GLOBAL PERSPECTIVE ON ISLAMIC BANKING & INSURANCEdata.islamic-banking.com/NH/PDF/176.pdfglobal...

44

GLOBAL PERSPECTIVE ON ISLAMIC BANKING & INSURANCE ISSUE NO. 176 JULY–SEPTEMBER 2010 RAJAB–RAMADAN 1431 FOCUS: TAYYAB INVESTMENT RISK SHARING AND ISLAMIC FINANCE TAKAFUL FOCUS: NORTH AMERICA FINANCIAL DECISIONS: INSIGHT FROM ISLAMIC TEXTS ANALYSIS: ISLAMIC RATE OF RETURN IIBI SUKUK WORKSHOP REVIEW PUBLISHED SINCE 1991

Transcript of GLOBAL PERSPECTIVE ON ISLAMIC BANKING & INSURANCEdata.islamic-banking.com/NH/PDF/176.pdfglobal...

GLOBAL PERSPECTIVE ON ISLAMIC BANKING & INSURANCE

ISSUE NO. 176JULY–SEPTEMBER 2010RAJAB–RAMADAN 1431

FOCUS: TAYYAB INVESTMENT

RISK SHARING AND ISLAMICFINANCE

TAKAFUL FOCUS: NORTH AMERICA

FINANCIAL DECISIONS:INSIGHT FROM ISLAMIC TEXTS

ANALYSIS: ISLAMIC RATE OF RETURN

IIBI SUKUK WORKSHOP REVIEW

PUBLISHED SINCE 1991

Decisions based on solid foundations

Shari’ah compliance services from IBS INTELLIGENCE

www.ibsintelligence.com

Tel: +44 (0)1303 262 636Email: [email protected]

Want to know more?For information on our Shari’ah compliance services, and to download the free Shari’ah compliance benchmark PDF, visit our website.

www.newhorizon-islamicbanking.com IIBI 3

NEWHORIZON Rajab–Ramadan 1431

Features

Regulars

10 Takaful in North America

Ajmal Bhatty, CEO takaful at Tokio Marine MiddleEast, Dubai, discusses the opportunities of the Islamicinsurance industry in Canada and the US, the challenges it faces and what can be done to overcome them.

14 Islamic rate of returnJoseph DiVanna, MD of Maris Strategies, discusses the key issues of the development of alternative bench-marks to LIBOR that can be used with confidence bythe Islamic finance industry.

18 Risk sharing and Islamic financeIslamic finance, based on risk sharing, has had a longand distinguished history. It has been shown to be inherently stable and socially equitable, argue AbbasMirakhor, first chair in Islamic finance at the Interna-tional Centre for Education in Islamic Finance, andNoureddine Krichene, economist at the IMF.

CONTENTS

10

32 IIBI LECTURESMarch, May and June lectures reviewed; July lecture preview.

37 APPOINTMENTS

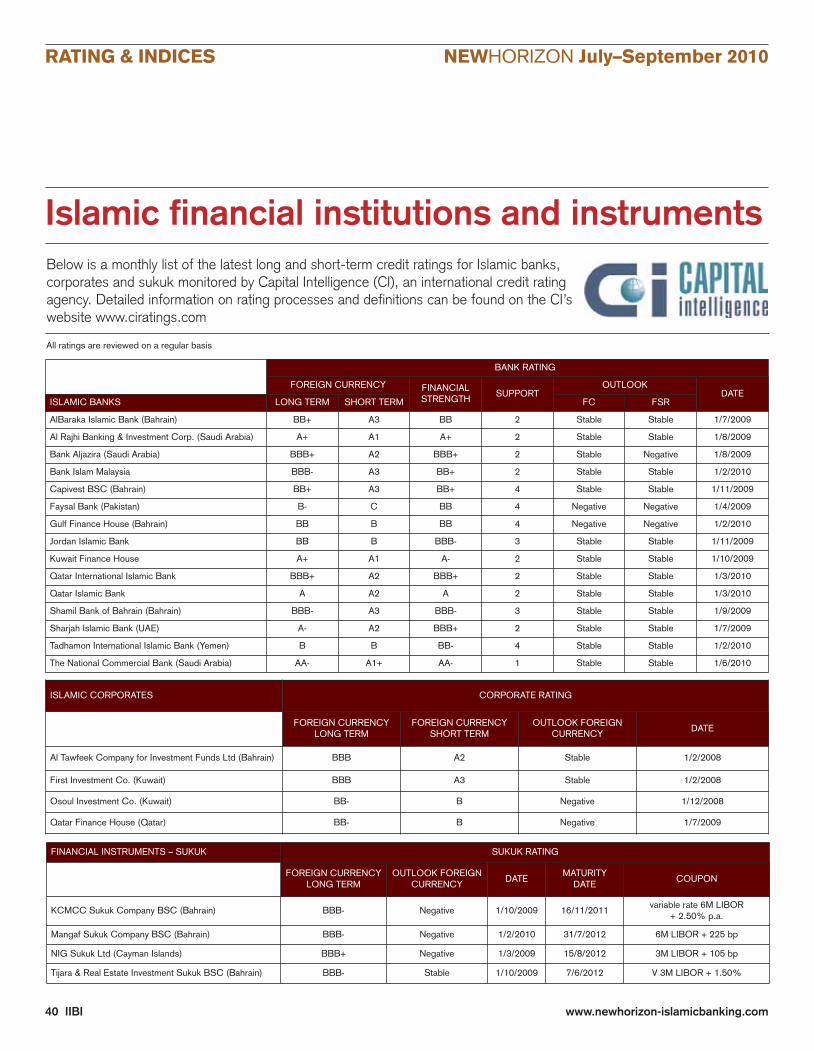

40 RATINGS AND INDICESIslamic financial institutions and instruments from Capital Intelligence (CI).

41 DIRECTORYComprehensive listing of Islamic finance industry players.

42 GLOSSARYIslamic finance terminology explained.

28 IIBI NEWSTAIB meets IIBI director general; Stenden University students visit;IIBI awards post graduate diplomas.

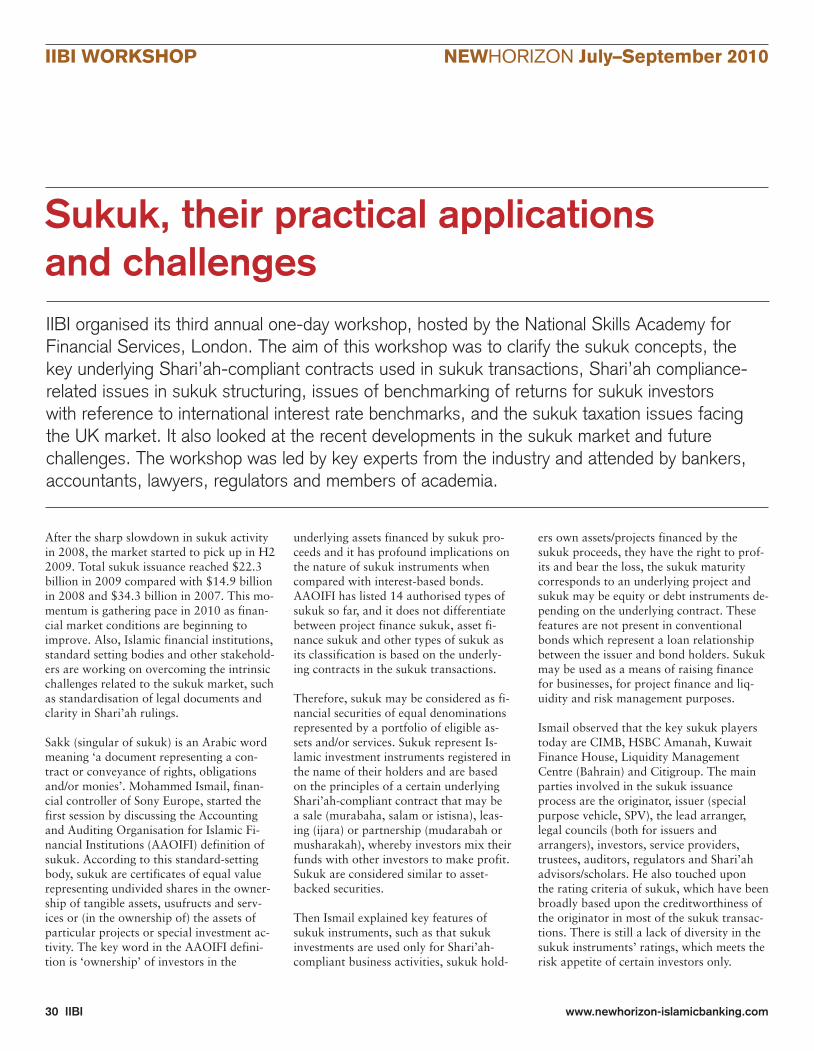

30 IIBI WORKSHOPSukuk, their practical applications and challenges.

05 NEWSA round-up of the important stories from the last quarter around the globe.

16 DIARYUpcoming Islamic finance events endorsed by the IIBI.

14

TAIB visits IIBI IIBI sukuk workshop

22 Psychology of financial decision-makingParvez Ahmed, PhD, US Fulbright scholar and associate professor of finance atthe University of North Florida, examines Islamic texts for insights about whatimpacts our financial decision-making.

26 Tayyab investment: beyond Islamic investingTrevor Norman, director at Volaw Trust, presents an overview of ethical investment within an Islamic context.

38 Book review‘The New Economics: A Bigger Picture’ by David Boyle and Andrew Simms.

www.newhorizon-islamicbanking.com

NEWHORIZON July–September 2010

Executive Editor’s Note

EDITORIAL

EXECUTIVE EDITORMohammad Ali Qayyum,Director General, IIBI

EDITORTanya Andreasyan

IIBI EDITORMohammad Shafique

NEWS EDITORLawrence Freeborn

IIBI EDITORIAL ADVISORY PANELMohammed AminRichard T de BelderAjmal BhattyStella CoxDr Humayon Dar Iqbal KhanDr Imran Ashraf Usmani

DESIGN CONSULTANTEmily Brown

PUBLISHED BY IBS Intelligence8 Stade StreetHythe, Kent, CT21 6BEUnited KingdomTel: +44 (0) 1303 262 636Fax: +44 (0) 1303 262 646Email: [email protected]: www.ibsintelligence.com

IBS Intelligence is a trading name of IBS Publishing Ltd

CONTACTAdvertisingMohammad ShafiqueInstitute of Islamic Banking and Insurance7 Hampstead Gate1A Frognal London NW3 6ALUnited Kingdom Tel: + 44 (0) 207 2450 404Fax: + 44 (0) 207 2459 769Email: [email protected]

SUBSCRIPTIONMohammad ShafiqueInstitute of Islamic Banking and Insurance7 Hampstead Gate1A Frognal London NW3 6ALUnited Kingdom Tel: + 44 (0) 207 2450 404Fax: + 44 (0) 207 2459 769Email: [email protected]

©Institute of Islamic Banking and InsuranceISSN 0955-095X

Deal not unjustly,and ye shall not be dealt with unjustly.

Surat Al Baqara, Holy Quran

NEWHORIZON July–September 2010

What drives our financial decision-making? It would be foolish to believe that we are guided by logic alone. Psychological and be-havioural factors, such as greed, are as much part of economic decision-making as cold rationality. In this issue of NewHorizon,Parvez Ahmed, a US scholar, ponders the idea that all human beingsare not always rational finds support in normative Islam. He exam-ines the Islamic texts, including the Holy Quran, to gain a clearerunderstanding of the fundamental nature of human existence andargues that this insight can be the key towards deconstructing whyhuman beings are often influenced by irrational thinking and cogni-tive dissonance when making money-related decisions.

Whilst the above subject is more philosophical than practical, theissue of creating alternative benchmarks to the London InterbankOffered Rate (LIBOR) is quite the opposite. Shari’ah scholars havebeen divided on the use of LIBOR in Islamic banking, as it gives the appearance of an interest-like quality to Shari’ah-compliant financial instruments. The development of an alternative to it has been extensively debated for the last few years, but is yet to produce far-reaching results. Shari’ah scholars have generally ap-proved the use of LIBOR as a benchmark since it is the interest it-self, rather than the benchmark rate, that is the forbidden part.

And as the development of Islamic finance continues, so does theIIBI’s input in promoting the industry worldwide, expanding its skill base and providing education opportunities to Islamic financenovices and specialists alike. The Institute’s Post Graduate Diploma(PGD) in Islamic Banking and Insurance continues to be highly regarded worldwide. Its holders can now obtain an MA degree in Islamic banking, finance and management within six months, offered by UK-based Markfield Institute of Higher Education(MIHE). It will admit the holders of PGD for the MA in IslamicBanking and holders have to complete only a research methodologymodule and a dissertation. The degree is validated and awarded bythe University of Gloucestershire.

EDITORIAL

This magazine is published to provide information on developments in Islamic finance, and not to provide professional advice. The views expressed in thearticles are those of the authors alone and should not be attributed to the organisations they are associated with or their management. Any errors andomissions are the sole responsibility of the authors. The Publishers, Editors and Contributors accept no responsibility to any person who acts, or refrainsfrom acting, based upon any material published in the magazine. The Editorial Advisory Panel exists to provide general advice to the editors regardingmatters that may be of interest to readers. All decisions regarding the published content of the magazine are the sole responsibility of the Editors, and theEditorial Advisory Panel accepts no responsibility for the content.

NEWHORIZON July–September 2010EDITORIAL

4 IIBI

Mohammad Ali QayyumDirector General IIBI

www.newhorizon-islamicbanking.com IIBI 5

NEWHORIZON Rajab–Ramadan 1431

Banque Zitouna, the first Islamicbank in Tunisia, has opened forbusiness. It was initiated and cre-ated by seven shareholders, in-cluding a well-known localbusinessman, Mohamed SakherEl Materi, chairman of PrincesseHolding Group. Princesse Hold-ing Group is the largest stake-holder in the bank.

Banque Zitouna offers around30 Islamic savings and loansproducts to retail and corporatecustomers. It has capital of $23million, which is expected to riseto $65 million by 2011. Thebank’s initial branch network ofnine offices is planned to in-crease to 20 next year.

‘Our idea of founding an Islamic

bank in Tunisia had several ob-jectives, including to consolidateand enrich the banking and fi-nancial system of our countryby offering new innovative solu-tions that complement the prod-

ucts and services already offeredby traditional banks,’ stated ElMateri.

Tunisia’s finance minister, Mo-hamed Ridha Chalghoum, who

Tunisia’s first Islamic bank opens doors

was present at the opening cer-emony of Banque Zitouna, saidthat the launch of the country’sfirst Islamic bank is part ofstrengthening financing mecha-nisms of the national economyand increasing the volumes ofsavings. Taoufik Baccar, gover-nor of the Central Bank ofTunisia, also attended the cere-mony. In his view, Banque Zi-touna will enrich the country’sbanking landscape, which cur-rently consists of aroundtwenty institutions. He alsonoted that the launch of thebank is in line with the five-year presidential programme,which includes establishingTunisia as ‘a hub for bankingservices and a regional finan-cial centre’.

NEWS

A new pan-Gulf Arab Shari’ahsupervisory board may be inplace by 2013, according to aShari’ah scholar, HusseinHamad Hassan. A regionalShari’ah council to oversee thestandardisation and harmoni-sation of Islamic finance indus-try, and to facilitate the spreadof services to a growing num-ber of clients, is ‘not a far-fetched reality’, according toHassan. He is head of theShari’ah committee of DubaiIslamic Bank and chairman ofthe Shari’ah CoordinationCouncil of Islamic FinancialInstitutions in the UAE. Has-san is also a member of the

board of the Accounting andAuditing Organisation for Is-lamic Financial Institutions(AAOIFI).

Hassan raised the issue of thecurrent difficulties faced byclients who may want to buyan Islamic financial product ina different country. Having asingle regional Shari’ah boardis seen as a way of easing this.The issue is also a topical one:Malaysia’s central bank, BankNegara Malaysia, is known tobe preparing a system to helpcross-border transactions be-tween Islamic financial institu-tions.

International Shari’ahcommittee mooted

In response to growing demandand a recovering economy, Pak-istan is looking to double thesize of its Islamic banking sec-tor over the next three years.Salim Ullah, director of Islamicbanking at the State Bank ofPakistan, wrote recently thatthe industry would grow to thesize of twelve per cent of itsconventional counterpart, fromsix per cent currently, in thenext two to three years. Thisprocess will be driven by ‘in-creasing awareness and inter-est’ in finance which complieswith the tenets of Islam, Ullahbelieves. Part of this increasinginterest is a response to the

flaws of the conventional sys-tem made clear by the recentglobal financial crisis, he stated.

Pakistan currently has six fully-fledged Islamic banks. Of these,Meezan Bank, which has over200 branches across the coun-try, is the largest. Others includeDawood Islamic Bank and Al-baraka Islamic Bank. On top ofthese six, another 13 lendersprovide both conventional andIslamic financial services, andthe State Bank of Pakistan hasrecently given authorisation toanother two. Pakistan is hometo about 170 million Muslims,second only to Indonesia.

High hopes for Islamicbanking in Pakistan

Medina of Sousse, Tunisia

6 IIBI www.newhorizon-islamicbanking.com

NEWHORIZON July–September 2010NEWS

The Central Bank of the UAE isplanning to offer the country’sfirst Shari’ah-compliant instru-ment by the end of 2010. Thecentral bank is working on in-troducing an Islamic certificateof deposit, as part of its effortsto develop a money market.‘There is a need for Shari’ah-compliant certificates of depositto be issued by the centralbank,’ stated Saif Hadef AlShamsi, senior executive direc-tor, the treasury department at the Central Bank. However,he added that the final producthas not been approved yet.

The Shari’ah Coordination

Committee of Islamic Finan-cial Institutions has reviewedthe bank’s proposal and hasgiven it preliminary approval,according to Hussein HamadHassan, chairman of the com-mittee. However, some ‘minorchanges’ are required.

He also noted that the CentralBank ‘cannot issue licences forIslamic banks and then askthem to accept products andservices that are not Shari’ah-compliant’.

There are forecasts of thebank raising up to $2.7 billionwithin a year of offering the

UAE Central Bank prepares first Islamic certificate of deposit

product. At present, it holdsover $16 billion from financialinstitutions in the countrythrough its conventional cer-tificates of deposit. The devel-opment follows the call of theAccounting and Auditing Or-ganisation for Islamic Finan-cial Institutions to widen thepool of money market securi-ties to help companies and in-vestors manage risk moreeffectively.

Malaysia, which has theworld’s largest market for Is-lamic debt, launched a newelectronic trading platform in2009 that enables its partici-

pants to buy and sell com-modities, such as palm oil,used as assets to back Islamicloans.

The UAE is now preparingnew legislation on establishinga federal debt market by theend of 2010, according to theCentral Bank’s governor, Sul-tan bin Nasser al-Suwaidi. Itwill allow the Central Bank toissue treasury bills, bonds andIslamic notes. Malaysia andBahrain already offer such se-curities as a monetary tool tomanage liquidity and to de-velop benchmarks for short-term bond yields.

Gulf African Bank, an Islamicbank in Kenya, has posted apre-tax profit of $310,000 forQ1 2010, which puts it oncourse for its first full-yearprofit, according to the bank’sCEO, Najmul Hassan.

Hassan spoke to the Reutersnews agency, describing thebank’s Shari’ah-compliant ac-tivity as a ‘successful model’and saying that the positivefigures indicate that the localmarket ‘has really acceptedGulf African Bank’.

There are plans to increase itsbranch network to 14 loca-tions by opening two morebranches shortly.

Hassan also indicated that the bank is in discussions withthe government regarding issu-ing sukuk. However, it is not yet known whether the govern-ment will issue a standalonesukuk or whether it will be atranche from its regular bonds.

In 2009, the bank partneredwith Kenya’s other Islamic bank, First Community Bank, to invest in a $12 million gov-ernment sukuk. The inauguralsukuk was a tranche in thecountry’s first infrastructurebond worth around $230 million.

Islam is the religion of around10 million people in Kenya.

Islamic bank in Kenya is a ‘successful model’

Pakistan’s first Islamicmicrofinance bank planned

Pak-Qatar Family Takaful isplanning to set up Pakistan’sfirst Shari’ah-compliant mi-crofinance bank. PervaizAhmed, director and foundingCEO of Pak-Qatar FamilyTakaful, said that the bankwill focus on the SME sector.

The microfinance bank willintroduce Islamic insurance(takaful), including familytakaful products, and short-term Shari’ah-compliant loansfor lower income groups, ac-cording to Ahmed.

The company will heavily in-vest to expand Pak-QatarFamily Takaful’s reach in the

course of 2010, as well as toacquire new technology andprovide innovative facilities to customers. In 2009, Pak-Qatar Family Takaful’s busi-ness stood at $10.6 millionand this year it aims to growthreefold, said Ahmed.

However, Ahmed acknowl-edged that takaful still faces alot of challenges in Pakistan.‘Lack of general awarenessand education amongst themasses about the use andbenefit of insurance, let alonetakaful, is the biggest impedi-ment in the growth of the in-surance industry in Pakistan,’he stated.

www.newhorizon-islamicbanking.com IIBI 7

NEWHORIZON Rajab–Ramadan 1431 NEWS

Islamic banking sees progress in India

Islamic non-banking financecompanies (NBFCs) are beingconsidered by India’s ministryof finance. This comes as a result of the reluctance of the country’s central bank, the Reserve Bank of India(RBI), to allow banks to offerIslamic finance products andservices.

The initiative is currently in theearly stages of discussion, saida finance ministry official. ‘Theidea is to start with NBFCs sothat they can gain experience.Also, this way issues regardingfinancing and the model of Islamic banking can be ad-dressed,’ the source explained.Together with the RBI, theministry will work on theguidelines and exemptions forIslamic NBFCs. At present, thegovernment allows four typesof NBFCs: asset financing, in-vestment, lending and infra-structure financing.

There are some NBFCs inIndia that are already working

with Shari’ah-compliant offer-ings, but the existing regula-tory framework makes themnon-viable. For example, Is-lamic NBFCs work on thelease-transaction and hire-pur-chase model, which results indouble taxation of profits.

Earlier, the RBI concluded thatIslamic banking did not fitinto India’s banking legisla-tion. There is some room forrule relaxation, indicated theofficial, but it was added that the ministry cannot deviatefrom the basic principles ofbanking. Areas such as assetclassification, accounting stan-dards, capital adequacy andprovisioning for bad assetswill be looked into.

Overall, India’s banking andfinance specialists agree thatinterest-free banking will be apositive development for thecountry’s market. The commit-tee on financial sector reform,chaired by a renowned Indianeconomist, Raghuram Rajan,

has recommended the intro-duction of this type of banking.Also, the Indian Centre for Is-lamic Finance (ICIF) has madepresentations to the RBI andIndia’s finance minister, PranabMukherjee, on Islamic bank-ing. In this presentation, theICIF has stated that ‘if financeis available without the burdencaused by pre-determined in-terest rates, it will be a wel-come development for all themarginalised sectors, and espe-cially SMEs. Interest-free Is-lamic banking can fill this gap.’

The ICIF has also supported the idea of Shari’ah-compliantNBFCs and suggested that theyshould be allowed to floatsukuk (Islamic bonds) to raisecapital.

The government of the Keralaregion has been in talks forsome time with an Islamic in-vestment entity about settingup an Islamic NBFC, sup-ported by the Kerala State In-dustrial Development

Corporation (KSIDC). In 2009,the KSIDC proposed to set upthe first state-supported Islamicbank in the region, with aneleven per cent stake held by the KSIDC. The entity was to be registered as an IslamicNBFC to start with, and con-verted into a fully-fledged Shari’ah-compliant bank later.

However, the venture has experienced set-backs when petitions challenging the cre-ation of this NBFC were filedby Subramaniam Swamy, headof the Janata Party, and R VBabu, secretary of Hindu AikyaVedi. Babu argued that theKSIDC, which has a mandate to promote industrial activitiesin Kerala, should not partici-pate, financially or otherwise, in a financial venture.

The issue has not been resolvedto date. Recently, the high courtof Kerala adjourned the petitionuntil early September. This wasdone after the RBI’s request formore time.

New Delhi,India

New Delhi,India

8 IIBI www.newhorizon-islamicbanking.com

NEWHORIZON July–September 2010NEWS

DBS Bank, one of the largestbanks in South East Asia andthe largest lender in the region,is rowing back on its ambitionsfor the Islamic banking industryfollowing heavy losses in itsShari’ah-compliant subsidiary,Islamic Bank of Asia (IBA). The move is being seen as asign that efforts to increase Is-lamic banking in Singapore arestruggling.

IBA, which is the only whollyowned, fully licensed Islamicbank in the city state, suffered aloss of $77 million last year, on$725 million of assets in 2009.

In response, IBA has transferredten of its 65 staff back to DBS(which owns just over 50 percent of IBA), while other staffare being redeployed within theIslamic bank. Staff to leave havenot been replaced, including theformer CEO, Vince Cook, wholeft IBA in December 2009.

There has been speculation thatIBA would be shut entirely butDBS has stated that it remainscommitted to growing Islamicbanking in Singapore. IBA’s tra-vails are perhaps mirrored bythose of Kuwait Finance HouseSingapore, which was set up to

manage the Islamic funds ofKuwait Finance House. It has

Slow progress for Islamic banking in Singapore

yet to do so, however, and hasalso seen its workforce cut.

Four major UAE companieshave teamed up to establish a new Islamic insurance firm.

The participants in the ven-ture are the National Bank ofAbu Dhabi, Aldar Properties

(a real estate firm), AbuDhabi National InsuranceCompany (Adnic) andTaqa (energy company).All four are either fully orpartially owned by thegovernment of Abu Dhabi.

The new takaful entity is currently under forma-tion, so no details arebeing disclosed. The UAEmarket is prime for Islamicinsurance providers, ex-perts believe. Al HilalBank, Abu Dhabi IslamicBank, Noor Islamic Bankand Dubai Islamic Bankhave already set up theirtakaful operations.

New takaful venture to belaunched in Abu Dhabi

Islamic insurance (takaful) ispoised to grow significantly inthe next four years, according toErnst & Young Islamic financialservices division. The team’s di-rector, Ashar Nazim, forecastedthe takaful business trebling insize over the next four years andreaching $25 billion.

He presented these findings dur-ing the recent launch of Ernst &Young’s third annual WorldTakaful report, which tookplace in London. Nazim notedthat the industry should play amore active role in facilitating‘consistent regulatory, legal, ac-counting, capital markets andtax regimes’.

The way forward for the indus-try, in his view, is to focus on

‘generating sustainable rev-enues from the core underwrit-ing business’. The discussionalso tackled the issues of cleardifferentiation between conven-tional and Islamic insurance, as well as the way for takafuloperators to increase scale ofactivity and at the same timedecrease dependence on a fewinvestment instruments.

Sameer Abdi, head of Ernst &Young Middle East financialservices group, described the Islamic insurance industry as a ‘case study in resilience’. According to Abdi, globaltakaful contributions grew 29per cent in 2008 and reached$5.3 billion, and are expectedto exceed $8.9 billion by theend of 2010.

High growth expectations for takaful

Singapore

10 IIBI www.newhorizon-islamicbanking.com

NEWHORIZON July–September 2010

Islamic insurance (takaful) has been grow-ing at an incredible pace in the Middle Eastand parts of Asia, Africa and Europe. How-ever, it has yet to find its place within theinsurance industry in North America, aplace for takaful that may be seen as aniche for its appeal to customers who find it aligned with their values and beliefs. Buttakaful need not be confined to a niche be-cause of its appeal to all of us who under-stand the benefits of socially responsibleinstitutions (SRIs), the socially responsibleways to invest for the good of society andenvironment that affects all of us.

Takaful has distinct differences from con-ventional insurance, although the two alsoshare many common aspects. Takaful pro-vides financial protection against unfore-seen risks just like conventional insurance.It is bound by and based on similar scien-tific rules and actuarial approaches to mor-tality rates, morbidity rates, loss ratios,claims experience and discounted cashflows for calculating price of risk and evalu-ation of liabilities. Islamic insurance is simi-lar to conventional mutual insurance as itspolicyholders conceptually own the co-op-erative takaful pool. However, takaful alsohas shareholders to support developmentand expansion plans unlike conventionalmutuals.

Insurance is risk mitigation through the ap-plication of law of large numbers. Takafulis the same except that its basic meaning is

Takaful in North America: a global view for local perspectiveWhat are the challenges for Islamic insurance in Canada and the US? How promising is theNorth American market? The Usury Free Association of North America (UFANA) recently held adedicated conference in Toronto, gathering international specialists to address these and othertopical questions. Ajmal Bhatty, CEO takaful at Tokio Marine Middle East, Dubai, presented hisview.

mutual protection through large numbersmade up of those who care to help eachother, and the pooling of their money goesbeyond this, to help the community and theenvironment.

If we ask anyone what is meant by insur-ance the answer is buying protection froman insurance company. When we ask thesame question about takaful, the answerought to be mutually protecting each other.There is a sense of mutuality – a conceptmore related to mutual companies, exceptthat mutual companies may have ethical investments as a matter of choice not obli-gation. Ethical investments are not a mustfor them.

The compliance system of takaful is meantto make it non-exploitative with little or no margin for misinterpretation. Moniesgenerated from its funds and reserves are invested to generate trade, wealth and employment, and not to create merely more money in reference to interest baseddealings.

Takaful expresses the essence of insurancein a way that focuses on shared responsibil-ity or solidarity amongst those who takepart for the common good. The risk istransferred from one to many but still therisk remains with them, shared jointly andnot transferred to a third party. In conven-tional insurance, the risk is transferred frommany to one party – the insurer.

TAKAFUL FOCUS

Ajmal Bhatty,Tokio Marine Middle East

www.newhorizon-islamicbanking.com IIBI 11

NEWHORIZON Rajab–Ramadan 1431 TAKAFUL FOCUS

Development of takaful around the world

Takaful started in 1979 and has perseveredas an industry in reaching its current stateespecially within the last five to six years,with consistent and rapid growth throughseveral companies. Some estimates indicateover 150 takaful companies and windowsworldwide.

The past growth of some 30 per cent perannum in Malaysia and 20 per cent perannum in some parts of the Middle Eastconsistently achieved over the last severalyears is actually considered to be on thelower side when compared to the takafuldynamics of several markets with potentialfor much higher growth. Much of this hold-ing back in the current markets of takaful inthe Middle East, Asia and Africa is to dowith the mindset of those players (insurers,brokers and reinsurers) who are well-en-trenched in these markets in conventionalinsurance and see takaful as a nicheonly. Takaful, for what it stands forin its essence of ethics, should rightlybe the mainstream form of insurancein countries where takaful is a cus-tomer-driven phenomenon.

It is this customer-driven push thatled lots of local and regional takafulcompanies to be established. Manybig international players for manyyears continued to argue that insur-ance offers the same as takaful, butthe fact of the matter is that some of the big international players havenow their own takaful companiesand windows. Amongst such compa-nies are Tokio Marine, AIG, Pruden-tial, HSBC Insurance, Zurich, AXA,Munich Re and Swiss Re. Tokio Marine, operating in Saudi Arabiasince 1967, was the first ever interna-tional player to have introduced taka-ful as a product in that market in2001. By January 2008, it was offer-ing takaful products in Saudi Arabia,Malaysia and Indonesia. The Groupalso has a family retakaful company(Shari’ah-compliant life reinsurance)in Singapore.

The estimated global takaful premiums were$3.4 billion in 2007 excluding Iran, and this number more than doubles to $7.5 bil-lion with Iran included. It is estimated thatabout 40 per cent of global takaful businessrelates to family takaful.

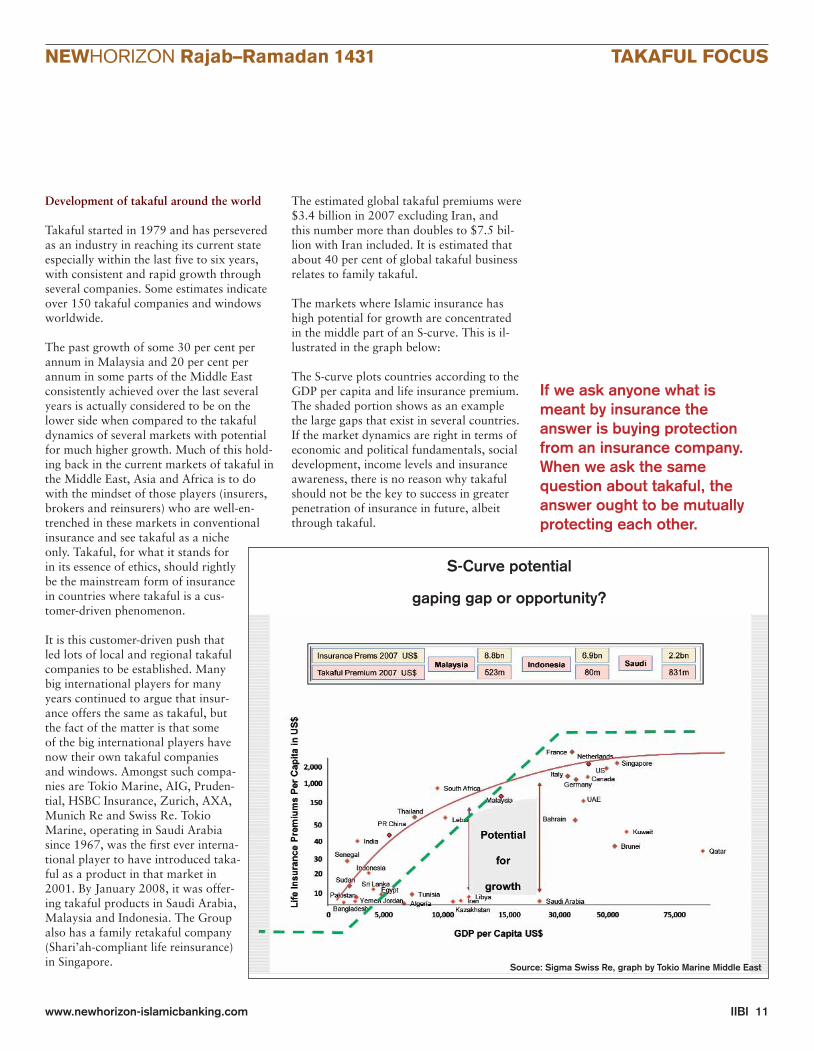

The markets where Islamic insurance hashigh potential for growth are concentratedin the middle part of an S-curve. This is il-lustrated in the graph below:

The S-curve plots countries according to theGDP per capita and life insurance premium.The shaded portion shows as an examplethe large gaps that exist in several countries.If the market dynamics are right in terms ofeconomic and political fundamentals, socialdevelopment, income levels and insuranceawareness, there is no reason why takafulshould not be the key to success in greaterpenetration of insurance in future, albeitthrough takaful.

Source: Sigma Swiss Re, graph by Tokio Marine Middle East

If we ask anyone what is meant by insurance the answer is buying protectionfrom an insurance company.When we ask the samequestion about takaful, theanswer ought to be mutuallyprotecting each other.

S-Curve potential

gaping gap or opportunity?

12 IIBI www.newhorizon-islamicbanking.com

NEWHORIZON July–September 2010TAKAFUL FOCUS

In 2008, Saudi Arabia had $6 per capitaspend on life insurance and yet other coun-tries with lower GDP per capita such asMalaysia had much higher spend of $226.The figure for Canada was $1,443 (withthe GDP per capita of $39,100) in 2008. It is not surprising that the compound an-nual growth of insurance in countrieswithin the middle part of the S-curve isvery high. The two graphs on the left illus-trate this in putting the growth of insur-ance over 2000 to 2008 within the contextof GDP per capita.

The world average growth was nine percent in general insurance. Most countrieswith takaful potential have shown higherthan average growth. Canada shows bettergrowth (twelve per cent per annum) thanthe world average and many of the matureinsurance markets, such as the UK, the USand Japan.

Whilst insurance awareness is low in manymarkets due to cultural reasons, takafulhas all the room to grow. In life insurance,referring to the graph below, the countrieson the middle part of the S-curve have all shown impressive consistent yearlygrowth: Malaysia 15 per cent, Egypt 17per cent, Indonesia 24 per cent, the UAE32 per cent and Saudi Arabia 37 per cent.Canada registered growth of nine per cent,higher than the US (four per cent). Theworld average growth was six per cent an-nually from 2000 to 2008.

The projected figures for the global size of takaful are estimated to be $7.7 billionby 2012 and up to $14 billion by 2015, as new companies open up and become es-tablished in the GCC, especially in Saudi Arabia and the Levant region, in additionto the growing markets of South East Asia and Asia Pacific, led by Pakistan,Malaysia and Indonesia. Europe holds agreat deal of promise for the growth oftakaful and a number of initiatives arebeing considered there. The total capitalcommitted within the takaful industry in2007 was around $3.5 billion. Takaful as-sets are estimated to grow to around $30billion to $40 billion by 2015, approxi-

Source: Sigma Swiss Re, graph by Tokio Marine Middle East

Source: Sigma Swiss Re, graph by Tokio Marine Middle East

Non Life CAGR 2000/08

Life CAGR 2000/08

business into takaful.

Finding interim solutions until solid perma-nent solutions can be found is the way togo, provided we have the will to persevereto deliver this system which is fair to all thestakeholders – the customers, shareholders,employees and the society at large. Theseare some key challenges facing promotersof takaful in North America:

❏ Pricing products competitively, thisbeing a function of returns on Shari’ah-compliant assets available (or not quiteavailable) locally.

❏ Promoting the takaful system correctlyand ensuring customer expectations aremet fully. This includes the co-operativeand community spirit and how funds con-tribute to the larger benefit of the commu-nity and environment.

❏ Creating and maintaining Shari’ahcredibility.

There is a large Muslim population inCanada and the US. Also, there are manypeople who find the concept of channellingfunds back into the community very ap-pealing. Takaful is evolving rapidly inother parts of the world, and it can do soin North America. Companies taking alead in securing an early market share with professional management and ratedsecurity should reap the long-term rewardsfrom this business. Anyone wishing to develop takaful for North America wouldbenefit from studying and learning fromboth successful and adverse experiences inother markets, to see how others have triedto overcome the challenges.

www.newhorizon-islamicbanking.com IIBI 13

NEWHORIZON Rajab–Ramadan 1431 TAKAFUL FOCUS

mately 40 per cent of this backing familytakaful business.

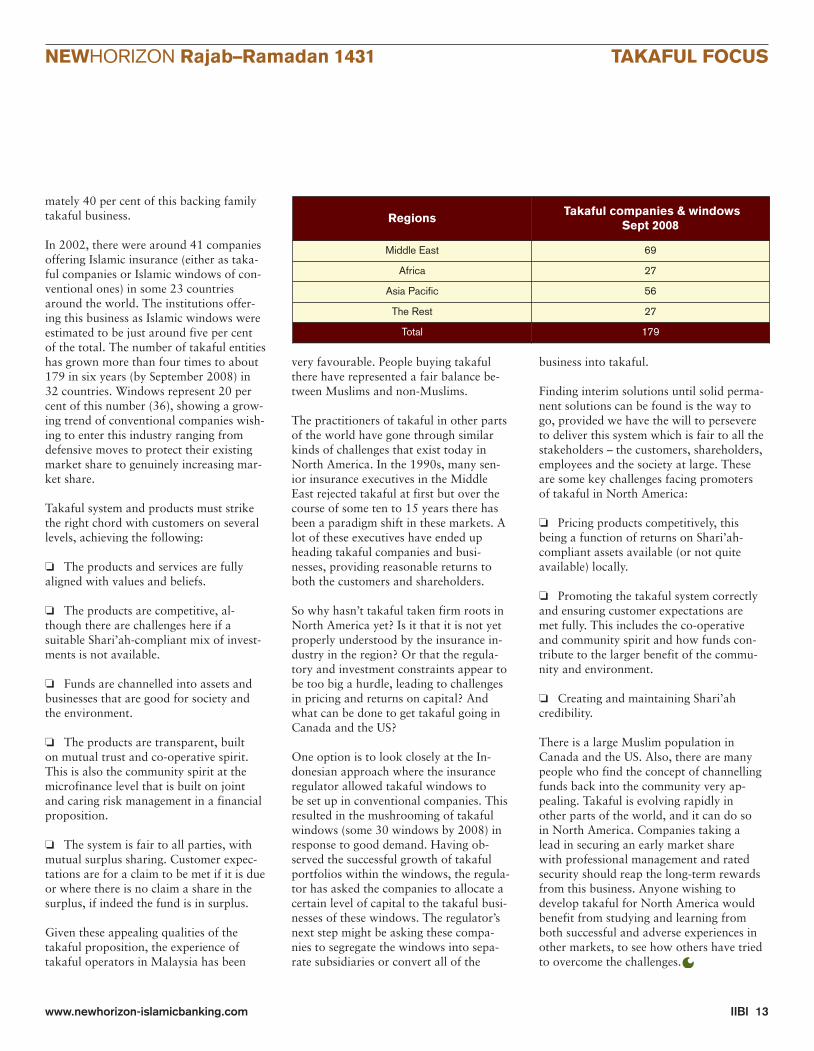

In 2002, there were around 41 companiesoffering Islamic insurance (either as taka-ful companies or Islamic windows of con-ventional ones) in some 23 countriesaround the world. The institutions offer-ing this business as Islamic windows wereestimated to be just around five per cent of the total. The number of takaful entitieshas grown more than four times to about179 in six years (by September 2008) in32 countries. Windows represent 20 percent of this number (36), showing a grow-ing trend of conventional companies wish-ing to enter this industry ranging fromdefensive moves to protect their existingmarket share to genuinely increasing mar-ket share.

Takaful system and products must strikethe right chord with customers on severallevels, achieving the following:

❏ The products and services are fullyaligned with values and beliefs.

❏ The products are competitive, al-though there are challenges here if a suitable Shari’ah-compliant mix of invest-ments is not available.

❏ Funds are channelled into assets andbusinesses that are good for society andthe environment.

❏ The products are transparent, built on mutual trust and co-operative spirit.This is also the community spirit at themicrofinance level that is built on jointand caring risk management in a financialproposition.

❏ The system is fair to all parties, withmutual surplus sharing. Customer expec-tations are for a claim to be met if it is dueor where there is no claim a share in thesurplus, if indeed the fund is in surplus.

Given these appealing qualities of thetakaful proposition, the experience oftakaful operators in Malaysia has been

very favourable. People buying takafulthere have represented a fair balance be-tween Muslims and non-Muslims.

The practitioners of takaful in other partsof the world have gone through similarkinds of challenges that exist today inNorth America. In the 1990s, many sen-ior insurance executives in the MiddleEast rejected takaful at first but over thecourse of some ten to 15 years there hasbeen a paradigm shift in these markets. Alot of these executives have ended upheading takaful companies and busi-nesses, providing reasonable returns toboth the customers and shareholders.

So why hasn’t takaful taken firm roots inNorth America yet? Is it that it is not yetproperly understood by the insurance in-dustry in the region? Or that the regula-tory and investment constraints appear tobe too big a hurdle, leading to challengesin pricing and returns on capital? Andwhat can be done to get takaful going inCanada and the US?

One option is to look closely at the In-donesian approach where the insuranceregulator allowed takaful windows to be set up in conventional companies. Thisresulted in the mushrooming of takafulwindows (some 30 windows by 2008) inresponse to good demand. Having ob-served the successful growth of takafulportfolios within the windows, the regula-tor has asked the companies to allocate acertain level of capital to the takaful busi-nesses of these windows. The regulator’snext step might be asking these compa-nies to segregate the windows into sepa-rate subsidiaries or convert all of the

RegionsTakaful companies & windows

Sept 2008

Middle East 69

Africa 27

Asia Pacific 56

The Rest 27

Total 179

14 IIBI www.newhorizon-islamicbanking.com

NEWHORIZON July–September 2010

Islamic finance is poised for a significantsurge as world markets reorganise andShari’ah-compliant banks reassess their po-sition in local markets. As a global market,Islamic banking has grown at an impressive27 per cent per annum over the past fiveyears, and is estimated to reach $1 trillionin 2010. Growth in the Islamic finance in-dustry will occur along three distinct fronts:organic growth, new market growth andproduct growth. Organic growth will con-tinue as Shari’ah-compliant banks persist in engaging their clients with additionalservices (aiming to increase deposits). Newmarket growth will consistently rise asmore banks are engaging previously un-banked populations in Africa, the MiddleEast and Southern Asia where the ratio ofpeople banked is very low. It is however thethird area of product growth which holdsthe most long-term benefits for Islamic fi-nance.

Shari’ah-compliant institutions are emerg-ing from 2009 with a renewed sense of confidence as the impact of the financial crisis is passing from a panicked search forguilty parties to a refocused approach torisk management. Islamic banks have beensomewhat insulated from the global finan-cial crisis because of their lack of access towhat is now labelled as ‘toxic assets’. WhatIslamic banks have noticed during the crisisis a steady increase in assets as investors/de-positors take conservative postures and amarked reduction in the generation of feeand investment income. Unlike their con-ventional counterparts, during 2008-09Shari’ah-compliant institutions continued adeliberate plan of innovation, mainly in re-

Islamic rate of return: the new IRR

The issue is discussed by Joseph DiVanna, MD of Maris Strategies, a Cambridge-basedstrategy think tank for financial services specialising in economic, demographic and consumerintelligence in emerging markets.

tail banking distribution, experimentingwith technology. Now these banks are turn-ing their attentions toward a longer-termgrowth agenda which includes product in-novation that is more distinctly a represen-tation of Islamic values and beliefs.

However, the rate at which this potential for growth is achieved is predicated on theestablishment of additional national and international financial infrastructure. Onekey area of discussion is in the use ofLIBOR (London Interbank Offered Rate) as an industry benchmark for sukuk andother instruments. Today, the performanceof Shari’ah-compliant products such assukuk are measured (or linked) to LIBOR as a benchmark, not by design, simply as a matter of convenience in the early stage of market development. To compete withconventional banks, which many of theirclients have been using for decades, Shar-i’ah-compliant institutions have adoptedthe use of LIBOR so customers have a read-ily recognised mechanism to assess the rela-tive rate of return on their productofferings.

Shari’ah scholars have been divided on the use of LIBOR as it gives the appearance of an interest-like quality to Shari’ah-com-pliant financial instruments. Conversely,some Islamic scholars have argued that sim-ply using an interest rate as a benchmarkfor determining the relative rate of returnfor a Shari’ah-compliant instrument doesnot render the instrument non-compliant.

‘In the final analysis, a benchmark is nomore than a number, and therefore non-

ANALYSIS

The key point of debate is the appearance of a Shari’ah-compliant financial instrumentto generate a fixed rate return.

www.newhorizon-islamicbanking.com IIBI 15

NEWHORIZON Rajab–Ramadan 1431 ANALYSIS

objectionable from a Shari’ah perspective. If it is used to determine the rate of repay-ment on a loan, then it is the interest-bear-ing loan that will be haram. LIBOR, as amere benchmark, has nothing to do withthe actual transaction or, more specifically,with the creation of revenues or returns,’says Shaykh Yusuf Talal DeLorenzo, chiefShari’ah officer and board member ofShariah Capital, a US-based Shari’ah advi-sory firm.

The key point of debate is the appearance of a Shari’ah-compliant financial instru-ment to generate a fixed rate return.Under Shari’ah principles, money cannotgenerate money, which in modern times is represented by interest. Numerous Shari’ah scholars have argued that instru-ments such as murabaha (debt) cannot besecuritised, since sukuk-backed pools ofmurabaha are simply the sale of docu-ments representing money, which can beinterpreted as merely trading of monies.On the other hand, Malaysian scholarshave argued that if the underlying receiv-able is associated with a true trade trans-action or to a commercial transfer of anon-monetary interest, such a receivablecan be traded freely for the purposes ofShari’ah.

Theoretically, a hybrid (debt/equity) sukukcould be structured to emulate a quasi-fixed return found in conventional bondswhereby the LIBOR benchmark wouldgive investors an understanding of the instrument’s return relative to a conven-tional counterpart. Thus if structuredproperly the hybrid sukuk can generate aprofit-based return that is comparable to aconventional LIBOR-based product. Whatthis boils down to is the fundamental needfor the industry to mature to a new levelthrough a process of product/market inno-vation that increases the depth of marketofferings. Market infrastructure such as aShari’ah-compliant money market instru-ment, the establishment of a secondarymarket and secondary market pricing arebut a few of challenges in the years tocome, which will reach higher levels ofdiscussion in 2010.

Islamic rate of return (IRR)

Fundamentally, the industry, or more specif-ically central banks, must address the cre-ation of a benchmark that represents thecost of capital in Shari’ah-compliant terms.Without a clear Islamic rate of return (IRR)LIBOR will continue to be used. The use of LIBOR and the development of an alter-native has been discussed and debated dur-ing the past five years resulting in fewalternatives. The central issue is the cost of capital and the establishment of an Is-lamic rate of return for procurement andplacement of funds. Some scholars advocatethe development of a mechanism similar to a rent index used when working with ijara instruments. Hence the industry willcontinue to use LIBOR as the only recog-nised benchmark. That said, the Islamic International Financial Market (IIFM), aBahrain-based non-profit international in-frastructure development institution, identi-fies several alternative theories:

❏ Abbas Mirakhor approach: proposesthat the cost of capital be measured withoutresort to a fixed and predetermined interestrate using equity financing as the source offinancial capital (Tobin ‘q’ theory).

❏ Sheikh Taqi Usamni approach: a bench-mark can be achieved by creating a commonpool which invests in asset-backed instru-ments (e.g. musharakah, ijara) where unitscan be sold and purchased on the basis oftheir net asset value determined on a peri-odic or daily basis.

❏ Bank Negara Malaysia (Malaysia’s cen-tral bank) approach: proposed in ‘Frame-work of the Rate of Return’ sometimesreferred to as mudarabah interbank invest-ments (MII) – a standard methodology tocalculate the distribution of profits and thederivation of the rates of return to deposi-tors. A calculation table prescribes the in-come and expense items that need to bereported. It also sets out the standard calcu-lation in deriving the net distributable in-come and a distribution table sets out thedistribution of the net distributable incomeposted from the calculation table among de-

Joseph DiVanna,Maris Strategies

16 IIBI www.newhorizon-islamicbanking.com

NEWHORIZON July–September 2010ANALYSIS

mand, savings and general investment de-posits according to their structures, maturi-ties and the pre-agreed profit sharing ratiosbetween the bank and the depositors.

Another alternative, which was introducedin 2004 by the State Bank of Pakistan (SBP)and the Pakistan Banks’ Association (PBA), is the KIBOR (Karachi Interbank OfferedRate) a benchmark for corporate lending inlocal currency defined as ‘the Average rate,Ask Side, for the relevant tenor, as publishedon Reuters page KIBOR or as published bythe Financial Markets Association of Pak-istan in case the Reuters page is unavailable.The banks and the borrowers are free to decide the relevant tenor of KIBOR and the spread over KIBOR at their discretion.KIBOR will be set for the lending facility onthe date of drawdown or on the mark-upreset date. The offer letters from the banksto their clients should clearly indicate theKIBOR’s tenor and the agreed spread, fre-quency of revision’. The six-month KIBOR is most widely used as a benchmark.

How will an Islamic interbank rate work?

One theoretical construct is the use of a mudarabah concept whereby Shari’ah-compliant institutions with excess reserves(surplus banks) can invest in the interbankmoney market which in turn providesfunding to banks looking for funds (deficitbanks). Surplus banks act as investorswhile the central bank acts as an entrepre-neur. The parties agree on a profit sharingratio between the surplus banks (70 percent) and the central bank (30 per cent).The surplus bank receives 70 per centprofit while the central bank will receive 30 per cent. The profit rate is based on the benchmark calculation of the profit as: profit equals (principal x profit rate xtime x profit sharing ratio) divided by365. Although theoretically, profit ratesare acting under a similar means as an interest rate there is a built-in risk associ-ated with the performance of the underly-ing assets associated with all thetransactions initiated by the banks.

Clearly, these types of mechanisms are intheir infancy and will require a great dealof discussion between Shari’ah scholars,central bankers, monetary policy makersand bankers.

Conclusion

The Islamic finance market will continueto grow and strengthen during 2010. The rate at which the growth will occur is dependent on two things: the develop-ment of supporting market infrastructuresuch as a replacement for LIBOR and the confidence in the bankers themselves to conduct business in challenging eco-nomic times. The development of alterna-tive benchmarks demonstrates the risingindependence of Islamic finance as a viable alternative to conventional financ-ing. As new economic data slowly reveals the emergence of renewed growth, Is-lamic finance is poised to enter 2010 as the first year of a new generation ofdevelopment.

Diary of events endorsed by the IIBIJuly

13–15: 4th International Takaful Summit,LondonSummit to gather practitioners and re-searchers from around the world to explorethe current state of the Islamic insurance industry.Contact: Abbas KhakuTel: +44 (0) 20 8861 2012Email: [email protected] www.takafulsummit.com

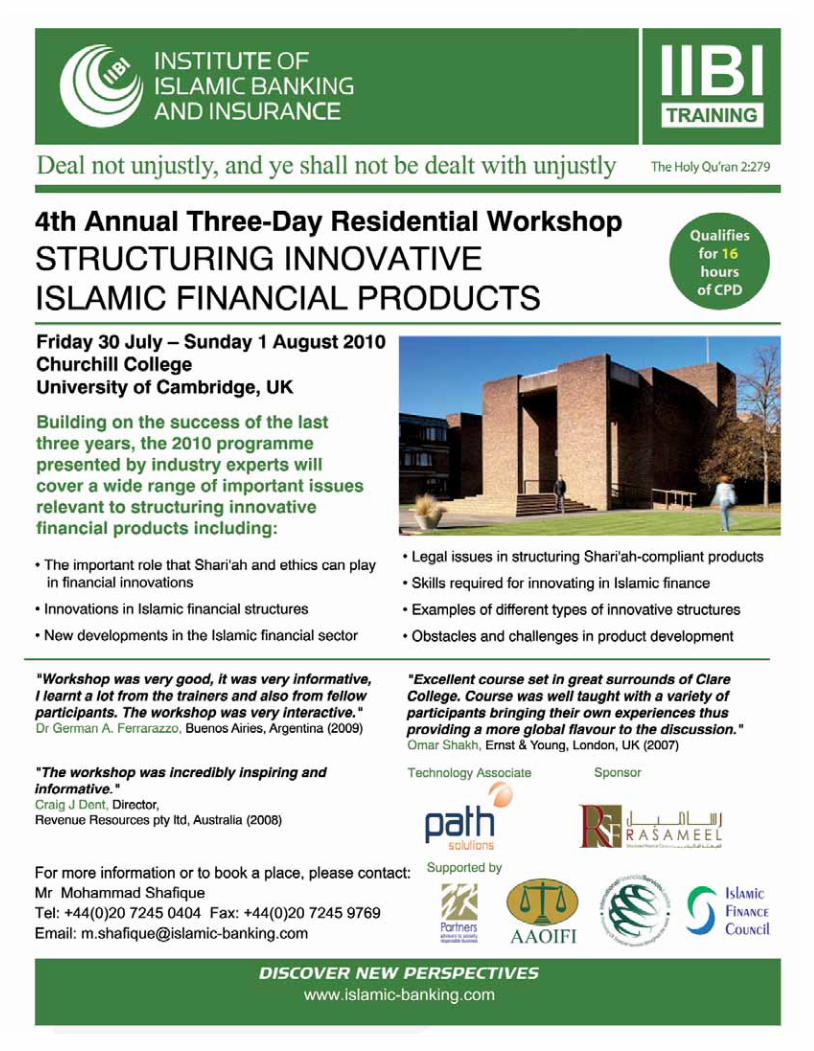

30 –1 August: Structuring Innovative Islamic Financial Products, Cambridge, UKFourth annual three-day residential work-shop to cover a wide range of highly topicalissues of structuring innovative Shari’ah-compliant financial products. Contact: Mohammad ShafiqueTel: +44 (0) 20 7245 0404Email: [email protected]

November

22–24: 17th Annual World Islamic Banking Conference (WIBC), BahrainConference to discuss the key issues, developments and challenges of Shari’ah-compliant banking and finance worldwide.Contact: Naomi NjorogeTel: +971 4 343 1200Email: [email protected]

Cambridge

Throughout 2010, IIBI is organising a number of training workshops to build the skill baseand share ideas among practitioners within the Islamic finance industry. The objective ofthe Institute’s training is to fill the human resource gap and to enhance the professionalskills of personnel who are either interested in building their careers or already involved in the Islamic finance sector. Training programmes are delivered by experienced profes-

sionals; the number of participants is kept small to ensure the interactive environment andprovide a practical learning experience for the participants with the help of suitable case

studies. For more information about upcoming programmes, please visit: www.islamic-banking.com

18 IIBI www.newhorizon-islamicbanking.com

NEWHORIZON July–September 2010

ever collateral may be involved, without los-ing the property rights claim to the moneylent. This is a violation of Islamic propertyrights principles. The most important ofthese principles are that:

❏ The Creator has ultimate property rightson all things.

❏ He (swt) has created resources for allmankind and no one can be denied access to these resources.

❏ Work is the only means by which indi-viduals gain the right of possession of property when they combine their physi-cal/mental abilities with natural resources to produce a product.

❏ Since resources belong to all mankind, a right is created in the products producedby the more able for the less able; in effectthe less able are silent partners in the products, income and wealth produced by the more able whose share has to be redeemed.

❏ All instantaneous property rights claims,such as theft, bribery, interest and gambling,are prohibited.

❏ A person can transfer a property rightsclaim to another via exchange, inheritanceor the redemption of the rights of the lessable. Interest rate-based debt contracts cre-ate an instantaneous property rights claimfor the creditor against the debtor regardlessof the outcome of the objective for whichthe two sides entered the contract. The cred-itor obtains this property rights claim with-out commensurate work.

Equity-based Islamic finance and risk sharing

The foundational principle of Islamic fi-nance is the prohibition of interest (riba)and interest-based contracts. This prohibi-tion has been stated in many verses inQuran and was explicated in many sayingsof the Prophet PBUH.

In Quran, Chapter Two, verse 275, Allahsays: ‘those who devour riba (interest) willstand except as stands one who the evil oneby his touch has driven to madness. That isbecause they say exchange is like riba; butAllah has permitted exchange and forbiddenriba.’ In Chapter Two, verse 276, ‘Allah willdestroy riba; but will increase charity’. Inverses 278-279, Chapter Two, ‘Oh you whobelieve fear Allah and give up what remainsof riba; if you do it not, take notice of warfrom Allah and His Apostle’.

As can be observed from the last part of the quoted verses, there is no rule violationin the Quran that has been treated as seri-ously as the charging of interest which isconsidered a paramount act of injustice. Aneconomic understanding of the essence ofthe above verses – that interest-based debtcontracts have to be replaced by contracts of exchange – would require analysis of par-ticularities of the two contracts. Interestrate-based debt contracts have two majorcharacteristics. Firstly, they are instrumentsof risk shifting, risk shedding and risk trans-fer. The second characteristic of interest-based debt contracts is that upon enteringinto this contract, the creditor attains aproperty rights claim on the debtor, equiva-lent to the principal plus interest and what-

Risk sharing and Islamic finance Abbas Mirakhor, first chair in Islamic finance at the International Centre for Education in IslamicFinance, Malaysia, and Noureddine Krichene, economist at the International Monetary Fund(IMF), with a PhD from University of California, Los Angeles, examine the issue.

Ordaining exchange to replace interest rate-based debt contracts has significant economicimplications. First, before parties can enterinto a contract of exchange they must haveproperty rights over the subject of exchange.Second, the parties need a place to undertakethe exchange: a market. Third, the marketneeds rules for its efficient operations.Fourth, the rules of market need enforce-ment. Exchange facilitates specialisation andallows the parties to share production, trans-portation, marketing, sales and price risks.Therefore exchange is above all a means ofrisk sharing. From an economic standpoint,by prohibiting interest rate-based contractsand ordaining exchange contracts, the Quranencourages risk sharing and prohibits risktransfer, risk shedding and risk shifting. In a typical risk sharing arrangement such as equity finance, the parties share the risk aswell as the reward of a contract. In an inter-est rate-based debt contract the risk is trans-ferred from the financier to the borrower,with the financier retaining not only theproperty rights claim to the principle and in-terest but also that of any collateral that hasenhanced the financing arrangement. In a risksharing arrangement such as equity participa-tion, the asset is invested in remunerativetrade and production activities, the return tothe asset is not known at the instant the assetis invested and is therefore a random vari-able, making equities risky assets. In equityinvestment, owners of money and physicalassets, and entrepreneurs, share the risk; theirincome is random and depends on the per-formance of the equity investment.

Not all debt contracts are forbidden in Islam.However, they have to be free of interest. Be-cause they are not remunerative, debt con-

ACADEMIC ARTICLE

www.newhorizon-islamicbanking.com IIBI 19

NEWHORIZON Rajab–Ramadan 1431 ACADEMIC ARTICLE

tracts cannot play a significant economicrole in financing trade and investment inIslamic finance. How about borrowing bythe needy and the poor for survival? BeforeIslam, and also in medieval Europe, thepoor used to borrow by pledging theirproperty as a collateral. As default was acommon event, the poor risked the loss ofall their properties with the consequencethat often they were forced into slavery. Asa direct consequence of the principles ofproperty rights, in Islam, the poor, the or-phans and the needy have a prescribed andmandatory share in the earnings of assets,which provide a safety net. Thus, the richare mandated to share the risk of the life ofthe poor. Prohibition of interest and theobligation of zakat and other prescribedduties levied on the well-to-do are statedoften jointly and not separately in both theQuran and the Sunnah. When the econom-ically more able shirk their duty of redeem-ing the rights of the less able, the poor willhave to borrow or fall in abject poverty.Existence of wide-spread poverty in a soci-ety is prima facie evidence of shirking ofthe duty of sharing.

Islamic finance is inherently stable, conventional finance is inherently unstable

Islamic finance, by emphasising equity investment and risk sharing, has character-istics that render it inherently stable. Conventional finance, being debt- and in-terest-based, has proven to be unstable.Hyman Philip Minsky, a prominent Ameri-can economist, dubbed conventional fi-nance instability ‘endogenous instability’because conventional finance experiences athree-phased cycle: relative calm, specula-tion and fictitious expansion, and then cri-sis and bankruptcy. The bankruptcy aspectof conventional finance is not limited tothe private sector as the recent Greek debtcrisis illustrates; governments too can facebankruptcy. Recent historical analysis hasdemonstrated that all financial, bankingand currency crises have been ultimatelydebt crises. The widespread bankruptciesof many developing countries in the recentpast shows that often governments thatborrowed what were considered as reason-

able debt levels compared to their GDPfound themselves in an unsustainable debtspiral due to increased debt service obliga-tions. Many found themselves with debt levels many times larger than the originalborrowed.

In the aftermath of the financial crisis thatbroke out in August 2007, the InternationalMonetary Fund (IMF) and regulators in in-dustrial countries have called for capital surcharges on banks and for strengthenedregulation and supervision to make conven-tional banking less crisis-prone. In contrastto the regulatory reforms proposed by theG20 group in its November 2008 summitand in following summits, the Chicago Re-form Plan (1935) advocated a financial sys-tem based on 100 per cent reserve banking,equity-based banking, and elimination of interest rate-based contracts. In line withmany classic economists, the authors of theChicago Reform Plan (1935) considered thatmodern banking created fictitious credit, expanded in a multiplicative way throughmoney creation, and contracted in a multi-plicative way through money destruction,causing grave gyrations in asset prices andlarge fluctuations in real economic activity.In the Chicago Reform Plan (1935), depositsat investment banks would be considered as equity shares and would finance long-term investment. Maurice Allais, a Nobellaureate in economics, strongly advocatedthe Chicago Reform Plan (1935) and calledfor a reform of the stock market in order toenhance its role in financial intermediationand reduce its speculative aspects.

Islamic finance and the evolutionary processof equity financing

In an Islamic finance system in which thereare no risk-free assets, where all financial as-sets are contingent claims, and in whichthere are no interest rate-based debt con-tracts, it has been shown that the rate of re-turn to financial assets was determined bythe return to the real sector. Output is di-vided between labour and capital. Oncelabour is paid, the profit is then divided be-tween entrepreneurs and equity owners.Since profits are ex post, returns on equities

In line with many classiceconomists, the authors of theChicago Reform Plan (1935)considered that modernbanking created fictitiouscredit, expanded in a multi-plicative way through moneycreation, and contracted in amultiplicative way throughmoney destruction, causinggrave gyrations in asset pricesand large fluctuations in realeconomic activity.

Abbas Mirakhor,International Centre for Education in Islamic Finance

20 IIBI www.newhorizon-islamicbanking.com

NEWHORIZON July–September 2010ACADEMIC ARTICLE

cannot be known ex ante. It is demon-strated that in such a system there is a one-to-one mapping between finance and realeconomy and that an equity-based finance is stable as assets and liabilities adjust toshocks, therefore the system is immune tobanking crisis and disruption in the pay-ments mechanism.

Equity financing has been an essential modeof financing of trade and industry through-out the centuries. It continues to be em-ployed as a mode of financing in manydeveloping countries where it has evolvedwith the advent of enterprise creation andeconomic growth.

Historically, enterprises were establishedwith share ownership and were recorded asshare owned or anonymous enterprises.Shares were not necessarily offered to thepublic via stock markets and were primarilyprivate contributions of founders of thecompany. In many countries, share-ownedcompanies continue to be formed withoutnecessarily resorting to stock market publicofferings. Nonetheless, with the spread ofequity-financed firms, stock markets, as aform of organised exchanges, became an in-tegral part of financial intermediation andin channelling savings to long-term invest-ment. Stock markets, considered as the first-best instruments of risk sharing, offerliquidity for listed shares in that the ownersof listed shares may sell them when theyneed liquidity. Moreover, liquidity and at-tractiveness of stocks have been enhancedby the proliferation of derivatives, such asoptions and futures, that allow portfolio insurance that provides protection againstbear markets. For instance, a protective put provides protection against stock down-turns. While stock markets have been vul-nerable to speculative bubbles and stockmarket crashes have been ruinous to saversand to pension funds, the main reason hasoften been informational problems, self-dealings such as insider trading, unregulatedshort sales that promote unnecessary specu-lation, lack of protection of minority shareholder rights, weak regulation and supervision, and even weaker enforcementof contracts.

The development of Islamic finance and itsequity financing aspects could be signifi-cantly rewarding for countries that seek an alternative to the conventional system.Many developing countries have tried to develop conventional banking to enhancetheir financial infrastructure; however, alarge number of these countries have experi-enced repeated severe banking and currencycrises and have failed so far to create a deep and stable financial system. Economicgrowth and employment in these countriescontinue to be severely constrained. Devel-oping long-term equity-based banking andefficient stock markets could be a promisingalternative for financing growth and em-ployment creation in all countries.

Islamic finance: balance between short-termless risky liquid assets and long-term, higherrisk, and less liquid assets – the vibrant stockmarket approach

For Islamic finance to achieve its expectedpotential, it has to emphasise long-term in-vestment and economic growth and not con-fine itself to short-term, highly liquid, andsafe commodity trade and cost-plus sale fi-nancing contracts. Long-term investmentsare more risky than short-term investments.In fact, the more distant in time the payoffsof an investment are, the riskier these pay-offs become. Risk increases with time. How-ever, long-term investments have higherexpected payoff. Nonetheless, a stumblingblock to long-term finance is liquidity, infor-mational problems, lack of level playingfield between equity and debt financing,weak regulation and enforcement as well as non-protection of minority shareholderrights. The liquidity problem has been ad-dressed by developing secondary marketswhere securities can be sold. The liquidity of equity shares is enhanced through twochannels. Firstly, over-the-counter (OTC)trade where deposits in investment accountsheld at an Islamic bank are transferred to anew owner who redeems the previous ownerfor the amount being deposited in long-termequity accounts. The second channel is or-ganised stock market exchanges where listedshares can be traded at low cost in liquidmarkets.

Noureddine Krichene,International Monetary Fund

www.newhorizon-islamicbanking.com IIBI 21

NEWHORIZON Rajab–Ramadan 1431 ACADEMIC ARTICLE

Risk sharing and equity finance was empha-sised in a recent paper, presented at the Inaugural Securities Commission Malaysia(SC) and Oxford Centre for Islamic Studies(OCIS) Roundtable, entitled ‘Developing aScientific Methodology on Shari’ah Gover-nance for Positioning Islamic Finance Glob-ally’. The paper notes that the first bestinstrument of risk sharing is a vibrant stockmarket, which is the most sophisticated mar-ket-based risk sharing mechanism. Develop-ing an efficient stock market can effectivelycomplement and supplement the existingand future array of other Islamic finance in-struments. It would provide the means forbusiness and industry to raise capital. Suchan active market would reduce the domi-nance of banks and debt financing whererisks become concentrated and create systemfragility. In the current evolution of Islamicfinance, what needs emphasis is long-terminvestment contracts that allow the growthof employment and income and expansionof the economy. Moreover, through holdingdiversified stock portfolios, investors caneliminate idiosyncratic risks specific to indi-vidual investor as well as to firms. Diversifi-cation can allow reduction in the overallportfolio risk. The paper calls for strength-ening the regulatory framework, levellingthe playing field between debt and equity, reducing the costs of equity market opera-tions through provisions of laws and regula-tions that promote market based barriers tospeculative abuse of stock markets, protec-tion of minority shareholders, regulation of reputational intermediaries – such as ac-countants, lawyers, and Shari’ah scholars –that certify companies and financial instru-ments, and strong enforcement of contracts.

Conclusion

Islamic finance, based on risk sharing, hashad a long and distinguished history, partic-ularly in the Middle Ages when it was thedominant form of financing investment andtrade in the then global economy. Eventoday, venture capital financiers use tech-niques very similar to Islamic risk sharingcontracts such as mudarabah. Conventionalbanking, which began with the goldsmiths’idea of fractional reserve banking, received

strong support from heavily subsidised lastresort lender central banks and rules andregulations heavily biased in favour of in-terest rate-based debt contracts and againstrisk sharing contracts. These developmentshave helped the perpetuation of a systemthat a number of well-known scholars,such as Keynes, deemed detrimental togrowth, development and to equitable in-come and wealth distribution. In more recent times, reforms proposed in theChicago Reform Plan (1935) and in agrowing literature thereafter have arguedthat the stability of a financial system canonly be assured by 100 per cent reservebanking to support the payment system ofthe country – which obviates the need forcostly central bank guarantees, on the onehand, and promotes equity-based invest-ment banking, on the other. Islamic fi-nance, based on risk sharing in investmentactivities and 100 per cent reserve bankingto ensure the safety of the payment system,has been shown to be inherently stable andsocially equitable. In such a system there isa one-to-one mapping between the growthof the financial sector and real sector activi-ties. This means that credit cannot expandor contract, as it does in the conventionalsystem, independently of the real sector. Tofoster further the development of Islamic finance, there is a need to emphasise risk-sharing aspect of the system; remove biasesagainst equity finance; reduce transactioncosts of stock market participation; create a market-based incentive structure to min-imise speculative behaviour; and developlong-term financing instruments as well aslow cost efficient secondary markets fortrading equity shares. These secondarymarkets would enable a better distributionof risk and achieve reduced risk with ex-pected payoffs in line with the overall stockmarket portfolio. Absent true risk sharing,Islamic finance may provide a false impres-sion of being all about developing debt-like, short-term, low risk and highly liquidfinancing without manifesting the most important dimension of Islamic finance: its ability to facilitate high growth of em-ployment and income with relatively lowrisk to individual investors and market participants.

The first best instrument of risk sharing is a vibrant stockmarket, which is the mostsophisticated market-based risksharing mechanism. Developingan efficient stock market caneffectively complement andsupplement the existing andfuture array of other Islamicfinance instruments.

22 IIBI www.newhorizon-islamicbanking.com

NEWHORIZON July–September 2010

(nafsi)’. Another verse in the Quran uses theword nafs to allude to human soul stating:‘It was We (God) who Created human be-ings, and We know what dark suggestionshis soul (nafsuhu) makes to him’ (50:16).The soul and the person make up the self.This self in the Quranic hermeneutics hasthree stages or states of development:

1. Nafs al-ammarah bi al-su’ (the self urging evil)

This is the stage of human developmentwhere the soul is motivated by base desiresand may suggest of wrong actions. Allahsays: ‘Surely the human self urges evil’(12:53). When in this primitive stage of itsdevelopment, the soul can overpower thenatural cognitive human processes and in-duce biases, such as the heuristic biases de-scribed in behavioural finance literature.

The Quran asserts that in this stage thehuman being may not always benefit fromall their God-given cognitive faculties. The‘animal instinct’ of the nafs al-ammarah willsometimes overpower the cognitive senses.‘They have hearts wherewith they do notunderstand; have eyes wherewith they donot see; have ears wherewith they do nothear. These are like cattle – no, but they areworse! These are the neglectful’ (7-179).

A well-known Islamic scholar, Al-Ghazali,interprets that at this stage the nafs can di-rect its owners to nifaq (hypocrisy, prideand arrogance) and hawa (base desire) lead-ing to greediness, negligence and restless-ness. This is the classic fear and greed state,

An economic and financial meltdown aspervasive as the one we just witnessed nat-urally evokes renewed interest in examin-ing the very fundamentals of the currenteconomic system. A dogmatic belief in theinvisible hand of the free market had dis-couraged financial regulation. Regulators,bankers and some academics were unwill-ing to budge from the assumption that investors are ‘rational’, all the while disre-garding a nascent body of scholarly re-search in finance and economics, whichsuggests that investor behaviour is not al-ways driven by logic alone. Psychologicalor behavioural factors, such as fear andgreed, are as much part of economic deci-sion making as cold rationality.

The idea that human beings, even the smartones, are not always rational finds supportin normative Islam. Understanding the fun-damental nature of human existence can be the key towards deconstructing whyhuman beings are often influenced by cog-nitive dissonance (perceiving somethingthat in reality does not exist) and not ra-tional logic, even when making decisionsabout money matters.

The Quran uses words like nafs and ruh togive different shades to the utterly complexhuman nature. Nafs linguistically can betranslated as ‘soul’ or ‘self’. The term ‘nafs’has different uses in the Holy Quran. Inmost instances, nafs is related to the humanself. In verse 54 of chapter twelve, the Kingof Egypt summons Prophet Yusuf (AS) bysaying: ‘Bring him unto me; I will take himespecially to serve about my own person

Psychology of financial decision-making:insights from Islamic textsBy Parvez Ahmed, PhD, US Fulbright scholar and associate professor of finance at theUniversity of North Florida.

which in the financial markets leads tospectacular booms and busts. The recentsub-prime mortgage crisis was caused bygreedy bankers pushing risky loans togreedy customers who were applying know-ing full well that the debt they were assum-ing was beyond their means to repay. So aslong as the house prices were going up, thedefaults of these extremely risky loans didnot overwhelm the banking system. Duringperiods of rising house prices, the banksfound it easy to dispose of the foreclosedhomes at higher prices, thus recoveringtheir bad loans. But when house pricesstalled, the risky bets turned sour and con-tributed mightily to the current economiccrisis. The banks in their own myopic viewof profitability preyed upon the greed offolks who should have known better.

2. Nafs al-lawwama (the blaming self)

As human beings begin to discern betweenright and wrong, the human soul may startthe process of self-examination. At thisstage, the soul may blame its owner for hisor her own shortcomings. In this self-reflec-tive state the soul becomes self-observantand self-critical. In Sura al-Qiyamah Allahsays: ‘And I do call to witness the nafs thatblames’ (75:2). At this stage of its develop-ment, the soul is called nafs al-lawwamaand far from being perfect the soul at thisstage exhibits bi-polarity – rememberingand forgetting, submitting and withdraw-ing, loving and hating, rejoicing and be-coming sad, accepting and rejecting,obeying and rebelling. This nafs is thehuman conscience.

FOOD FOR THOUGHT

www.newhorizon-islamicbanking.com IIBI 23

NEWHORIZON Rajab–Ramadan 1431 FOOD FOR THOUGHT

If this stage is provided proper nurturing itcan spur human beings towards growth andperfection. Thus, under the right set of im-pulses (conditions), the human soul can beself-reflecting and self-correcting. The role of good regulation in the market is to createthe conditions that allow human beings a mo-ment of self-reflection even under the mosttempting of situations.

Well-known behavioural economist, RichardThaler, and law professor, Cass Sunstein, intheir book, ‘Nudge’, suggest that improvingthe choice architecture in mortgages by mak-ing mortgage forms easy to understand canhelp borrowers avoid the lure of sub-primemortgages. At least one economist has sug-gested banning certain type of mortgages thatare extremely misleading such as those withfeatures like negative amortisation or balloonpayments. Others favour an approach thatforces borrowers to wait for a period aftersigning their papers, allowing them the op-tion to withdraw if they become over-whelmed with the well-known psychologicalphenomenon known as ‘buyer’s remorse’.Even Islamic mortgages can improve theirchoice architecture by disclosing upfront theimplicit interest (sometimes euphemistically labeled as rate of return or profit) in a mort-gage contract. Timely, accurate and easy tounderstand disclosures of complicated finan-cial contracts will allow borrowers andbankers to avoid the greed trap.

3. Nafs al-mutma’inna (the self at peace)

When a person advances to this stage he orshe achieves harmony with their immediatesurroundings and accepts their current stateof being as God’s will. At this stage, the per-sonality shows signs of mildness, tolerance,forgiveness, and understanding. This stage ofnafs ultimately leads to resolution of one’sinner conflicts and attainment of harmonywith God. This is the soul to whom it is saidat the time of death: ‘O soul at peace, returnto your Lord, well pleased and well-pleasing.Enter with My servants, enter into My Gar-den’ (89:27-30).

This stage can be viewed as the state of ra-tionality as the Quran asserts that its message

is truly directed towards people of intellect.The foundation of intellect is rationality.Numerous times (at least 13) in the Quran,God asks a rhetorical question, ‘a fa-lataqilun?’, or ‘will you then not understandor use reason?’. For example, chapter 21,verse 67 Allah points out that worshippingone God is not just a matter of faith butalso of reason. It is not just a matter of theheart but also of the mind. While chapter23, verse 80 points out that the cosmicorder of life and death, the alteration of dayand night are not accidents but part of HisDivine Order and to understand this orderrequires exertion of intellectual energy. In itsrational state, the soul confronts and ac-cepts the reality of human existence, whichin the Quranic view is to be God-centric, es-chewing base human desires. However, thisstate of rationality does not come by osmo-sis. It is the result of striving (jihad al-akbar,considered as a major struggle and far moredifficult than fighting on a battlefield). Theone who succeeds in this struggle can riseabove and beyond the level of angels.

A Cherokee Indian legend tells of a man explaining to his son about a battle thatgoes on inside people. He said: ‘My son, thebattle is between two wolves inside us. Theevil wolf is anger, envy, jealousy, sorrow, regret, greed, arrogance, self-pity, guilt, re-sentment, inferiority, lies, false pride, superi-ority, and ego. The good wolf is joy, peace,love, hope, serenity, humility, kindness,benevolence, empathy, generosity, truth,

compassion and faith.’ The son thoughtabout it for a minute and then asked his father: ‘Which wolf wins?’ The old manreplied: ‘The one you feed.’

The best vaccinations against being the vic-tim of unscrupulous brokers and bankers is to avoid the greed trap by training thehuman soul to feel satisfied with what wehave and not long for what we do not own.The famous line in the movie ‘Wall Street’,that ‘greed is good’, has proven to be an exaggeration of truth. Being ambitious isgood, but ambition need not imply in-dulging in unmitigated hedonism. Ambitioncan also take the form of worshipping Godby helping His creation and being a goodsteward of the planet, thus embracing theideas inherent in all great philosophies (reli-gious or otherwise) that happiness resultsfrom the pursuit of what Adam Smith de-scribed as the ‘internal good’.

Beethoven wrote his ninth symphony whilehe was deaf and yet he frequently mis-placed his house keys. This has led RichardThaler and Cass Sunstein (who was BarackObama’s colleague at University of ChicagoLaw School and is one of his informal advi-sors) to ask, how can human beings be sobrilliant and yet so dumb at the same time?The answer lies in the understanding of thestages of development of the human soul.The three stages identified above are notstatic states. They are dynamic, indicatingthat human beings can vacillate between

Islamic mortgages can improve their choice architecture bydisclosing upfront the implicit interest (sometimes euphemisticallylabeled as rate of return or profit) in a mortgage contract. Timely,accurate and easy to understand disclosures of complicatedfinancial contracts will allow borrowers and bankers to avoid thegreed trap.

24 IIBI www.newhorizon-islamicbanking.com

NEWHORIZON July–September 2010FOOD FOR THOUGHT

nafs al-ammarah and nafs al-mutma’inna.If left without nurturing and spiritual de-velopment the base desires or ‘animal spir-its’ can overwhelm the cognitive faculties.Thus, the assumption so deeply held bythe Chicago school of economic thought,that markets by the power of the ‘invisiblehand’ (supply and demand) will resolvemost of society’s economic problems, isunsupported in Islamic hermeneutics. Key-nesians, on the other hand, take the viewthat markets often fail and such failure canbe repetitive rather than self-correcting.The Keynesians favour frequent interven-tions in the market to correct its excesses.

The Behaviouralists (Thaler being one ofits foremost proponents), on the otherhand, have struck a balance between thedogmatic polarity of the Chicago school’slaissez-faire and the Keynesian school’sheavy-handed governmental interventions.The Behaviouralists support the notionthat markets can sometimes experiencedeep shocks (bubbles and busts). Theseshocks are more likely when people areforced to make complicated choices. TheBehaviouralists do not support draconianregulations but view that people will haveto be given gentle nudges (Thaler and Sun-stein call it ‘libertarian paternalism’) tomotivate rational choices. Thaler and Sun-stein assert that ‘libertarian paternalism isa relatively weak, soft and non-intrusivetype of paternalism because choices arenot blocked, fenced off or significantlyburdened. A nudge, as we will use theterm, is any aspect of the choice architec-ture that alters people’s behaviour in a predictable way without forbidding anyoptions or significantly changing their economic incentives. To count as a merenudge, the intervention must be easy andcheap to avoid. Nudges are not mandates.’This view supports the idea in Islamichermeneutics that without appropriatestimulus the nafs will not travel from itsal-ammarah stage to the al-mutma’innastate.