GLOBAL The Global Macro Outlook -...

74

Please refer to page 72 for important disclosures and analyst certification, or on our website www.macquarie.com/research/disclosures. GLOBAL Key forecasts, changes this month 1) Tables for real GDP growth, CPI, interest rates, currencies and commodity prices are on pages 11-13. Online access to our global macro forecasts is available on request 2) With the global industrial production growth trough now ten months ago (December 2015) and the OECD LI trough already eight months ago (February 2016), the question has become the durability of the up-cycle 3) We present 32 charts over ten pages, arguing that the cycle continues through 2017 4) Being less than halfway into the upswing, unsurprisingly, our forecasts are largely unchanged this month Analyst(s) Macquarie Capital Securities (Japan) Limited Peter Eadon-Clarke +81 3 3512 7850 [email protected] Macquarie Capital Markets Canada Ltd. David Doyle, CFA +1 416 848 3663 [email protected] Macquarie Securities (Australia) Limited James McIntyre, CFA +61 2 8232 8930 [email protected] Macquarie Capital Limited Larry Hu PhD +852 3922 3778 [email protected] Jerry Peng +852 3922 3548 [email protected] Macquarie Capital Securities India (Pvt) Ltd Tanvee Gupta Jain +91 22 6720 4355 [email protected] Macquarie Equities South Africa (Pty) Ltd Elna Moolman +27 11 583 2570 [email protected] Macquarie Capital (Europe) Limited Matthew Turner +44 20 3037 4340 [email protected] Colin Hamilton +44 20 3037 4061 [email protected] 18 October 2016 The Global Macro Outlook 2017: in 10 pages and 32 charts After a February 2016 trough, the OECD Leading Indicator has recovered for six months. Please see the data on page 2. The industrial cycle was, we believe, the principal cause of the 2014-16 deceleration in global growth, and will be the driver of the forecast 2017-18 recovery. The durability of this upswing is strengthened by: 1) the employment-led recovery underway in Europe, 2) the healing of private sector balance sheets in advanced economies, and 3) the expected second leg up in the US consumption growth story, pages 2-10. Global real GDP growth; Macquarie’s the long grinding cycle forecast Note: The Total-16 is the IMF’s 10-advanced and 6 EM economies. Forecasts are Macquarie where available, alternatively the IMF – please see Fig 170. The country weights use market exchange rates, not PPP Source: IMF, Macquarie Research, October 2016 Our 2016-18 global real GDP growth forecasts are 2.2%, 2.6% and 2.7%, respectively, a continuation of our “the long grinding cycle” of neither global lift- off nor slump. There are three core forecasts underpinning our outlook: 1) A slow and cautious trajectory of Fed Funds rate increases: Our base case has a 25bp increase in December and then 25bps every six months thereafter, eventually reaching 2% in 2019: 7 October 2016 US Economics Wages, construction & edging to full employment. 2) We believe the Chinese authorities have the willingness and ability to maintain control of the RMB. We expect the RMB to appreciate modestly in 2017: 7 September 2016 China Macro: What is missing from the Trilemma and the implications for the RMB. 3) Oil prices trade higher in 2017 and 2018, to (Brent) $61/bbl and $68/bbl, whilst commodity prices are mixed reflecting China’s housing sector softening, Fig.36. Short-term business-cycle judgements are more likely to succeed with a deep awareness of more medium- and longer-term issues. In global macroeconomics, there are a considerable number of the latter. We examine 20 of them from page 30; topical issues investigated in our Macq-ro insights reports. 2.60 2.77 2.69 2.53 2.22 2.65 2.70 2.66 2.62 0.0 1.0 2.0 3.0 4.0 5.0 2012 2013 2014 2015 2016 2017 2018 2019 2020 16-Total Average 1980-2011, 3.0% p.a The long grinding cycle, 2.5% p.a Average 1980- 2011, 3.0% p.a The long grinding cycle, 2.5% p.a (Global real GDP growth)

Transcript of GLOBAL The Global Macro Outlook -...

Please refer to page 72 for important disclosures and analyst certification, or on our website

www.macquarie.com/research/disclosures.

GLOBAL

Key forecasts, changes this month

1) Tables for real GDP growth, CPI, interest

rates, currencies and commodity prices

are on pages 11-13. Online access to our

global macro forecasts is available on

request

2) With the global industrial production

growth trough now ten months ago

(December 2015) and the OECD LI

trough already eight months ago

(February 2016), the question has

become the durability of the up-cycle

3) We present 32 charts over ten pages,

arguing that the cycle continues through

2017

4) Being less than halfway into the upswing,

unsurprisingly, our forecasts are largely

unchanged this month

Analyst(s) Macquarie Capital Securities (Japan) Limited Peter Eadon-Clarke +81 3 3512 7850 [email protected] Macquarie Capital Markets Canada Ltd. David Doyle, CFA +1 416 848 3663 [email protected] Macquarie Securities (Australia) Limited James McIntyre, CFA +61 2 8232 8930 [email protected] Macquarie Capital Limited Larry Hu PhD +852 3922 3778 [email protected] Jerry Peng +852 3922 3548 [email protected] Macquarie Capital Securities India (Pvt) Ltd Tanvee Gupta Jain +91 22 6720 4355 [email protected] Macquarie Equities South Africa (Pty) Ltd Elna Moolman +27 11 583 2570 [email protected] Macquarie Capital (Europe) Limited Matthew Turner +44 20 3037 4340 [email protected] Colin Hamilton +44 20 3037 4061 [email protected]

18 October 2016

The Global Macro Outlook 2017: in 10 pages and 32 charts After a February 2016 trough, the OECD Leading Indicator has recovered for six

months. Please see the data on page 2. The industrial cycle was, we believe, the

principal cause of the 2014-16 deceleration in global growth, and will be the

driver of the forecast 2017-18 recovery.

The durability of this upswing is strengthened by: 1) the employment-led

recovery underway in Europe, 2) the healing of private sector balance sheets in

advanced economies, and 3) the expected second leg up in the US

consumption growth story, pages 2-10.

Global real GDP growth; Macquarie’s the long grinding cycle forecast

Note: The Total-16 is the IMF’s 10-advanced and 6 EM economies. Forecasts are Macquarie where available, alternatively the IMF – please see Fig 170. The country weights use market exchange rates, not PPP

Source: IMF, Macquarie Research, October 2016

Our 2016-18 global real GDP growth forecasts are 2.2%, 2.6% and 2.7%,

respectively, a continuation of our “the long grinding cycle” of neither global lift-

off nor slump. There are three core forecasts underpinning our outlook:

1) A slow and cautious trajectory of Fed Funds rate increases: Our

base case has a 25bp increase in December and then 25bps every six

months thereafter, eventually reaching 2% in 2019: 7 October 2016 US

Economics Wages, construction & edging to full employment.

2) We believe the Chinese authorities have the willingness and ability

to maintain control of the RMB. We expect the RMB to appreciate

modestly in 2017: 7 September 2016 China Macro: What is missing

from the Trilemma and the implications for the RMB.

3) Oil prices trade higher in 2017 and 2018, to (Brent) $61/bbl and

$68/bbl, whilst commodity prices are mixed reflecting China’s housing

sector softening, Fig.36.

Short-term business-cycle judgements are more likely to succeed with a deep

awareness of more medium- and longer-term issues. In global macroeconomics,

there are a considerable number of the latter. We examine 20 of them from page

30; topical issues investigated in our Macq-ro insights reports.

2.60 2.77 2.69 2.532.22 2.65 2.70 2.66 2.62

0.0

1.0

2.0

3.0

4.0

5.0

2012 2013 2014 2015 2016 2017 2018 2019 2020

16-Total Average 1980-2011, 3.0% p.a The long grinding cycle, 2.5% p.a

Average 1980-2011, 3.0% p.a

The long grinding cycle, 2.5% p.a

(Global real GDP growth)

Macquarie Research The Global Macro Outlook

18 October 2016 2

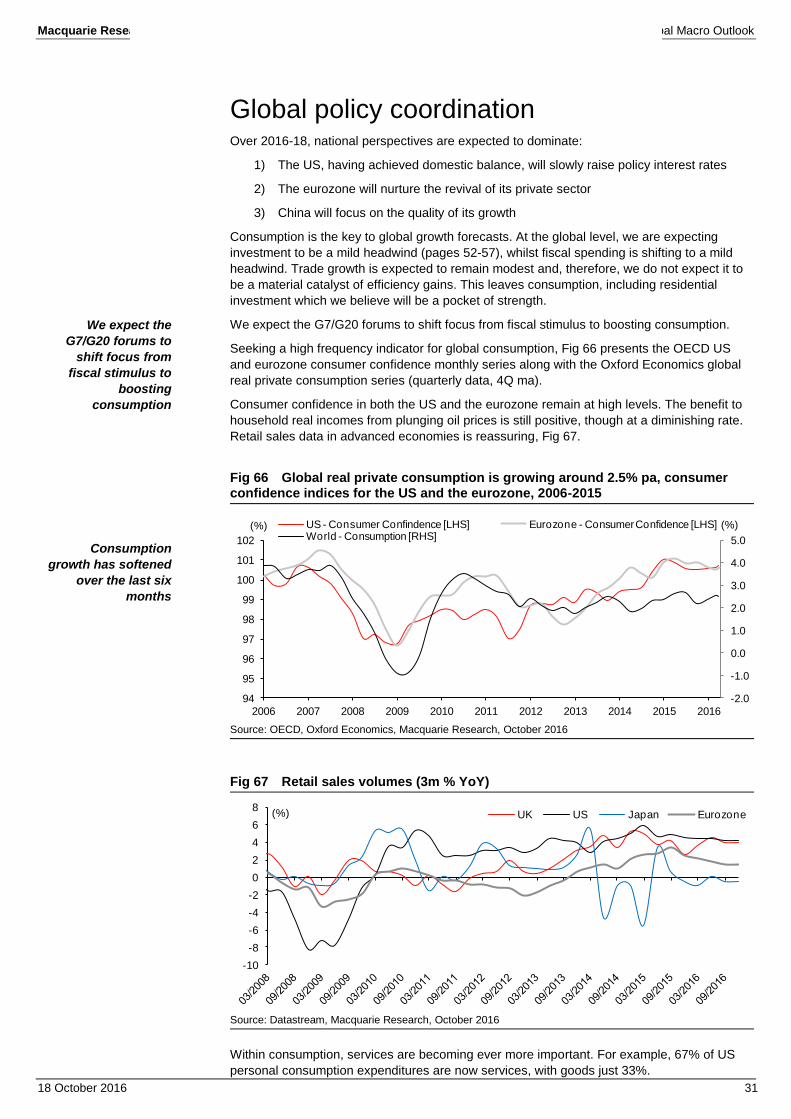

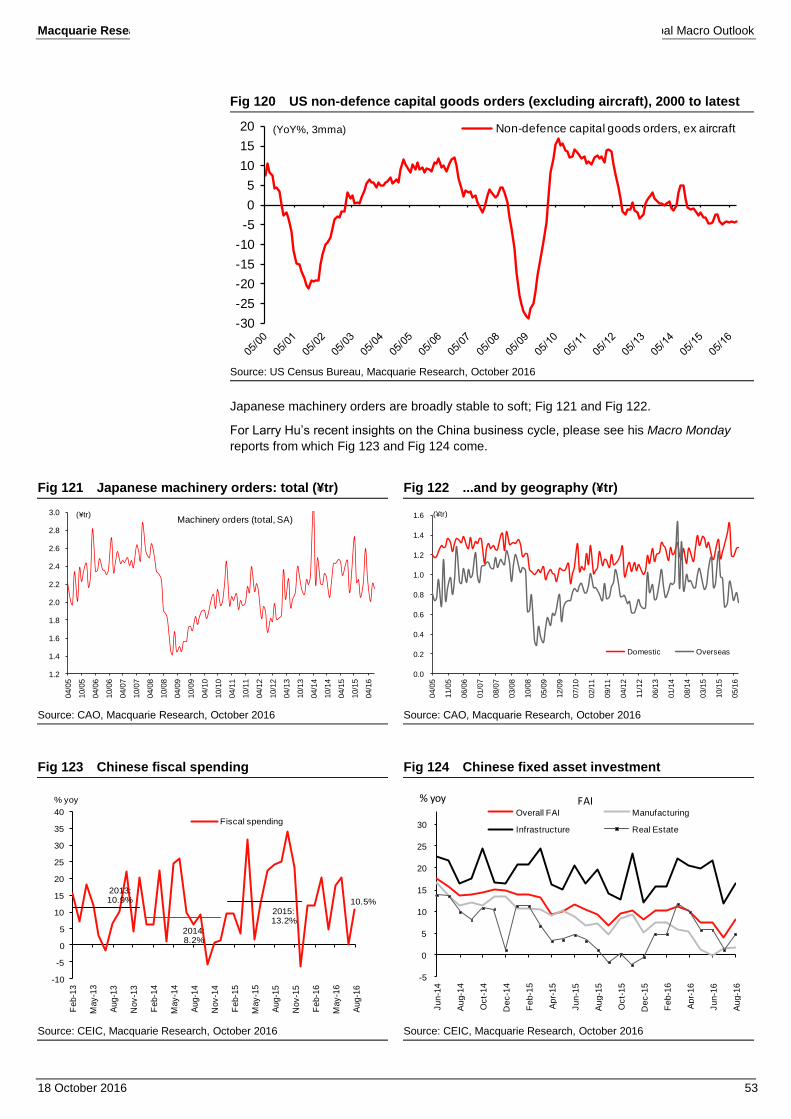

The cycle through 2017 In a further 9 pages and 31 charts

The global IP recovery is continuing post its December 2015 nadir of +0.4% YoY, with the

latest reading being +2.0% YoY in August 2016. Please see the 12 October 2016

Commodities Comment. Our 2017 forecast is +2.4%. This drives a mild acceleration in global

real GDP growth through 2017.

This broadening of growth is supported by the OECD LI, below, which focuses on GDP and

inflected in March 2016.

The eurozone is now following the US into an employment-led recovery, from page 3.

The US is expected to continue its long grinding cycle recovery, from page 5.

China’s real GDP growth rate is forecast to fade gently (2016 6.7%, 2017 6.4%, 2018 6.0%),

from page 7, whilst EM economies in general continue to grow at recent moderated rates.

The global real interest rate is expected to rise with the cycle, from page 9.

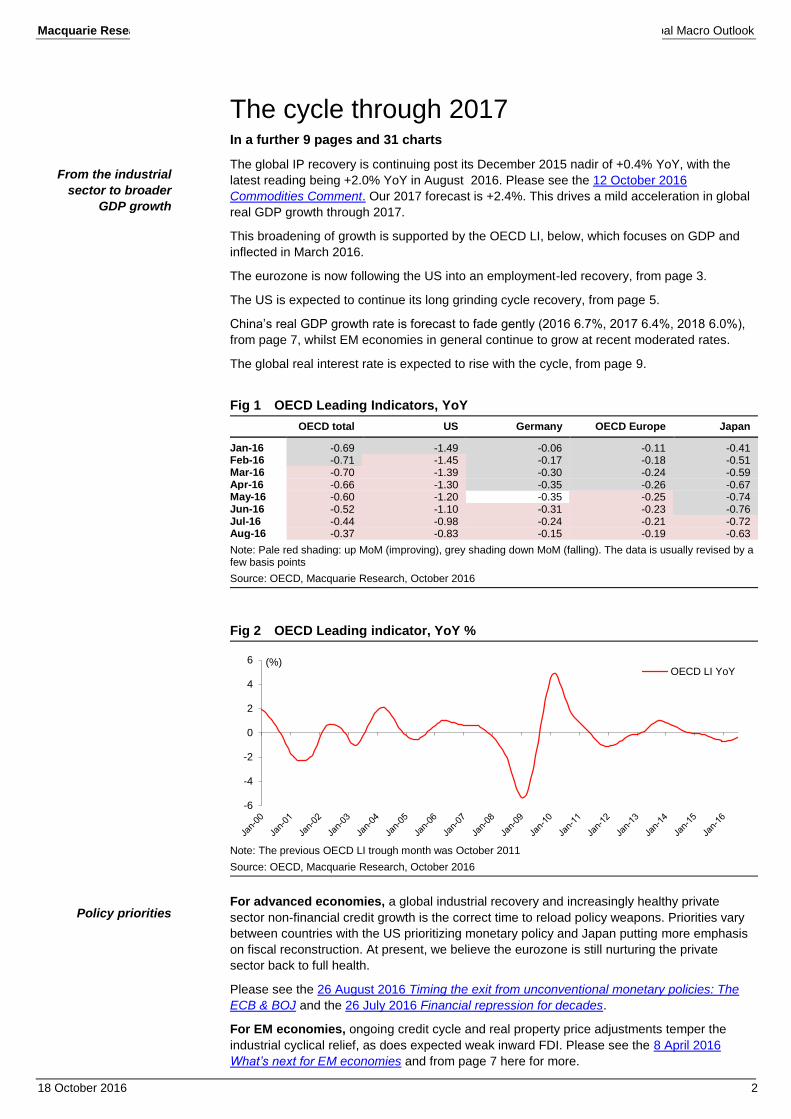

Fig 1 OECD Leading Indicators, YoY

OECD total US Germany OECD Europe Japan

Jan-16 -0.69 -1.49 -0.06 -0.11 -0.41 Feb-16 -0.71 -1.45 -0.17 -0.18 -0.51 Mar-16 -0.70 -1.39 -0.30 -0.24 -0.59 Apr-16 -0.66 -1.30 -0.35 -0.26 -0.67 May-16 -0.60 -1.20 -0.35 -0.25 -0.74 Jun-16 -0.52 -1.10 -0.31 -0.23 -0.76 Jul-16 -0.44 -0.98 -0.24 -0.21 -0.72 Aug-16 -0.37 -0.83 -0.15 -0.19 -0.63

Note: Pale red shading: up MoM (improving), grey shading down MoM (falling). The data is usually revised by a few basis points

Source: OECD, Macquarie Research, October 2016

Fig 2 OECD Leading indicator, YoY %

Note: The previous OECD LI trough month was October 2011

Source: OECD, Macquarie Research, October 2016

For advanced economies, a global industrial recovery and increasingly healthy private

sector non-financial credit growth is the correct time to reload policy weapons. Priorities vary

between countries with the US prioritizing monetary policy and Japan putting more emphasis

on fiscal reconstruction. At present, we believe the eurozone is still nurturing the private

sector back to full health.

Please see the 26 August 2016 Timing the exit from unconventional monetary policies: The

ECB & BOJ and the 26 July 2016 Financial repression for decades.

For EM economies, ongoing credit cycle and real property price adjustments temper the

industrial cyclical relief, as does expected weak inward FDI. Please see the 8 April 2016

What’s next for EM economies and from page 7 here for more.

-6

-4

-2

0

2

4

6 (%)OECD LI YoY

From the industrial

sector to broader

GDP growth

Policy priorities

Macquarie Research The Global Macro Outlook

18 October 2016 3

Advanced economies: Private sector balance sheet repair & revival

Debt is not inherently a problem. Intermediated by the financial system, it is the main way that

savers earn returns. Savers, to be sustainably paid, however, require debt to be deployed into

debt-serviceable activities. We regard private sector non-financial credit growth broadly in line

with nominal GDP growth to be healthy.

Private sector balance sheet repair and the revival of private sector non-financial credit

growth is a sign of progress, of the economy healing from its previous excesses.

The revival of private sector credit demand is a prerequisite for the successful withdrawal of

extraordinary central bank support for the economy.

In the case of Japan, the excess of credit growth over nominal GDP growth over the 1980s

“Bubble” was followed by a protracted period of balance sheet adjustment (credit growth

beneath nominal GDP growth, Fig.3). We believe Japan endured a vicious cycle of policy and

regulatory mistakes, which US policy avoided after the Global Financial Crisis, Fig.4.

Fig 3 Japan: private non-financial credit growth vs. Nominal GDP growth

Fig 4 US private sector nonfinancial credit is growing faster than GDP for the first time since 2008

Source: FRB of St Louis, Datastream, Macquarie Research, October 2016 Source: FRB of St. Louis, Macquarie Securities, October 2016

Nevertheless, even in the US, the repair process took a total of seven years. It took three

years from when private sector credit growth first collapsed (2008) until it first went positive

again (2011) and another four years until it exceeded nominal GDP growth (2015).

Fig 5 Euro Area: private nonfinancial credit growth vs. Nominal GDP growth

Fig 6 The fiscal impulse: the eurozone’s 2011-13 fiscal squeeze

Source: FRB of St Louis, Datastream, Macquarie Research, October 2016

Note: Year-over-year change in the cyclically adjusted net lending (+) or net borrowing (-) of general government, adjusted based on potential GDP, excessive deficit procedure. Forecasts for 2015-17 from the European Commission. Source: EC Annual Macroeconomic Database, Macquarie Research, October 2016

-12

-9

-6

-3

0

3

6

1992 1993 1995 1997 1999 2001 2003 2005 2007 2009 2011 2013 2015

(YoY % change)

Private nonfinancial credit

Nominal GDP

late

-4

-2

0

2

4

6

8

10

12(YoY% change) Private nonfinancial credit

Nominal GDP

latest

-6

-4

-2

0

2

4

6

8

10

12

14(YoY % change) Private nonfinancial credit

Nominal GDP

-2

-1

0

1

2

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

(% of potential GDP)

YoY change in cyclically adjusted budget balance

The case of Japan

The US

Macquarie Research The Global Macro Outlook

18 October 2016 4

The eurozone is behind the US because of the 2011-13 fiscal squeeze, Fig 6, and a second

credit crunch in 2011-13, Fig 7, such that private sector credit growth double-dipped and has

only gone positive again in 2015, four years behind the US (2015 versus 2011), Fig 5.

Nonetheless, a recovery is underway, led by strengthening employment. As employment

increases, Fig 8, households become more confident to borrow, Fig 9 and Fig 10. Auto sales

are also recovering across Europe, Fig 11 and Fig 12.

Fig 7 Euro-zone: Tight lending conditions 2007-09 and 2011-13

Fig 8 Eurozone employment growth, YoY, %, 2002 to latest: +1.5% YoY

Note: Net percentage is used. The net percentage is defined as the difference between the sum of the percentages for “tightened considerably” and “tightened somewhat”, and the sum of the percentages for “eased somewhat” and “eased considerably”. Positive numbers imply tight lending conditions.

Source: left-hand chart: ECB, Macquarie Research, October 2016, right-hand chart: Eurostat, Macquarie Research, October 2016

Fig 9 Euro area consumer credit outstanding, YoY, %, 2005 to latest

Fig 10 Germany, France and Spain: consumer credit outstanding, YoY, %, 2005 to latest

Note: the latest value is 605.4 billion Euro. Source: ECB, Macquarie Research, October 2016

Source: ECB, Macquarie Research, October 2016

Fig 11 European new vehicle registrations, YoY, % Fig 12 European car sales, units, SA

Source: National car data, Macquarie Research, October 2016 Source: ECB, Macquarie Research, October 2016

-40

-20

0

20

40

60

80

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

(%)Changes in credit standards applied to enterprises over the past three months

-2.5

-2.0

-1.5

-1.0

-0.5

0.0

0.5

1.0

1.5

2.0

2.5

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

(%, YoY)Eurozone unemployment growth

-6

-4

-2

0

2

4

6

8

10

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

(%, YoY)Loans to households consumer credit

-20

-15

-10

-5

0

5

10

15

20

25

30

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

(%, YoY)Germany - Loans to households consumer credit

France - Loans to households consumer credit

Spain- Loans to households consumer credit

(20%)

(15%)

(10%)

(5%)

0%

5%

10%

15%

2010 2011 2012 2013 2014 2015 2016

YoY change12m moving average

800,000

850,000

900,000

950,000

1,000,000

1,050,000

1,100,000

1,150,000

1,200,000

1,250,000

Jan-12 Jan-13 Jan-14 Jan-15 Jan-16

The eurozone

Macquarie Research The Global Macro Outlook

18 October 2016 5

Whilst the eurozone is now following the US into an employment-led recovery, the US is

expected to continue its long grinding cycle recovery.

The energy-capex collapse induced growth slowdown in the US over 2015 and the 1H 2016

is over. After a forecast 1.5% real GDP growth this year, we are forecasting 2.4% pa real

GDP growth for both 2017 and 2018. Sometimes it is valuable to look backwards, to increase

one’s confidence in the future.

Fig 13 Energy-capex (red), Residential investment (green) and non-energy, non-resi. (blue) 2010=1.0

Fig 14 Energy & mining related investment as a share of non-residential investment, %

Source: BEA, Macquarie Research, October 2016 Source: BEA, Macquarie Research, October 2016

Fig 15 Average hourly earnings, YoY, %, oil states (blue), non-oil states (red), 3/2008 to latest

Fig 16 Civilian non-institutional population 25-54 year olds (12-month ma), 2002 to 2025E

Source: BLS, Macquarie Research, October 2016 Source: BLS, Census Bureau, Macquarie Research, October 2016

Fig 17 US residential investment share in GDP (%) Fig 18 US construction employment, % of total

Source: BEA, BLS, Macquarie Research, October 2016 Source: BEA, BLS, Macquarie Research, October 2016

0.3

0.5

0.7

0.9

1.1

1.3

1.5

1.7

1.9

2.1

2.3

1Q10 1Q11 1Q12 1Q13 1Q14 1Q15 1Q16 1Q17

Private investment (nominal $) (1Q 2010=1.00)

1Q10 = 1.00energy & mining

investment

non-residential investment ex-energy & mining investment

residentialinvestment

0%

2%

4%

6%

8%

10%

12%

14%

1959 1964 1969 1974 1979 1984 1989 1994 1999 2004 2009 2014

Energy & mining related investment as a share of non-residential investment

Average

+1STDEV

-1STDEV

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

4.0%

4.5%

Mar-08 Mar-09 Mar-10 Mar-11 Mar-12 Mar-13 Mar-14 Mar-15 Mar-16

Average hourly earnings YoY% change (3moMA)

current = 2.9%

non-oil

states

oil states

121,000,000

122,000,000

123,000,000

124,000,000

125,000,000

126,000,000

127,000,000

128,000,000

129,000,000

130,000,000

2002 2004 2006 2008 2010 2012 2014 2016 2018 2020 2022 2024

Civilian noninstitutional population25-54 years (12moMA)

Note: Projections in 25-54 population from BLS

2.0%

2.5%

3.0%

3.5%

4.0%

4.5%

5.0%

5.5%

6.0%

6.5%

7.0%

1970 1975 1980 1985 1990 1995 2000 2005 2010 2015

US residential investment share of GDP

+1 STDEV

Average

-1 STDEV

2005-6

1987

1973 1978

1999

Recession risks elevated when housing's importance is high

Expansions are likely when housing's importance is low and rising

4.0%

4.2%

4.4%

4.6%

4.8%

5.0%

5.2%

5.4%

5.6%

5.8%

1970 1975 1980 1985 1990 1995 2000 2005 2010 2015

2006

2000

1990

1979

1973

US construction employment as share of total employment

+1 STDEV

Avg

-1 STDEV

The US energy-

capex collapse

Macquarie Research The Global Macro Outlook

18 October 2016 6

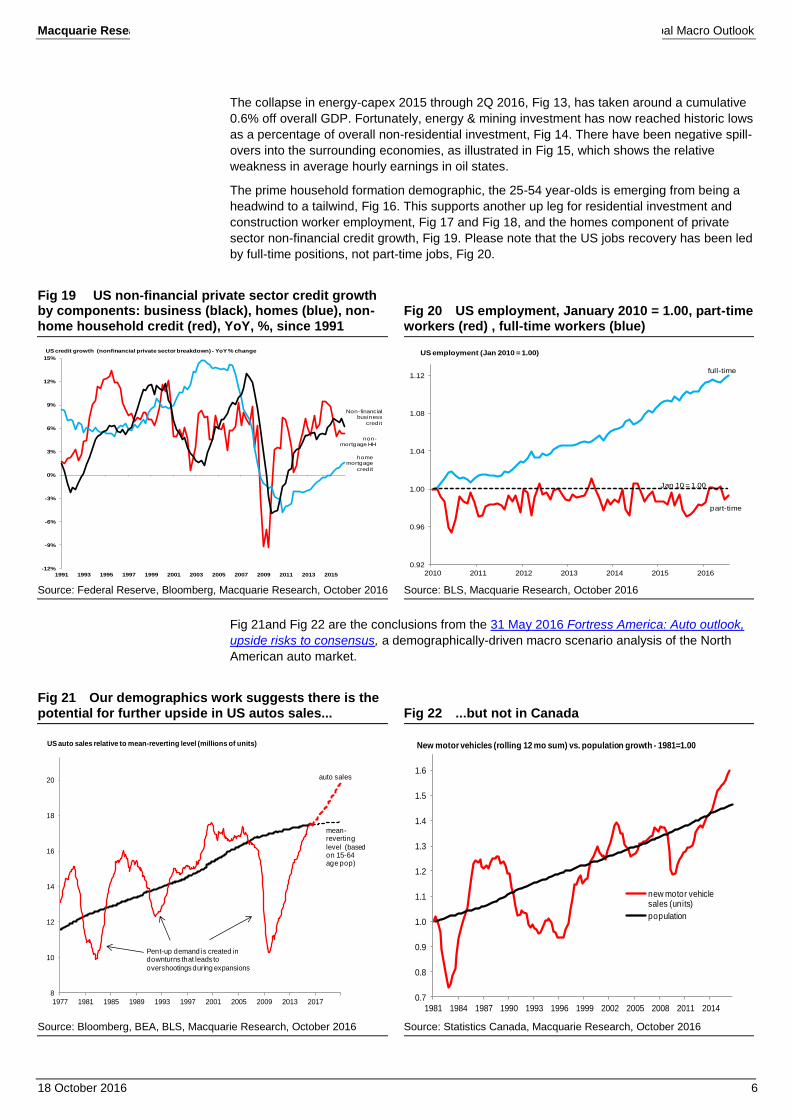

The collapse in energy-capex 2015 through 2Q 2016, Fig 13, has taken around a cumulative

0.6% off overall GDP. Fortunately, energy & mining investment has now reached historic lows

as a percentage of overall non-residential investment, Fig 14. There have been negative spill-

overs into the surrounding economies, as illustrated in Fig 15, which shows the relative

weakness in average hourly earnings in oil states.

The prime household formation demographic, the 25-54 year-olds is emerging from being a

headwind to a tailwind, Fig 16. This supports another up leg for residential investment and

construction worker employment, Fig 17 and Fig 18, and the homes component of private

sector non-financial credit growth, Fig 19. Please note that the US jobs recovery has been led

by full-time positions, not part-time jobs, Fig 20.

Fig 19 US non-financial private sector credit growth by components: business (black), homes (blue), non-home household credit (red), YoY, %, since 1991

Fig 20 US employment, January 2010 = 1.00, part-time workers (red) , full-time workers (blue)

Source: Federal Reserve, Bloomberg, Macquarie Research, October 2016 Source: BLS, Macquarie Research, October 2016

Fig 21and Fig 22 are the conclusions from the 31 May 2016 Fortress America: Auto outlook,

upside risks to consensus, a demographically-driven macro scenario analysis of the North

American auto market.

Fig 21 Our demographics work suggests there is the potential for further upside in US autos sales... Fig 22 ...but not in Canada

Source: Bloomberg, BEA, BLS, Macquarie Research, October 2016 Source: Statistics Canada, Macquarie Research, October 2016

-12%

-9%

-6%

-3%

0%

3%

6%

9%

12%

15%

1991 1993 1995 1997 1999 2001 2003 2005 2007 2009 2011 2013 2015

non-mortgage HH

home mortgage

credit

US credit growth (nonfinancial private sector breakdown) - YoY % change

Non-financialbusiness

credit

0.92

0.96

1.00

1.04

1.08

1.12

2010 2011 2012 2013 2014 2015 2016

US employment (Jan 2010 = 1.00)

Jan 10 = 1.00

part-time

full-time

8

10

12

14

16

18

20

22

1977 1981 1985 1989 1993 1997 2001 2005 2009 2013 2017

US auto sales relative to mean-reverting level (millions of units)

auto sales

mean-reverting

level (based on 15-64 age pop)

Pent-up demand is created in downturns that leads to

overshootings during expansions

0.7

0.8

0.9

1.0

1.1

1.2

1.3

1.4

1.5

1.6

1.7

1981 1984 1987 1990 1993 1996 1999 2002 2005 2008 2011 2014

new motor vehicle sales (units)

population

New motor vehicles (rolling 12 mo sum) vs. population growth - 1981=1.00

Macquarie Research The Global Macro Outlook

18 October 2016 7

China, EM more generally and global trade growth

With the advanced economies doing a little better, global growth is able to accommodate the

ongoing gentle fade in China’s growth.

Rather than a hard stop of the investment-driven, credit-driven growth models of Malaysia,

Thailand, Indonesia and Korea as occurred in 1997, below, as marginal capital providers

(cross-border bank lending) withdrew, we expect the Chinese-case marginal capital providers

(households depositing into the Chinese banking system) to persist.

Fig 23 Gross fixed capital formation, % of GDP

Note: Investment is private investment and includes residential investment. The last two data points are IMF forecasts

Source: BIS, Macquarie Securities, October 2016

Whilst China’s ratio of investment (including residential investment) to GDP is declining

(Fig.24) as the rate of growth of investment slows (Fig 25), it still has a lot further to decline to

meet international norms.

Fig 24 China’s investment, % of GDP Fig 25 China’s investment (US$ tr)

Source: IMF WEO database, Macquarie Research, October 2016 Source: IMF WEO database, Macquarie Research, October 2016

China’s real GDP growth continues to fade as the relative productivity of marginal investment

deteriorates.

We are forecasting Chinese real GDP growth to be 6.4% in 2017 and 6.0% in 2018 after

6.7% this year.

For emerging market economies more generally, growth has been fading since 2012 as the

economies looks for a new growth engine, and unwinds the credit excesses of the past.

Fig 26 shows the ratio of private non-financial credit to GDP and its growth over the last five

years.

10

20

30

40

50

1970

1972

1974

1976

1978

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

2002

2004

2006

2008

2010

2012

2014

(% of GDP) Malaysia Thailand Indonesia Korea

25

30

35

40

45

50

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

2002

2004

2006

2008

2010

2012

2014

2016

(%GDP) China's investment, % of GDP

0.0

1.0

2.0

3.0

4.0

5.0

6.0

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

2002

2004

2006

2008

2010

2012

2014

2016

(US$tr) China's investment

The ongoing gentle

fade in China’s

growth

Emerging market

economies more

generally

Macquarie Research The Global Macro Outlook

18 October 2016 8

Whilst the ratio to GDP generally increases with economic development and financial

deepening, relative to other EM economies shown below, some countries appear elevated,

implying a need to go through a period of private debt adjustment.

Fig 26 Private non-financial credit, level and growth, for leading EM economies

Note: The BIS does not have data for the Philippines

Source: BIS, Macquarie Research, October 2016

A particular challenge for non-China EM is our belief that China began a serious import

substitution phase in 2015 and this will continue for as long as the old growth model

persists, and SOE’s invest with a perceived near zero cost of capital.

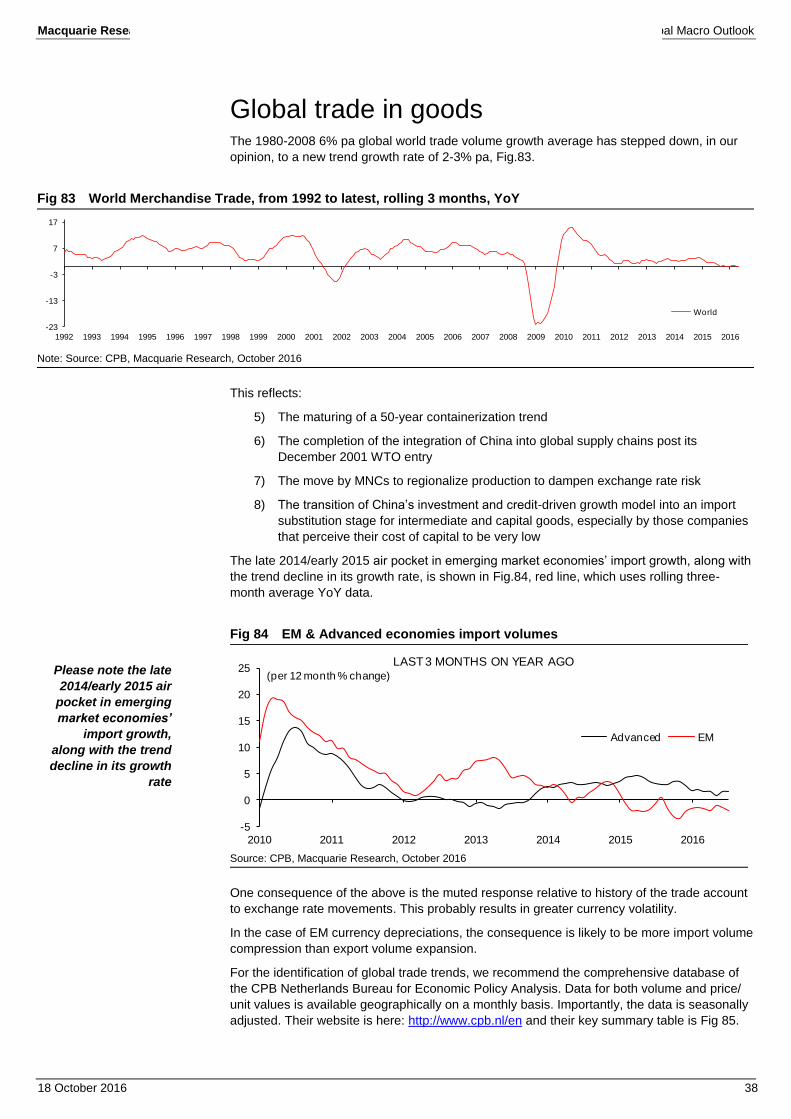

The 1980-2008 6% pa global world trade volume growth average has stepped down, in our

opinion, to a new trend growth rate of 2-3% pa, Fig 27.

Fig 27 World Merchandise Trade, from 1992 to latest, rolling 3 months, YoY

Note: as a consistency check, we are looking for real GDP growth to accelerate 50bp, 2018 versus 2016 (chart front cover), and if advanced economies are the source of this (with global GDP 60:40 advanced economies: EM on market exchange rates) it implies advanced economies will accelerate by 80bp (80bp times 0.6 equals 48bp, approximately equal to 50bp). If the OECD LI needs to rise 80bp from its low of -71bp in February 2016, then it is only going to go marginally positive in this cycle, at +10bp or so. Given the relationship in the above chart, the reacceleration in world trade could be very modest

Source: CPB, Macquarie Research, October 2016

This reflects:

1) The maturing of a 50-year containerization trend

2) The completion of the integration of China into global supply chains post its

December 2001 WTO entry

3) The move by MNCs to regionalize production to dampen exchange rate risk

4) The transition of China’s investment and credit-driven growth model into an import

substitution stage for intermediate and capital goods, especially by those companies

that perceive their cost of capital to be very low

Brazil

Mexico

Russia

Turkey

India

China

Indonesia

Malaysia

Singapore

Thailand

0

10

20

30

40

50

60

0 50 100 150 200 250

2015 3Q vs 2010 3Q

Private debt as % of GDP

Change in five years (%)

-6

-4

-2

0

2

4

6

-23

-13

-3

7

17

1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

World Merchandise Trade, YoY [LHS] OECD LI, YoY [RHS]

(%) (%)

Macquarie Research The Global Macro Outlook

18 October 2016 9

The late 2014/early 2015 air pocket in emerging market economies’ import growth, along with

the trend decline in its growth rate, is shown in Fig 28, red line, which uses rolling three-

month average YoY data.

These headwinds will persist even as the OECD LI recovers to a positive YoY level.

Fig 28 EM & Advanced economies import volumes

Source: CPB, Macquarie Research, October 2016

One consequence of the above is the muted response relative to history of the trade account

to exchange rate movements. This probably results in greater currency volatility. In the case

of EM currency depreciations, the consequence is likely to be more import volume

compression than export volume expansion.

The long, grinding cycle and low real interest rates

The principal driver of record low bond yields has evolved from cyclical factors (secular

stagnation), through a private sector balance sheet recession (completed in the US and

Japan, progressing, but ongoing in the eurozone) to fiscal reconstruction (reloading the fiscal

policy tool weapon) using the tool of financial repression.

The political consequences of ‘the long grinding cycle’ have been intensifying. Entitlement

program promises are under pressure. Politicians are not only looking to boost global growth,

somehow, but also to ensure low funding costs persist for as long as possible.

Fig 29 10-year real bond yields, G7 ex Italy, 1985-2013, quarterly, %

Note: National Bureau of Economic research (NBER) working paper “Measuring the world interest rate” by Mervyn King & David Low (2014) The US enters the sample in 1999 with the first TIPS issue.

Source: NBER above, Macquarie Research, October 2016

The 26 July 2016 Macq-ro insights: Financial repression for decades examined these issues,

and concluded that the 10-year US TIP yield was a reasonable proxy to monitor, Fig.30.

Please note how it (the red line) has trended down from ~2% in 2003 to ~10bps recently.

-5

0

5

10

15

20

25

2010 2011 2012 2013 2014 2015 2016

Advanced EM

(per 12 month % change)

LAST 3 MONTHS ON YEAR AGO

-1

0

1

2

3

4

5

6

1985 1987 1989 1991 1993 1995 1997 1999 2001 2003 2005 2007 2009 2011 2013

(%) Weighted real rate Unweighted real rate

Financial repression

for decades

Macquarie Research The Global Macro Outlook

18 October 2016 10

The 10-year TIPS yield was lowest during the most aggressive phase of US monetary easing

in 2012 (QE3), increased sharply with the May 2013 ‘Taper Tantrum’, and has drifted lower

since the Fed began to slowly and cautiously withdraw its extraordinary monetary easing.

Fig 30 US TIPs yields, %

Source: US Department of the Treasury, FED, Macquarie Research, October 2016

The cycle and the trend: Integrated global capital markets imply that we should expect a

mild recovery in global real GDP growth over 2017-18 to lead to a mild increase in the global

real interest rate (50bp or so). In addition to the global real interest rate, nominal bond yields

have an additional element relating to inflationary expectations. Fig.31 illustrates this for the

US 10-year bond. Our forecasts for US inflation suggest that the inflation compensation

element will increase going forward; leading to an overall increase in nominal US bond yields.

Nonetheless, real interest rates are expected to remain well beneath our 2.5% pa global real

GDP growth forecast.

Fig 31 We anticipate the inflation compensation element to drive an increase in the 10-year Treasury yield

Note: Over time US 10-year bond yields are expected to have a global real interest rate component of around 0.5%, and an inflation compensation component of around 2%.

Source: Bloomberg, Macquarie Research, October 2016

For advanced economies, a global industrial recovery and increasingly healthy private sector

non-financial credit growth is the correct time to reload policy weapons. Priorities vary

between countries with the US prioritizing monetary policy and Japan putting more emphasis

on fiscal reconstruction. The eurozone continues to focus on nurturing the private sector back

to robust health, in our opinion.

-2

-1

0

1

2

3

4

5

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

(yield, %)Treasury inflation protected securities - 5 yearTreasury inflation protected securities - 7 yearTreasury inflation protected securities - 10 yearTreasury inflation protected securities - 20 yearTreasury inflation protected securities - long term

-1.5

-1.0

-0.5

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

real yield

inflation compensation

2005-14 infl. comp avg

10 year Treasury yield components

forecast

forecast

Real interest rates

are expected to

remain well beneath

our 2.5% pa global

real GDP growth

forecast

Macquarie Research The Global Macro Outlook

18 October 2016 11

Forecasts and revisions Fig.32 & Fig.33 present our principal real GDP forecasts and revisions.

Revisions over the last month have been minor. Over the last four months:

1) UK real GDP growth forecasts are: 2016 2.0% (versus 1.9%), 2017 1.2% (2.3%).

2) Eurozone real GDP growth forecasts are: 2016 1.6% (1.8%), 2017 1.4% (1.7%)

For 2017, we are beneath consensus on Canada, Australia and Japan.

We are above-consensus in our 2017 forecasts for the US and most of Asia.

Fig 32 Macquarie’s real GDP forecasts

Calendar Year YoY (%) 4Q on 4Q (%) 2014 2015 2016 2017 2018 2014 2015 2016 2017 2018

US 2.4 2.6 1.6 2.4 2.1 2.5 1.9 2.0 2.3 2.0 Eurozone 0.9 1.9 1.6 1.4 1.6 1.0 1.9 1.5 1.6 1.6 Japan -0.1 0.6 0.4 0.6 0.7 -0.9 0.8 0.4 0.6 0.7 UK 2.9 2.2 2.0 1.2 1.2 2.9 2.2 2.0 1.2 1.2 Canada 2.5 1.1 1.2 1.8 1.6 2.4 0.3 1.6 1.7 1.5 Australia 2.6 2.4 2.8 2.3 3.2 2.2 2.8 2.3 2.7 3.5 New Zealand 3.7 2.5 3.4 3.3 2.4 4.1 2.3 3.5 3.0 2.2

China 7.2 6.8 6.7 6.4 6.0 7.2 6.8 6.7 6.4 6.0 S. Korea 3.3 2.6 2.9 2.9 2.7 2.7 3.1 2.7 2.8 2.7 Taiwan 3.9 0.6 1.3 2.0 2.3 3.4 -0.9 2.3 2.0 2.3 Hong Kong 2.6 2.4 1.2 1.5 2.0 2.5 1.9 1.2 1.5 2.0 Indonesia 5.0 4.8 4.9 5.0 5.2 5.0 5.0 4.5 5.0 5.2 Malaysia 6.0 5.0 4.3 4.7 5.1 5.7 4.5 5.0 4.7 5.1 Singapore 3.3 2.0 1.9 2.1 2.4 2.9 1.7 1.9 2.1 2.4 Philippines 6.2 5.9 6.2 6.1 6.3 6.6 6.6 5.6 6.1 6.3 Thailand 0.8 2.8 3.2 3.3 3.5 2.1 2.8 3.0 3.3 3.5 India 6.7 7.2 7.6 7.8 7.7 6.6 7.2 7.9 7.8 7.5

South Africa 1.5 1.2 0.4 0.9 1.7 1.3 0.0 0.7 0.9 1.3

Source: Macquarie Research, October 2016

Fig 33 Macquarie’s real GDP forecasts: revisions, and versus consensus

2016 YoY (%) 2017 YoY (%) Previous

Macquarie forecast (*)

Current Macquarie

Forecast Consensus Spread (2) versus (3)

Previous Macquarie forecast (*)

Current Macquarie

Forecast Consensus Spread (6) versus (7)

(1) (2) (3) (4) (5) (6) (7) (8)

US (**) 1.9 2.0 1.9 0.1 2.3 2.3 2.1 0.2 Eurozone 1.6 1.6 1.5 0.1 1.4 1.4 1.3 0.1 Japan 0.4 0.4 0.6 -0.2 0.6 0.6 0.8 -0.2 UK 1.9 2.0 1.7 0.3 1.1 1.2 0.7 0.5 Canada (**) 1.6 1.6 1.5 0.1 1.7 1.7 2.0 -0.3 Australia 3.0 2.8 2.9 -0.1 2.3 2.3 2.8 -0.5 New Zealand 3.2 3.4 3.0 0.4 3.3 3.3 2.8 0.5

China 6.7 6.7 6.6 0.1 6.4 6.4 6.3 0.1 S. Korea 2.9 2.9 2.6 0.3 2.9 2.9 2.6 0.3 Taiwan 1.3 1.3 1.0 0.3 2.4 2.0 1.7 0.3 Hong Kong 2.0 1.2 1.2 0.0 2.6 1.5 1.5 0.0 Indonesia 4.9 4.9 5.0 -0.1 5.0 5.0 5.3 -0.3 Malaysia 4.3 4.3 4.1 0.2 4.7 4.7 4.3 0.4 Singapore 1.9 1.9 1.7 0.2 2.1 2.1 1.8 0.3 Philippines 6.2 6.2 6.4 -0.2 6.1 6.1 6.1 0.0 Thailand 3.2 3.2 3.1 0.1 3.3 3.3 3.2 0.1 India (***) 7.6 7.6 7.6 0.0 7.6 7.6 7.7 -0.1

South Africa 0.3 0.4 0.4 0.0 0.9 0.9 1.3 -0.4

Note: (*) August 2016. Calendar year numbers for all countries bar the US and Canada, marked with a (**) which are 4Q on 4Q, and India, marked with a (***) which is fiscal year (to FY3/17 and FY3/18) and is based on the new series, growth measured on a GVA basis. Consensus numbers for calendar year countries are from Consensus Economics, otherwise the numbers are from Bloomberg.

Source: Consensus Economics, Bloomberg, Macquarie Research, October 2016

For 2017, we are

beneath consensus

on Canada,

Australia and Japan

We are above

consensus in our

2017 forecasts for

the US and most of

Asia

Macquarie Research The Global Macro Outlook

18 October 2016 12

In line with the continuation of moderate real and nominal global real GDP growth, The Long

Grinding Cycle, our interest rate forecasts are commensurately subdued. Please note that we

are forecasting the US 10-year bond yield to have a cycle high in 2018 of only 2.70%.

Fig 34 Macquarie’s interest rate forecasts

Year end Policy or cash rate (*) (%) 10-year bond yield (%) 2014 2015 2016 2017 2018 2014 2015 2016 2017 2018

US 0.00 0.25 0.50 1.00 1.50 2.17 2.27 1.90 2.30 2.70 Eurozone 0.05 0.05 0.00 0.00 0.00 0.54 0.63 0.50 1.00 1.50 Japan 0.07 0.04 0.00 0.00 0.00 0.33 0.27 -0.10 -0.10 0.20 UK 0.50 0.50 0.25 0.25 0.50 1.79 1.96 1.20 1.20 1.75 Canada 1.00 0.50 0.50 0.50 0.75 1.79 1.39 1.25 1.40 1.50 Australia 2.50 2.00 1.50 1.00 1.00 2.81 2.88 1.75 1.90 2.10 New Zealand 3.50 2.50 1.75 1.25 1.75 3.67 3.58 2.40 2.60 2.70

China 5.60 4.35 4.10 4.10 4.10 S. Korea 2.00 1.50 1.25 1.50 1.75 Taiwan 1.88 1.63 1.50 2.00 2.50 Indonesia 7.75 7.50 6.50 6.50 6.50 Malaysia 3.25 3.25 2.75 2.50 2.50 Singapore 0.50 0.88 1.50 1.80 2.00 Philippines 4.00 4.00 2.75 2.50 2.50 Thailand 2.00 1.50 1.50 1.75 2.25 India 8.00 6.75 6.25 6.00 6.00

South Africa 5.75 6.25 7.00 7.00 7.00

Note: (*) Policy or cash rate, US: Fed Funds rate, Eurozone: EMU Refi Rate, Japan: overnight call rate, UK: Repo rate, Canada: Cash rate, Australia: Cash rate, New Zealand: Official cash rate, China: 1-year working capital, South Korea: Overnight call rate, Taiwan: Official discount rate; HK: discount window base; Indonesia: 1-month SBI rate, Malaysia: Overnight policy rate, Singapore: 3-month interbank rate, Philippines: Reverse repo rate, Thailand: 14-day repo rate, India: Repo rate, South Africa: Repo rate

Source: Macquarie Research, October 2016

We are forecasting calendar year 2016 CPI of 1.3% YoY in the US, 0.4% YoY in the Euro-

zone, and 2.0% YoY in China: so moderate inflation, not deflation. In 2017, the US and

eurozone inflation forecasts are 2.5% and 1.6% respectively.

After a period of broad US$ strength in 2015, we believe individual currencies will at different

times pass their lows versus the US$. Whilst relative monetary policy stances will remain

important, resulting capital flows now have to exceed mounting current account surpluses in

Japan and the Eurozone (partially reflecting the falls in oil and other resource prices). On our

forecasts, the Yen passes its weakest point first (4Q 2015), and then the Euro (1Q 2017).

Fig 35 Macquarie’s CPI and currency forecasts

Year end CPI (%, YoY) Currency versus US$ (Year-end) 2014 2015 2016 2017 2018 2014 2015 2016 2017 2018

US 1.6 0.1 1.3 2.5 2.4 Eurozone 0.4 0.0 0.4 1.6 1.5 1.21 1.09 1.08 1.11 1.12 Japan 2.7 0.8 -0.1 0.3 0.5 119.8 120.41 105.00 101.00 97.00 UK 1.5 0.0 0.7 2.3 2.5 1.56 1.47 1.27 1.35 1.40 Canada 1.9 1.1 1.5 1.8 2.0 1.16 1.39 1.36 1.45 1.45 Australia 2.5 1.5 1.2 1.9 1.8 0.82 0.73 0.76 0.72 0.73 New Zealand 1.2 0.3 0.5 1.1 1.6 0.78 0.68 0.72 0.68 0.67

China 1.5 1.5 2.0 2.0 2.5 6.20 6.49 6.60 6.40 6.20 S. Korea 1.3 0.7 1.1 1.9 2.0 1099 1173 1130 1150 1130 Taiwan 1.2 -0.3 1.3 1.4 1.5 31.60 32.85 33.40 34.00 35.00 Hong Kong 4.4 3.0 2.5 2.0 2.2 7.75 7.75 7.80 7.80 7.80 Indonesia 6.4 6.4 4.1 4.9 5.0 12440 13795 13500 13700 13500 Malaysia 3.1 2.1 2.7 2.8 2.6 3.50 4.29 4.20 4.15 4.10 Singapore 1.0 -0.5 -0.3 1.0 1.4 1.31 1.42 1.37 1.35 1.33 Philippines 4.2 1.4 1.6 2.8 3.3 44.73 47.06 46.50 46.00 45.50 Thailand 1.9 -0.9 0.3 1.7 2.2 32.92 36.04 35.50 36.20 36.00 India 6.7 4.9 5.2 5.0 5.0 62.71 66.50 68.20 69.69 70.57

South Africa 6.1 4.6 6.5 5.5 5.5 11.57 15.50 14.50 14.50 14.00

Note: The currency forecasts are presented in the most common format. Normally, this is per US$, but exceptions where it is US$ per other currency include: the Euro, Sterling, Australia and NZ dollars

Source: Macquarie Research, October 2016

We forecast the US

10-year bond yield

to have a cycle high

in 2018 of only

2.70%

We are not

forecasting deflation

After a period of

broad US$ strength

in 2015, we believe

individual

currencies will at

different times reach

their lows versus

the US$

Whilst relative

monetary policy

stances will remain

important, resulting

capital flows now

have to exceed

mounting current

account surpluses

in Japan and the

Eurozone

On our forecasts the

Yen passes its

weakest point first,

(4Q 2015) and then

the Euro (1Q 2017)

Macquarie Research The Global Macro Outlook

18 October 2016 13

The latest Macquarie commodity team commodity price forecasts are below. Commentary

follows the table. The next page looks at oil, with comments on other commodities on the

subsequent pages.

Fig 36 Macquarie’s commodity price forecasts

2015 2016 2016 2016 2017 2017 2017 2018 2019 2020 2021

Unit CY CY Q3 Q4 Q1 Q2 CY CY CY CY CY LT $2016

Base Metals Copper $/tonne 5,503 4,693 4,772 4,600 4,500 4,650 4,563 4,413 4,650 5,188 6,100 5,900 Aluminium $/tonne 1,663 1,547 1,620 1,480 1,450 1,450 1,438 1,425 1,413 1,413 1,450 1,350 Zinc $/tonne 1,932 2,038 2,255 2,300 2,200 2,400 2,425 2,700 2,825 2,663 2,380 2,300 Nickel $/tonne 11,836 9,522 10,265 10,500 11,000 11,500 11,625 13,000 14,000 15,000 16,000 15,000 Lead $/tonne 1,786 1,819 1,873 1,940 1,910 1,960 2,003 2,190 2,085 1,945 1,928 1,950 Tin $/tonne 16,077 17,141 18,624 17,500 17,500 17,500 17,500 18,000 18,500 19,000 19,500 18,000 Steel and Raw Materials Iron ore - 62% Fe $/t CFR 56 53 59 50 52 52 50 47 50 60 60 60 Hard coking coal $/t FOB 102 107 93 170 140 115 121 115 120 125 125 105 Steel - World Export HRC

$/tonne 370 363 372 380 370 370 370 350 335 345 345 380

Energy Crude Oil - Brent $/barrel 52 44 45 52 56 62 61 68 73 75 77 68 Crude Oil - WTI $/barrel 49 43 44 49 51 57 56 62 67 69 71 63 Henry Hub Gas $/MMBTU 2.6 2.5 2.9 2.9 3.2 3.0 3.2 3.3 3.3 3.2 3.2 2.9 Thermal coal - Aus Spot $/t FOB 59 58 67 63 60 58 58 55 53 50 50 48 Uranium $/lb 37 28 26 27 29 29 29 31 34 37 40 43 Lithium carbonate $/t CFR

China 5,190 7,547 8,300 8,275 8,300 8,300 8,250 7,500 7,000 6,750 6,750 6,000

Precious Metals Gold $/oz 1,160 1,262 1,335 1,275 1,325 1,375 1,381 1,375 1,406 1,438 1,388 1,250 Silver $/oz 16 17 20 18 19 20 20 21 22 23 23 18 Platinum $/oz 1,053 1,000 1,085 1,000 1,025 1,050 1,094 1,219 1,331 1,363 1,325 1,400 Palladium $/oz 692 604 675 650 625 625 644 775 781 763 738 800 Agriculture MacPI 1997-

2000=100 149 148 145 152 153 154 155

Potash $/t FOB 303 247 220 225 225 220 221 230 240 250 250 280 Urea $/t FOB 273 195 184 190 220 200 203 200 200 210 215 240 Ammonia $/t FOB 385 231 204 185 215 225 223 230 230 230 245 250 Natural Rubber USc/kg 137 126 117 118 118 120 118 120 123 126 129 115 Others Alumina $/t FOB 301 236 234 235 250 250 248 240 223 223 230 225 Manganese ore $/mtu CIF 2.9 3.5 4.0 3.5 3.0 3.0 3.0 3.3 3.3 3.5 3.8 2.8 Ferrochrome (EU contract)

c/lb 107 96 98 110 100 105 103 100 105 110 110 105

Source: Macquarie Research, October 2016

Whilst the US Federal Reserve and their policies are regarded as the fulcrum of global capital

markets, the commodity complex provides a useful spyglass on global developments.

Based on a simple up/down ratio, 2016 is expected to be another challenging year of trying to

align supply with sluggish demand growth, Fig.37.

Fig 37 Macquarie commodity price forecasts, YoY simple up/down ratio

2015 2016 2017 2018 2019 2020 2021

YoY, number of forecasts up 2 8 16 15 16 17 12 YoY, number of forecasts down 23 19 10 11 6 6 5 YoY, number of forecasts unchanged 0 3 1 0 4 3 9

Note: The two commodity price rises in 2015 were uranium and potash

Source: Macquarie Research, October 2016

Macquarie Research The Global Macro Outlook

18 October 2016 14

Oil The oil supply and demand modelling undertaken by Vikas Dwivedi indicates that beyond short-term disruptions, crude remains on a path to structural rebalance.

Vikas continues to believe that the market will reach a more sustainable balance marked by

seasonally normal draws in 4Q16, driven by further U.S. onshore declines and continued

demand growth.

Fig 38 Oil demand remains highly correlated to global growth

Source: World Bank, BP Statistical, Macquarie Research, October 2016

Vikas’ crude price forecasts remains unchanged; believing that the price levels forecast at the

start of the year continue to remain appropriate given the global crude fundamental backdrop.

Vikas expects Brent prices to average $45/bbl in 2016, and WTI to average $42/bbl.

Beyond the current year, he expects Brent to average $61/bbl in 2017 and $68/bbl in 2018,

and for WTI to average $56/bbl and $62/bbl, respectively.

Fig 39 Annual Brent & WTI forecast

Source: Macquarie Research, Annual Price Forecasts, October 2016

Fig 40 Quarterly Brent and WTI forecast

Source: Macquarie Research, Bloomberg, October 2016

For more detail behind the above, please see 22 June 2016 Through the looking glass: stage

set for global crude rebalance and 30 September 2016 OPEC’s fuzzy agreement.

2016 2017 2018

Base Case $45 $61 $68

WTI Base Case $42 $56 $62

WTI - Brent ($3) ($5) ($6)

$68

($6)

Normalized Price

$74

3Q16E 4Q16E 1Q17E 2Q17E 3Q17E 4Q17E 1Q18E 2Q18E 3Q18E 4Q18E

Brent forecast $47 $52 $56 $62 $65 $62 $65 $67 $70 $69

WTI - Brent ($3) ($3) ($5) ($5) ($5) ($5) ($6) ($6) ($6) ($6)

WTI $45 $49 $51 $57 $60 $57 $59 $61 $64 $63

Consensus $46 $49 $51 $54 $56 $59 $61 $62 $62 $63

Forward Curve $51 $52 $52 $53 $53 $54 $54 $55 $55 $55

Brent vs. Cons $1 $3 $5 $9 $10 $3 $4 $5 $8 $6

Brent vs. Fwds ($4) $0 $4 $9 $12 $8 $11 $12 $15 $14

We expect Brent to

average $61/bbl in

2017 and $68/bbl

in 2018

Vikas continues to

believe that the

market will reach a

more sustainable

balance marked by

seasonally normal

draws in 4Q16,

driven by further

U.S. onshore

declines and

continued demand

growth

Macquarie Research The Global Macro Outlook

18 October 2016 15

Commodities If the first leg of the recovery in commodity prices this year was sentiment-driven, being a

realisation that China was not going to collapse and the Fed was not going to tighten

aggressively, the second has been based more on the fundamentals. For some, especially

the industrial-focused commodities, stronger demand growth has driven the delta. In others,

supply cuts have been overdone. The end result is similar. Prices across a broad range of

commodities have had to rise to invoke a positive supply reaction, the polar opposite of end-

2015. These are topics we explore further in our recent Commodities Compendium.

We are comfortable that, after a year-end dip, the first half of 2017 will see a continuation of

the factors that have assisted commodity markets in recent times, with manufacturing and

Chinese construction outperforming. Our confidence that January 2016 marked the nadir

continues to grow.

But to be clear, fundamentals do not point to any sustained inflationary bottlenecks ex raw

material constraints. The long-term challenges of overcapacity and lower industrial demand

growth than recent norms are still very much in place, while the semi-permanent state of low

interest rates means the ‘reset button’ of producer failures has essentially been removed,

particularly as governments become more and more involved.

Thus, if 2016 was the year of relief for commodity producers, then 2017 provides a window of

opportunity for sustainable strategy to be formed, as the long-term prognosis of weaker

economic growth has not changed. Commodity price inflation over 2016 has eased the

pressure on producer balance sheets, but growth options remain limited in the main. In both

metals and energy, we expect 2017 to mark a pick-up in industry capex and also a return to

cost inflation.

Fig 41 Current price levels are unlikely to yield further supply cuts

Fig 42 The 4Q hard coking coal contract rose over 100% QoQ

Source: Wood Mackenzie, CRU, Macquarie Research, October 2016 Source: TEX Report, Macquarie Research, October 2016

In oil, the agreement among OPEC members to cut production to a range between 32.5 and

33.0 MM BPD certainly stunned the market. The agreement, even if it is ratified at the

November 30th OPEC meeting and tightly executed, only changes our rebalancing base

marginally. It does however cut off the upwardly biased production skews that could have

stretched the rebalancing period out as far as one year beyond our mid-2017 base case. In

our assessment, the 33.0 MM BPD target is achievable and may turn out to be a smart move.

In a recent note we analysed scenarios below which allow the agreement to work. The deal

will have to (1) allow members which have ongoing supply disruptions to grow, (2) allow

weaker members to stay flat, (3) have buy-in from rich members for material production cuts,

and (4) have Russia participate. The risk to OPEC is that the desired price response may be

a needle threading exercise – not enough price action results in a market share giveaway and

too much price action accelerate shale growth, i.e. market share giveaway.

The coal markets remain a key area of focus. Notably, 4Q hard coking coal has settled at

$200/t FOB Australia – up over 100% QoQ. This level, while still slightly below current spot,

comes in above most expectations (our forecast was for $170/t) and marks the highest USD

settlement since 3Q12 and the highest in AUD since 2011.

0%

10%

20%

30%

40%

50%

60%

70%

80%

Mn O

re

Met C

oal

Therm

al

Co

al

Zin

c

Go

ld

PG

M B

asket

Alu

min

ium

Iro

n O

re

Co

pp

er

Ura

niu

m

Nic

kel

Proportion of supply losing money - cash basis

As of Jan 16 Current

20

0 22

52

09

22

53

30

31

52

85

23

52

10

22

51

70

16

51

72

14

51

52

14

31

20

12

01

19

11

71

10

93

89

81 84 93

20

00

50

100

150

200

250

300

350

2Q

10

3Q

10

4Q

10

1Q

11

2Q

11

3Q

11

4Q

11

1Q

12

2Q

12

3Q

12

4Q

12

1Q

13

2Q

13

3Q

13

4Q

13

1Q

14

2Q

14

3Q

14

4Q

14

1Q

15

2Q

15

3Q

15

4Q

15

1Q

16

2Q

16

3Q

16

4Q

16

$/t

, F

OB

Austr

alia

Premium hard coking coal settlements

If the first leg of the

recovery in

commodity prices

this year was

sentiment-driven,

being a realisation

that China was not

going to collapse

and the Fed was not

going to tighten

aggressively, the

second has been

based more on the

fundamentals

Macquarie Research The Global Macro Outlook

18 October 2016 16

The catalyst for tightness in the coal market has been the Chinese supply restrictions seen

this year. However, with prices now accelerating higher, these restrictions are being eased.

Prior to the October Golden Week holiday, the NDRC issued a notice that 791 coal mines that

met the “Level 1 safety standard” in 2015 would be allowed to lift their operating rate to their

previous 330-day registered capacity level rather than operate at the restricted 276-day

output level for the remainder of the year. In all, our industry contacts expect up to 900 mines

could lift output in 4Q16. The impact of these coal mines lifting output back to the full 330-day

output rate should be around 60–80mt of additional coal supply in 4Q alone, but this supply is

likely to be biased more to thermal coal than met. Nonetheless, we expect this supply

increment to result in lower coal prices for both thermal and met in the months ahead.

Agricultural commodity markets have underperformed other commodities since the start of

the year, dragged down by continued weakness in grains. Indeed, Macquarie’s proprietary

MacPI agricultural commodity index ended August at 143.1, just below end-December levels,

but with the staple grains component down 13.5% over the same period. While weather risks

may have been building into mid-year, they have since dissipated. As a result, we have now

seen four seasons in a row with close on perfect production, and with crops all but realised,

US ending stocks are set to be once again higher. With this, the pressures on agricultural

supply are increasing. Even in a low-interest-rate environment, farmers are struggling. The

potential for more widespread farmer bankruptcies in the US is rising, and while this will not

cause permanent supply reduction it may lead to a loss of planted area in 2017.

For the remainder of 2016, a combination of a likely Federal Reserve rate hike and the

standard 4Q Northern Hemisphere industrial slowdown does not bode well for commodity

prices. Already in October bullion prices have tumbled as a hike comes into view, while the

noticeable increase in long-term bond yields could mark the start of a structural shift which

may have large repercussions, something we considered here.

While improved Chinese confidence means the 2015 whiplash event and subsequent

demand vacuum is highly unlikely to be repeated, we expect steel and bulk commodities to

come under some pressure, while precious metals will also underperform. In contrast, we

believe US natural gas, nickel, alumina and nitrogen will outperform. Met coal is very much a

special situation, with acute supply constraint likely to be transient.

In the medium to longer term, supply remains a differentiating factor across commodity

markets. Exposure to those commodities for which demand growth will need to reincentivise

latent supply through price inflation is preferable, while exposure to those with true raw

material constraints is a must. On an 18-month view we are bullish on US natural gas, crude

oil, nickel, zinc, gold, silver and chrome from today’s levels.

We are concerned that the longer-term challenges of persistent overcapacity are

underappreciated for potash, alumina, aluminium and steel.

Fig 43 Positions of key mined/extracted commodities in the fundamental cycle – arrow shows 2-year progression

Source: Macquarie Research, October 2016

Strong Demand Push Demand destruction Market back in balance Strong supply grow th High stocks Stocks Draw ing Supply constraint

or deficit market Capex accelerating Capex peaking Stocks building Strong supply reaction Limited new supply Capex lagging

Price Acceleration Price peaking Prices falling Severe price decline Prices stablise at low level Prices stable Pricing to encourage supply

Manganese

Lead

Uranium

Thermal Coal

Met Coal

Iron Ore

Aluminium

Zinc

Copper

Nickel

Chrome

Palladium

Gold

Potash

Platinum

Tin

Oil

US Natural Gas

Silver

Bauxite

LNG

Diamonds

Nitrogen

Steel

Alumina

Lithium

Macquarie’s

proprietary MacPI

agricultural

commodity index

ended August at

143.1, just below

end-December

levels, but with the

staple grains

component down

13.5% over the

same period

Macquarie Research The Global Macro Outlook

18 October 2016 17

United States Economic activity appears to once again be expanding at an above potential pace following a

slower pace of growth around the turn of the year. In Fortress America – It’s go time: Growth

drags complete we highlighted that inventories and energy & mining investment were a

substantial headwind to growth, subtracting ~ 1.1 percentage points from GDP over the last

four quarters. These drags now look to have dissipated, a development that should lead to a

firmer underlying trend.

Further supporting this view is that the ISM manufacturing PMI has now shown expansion in

6 of the last 7 months, with particular strength in the forward-looking new orders component.

Additionally, readings on consumer spending have continued to be strong, supported by

persistent job gains and improving wage growth. With a personal savings rate that is 1.8 ppt

above its 2002-7 average, the consumer is well positioned to continue to support the outlook.

September’s employment report further solidified that the job market remains on firm footing.

Over the past 3 months job gains have averaged ~190k, a healthy rate that should dispel the

notion that the economy is slowing. However, employment gains are now showing signs of

moderating amidst a labour market that is close to full employment. Thus far in 2016 job gains

have averaged ~180k/month which is noticeably slower than the monthly pace of ~230k seen

in 2015.

We attribute the slowdown in job growth to reduced labour market slack as opposed to

decreased employment demand. Jobless claims remain at historically low levels while job

openings are at an all-time high, suggesting worker demand remains healthy. As unabsorbed

worker capacity increasingly diminishes we expect jobs gains to further slow to ~150k/month

through end-17, a pace nearly double what is required to further reduce slack. This should

continue to put upward pressure on wages, which have already shown clear signs of moving

higher particularly in the construction industry (Fig 44).

Most importantly, the outlook for residential investment remains strong despite a softer

reading in 2Q. It is low and rising as a share of GDP, a dynamic that insulates the economy

from any potential downturn. We believe that this area can rise at a double-digit pace for the

next 3-4 years, a thesis we outlined in Accelerating Housing, Macro Impact.

On the policy front, we believe that the Federal Reserve is poised to continue a rate hike

cycle that should prove gradual, cautious, and supportive of risk-taking. The pace of hikes is

likely to be, on average, 50bps per year until the upper end of the fed funds rate range

reaches our forecasted terminal level of 2%. We foresee this occurring in mid-2019. A key

input into our thesis is our belief that the neutral policy rate in the US is likely to remain at

present levels rather than increase over time. This will lead to a slower pace of rate hikes for

the duration of the cycle than the FOMC currently projects.

Fig 44 Construction wages are showing particular strength

Source: BLS, Macquarie Research, October 2016

0%

1%

2%

3%

4%

5%

6%

1995 1997 1999 2001 2003 2005 2007 2009 2011 2013 2015

YoY % change

YoY % change (3moMA)

Average hourly earnings of prod & nonsupervisory employees: construction

After subtracting ~

1.1 percentage

points from growth

over the past four

quarters, the drag

from inventories

and energy &

mining investment

looks complete

We expect

employment gains

to average

~150k/month

through end-17 as

the economy nears

full employment

The Fed is likely to

raise rates gradually

and to a lower level

than in previous

expansions

Macquarie Research The Global Macro Outlook

18 October 2016 18

China Recovery continued in September: China will release September and 3Q data on October

19. Thanks to the property market and price reflation, the economy continues to improve. For

September, industrial production (IP) growth could be stable at around 6.3% YoY. We expect

real GDP to grow 6.7% YoY in 3Q16, the same as in the previous two quarters. But nominal

GDP growth, which improved to 7.2% YoY in 1H16 from 6.4% in 2015, is set to pick up

further in 2H16 (see September data preview: Recovery on reflation and real estate).

PMIs suggest stable growth in Sep: The NBS manufacturing PMI came in flat at 50.4 in

Sep, which is the highest level since Nov 2014. Meanwhile, the Caixin PMI edged up slightly

to 50.1 from 50.0 in Aug. At this moment, the economy is supported by the property market

and price reflation, which has led to a rebound in corporate earnings. Industrial profits jumped

20% yoy in Aug, the fastest growth in three years. As such, the PBoC would postpone cutting

the interest rate. Rather, the focus has shifted to managing the financial risks in the bond and

property markets

A temporary triumph on capital outflows: The detailed 2Q16 Balance of Payment data

released last month gives us more information on the current state of capital outflows. It

shows that China’s FX reserves dropped by US$35bn in 2Q16, which is much improved from

the US$100+bn decline in each of the prior three quarters. Meanwhile, hot money outflows

started to stall in 2Q16 (Fig 45). It’s in line with our previous analysis of capital flows based on

the 2015 BoP data (Dissecting China’s capital outflows in 2015 ). Essentially, because hot

money has been largely exhausted after two years of outflows, also capital controls are more

effective for domestic money than foreign money, China’s capital outflows pressure would be

much eased in 2016. Therefore, the market fears on capital outflows earlier this year are

overdone. That said, for the PBoC, it’s just a triumph of a battle, not a war, because the

slowdown of capital outflows has been achieved with tightened capital controls, which run

against China’s long-term goal of the RMB internationalization and Capital Account

openness.

The next battle for the PBoC: Last month, we published a report on the long-term outlook

for the RMB (How to think about the RMB?). Against the consensus, which expects the RMB

to have a trend depreciation, we forecast the USD/CNY to end 2017 at 6.4 and appreciate

more in the long run. The report has received a lot of push-back, just like many of our reports

related to the RMB. For instance, on the same day of the RMB devaluation last August, we

forecasted that the depreciation would be less than 5% from then on to the year-end (link). In

our 2016 outlook (link), we forecasted the USD/CNY to end 2016 at 6.6. Earlier this year, we

forecasted that capital outflows are easily manageable as hot money has largely gone (link).

Fig 45 Carry trade unwinding reversed in 2Q16

Source: CEIC, Macquarie Research, October 2016

-150

-100

-50

0

50

100

150

Mar-

09

Jun

-09

Sep

-09

Dec-0

9

Mar-

10

Jun

-10

Sep

-10

Dec-1

0

Mar-

11

Jun

-11

Sep

-11

Dec-1

1

Mar-

12

Jun

-12

Sep

-12

Dec-1

2

Mar-

13

Jun

-13

Sep

-13

Dec-1

3

Mar-

14

Jun

-14

Sep

-14

Dec-1

4

Mar-

15

Jun

-15

Sep

-15

Dec-1

5

Mar-

16

Jun

-16

Capital flows due to carry tradeUSD bn

Outflows

Inflows (1Q09-2Q14)US$742bn

Outflows (3Q14-1Q16)US$452bn

Recovery continued

in Sep

Capital outflows

have slowed

We expect RMB to

appreciate in 2017

Macquarie Research The Global Macro Outlook

18 October 2016 19

Admittedly, the dominant expectation is a trend depreciation for the RMB. With that, the RMB

internationalization has backtracked as the RMB deposits in HK have already dropped to

RMB670bn from the peak of RMB1tn in Dec 2014. For the Chinese government, which has

spent tons of effort on things like the SDR and AIIB, it has so much to lose from the

termination of RMB internationalization, which is also important to One-Belt-One-Road.

Therefore, the next target for the PBoC has to be the prevalent depreciation expectations.

How to win the battle with depreciation expectation? Over the past year, the RMB has

had a slow depreciation and limited volatility. Since most people are trend-followers, no

wonder the depreciation expectation is so prevalent at this moment. To win the battle with

depreciation expectation, the PBoC needs a new strategy, which is to guide the RMB

stronger while increasing the volatility. Under the new strategy, the market knows the long-

term direction of the RMB but not the short-term trading band. Therefore, when the RMB falls

to some extent, speculators would expect it to reverse and start buying. By doing so, the

PBoC essentially changes the one-way expectation by winning allies among market

participants. Over time, the PBoC could gradually increase the band and ultimately let the

RMB be determined by market forces. To be sure, at the beginning of the year when lots of

people forecasted a one-off depreciation, we argued that the best strategy for the PBoC in

2016 is a stable RMB (link), because at that time the credibility for the PBoC was not enough

and capital outflow pressure was high. It turns out that a stable RMB is also the actual

strategy adopted by the PBoC. However, the situation has changed as capital flows have

eased. So it’s time to move on.

Property prices and exchange rate: One push-back to our positive RMB view is that the

PBoC has to depreciate the currency to keep property prices near the current level. We agree

that rising home prices could cause more Chinese residents to sell their property in China and

buy foreign assets. However, there are other and probably more important channels to

influence the RMB, such as trade balances and economic growth. That’s why China’s home

prices have increased rapidly over the past 15 years but the RMB has also appreciated.

Moreover, while in this round of property up-cycle, home prices do increase quickly in certain

cities, but the rise is not a broad-based one (Fig 46). Over the past 12 months, 48 out of the

70 biggest cities had home price growth of less than 5%. As such, if the property market

could cool down in the next six months as we are expecting, the negative impact on the RMB

will be limited.

More cities introducing property curbs: Over the past couple of weeks, more than a dozen

cities tightened their property measures. It’s not surprising at all, as China had four such

property short-cycles in the past decade. This is just the fifth one. According to past

experience, the sector could cool down in 1H17 and the rate-cutting cycle would resume

around mid-2017 to support the economy. But for 4Q16, the property sector should remain

supportive, as developers are quickening the pace of construction after the strong sales in the

past few months.

Fig 46 Home prices increase mainly in top cities

Source: CEIC, Macquarie Research, October 2016

100

110

120

130

140

150

160

170

180

190

Feb-1

1

Aug

-11

Feb-1

2

Aug

-12

Feb-1

3

Aug

-13

Feb-1

4

Aug

-14

Feb-1

5

Aug

-15

Feb-1

6

Aug

-16

Tier 1 Tier 2 Tier 3

2010=100

More volatility for

RMB is needed

Limited impact of

property market on

RMB

Property sector to

cool down in 2017

Macquarie Research The Global Macro Outlook

18 October 2016 20

Eurozone The Euro-zone economy continues its recent trend of steady but slow growth. We see some

darker clouds on the horizon however from higher oil prices and the collapse in Sterling.

Economic data in the last month has been mixed. The PMI surveys remain gloomy - in

September the Eurozone composite was just 52.6, its lowest since January 2015, and

averaged over the quarter pointing to slower GDP than 2Q’s 0.3%. But the PMIs look a little

strange, with a very weak Germany services sector the main drag. In contrast the European

Commission sentiment indicator in September saw its highest since January 2016.

Both surveys agree the industrial sector has improved. The manufacturing PMI rose to 52.6 in

September, its best in three months. Industrial output gained 1.6% MoM, and over the quarter

as whole - assuming a flat September - will eke out a modest 0.4% QoQ growth. In the past

this has been consistent with our forecast for GDP of around 0.3% QoQ.

Fig 47 Eurozone IP growth, QoQ (assuming Sep flat) Fig 48 Oil to take toll on buoyant retail sector, % YoY

Source: Eurostat, Macquarie Research, October 2016 Source: Macrobond, Macquarie Research, October 2016

Two new concerns on the growth front are coming in to view. The first is the higher oil price

and the impact it will have on consumer incomes. From being down 50% YoY in the middle of

2015, oil is now higher YoY, and if the current euro price is maintained will be up 30% YoY in

1Q. We think this is likely to see retail sales growth slow, something that we have already

seen initial signs of (Fig.48).

Second, Brexit. The recession in the UK many forecast hasn’t materialised, and as such our

expectation of only a modest impact on the Eurozone economic is playing out. But a new

problem is the steep devaluation of Sterling against the euro. There is a good correlation

between the exchange rate and Eurozone exports to the UK, and if the current devaluation is

sustained history suggests imports might fall 15% - €3bn a month. This is not a huge amount

in the context of a €10 trillion economy. But it is a fair amount in the context of a 1.5% growth

rate. We think it means Eurozone GDP will be a below consensus 1.4% in 2017, and the euro

will weaken against Sterling.

This brings us onto the ECB, and the thorny issue of its QE programme expiring in March.

Ahead of its October and - more importantly - December meetings the usual series of press

leaks about policy have started. Some excitement came from a press report that the bank

was considering ‘tapering’, but a closer reading suggests policymakers were only saying

when the time comes to end QE they would ‘taper’, rather than do a hard stop. We think that

time is a long way off (see “Timing the exit from unconventional monetary policies: the ECB &

BOJ) and December is likely to see the ECB announce an extension plus changes to its rules

on eligibility. It remains debatable whether the ECB should have started QE; we see no

reason why they should now stop.

Survey data mixed,

IP improving

Oil and Sterling

present new

headwinds

ECB will not taper

Macquarie Research The Global Macro Outlook

18 October 2016 21

United Kingdom Sterling is becoming an issue. The UK currency suffered a torrid time in the wake of a speech

by the UK Prime Minister, Theresa May, on 2 October putting some flesh on how the UK

government plans to exit from the European Union (EU). By 13 October it had fallen 4%

against the euro and 6% against the dollar, against the latter hitting repeated 31-yr lows.

The Chancellor (finance minister) Phillip Hammond attributed the weakness to financial

markets only now realising the UK really was going to leave the EU. But May’s

announcement that the UK would by March 2017 file Article 50 to start the two-year process

of leaving was not that remarkable (if at the earlier end of consensus).

We see two more plausible reasons for sterling’s slump. First, the extent of the powers the

government wants to take back from the EU - basically all of them (May cited the need to

control immigration, prevent the ECJ having a sway in the UK and even the right to ‘label our

food’) means Single Market membership is a long shot, and being outside will hit trade.

Second, the government has radical plans for what it wants to do with that power, with the PM

in a second speech promised a ‘revolution’, outlining a more interventionist economic policy

with politics such as worker board representation. For good measure she added a critique of

the side-effects of the Bank of England’s cheap money policy. If she is serious then a weaker

currency is likely to be a feature, not a fault.

But how serious is she? The remarks came at a party conference, not the most reliable guide,

and a number of clarifications have since been made, suggesting there is still much left

undecided about both Brexit and future economic policy. Sterling is probably due a bounce -

something which should be aided by a record short-position on the CME futures market.

Fig 49 Sterling v USD/EUR/BoE Index, 1995 = 100

Fig 50 UK core goods inflation (lagged 12m) v sterling, % YoY

Source: Macrobond, Markit, Macquarie Research, September 2016 Source: ONS, Macquarie Research, September 2016

That said, FX markets are not so prone to be being ‘too short’ - after all natural longs and

shorts are so large - and there seems little reason to expect a quick strengthening while so

much uncertainty prevails. Neither the government nor Bank of England officials seem too

concerned. The question that now arises is how the sterling devaluation will start to feed into

the real economy.

The bad news will come from inflation, and down the line consumer spending. The headline

rate was set to rise sharply on the back of the higher oil price, and now imported food, but

even the core rate will be affected – Fig.50 shows a good correlation between the change in

Sterling on a YoY basis and that index lagged 12 months. Market inflation measures are

rising sharply - the 5yr implied rate reached 3%, its highest in 15months.

The good news should be a better economy. Oxford Economics’ global model suggests a 5%

fall in Sterling adds about 0.1% QoQ to GDP growth. Of course if FX markets are selling

Sterling on fears of lower growth this might be offset by other factors, but very short-term we

raise our GDP forecasts modestly.

Trade and the

economy threaten

Sterling

Inflation and growth

to be boosted…at

least in the

short-term

Macquarie Research The Global Macro Outlook

18 October 2016 22

Japan Our real GDP growth forecasts remain anaemic, with modest contributions expected from

consumption and net exports.

Fig 51 Japan: key macroeconomic forecasts

CY11 CY12 CY13 CY14 CY15 CY16E CY17E CY18E CY19E

GDP (YoY, %) -0.5 1.7 1.6 -0.1 0.6 0.4 0.6 0.7 0.8 CPI (YoY, %) -0.3 0.0 0.4 2.7 0.8 -0.1 0.3 0.5 0.9 (**) Overnight call rate (*) 0.1 0.1 0.0 0.1 0.0 0.0 0.0 0.0 0.0 10-year JGB (*) 0.99 0.79 0.74 0.3 0.3 -0.1 -0.1 0.2 0.3 ¥/$ (*) 77.6 86.3 105.4 119.8 120.4 105 101 97 95 Note: CPI is the headline CPI ex fresh foods. (*): per period end, Macquarie forecasts. (**) The consumption tax rate increase to 10% from 8% is now scheduled for October 2019

Source: Bloomberg, Macquarie Research, September 2016