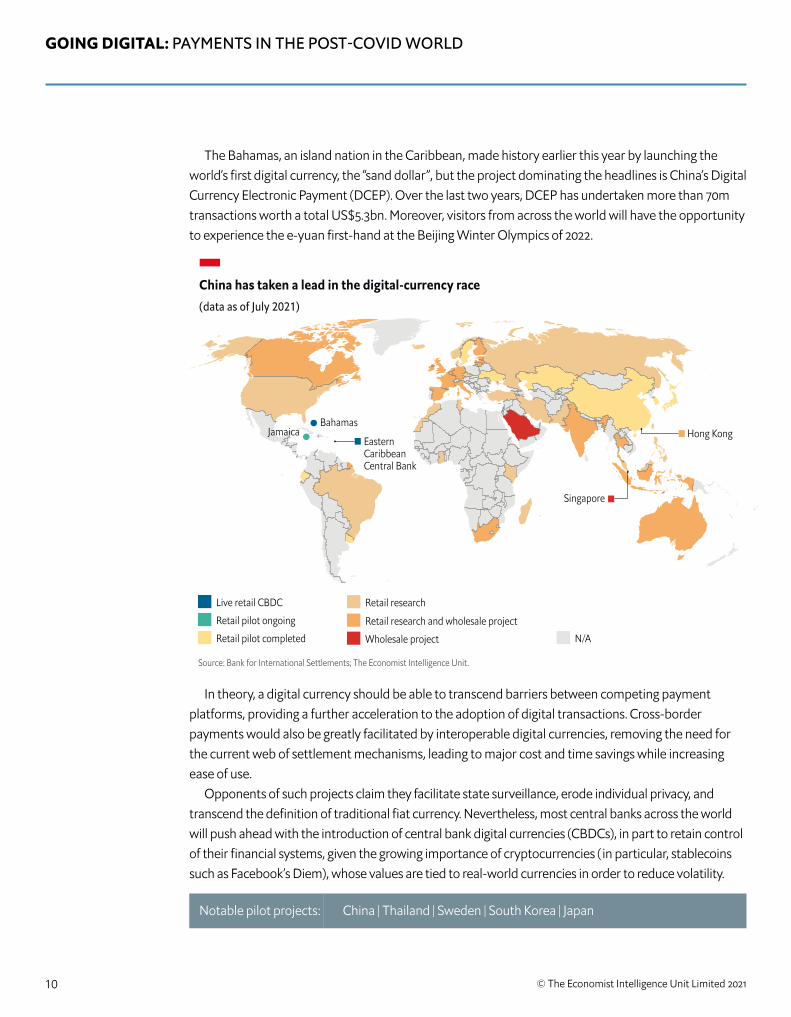

The Bahamas, an island nation in the Caribbean, made history earlier this year by launching the world’s first digital currency, the “sand dollar”, but the project dominating the headlines is China’s Digital Currency Electronic Payment (DCEP). Over the last two years, DCEP has undertaken more than 70m transactions worth a total US$5.3bn. Moreover, visitors from across the world will have the opportunity to experience the e-yuan first-hand at the Beijing Winter Olympics of 2022.

In theory, a digital currency should be able to transcend barriers between competing payment platforms, providing a further acceleration to the adoption of digital transactions. Cross-border payments would also be greatly facilitated by interoperable digital currencies, removing the need for the current web of settlement mechanisms, leading to major cost and time savings while increasing ease of use.

Opponents of such projects claim they facilitate state surveillance, erode individual privacy, and transcend the definition of traditional fiat currency. Nevertheless, most central banks across the world will push ahead with the introduction of central bank digital currencies (CBDCs), in part to retain control of their financial systems, given the growing importance of cryptocurrencies (in particular, stablecoins such as Facebook’s Diem), whose values are tied to real-world currencies in order to reduce volatility.

China has taken a lead in the digital-currency race

Source: Bank for International Settlements; The Economist Intelligence Unit.

Live retail CBDC

Retail pilot ongoing

Retail pilot completed

Retail research

Retail research and wholesale project

Wholesale project N/A

Hong Kong

Singapore

Bahamas

(data as of July 2021)

JamaicaEastern Caribbean Central Bank

Notable pilot projects: China | Thailand | Sweden | South Korea | Japan

GOING DIGITAL: PAYMENTS IN THE POST-COVID WORLD

© The Economist Intelligence Unit Limited 202111

Transform or perishDespite the enthusiasm around emerging modes of payment, numerous sources of apprehension remain unaddressed. These include concerns around data security, financial fraud, cybersecurity and the role of regulators, many of whom are behind the curve when it comes to technological advancement. The absence of common regulatory standards among geographically contiguous countries, potentially leading to the creation of regional monopolies, is a related concern.

Regulators must work towards the standardisation of technology such as quick-response (QR) codes, while also building universally accessible payments infrastructure, such as India’s Unified Payments Interface (UPI) or Brazil’s Pagamento Instantâneo Brasileiro (Pix). These allow for the participation of private firms, providing an additional fillip to the digital economy. Equally crucial, however, will be the ability of regulators to monitor payments platforms to stem any bad-debt or other solvency issues that emerge from buy now pay later (BNPL) companies or speculative trading involving decentralised digital currencies, such as Bitcoin.

Meanwhile, traditional companies, such as bricks-and-mortar banks, run the risk of being over-run by their digital counterparts and payment-platform providers, despite their own significant investments in technology. Many have been unable to create the culture of innovation that is the hallmark of the digital player, although some have hived off digital businesses or turned to acquisitions to remain relevant in an increasingly digitalised world.

The benefits of digital payment systems significantly outweigh the risks associated with them, however. For governments, they provide an avenue to raise financial inclusion and further the cause of economic development. Individuals, especially those in developing countries, can more effectively participate in economic activity. Private organisations will benefit from the new opportunities created as a result.

© The Economist Intelligence Unit Limited 202112

EIU Viewpoint We monitor the world to prepare you for what’s ahead

Understand a country’s political, policy and economic outlook with the world’s best forward-looking analysis and data. Our award-winning expertise looks at global dynamics that impact your organisation, helping you to operate effectively and plan for the future. Included in our service:

• Global and regional outlook spanning politics, economics and market-moving topics

• Daily insights on the developments that impact the future outlook

• Executive summaries of country forecasts over the medium-term outlook

• Medium-term country forecasts on ~200 countries’ political and economic landscape

• Long-term country forecasts on the structural trends shaping ~80 major economies

• Industry analysis on the outlook for 26 sectors in ~70 markets

• Commodity forecasts on supply, demand and prices of 25 critical goods

• Macroeconomic data on forecasts, as well as historic trends

• Industry data on demand and supply of key goods, now and in the future

• Proprietary ratings on the business environment

• Thematic analysis of the cross-cutting issues that our experts expect to shape the global outlook

How EIU Viewpoint helps you to stay ahead

Unparalleled coverage - global, regional and country-level analysis for nearly 200 markets. 20,000 data series every month, led by our worldwide network of expert analysts and on the ground contributors

360-degree view - our approach is unique; deliberately designed to intersect politics, policy and the economy, our methodology leads to a more nuanced perspective than simple number crunching

Beating consensus - with over 70 years of experience, we have a track record of making bold calls and getting them right

Evidence-based insights - our editorial team is fiercely independent and rightly so. This ensures you can trust our analysis and apply the insights it offers with confidence.

Find out more information about our service features, delivery platforms and how EIU Viewpoint could benefit your organisation by visiting:

eiu.com/viewpoint

Cover image - © Panuwatccn/Shutterstock

Copyright

© 2021 The Economist Intelligence Unit Limited. All rights reserved. Neither this publication nor any part of it may be reproduced, stored in a retrieval system, or transmitted in any form or by any means, electronic, mechanical, photocopying, recording or otherwise, without the prior permission of The Economist Intelligence Unit Limited.

While every effort has been taken to verify the accuracy of this information, The Economist Intelligence Unit Ltd. cannot accept any responsibility or liability for reliance by any person on this report or any of the information, opinions or conclusions set out in this report.