Globalisation and Changing Corporate Form

40

1 Globalisation and Changing Corporate Form Gianmarco I.P. Ottaviano London School of Economics, U Bologna and CEPR The Third CEPR-Modena Conference on Growth in Mature Economies: Revisiting the Contribution of Openness 11-12 May 2015

Transcript of Globalisation and Changing Corporate Form

1

Globalisation and Changing Corporate Form

Gianmarco I.P. Ottaviano London School of Economics, U Bologna and CEPR

The Third CEPR-Modena Conference on Growth in Mature Economies:Revisiting the Contribution of Openness

11-12 May 2015

2

‘Alien Invasion’: GVCs and BGs Global Value Chains (GVCs):

Networks of supply Input-output relations

Global Business Groups (GBGs): Networks of control Ownership relations

They are the ‘brains’ (GBGs) and ‘brawn’ (GVCs) of globalization

Yet, our understanding of their parallel and joint contributions to growth is still rather limited

For example, control chains are often unrelated to supply chains: Why?

3

Global Value Chains (GVCs) Background:

Emergence of GVCs Vertically and geographically fragmented

production Trade in intermediate goods and tasks

UNCTAD (2013): Intra- and inter-firm GVCs of multinational

enterprises account for 80% of global trade GVCs are responsible for significant double-

counting in global trade figures GVCs make extensive use of both market and

internal services (~ BGs)

4

CompNet and GVCs Gross flows of goods and services crossing

borders back and forth are hardly informative of value added (VA), factor income and factor content generated in a country

Direct impact on the assessment of the country’s ‘competitiveness’ (i.e. ability to generate VA, income, employment, ultimately welfare for its citizens)

Competitiveness Research Network (CompNet): all ESCB central banks plus international organisations interested in competitiveness issues

CompNet Interim Report (2013)

5

CompNet and GVCs CompNet: comprehensive set of indicators to

assess integration of countries into GVCs and the implications for country performance

Research questions: What is the evidence on the importance of GVCs

in the euro area? Which firms take part in GVCs? Which countries are net gainers/losers from

participating in GVCs? What are the effects of GVCs on the

interdependencies between economies and external imbalances?

6

CompNet: Europe and GVCs Identification and measurement of GVCs are

crucial for policy assessment, especially for highly integrated EU countries

Still much work to be done in: Disentangling VA in trade flows Measuring countries’ involvement in vertically

fragmented production Assessing countries’ position within value chains

7

CompNet: Europe and GVCs The main statistical tool used in analysing GVCs

consists in global input-output tables But additional micro-level evidence needed as

strong assumptions are required for the construction of global input-output tables

CompNet uses data provided by the OECD-WTO initiative Trade in Value-Added (TiVA) and by the EU project World Input-Output Database (WIOD)

8

CompNet: Disentangling Value Added Given high and growing import content of

exports, traditional trade statistics that record gross flows of goods and services each time they cross borders are increasingly uninformative of the actual VA generated in a country

For instance, in gross terms the main export partner of Germany is France, and for Italy and France it is Germany

However, in value added terms (according to OECD data) for all three major euro countries, the main export partner is the United States

9

CompNet: Disentangling Value Added Based on the WIOD, Amador, Cappariello and

Stehrer (2013) report on euro area countries in 2000-2011: In 2011 foreign VA content of exports (reflecting

foreign inputs in the production of exports) averaged about 32%, with smaller countries generally exhibiting higher values

Some evidence of pro-cyclical pattern Evidence of growing engagement in GVCs for the

majority of the euro area countries, which regained momentum after the trade collapse of 2009

Imported VA share in exports of goods is higher than in exports of services, making the latter more important in VA terms

10

Foreign VA in Euro Area Exports

Source: CompNet Interim Report (2013)

averagein 2011

11

CompNet: Measuring Countries Involvement Import content of exports traditionally taken as

measure of countries’ involvement in GVCs This emphasizes foreign upstream suppliers but

countries also supply inputs to foreign downstream customers

Koopmans, Powers, Wang and Wei (2011) stress two dimensions: Use of foreign inputs for own exports (Foreign VA) Supply of intermediates for other countries’

exports (re-exported Domestic VA) European countries appear to be highly and

increasingly integrated into GVCs

12

CompNet: Decomposition of VA

Source: CompNet Interim Report (2013)

13

GVC Participation of Euro Countries

upstreamaveragein 2011

14

CompNet: Assessing countries’ position ‘Upstream countries’ specialise in the production

of raw materials or intangibles necessary at the beginning of the value chain (e.g. research and design)

‘Downstream countries’ specialise in the assembly of final products or customer services

De Backer and Miroudot (2013) compute ‘upstreamness’ as ‘distance to final demand’: number of production stages (plants) a product goes through before reaching final demand

15

CompNet: Assessing countries’ position Between 1995 and 2008:

Most euro countries managed to move upstream Only a few countries in Europe moved

downstream (Poland, Portugal, Romania, Slovakia and Slovenia)

General trend consistent with the overall increase in the length of GVCs and the emergence of outsourcing as outsourcing inherently increases the distance to final demand

More research needed to assess the pros and cons of ‘upstreamness’ for countries

16

CompNet: Assessing countries’ position

Source: CompNet Interim Report (2013)

17

ETLA: Who Captures Value in GVCs? Multinational companies vs. national

governments: Companies look at own global ability to capture

profits (only a component of total value added) at the corporate level: otherwise largely indifferent to the geographical distribution of value added

Governments look at the sum of value added captured within national borders (GDP): otherwise largely indifferent to the organizational distribution of value added

Increasingly divergent interests

18

ETLA: Who Captures Value in GVCs? TiVA and WIOD still fall short of describing how

GVCs operate in practice and how their economic gains are distributed across countries

A recent report by ETLA (Ali-Yrkkö and Rouvinen, 2013) builds on 40 detailed case studies of individual products/services by firms residing in Finland to analyze those issues in finer detail

For instance: Impacts of re-locating assembly processes Consequences of multinational corporations’

internal transfer pricing practices

19

ETLA: Value Capture in a Smartphone Snapshot: Nokia N95 (2007) Unbundled pre-tax retail price (VA): €546 VA by 600 components, software and

intellectual property VA by actors, functions, and geographies Depending on the input, 1-8 stages before the

final assembly by Nokia and 2-4 stages after it Assembly in two locations: Beijing (China) and

Salo (Finland) Countries of final sale (VA of distribution

arises in the country of final sale)

20

ETLA: Value Capture in a SmartphoneA stylized supply chain of the Nokia N95

Source: Ali-Yrkkö, Rouvinen, Seppälä and Ylä-Anttila (2011)

21

ETLA: Where Assembled Does (Not) MatterVA captured in Finland for Nokia N95: Beijing vs. Salo

Source: Ali-Yrkkö, Rouvinen, Seppälä and Ylä-Anttila (2011)

22

ETLA: Value Capture in 3 Dumbphones Over time (last dumbphone: same year as Nokia

N95 smartphone): Nokia 3310 (2000, VA €78.60) Nokia 1100 (2003; VA €62.70) Nokia 1200 (2007, VA €27.00)

Analysis of these three similar phones over time shows: Rapid decline in price of a given feature set Gradual shift of tasks towards developing countries Shift concerns physical components and assembly as

well as design and other intangible aspects of the GVC

23

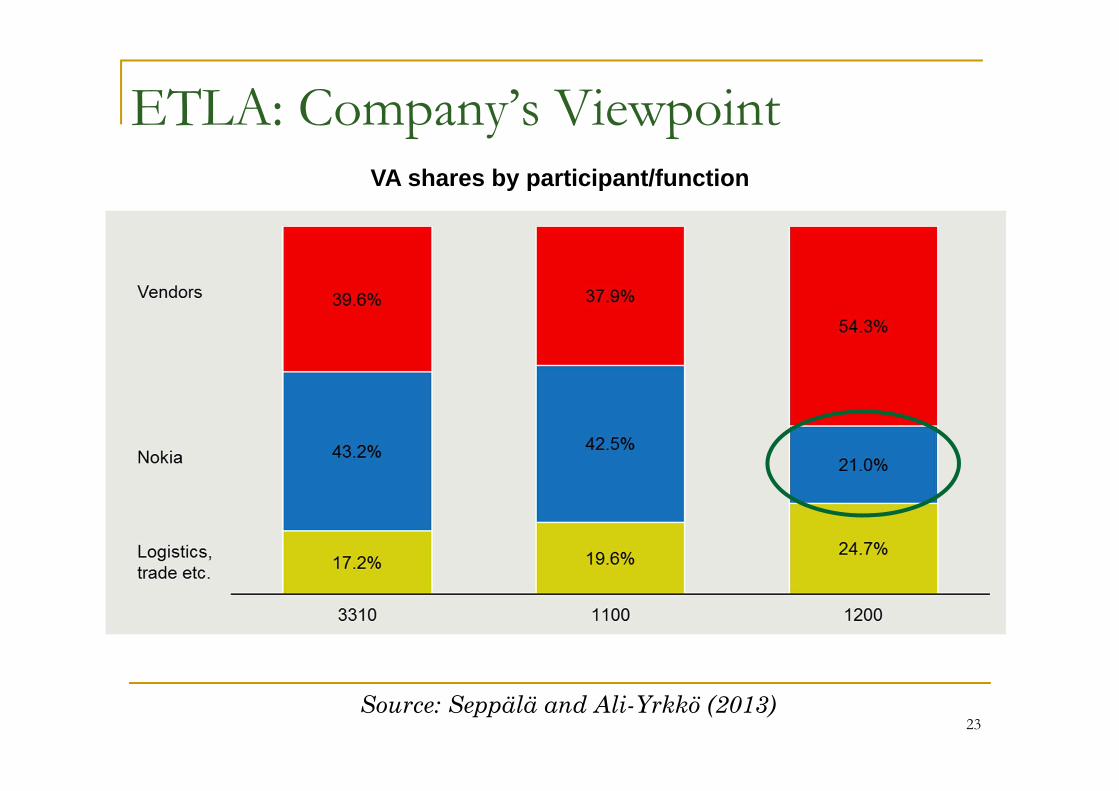

ETLA: Company’s ViewpointVA shares by participant/function

Source: Seppälä and Ali-Yrkkö (2013)

24

ETLA: Government’s ViewpointThe geography of VA

Source: Seppälä and Ali-Yrkkö (2013)

25

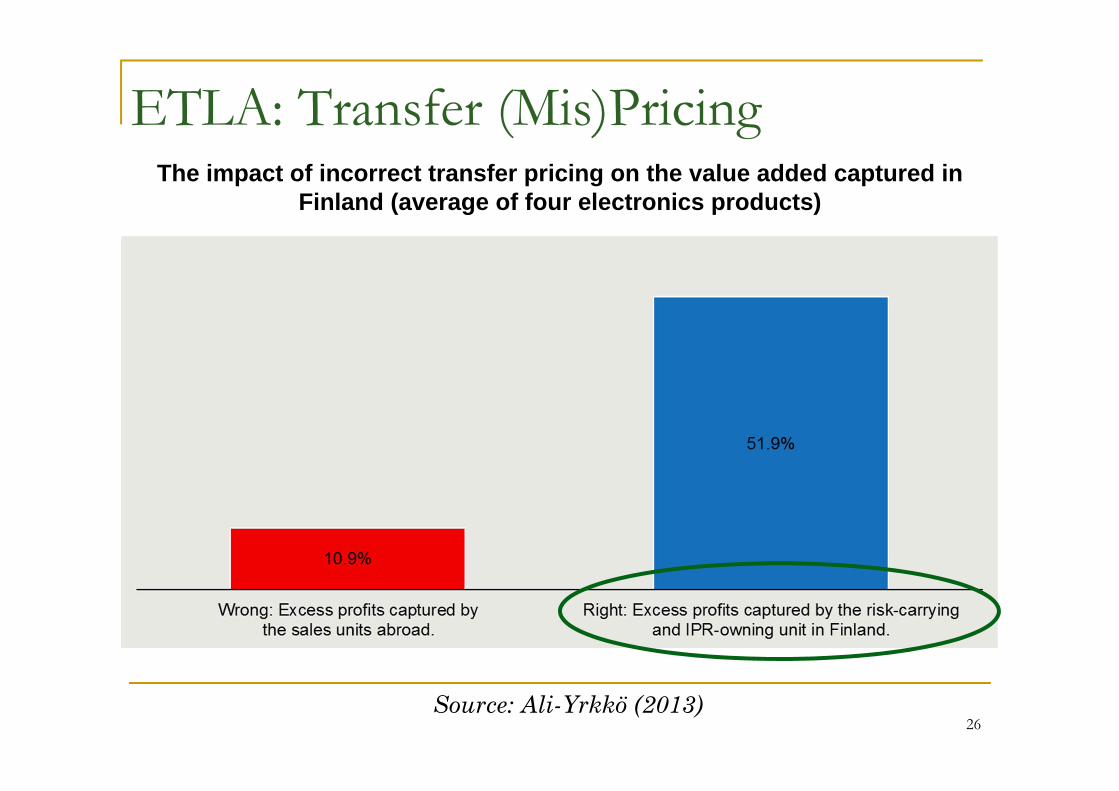

ETLA: Company vs. Government Four electronics products by the same company:

Transfer pricing When parent company carries most of the risks and

owns all relevant intellectual property, it should capture any ‘excess profits’ (OECD, 2010)

According to this principle, the price that the parent company charged its sales subsidiaries was too low

Using more appropriate transfer prices increases the VA share of the home country by 42-66% depending on the product

This has direct consequences on measured GDP It also increases the exports of the home country and

the imports of the countries where the sales units are located

26

ETLA: Transfer (Mis)PricingThe impact of incorrect transfer pricing on the value added captured in

Finland (average of four electronics products)

Source: Ali-Yrkkö (2013)

27

ETLA: Value Creation and Capture

Source: Pajarinen, Rouvinen and Ylä-Anttila (2012)

‘Smile Curve’: VA per hour in different stages of GVC

28

Summary on GVCs GVCs raise positive and normative issues for mature

economies: Involvement Positioning Value capture

Normative issues: companies’ and governments’ viewpoints do not coincide: GVCs are an inescapable opportunity for companies GVCs can be an elusive challenge for governments Corporate boundaries vs. national boundaries

Positive issues: Measurement still caught between I-O tables and case

studies: Need for large disaggregated datasets (~ next slides 29 and 30)

Conceptual framework still very unbalanced between ‘brains’ and ‘brawn’ (~ subsequent slides on GBGs)

29

Trade Networks at Firm Level by Categories of Goods: Costa Rica and Japan

Source: Carballo, Ottaviano and Volpe Martinkus (2013)

Differentiated goods Homogeneous goods

30

Trade Networks at Firm Level by Categories of Goods: Costa Rica and US

Source: Carballo, Ottaviano and Volpe Martinkus (2013)

Differentiated goods Homogeneous goods

31

Global Business Groups (GBGs) By now GVCs are ‘familiar aliens’ GBGs instead remain ‘unfamiliar aliens’:

A commonly accepted definition of `business group' (BG) does not exist in the economic or business literature (Altomonte and Rungi, 2013)

“The economics literature has not had much to say about non-standard organizational forms [...] now much discussed in the business and organizational literatures, including joint ventures, strategic alliances, networks, business groups, clans, and virtual organizations” (Baker, Gibbons and Murphy, 2002)

Among these non-standard organizational forms business groups (BGs) stand out as essentially lacking any ‘economic theory’

32

What is a Business Group? The lowest common denominator of alternative

views defines BGs as hybrid organizations of economic activities, halfway between markets and hierarchies, that: Exchange intermediate goods and services on the

market, but possibly through a transfer price Relocate financial resources across affiliates, but

at more favourable conditions if confronted with external financing (`internal capital market')

Coordinate management decisions through majority stakes in controlled assets, but have to consider as well minority shareholders’ protection

33

What is a Business Group? (Cont.)

More generally, BGs exhibit a flexible form of asset ownership that: Provides incentives to self-enforce promises of

cooperation among affiliates, given the control exerted by a common parent

But enjoys the freedom of organizing activities within a market-like environment, as each affiliate maintains formal property rights on its production assets

34

A Working Definition of BG Define a BG as:

A set of at least two legally autonomous firms Whose economic activity is coordinated through

some form of hierarchical control via equity stakes Legal autonomy and hierarchy jointly characterize

BGs, distinguishing them from: ‘Independent firms’, as these are legally

autonomous but operate without impending hierarchies

‘Multidivisional firms’, as these are organized in a hierarchy of branches without autonomous legal status

35

The Pervasiveness of BGs

According to this definition, BGs are ubiquitous and impactful (Altomonte and Rungi, 2013): Most of the Fortune 500 companies, the top 2,000

R&D firms listed by the Industrial R&D Investment Scoreboard (IRI, 2011), as well as the top 100 largest MNEs listed by UNCTAD (2011) can be included under the category of domestic or cross-border BGs

At least 75% (65%) of total US (French) trade can be linked to firms organized as multinational BG

36

Why Do Business Groups Exist?

Why BGs organize a number of formally independent firms under a common hierarchy?

In finance BGs are typically explained in terms of some kind of ‘institutional arbitrage’ (e.g. chain control, tax arbitrage, ‘tunnelling’) or ‘portfolio management’ (e.g. risk sharing)

However, it is hard to think of ‘institutional arbitrage’ and ‘portfolio management’ as the main explanations of the pervasiveness of BGs also within countries

Indeed, any fundamental explanation of the existence of BGs should not rely on cross-country asymmetries

37

Why Do Business Groups Exist? (Cont.) In economics models of BGs are virtually absent Theories of the (boundaries of the) firm generally

focus on the ‘vertical integration decision’ as a binary choice about sourcing intermediate inputs from within the firm or not (Helpman, 2006)

Some times the ‘relaxed problem’ allowing for non-binary outcomes is used as a technical trick to characterize the binary decision (Antras and Chor, 2013; Alfaro, Antras, Chor and Conconi, 2015) but its not understood as a possible way of modelling BGs

Moreover, in these theories control chains are always related (actually embedded) in supply chains

38

Why Do Business Groups Exist? (Cont.)

Alternatively the firm has been modelled as a ‘knowledge-based hierarchy’ (Garicano, 2000; Garicano and Rossi-Hansberg, 2012)

Here the organizational structure depends on the costs of acquiring and communicating knowledge among agents involved with different tasks (‘organization decision’)

Idea: In certain cases BGs are the most efficient means to create and transmit knowledge between linked activities (Altomonte, Garicano, Ottaviano and Rungi, in progress)

39

Where We Stand

Input-output relations drive VCs; knowledge creation and transmission drive BGs

Knowledge flows do not necessarily follow Intermediate inputs flows and vice versa

National borders interfere with these flows but cannot explain the pervasiveness of BGs

It is knowledge creation and transmission within BGs that determines growth in the long run

It is ‘brains’ over ‘brawn’ … but our models are mostly ‘brainless’!