Global market review of automotive tyres forecasts to 2017 2010

96

Global market review of automotive tyres – forecasts to 2017 2010 edition

Transcript of Global market review of automotive tyres forecasts to 2017 2010

Global market review of automotive tyres – forecasts to 2017

2010 edition

Page i

© 2010 All content copyright Aroq Ltd. All rights reserved.

Global market review of automotive

tyres – forecasts to 2017

2010 edition

April 2010

By Matthew Beecham

Published by

Aroq Limited

Seneca House

Buntsford Park Road

Bromsgrove

Worcestershire

B60 3DX

United Kingdom

Tel: +44 (0)1527 573 600

Fax: +44 (0)1527 577 423

Web: www.just-auto.com

Registered in England no: 4307068

Page ii

© 2010 All content copyright Aroq Ltd. All rights reserved.

Single-user licence edition

This report is provided for individual use only. If you would like to share this

report with your colleagues, please order additional copies or sign up for a

multi-user licence by contacting:

Chris Clarke

Research manager, just-auto.com

Tel: +44 (0)1527 573 615

Email: [email protected]

Copyright statement

© 2010 All content copyright Aroq Limited. All rights reserved.

This publication, or any part of it, may not be copied, reproduced, stored in a

retrieval system, or be transmitted in any form by any means electronic,

mechanical, photocopying, recording or otherwise without the prior written

permission of Aroq Limited. This report is the product of extensive research

work. It is protected by copyright under the Copyright, Designs and Patents Act

1988. The authors of Aroq Limited’s research reports are drawn from a wide

range of professional and academic disciplines. The facts within this report are

believed to be correct at the time of publication but cannot be guaranteed. All

information within this study has been reasonably verified to the author’s and

publisher’s ability, but neither accept responsibility for loss arising from

decisions based on this report.

Incredible ROI for your budget – single and multi-user licences

We understand the pressure your research budget is under and price our

reports realistically. You won’t find our reports with four, or even five-figure

price tags, but you will find that they make some of the competition look

expensive. Each title is available to you on a single-user basis, supplied on the

strict understanding that each title is not to be copied or shared. Alternatively,

titles can be shared within departments or entire corporations via a cost-

effective multi-user licence. Multi-user licences can also save you money by

avoiding unnecessary order duplication. To further add value, all multi-user

Page iii

© 2010 All content copyright Aroq Ltd. All rights reserved.

copies are hosted on a password protected extranet for your department or

company – saving you time, resources and effort when sharing research with

your colleagues. To find out more about multi-user pricing, please contact

Chris Clarke.

just-auto.com membership

From just GBP99/US$170/EUR120* a year you will gain access to a growing

portfolio of exclusive management briefing reports, and also receive 12 new

briefings for each year you are a member. As well as this impressive list of

members’ only reports, you also gain one year’s access to a constantly-

updated stream of news, feature articles and analysis. Established in 1999,

just-auto has rapidly evolved into the premier source of global automotive

news, analysis and data for busy senior executives. For details of the current

special joining offer visit: www.just-auto.com/offer.aspx

*Prices correct at time of publication.

Page iv Contents

© 2010 All content copyright Aroq Ltd. All rights reserved.

Contents

Single-user licence edition .......................................................................................................... ii

Copyright statement ............................................................................................................... ii Incredible ROI for your budget – single and multi-user licences ............................................. ii just-auto.com membership ..................................................................................................... iii

Contents ...................................................................................................................................... iv

List of figures .............................................................................................................................. vi

List of tables .............................................................................................................................. vii

Preface ........................................................................................................................................ ix

Research methodology ......................................................................................................... ix Report coverage ................................................................................................................... ix The author ............................................................................................................................. x

Chapter 1 Introduction ................................................................................................................ 1

Chapter 2 The market .................................................................................................................. 2

Market trends ......................................................................................................................... 2 Market players ....................................................................................................................... 4

Bridgestone ................................................................................................................... 5 Q&A with Bridgestone ............................................................................................. 5

Continental .................................................................................................................. 10 Q&A with Continental ............................................................................................ 10

Cooper Tire & Rubber .................................................................................................. 14 Q&A with Cooper Tire & Rubber ........................................................................... 15

Goodyear..................................................................................................................... 21 Q&A with Goodyear Dunlop UK ............................................................................ 22

Hankook Tire ............................................................................................................... 27 Kumho Tires ................................................................................................................ 27 Michelin ....................................................................................................................... 27 Pirelli ........................................................................................................................... 28

Toyo Tire & Rubber ..................................................................................................... 28 Sumitomo Rubber Industries ....................................................................................... 28 Yokohama Rubber ....................................................................................................... 29

Emerging markets ................................................................................................................ 32 Brazil ........................................................................................................................... 32

China ................................................................................................................................... 32 Hungary ....................................................................................................................... 34 India ............................................................................................................................ 34 Mexico ......................................................................................................................... 34 Romania ...................................................................................................................... 34 Russia ......................................................................................................................... 35

Page v Contents

© 2010 All content copyright Aroq Ltd. All rights reserved.

Thailand ...................................................................................................................... 35 Turkey ......................................................................................................................... 36 Investments in Europe ................................................................................................. 36 Investments in North America ...................................................................................... 36 Investments in Asia...................................................................................................... 37

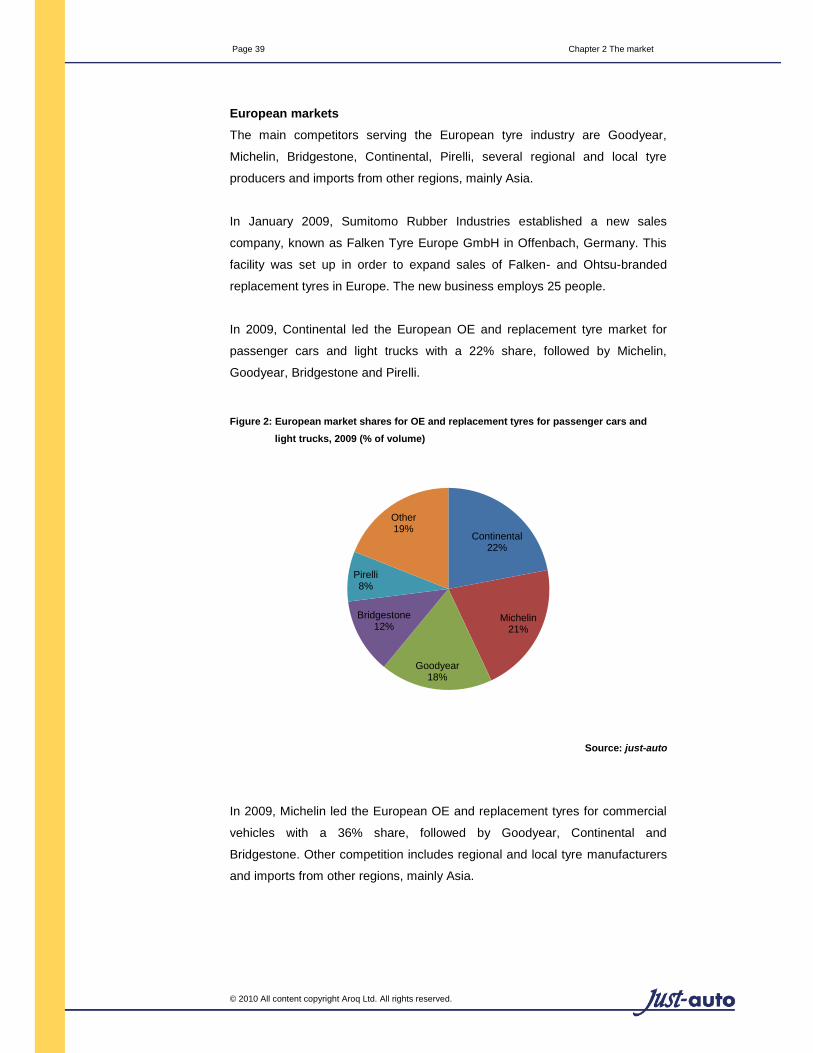

Market shares ...................................................................................................................... 37 World ........................................................................................................................... 37 European markets ....................................................................................................... 39 North American markets .............................................................................................. 40 Asian markets .............................................................................................................. 42

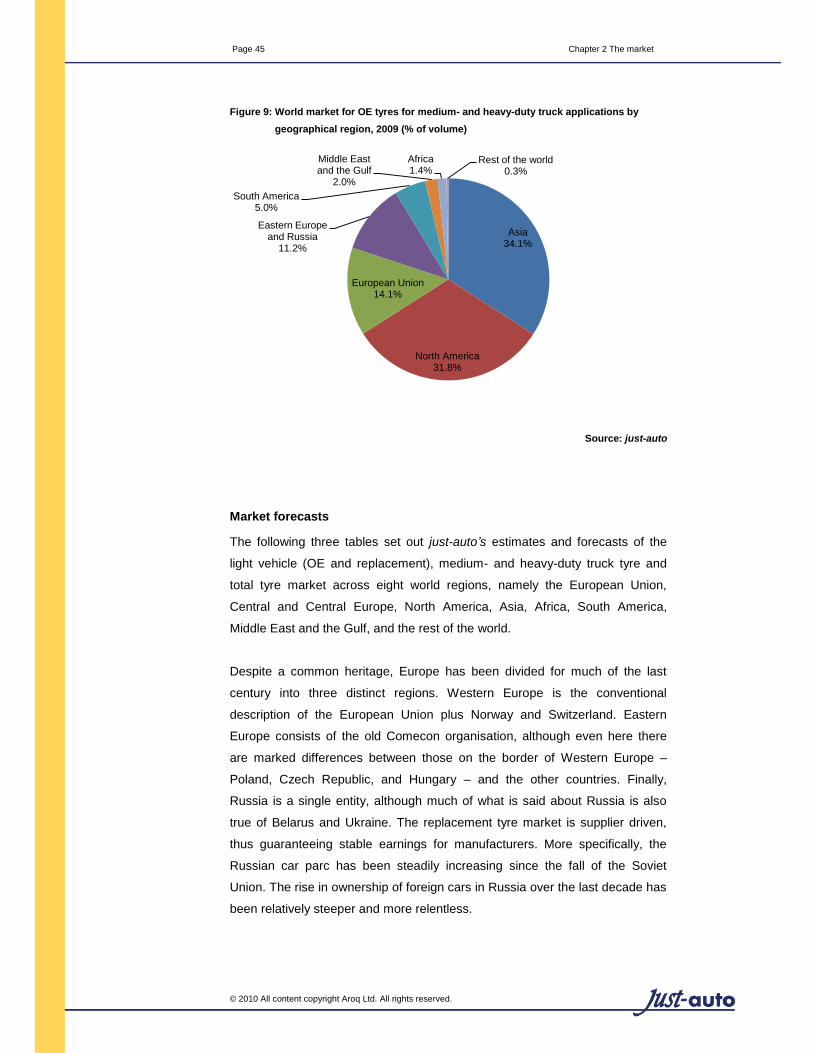

Market size .......................................................................................................................... 44 Market forecasts .................................................................................................................. 45

Chapter 3 Technical review ....................................................................................................... 53

Defining the elements .......................................................................................................... 53 Run-flat tyres ....................................................................................................................... 54 Tyre labelling ....................................................................................................................... 56 Tyre pressure monitoring systems (TPMS) .......................................................................... 56 Other innovations ................................................................................................................. 57

Chapter 4 Manufacturers ........................................................................................................... 58

Bridgestone ......................................................................................................................... 58 Continental .......................................................................................................................... 59 Cooper Tire & Rubber .......................................................................................................... 66 Goodyear ............................................................................................................................. 67

Hankook Tire ....................................................................................................................... 73 Kumho Tires ........................................................................................................................ 75 Michelin ............................................................................................................................... 77 Pirelli .................................................................................................................................... 79 Sumitomo Rubber Industries ................................................................................................ 80 Toyo Tire & Rubber Co Ltd .................................................................................................. 82 Yokohama Rubber ............................................................................................................... 82

Appendix: Glossary of terms .................................................................................................... 84

Page vi List of figures

© 2010 All content copyright Aroq Ltd. All rights reserved.

List of figures

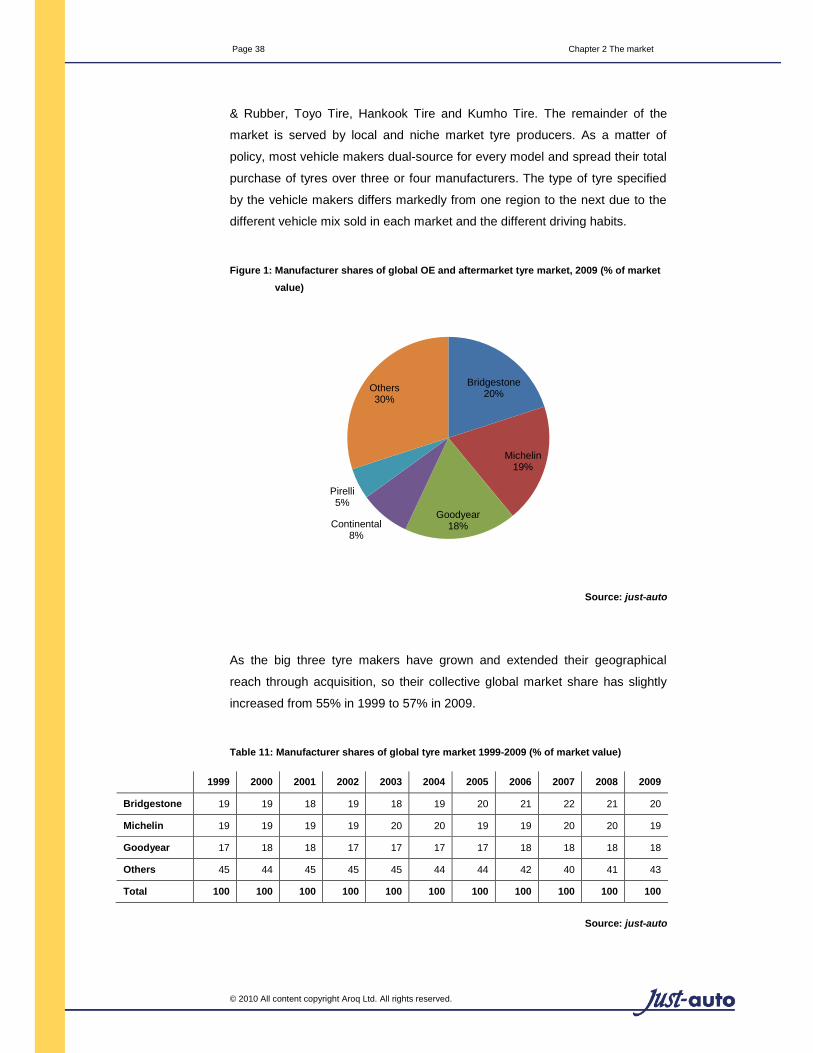

Figure 1: Manufacturer shares of global OE and aftermarket tyre market, 2009 (% of market value)

.............................................................................................................................. 38

Figure 2: European market shares for OE and replacement tyres for passenger cars and light

trucks, 2009 (% of volume) .................................................................................... 39

Figure 3: European market shares for OE and replacement tyres for medium- and heavy-duty

trucks, 2009 (% of volume) .................................................................................... 40

Figure 4: North America market shares for OE and replacement tyres for passenger cars and light

trucks, 2009 (% of volume) .................................................................................... 41

Figure 5: North American market shares for OE and replacement tyres for medium and heavy duty

trucks, 2009 (% of volume) .................................................................................... 41

Figure 6: South Korean OE tyre market shares, 2009 (% of volume) ........................................... 43

Figure 7: South Korean replacement tyre market shares, 2009 (% of volume) ............................. 43

Figure 8: World market for OE tyres for passenger cars and light truck applications by

geographical region, 2009 (% of volume) ............................................................... 44

Figure 9: World market for OE tyres for medium- and heavy-duty truck applications by

geographical region, 2009 (% of volume) ............................................................... 45

Figure 10: Continental AG’s passenger and light trucks tyres sales by region, 2007 and 2008 (% of

net sales) ............................................................................................................... 61

Figure 11: Continental AG’s commercial vehicle tyres sales by region, 2007 and 2008 (% of net

sales) ..................................................................................................................... 63

Page vii List of tables

© 2010 All content copyright Aroq Ltd. All rights reserved.

List of tables

Table 1: Tyre size trends over six generations of VW Golf ............................................................. 4

Table 2: Bridgestone’s sales by geographical region, 2003-2008 (% of net sales) ....................... 29

Table 3: Goodyear’s tyre sales by operating segment, 2006-2008 (% of net sales) ...................... 29

Table 4: Michelin’s sales by geographical region, 2003-2008 (% of net sales) ............................. 30

Table 5: Cooper Tire & Rubber’s sales by geographical region, 2003-2008 (% of net sales) ........ 30

Table 6: Hankook Tire’s sales by geographical region, 2003-2008 (% of net sales) ..................... 30

Table 7: Kumho Tire’s sales by geographical region, 2003-2007 (% of net sales) ........................ 31

Table 8: Pirelli’s sales by geographical region, 2003-2008 (% of net sales) .................................. 31

Table 9: Toyo Tire & Rubber’s sales by geographical region, 2003-2009 (% of net sales) ............ 31

Table 10: Yokohama’s sales by geographical region, 2003-2009 (% of net sales) ....................... 32

Table 11: Manufacturer shares of global tyre market 1999-2009 (% of market value) .................. 38

Table 12: World light vehicle tyre sales by region, split by OE and replacement units, 2006-2017

(m units)................................................................................................................. 46

Table 13: European Union light vehicle tyre replacement units by market, 2006-2017 (m units) ... 48

Table 14: World medium- and heavy-duty truck tyre sales by region, split by OE and replacement

units, 2006-2017 (m units) ..................................................................................... 49

Table 15: World tyre sales (all applications) by region, split by OE and replacement units, 2006-

2017 (m units) ........................................................................................................ 51

Table 16: Bridgestone’s three generations of run-flat tyres, 1987-2010 ........................................ 55

Table 17: Bridgestone’s production and R&D operations worldwide, 2009 ................................... 59

Table 18: Goodyear’s tyre sales by operating segment, 2006-2008, (m tyres) ............................. 68

Table 19: Goodyear’s worldwide tyre sales, OE and replacement, 2003-2008 (m tyres) .............. 68

Table 20: Goodyear’s North American Tire sales, OE and replacement, 2003-2008 (m tyres) ..... 69

Table 21: Goodyear’s European Union Tire sales, OE and replacement, 2006-2008 (m tyres) .... 69

Table 22: Goodyear’s Latin American Tire sales, OE and replacement, 2003-2008 (m tyres) ...... 69

Page viii List of tables

© 2010 All content copyright Aroq Ltd. All rights reserved.

Table 23: Goodyear’s Asia Pacific Tire sales, OE and replacement, 2003-2008 (m tyres) ............ 70

Table 24: Goodyear’s strategic business units, 2010 ................................................................... 70

Table 25: Goodyear’s tyre-related facilities worldwide, 2010 ........................................................ 71

Table 26: Hankook Tire’s consolidated sales and operating profit, fiscal years 2008, 2009 and

forecast for 2010, (KRW bn) .................................................................................. 75

Table 27: Michelin’s production sites worldwide, 2009 ................................................................. 77

Table 27 (continued): Michelin’s production sites worldwide, 2009 ............................................... 78

Table 27 (continued): Michelin’s production sites worldwide, 2009 ............................................... 79

Table 28: Pirelli tyre plants worldwide, 2010 ................................................................................ 79

Table 29: Sumitomo Rubber Industries’ net sales and operating income, 2006, 2007, 2008 and

nine months ended 30 September 2008 and 2009 (JPY m) ................................... 81

Table 30: The Yokohama Rubber Co Ltd’s tyre-related facilities in Japan, 2010 .......................... 83

Note: data in some tables may not sum due to rounding.

Page ix Preface

© 2010 All content copyright Aroq Ltd. All rights reserved.

Preface

Research methodology

This report is intended to provide an overview of the road tyre industry,

providing top level market fitment, volume and value forecasts through 2017.

Our forecasts are not extrapolative but dependent on the underlying drivers of

supply and demand. Our forecasts are largely based on interviews with the

author’s extensive international network of industry contacts. This allows us to

consider and explain the meaning and implications of industry events, rather

than offer simple description based on incomplete data.

Our approach is divided into two distinct methodologies:

○ qualitative interviews – these are generally opinion-based, which aim

to build knowledge about future tyre market trends and company

strategies;

○ quantitative interviews – typically fact-based, focused on establishing

market values, shares, and volumes.

Our research typically concentrates on applications for light vehicles which

include all cars, light trucks and the various cross-over vehicle styles such as

sports utility vehicles and people carriers. These vehicles collectively account

for about 96% of the global vehicle build.

Our market forecasts are set out by region, i.e. European Union, Eastern

Europe and Russia, North America, Asia, Africa, South America, Middle East

and the Gulf, and the rest of the world. For the purposes of this report, the

European Union includes Austria, Belgium, Denmark, Finland, France,

Germany, Greece, Ireland, Italy, the Netherlands, Portugal, Spain,

Switzerland, Sweden and the UK.

Report coverage

In this, the sixth edition of this report, just-auto reviews the key market drivers

for road tyres, and updates the market analysis. Following our market overview

in Chapter 1, just-auto’s product fitment forecasts in Chapter 2 predict in some

detail how the OE and replacement market for passenger car, light truck,

medium- and heavy-duty truck tyre market will evolve in the European Union;

Page x Preface

© 2010 All content copyright Aroq Ltd. All rights reserved.

Eastern Europe and Russia; North America; Asia; Africa; South America;

Middle East and the Gulf; and the rest of the world from 2006 through to 2017.

This chapter includes exclusive Q&As with Bridgestone, Cooper Tire &

Rubber, Continental and Goodyear. An updated review of new product

developments is presented in Chapter 3, while Chapter 4 provides profiles of

the major manufacturers, namely Bridgestone, Continental, Cooper Tire &

Rubber, Goodyear, Hankook Tires, Kumho, Michelin, Pirelli, Sumitomo, Toyo

Tires, and Yokohama.

The author

Matthew Beecham has more than 18 years’ experience of researching, writing

and analysing market and technical trends in the global automotive

components industry. Since 2000, he has served as an associate editor for

just-auto. In addition to tyres, he authors a range of global auto components’

market research reviews, including batteries, braking systems, coatings,

clutches, cockpits, driver assistance systems, door modules, electric motors,

engine cooling systems, exhaust systems, front-end modules, fuel injection,

fuel tanks, glazing systems, ignitions, interiors, lighting, mirrors, roof systems,

shock absorbers, spark plugs, rotating electrics, tyre pressure monitoring

systems, wheels and wipers. Matthew’s freelance assignments have included

working for AT Kearney, Belron, Bridgehead International, McKinsey, Kuwait

Institute for Scientific Research, Motorsport Industry Association, Motor

Industry Research Association and the Economist Intelligence Unit. He has

also written for magazines including Car Graphic (Japan), JAMA (Japan) and

Automotive Engineer (UK). He was awarded a PhD in automotive technology

transfer from Cranfield University.

Page 3 Chapter 2 The market

© 2010 All content copyright Aroq Ltd. All rights reserved.

He continued: “Last year, a good 15m of these tyres – which are manufactured

in sizes between 17 inches and 23 inches – were sold to markets in Western

and Central Europe. We expect demand to rise to 20.4m tyres by 2012. This

represents a growth of more than 35% compared with 2007 levels.” The main

European markets for these UHP tyres are the UK, Germany, France, Italy,

and Spain. “The UK and Germany alone constitute almost half of sales in the

sector,” said Setzer. “However, seen as a percentage we are expecting sales

of high-performance tyres to increase even more in southern Europe than in

the UK and Germany.”

Hankook Tire also reports strong growth in UHP tyres. In its latest earnings

announcement, the company stated: “[Our] overall global sales of UHP marked

a 9.6% year-over-year increase. In particular, Hankook Tire’s UHP supplies to

global carmakers showed remarkable growth in the global market and in China

with 129% and 46% year-over-year increases, respectively.” Meanwhile,

Kumho Tire used the 2009 Frankfurt motor show to introduce its latest UHP

tyres.

Other factors impacting on tyre design include increased chassis development.

In addition, the larger number of car segments have led to an increase in the

complexity of the tyre market. Performance no longer just relates to speed

alone. The fact that comfort, noise levels, safety and traction have become

increasingly important means that so-called performance tyres are often fitted

to cars from the lower medium sector of the market. The W, Y, Z and 4x4

markets have been showing strong growth thanks to the trends in the

performance sector and a desire for alloy wheels. There has also been a

change with regard to tyre dimensions, partly because people like highly styled

wheels with low profile tyres.

To illustrate how tyre sizes have changed over the years as vehicles have

become heavier, Michelin draws upon the example of the Volkswagen Golf.

Page 4 Chapter 2 The market

© 2010 All content copyright Aroq Ltd. All rights reserved.

Table 1: Tyre size trends over six generations of VW Golf

VW Golf 1 VW Golf 2 VW Golf 3 VW Golf 4 VW Golf 5 VW Golf 6

Engine 1.1 L 1.3 L 1.4 L 1.6 L 1.6 L FSI 16 V 1.4 L TSI

Horse power

50 55 60 100 115 121

Empty vehicle (kg)

750 845 960 1,175 1,185 1,215

Tyre size 155/80SR13 175/70SR13 175/70TR13 155/80HR14 195/65HR15 205/55HR16

Source: Michelin

Although the tyre market has been growing – albeit at a modest rate year-on-

year – the industry has not been particularly profitable. It is essentially a

commodity industry and although it has high-tech products, the majority of its

products are vulnerable to price competition from low-cost manufacturers. An

obvious reaction has been the development of brands, but an examination of

the accounts of companies in the industry shows that there are some distinct

advantages in size. In many analyses, the big three manufacturers are

demonstrated to have a clear advantage over their smaller competitors and it

is this in-built disadvantage that has encouraged the mid-sized companies to

look for alternative courses. None have given up the tyre industry as they have

too much invested in it.

In summing-up the world market for tyres, Michelin states: “With emerging

countries experiencing vigorous growth, tyre market volume growth should be

fairly evenly distributed between mature and developing countries. In addition,

all tyre markets have a strong value growth potential due to increasing demand

for top-of-the-range vehicles (as road users look for more safety and comfort),

the need for the trucking industry to improve its returns and equipment

reliability. Beyond these volume and value growth trends, markets are on the

verge of profound changes driven by growing environmental concerns.”

Market players

The major competitors in the global tyre market include Goodyear, (based in

the US), Bridgestone (based in Japan) and Michelin (based in France). Other

significant market players include Continental, Cooper, Hankook, Kumho,

Pirelli, Toyo, Yokohama and various regional tyre manufacturers.

Page 5 Chapter 2 The market

© 2010 All content copyright Aroq Ltd. All rights reserved.

The basis of competition among tyre makers includes product design,

performance, price, reputation, warranty terms, customer service and

consumer convenience.

Bridgestone

Bridgestone produces tyres and tubes for passenger cars, trucks, buses,

construction and mining vehicles, industrial and agricultural machinery, aircraft,

motorcycles and scooters. Tyres account for 80% of Bridgestone’s sales.

Bridgestone also produces antivibration and noise-insulating materials,

polyurethane foam products, office equipment, industrial rubber products,

building materials, belts, hoses, marine products and other rubber parts. Tyres

account for 80% of Bridgestone Group sales worldwide. The company

operates facilities in Argentina, Australia, Belgium, Brazil, Canada, China,

Costa Rica, France, Indonesia, Italy, Japan, Mexico, New Zealand, Poland,

South Africa, Spain, Taiwan, Thailand, the UAE, the UK, the US and

Venezuela. In August 2009, Bridgestone opened its Kitakyushu plant in Japan.

This plant produces large and ultra-large off-road radial tyres for construction

and mining vehicles.

Q&A with Bridgestone

In January 2010, Matthew Beecham talked with Franco Annunziato, senior

vice president, technology, Bridgestone Europe.

just-auto: Now that legislation is coming in to make TPMS mandatory, the

motorist no longer has to pay extra. What is the future for this technology? Do

you think that indirect TPMS will become a standard feature of on future

electronic stability control systems?

Franco Annunziato: We fully support accurate TPMS, firstly as an important

safety factor, reducing the numbers of failures due to running at low pressure,

and secondly, because it can maintain the tyres’ optimum rolling resistance

when the pressure is correctly adjusted.

The indirect TPMS system relies on the ABS sensors which are fitted to almost

100% of all cars today. The electronics evaluate any difference in the speed of

rotation of one tyre versus the others so detecting a deflation.

Page 6 Chapter 2 The market

© 2010 All content copyright Aroq Ltd. All rights reserved.

A direct TPMS measures the internal pressure of the tyre with a sensor and

transmits this to a receiver in the vehicle. The electronics can then display and

follow the real internal pressure of the tyre.

The EU regulation will be a major driver to bring TPMS to all users; however it

is not yet certain which TPMS type will become mandatory.

j-a: As I understand it, TPMS technology is evolving to the point where one

scenario could be this: As soon as the TPMS tells you that your tyre needs

servicing, the nearest licensed service station will be automatically alerted

through your car’s GPS, giving you directions to a site where qualified

personnel will be awaiting your arrival. How far away are we from achieving

this?

FA: Most high-end vehicles have now a GPS system as standard equipment;

its navigation software often contains the locations of approved service

centres. Linking vehicle faults, such as low tyre pressure, and service centres

is the next logical step in such a system. Adding in the communication from car

to service centre is also becoming possible as manufacturers add internet

connectivity.

Such systems could therefore be implemented relatively soon if the car

manufacturer sees a requirement.

j-a: Run-flat tyres have also done a lot to improve vehicle safety yet come with

a high price tag. Do you see technological evolution bringing run-flat and self-

inflating tyres into the cheaper mainstream?

FA: SSR features a side-supported rubber aiming to support the load of the

vehicle when the tyre deflates.

Therefore, in principle the cost of a RFT will be higher than a regular tyre,

because of the side-supported rubber.

However SSR system means ‘spareless’ which could result in eliminating a full

spare tyre or temporary spare tyre or sealing kit. So we believe it could be

possible to equal or even improve the cost of a regular tyre when we consider

it as a complete system.

Page 7 Chapter 2 The market

© 2010 All content copyright Aroq Ltd. All rights reserved.

j-a: In addition to driver safety, the current focus is to find ways in which to

reduce CO2 emissions. As 25% of all CO2 emissions are generated by road

traffic and about 20-3% of a vehicle’s energy consumption can be attributed to

tyres alone, measures to improve rolling resistance remain a top priority. Could

you draw on an example of a recent tyre innovation which demonstrates how

your company has reduced rolling resistance?

FA: First, I would like to emphasise that although the figures you quote are

correct, the energy consumption attributed to tyres cannot be eliminated, and

will always be significant. Nevertheless, tyre companies continue to make

inroads to reducing the rolling resistance of tyres to contribute to reducing CO2

emissions.

All tyre companies are faced with the same challenge whereby tyre

performances are linked to each other. For example, it is possible to make a

tyre with far superior low rolling resistance than current tyres, but the penalty

would be that the wet braking performance of the same tyre would be

unacceptable, and even dangerous. That is why the European labelling

regulation includes both energy efficiency and wet braking performance on the

same label.

Our company has introduced nanoprotech technology in the tread rubber

compounds, which lowers the rolling resistance coefficient by reducing energy

loss in the top compound during rotation.

j-a: As we see it, most tyre manufacturers offer a low rolling resistance tyre in

their range yet few currently advertise the use of the silica-silane technology in

their commercial vehicle ranges. Why is that?

FA: The use of silica silane is a feature. Communication tends to focus on the

benefits rather than the features that actually bring those benefits.

j-a: In addition to low rolling resistance, low tyre/road noise are requirements

imposed on modern tyres for environmental and economic considerations.

Could you draw on an example of a recent tyre innovation which demonstrates

how your company has reduced rolling tyre noise, perhaps highlighting certain

new processes or developments?

Page 8 Chapter 2 The market

© 2010 All content copyright Aroq Ltd. All rights reserved.

FA: Reducing tyre road noise is a challenge for all tyre manufacturers. It has

been proven that road surfaces and the materials used to make them can

contribute more to the reduction of tyre road noise than the tyre itself. Also, the

quietest tyre possible to make is a slick, that is, a tyre with no tread pattern at

all. Slicks are not an option for normal cars as the lack of wet grip would be

unacceptable. It is the grooves of a tyre’s tread pattern that contribute to

creating external noise, but it is the same grooves that allow for water

evacuation and directional stability, and grip on wet surfaces. By optimising

tread design, it is possible to achieve the regulated noise limits, and this is

where most of the advances have been made with regards to tyre noise.

j-a: In what ways will information on the new EU tyre regulatory standards

provide a better service for the end-consumer?

FA: The end-consumer will be able to recognise the performances of each tyre

before they purchase it, thanks to a performance label that must be displayed

with the tyre, and on point-of-sale material. The label, inspired by the energy

efficiency label which is currently displayed on refrigerators and other white

goods, will show the wet grip grading of the tyre and the measured external

noise in dbA as well as the energy efficiency rating on a seven-grade scale.

Thanks to the label information, consumers can make their choice depending

on their own preference; maximum safety or maximum fuel economy.

j-a: In your view, what tyre regulatory information needs to be communicated

to the consumer?

FA: We consider safety to be of paramount importance. The only contact that

a tyre has with the road is through its tyre footprints. In the interests of road

safety, customers need to understand safety performances.

As end-users are increasingly seeking ways to reduce their impact on the

environment, the fuel efficiency of their vehicle has become the first criterion

when choosing their new car. Tyre performance also affects the fuel efficiency

of a vehicle. Therefore, communicating this value to consumers is very

important.

j-a: As I understand it, truck tyres are included in the requirement for tyre

labelling. Would you agree that, given the importance of truck tyres to the

Page 9 Chapter 2 The market

© 2010 All content copyright Aroq Ltd. All rights reserved.

economy of fleet transport, purchasers of truck tyres should receive greater

clarity through the use of labelling?

FA: We agree that fleet operators also need information on tyre performance.

However, our experience is that purchasers of truck tyres are usually well

informed professionals with real data available to them showing the economic

effect of their tyres on their operations. This data includes many additional

performances that are not considered in car tyre usage. For example, the

durability and life of the tyres, and their suitability for reuse as retreaded tyres,

thereby saving both money and environmental impact.

j-a: Ultimately, I guess if the information on the tyre sidewall was easier to

read, it could be a better method of communicating information instead of

sticky pictogram labels which could be dirty, incorrect or even missing at the

point-of-sale. Would you agree?

FA: The regulation foresees that the label information will be communicated by

several other methods such as on websites, and printed material available at

points of sale, so it is not at all confined to sticky labels. Incorporating the

information on tyre sidewalls has several disadvantages. It is often difficult to

read and understand sidewall printed information. The information is basically

only needed before the tyres are purchased, and has no meaningful role once

the tyre choice and purchase has been made. The actual physical tyres being

purchased are often not seen by the customer until after they have been fitted

to the car. They are chosen from catalogues, website information and the

advice of sales staff using sales brochures.

j-a: In the medium term, is RFID a better solution?

FA: Not for informing customers before they make their purchase decision.

RFID is good for identifying and tracking the performance of tyres once they

are in operation.

j-a: People talk of the intelligent tyre as vehicles change. With newer forms of

propulsion, in what ways will the tyre change and adapt to such technology?

FA: There have been, and still are, many research projects looking at various

ways to bring information from the tyre to the vehicle. As the tyre is the contact

point to the road, dynamic feedback in real time of tyre/surface interaction

Page 10 Chapter 2 The market

© 2010 All content copyright Aroq Ltd. All rights reserved.

could provide benefits to ESP, ABS and other systems reliant on knowledge of

the level of tyre grip. Unfortunately, integrating electronics inside such a harsh

environment, with high rotational and shock g forces, is not simple, especially

as adding weight has a negative impact on vehicle dynamics. Many in-vehicle

sensing systems can already estimate grip levels quite well, so cost/benefit is

not high to have an in-tyre solution.

For future vehicles, whether fossil-fuelled, electric or some hybrid form, the

need to maintain safety and optimise rolling resistance will be increasingly

important so TPMS should become a key vehicle component.

Continental

Continental AG designs and manufactures tyres for passenger car and

commercial vehicle applications. Through an alliance with Yokohama Rubber

Co, the partners rank as one of the world’s largest tyre manufacturers. The

company also develops brake systems, electronic chassis systems and

integrated starter-alternator technology. Its passenger and light truck tyres

business produces passenger car and light truck tyres at its factories in Spain,

Germany, France, Mexico, China and the US. Continental’s commercial

vehicle tyres business operates facilities located in Germany, Austria and the

US. Over the past few years, Continental has invested in new products in

order to consolidate and extend its market leadership in Europe. In spring

2010, the company plans to launch its so-called ContiSportContact 5 P tyre for

a sports car. This company will subsequently launch its ContiSportContact 5 in

spring 2011.

Q&A with Continental

In January 2010, Matthew Beecham talked with executives of Continental AG

about its tyre innovations.

just-auto: Run-flats have done a lot to improve vehicle safety yet come with a

high price tag. Do you see technological evolution bringing run-flat and self-

inflating tyres into the cheaper mainstream?

Continental: This depends not only on us as a manufacturer of tyres but on

the automobile industry itself. To get cheaper versions of tyres with extended

mobility technologies we need more cars produced with these technologies,

not just a handful of manufacturers of mid- and luxury-class vehicles. On the

other hand, we produce not only tyres with run-flat technologies like SSR [self

Page 11 Chapter 2 The market

© 2010 All content copyright Aroq Ltd. All rights reserved.

supporting run-flat] tyres but other run-flat technologies as well, like ContiSeal

or ContiComfortKit. So we have extended mobility systems over a broad range

for nearly any need and application.

j-a: In addition to driver safety, the current focus is to find ways in which to

reduce CO2 emissions. As 25% of all CO2 emissions are generated by road

traffic and about 20-30% of a vehicle’s energy consumption can be attributed

to tyres alone, measures to improve rolling resistance remain a top priority.

Could you draw on an example of a recent tyre innovation which demonstrates

how your company has reduced rolling resistance?

Continental: We do not only look [at] rolling resistance but [at] the

combination with all safety-relevant improvements on tyres. Therefore we

would speak about our tyre for the blue technology cars from VW and other

companies that are equipped, for example, with the ContiPremiumContact 2.

This tyre combines safety and low rolling resistance at a high level. We can

produce this tyre because we know the car and its driver assistance systems,

such as ESC. With this knowledge, we can combine short braking distances –

even on wet roads – with a lower rolling resistance.

j-a: In addition to low rolling resistance, low tyre/road noise is a requirement

imposed on modern tyres for environmental and economic considerations.

Could you draw on an example of a recent tyre innovation which demonstrates

how your company has reduced rolling tyre noise, perhaps highlighting certain

new processes or developments?

Continental: Based on the upcoming noise regulations, the tyre type we have

to focus on is the drive axle tyre. Rib tyres – which are usually used on front

and trailer axles – are already noise optimised because of their tread design

structure. Due to the special demand on traction, drive axle tyres have to

follow a certain tread design which makes some additional noise optimisation

necessary. Therefore we are working with the German road association, BASt

(Bundesanstalt für Straßenwesen) and some universities with the aim lowering

these emissions. Within this co-operation we want to achieve a noise reduction

of 3-4dB for certain tyre types in order to meet the new regulation.

j-a: In what ways will information on the new EU tyre regulatory standards

provide a better service for the end-consumer?

Page 12 Chapter 2 The market

© 2010 All content copyright Aroq Ltd. All rights reserved.

Continental: We feel that consumers can be better informed about short

braking distances, rolling resistance and tyre noise. And we expect motorists

will find out that there is a general target conflict in short braking distances, low

rolling resistance and low noise. The EU tyre label gives a short overview

about the performance information regarding these criteria which is good – but

it is still reflecting only three of more than ten tyre performance criteria.

j-a: In your view, what tyre regulatory information needs to be communicated

to the consumer?

Continental: Based on the diametric physical target conflicts of very low

rolling resistance and best braking results, consumers should be informed that

these criteria depend on each other systematically – both of which cannot be

maximised at the same time. Consumers should also be informed that the

label is consequently relying on a self-certification procedure of the tyre

industry. If one considers that we still find summer tyres without any winter

performance but marked with the M+S-symbol, we all should make sure that

the label information is declared according to the tyre performance. The other

thing consumers should be informed about is the idea of regulating tyre noise.

j-a: Ultimately, I guess if the information on the tyre sidewall was easier to

read, it could be a better method of communicating information instead of

sticky pictogram labels which could be dirty, incorrect or even missing at the

point-of-sale. Would you agree?

Continental: As the label has to be shown at the point-of-sale and not on the

tyre itself we do not have this problem. On the sidewall a mass of other

information is given – therefore the information in the label would not be easy

to find for an end-consumer. If you consider a low-aspect ratio tyre, such as [a

type with] 40% [ratio] the symbols would be that tiny that they could not be

readable. Therefore it is the best way to show the information at the point-of-

sale via any sort of technical promotional literature.

j-a: In the medium term, is RFID a better solution?

Continental: The idea sounds good but the data on the chip should be

readable for everyone, at each point-of-sale. A data reader would be

necessary at each European tyre dealer between Norway and Greece, as well

as Portugal and Romania. We think that this is not realistic. And another point

Page 13 Chapter 2 The market

© 2010 All content copyright Aroq Ltd. All rights reserved.

would be the question of who has to pay for this additional equipment? In the

end, probably the end-consumer would have to do that when purchasing the

tyres.

j-a: People talk of the ‘intelligent tyre’ as vehicles change. With newer forms of

propulsion, in what ways will the tyre change and adapt to such technology?

Continental: Hybrid-driven cars need nearly the same tyres as cars with a

normal gasoline or diesel engine. Mostly, the normal engine is supported by an

electric engine. This saves fuel and minimises emissions. The speed and

handling of these cars is similar to conventional vehicles.

Tyres for electric driven cars need a very low rolling resistance to enlarge the

operating distance. We are working on this and – so we believe – are in a

leading position. But we do not want to sacrifice the longer operation time to

long braking results. We are working on this target conflict together with our

customers in the automobile industry, and hope for good results shortly.

j-a: Now that legislation is coming in to make TPMS mandatory, the motorist

no longer has to pay extra. What is the future for this technology? Do you think

that indirect TPMS will become a standard feature of on future ESC systems?

Continental: As a member of the Rubber Manufacturing Association and

ETRTO [European Tyre and Rim Technical Organisation], Continental has

already been advocating short warning times and tight warning thresholds for

several years. Derived from this, and with respect for our environmental

responsibility, Continental is confirming its statement and recommends the

direct measuring tyre pressure monitoring systems, Tire Guard.

j-a: As I understand it, TPMS technology is evolving to the point where one

scenario could be this: As soon as the TPMS tells you that your tyre needs

servicing, the nearest licensed service station will be automatically alerted

through your car’s GPS, giving you directions to a site where qualified

personnel will be awaiting your arrival. How far away are we from achieving

this?

Continental: This scenario forms part of the focus on the so-called Intelligent

Tire. Continental’s know-how of tyres, TPMS, navigation systems and vehicle-

to-vehicle communication means that it is in the best position for realising this

Page 14 Chapter 2 The market

© 2010 All content copyright Aroq Ltd. All rights reserved.

kind of functionality in-house. To be concrete, with the legislation making

TPMS mandatory, the already available Intelligent Tire technology and

navigation systems penetrating the market more and more, nothing prevents

this feature coming to the market together in the legislation time frame.

j-a: In the early days of indirect TPMS development, it was said that the

system had within it all the information required to create a vehicle ‘black box’

similar to that found on aircraft. Yet as we see it, this idea never really took off

into mainstream vehicles. Would you agree? In what other ways are TPMS

being developed?

Continental: You are right. Black-box functionality never really took off. Next-

generation TPMS systems are focusing on integrating the up-to-now fully

mechanical tyres into the electronic control algorithms of modern vehicles. This

concept is known as the intelligent tyre system. It extends the scope of classic

TPMS systems to electronically identify tyre properties and even measure

physical data at the tyre-road interface. Early applications will enable CO2

assistant functionalities to improve gas mileage and reduce greenhouse gas

emissions. Load detection and filling assistant functions will help the driver in

selecting correct target pressures and filling the tyres to the desired pressure

levels. The ultimate target, however, is using tyre-related data to improve

chassis algorithms, e.g. roll-over protection or brake distance, thus enhancing

the fun of driving and vehicle safety at the same time.

Cooper Tire & Rubber

Cooper Tire & Rubber manufactures passenger, light truck, medium truck,

motorsport and motorcycle tyres which are sold nationally and internationally in

the replacement tyre market to independent tyre dealers, wholesale

distributors, regional and national retail tyre chains and large retail chains that

sell tyres as well as other automotive racing products. In terms of Cooper Tire

& Rubber’s overseas operations, the company has a manufacturing facility,

technical centre and distribution centre and its European headquarters office

located in the UK. In addition, the company operates five distribution centres

and fives sales offices in Europe. It also has two manufacturing facilities, 18

distribution centres, a technical centre, two sales offices and an administrative

office in China. The company also has a purchasing office in Singapore. In

Mexico, Cooper Tire & Rubber has a sales office and four distribution centres.

The company says it is expanding its operations in what are considered low-

cost countries. These initiatives include the Cooper Kenda Tire manufacturing

Page 15 Chapter 2 The market

© 2010 All content copyright Aroq Ltd. All rights reserved.

joint venture in China, the Cooper Chengshan joint venture in China and its

investment in a manufacturing facility in Mexico.

Q&A with Cooper Tire & Rubber

Matthew Beecham talked with Chuck Yurkovich, Cooper Tire’s vice president

of global technology.

just-auto: Now that legislation is coming in to make tyre pressure monitoring

systems (TPMS) mandatory, the motorist no longer has to pay extra. What is

the future for this technology? Do you think that indirect TPMS will become a

standard feature on future ESC systems?

Chuck Yurkovich: In Europe, COM 2008/316 – Vehicle Safety & Environment

Directive has been implemented. The objective of the directive is to lay down

harmonised rules on the construction of motor vehicles with a view to ensuring

the functioning of the internal market while at the same time providing for a

high level of safety and environmental protection. The proposal aims at

enhancing the safety of vehicles by requiring the mandatory fitting of some

advanced safety features. The proposal also aims at enhancing the

environmental performance of vehicles by reducing the amount of road noise

and vehicle CO2 emissions from tyres. Finally, the proposal contributes to the

competitiveness of the automotive industry by simplifying the existing vehicle

safety type-approval legislation, improving transparency and easing

administrative burden.

This legislation impacts both vehicle and tyre manufacturers. From 2012, all

new passenger vehicles will need to have the following systems fitted as

standard:

○ Electronic Stability Control;

○ Lane Departure Warning System;

○ Advanced Emergency Braking System;

○ Tyre Pressure Monitoring System.

Also, tyre manufacturers will need to comply with minimum values in the

following criteria:

○ noise;

○ rolling resistance;

○ wet grip.

Page 16 Chapter 2 The market

© 2010 All content copyright Aroq Ltd. All rights reserved.

Essentially this piece of new legislation will address both the environmental

impact of vehicles and tyres and the safety issues as well. So, in Europe,

TPMS will be on every new vehicle and it will be up to vehicle and tyre

manufacturers to exploit new technologies associated with this enforced

legislation.

Indirect systems have several advantages over direct sensor systems

including lower initial cost and much lower maintenance costs. They also

provide the motorists with much more flexibility and choice for replacement

tyres since indirect systems are very tyre neutral. Indirect systems are also

very compatible with electronically controlled suspension systems because

they utilise the same types of tyre information. On the other hand, indirect

systems can’t provide the wealth of tyre-specific data that direct sensors,

despite their high costs and maintenance issues, are capable of.

In the future, we see tyre sensor technology merging with RFID technology to

provide a low-cost, low-maintenance solution. Instantaneous tyre pressure is

only one dimension of the tyre’s operating condition that can be monitored and

reported. Tyre ID, running temperature, revolution count, tyre pressure history,

including severe under-inflation and overloading, etc, are examples of other

types of data that can be monitored, reported or archived by embedded chips

and then reported to on-board vehicle systems or external monitoring systems

– such as at tyre dealerships. The electronic technology is already here.

Cooper has patented technology which we continue to pursue in this field.

What is needed are better-defined data format standards so that vehicle

manufacturers and tyre manufacturers can continue to develop their

independent technologies, but so that all components can share the same

types of data through common formats.

j-a: As I understand it, TPMS technology is evolving to the point where one

scenario could be this: As soon as the TPMS tells you that your tyre needs

servicing, the nearest licensed service station will be automatically alerted

through your car’s GPS, giving you directions to a site where qualified

personnel will be awaiting your arrival. How far away are we from achieving

this?

CY: The GPS technology is here today. Regardless of whether or not the tyre

service centre is informed of your vehicle’s condition, I’d certainly want my tyre

service centre advertised in the GPS software. If a GPS system can show the

Page 17 Chapter 2 The market

© 2010 All content copyright Aroq Ltd. All rights reserved.

driver where the nearest fast food restaurant is, it can certainly direct him to

the nearest tyre service centre. As a result, we could see this opportunity

occurring anytime with consumer awareness.

j-a: Run-flats have also done a lot to improve vehicle safety yet come with a

high price tag. Do you see technological evolution bringing run-flat and self-

inflating tyres into the cheaper mainstream?

CY: To the best of our knowledge, there is no new low cost material

technology in the short term that can provide the material property

performance requirements for stiffness, low hystersis, and fatigue that can

make run-flat technology affordable to the mainstream market. It should be

pointed out that the current self-supporting, run-flat technology typically carries

a 20-30% weight penalty for the additional materials used to make the run-flat,

self-supporting (inserts). These materials are expensive and must be passed

on to the consumer to maintain profitability for the tyre companies.

In the longer term, non-pneumatic tyre technology, which takes a completely

different approach, is continuing to advance due to new design concepts and

the utilisation of non-standard tyre industry polymers such as polyurethanes

and thermo-plastic elastomers. This technology, due to its lighter weight

construction and potentially lower material costs, could one day become

available at a price that is reachable to all consumers.

j-a: In addition to driver safety, the current focus is to find ways in which to

reduce CO2 emissions. As 25% of all CO2 emissions are generated by road

traffic and about 20-30% of a vehicle’s energy consumption can be attributed

to tyres alone, measures to improve rolling resistance remain a top priority.

Could you draw on an example of a recent tyre innovation which demonstrates

how your company has reduced rolling resistance?

CY: In 2009, Cooper Tire introduced its GFE product line which stands for

Greater Fuel Efficiency. This low-rolling resistance tyre takes advantage of the

latest technology for design/materials and typically offers fuel efficiency

improvements over conventional replacement tyres of 4-6%. This tyre features

optimal tyre shape, traction compensating sipes, and ultra low rolling

resistance tread formulation utilising silica-silane with functionalised polymer

technology. It should be noted that as greater emphasis is placed on fuel

Page 18 Chapter 2 The market

© 2010 All content copyright Aroq Ltd. All rights reserved.

efficiency in the future, this technology will eventually become the mainstay for

all products in the industry.

j-a: As we see it, most tyre manufacturers offer a low rolling resistance tyre in

their range yet few currently advertise the use of the silica-silane technology in

their commercial vehicle ranges. Why is that?

CY: Utilisation of silica-silane technology in commercial vehicle tyres typically

will not provide as much of as advantage for rolling resistance as it does for

light duty vehicles due to the differences in polymer systems currently used for

the treads. Commercial vehicles typically use 100% natural rubber polymer in

the tread due to heat build-up and durability performance requirements. In

comparison light duty vehicle tyres typically use 100% synthetic polymers in

the treads to achieve its performance requirements of wear and traction.

Natural rubber is inherently highly resilient (low hystersis) so the rolling

resistance improvements observed with silica-silane technology are minimal in

comparison. As a result, you probably do not see the advertisement of silica-

silane technology for the commercial vehicle industry since the benefit at this

time is not great enough to warrant its use and compensate for the trade-offs

of higher costs and poorer tread wear.

j-a: In addition to low rolling resistance, low tyre/road noise is a requirement

imposed on modern tyres for environmental and economic considerations.

Could you draw on an example of a recent tyre innovation which demonstrates

how your company has reduced rolling tyre noise, perhaps highlighting certain

new processes or developments?

CY: Like many tyre characteristics, successfully reducing tyre/road noise often

involves overcoming other performance trade-offs. Since a significant amount

of the tyre-related portion of tyre/road noise is generated by the tread pattern,

we spend considerable time and effort in determining proper tread groove

placement, depth and pitch sequencing in order to optimize the balance of

tyre/road noise and wet traction. To do this effectively, we’ve invested in

development of both predictive and testing tools. For example, we have

developed a tool that enables prediction of in-vehicle tyre sound quality

characteristics from the test data of a single tyre in an indoor noise

chamber. We are also developing methods to further extrapolate that indoor,

single tyre test data to predict performance on the pass-by noise test specified

Page 19 Chapter 2 The market

© 2010 All content copyright Aroq Ltd. All rights reserved.

by many regulations. This enables us to optimise tyre noise for both the

customer and the environment.

j-a: In what ways will information on the new EU tyre regulatory standards

provide a better service for the end consumer?

CY: The labelling proposal will ensure the supply of ‘standardised information’

not only on fuel efficiency, but also on wet grip and rolling noise so that

consumers and end-users can make an informed choice between tyre

manufacturers.

Also, tyre labelling will provide a means for European consumers to make

better purchase decisions based on what’s most important to them: brand,

product performance, price, warranty, contributions to fuel efficiency, or

contribution to vehicle noise.

In the end, this new legislation may actually give consumers less choice if the

vehicle manufacturers stipulate that in order to maintain the CO2 emission of

the vehicle, they will have to fit a replacement tyre with the same rolling

resistance grading.

j-a: In your view, what tyre regulatory information needs to be communicated

to the consumer?

CY: The E-mark in conjunction with the W and S marks signifies on the tyre’s

sidewall that the tyre has been type-approved to the ECE regulations. The

most appropriate means of communicating consumer information is at the

point-of-sale where consumers can understand the information prior to

purchasing tyres.

j-a: As I understand it, truck tyres are included in the requirement for tyre

labelling. Would you agree that, given the importance of truck tyres to the

economy of fleet transport, purchasers of truck tyres should receive greater

clarity through the use of labelling?

CY: Communicating labelling information is very important to the commercial

tyre sector and should be made readily available for fleets to make educated

purchase decisions based on several criteria that are most important to them:

Page 20 Chapter 2 The market

© 2010 All content copyright Aroq Ltd. All rights reserved.

product performance/brand, tread wear, retreadability, price, warranty,

contributions to fuel efficiency, contribution to vehicle noise, etc.

j-a: Ultimately, I guess if the information on the tyre sidewall was easier to

read, it could be a better method of communicating information instead of

sticky pictogram labels which could be dirty, incorrect or even missing at the

point-of-sale. Would you agree?

CY: The best method is to inform the consumer prior to purchasing their tyres.

I would agree that labels are not an effective way to communicate this

information to the consumer prior to sale, but having the information engraved

into the sidewall of the tyre won’t be any more effective. The consumer will

typically not see the label on the tread or the sidewall of the tyre prior to their

purchase. The information needs to be available to the consumer either prior

to the sale or at the point-of-sale so they can make a well-informed decision on

what tyre will best meet their needs.

Lastly, there is a proposal that the receipt given to the consumer after they

have purchased their tyres should contain the rolling resistance and wet grip

grades along with the noise value of the tyre they have purchased. If adopted,

this would be an additional communication method that could serve to

permanently document the tyre label regulatory information.

j-a: In the medium term, is RFID a better solution?

CY: RFID tags are used in some motorsport applications to understand the

forces that tyres see during usage. Other companies use them for processing

tyres through the manufacturing plant. There is also some usage in truck tyres

to monitor tyre performance. However, there does not seem to be a move to

more widespread use of RFID chips. Cost, practicality and the usefulness of

the information generated still has not been fully determined and we currently

do not see this as a better solution towards communicating consumer

information ratings on rolling resistance, noise and wet traction.

j-a: People talk of the intelligent tyre as vehicles change. With newer forms of

propulsion, in what ways will the tyre change and adapt to such technology?

CY: I foresee two parallel paths on how tyres will change:

○ tyres for what I’ll call ‘evolution of conventional vehicle platforms’;

Page 21 Chapter 2 The market

© 2010 All content copyright Aroq Ltd. All rights reserved.

○ tyres for ‘new, revolutionary mobility platforms’.

In the first case, the modern pneumatic tyre and the internal-combustion

engine powered automobile have co-evolved over decades. They will continue

to evolve together under the evolutionary pressures of increased performance

demands (traction, rolling resistance, noise, etc) and their development will

explore the limits of materials and tyre construction technology within the

boundaries (tyre size constraints, drive trains, vehicle mass) of these types of

vehicle platforms.

Simultaneously, we are seeing a variety of new types of vehicles and

alternative drive trains that open up possibilities for revolutionary tyre

concepts. Not all of these new concepts will reach market viability. Some of

these new vehicle technologies will, however, find a niche and new

opportunities for tyre technology will emerge such as the non-pneumatic

Resilient-NPT concept being co-developed with Cooper.

An example of the types of engineered materials that I envision are just around

the corner are polymers and fillers that respond dynamically to the

instantaneous energy environment of the tyre, providing low hysteresis (i.e.,

energy absorption and heat generation) at steady state highway speeds, but a

high rate or energy dissipation during braking). A number of technologies are

under development to improve the durability – both in maximum speed and

mileage range – of conventional pneumatic run-flat tyres through advanced

tyre constructions and materials. Our Cooper run-flat products already exceed

European standards.

Our European technical centre in the UK is taking the lead in our technology

development focused on optimising the balance of tyre performance

characteristics required to meet the EU regulations that take effect in just a few

years. While ‘nano-technology’ and ‘smart materials’ are probably overused

buzzwords, I expect that we will continue to see the commercialisation of new

reactive polymers and filler systems that are engineered to work together in

composite structures to provide levels of tyre performance that far exceed the

performance based on the use of any of these materials alone.

Goodyear

Goodyear develops and manufactures tyres for cars, trucks, buses, aviation,

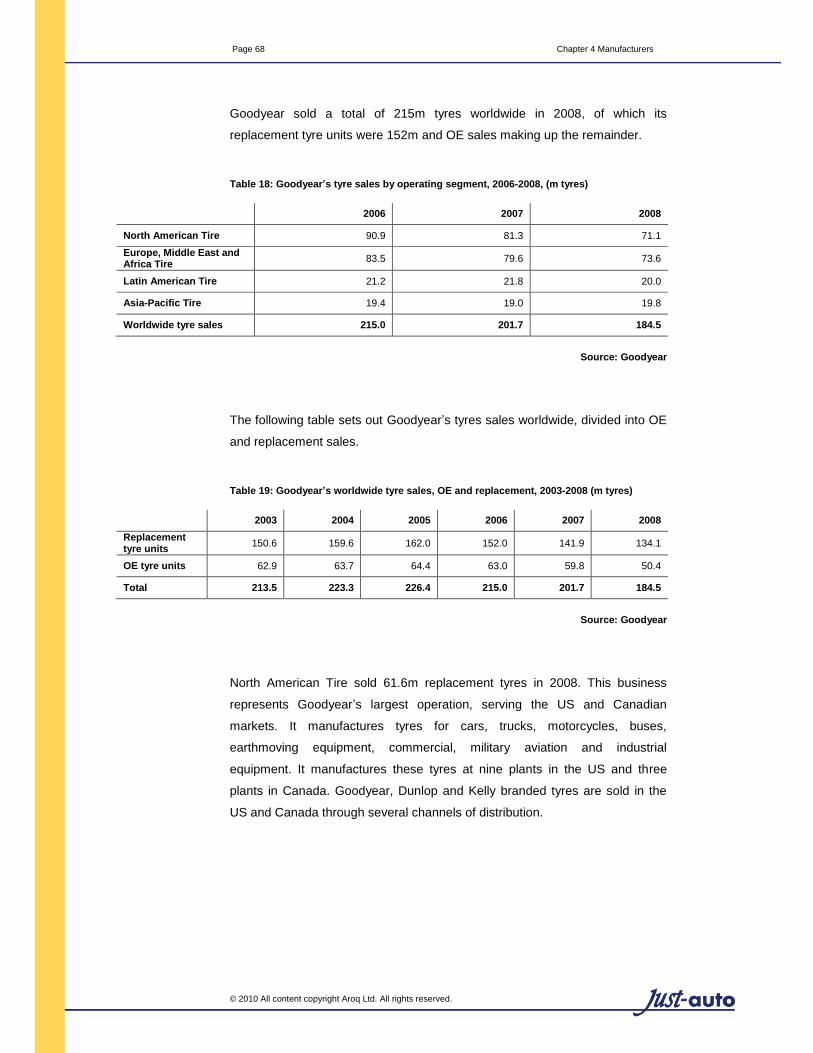

motorcycles, earthmoving and mining equipment, industrial equipment and

Page 22 Chapter 2 The market

© 2010 All content copyright Aroq Ltd. All rights reserved.

other applications. The company serves the OE and aftermarket. Its brands

include Goodyear, Dunlop, Kelly, Fulda, Debica and Sava as well as other

‘house’ brands and private-label brands of other companies. Goodyear also

manufactures rubber-related chemicals for various applications. The company

is one of the world’s largest operators of commercial truck service and tyre

retreading centres. The company operates 61 factories in 25 countries. All in

all, Goodyear currently employs 74,700 people.

Q&A with Goodyear Dunlop UK

In January 2010, Matthew Beecham talked with James Bailey, manager,

corporate communications at Goodyear Dunlop UK.

just-auto: Now that legislation is coming in to make TPMS mandatory, the

motorist no longer has to pay extra. What is the future for this technology? Do

you think that indirect TPMS will become a standard feature of future ESC

systems?

James Bailey: All ESC systems have the hardware required to implement

indirect TPMS; indirect TPMS is a software routine which is refined to work on

individual vehicle models through an extensive vehicle/tyre testing programme.

The cost of implementation will be only a few euros per vehicle and this will be

the most cost effective method of meeting the new EU TPMS regulation

requirements in the future – so yes, one day they will become standard on

future ESP systems.

j-a: As I understand it, TPMS technology is evolving to the point where one

scenario could be this: As soon as the TPMS tells you that your tyre needs

servicing, the nearest licensed service station will be automatically alerted

through your car’s GPS, giving you directions to a site where qualified

personnel will be awaiting your arrival. How far away are we from achieving

this?

JB: This scenario only has the potential to work with RunOnFlat tyres, and is

potentially very dangerous with normal tyres. It is one of the long-term

possibilities for the RunOnFlat technology that we manufacture. We do not find

acceptable any TPMS implementation that allows any tyre to be driven below

the ETRTO minimum inflation for the application’s load and speed without

issuing an immediate warning to the driver.

Page 23 Chapter 2 The market

© 2010 All content copyright Aroq Ltd. All rights reserved.

j-a: In the early days of indirect TPMS development, it was said that the

system had within it all the information required to create a vehicle ‘black box’

similar to that found on aircraft. Yet as we see it, this idea never really took off

into mainstream vehicles. Would you agree? In what other ways are TPMS

being developed?

JB: Indirect TPMS takes all of its data from the ABS/ESP system. So it is the

ABS/ESP system that could have the information to create a black box.

Goodyear would, of course, welcome having a vehicle recording of tyre

pressure. We could use this to analyse any tyre-related incidents and show the

contribution of incorrect inflation in tyre problems.

But vehicle black boxes would also show what the driver was doing and

whether he was speeding etc. It is not the issue of TPMS that has prevented

black boxes [from] appearing in vehicles [as] there are many other issues,

such as civil liberties issues.

Linking TPMS with tyre load detection on the vehicle would allow it to give you

the best recommended tyre pressure for the current load of your vehicle before

going on holiday, or recommend different pressures for different conditions.

There are tremendous opportunities.

j-a: Run-flats have done a lot to improve vehicle safety yet come with a high

price tag. Do you see technological evolution bringing run-flat and self-inflating

tyres into the cheaper mainstream?

JB: Goodyear and Dunlop RunOnFlats are already a popular option on more

mainstream cars such as the Mini and BMW 1 Series. Ten years ago, it was a

technology that you only really saw in the limousine or supercar segment, for

example, on the 7 Series BMW or Corvette. As more customers therefore

experience the benefits of RunOnFlat tyres, we expect them to demand the

same levels of security and safety in their next vehicle purchase.

The difficulties of packaging a car to meet safety legislation, provide adequate

boot and passenger space and, increasingly, to accommodate alternative fuel

cells or hybrid technology means that the spare wheel is becoming a

dispensable part of car design.

Page 24 Chapter 2 The market

© 2010 All content copyright Aroq Ltd. All rights reserved.

Whilst there are other mobility solutions, such as inflation canisters available,

none of the solutions offers the convenience, safety and personal security

benefits of RunOnFlat technology.

j-a: In addition to driver safety, the current focus is to find ways in which to

reduce CO2 emissions. As 25% of all CO2 emissions are generated by road

traffic and about 20-30% of a vehicle’s energy consumption can be attributed

to tyres alone, measures to improve rolling resistance remain a top priority.

Could you draw on an example of a recent tyre innovation which demonstrates

how your company has reduced rolling resistance?

JB: The latest Goodyear EfficientGrip features our ‘FuelSaving Technology’.

This comprises several technology advances which directly affect the tyre’s

rolling resistance: an improved construction with special lightweight materials;

an enhanced building and manufacturing process and an innovative compound

technology with a new material formulation that delivers excellent results in

mileage, wet braking and rolling resistance.

Using new materials and an efficient structure, the tyre’s weight has been

reduced by about 10%. Less material with less heat generation leads to

reduced rolling resistance levels. Compared to its predecessor, the

EfficientGrip features a lower polyester ply end and a sidewall using less

material, which contributes to the lower weight as well as to reduced rolling

resistance.

Part of this technology is a patented CoolCushion Layer. A new thermoplastic

ingredient used as a reinforcing agent partially replaces carbon black for less

weight and less heat generation, resulting in a further decrease in rolling

resistance.

Rolling resistance is mainly caused by the energy loss due to the deformation

of the tyre. Less deformation means less energy loss and hence, less rolling

resistance. Goodyear engineers used the latest computer simulation

technologies to analyse the tyre’s potential deformation behaviour during

driving. To reduce tyre deformation you need to look at all parts of the tyre and

not only at one element. For the EfficientGrip, we developed a new tyre shape

and structure, and used materials that are very strong and lightweight.

Page 25 Chapter 2 The market

© 2010 All content copyright Aroq Ltd. All rights reserved.

However, Goodyear has a focus on wet weather safety as a priority. Award-

winning tyres such as OptiGrip are evidence of our technology in this area. In

EfficientGrip, we haven’t compromised on this in the pursuit of fuel saving. For

the tyre’s wet performance, we mainly improved the tread design with its

grooves and blades and developed an innovative silica tread compound.

j-a: As we see it, most tyre manufacturers offer a low rolling resistance tyre in