Global petrochemical industry outlook shifting trade · PDF fileGlobal petrochemical industry...

42

Page 1 Macquarie Research is a division of Macquarie Group Limited, an affiliate and parent company of Macquarie Capital (USA) Inc., a registered broker - dealer and member of The Financial Industry Regulatory Authority (“FINRA”). All transactions by U.S. investors involving securities discussed in this report must be effected through Macquarie Capital (USA) Inc., which assumes responsibility in the U.S. for the contents of this report. Please read Disclaimer on Page 38-42 Global petrochemical industry outlook – shifting trade flows

Transcript of Global petrochemical industry outlook shifting trade · PDF fileGlobal petrochemical industry...

Page 1

Macquarie Research is a division of Macquarie Group Limited, an affiliate and parent company of Macquarie Capital (USA) Inc., a registered broker - dealer and

member of The Financial Industry Regulatory Authority (“FINRA”). All transactions by U.S. investors involving securities discussed in this report must be effected

through Macquarie Capital (USA) Inc., which assumes responsibility in the U.S. for the contents of this report.

Please read Disclaimer on Page 38-42

Global petrochemical industry outlook

– shifting trade flows

Page 2

Macquarie offers commodities expertise – a bit of background on us

30+ years in metals

markets, one of the

longest track records

globally

Over $US1 billion of

working capital

financing for

commodity companies

Trader and physical

supplier of natural gas,

LNG, power, oil, coal,

ethanol, grains and

freight

Unique ability to price

energy physical

products based on oil

indexation, volume

swing, tolling and load

shapes

Winner of the

Commodity Business

Awards 2011 & 2012 –

Excellency in Softs and

Agricultural Markets

Macquarie enters into

a supply & offtake

agreement with NARL

Refinery, a KNOC

company

Leading provider of

agricultural hedging

products

#4 physical gas

marketer in North

America, the highest-

ranked non-producer 1

Page 3

A macro outlook on the petrochemical industry –

gauging demand

Page 4 Source: Macquarie Capital (USA), September 2013

We forecast rising global economic health

-1%

0%

1%

2%

3%

4%

5%

6%

7%

8%

World Real GDP (y/y)

US Real GDP (y/y)

OECD Real GDP (y/y)

Euro zone Real GDP

(y/y)

Total Asia (ex JPN) Real

GDP (y/y)

SE Asia Real GDP (y/y)

NE Asia Real GDP (y/y)

China Real GDP (y/y)

Brazil Real GDP (y/y)

Global GDP Growth Estimates

2012 2013E 2014E

Page 5 Source: Macquarie Capital (USA), September 2013

We forecast rising global economic health

-2%

-1%

0%

1%

2%

3%

4%

5%

6%

7%

8%

World Real GDP US Real GDP OECD Real GDP Euro zone Real GDP Total Asia (ex JPN) Real GDP

China Real GDP

2013 GDP Estimates

2013 LTM 2013 YTD 2013E 4Q13E

Page 6

A macro outlook on the petrochemical industry – a

look at the cost landscape

Page 7 Source: IHS, Macquarie Capital (USA), September 2013

Oil-to-gas ratio likely to remain elevated

0x

10x

20x

30x

40x

50x

19992000

20012002

20032004

20052006

20072008

20092010

20112012

2013E

2014E

2015E

Macquarie - Predicted Oil/Gas Ratio

Page 8 Source: IHS, Macquarie Capital (USA), September 2013

Global Cost Setting – Advantage USA

-

200

400

600

800

1,000

1,200

0 20 40 60 80 100 120 140 160 180

20122007

North East Asia

Middle East Ethane

Middle East Avg

Alberta Ethane

US Ethane

US Avg

South East AsiaWestern Europe Avg

North East Asia

Middle East Avg

South East Asia

US AvgWestern Europe Avg

Ethylene Production Costs,

US$/MT

Cumulative Ethylene Capacity, million MT

2016E

US Ethane

US Avg

Page 9

Ethylene cash costs – North America remains highly favorable

Source: IHS, Macquarie Capital (USA), September 2013

0

200

400

600

800

1000

1200

1400

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013E 2014E

Regional Cash Costs (US$/MT)

North America Northeast Asia Southeast Asia West Europe

North American cash costs have dropped 65% since 2008

Page 10 Source: Bloomberg, Macquarie Capital (USA), September 2013

North American ethane prices have de-coupled from oil

$0

$2

$4

$6

$8

$10

$12

$14

0

20

40

60

80

100

120

140

1Q

02

3Q

02

1Q

03

3Q

03

1Q

04

3Q

04

1Q

05

3Q

05

1Q

06

3Q

06

1Q

07

3Q

07

1Q

08

3Q

08

1Q

09

3Q

09

1Q

10

3Q

10

1Q

11

3Q

11

1Q

12

3Q

12

1Q

13

Brent ($/bl) - LHS Ethane (c/gal) - LHS Natural Gas ($/mmbtu) - RHS

Ethane has decoupled from crude

$0

$2

$4

$6

$8

$10

$12

$14

0

20

40

60

80

100

120

140

160

180

1Q

02

3Q

02

1Q

03

3Q

03

1Q

04

3Q

04

1Q

05

3Q

05

1Q

06

3Q

06

1Q

07

3Q

07

1Q

08

3Q

08

1Q

09

3Q

09

1Q

10

3Q

10

1Q

11

3Q

11

1Q

12

3Q

12

1Q

13

Brent ($/bl) - LHS Propane (c/gal) - LHS Natural Gas ($/mmbtu) - RHS

Propane has also fallen sharply, towards nat. gas

Page 11 Source: Macquarie Capital (USA), September 2013

US ethane production poised to rise further, sharply…

Page 12

Ethylene margins – a regional outlook

Source: IHS, Macquarie Capital (USA), September 2013

0

200

400

600

800

1000

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Regional Ethylene Margins (US$/MT)

North America NorthEast Asia SouthEast Asia Western Europe

0

100

200

300

400

500

600

North America NorthEast Asia SouthEast Asia Western Europe

Regional Ethylene Margins (US$/MT)

2000-2009 Avg 2010-2014E Avg

Page 13

A macro outlook on the petrochemical industry

– what do these shifts mean for co-products

and aromatics?

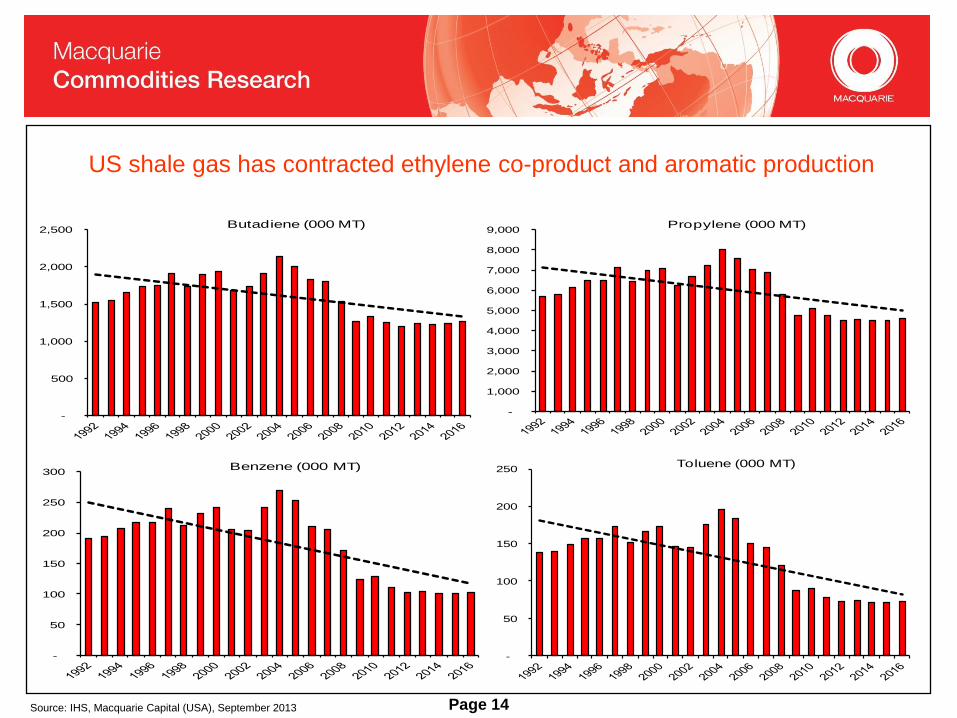

Page 14

US shale gas has contracted ethylene co-product and aromatic production

-

500

1,000

1,500

2,000

2,500 Butadiene (000 MT)

-

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000 Propylene (000 MT)

-

50

100

150

200

250

300 Benzene (000 MT)

-

50

100

150

200

250 Toluene (000 MT)

Source: IHS, Macquarie Capital (USA), September 2013

Page 15 Source: Bloomberg, IHS, Macquarie Capital (USA), September 2013

Benzene values have lifted amid tightening supply

-500

-400

-300

-200

-100

0

100

200

0

50

100

150

200

250

300

350

May-11Aug-11Nov-11Feb-12May-12Aug-12Nov-12 Feb-13May-13

OtherW. EuropeAsiaDelta: Asia Spot - U.S. Contract

Thousand Metric Tons Dollars Per Metric Ton

U.S. Benzene Imports

0

100

200

300

400

500

600

700

Jan-08

Jul-08

Jan-09

Jul-09

Jan-10

Jul-10

Jan-11

Jul-11

Jan-12

Jul-12

Jan-13

Jul-13

Benzene Contract SM

Spot SM Cumene, Formula

Cents Per Gallon

U.S. Benzene Netback Values

Page 16 Source: Bloomberg, IHS, Macquarie Capital (USA), September 2013

Margin and Spread Forecasts - Asia

2010 2011 2012 2013E 2014E 2015E Avg (2003-2012)

Dubai Crude (US$/bbl) 78 106 109 105 113 115 69

NCC benchmark margin (US$) 282 285 250 260 275 302 259

Ethylene-Naphtha spread 386 260 276 350 380 430 371

Propylene-Naphtha margin 474 510 411 400 380 400 421

Benzene-Naphtha spread 200 175 276 400 450 450 256

Butadiene-Naphtha spread 1,085 1,895 1,155 700 860 1,000 736

PX-Naphtha spread 328 616 570 570 500 480 438

HDPE-Naphtha 457 387 373 452 482 583 509

PP-Naphtha 501 500 378 421 434 507 494

HDPE-Ethylene 70 125 94 100 100 150 135

PP-Propylene 25 -10 -31 20 50 100 69

PVC-Ethylene 391 418 320 350 370 400 358

MEG-Ethylene 211 465 291 370 430 470 300

PTA-PX 256 228 80 50 40 50 177

Polyester cash margin 397 336 200 160 200 250 305

Page 17

A macro outlook on the petrochemical industry – a

quick look at technology and supply growth

Page 18

LPG

• BP/UOP, Cyclar

• Mobil, M-2 Forming

• IFP/Salutec, Aroforming

• Research Association of Japan, Z F

orming

• Asahi Chemical, Alpha Process

Methanol

• In research

Other Advantaged Feedstocks (Paraff

inic, etc)

• ChevronPhillips, Aromax

• UOP, RZ Platforming

New Technologies for Benzene – not

yet commercialized

Source: IHS, CEH, Macquarie Capital (USA), September 2013

Example: Benzene. Most new technologies will unlikely be meaningful near term

Page 19 Source: IHS, Macquarie Capital (USA), September 2013

Regional capacity growth

Additional

Capacity

% of

Additional

Additional

Capacity

% of

Additional

Additional

Capacity

% of

Additional

Middle East 3,127 10% 14,192 40% 13,281 26%North America 8,863 29% 791 2% 11,090 21%Northeast Asia 7,994 26% 11,587 32% 16,894 33%Southeast Asia 3,177 10% 2,541 7% 4,538 9%Western Europe 5,045 17% 2,850 8% (2,264) -4%Others 2,122 7% 3,874 11% 8,052 16%

30,328 35,835 51,591

Additional

Capacity

% of

Additional

Additional

Capacity

% of

Additional

Additional

Capacity

% of

Additional

Middle East 154 1% 1,653 15% 3,454 16%North America 1,899 18% (1,071) -10% 900 4%Northeast Asia 6,188 60% 7,399 68% 9,410 42%Southeast Asia 1,530 15% 2,191 20% 2,985 13%Western Europe 478 5% 25 0% 120 1%Others 55 1% 679 6% 5,296 24%

10,304 10,876 22,165

Additional

Capacity

% of

Additional

Additional

Capacity

% of

Additional

Additional

Capacity

% of

Additional

Middle East 1,049 6% 5,369 28% 6,293 33%North America 6,104 36% 1,916 10% 4,868 25%Northeast Asia 793 5% 1,262 7% 772 4%Southeast Asia 2,233 13% 2,080 11% 3,701 19%Western Europe 5,268 31% 3,071 16% (1,333) -7%Others 1,497 9% 5,679 29% 4,967 26%

16,944 19,377 19,268

Regional Propylene Capacity Growth (000 MT)

1990-1999 2000-2009 2010-2019E

Regional Ethylene Capacity Growth (000 MT)

1990-1999 2000-2009 2010-2019E

Regional Paraxylene Capacity Growth (000 MT)

1990-1999 2000-2009 2010-2019E

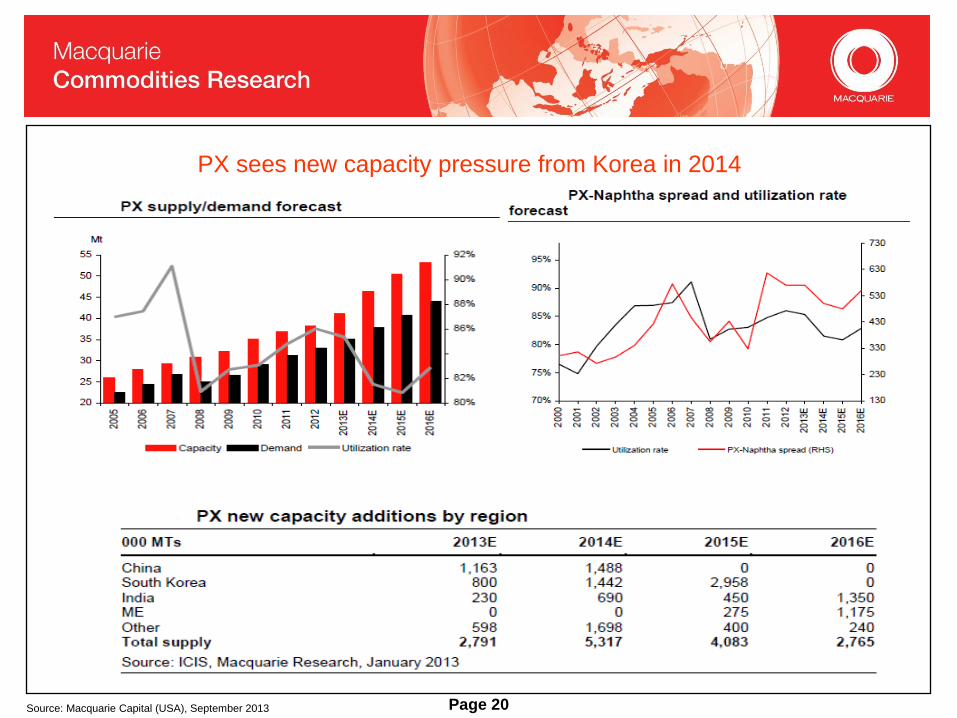

Page 20 Source: Macquarie Capital (USA), September 2013

PX sees new capacity pressure from Korea in 2014

Page 21 Source: Company data, Macquarie Capital (USA), September 2013

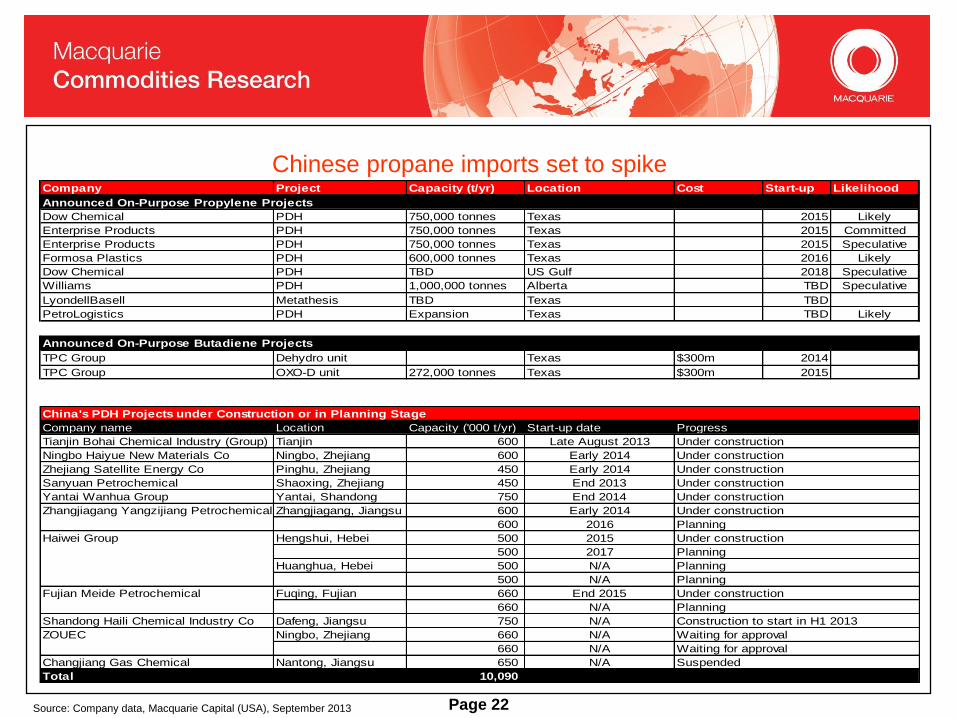

On-Purpose Propylene and Butadiene Production Company Project Capacity (t/yr) Location Cost Start-up Likelihood

Dow Chemical PDH 750,000 tonnes Texas 2015 Likely

Enterprise Products PDH 750,000 tonnes Texas 2015 Committed

Enterprise Products PDH 750,000 tonnes Texas 2015 Speculative

Formosa Plastics PDH 600,000 tonnes Texas 2016 Likely

Dow Chemical PDH TBD US Gulf 2018 Speculative

Williams PDH 1,000,000 tonnes Alberta TBD Speculative

LyondellBasell Metathesis TBD Texas TBD

PetroLogistics PDH Expansion Texas TBD Likely

TPC Group Dehydro unit Texas $300m 2014

TPC Group OXO-D unit 272,000 tonnes Texas $300m 2015

Company name Location Capacity ('000 t/yr) Start-up date Progress

Tianjin Bohai Chemical Industry (Group) Tianjin 600 Late August 2013 Under construction

Ningbo Haiyue New Materials Co Ningbo, Zhejiang 600 Early 2014 Under construction

Zhejiang Satellite Energy Co Pinghu, Zhejiang 450 Early 2014 Under construction

Sanyuan Petrochemical Shaoxing, Zhejiang 450 End 2013 Under construction

Yantai Wanhua Group Yantai, Shandong 750 End 2014 Under construction

Zhangjiagang Yangzijiang Petrochemical Zhangjiagang, Jiangsu 600 Early 2014 Under construction

600 2016 Planning

Haiwei Group Hengshui, Hebei 500 2015 Under construction

500 2017 Planning

Huanghua, Hebei 500 N/A Planning

500 N/A Planning

Fujian Meide Petrochemical Fuqing, Fujian 660 End 2015 Under construction

660 N/A Planning

Shandong Haili Chemical Industry Co Dafeng, Jiangsu 750 N/A Construction to start in H1 2013

ZOUEC Ningbo, Zhejiang 660 N/A Waiting for approval

660 N/A Waiting for approval

Changjiang Gas Chemical Nantong, Jiangsu 650 N/A Suspended

Total 10,090

China's PDH Projects under Construction or in Planning Stage

Announced On-Purpose Propylene Projects

Announced On-Purpose Butadiene Projects

Page 22 Source: Company data, Macquarie Capital (USA), September 2013

Company Project Capacity (t/yr) Location Cost Start-up Likelihood

Dow Chemical PDH 750,000 tonnes Texas 2015 Likely

Enterprise Products PDH 750,000 tonnes Texas 2015 Committed

Enterprise Products PDH 750,000 tonnes Texas 2015 Speculative

Formosa Plastics PDH 600,000 tonnes Texas 2016 Likely

Dow Chemical PDH TBD US Gulf 2018 Speculative

Williams PDH 1,000,000 tonnes Alberta TBD Speculative

LyondellBasell Metathesis TBD Texas TBD

PetroLogistics PDH Expansion Texas TBD Likely

TPC Group Dehydro unit Texas $300m 2014

TPC Group OXO-D unit 272,000 tonnes Texas $300m 2015

Company name Location Capacity ('000 t/yr) Start-up date Progress

Tianjin Bohai Chemical Industry (Group) Tianjin 600 Late August 2013 Under construction

Ningbo Haiyue New Materials Co Ningbo, Zhejiang 600 Early 2014 Under construction

Zhejiang Satellite Energy Co Pinghu, Zhejiang 450 Early 2014 Under construction

Sanyuan Petrochemical Shaoxing, Zhejiang 450 End 2013 Under construction

Yantai Wanhua Group Yantai, Shandong 750 End 2014 Under construction

Zhangjiagang Yangzijiang Petrochemical Zhangjiagang, Jiangsu 600 Early 2014 Under construction

600 2016 Planning

Haiwei Group Hengshui, Hebei 500 2015 Under construction

500 2017 Planning

Huanghua, Hebei 500 N/A Planning

500 N/A Planning

Fujian Meide Petrochemical Fuqing, Fujian 660 End 2015 Under construction

660 N/A Planning

Shandong Haili Chemical Industry Co Dafeng, Jiangsu 750 N/A Construction to start in H1 2013

ZOUEC Ningbo, Zhejiang 660 N/A Waiting for approval

660 N/A Waiting for approval

Changjiang Gas Chemical Nantong, Jiangsu 650 N/A Suspended

Total 10,090

China's PDH Projects under Construction or in Planning Stage

Announced On-Purpose Propylene Projects

Announced On-Purpose Butadiene Projects

Chinese propane imports set to spike

Page 23

Challenges relating to feedstock availability

Page 24

China shale: Vast resource base, ambitious targets

Source: EIA, Macquarie Capital (USA), September 2013

Page 25

China shale: Vast dry gas and oil potential, wet gas

(NGL) opportunity appears less well defined

Source: EIA, Macquarie Capital (USA), September 2013

Page 26 Source: IEA, Macquarie Capital (USA), September 2013

NGL Supply Trends

Page 27

U.S. NGL Production Grows Lighter

Source: EIA, Macquarie Capital (USA), September 2013

Source: IEA, Macquarie Capital, Naphtha and NGLs analysis, September 2013

New crudes more paraffinic but N+2A ratings comparable to old crudes

Page 28

Page 29

Will China stabilize and recharge growth

Page 30

Regional indicators denote improving conditions

40

45

50

55

60

Ma

r-1

2

Ap

r-1

2

Ma

y-1

2

Ju

n-1

2

Ju

l-1

2

Au

g-1

2

Se

p-1

2

Oc

t-1

2

No

v-1

2

De

c-1

2

Ja

n-1

3

Fe

b-1

3

Ma

r-1

3

Ap

r-1

3

Ma

y-1

3

Ju

n-1

3

Ju

l-1

3

Au

g-1

3

Regional PMI

US PMI Germany PMI China PMI

45

50

55

Ma

r-1

2

Ap

r-1

2

Ma

y-1

2

Ju

n-1

2

Ju

l-1

2

Au

g-1

2

Se

p-1

2

Oc

t-1

2

No

v-1

2

De

c-1

2

Ja

n-1

3

Fe

b-1

3

Ma

r-1

3

Ap

r-1

3

Ma

y-1

3

Ju

n-1

3

Ju

l-1

3

Au

g-1

3

China PMI by subindex

China New Orders PMIChina New Export Orders PMIChina Manufacturing PMI

Source: Bloomberg, Macquarie Capital (USA), September 2013

Page 31

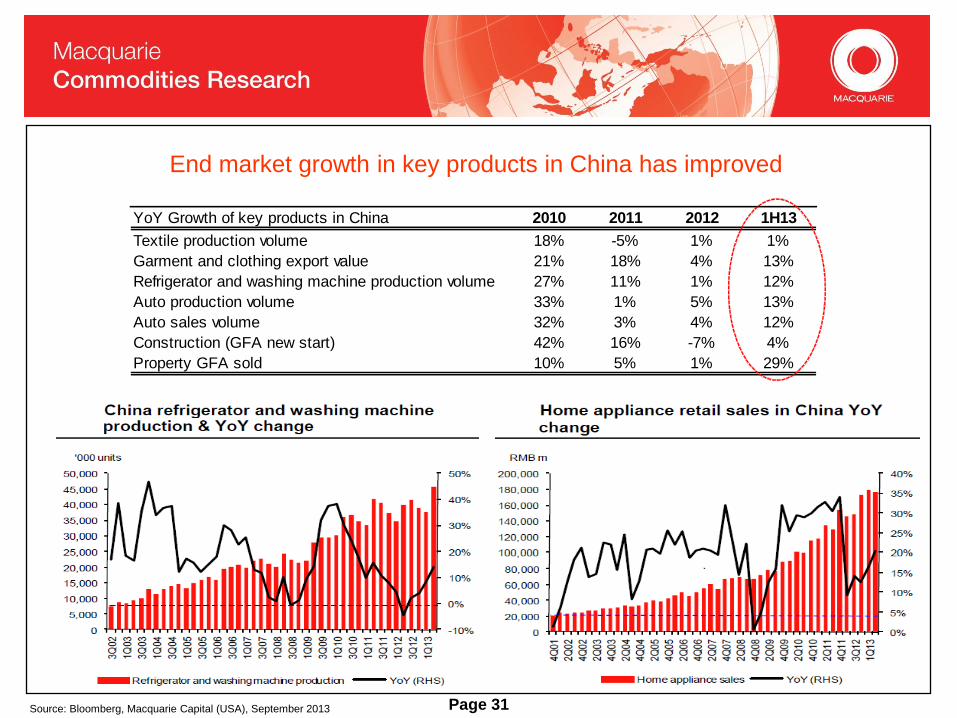

End market growth in key products in China has improved

YoY Growth of key products in China 2010 2011 2012 1H13

Textile production volume 18% -5% 1% 1%

Garment and clothing export value 21% 18% 4% 13%

Refrigerator and washing machine production volume 27% 11% 1% 12%

Auto production volume 33% 1% 5% 13%

Auto sales volume 32% 3% 4% 12%

Construction (GFA new start) 42% 16% -7% 4%

Property GFA sold 10% 5% 1% 29%

Source: Bloomberg, Macquarie Capital (USA), September 2013

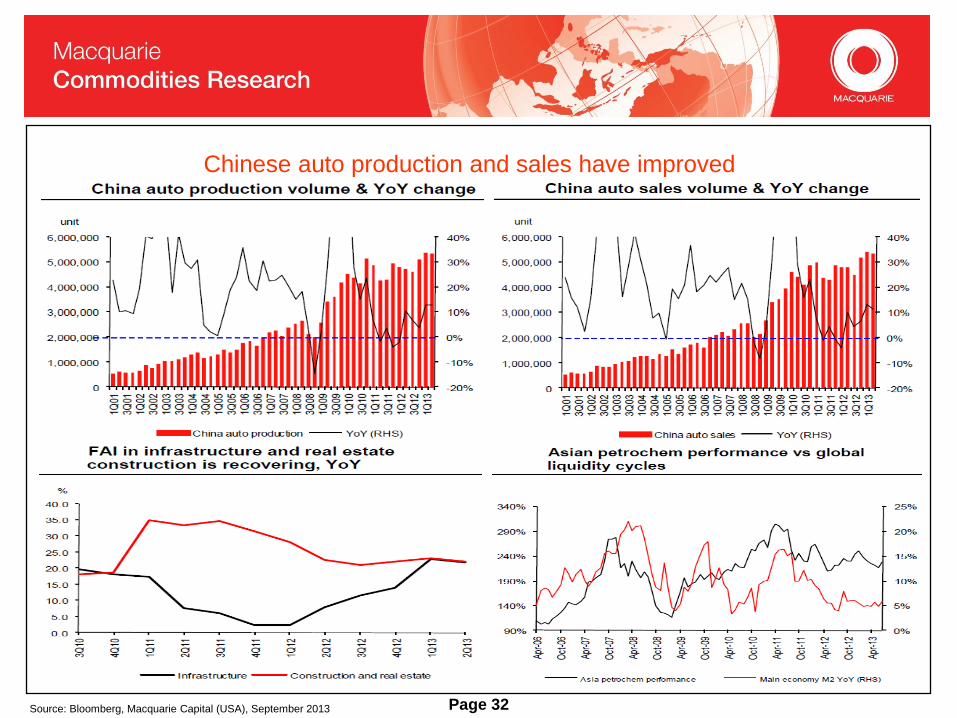

Page 32

Chinese auto production and sales have improved

Source: Bloomberg, Macquarie Capital (USA), September 2013

Page 33

China residential property sold vs. new starts (6m lag)

Source: Bloomberg, Macquarie Capital (USA), September 2013

-60%

-40%

-20%

0%

20%

40%

60%

80%

100%

120%

Jan

-10

Ap

r-10

Jul-1

0

Oct-

10

Jan

-11

Ap

r-11

Jul-1

1

Oct-

11

Jan

-12

Ap

r-12

Jul-1

2

Oct-

12

Jan

-13

Ap

r-13

Jul-1

3

GFA new starts (6m lag, YoY,%) GFA sold (YoY,%)

Page 34

Conclusions

•Demand is moving in the right direction – we anticipate a YoY pickup globally in 2014

•A wide oil/gas ratio will persist – this showcases a significant difference in regional base chemical production

costs.

•Ethylene cracker co-product production will remain under pressure – this due to light feeds

•NGL and ethylene –chain export opportunities out of North America are set to rise., but many co-products (i.e.

benzene) will need to be imported

•Companies from around the world are studying investment opportunities in the US.

•Capex targeting on purpose co-product production has picked up in China.

•China’s forecast growth rates will not be what they were, and we remain cautious medium term.

.

Source: IHS, Macquarie Capital (USA), September 2013

Page 35 Source: Bloomberg, IHS, Macquarie Capital (USA), September 2013

Additional tables

Page 36 Source: Bloomberg, IHS, Macquarie Capital (USA), September 2013

Additional tables

Page 37 Source: Bloomberg, IHS, Macquarie Capital (USA), September 2013

Additional tables

Page 38 Page 38

Important disclosures:

Recommendation definitions

Macquarie - Australia/New Zealand

Outperform – return > 3% in excess of benchmark return

Neutral – return within 3% of benchmark return

Underperform – return > 3% below benchmark return

Benchmark return is determined by long term nominal GDP growth

plus 12 month forward market dividend yield

Macquarie – Asia/Europe

Outperform – expected return >+10%

Neutral – expected return from -10% to +10%

Underperform – expected <-10%

Macquarie First South - South Africa

Outperform – return > 10% in excess of benchmark return

Neutral – return within 10% of benchmark return

Underperform – return > 10% below benchmark return

Macquarie - Canada

Outperform – return > 5% in excess of benchmark return

Neutral – return within 5% of benchmark return

Underperform – return > 5% below benchmark return

Macquarie - USA

Outperform – return > 5% in excess of benchmark return

Neutral – return within 5% of benchmark return

Underperform – return > 5% below benchmark return

Volatility index definition* This is calculated from the volatility of historic

price movements.

Very high–highest risk – Stock should be

expected to move up or down 60-100% in a year

– investors should be aware this stock is highly

speculative.

High – stock should be expected to move up or

down at least 40-60% in a year – investors should

be aware this stock could be speculative.

Medium – stock should be expected to move up

or down at least 30-40% in a year.

Low–medium – stock should be expected to

move up or down at least 25-30% in a year.

Low – stock should be expected to move up or

down at least 15-25% in a year.

* Applicable to Australian/NZ stocks only

Recommendation – 12 months

Note: Quant recommendations may differ from

Fundamental Analyst recommendations

Financial definitions

All "Adjusted" data items have had the following

adjustments made:

Added back: goodwill amortisation, provision for

catastrophe reserves, IFRS derivatives & hedging, IFRS

impairments & IFRS interest expense

Excluded: non recurring items, asset revals, property

revals, appraisal value uplift, preference dividends &

minority interests

EPS = adjusted net profit /efpowa*

ROA = adjusted ebit / average total assets

ROA Banks/Insurance = adjusted net profit /average

total assets

ROE = adjusted net profit / average shareholders funds

Gross cashflow = adjusted net profit + depreciation

*equivalent fully paid ordinary weighted average number

of shares

All Reported numbers for Australian/NZ listed stocks

are modelled under IFRS (International Financial

Reporting Standards).

Recommendation proportions – For quarter ending 30 June 2013

AU/NZ Asia RSA USA CA EUR

Outperform 49.80% 57.68% 48.05% 41.13% 61.75% 47.10% (for US coverage by MCUSA, 8.12% of stocks covered are investment banking clients)

Neutral 39.85% 24.45% 42.86% 54.70% 34.42% 30.89% (for US coverage by MCUSA, 6.60% of stocks covered are investment banking clients)

Underperform 10.35% 17.87% 9.09% 4.17% 3.83% 22.01% (for US coverage by MCUSA, 0.00% of stocks covered are investment banking clients)

Page 39 Page 39

Company Specific Disclosures:

Important disclosure information regarding the subject companies covered in this report is available at www.macquarie.com/research/disclosures.

Analyst Certification:

The views expressed in this research accurately reflect the personal views of the analyst(s) about the subject securities or issuers and no part of the compensation of the analyst(s) was,

is, or will be directly or indirectly related to the inclusion of specific recommendations or views in this research. The analyst principally responsible for the preparation of this research

receives compensation based on overall revenues of Macquarie Group Ltd ABN 94 122 169 279 (AFSL No. 318062) (MGL) and its related entities (the Macquarie Group) and has taken

reasonable care to achieve and maintain independence and objectivity in making any recommendations.

General Disclaimers:

Macquarie Securities (Australia) Ltd; Macquarie Capital (Europe) Ltd; Macquarie Capital Markets Canada Ltd; Macquarie Capital Markets North America Ltd; Macquarie Capital (USA)

Inc; Macquarie Capital Securities Ltd and its Taiwan branch; Macquarie Capital Securities (Singapore) Pte Ltd; Macquarie Securities (NZ) Ltd; and Macquarie First South Securities (Pty)

Limited; Macquarie Capital Securities (India) Pvt Ltd; Macquarie Capital Securities (Malaysia) Sdn Bhd; Macquarie Securities Korea Limited and Macquarie Securities (Thailand) Ltd are

not authorized deposit-taking institutions for the purposes of the Banking Act 1959 (Commonwealth of Australia), and their obligations do not represent deposits or other liabilities of

Macquarie Bank Limited ABN 46 008 583 542 (MBL) or MGL. MBL does not guarantee or otherwise provide assurance in respect of the obligations of any of the above mentioned

entities. MGL provides a guarantee to the Monetary Authority of Singapore in respect of the obligations and liabilities of Macquarie Capital Securities (Singapore) Pte Ltd for up to SGD 35

million. This research has been prepared for the general use of the wholesale clients of the Macquarie Group and must not be copied, either in whole or in part, or distributed to any other

person. If you are not the intended recipient you must not use or disclose the information in this research in any way. If you received it in error, please tell us immediately by return e-mail

and delete the document. We do not guarantee the integrity of any e-mails or attached files and are not responsible for any changes made to them by any other person. MGL has

established and implemented a conflicts policy at group level (which may be revised and updated from time to time) (the "Conflicts Policy") pursuant to regulatory requirements (including

the FSA Rules) which sets out how we must seek to identify and manage all material conflicts of interest. Nothing in this research shall be construed as a solicitation to buy or sell any

security or product, or to engage in or refrain from engaging in any transaction. In preparing this research, we did not take into account your investment objectives, financial situation or

particular needs. Before making an investment decision on the basis of this research, you need to consider, with or without the assistance of an adviser, whether the advice is appropriate

in light of your particular investment needs, objectives and financial circumstances. There are risks involved in securities trading. The price of securities can and does fluctuate, and an

individual security may even become valueless. International investors are reminded of the additional risks inherent in international investments, such as currency fluctuations and

international stock market or economic conditions, which may adversely affect the value of the investment. This research is based on information obtained from sources believed to be

reliable but we do not make any representation or warranty that it is accurate, complete or up to date. We accept no obligation to correct or update the information or opinions in it.

Opinions expressed are subject to change without notice. No member of the Macquarie Group accepts any liability whatsoever for any direct, indirect, consequential or other loss arising

from any use of this research and/or further communication in relation to this research. Clients should contact analysts at, and execute transactions through, a Macquarie Group entity in

their home jurisdiction unless governing law permits otherwise.

Disclaimer: The information contained in this e-mail is confidential and has been furnished to you solely for your use. You may not disclose, reproduce or distribute the information in any

way. Macquarie does not guarantee the integrity of this e-mail or attached files.

Macquarie Capital (USA) Inc. affiliate research reports and affiliate employees are not subject to the disclosure requirements of FINRA rules. Any persons receiving this report directly from

Macquarie Capital (USA) Inc. and wishing to effect a transaction in any security described herein should do so with Macquarie Capital (USA) Inc. In Germany, this research is issued

and/or distributed by Macquarie Capital (Europe) Limited, Niederlassung Deutschland, which is authorised and regulated by the UK Financial Services Authority and in Germany by BaFin.

Macquarie salespeople, traders and other professionals may provide oral or written market commentary or trading strategies to our clients that reflect opinions which are contrary to the

opinions expressed in this research. Macquarie Research produces a variety of research products including, but not limited to, fundamental analysis, macro-economic analysis,

quantitative analysis, and trade ideas. Recommendations contained in one type of research product may differ from recommendations contained in other types of research, whether as a

result of differing time horizons, methodologies, or otherwise.

Page 40 Page 40

Country-Specific Disclaimers:

Australia: In Australia, research is issued and distributed by Macquarie Securities (Australia) Ltd (AFSL No. 238947), a participating organisation of the Australian Securities Exchange.

New Zealand: In New Zealand, research is issued and distributed by Macquarie Securities (NZ) Ltd, a NZX Firm. Canada: In Canada, research is prepared, approved and distributed by

Macquarie Capital Markets Canada Ltd, a participating organisation of the Toronto Stock Exchange, TSX Venture Exchange & Montréal Exchange. Macquarie Capital Markets North

America Ltd., which is a registered broker-dealer and member of FINRA, accepts responsibility for the contents of reports issued by Macquarie Capital Markets Canada Ltd in the United

States and sent to US persons. Any person wishing to effect transactions in the securities described in the reports issued by Macquarie Capital Markets Canada Ltd should do so with

Macquarie Capital Markets North America Ltd. The Research Distribution Policy of Macquarie Capital Markets Canada Ltd is to allow all clients that are entitled to have equal access to our

research. United Kingdom: In the United Kingdom, research is issued and distributed by Macquarie Capital (Europe) Ltd, which is authorised and regulated by the Financial Services

Authority (No. 193905). Germany: In Germany, research is issued and distributed by Macquarie Capital (Europe) Ltd, Niederlassung Deutschland, which is authorised and regulated in the

United Kingdom by the Financial Services Authority (No. 193905). France: In France, research is issued and distributed by Macquarie Capital (Europe) Ltd, which is authorised and

regulated in the United Kingdom by the Financial Services Authority (No. 193905). Hong Kong & Mainland China: In Hong Kong, research is issued and distributed by Macquarie Capital

Securities Ltd, which is licensed and regulated by the Securities and Futures Commission. In Mainland China, Macquarie Securities (Australia) Limited Shanghai Representative Office only

engages in non-business operational activities excluding issuing and distributing research. Only non-A share research is distributed into Mainland China by Macquarie Capital Securities Ltd.

Japan: In Japan, research is Issued and distributed by Macquarie Capital Securities (Japan) Limited, a member of the Tokyo Stock Exchange, Inc., Osaka Securities Exchange Co. Ltd.

(Financial Instruments Firm, Kanto Financial Bureau (kin-sho) No. 231, a member of Japan Securities Dealers Association and The Financial Futures Association of Japan and Japan

Investment Advisers Association). India: In India, research is issued and distributed by Macquarie Capital Securities (India) Pty Ltd., 92, Level 9, 2 North Avenue, Maker Maxity, Bandra

Kurla Complex, Bandra (East), Mumbai – 400 051, India, which is a SEBI registered Stock Broker having membership with National Stock Exchange of India Limited (INB231246738) and

Bombay Stock Exchange Limited (INB011246734). Malaysia: In Malaysia, research is issued and distributed by Macquarie Capital Securities (Malaysia) Sdn. Bhd. (Company registration

number: 463469-W) which is a Participating Organisation of Bursa Malaysia Berhad and a holder of Capital Markets Services License issued by the Securities Commission. Taiwan: In

Taiwan, research is issued and distributed by Macquarie Capital Securities Ltd, Taiwan Branch, which is licensed and regulated by the Financial Supervisory Commission. No portion of the

report may be reproduced or quoted by the press or any other person without authorisation from Macquarie. Nothing in this research shall be construed as a solicitation to buy or sell any

security or product. Research Associate(s) in this report who are registered as Clerks only assist in the preparation of research and are not engaged in writing the research. Thailand: In

Thailand, research is produced with the contribution of Kasikorn Securities Public Company Limited, issued and distributed by Macquarie Securities (Thailand) Ltd. Macquarie Securities

(Thailand) Ltd. is a licensed securities company that is authorized by the Ministry of Finance, regulated by the Securities and Exchange Commission of Thailand and is an exchange

member of the Stock Exchange of Thailand. Macquarie Securities (Thailand) Limited and Kasikorn Securities Public Company Limited have entered into an exclusive strategic alliance

agreement to broaden and deepen the scope of services provided to each parties respective clients. The strategic alliance does not constitute a joint venture. The Thai Institute of Directors

Association has disclosed the Corporate Governance Report of Thai Listed Companies made pursuant to the policy of the Securities and Exchange Commission of Thailand. Macquarie

Securities (Thailand) Ltd does not endorse the result of the Corporate Governance Report of Thai Listed Companies but this Report can be accessed at: http://www.thai-

iod.com/en/publications.asp?type=4. South Korea: In South Korea, unless otherwise stated, research is prepared, issued and distributed by Macquarie Securities Korea Limited , which is

regulated by the Financial Supervisory Services. Information on analysts in MSKL is disclosed at

http://dis.kofia.or.kr/fs/dis2/fundMgr/DISFundMgrAnalystPop.jsp?companyCd2=A03053&pageDiv=02. South Africa: In South Africa, research is issued and distributed by Macquarie First

South Securities (Pty) Limited, a member of the JSE Limited. Singapore: In Singapore, research is issued and distributed by Macquarie Capital Securities (Singapore) Pte Ltd (Company

Registration Number: 198702912C), a Capital Markets Services license holder under the Securities and Futures Act to deal in securities and provide custodial services in Singapore.

Pursuant to the Financial Advisers (Amendment) Regulations 2005, Macquarie Capital Securities (Singapore) Pte Ltd is exempt from complying with sections 25, 27 and 36 of the Financial

Advisers Act. All Singapore-based recipients of research produced by Macquarie Capital (Europe) Limited, Macquarie Capital Markets Canada Ltd, Macquarie First South Securities (Pty)

Limited and Macquarie Capital (USA) Inc. represent and warrant that they are institutional investors as defined in the Securities and Futures Act. United States: In the United States,

research is issued and distributed by Macquarie Capital (USA) Inc., which is a registered broker-dealer and member of FINRA. Macquarie Capital (USA) Inc, accepts responsibility for the

content of each research report prepared by one of its non-US affiliates when the research report is distributed in the United States by Macquarie Capital (USA) Inc. Macquarie Capital

(USA) Inc.’s affiliate’s analysts are not registered as research analysts with FINRA, may not be associated persons of Macquarie Capital (USA) Inc., and therefore may not be subject to

FINRA rule restrictions on communications with a subject company, public appearances, and trading securities held by a research analyst account. Information regarding futures is provided

for reference purposes only and is not a solicitation for purchases or sales of futures. Any persons receiving this report directly from Macquarie Capital (USA) Inc. and wishing to effect a

transaction in any security described herein should do so with Macquarie Capital (USA) Inc. Important disclosure information regarding the subject companies covered in this report is

available at www.macquarie.com/research/disclosures, or contact your registered representative at 1-888-MAC-STOCK, or write to the Supervisory Analysts, Research Department,

Macquarie Securities, 125 W.55th Street, New York, NY 10019.

© Macquarie Group

Page 41

• This presentation has been prepared by Macquarie Bank Limited Seoul Branch('MBLSB') for

information purpose only and intended for professional investors as described under article

10 of the Presidential Decree to the Financial Investment Services and Capital market Act(the

Act). No part of this presentation material is to be construed as a solicitation to buy or sell an

y product, or to engage in any transaction and may not be distributed, either directly or

indirectly , to the public or any member of the public in Korea, other than to professional

investors as described above. To the extent permitted by law, the MBLSB does not accept a

ny responsibility for errors or misstatements, negligent or otherwise, nor for any direct, indir

ect, consequential or other loss arising from any use of the information in this presentation

material and/or further communication in relation to this information. The information may b

e based on assumptions or market conditions, and if those assumptions or market condition

s change, the information may change. No independent verification of the information has be

en made. This presentation material may not be copied or distributed in whole or in part to a

ny third party without the prior written consent of MBLSB.

Disclaimer

Page 42

Contact Macquarie Capital (USA) Inc.

Macquarie Capital (USA) Inc.

125 W. 55th Street, Level 22

New York, NY 10019

(212) 231 1000

Macquarie Capital (USA) Inc.

2 Embarcadero Center, Suite 200

San Francisco, CA 94111

(415) 762 5000

Macquarie Capital (USA) Inc.

225 Franklin Street, 17th Floor

Boston, MA 02110

(617) 598 2500

Macquarie Capital (USA) Inc.

1 North Wacker Drive, Suite 900

Chicago, IL 60606

(312) 660 9215

Macquarie Capital (USA) Inc

1225 17th Street, Suite 1600

Denver, CO, 80202

(303) 952 2800

24 Hour Toll-Free

1-888 MAC STOCK

1-888 622 7862

SALES TRADING US Robert DeRosa (212) 231 2594 Nicholas Struk (212) 231 2487 Greg Calvino (212) 231 0902 Pat Caufield (212) 231 2581 Mark Corcoran (212) 231 0951 John Curley (617) 598 2506 Bill Durand (212) 231 2413 Tom Durand (212) 231 8024 Brad Hoenig (212) 231 8089 Michael Ingrassia (212) 231 8064 Jon Jensen (617) 598 2517 Carlos Jimenez (212) 231 0883 Allen Jordan (212) 231 0947 Marty Livingston (212) 231 2523 Ross Peet (212) 231 0953 John Pennington (212) 231 2488 Stephen Sibilia (212) 231 8030 John Strack (212) 231 8067 Tarik Turner (212) 231 6365 Jess Wilson (617) 598 2509 Lance Wood (415) 762 5009 International Chris Reale (212) 231 2555 Ryan Bakker (212) 231 8083 Guy Devereux (212) 231 0900 Kai Keller (212) 231 2555 Marc Rosa (212) 231 2555

Australia/NZ Daniel Pittorino (212) 231 2552 Charlotte Edelman (212) 231 2571 Rowland Hirst (212) 231 2553 Asia Eric Roles (212) 231 2559 Darrin Blumenthal (212) 231 2562 Paul Colaco (212) 231 2496 Jeff Evans (617) 598 2508 Mark Lawrence (212) 231 2516 Mehvish Mirza (212) 231 2519 Todd Narter (415) 762 5005 Sheila Schroeder (415) 762 5003 Peter Slater (617) 598 2502 Navin Vallabhaneni (212) 231 2483 Jean Zhang (212) 231 6397 Europe Martin Pommier (212) 231 8054 Chris Carr (212) 231 6398 Jan Halaska (617) 598 2503 Jessica London (212) 231 0977 Matthew Schibanoff (212) 231 0989 Doug Stone (212) 231 2606 South Africa Mario Casis (212) 231 0937

SALES US Austin Graham (212) 231 0902 Juliana Biolsi (212) 231 2505 Michael Burguieres (212) 231 2506 Michael Cagney (312) 660 9144 Brian Cohen (212) 231 8002 Michael D’Arcangelo (212) 231 2573 Peter Doerr (312) 660 9052 Roni Gudell (617) 598 2504 Jim Isentol (212) 231 2567 Greg Jannetta (617) 598 2507 Alex Martin (212) 231 0376 Khristina McLaughlin (212) 231 8012 Rob Moderelli (212) 231 2495 Heidi Muccifori (212) 231 2466 Bruce Murdock (212) 231 8025 Tad Nacheff (212) 231 2615 Brad Neill (312) 660 9051 Todd Pigott (212) 231 8007 Jack Rose (415) 762 5002 Mark Swank (212) 231 2415 Ben Taylor (415) 762 5025 Liz Whiteley (617) 598 2501 Email Addresses [email protected] eg [email protected]

TRADING Michael Cornette (212) 231 0882 Matt Coleman (212) 231 2534 Michael Nevitt (212) 231 2408 Sam Panageas (212) 231 2459 Chris Richards (212) 231 0902 Peter Schwartz (212) 231 6381 EXECUTION SERVICES (PT/EE) James Henry (212) 231 0900 Steve Bloom (212) 231 0934 Ed Eng (212) 231 0900 Matt McNamara (212) 231 0900 Victor Morange (212) 231 2538 George Nikitiadis (212) 231 0884 Robert Redfield (415) 762 5027 CORPORATE ACCESS Katie Gray (212) 231 1318 Maria Martin (212) 231 2557 Erica Miolla (212) 231 6542 Katie Nahnybida (212) 231 6364