Global Trade in the Americas › ...Increased global trade regulations and governmental scrutiny has...

37

Global Trade in the Americas Minimizing Cost & Maximizing Value 50 th Annual IABA Conference Ricardo Goncalves, Deloitte Michele E. McGuire, Deloitte Cecilia Montano Hernandez, Deloitte June 27, 2014 © 2014. For information, contact Deloitte Touche Tohmatsu Limited. 1

Transcript of Global Trade in the Americas › ...Increased global trade regulations and governmental scrutiny has...

Global Trade in the Americas Minimizing Cost & Maximizing Value 50th Annual IABA Conference

Ricardo Goncalves, Deloitte Michele E. McGuire, Deloitte Cecilia Montano Hernandez, Deloitte June 27, 2014

© 2014. For information, contact Deloitte Touche Tohmatsu Limited. 1

Ø Introduction

Ø Effectively Utilizing Free Trade Agreements to Minimize Costs

Ø Managing the Interaction Between Customs Value and Transfer Pricing in Related Party Imports

Ø Managing the Impact of Export Controls in the Americas

Ø Automating Global Trade to Increase Compliance and Decrease Costs

Ø Conclusion

Agenda

© 2014. For information, contact Deloitte Touche Tohmatsu Limited. 2

Introduction

3 © 2014. For information, contact Deloitte Touche Tohmatsu Limited.

Global Trade in the Americas Maximizing Benefits & Minimizing Costs

4 © 2014. For information, contact Deloitte Touche Tohmatsu Limited.

Increased global trade regulations and governmental scrutiny has led to increased costs to companies.

The effective use and management of free trade agreements (FTAs), customs valuation, export controls, and global trade automation can provide significant duty and cost-savings opportunities and minimize costs associated with non-compliance

Security (national security, supply chain security, public health and consumer product safety)

Economy (revenue generation through duty/fee collection, non trade barriers)

Social Responsibility (corporate responsibility, public relations concerns)

COST

Effectively Utilizing Free Trade Agreements to Minimize Costs

5 © 2014. For information, contact Deloitte Touche Tohmatsu Limited.

Main reasons for Using a FTA

6 Free Trade Agreements in America

Increase investment opportunities

Eliminate foreign trade barriers

Establish a dispute resolution plan

Establish preferential tariffs, for goods that qualify as originating in the region

Provide protection – Intellectual property

Promote conditions of fair competition

Growth of FTAs in the Americas The entry into force of the North American Free Trade Agreement (NAFTA) in 1994 spurred a rapid growth of free trade agreements (FTAs) within the Americas. In 1994 there were 9 FTAs within the Americas; today there are almost 90.

More than half of the current FTAs are bilateral agreements with countries located outside the Americas. The remaining FTAs are multilateral, many of which are interregional. Key intraregional FTAs include:

© 2014. For information, contact Deloitte Touche Tohmatsu Limited. 7

NAFTA Mexico – Central America

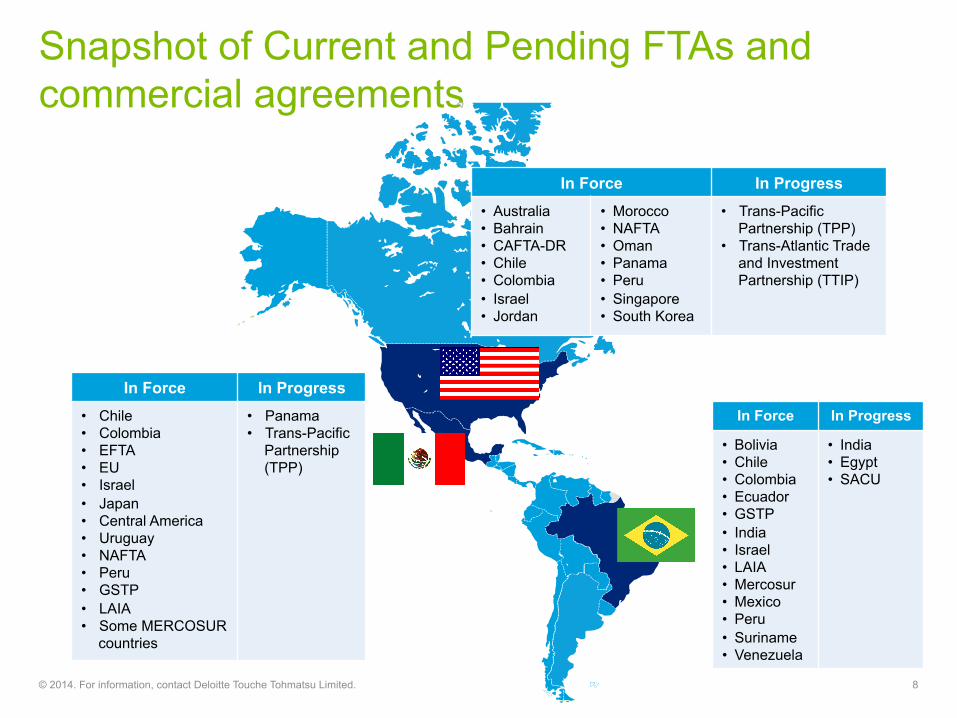

Snapshot of Current and Pending FTAs and commercial agreements

© 2014. For information, contact Deloitte Touche Tohmatsu Limited. 8

In Force In Progress • Chile • Colombia • EFTA • EU • Israel • Japan • Central America • Uruguay • NAFTA • Peru • GSTP • LAIA • Some MERCOSUR

countries

• Panama • Trans-Pacific

Partnership (TPP)

In Force In Progress • Australia • Bahrain • CAFTA-DR • Chile • Colombia • Israel • Jordan

• Morocco • NAFTA • Oman • Panama • Peru • Singapore • South Korea

• Trans-Pacific Partnership (TPP)

• Trans-Atlantic Trade and Investment Partnership (TTIP)

In Force In Progress

• Bolivia • Chile • Colombia • Ecuador • GSTP • India • Israel • LAIA • Mercosur • Mexico • Peru • Suriname • Venezuela

• India • Egypt • SACU

Trends in FTAs in the Americas

9 Free Trade Agreements in America

New generation FTAs are focusing on more than just tariff reduction

Focus is on more effective market access and reduction of non-tariff barriers

Considering new issues in preparation for multilateral negotiationsand agreements (investment, intellectual property,

public procurement, competition, sustainable development, cultural cooperation, etc.)

Overall challenge will be to enhance compatibility and coherence of regulatoryapproaches

for behind the border issues

Enhance transparency and consistency

Challenges of FTAs in the Americas

10 Free Trade Agreements in America

Market Access: Focus less on reduction of non-tariff barriers Automation

Needs: Cross-functional linkages across corporation

Product Tracking: Trace the country origin of raw materials and goods

Standard regulations: Reach consistency on FTA application

Growth of Free Trade Agreements

Over regulation: Increased regulatory

scrutiny and need for enhanced trade data management

Realizing the Benefits of Free Trade Agreements

Build FTAs and other trade preference programs into your sourcing/buying process:

• Conduct awareness training

• Integrate steps into existing processes (i.e., checklist, spreadsheet, trade department contact)

• Automate

• Make it easy

• Have a full view of your supply chain

• Seek refunds where possible

• Keep up with pending agreements and inform your sourcing teams

• Participate in Trade Associations and, where possible, trade negotiations

Taking Advantages of FTAs

Origin rules are highly complex, consequently every business should:

• Implement a strong cross functional procedures and control environment

• Track HTS and customs value changes and monitor effect on origin

• Confirm that focus and allocation of resources correspond to the impact/importance

• Allocate the overall responsibility in-house and ensure visibility and proper communication lines internally and externally

• Implement proper KPIs • Utilize Simplified Procedures where

available • Automate if cost effective • Be involved in all supply chain restructuring

Using FTAs

© 2014. For information, contact Deloitte Touche Tohmatsu Limited. 10

Managing the Interaction Between Customs Valuation and Transfer Pricing in Related Party Imports

12 © 2014. For information, contact Deloitte Touche Tohmatsu Limited.

The Tension Between Customs Valuation and Transfer Pricing

The different goals of income tax and customs authorities can create a “whip saw” effect on importers even though both authorities are interested in proving the arm’s length nature of a related party transaction.

© 2014. For information, contact Deloitte Touche Tohmatsu Limited. 12

Importers want to maximize the value of imported inventory for income tax withholding purposes

Value of imported inventory subject to income tax rules

Importers want to minimize the value of imports to lower

customs duty burden

Value of imports subject to customs authority valuation

requirements

TAX

CUSTOMS The value for transfer pricing purposes may often serve as an acceptable starting point for determining the import value, but is not the end point.

VALUE

VALUE

• The World Trade Organization (WTO) Agreement on Customs Valuation provides a hierarchy of six valuation methods, with the preferred method appraisement to be Transaction Value (“TV”), which is the “price paid or payable”.

• The transfer price may be used as the basis of transaction value provided local customs authorities’ “arm’s length” requirements are met.

• The WTO sets forth two tests the importer must meet in order to satisfy the “arm’s length” test and maintain the use of transaction value:

1) Circumstances of Sale 2) Test Values

• Each WTO country has its own interpretation and application of the arm’s length tests and, consequently, the evidence used to support transfer prices as transaction may vary from country to country. − The World Customs Organization (WCO) has established committees to allow

member countries to consult with each other and promote uniformity in the application of WTO valuation methods.

Acceptability of Transfer Prices as Customs Value

© 2014. For information, contact Deloitte Touche Tohmatsu Limited. 13

Customs Valuation Perspective Transfer Pricing Perspective

Definition of “related party”

• 5% or more ownership • Sufficient control (shared

board members, etc.)

50% or more ownership

Arm’s length test

Product-focused profitability analysis. Either: • Circumstances of Sale Test; or • Test Values

Customs value must be approached in accordance with the WTO valuation hierarchy

Function-focused profitability analysis. Best method of: • Comparable Uncontrolled Price

Method (CUP) • Resale Price Method (RPM) • Cost Plus (CP) • Comparable Profits Method

(CPM) / Transactional net Margin Method (TNMM)

• Profit Split

Basis Transaction by Transaction Aggregate for one to three years

Differences in Interpretation – OECD v. WTO Rules

15 © 2014. For information, contact Deloitte Touche Tohmatsu Limited.

Customs authorities’ “arm’s length” test differs from the arm’s length test applied by Tax authorities

• Many TP strategies allow for retroactive transfer price adjustments (either upward or downward).

• Adjusting the TP means the Transaction Value for the goods has changed, requiring adjustments to the customs value.

• Such TP adjustments may require adjustments to the previously declared customs value, depending rules of the country in question.

− Upward adjustments may result in additional duties and taxes owed (if required within the subject jurisdiction)

− Downward adjustments may result in a duty refund (if allowable within the subject jurisdiction)

Customs Treatment of Transfer Pricing Adjustments

© 2014. For information, contact Deloitte Touche Tohmatsu Limited. 15

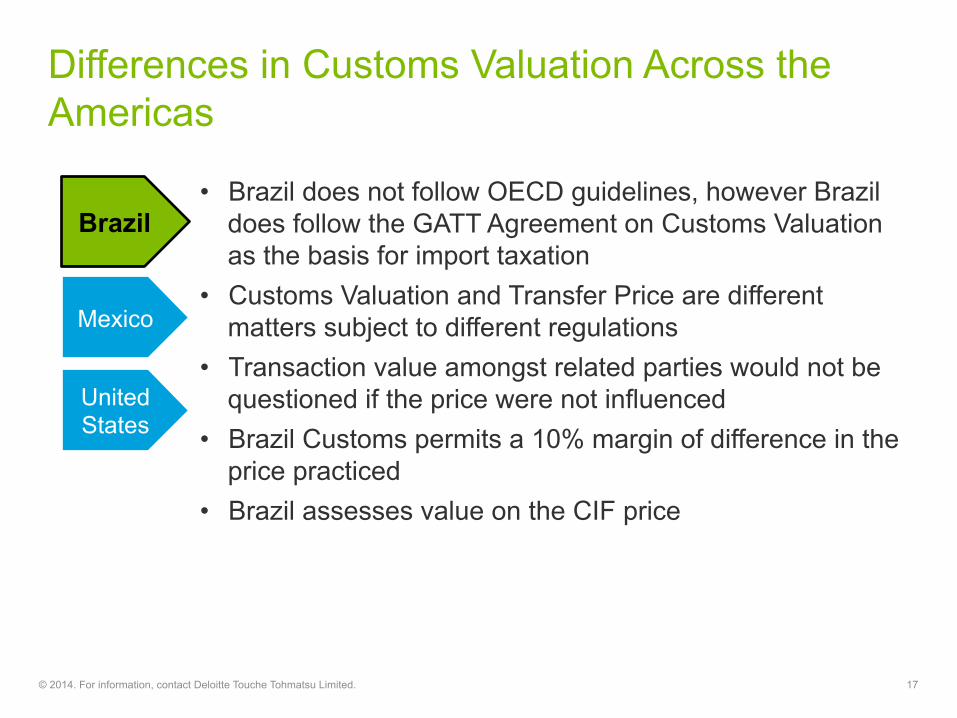

Differences in Customs Valuation Across the Americas

• Brazil does not follow OECD guidelines, however Brazil does follow the GATT Agreement on Customs Valuation as the basis for import taxation

• Customs Valuation and Transfer Price are different matters subject to different regulations

• Transaction value amongst related parties would not be questioned if the price were not influenced

• Brazil Customs permits a 10% margin of difference in the price practiced

• Brazil assesses value on the CIF price

17

Brazil

© 2014. For information, contact Deloitte Touche Tohmatsu Limited.

Mexico

United States

18

Brazil

© 2014. For information, contact Deloitte Touche Tohmatsu Limited.

Mexico

United States

• Customs Valuation and Transfer Pricing are different matters subject to different regulations.

• Importers are required to report to customs authorities a transfer pricing adjustment that modifies the price paid by the importer.

• The transfer pricing study are not enough to support the use of the transaction value method of customs valuation. However, transfer pricing studies may contain information useful to supporting transaction value.

• Transaction value is defined as the price paid or payable by the importer and may include transport, insurance and freight (CIF) costs payable by the importer unless these are broken down and indicated separately.

• According to the Mexican authorities, 78.6% of import transactions have a customs value determined using the transaction value method of valuation.

Differences in Customs Valuation Across the Americas (con’t)

19

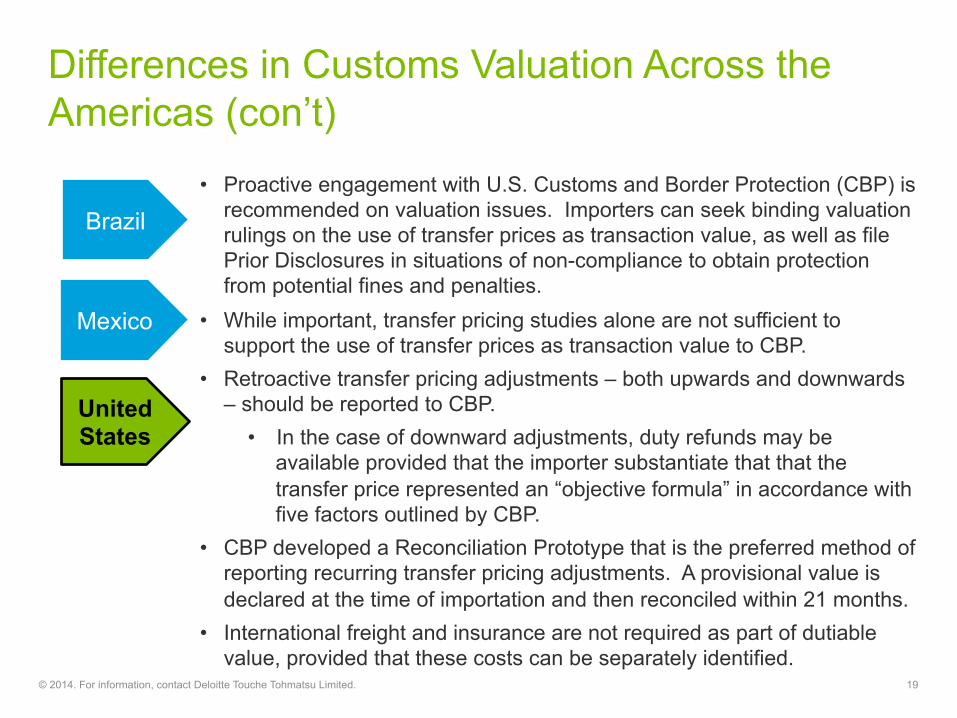

• Proactive engagement with U.S. Customs and Border Protection (CBP) is recommended on valuation issues. Importers can seek binding valuation rulings on the use of transfer prices as transaction value, as well as file Prior Disclosures in situations of non-compliance to obtain protection from potential fines and penalties.

• While important, transfer pricing studies alone are not sufficient to support the use of transfer prices as transaction value to CBP.

• Retroactive transfer pricing adjustments – both upwards and downwards – should be reported to CBP.

• In the case of downward adjustments, duty refunds may be available provided that the importer substantiate that that the transfer price represented an “objective formula” in accordance with five factors outlined by CBP.

• CBP developed a Reconciliation Prototype that is the preferred method of reporting recurring transfer pricing adjustments. A provisional value is declared at the time of importation and then reconciled within 21 months.

• International freight and insurance are not required as part of dutiable value, provided that these costs can be separately identified.

© 2014. For information, contact Deloitte Touche Tohmatsu Limited.

Brazil

Mexico

United States

Differences in Customs Valuation Across the Americas (con’t)

Proactive Planning for Customs Valuation

Prospective Adjustments

Retroactive Adjustments

Setting the Transfer Price IP Planning

• Intercompany price should satisfy customs valuation rules in addition to tax rules

• If customs valuation rules are not satisfied, Customs may require adjustments to customs values

• Examine impact of a change in price of future customs value declarations to determine if: o There is a risk

that Customs authorities may scrutinize or stop shipments

o An advance ruling should be considered

• Upward adjustments may result in additional duties, VAT, interest charges/penalties and require disclosure

• Downward adjustments may provide refunds or consider undervaluation and error requiring disclosure

• IP payments are frequently dutiable and may need to be added to customs value, which varies by country.

© 2014. For information, contact Deloitte Touche Tohmatsu Limited. 1 9

Effective Customs Valuation Practices

Clear Communication & Collaboration • If your Customs and Tax functions are not within

the same department, establish the dotted line

• Plan together for retroactive and prospective transfer pricing adjustments

Coordinate Tax & Customs Documentation • Frequent adjustments may warrant participation

in Customs programs to facilitate repeated post-transaction adjustments (e.g., U.S., Australia, Japan)

• Pursue joint APAs and customs value rulings

Implement Robust Processes

• Include requirements in customs and transfer pricing policies and procedures

• Implement training for key tax and customs personnel

• Execute periodic reviews to confirm that the intercompany price still satisfies Customs requirements

• Develop global processes with local procedures to match local country requirements

• Revisit customs value requirements when changes transfer pricing policies, systems, etc., occur

Participate in Special Programs

• Conduct contemporaneous TP studies and customs valuation assessments

• Document the acceptability of a transfer price as transaction value under the customs tests

• Determine whether retroactive transfer pricing adjustments require reporting of adjusted customs values to the Customs Authorities

• Draft your TP studies, policies, APAs, etc., to confirm they support customs requirements

© 2014. For information, contact Deloitte Touche Tohmatsu Limited. • 20

Managing the Impact of Export Controls in the Americas

22 © 2014. For information, contact Deloitte Touche Tohmatsu Limited.

What are export controls?

23 © 2014. For information, contact Deloitte Touche Tohmatsu Limited.

Foundations of Export Controls

End User

End Use

Country

Product

What are export controls? § Product Controls - Restrictions on the export

(and re-export) of controlled items, technology and software.

§ End-User Controls – Restrictions on exports to specific entities or persons can be prohibited or may require a license, and companies must screen entities in the supply chain against applicable restricted party lists.

§ End-Use Controls – The final end use of products, even though ground movers are commercial items, can trigger a license requirement if utilized in a military or controlled application.

§ Destination Controls - embargoes and sanctions against specific countries can restrict exports of products and technology.

Who is affected? All companies that export and import sensitive products and/or technologies. Typically the most complex companies operating in the Aerospace & Defense, Chemicals, Telecommunications, Oil & Gas industries.

Many advanced economies follow the Wassenaar Arrangement, a multilateral agreement between 41 participating countries to control exports of sensitive commercial or ‘dual-use’ goods and technologies. The four countries below are Wassenaar members and have export controls in place to control goods and technologies that could compromise national security:

• Argentina • Canada • Mexico • United States

Export Controls Across the Americas

24 © 2014. For information, contact Deloitte Touche Tohmatsu Limited.

Each country is free to implement its own export control framework.

Some other countries in the Americas have export control regimes are in place that focus on a more targeted list of controlled items including:

• Brazil – Export Law 9112 controls on military, space and nuclear items and technology.

• Chile – Exporter registration requirements, export licensing for certain listed products.

Many in the Americas do not currently have robust export control system in place, and are focused on the regulation of exports for agricultural, foreign exchange, short supply, and other unilateral objectives.

1) Impact of new export control requirements in Mexico − Companies doing business in Mexico need to carefully evaluate the products listed as requiring

an export permit, and also whether the ultimate customer is located in one of those countries that is exempt from the export permit requirement.

− Failure to comply is sanctioned, and it may include fines, administrative and criminal penalties

2) Extra-territorial reach of U.S. re-export controls − U.S. export control regulations apply to re-exports of US products and technology and the

activities of US persons, such as: o Shipment of a controlled U.S. origin item from one foreign country to another foreign country; o Releasing U.S. controlled technology to foreign nationals in a foreign country; and o US nationals are subject to U.S. export compliance regulations, wherever located.

− Therefore, foreign affiliates of US companies are required to comply with local country and US export compliance laws, including developing and maintaining an Internal Compliance Program with knowledgeable resources to identify and manage these US requirements.

3) Prospects for new export control regulations across the Americas − There is a growing focus by international community on national security, anti-terrorism, and the

growth of supply chain security programs in order to establish secure trade lanes with largest economies.

− Countries in the Americas (and elsewhere) are reviewing their position on export control regulations and enforcement in support of secure trade lanes.

Impacts of Export Controls

25 © 2014. For information, contact Deloitte Touche Tohmatsu Limited.

Non-compliance with export controls can result in severe monetary and criminal penalties against both an individual as well as companies, and can result in the loss of contracts, governmental debarment, and the denial of export privileges.

In addition to the monetary and criminal penalties, there are additional factors to be considered resulting from non-compliance.

Cost of Non-Compliance with Export Controls

26 © 2014. For information, contact Deloitte Touche Tohmatsu Limited.

Reputation Risk – Export violations oftentimes are published and could cause a ‘headline risk’. Does your company want to be featured in the Wall Street Journal for export violations? Business Disruption – Export violations and delays at the border can often disrupt the operational tempo of business operations. Bankruptcy or insolvency – Export violations can come with multi-million dollar penalties which could jeopardize a businesses ability to continue operations.

Export Controls

Examples of Penalties for export control violations include:

27 © 2014. For information, contact Deloitte Touche Tohmatsu Limited.

Company Type of Export Violation Penalty

Major European Bank

Violations of U.S. embargoes and economic sanctions.

$619 million settlement- largest penalty to date for OFAC sanctions violations.

Medical Instruments Company

U.S. export controlled items to Iran; export filing/documentation misrepresentation.

22 violations of U.S. export control regulations consisting of exporting ultrasound equipment from the United States to Iran through Belgium. $500,000 civil penalty.

International Oil and Gas Service Company

Unauthorized exports of oil and gas equipment to Iran, Syria, and Cuba via a foreign subsidiary.

$100 million ($50m Criminal and $50m Civil penalty)- Largest civil penalty ever levied by BIS

Engineering company in Brazil

Unauthorized release of software to design offshore oil and gas structures developed in the U.S. and released to Iran.

Fined $250,000 and ordered to forfeit $218,582 in revenue, plus 5 years in prison for the company owners.

Major defense contractor

ITAR violations for exports of night vision technology without proper license, including releasing technology to non-U.S. nationals.

Criminal penalties totaling $100 million ($50 million fine and $50 million in investment towards night vision technology). Comprehensive export compliance audit, monitoring and training effort significantly enhanced.

28 © 2014. For information, contact Deloitte Touche Tohmatsu Limited.

Automating Global Trade to Increase Compliance and Decrease Costs

29

Bridging the Gap through Automation

© 2014. For informa0on, contact Deloi7e Touche Tohmatsu Limited. 29

Global Trade Automa/on

Regulatory Concerns

External Pressures

Internal Interests

Resource Ra/onaliza/on

New import/export regulations and increased enforcement activity, along with internal and external business pressures, add more responsibility onto limited global trade resources. Global trade automation can help balance those competing concerns.

Resources

Global Trade Resource Gap

“Improve the productivity of the trade compliance department by implementing new technology” was identified as the top strategic action to improve global trade compliance. - Top Strategic Actions to Improve GTC, Aberdeen Group, October 2011

Limited resources may increase vulnerability to: – Late detection of trade barriers – Errors and penalties – Heavy reliance on outside agents – Lack of trade planning

29

Bridging the Gap through Automation (con’t)

© 2014. For informa0on, contact Deloi7e Touche Tohmatsu Limited.

Benefits of an automated, integrated global trade strategy

31

Ø Improve cycle and delivery time

Ø Reduce inventory – improve process and transaction visibility

Ø Potential duty-savings, vendor rationalization, warehousing, etc.

Ø Avoid offsetting cost-savings with increased duty / irrecoverable VAT

Ø Increase knowledge level on central level

Supply chain enhancement

Improved regulatory compliance

Increased profit and decreased cost

of goods Flexibility to change

Ø Central management of country-specific regulations, new laws

Ø Reduced penalties and administrative burden with government issues

Ø Tighter control on compliance

Ø Comprehensive records and auditability

Ø Supports preference determination

Ø Lower import duty burden

Ø Minimize bank/cash guarantees

Ø FTE consolidation

Ø Less administrative burden for sales transactions

Ø Increased customer satisfaction = stronger customer relationships

Ø Maximized usage of Free Trade Agreement benefits

Ø Streamline/ Centralize business operations

Ø Anticipate and prepare for future trade opportunities/challenges

© 2014. For information, contact Deloitte Touche Tohmatsu Limited.

Process Improvements through Automation

32 © 2014. For information, contact Deloitte Touche Tohmatsu Limited.

• Corporations site the growing complexity of security regulations and growing operational footprint as the impetus to automate trade compliance functions.

• More than half of respondents believe internal resistance and lack of understanding to be the greatest obstacle to implementing global trade management solutions.

• 60% of respondents listed implementing or collaborating with technology as a top priority for the coming year.

• 32% of companies claim to be “mostly manual” while 64% use manual spreadsheets as part of their compliance processes.

9.1%

25.9%

4.3%

35.0%

3.7% 9.8%

-1.0% N/A

Average Annual Improvement in

Effectivess

Increase in Productivity of Trade

Compliance Staff

Decrease in Supply Chain Interruptions

Reduction in Fines based on RPL

Screening

Automated Companies

Mostly Manual Companies

Source: 2011 Aberdeen Group Study

Providers of Global Trade Automation Solutions

33 © 2014. For information, contact Deloitte Touche Tohmatsu Limited.

34 © 2014. For information, contact Deloitte Touche Tohmatsu Limited.

Conclusion

© 2014. For information, contact Deloitte Touche Tohmatsu Limited. 35

• Build robust policies to obtain full supply chain visibility and proactively manage global filing requirements to anticipate and minimize potential supply chain delays

• Use trade automation to achieve Ø Timely insights into filing status, import/export processes, potential compliance risks Ø Reduced lead time, improved working capital and lower inventory carrying costs Ø Simplified trade management, and elimination of manual errors

• Build robust policies to manage FTA qualification and valuation of related party transactions, including cross-functional links between Tax and Trade Compliance

• Use trade automation to achieve Ø Centralized view for reduced errors and increased efficiency Ø Faster and easier compliance checks Ø Efficient compliance with e-filing mandates worldwide

Accelerate Trade

Ensure Compliance

Minimize Cost • Position Trade Compliance as a strategic business partner to be involved in supply

chain decisions and identify opportunities for FTAs and other savings mechanisms • Use trade automation to achieve:

Ø On-going compliance with fluctuating global regulations and agreements Ø Reduced duties and lower landed cost Ø Increased supply chain security and proactive risk management

Conclusion

Speaker bios Michele E. McGuire is the Principal in charge of Deloitte Tax LLP’s National Customs and Global Trade group. Michele has over

20 years of experience advising clients on numerous global trade matters and specializes in the operational side of global trade, helping clients assess and design their global trade management process including automated solutions. Michele’s deep regulatory and operational background allows her to apply real life practical solutions for her clients which are not only compliant with a myriad of global trade regulations but are also efficient and effective. Michele has extensive experience in advising Fortune 500 companies on numerous global trade management issues including; first sale for export planning and implementation; focused assessment and audit support; global internal control and process reviews and function design; designing and implementing automated global trade management systems including SAP’s Global Trade Services module, designing and implementing compliance programs; advising on other government agency requirements, designing and implementing Foreign Trade Zones and bonded facilities; on site customs training for clients; advising on various international trade agreements; advising on C-TPAT; tariff classification; customs valuation; country of origin determinations and marking. Phone: +1 312 486 9845 Email: [email protected]

Cecy Montano Hernandez is a Deloitte Mexico indirect tax partner and Mexican and Latin American service line leader, specialized in foreign trade, customs and indirect tax. She has more than 17 years of experience in foreign trade. Before joining Deloitte, Cecilia spent several years as Logistics and Customs Compliance Manager in the private sector. Currently Cecilia helps multinational companies identify indirect tax opportunities and has worked with clients around the world on projects involving due diligence, customs audits and tax strategies relative to investments in Mexico, among others. She works with clients operating across many industries. Cecilia is currently the Vice President of the Mexican Importers and Exporters Association, and participates as an active member of the most relevant associations in Mexico related to foreign trade and customs matters. She has a strong relationship with the Mexican Government in topics related to foreign trade and customs and regularly participates strategically with them, where necessary. Phone: +51 55 5080 6419 Email: [email protected]

Ricardo Goncalves is a Customs professional with more than 10 years of experience in Brazilian Customs and Foreign Trade and Brazilian Taxation. Also experienced in the industry, trading and services sectors, Ricardo has acquired knowledge in several topics related to the Brazilian Import and Export operations (i.e. Duties and Taxes, Commercial, Administrative, Operational, etc.). Currently he acts as a Customs and Global Trade Manager assisting companies on Customs consulting, related to indirect taxation on import and export operations, tax planning, taxes benefits application (i.e. Free Trade Agreements and Special Customs Regimes), import and export compliance diagnoses (i.e. Tariff Classification Code, Customs Valuation, Customs Clearance, etc.), among other topics. Ricardo also participates on projects for the implementation of the Brazilian IRS Express Customs Clearance Process for Brazilian manufacturers – Blue Line (“Linha Azul”). Phone: +55 11 5186 1371 Email: [email protected]

© 2014. For information, contact Deloitte Touche Tohmatsu Limited.

36

Deloitte refers to one or more of Deloitte Touche Tohmatsu Limited, a UK private company limited by guarantee, and its network of member firms, each of which is a legally separate and independent entity. Please see www.deloitte.com/about for a detailed description of the legal structure of Deloitte Touche Tohmatsu Limited and its member firms. Deloitte provides audit, tax, consulting, and financial advisory services to public and private clients spanning multiple industries. With a globally connected network of member firms in more than 150 countries, Deloitte brings world-class capabilities and high-quality service to clients, delivering the insights they need to address their most complex business challenges. Deloitte has in the region of 200,000 professionals, all committed to becoming the standard of excellence. This presentation contains general information only, and none of Deloitte Touche Tohmatsu Limited, its member firms, or their related entities (collectively, the “Deloitte Network”) is, by means of this publication, rendering professional advice or services. Before making any decision or taking any action that may affect your finances or your business, you should consult a qualified professional adviser. No entity in the Deloitte Network shall be responsible for any loss whatsoever sustained by any person who relies on this communication. © 2014. For information, contact Deloitte Touche Tohmatsu Limited. 37