Global Smart Water Market 'Unearthing the REAL Value of Water ...

29

Global Smart Water Market ‘Unearthing the REAL Value of Water and the Industry’ Presented at the Tekes Seminar on BioRefine and Water on 27 th November 2012 at the Marina Congress Center in Helsinki By Fredrick Royan – Research Director, Global Environment (Water) Markets [email protected]

Transcript of Global Smart Water Market 'Unearthing the REAL Value of Water ...

Global Smart Water Market

‘Unearthing the REAL Value of Water and the Industry’

Presented at the Tekes Seminar on BioRefine and Water on 27th November 2012 at the Marina Congress Center in Helsinki

By

Fredrick Royan – Research Director, Global Environment (Water) Markets

Agenda

2

About Frost & Sullivan

Global Water Market – Key Data and Mega Trend Drivers

Key Challenges of the Global Water Industry

Smart is the New Green

Process and operational efficiency improvement drivers

Landscape of the Global Smart Water Market

Market opportunities in the Global Smart Water Market

Market Segment Hot-spots

Regional Hot-spots

Illustrate the business case of Smart Water Solutions with project

examples

Highlight the Competitive Landscape, Business Models and related

opportunities for Finnish Companies

The Frost & Sullivan Story

3

Pioneered Emerging Market & Technology Research

• Global Footprint Begins

• Country Economic Research

• Market & Technical Research

• Best Practice Career Training

• MindXChange Events

Partnership Relationship with Clients

• Growth Partnership Services

• GIL Global Events

• GIL University

• Growth Team Membership™

• Growth Consulting

Visionary Innovation

• Mega Trends Research

• CEO 360 Visionary Perspective

• GIL Think Tanks

• GIL Global Community

• Communities of Practice

Our Industry Coverage

4

Aerospace & Defense Measurement & Instrumentation

Information & Communication

Technologies

Healthcare Environment & Building Technologies

Energy & Power Systems

Chemicals, Materials & Food

Electronics & Security

Industrial Automation & Process Control

Automotive Transportation & Logistics

Consumer Technologies

Minerals & Mining

Megatrends provide a big lens when evaluating

future growth opportunity areas for Smart Water

5

$ 425 Billion

Total Global Water Market Value

Key Global Water Growth Drivers

International

Agency

Environment

Protection

Agencies

Business &

Financial

Agencies

Soci

al &

Eco

no

mic

al

Rapid

Population

Growth &

Urbanisation

Water Quality &

Public Health

Water Supply &

Sanitation

Needs of Remote

Communities Ec

olo

gic

al

Carbon

footprint

Storm/Flood

water

Management

Water

Stress/Droughts

Po

litic

al &

Fin

an

cia

l

Construction

Technical engineering & design

Operations & maintenance

Chemicals supply

Technology/equipment supply

R & D and piloting

Water management

Ke

y a

ctivitie

s

acro

ss th

e v

alu

e

ch

ain

Top 10 Challenges of the Global Water Market

6

Institutional

Capacity and

Resources

Governance and

Accountability

Water Resource

Availability &

Water-Energy Nexus

Public Health – Water

Quality, Access to

Sanitation and Safe

Disposal

Sustainability of

Water Utilities and

Cities Risk in Water Intensive

Industry and Global Trade

Top 10 Global

Water Market

Challenges

Source: Frost & Sullivan

Relatively High

Capex and Opex

Population Growth

and Urbanisation

Climate Change

and Extreme

Weather Events

VALUE of Water and Non-

revenue Water(NRW)

$425 Billion Global Water Market by Segments Mega Trends Influencing Technology Innovation in Global Water Market

Segments

$246 Billion

$ 80 Billion

$32 Billion

$35 Billion

$17 Billion

$15 Billion

Mega Trends of Value Chain Integration and Industry Convergence is set to combine

Treatment technologies, Chemicals and Process Control & Automation into a combined

segment of SOLUTIONS

Water & Wastewater Utilities

Design & Engineering,

Maintenance and Monitoring

Services and Operation Services

Build Infrastructure

Water & Wastewater

Treatment Technologies

Chemicals

Process Control &

Automation

New Segment of Smart Solutions is a Key Enabler in

Unearthing the VALUE of the Water Industry

8

Value Chain of the Water Industry with Representative Sample of Industry Participants

Smart Water Analytics, Meters and Software Companies

Design & Engineering Companies

Process Automation and Control

Chemicals & Materials

O&M Companies

Treatment Technology

Water Utilities

Industries

Mega Trend – Smart is the New Green

9

Smart Water Solutions are Set to Revolutionise

Management Methods Across the Water Cycle

10

‘S” Governance

‘S’ City Planning

‘S’ Water

‘S’ Business

‘S’ ICT

‘S’ Mobility

‘S’ Citizen

‘S’ Buildings

Source: Frost & Sullivan

Real time monitoring and management of Services along the Water Cycle

Data Analysis and Exchange

Future Smart Water Grid

Smart Water eters

Smart alves and ipes

Smart Water uality

Monitors

Smart P mps

Note: Image was adapted from UK Drinking Water Inspectorate. Source: Frost & Sullivan analysis.

Sewage Treatment

Factories

Sea River

Reservoir

Homes and Businesses

Water Treatment Works

Ground Water Data

Concentrator and Communications

Smart Water – Key Drivers

12

Economic -Cost of energy

-Water use inefficiencies

Technological -ICT integration

-Increased granularity

-Exposed relationships

Social -Urbanization

-Globalization

-Access to Information

and Water

Environmental -Water scarcity

-Resilience to

climate change

-Increased demand

-Carbon footprints

Political -Efficiency

-Innovation

-Accountability

-Sustainability

‘S” Governance

‘S’ City Planning

‘S’ Water

‘S’ Business

‘S’ ICT

‘S’ Mobility

‘S’ Citizen

‘S’ Buildings

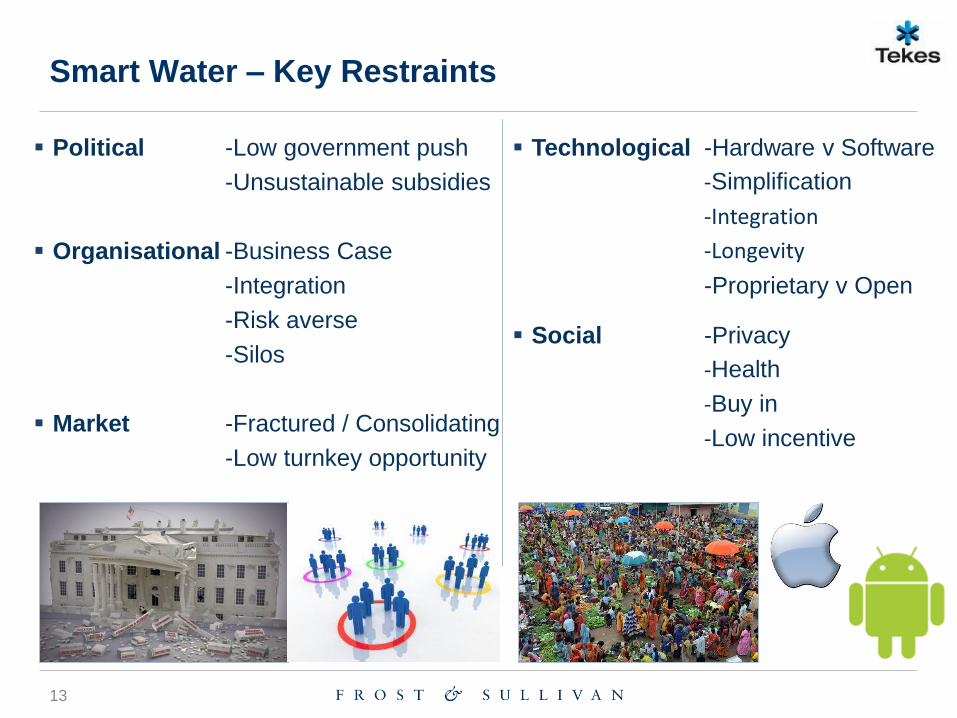

Smart Water – Key Restraints

13

Political -Low government push

-Unsustainable subsidies

Organisational -Business Case

-Integration

-Risk averse

-Silos

Market -Fractured / Consolidating

-Low turnkey opportunity

Technological -Hardware v Software

-Simplification

-Integration

-Longevity

-Proprietary v Open

Social -Privacy

-Health

-Buy in

-Low incentive

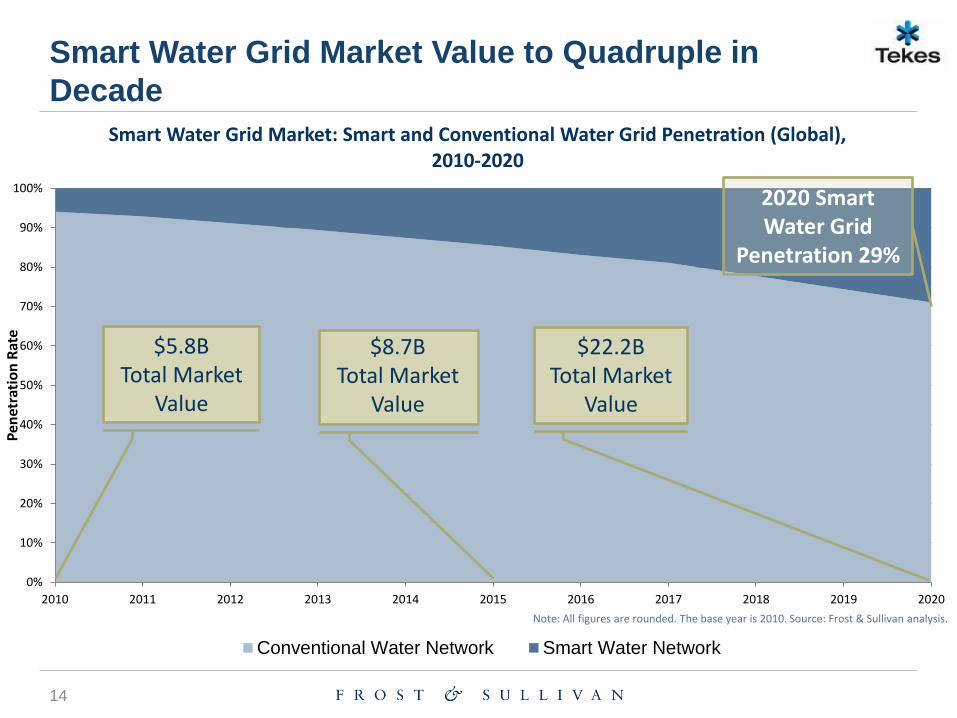

Smart Water Grid Market Value to Quadruple in

Decade

14

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

Pen

etra

tio

n R

ate

Smart Water Grid Market: Smart and Conventional Water Grid Penetration (Global), 2010-2020

Conventional Water Network Smart Water Network

$5.8B Total Market

Value

$22.2B Total Market

Value

$8.7B Total Market

Value

2020 Smart Water Grid

Penetration 29%

Note: All figures are rounded. The base year is 2010. Source: Frost & Sullivan analysis.

Smart Water – Market Landscape and Key Segments

15

Combined

Analytical

Control

and

Automation

System

(expected)

Water Utilities

Design and

Engineering

Services

$0.34 billion

Automation

and Control

$1.05 billion

Smart Water

Infrastructure (including

Communications)

$3.38 billion

Analytical

Software

$1.03 billion

Hard

ware

S

oftw

are

Pumps Pipes and Valves Data Loggers

Radio Frequency

Mesh

Radio Frequency

Point-to-Point

Cellular Fibre Optic

Power Line

Communication

Broadband

Hydraulic

Modelling

Grid

Monitoring

Prediction

Analysis

Asset

Management

Queries and

Remote Upgrades

Cyb

er S

ecu

rity

Meter Data

Management

Event

Prioritisation

Bespoke

Reports

Remote Pressure Control

AMR/AMI

Meters Sensors

Remote Energy Generators

SCADA

Programmable Logic Controller

Human Machine Interface

Segment and

Market Size, 2010

Distributed Control System

Source: Frost & Sullivan analysis.

Smart Water Market – Hot-Spots by Market Segment

16

Smart Water Infrastructure, $3.38

billion

Automation and Control, $1.05 billion

ICT, Software and Analytics, $1.03 billion

Design and Engineering Services, $0.34 billion

0,00

0,50

1,00

1,50

2,00

2,50

3,00

3,50

4,00

0,0 5,0 10,0 15,0 20,0 25,0 30,0

20

10

Mar

ket

Size

($

Bill

ion

)

CAGR (%), 2010-2020

Smart Water Grid Market: Vertical Market Attractiveness by Segment (Global), 2010-2020

Note: Size of bubble indicates degree of market share. All figures are rounded. The base year is 2010. Source: Frost & Sullivan analysis. .

Smart Water Market – Hot-Spots by Regional

Segments

17

North America, $2.42 billion

Europe, $1.68 billion

APAC, $0.82 billion

LatAm, $0.33 billion

MEA, $0.54 billion

0,00

0,50

1,00

1,50

2,00

2,50

3,00

0,0 5,0 10,0 15,0 20,0 25,0

20

10

Mar

ket

Size

($

Bill

ion

)

CAGR (%), 2010-2020

Smart Water Grid Market: Regional Attractiveness by Region (Global), 2010-2020

Note: Size of bubble indicates degree of market share. All figures are rounded. The base year is 2010. Source: Frost & Sullivan analysis. .

2020 Smart Water Meter Penetration in Europe – 52%

18

0

40 000

80 000

120 000

160 000

200 000

240 000

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2030

Un

its

('0

00

)

Smart Water Meter Market Penetration, 2007 - 2020, 2030 (Europe)

Households ('000) Water Meters ('000) Smart Water Meters ('000)

$1.2B

Total Market

Value

$2.6B

Total Market

Value

$7.8B

Total Market

Value

*Based on predicted scenario

2020 Smart Water Meter Market in Europe – Network

Management is likely to be the major contributor to

the market growth

19

Smart Water Meter Manufacturers,

$311.1 m

Meter Installers, $163.8 m

Network & Data Management, $744.0 m

0,0

5,0

10,0

15,0

20,0

25,0

30,0

35,0

40,0

0,0 10,0 20,0 30,0 40,0 50,0 60,0 70,0 80,0

Gro

wth

Ra

te, 2

01

0-2

02

0 (

%)

Market Share, 2010 (%)

Smart Water Metering Market: Market Attractiveness by Vertical Market (Europe), 2010-2020

Note: Bubble size and figures adjacent bubble name refers to market size in $ million for 2010. All figures are rounded. The base year is 2010.

Source: Frost & Sullivan analysis.

Smart Water Management to bring Paradigm Shift as

Traditional Practices Overhauled for ICT-enabled Abilities

20

Departmentalized Water Utility Structure

Integrated through new data and information communication

...From

Responsive Customer

Service Proactive

Reactionary Maintenance

and Repair Pre-emptive

Set Rates Billing

Based on Accurate Consumption Levels

Hands-on System Management

Remote fixes and prioritized call-outs

Manual Data Collection Automated

Inefficient Energy Consumption Optimized

...To

Source: Frost & Sullivan analysis.

Project Example – Global Water in the US

21

Source: Global Water

Project Example – Takadu’s Web Interface for Utilities

22

Source: Takadu

Complex Smart Water Universe – Relationships

Between Players will be Crucial to Future

Development

23

Utilities

Communications

Smart Analytics

Automation and Control

Design and Engineering Smart Hardware

Smart Water Market – Development Areas

24

Source: Google Images

Smart Irrigation and Agriculture

Smart Ultrapure Water

Smart Water Supply Management Smart Water Distribution

Management

Smart Wastewater Management

Smart Combined Sewer Overflows

Source: greatlakes.org

Source: usa.siemens.com

Source: organo.co.jp

Source: treehugger.com

Source: agreenstarlandscape.com

Source: precisionmeters.co.za

Smart Water Supply, Wastewater Management,

Recycling and Discharge Metering to Witness

Continued Revenue Growth

25

There are existing related market opportunities outside of the direct smart water grid and smart water metering markets:

Smart Water Resource Management

Smart Wastewater

Both hardware and software can drive revenue. Software with annual fees and servicing contracts, however, can ensure consistent and higher revenue.

• Drainage and runoff monitoring • Water harvesting • Reservoir monitoring • Water resource reallocation

• Water discharge metering • Water discharge quality • Water treatment, reuse and recycling

Sou

rce:

ow

fp.o

uce

.ox.

ac.u

k

Sou

rce:

vo

lcan

oes

.usg

s.go

v

Source: Frost & Sullivan analysis.

Mapping of a Few Finnish Companies in the Global

Smart Grid Market Landscape and Sample of

Competitors/Customers

26

Design and

Engineering

Services $0.34 billion

Analytical

Software $1.03

billion

Automation

and Control

$1.05 billion

Smart Water

Infrastructure

(including

Communicatio

ns)

$3.38 billion

Combined

Analytical

Control

and

Automation

System

(expected)

Programmable Logic Controller, Distributed Control System, Human Machine

Interface, SCADA

Radio Frequency Mesh, Radio Frequency Point-to-Point, Power Line

Communication, Cellular, Fibre Optic, Broadband

Sensors, Pumps, AMR/AMI Meters, Pipes and Valves, Remote Energy Generators, Data loggers, etc

Hydraullic Modelling, Grid Monitoring, Prediction Analysis, Queries and Remote

Upgrades, AMR/AMI Metering, asset management, Event Prioritisation, Bespoke

reports, etc

Hard

ware

S

oftw

are

Cyb

er S

ecu

rity

Segment and

Market Size in 2010

Source: Frost & Sullivan analysis.

High Level of Industrial Convergence and Movement

in the Smart Water Grid Market

27

Smart

Water

Meters

Engineering

and Design

Firms

Telemetry

Smart Pumps,

Pipes and

Valves

Software and

Analytic

Firms

ICT,

Automation

and Control

Smart Water

Meters Active Unlikely Active Likely Active Possible

Engineering and

Design Firms Unlikely Active Possible Unlikely Possible Possible

Telemetry Possible Unlikely Active Possible Active Possible

Smart Pumps,

Pipes and Valves Possible Unlikely Active Active Active Possible

Software and

Analytic Firms Unlikely Unlikely Unlikely Unlikely Active Active

ICT, Automation

and Control Possible Active Active Possible Active Active

Vertical Market

Integration

Source: Frost & Sullivan analysis.

Smart Water Grid Market: Future Business Models by Vertical Market (Global), 2012

Key Conclusions

28

• Water Utilities see an opportunity of Unearthing the Value of the ICT

infrastructure especially in the water supply networks

• Cost Recovery Based Water Tariffs will be key Enablers of Smart Water

especially in the high potential emerging markets

• The Global Water Industry is set to strongly benefit from the current trend of

industry convergence(Ex. Xylem acquiring YSI) to quench the technology thirst

of the Water Sector

• Smart Water solutions deliver tangible benefits and addresses key

inadequacies and inefficiencies of the Water Industry

• Global Challenge of Water Stress has transformed Smart Water from a Virtual

solution to a REAL and urgent need for the Water Industry

Questions?

29

Thank you for listening