Global MRO Commercial Fleet Dynamics & Trends · Global MRO Commercial Fleet ... Boeing, Airbus,...

16

October 18-19, 2017: Miami, USA Global MRO Commercial Fleet Dynamics & Trends

Transcript of Global MRO Commercial Fleet Dynamics & Trends · Global MRO Commercial Fleet ... Boeing, Airbus,...

October 18-19, 2017: Miami, USA

Global MRO Commercial Fleet

Dynamics & Trends

1

TODAY’S AGENDA

Global Fleet Demographics

Commercial Air Transport Fleet Forecast

Fleet Growth Risks & Implications

2Source: CAPA, Alton analysis

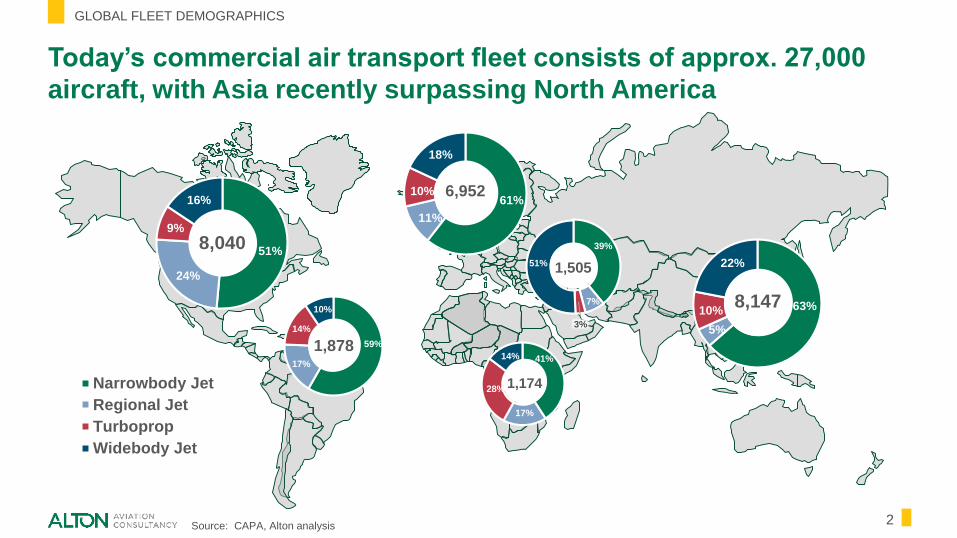

Today’s commercial air transport fleet consists of approx. 27,000

aircraft, with Asia recently surpassing North America

GLOBAL FLEET DEMOGRAPHICS

Narrowbody Jet

Regional Jet

Turboprop

Widebody Jet

51%

24%

9%

16%

8,040

61%

11%

10%

18%

6,952

63%

5%

10%

22%

8,147

59%

17%

14%

10%

1,87841%

17%

28%

14%

1,174

39%

7%

3%

51% 1,505

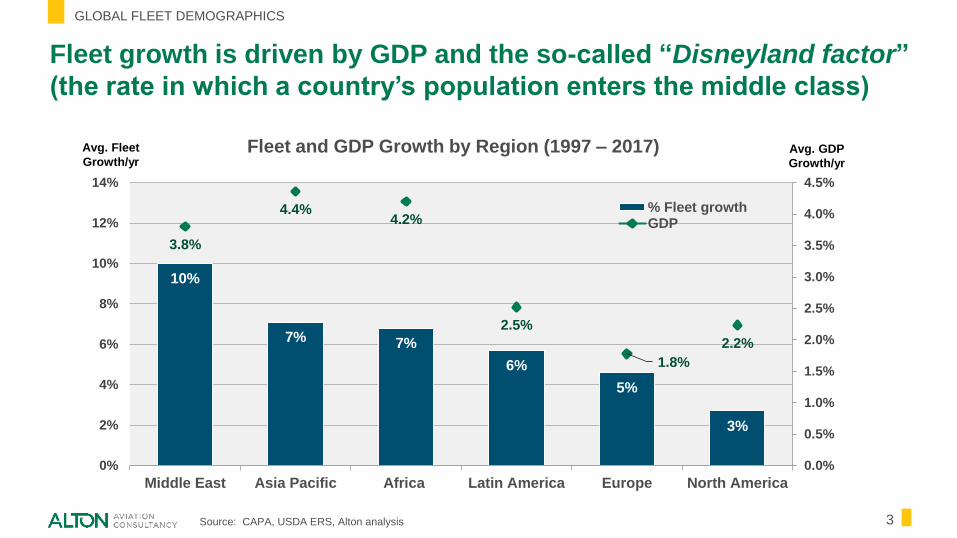

Fleet growth is driven by GDP and the so-called “Disneyland factor”

(the rate in which a country’s population enters the middle class)

GLOBAL FLEET DEMOGRAPHICS

3Source: CAPA, USDA ERS, Alton analysis

Fleet and GDP Growth by Region (1997 – 2017)

10%

7% 7%

6%

5%

3%

3.8%

4.4%4.2%

2.5%

1.8%

2.2%

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

4.0%

4.5%

0%

2%

4%

6%

8%

10%

12%

14%

Middle East Asia Pacific Africa Latin America Europe North America

% Fleet growthGDP

Avg. GDP

Growth/yr

Avg. Fleet

Growth/yr

4Source: CAPA, Alton analysis

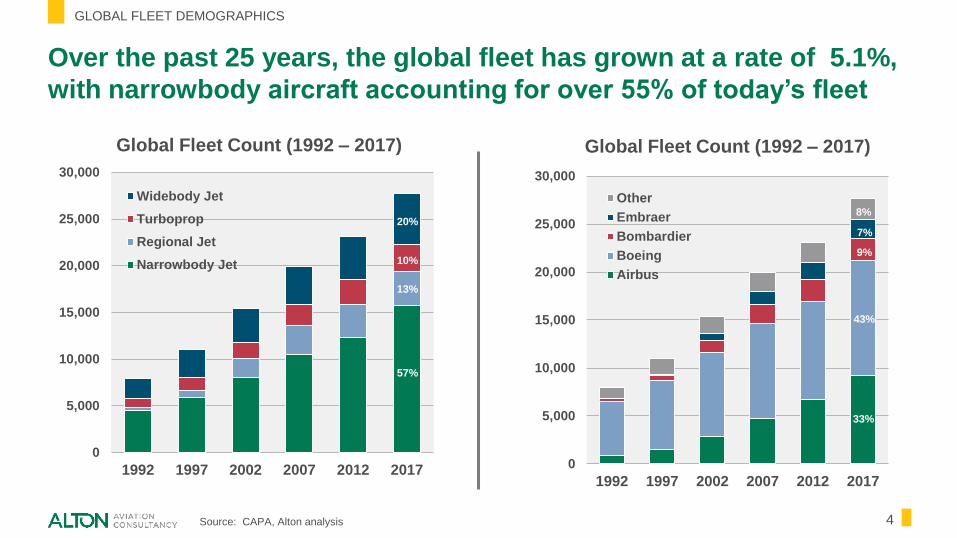

Over the past 25 years, the global fleet has grown at a rate of 5.1%,

with narrowbody aircraft accounting for over 55% of today’s fleet

GLOBAL FLEET DEMOGRAPHICS

0

5,000

10,000

15,000

20,000

25,000

30,000

1992 1997 2002 2007 2012 2017

Widebody Jet

Turboprop

Regional Jet

Narrowbody Jet

20%

10%

13%

57%

Global Fleet Count (1992 – 2017) Global Fleet Count (1992 – 2017)

0

5,000

10,000

15,000

20,000

25,000

30,000

1992 1997 2002 2007 2012 2017

Other

Embraer

Bombardier

Boeing

Airbus

33%

43%

8%

7%

9%

5Source: CAPA, Alton analysis

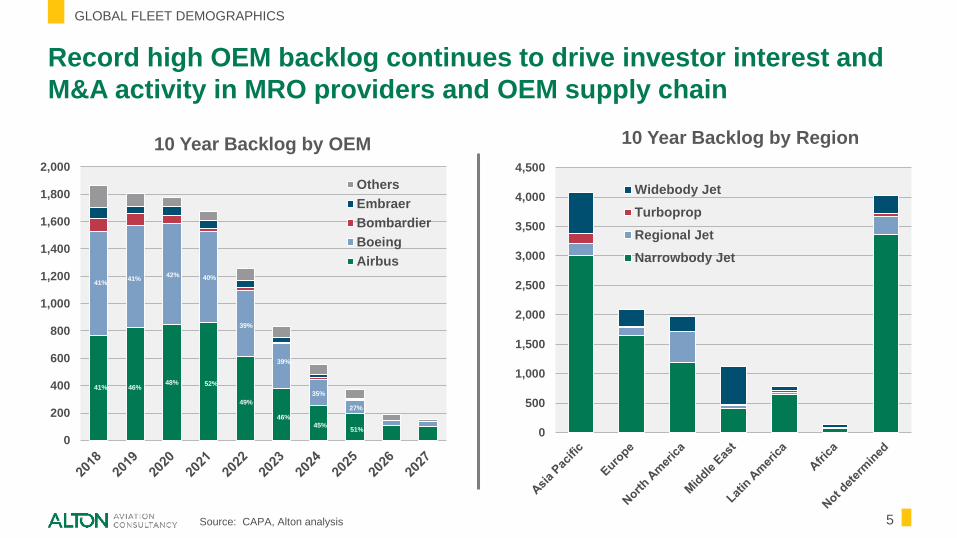

Record high OEM backlog continues to drive investor interest and

M&A activity in MRO providers and OEM supply chain

GLOBAL FLEET DEMOGRAPHICS

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

2,000

10 Year Backlog by OEM

Others

Embraer

Bombardier

Boeing

Airbus40%

45%

46%

49%

52%48%

41%

46%41%

41%

35%

39%

39%

42%

51%

27%

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

10 Year Backlog by Region

Widebody Jet

Turboprop

Regional Jet

Narrowbody Jet

6Source: CAPA, Alton analysis

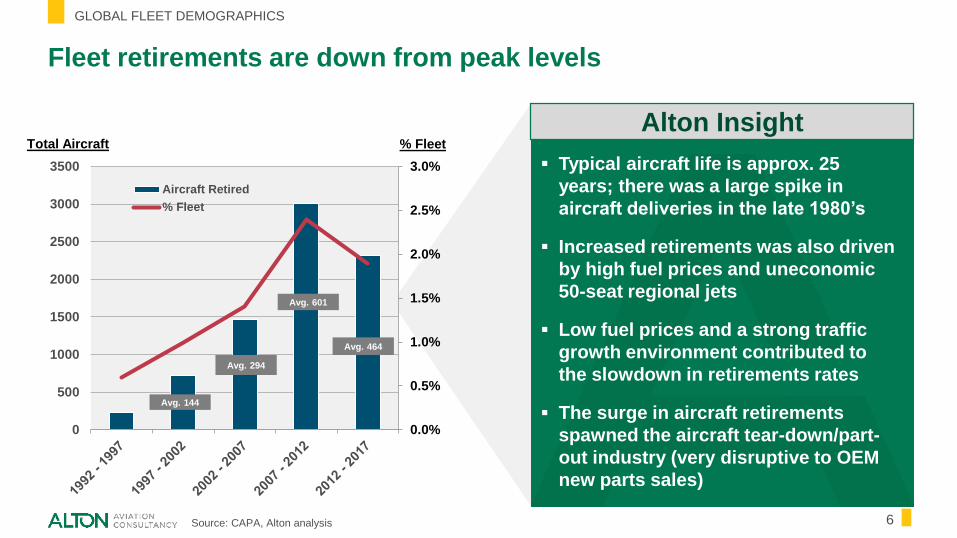

Fleet retirements are down from peak levels

GLOBAL FLEET DEMOGRAPHICS

$66B

Alton Insight

▪ Typical aircraft life is approx. 25

years; there was a large spike in

aircraft deliveries in the late 1980’s

▪ Increased retirements was also driven

by high fuel prices and uneconomic

50-seat regional jets

▪ Low fuel prices and a strong traffic

growth environment contributed to

the slowdown in retirements rates

▪ The surge in aircraft retirements

spawned the aircraft tear-down/part-

out industry (very disruptive to OEM

new parts sales)

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

0

500

1000

1500

2000

2500

3000

3500

Aircraft Retired

% Fleet

Avg. 464

Avg. 144

Avg. 601

Avg. 294

% FleetTotal Aircraft

7Source: Boeing Forecast (excludes turboprop), Alton analysis

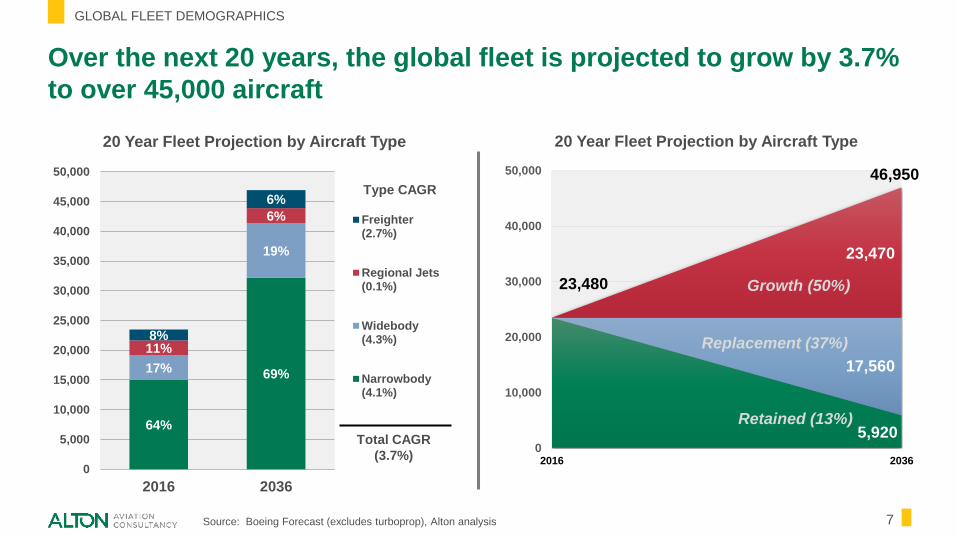

Over the next 20 years, the global fleet is projected to grow by 3.7%

to over 45,000 aircraft

23,480

5,920

17,560

23,470

0

10,000

20,000

30,000

40,000

50,000

2016 2036

Growth (50%)

46,950

Replacement (37%)

Retained (13%)

GLOBAL FLEET DEMOGRAPHICS

20 Year Fleet Projection by Aircraft Type

64%

69%17%

19%

11%

6%

8%

6%

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

45,000

50,000

2016 2036

Freighter(2.7%)

Regional Jets(0.1%)

Widebody(4.3%)

Narrowbody(4.1%)

Type CAGR

Total CAGR

(3.7%)

20 Year Fleet Projection by Aircraft Type

8

FLEET GROWTH RISKS & IMPLICATIONS

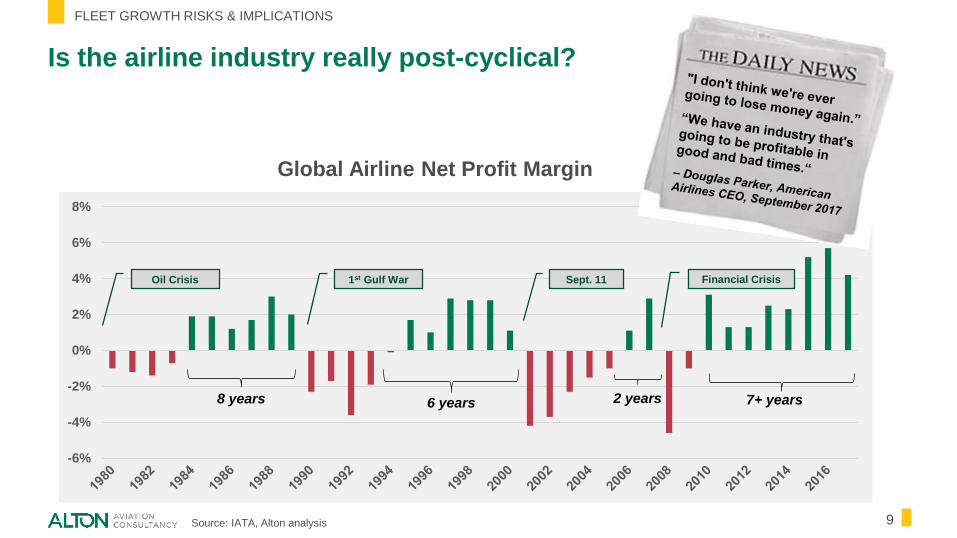

9Source: IATA, Alton analysis

Is the airline industry really post-cyclical?

FLEET GROWTH RISKS & IMPLICATIONS

$66B-6%

-4%

-2%

0%

2%

4%

6%

8%

Financial CrisisSept. 111st Gulf WarOil Crisis

Global Airline Net Profit Margin

8 years 6 years 2 years 7+ years

10Source: Boeing, Airbus, CAPA, Alton analysis

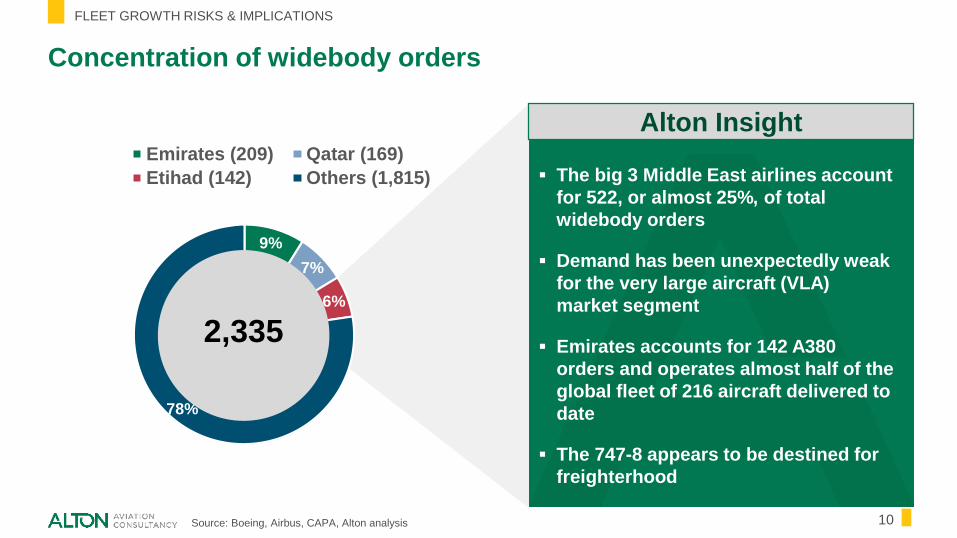

Concentration of widebody orders

FLEET GROWTH RISKS & IMPLICATIONS

$66B

Alton Insight

▪ The big 3 Middle East airlines account

for 522, or almost 25%, of total

widebody orders

▪ Demand has been unexpectedly weak

for the very large aircraft (VLA)

market segment

▪ Emirates accounts for 142 A380

orders and operates almost half of the

global fleet of 216 aircraft delivered to

date

▪ The 747-8 appears to be destined for

freighterhood

9%

7%

6%

78%

Emirates (209) Qatar (169)

Etihad (142) Others (1,815)

2,335

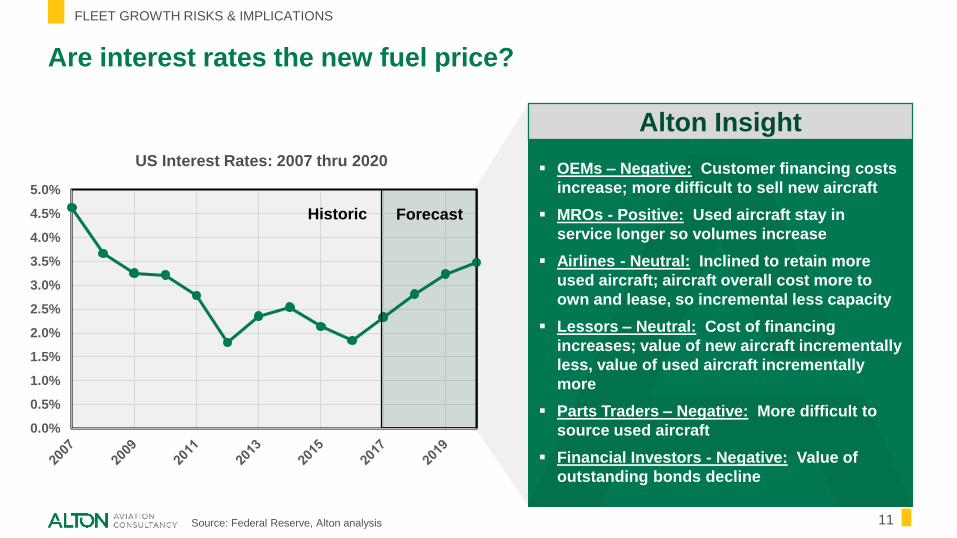

11Source: Federal Reserve, Alton analysis

Are interest rates the new fuel price?

FLEET GROWTH RISKS & IMPLICATIONS

Alton Insight

▪ OEMs – Negative: Customer financing costs

increase; more difficult to sell new aircraft

▪ MROs - Positive: Used aircraft stay in

service longer so volumes increase

▪ Airlines - Neutral: Inclined to retain more

used aircraft; aircraft overall cost more to

own and lease, so incremental less capacity

▪ Lessors – Neutral: Cost of financing

increases; value of new aircraft incrementally

less, value of used aircraft incrementally

more

▪ Parts Traders – Negative: More difficult to

source used aircraft

▪ Financial Investors - Negative: Value of

outstanding bonds decline

US Interest Rates: 2007 thru 2020

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

4.0%

4.5%

5.0%

Historic Forecast

12

SUMMARY &

CONCLUSION

▪ Overall, the state of the aviation industry is strong

▪ Airbus’ C-Series investment is an industry game changer

▪ Over-concentration of widebody orders in the Middle East

▪ Limited market demand for the very large aircraft (VLA) segment

▪ Interest rates are the new fuel cost

ALTONAVIATION.COM

NEW YORK | HONG KONG | BEIJING | TOKYO

Jonathan M. Berger

+1 212 301 0573

14

Agile. Global. Independent.

COMPANY INTRODUCTION

Alton Aviation Consultancy is a boutique aviation consulting firm

with deep domain expertise across the aviation value chain

Aircraft Leasing &

Financing AdvisoryAirlines

Aviation &

Aerospace Investors

Business &

General Aviation

Aerospace Manufacturers

& Supply ChainMRO & Aftermarket Airports Specialty Projects

In China, Alton Aviation Consultancy is known as 德世国际航空咨询(北京)有限公司, or De Shi.

Alton supports a global client base from offices in the U.S., China,

Hong Kong, and Tokyo, with additional associates worldwide

COMPANY INTRODUCTION

380 Lexington Avenue

17TH Floor

New York, New York 10168

USA

+1 212 256 [email protected]

New York

8 Guanghua Dongli

China Overseas Plaza

South Tower, Floor 11,

Suite A053

Chaoyang, Beijing 100020

China

+86 10 8598 4981

Beijing

136 Des Voeux Road Central

Suite 903

Central

Hong Kong

+852 8191 [email protected]

Hong Kong

Konan

Minato-Ku

Tokyo, Japan

+81 90 8057 1956

Tokyo

15