Uluslararası İtibar Yönetimi Konferansı 2012-Gençlerin Gözüyle Etik- Bülent Şenver

Global Trends in Digital Banking – How to win? Bogazici University Banking Lecture

October, 2014

Global-Trends-Digital-Banking-BU Banking Lecture-19Sep14_v2.pptx 1

Draft—for discussion only

Co

pyrig

ht ©

2014 b

y T

he

Bo

sto

n C

on

su

ltin

g G

rou

p,

Inc.

All

rig

hts

re

se

rve

d.

Key messages

Digital channels within banks have grown continuously and significantly – outpacing all

other channels and changing the traditional sources of competitive advantage for banks

Banks around the world have experimented with different Digital service models since the

late 90's – but no clear winning model with a broad product offering has emerged

However, as Digital continues to grow and evolve, recent observations indicate that broader

offering Digital banks are showing promising signs of future success

As Traditional Banks move to capitalize on Digital trend, it's critical to align on specific

strategic vision and objectives, core value proposition and operating model before acting

Global-Trends-Digital-Banking-BU Banking Lecture-19Sep14_v2.pptx 2

Draft—for discussion only

Co

pyrig

ht ©

2014 b

y T

he

Bo

sto

n C

on

su

ltin

g G

rou

p,

Inc.

All

rig

hts

re

se

rve

d.

Agenda

Share perspectives on the Digital banking landscape

Review a Digital banking case study

Global-Trends-Digital-Banking-BU Banking Lecture-19Sep14_v2.pptx 3

Draft—for discussion only

Co

pyrig

ht ©

2014 b

y T

he

Bo

sto

n C

on

su

ltin

g G

rou

p,

Inc.

All

rig

hts

re

se

rve

d.

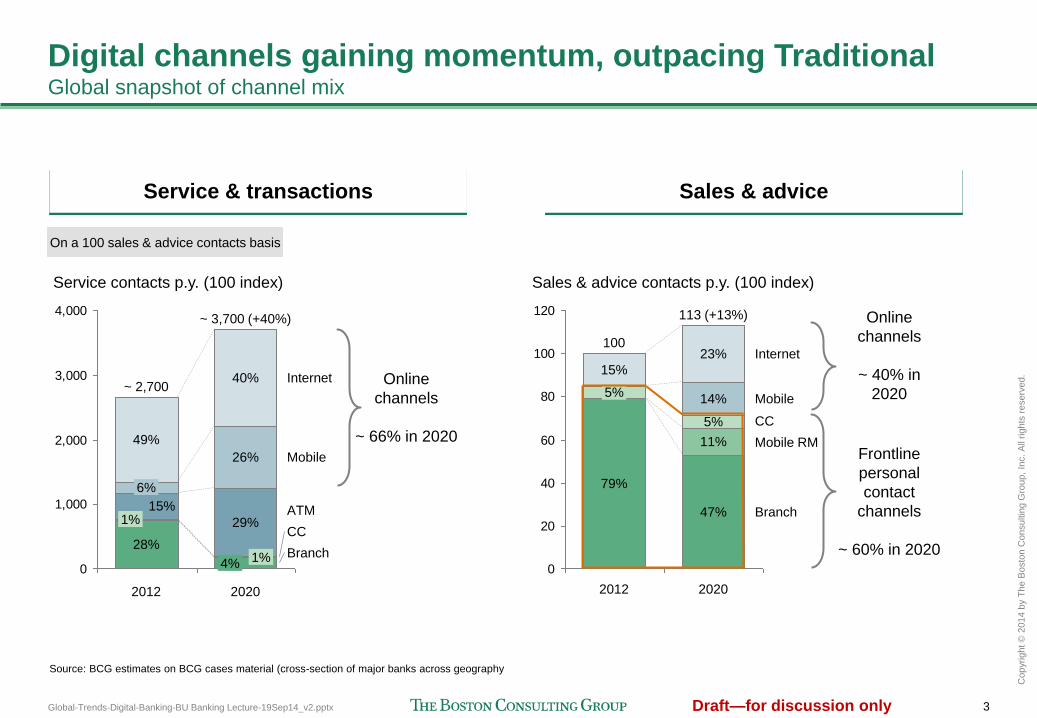

Digital channels gaining momentum, outpacing Traditional Global snapshot of channel mix

Source: BCG estimates on BCG cases material (cross-section of major banks across geography

Service & transactions Sales & advice

0

1,000

2,000

3,000

4,000

Service contacts p.y. (100 index)

Branch

CC

ATM

2020

~ 3,700 (+40%)

4% 1%

29%

26%

40%

2012

~ 2,700

28%

1% 15%

6%

49%

Mobile

Internet Online

channels

~ 66% in 2020

On a 100 sales & advice contacts basis

0

20

40

60

80

100

120

Sales & advice contacts p.y. (100 index)

Branch

Mobile RM

CC

Mobile

Internet

2020

113 (+13%)

47%

11%

5%

14%

23%

2012

100

79%

5%

15%

Frontline

personal

contact

channels

~ 60% in 2020

Online

channels

~ 40% in

2020

Global-Trends-Digital-Banking-BU Banking Lecture-19Sep14_v2.pptx 4

Draft—for discussion only

Co

pyrig

ht ©

20

14

by T

he

Bo

sto

n C

on

su

ltin

g G

rou

p,

Inc.

All

rig

hts

re

se

rve

d.

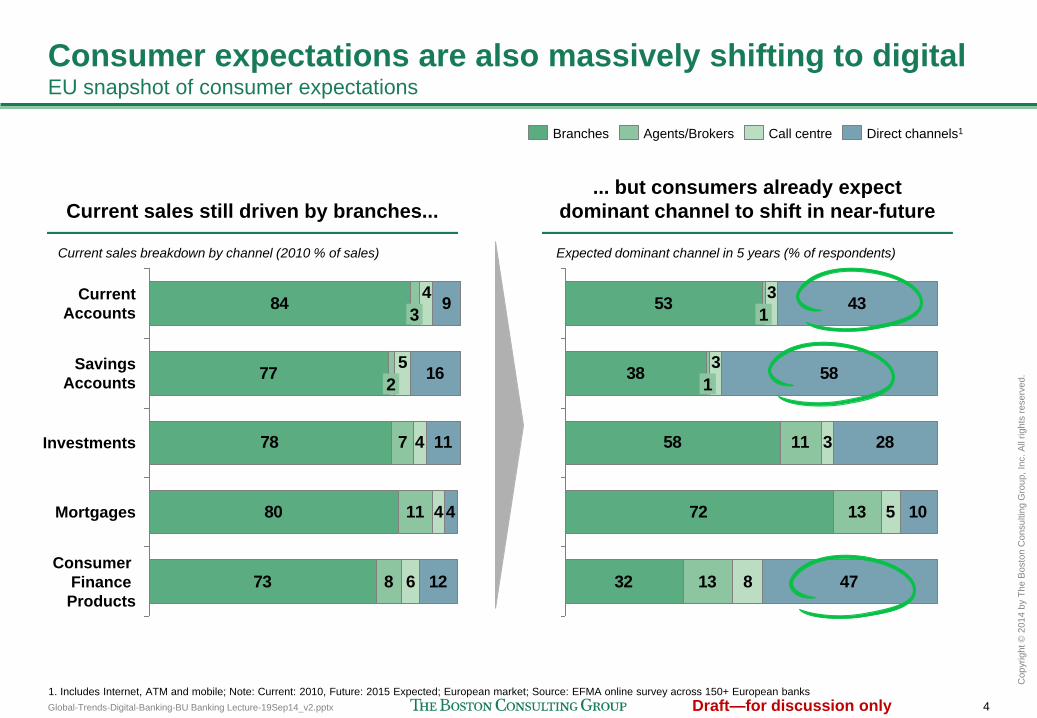

Consumer expectations are also massively shifting to digital EU snapshot of consumer expectations

1. Includes Internet, ATM and mobile; Note: Current: 2010, Future: 2015 Expected; European market; Source: EFMA online survey across 150+ European banks

77

78

80

73

7

11

8

4

4

6

9

16

11

4

12

84

5

4

Mortgages

Investments

Savings

Accounts 2

Current

Accounts 3

Consumer

Finance

Products

38

58

72

32

11

13

13

3

5

8

43

58

28

10

47

53

3

3

1

1

Direct channels1 Call centre Agents/Brokers Branches

Current sales still driven by branches...

... but consumers already expect

dominant channel to shift in near-future

Current sales breakdown by channel (2010 % of sales) Expected dominant channel in 5 years (% of respondents)

Global-Trends-Digital-Banking-BU Banking Lecture-19Sep14_v2.pptx 5

Draft—for discussion only

Co

pyrig

ht ©

20

14

by T

he

Bo

sto

n C

on

su

ltin

g G

rou

p,

Inc.

All

rig

hts

re

se

rve

d.

Many 'myths' to dispel about Digital Banking

Reality #3: New players, until now, typically focus on non-traditional products, with opportunities for banks to participate (and expand their offerings)

Reality #6: The challenge is to ensure customer data is consistent, coherent, and at the frontlines to drive more productive conversations

Reality #5: Products portfolio need to be aligned across the bank to avoid cannibalization. Also, complex traditional products online may result in a poor customer experience

Reality #2: There are natural cross-channel customer journeys which should be enabled. Attempts to enable all possible cross-channel journeys drives complexity and cost

Reality #1: The need for branch-based advisory services will continue to remain important. Digital frees up branch staff to focus on advisory sales

Myth #1: The Branch is dead

Myth #5: All traditional products

need to be available online

Myth #2: Customers want an

omni-channel experience

Myth #3: Traditional banks

attacked by new digital players

Myth #4: Banks must become like

Facebook or perish

Myth #6: Digital banking requires

Big Data

Reality #4: Most social media initiatives have disappointed. Banks must harness the power of social media to drive customer reviews and build customer advocacy

Digital banking Myths Digital Banking realities

Global-Trends-Digital-Banking-BU Banking Lecture-19Sep14_v2.pptx 6

Draft—for discussion only

Co

pyrig

ht ©

20

14

by T

he

Bo

sto

n C

on

su

ltin

g G

rou

p,

Inc.

All

rig

hts

re

se

rve

d.

To date, three waves of digital banking trends Successful direct models have been "surgical"– focused on narrow offerings and segments

Product specialist

1

"Universal"

Digital Bank

2

Customer segment

specialist

3

1995 2000 2005 2010 2014

?

?

Too early

to assess

Pure niche player 4

1990s: Universal bank 2000s: Specialists Current: New wave

?

?

Too early

to assess

Global-Trends-Digital-Banking-BU Banking Lecture-19Sep14_v2.pptx 10

Draft—for discussion only

Co

pyrig

ht ©

20

14

by T

he

Bo

sto

n C

on

su

ltin

g G

rou

p,

Inc.

All

rig

hts

re

se

rve

d.

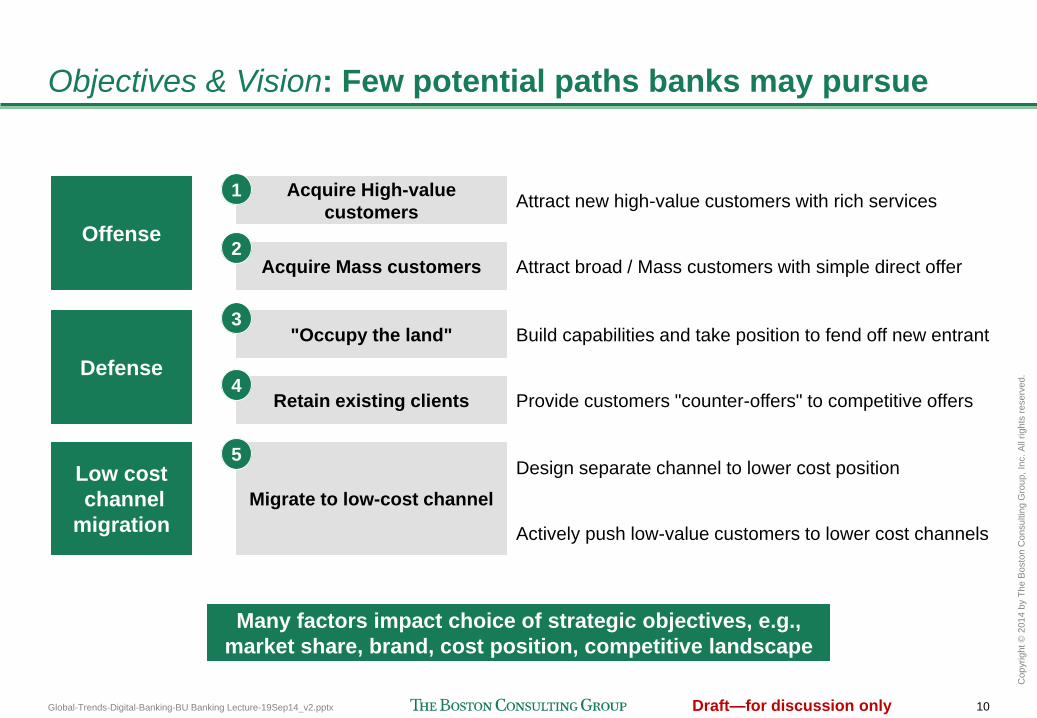

Objectives & Vision: Few potential paths banks may pursue

Offense

Defense

Low cost

channel

migration

Attract new high-value customers with rich services Acquire High-value

customers

Acquire Mass customers

"Occupy the land"

Retain existing clients

Migrate to low-cost channel

1

2

3

4

5

Attract broad / Mass customers with simple direct offer

Build capabilities and take position to fend off new entrant

Provide customers "counter-offers" to competitive offers

Design separate channel to lower cost position

Actively push low-value customers to lower cost channels

Many factors impact choice of strategic objectives, e.g.,

market share, brand, cost position, competitive landscape

Global-Trends-Digital-Banking-BU Banking Lecture-19Sep14_v2.pptx 11

Draft—for discussion only

Co

pyrig

ht ©

2014 b

y T

he

Bo

sto

n C

on

su

ltin

g G

rou

p,

Inc.

All

rig

hts

re

se

rve

d.

Agenda

Share perspectives on the Digital banking landscape

Review a Digital banking case study

Global-Trends-Digital-Banking-BU Banking Lecture-19Sep14_v2.pptx 12

Draft—for discussion only

Co

pyrig

ht ©

20

14

by T

he

Bo

sto

n C

on

su

ltin

g G

rou

p,

Inc.

All

rig

hts

re

se

rve

d.

Case study: mBank is the biggest Polish online bank

and part of third largest Polish bank, BRE Bank

• The third Polish banking group with

comprehensive financial offer tailored to the needs

of corporate clients, Private Banking clients, and

retail clients

• Member of Commerzbank Group

• ~6,000 employees

• BRE Retail banking (mBank, MultiBank, mBank

Czech Rep. & Slovakia) serves total 4.1 million

customers

• First Polish pure-play online bank founded in 2000

• Currently #3 retail bank and the biggest online bank

• Full retail and SME product range available behind

single login

• Launched in Czech Republic and Slovakia in 2007

• $10.2 billion deposits & $11.4 billion loans at the end of

2012

Business results [2012 EOY, USD in million] Results by country (2012 EOY, USD in million)

0

20,000

10,000 10,514

Deposits Loans

11,573

400

200

0

374

Net Income

Source: BRE Bank Investor Relations, Bankier.pl

• 3.5 Mn customers

• $8,800 Mn deposits

• $10,900 Mn loans

• 0.17 Mn customers

• $439 Mn deposits

• $88 Mn loans

• 0.44 Mn customers

• $923 Mn deposits

• $458 Mn loans

Global-Trends-Digital-Banking-BU Banking Lecture-19Sep14_v2.pptx 13

Draft—for discussion only

Co

pyrig

ht ©

20

14

by T

he

Bo

sto

n C

on

su

ltin

g G

rou

p,

Inc.

All

rig

hts

re

se

rve

d.

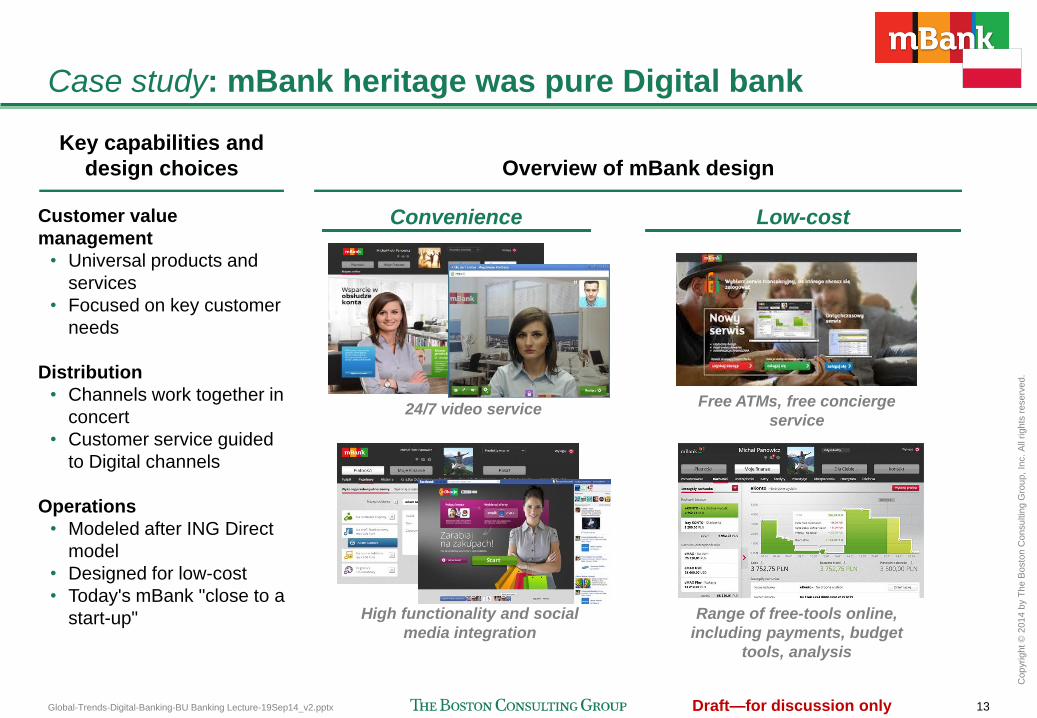

Case study: mBank heritage was pure Digital bank

Key capabilities and

design choices Overview of mBank design

Customer value

management

• Universal products and

services

• Focused on key customer

needs

Distribution

• Channels work together in

concert

• Customer service guided

to Digital channels

Operations

• Modeled after ING Direct

model

• Designed for low-cost

• Today's mBank "close to a

start-up"

Convenience Low-cost

Free ATMs, free concierge

service

Range of free-tools online,

including payments, budget

tools, analysis

24/7 video service

High functionality and social

media integration

Global-Trends-Digital-Banking-BU Banking Lecture-19Sep14_v2.pptx 14

Draft—for discussion only

Co

pyrig

ht ©

20

14

by T

he

Bo

sto

n C

on

su

ltin

g G

rou

p,

Inc.

All

rig

hts

re

se

rve

d.

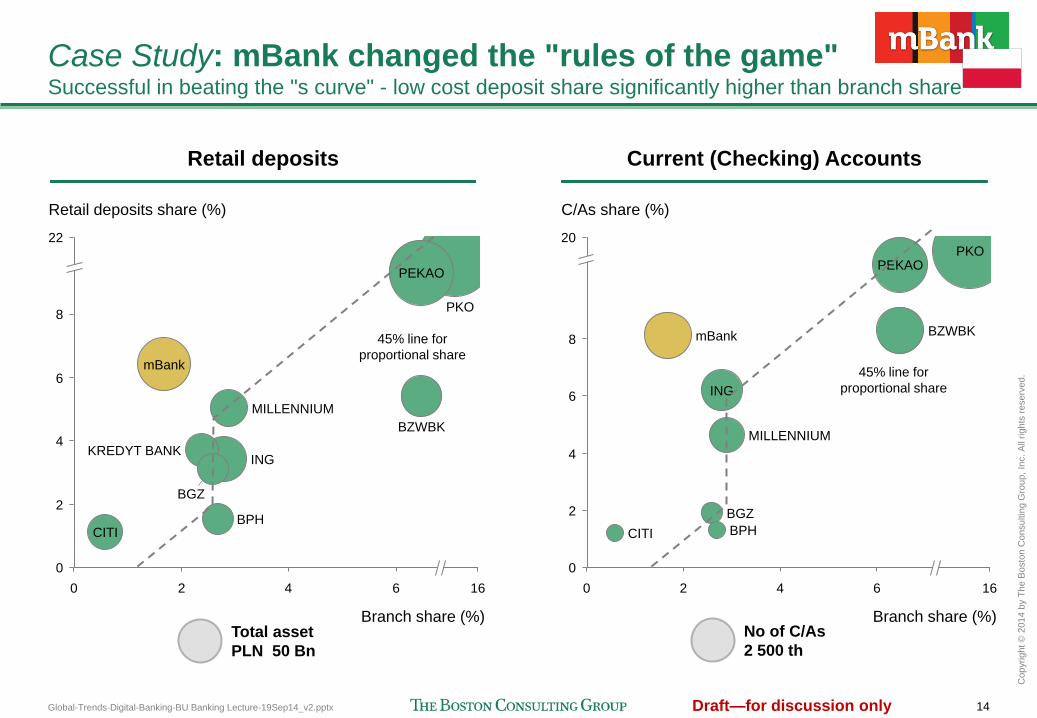

Case Study: mBank changed the "rules of the game" Successful in beating the "s curve" - low cost deposit share significantly higher than branch share

Retail deposits Current (Checking) Accounts

22

8

6

4

2

0

16 6 4 2 0

CITI BPH

BGZ

KREDYT BANK

MILLENNIUM

BZWBK

mBank

ING

Branch share (%)

PKO

Retail deposits share (%)

PEKAO

Total asset

PLN 50 Bn

20

8

6

4

2

2 0 4 6 16

0

C/As share (%)

CITI BPH

BGZ

MILLENNIUM

Branch share (%)

BZWBK mBank

ING

PEKAO PKO

No of C/As

2 500 th

45% line for

proportional share

45% line for

proportional share

Global-Trends-Digital-Banking-BU Banking Lecture-19Sep14_v2.pptx 15

Draft—for discussion only

Co

pyrig

ht ©

2014 b

y T

he

Bo

sto

n C

on

su

ltin

g G

rou

p,

Inc.

All

rig

hts

re

se

rve

d.

Case Study: mBank success based on few key factors

Well defined, attractive

target segment

Consistent, differentiated

positioning and marketing

Broad (like traditional bank)

offer & ALWAYS better deal

Best-in-class "feel & look"

transactional (core)

banking products

Key success factors Description

• Focused in segment selection; did not try to pursue all segments

• ~20-35 years, students - High potential: modern, educated, open for novelty

• (Such) customers grow in professional life/ wealth – currently mBank with

probably the most attractive, mass affluent customer base

• Distancing from "traditional banks" (like Apple vs IBM)

• "Do not pay for "bricks" of traditional banks, get better offer"

• "Why to pay for no choice of investments – get all funds at no fees"

• By leveraging scale/ power on suppliers (funds, insurance), analytical

advantage (one-to-one pricing), process convenience (loans)

• Often beyond banking e.g. insurance, experimented MVNO, etc.

• Creates very high recommendation levels/ NPS

• Believe: Customer transact daily (getting loans occasionally) - this is how

they build satisfaction, advocacy and stickiness

• Transactions as great source of Information and Touch points allowing best

offer (e.g. preapprovals, discounts, real time/ relevant offer)

Thank you

bcg.com | bcgperspectives.com