global Marine Insurance Casualty Trends - Iumi · CONTENTS –CASUALTY TRENDS SHIPOWNERS’...

60

ASTRID SELTMANN Vice chairman, IUMI Facts & Figures Committee Analyst/Actuary, The Nordic Association of Marine Insurers (Cefor) Global Marine Insurance Casualty trends

Transcript of global Marine Insurance Casualty Trends - Iumi · CONTENTS –CASUALTY TRENDS SHIPOWNERS’...

ASTRID SELTMANN

Vice chairman, IUMI Facts & Figures CommitteeAnalyst/Actuary, The Nordic Association of Marine Insurers (Cefor)

Global Marine Insurance

Casualty trends

CONTENTS

• The Global Marine Insurance Market

• Vessel values & fleet trends with impact on casualty trends

• CASUALTY TRENDS

Main data sources:

Premiums: IUMI (Global Marine Insurance Report published September 2016)

Fleet data: Clarkson Research, Lloyds List Intelligence

Vessel values: The Nordic Marine Insurance Statistics (NoMIS)

Casualties: Lloyds List Intelligence;

The Nordic Marine Insurance Statistics (NoMIS)

CONTENTS – CASUALTY TRENDS

SHIPOWNERS’ LIABILITY (Crew, Environment, collision etc.)

• Pool claims International Group of P&I Clubs

OFFSHORE ENERGY

• Casualties on mobile offshore units

HULL CASUALTY TRENDS

• Total and major losses and their impact

• ‘Serious’ (LLI / IMO etc.) versus ‘Major’ (Insurance) casualties – beware of the terminology!

• Trends by type of casualty

• Trends by vessel type / age group

• Special:

‐ Cost driving factors

‐ Effect of Lay-ups on the claims frequency

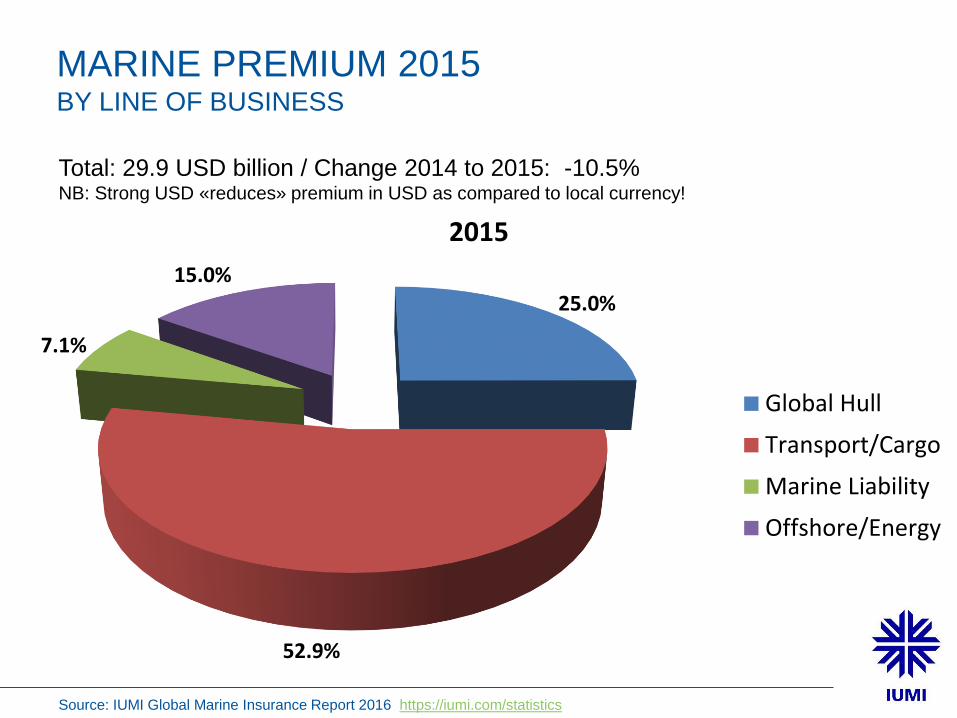

THE GLOBAL MARINE INSURANCE MARKET

25.0%

52.9%

7.1%

15.0%

2015

Global Hull

Transport/Cargo

Marine Liability

Offshore/Energy

MARINE PREMIUM 2015BY LINE OF BUSINESS

Source: IUMI Global Marine Insurance Report 2016 https://iumi.com/statistics

Total: 29.9 USD billion / Change 2014 to 2015: -10.5%NB: Strong USD «reduces» premium in USD as compared to local currency!

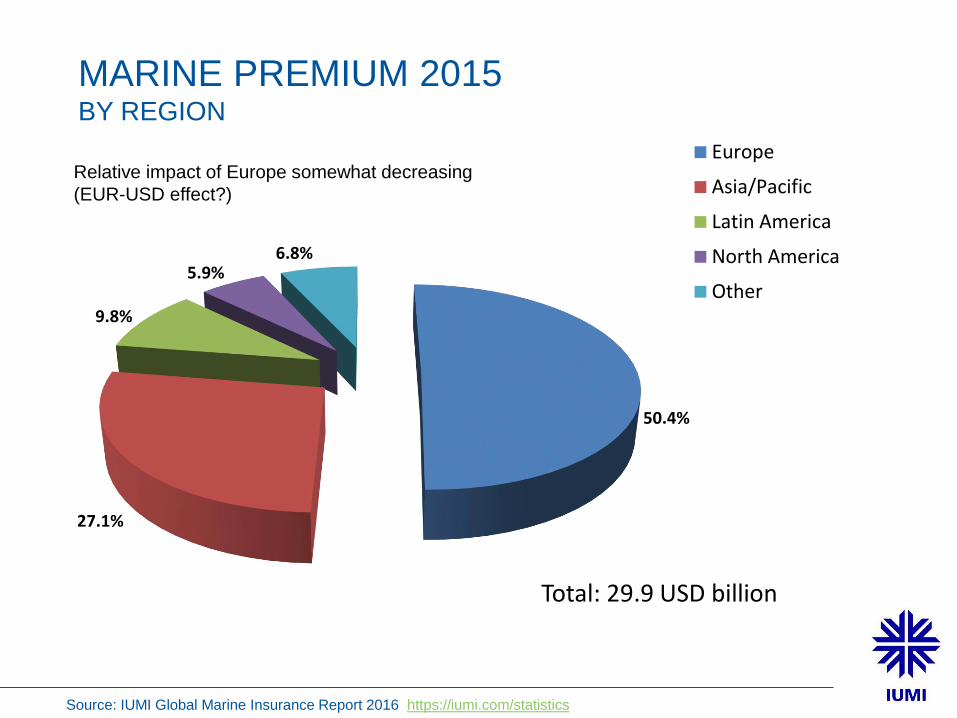

50.4%

27.1%

9.8%

5.9%6.8%

2015Europe

Asia/Pacific

Latin America

North America

Other

MARINE PREMIUM 2015BY REGION

Relative impact of Europe somewhat decreasing

(EUR-USD effect?)

Total: 29.9 USD billion

Source: IUMI Global Marine Insurance Report 2016 https://iumi.com/statistics

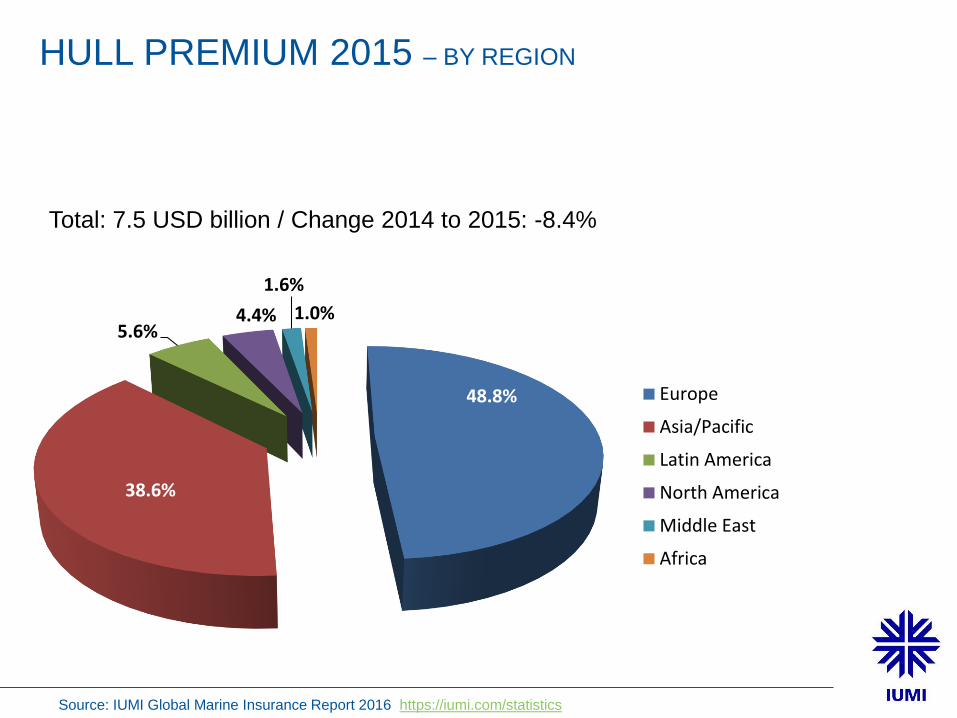

48.8%

38.6%

5.6%4.4%

1.6%

1.0%2015

Europe

Asia/Pacific

Latin America

North America

Middle East

Africa

HULL PREMIUM 2015 – BY REGION

Total: 7.5 USD billion / Change 2014 to 2015: -8.4%

Source: IUMI Global Marine Insurance Report 2016 https://iumi.com/statistics

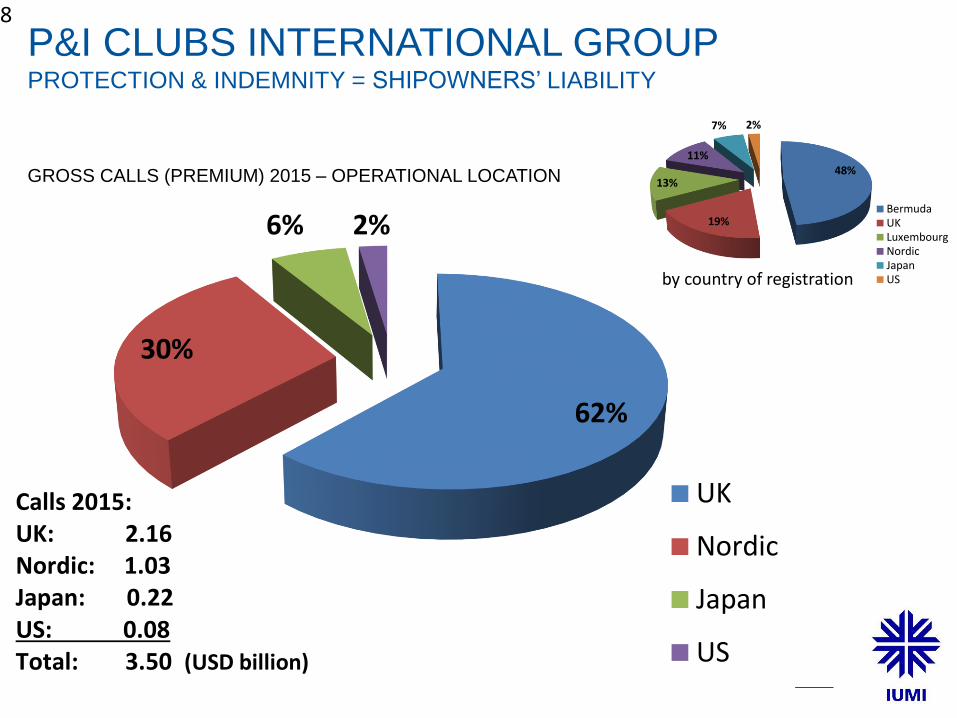

62%

30%

6% 2%

UK

Nordic

Japan

US

Calls 2015:UK: 2.16 Nordic: 1.03Japan: 0.22US: 0.08Total: 3.50 (USD billion)

P&I CLUBS INTERNATIONAL GROUPPROTECTION & INDEMNITY = SHIPOWNERS’ LIABILITY

GROSS CALLS (PREMIUM) 2015 – OPERATIONAL LOCATION 48%

19%

13%

11%

7% 2%

BermudaUKLuxembourgNordicJapanUSby country of registration

8

VESSEL VALUES

© Astrid Seltmann

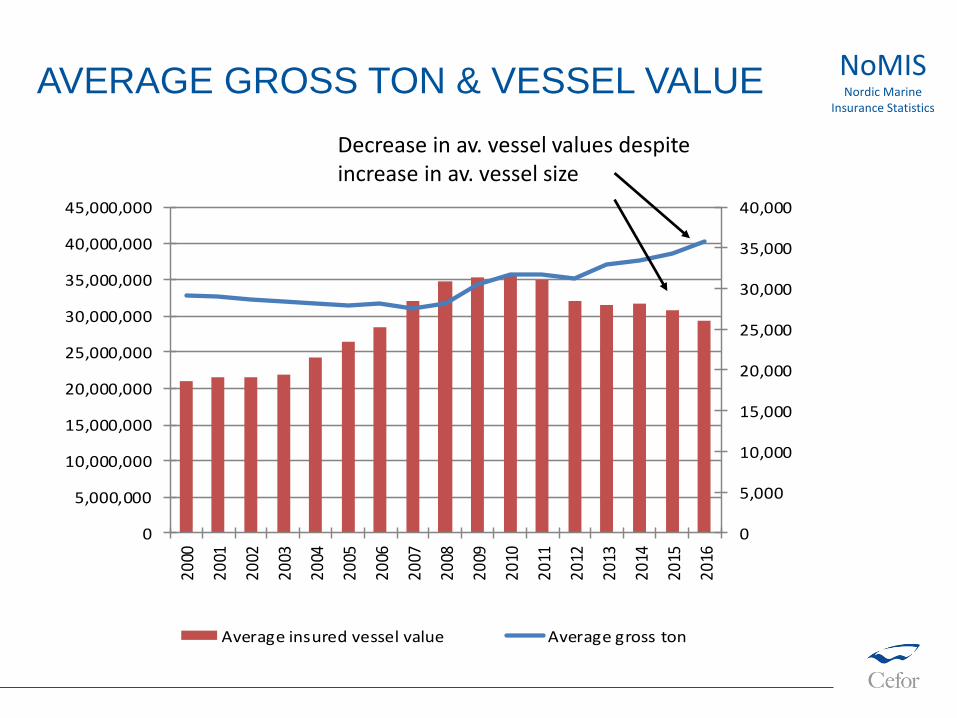

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

0

5,000,000

10,000,000

15,000,000

20,000,000

25,000,000

30,000,000

35,000,000

40,000,000

45,000,00020

00

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

Average insured vessel value Average gross ton

AVERAGE GROSS TON & VESSEL VALUENoMISNordic Marine

Insurance Statistics

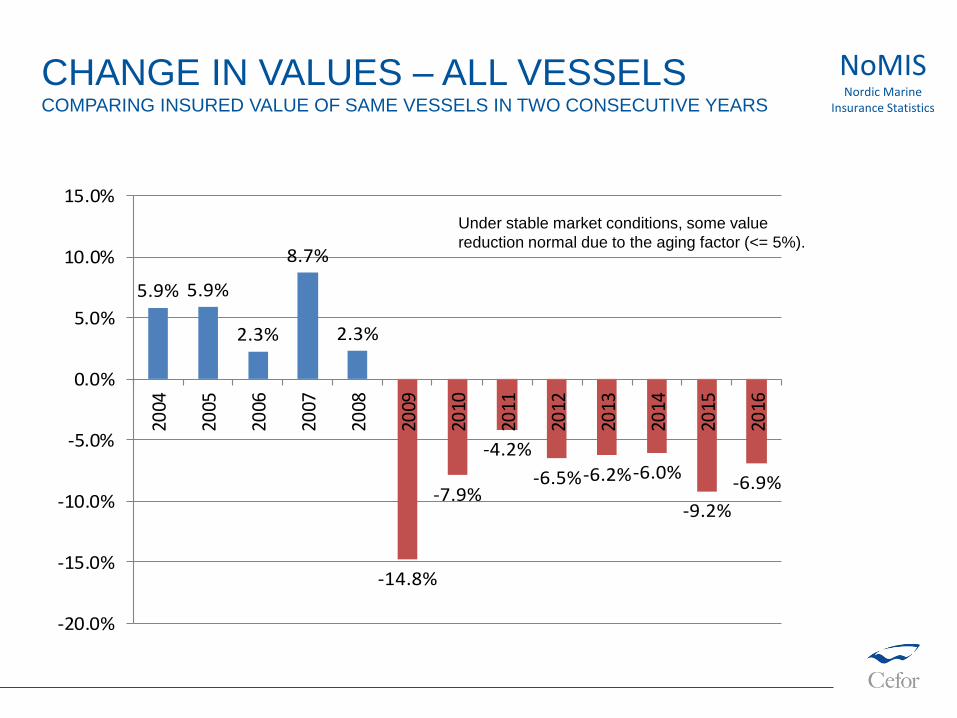

Decrease in av. vessel values despiteincrease in av. vessel size

5.9% 5.9%

2.3%

8.7%

2.3%

-14.8%

-7.9%

-4.2%

-6.5%-6.2%-6.0%

-9.2%

-6.9%

-20.0%

-15.0%

-10.0%

-5.0%

0.0%

5.0%

10.0%

15.0%

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

Under stable market conditions, some value

reduction normal due to the aging factor (<= 5%).

CHANGE IN VALUES – ALL VESSELSCOMPARING INSURED VALUE OF SAME VESSELS IN TWO CONSECUTIVE YEARS

NoMISNordic Marine

Insurance Statistics

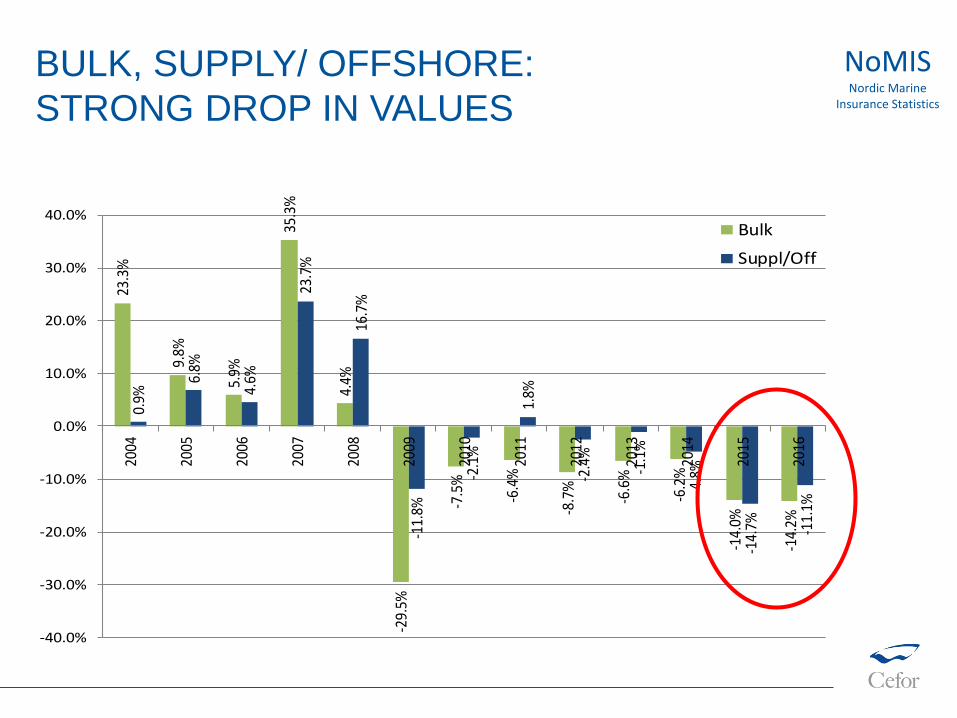

BULK, SUPPLY/ OFFSHORE:

STRONG DROP IN VALUES23

.3%

9.8%

5.9%

35.3

%

4.4%

-29.

5%

-7.5

%

-6.4

%

-8.7

%

-6.6

%

-6.2

%

-14.

0%

-14.

2%

0.9%

6.8%

4.6%

23.7

%

16.7

%

-11.

8%

-2.1

%

1.8%

-2.4

%

-1.1

%

-4.8

%

-14.

7% -11.

1%

-40.0%

-30.0%

-20.0%

-10.0%

0.0%

10.0%

20.0%

30.0%

40.0%

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

Bulk

Suppl/Off

NoMISNordic Marine

Insurance Statistics

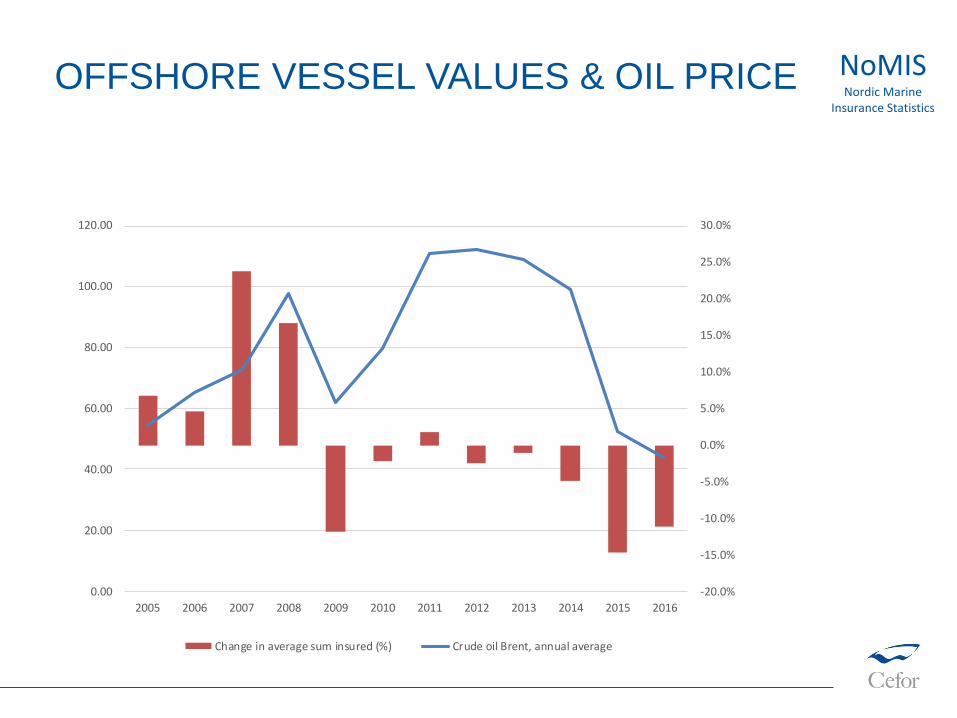

OFFSHORE VESSEL VALUES & OIL PRICE

-20.0%

-15.0%

-10.0%

-5.0%

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

0.00

20.00

40.00

60.00

80.00

100.00

120.00

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Change in average sum insured (%) Crude oil Brent, annual average

NoMISNordic Marine

Insurance Statistics

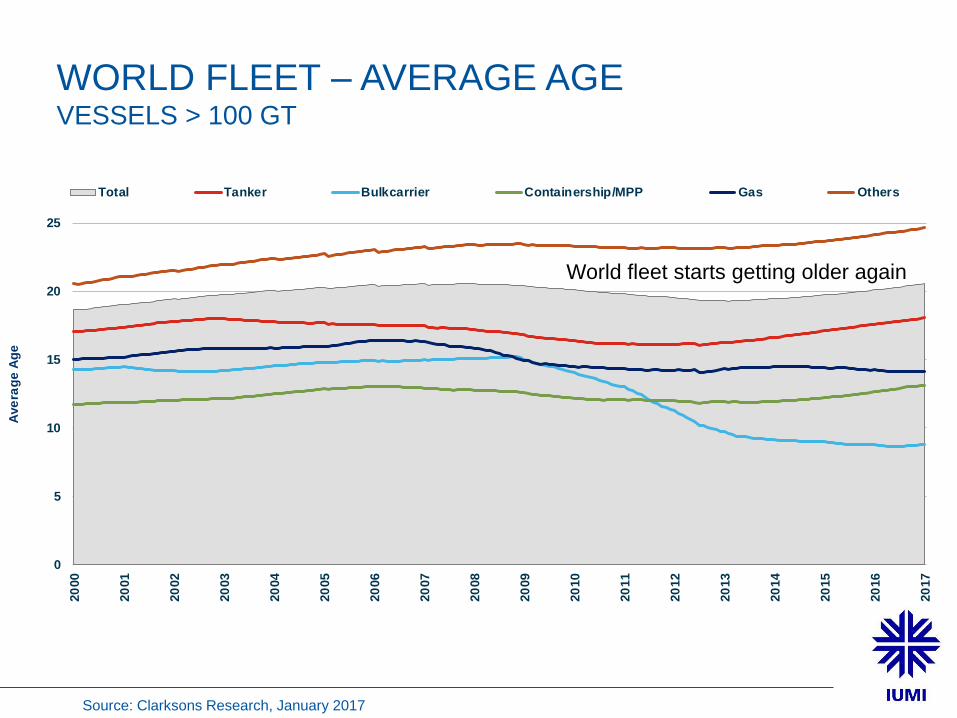

WORLD FLEET – AVERAGE AGEVESSELS > 100 GT

Source: Clarksons Research, January 2017

0

5

10

15

20

25

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

20

17

Ave

rag

e A

ge

Total Tanker Bulkcarrier Containership/MPP Gas Others

World fleet starts getting older again

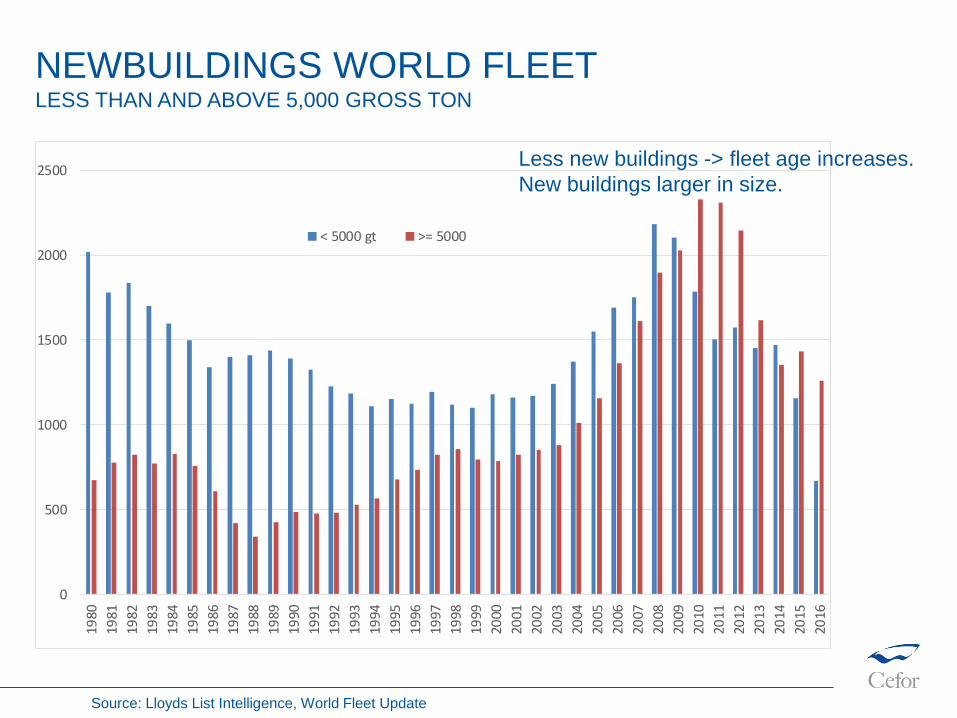

NEWBUILDINGS WORLD FLEETLESS THAN AND ABOVE 5,000 GROSS TON

0

500

1000

1500

2000

2500

1980

1981

1982

1983

1984

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

< 5000 gt >= 5000

Source: Lloyds List Intelligence, World Fleet Update

Less new buildings -> fleet age increases.

New buildings larger in size.

CASUALTY TRENDS

© Astrid Seltmann

No claim – just a matter of perspective!

TYPES OF (INSURED) CASUALTIES

• Physical damage – vessels, offshore energy units, cargo

• Third party liability

‐ To object e.g. collision

‐ People (passengers, crew)

‐ Environmental damage (e.g. oil spill)

• Loss of income

• Terror etc.

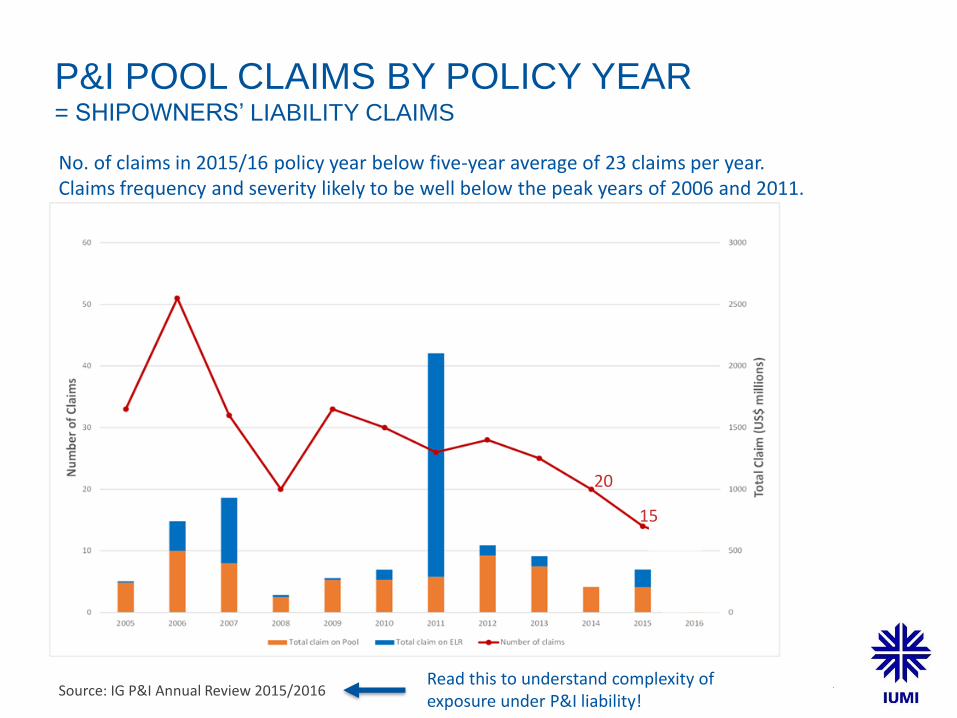

P&I POOL CLAIMS BY POLICY YEAR= SHIPOWNERS’ LIABILITY CLAIMS

No. of claims in 2015/16 policy year below five-year average of 23 claims per year. Claims frequency and severity likely to be well below the peak years of 2006 and 2011.

Source: IG P&I Annual Review 2015/2016Read this to understand complexity of exposure under P&I liability!

15

20

OFFSHORE ENERGY CLAIMS TRENDS –

MOBILES

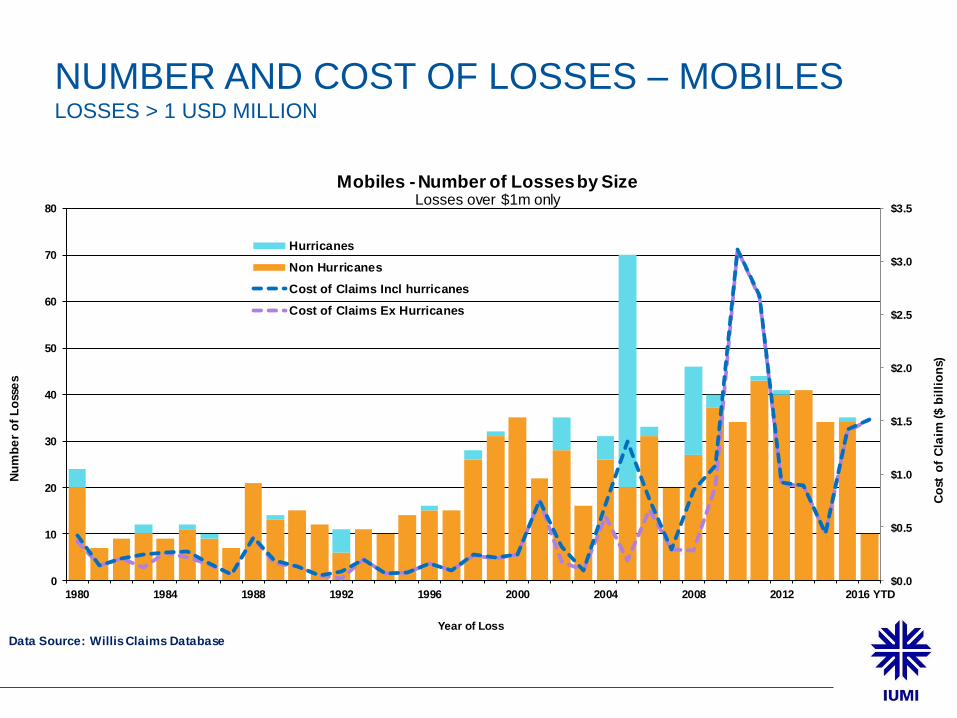

NUMBER AND COST OF LOSSES – MOBILESLOSSES > 1 USD MILLION

$0.0

$0.5

$1.0

$1.5

$2.0

$2.5

$3.0

$3.5

0

10

20

30

40

50

60

70

80

1980 1984 1988 1992 1996 2000 2004 2008 2012 2016 YTD

Co

st o

f C

laim

($ b

illi

on

s)

Nu

mb

er

of

Lo

sse

s

Year of Loss

Mobiles - Number of Losses by SizeLosses over $1m only

Hurricanes

Non Hurricanes

Cost of Claims Incl hurricanes

Cost of Claims Ex Hurricanes

Data Source: Willis Claims Database

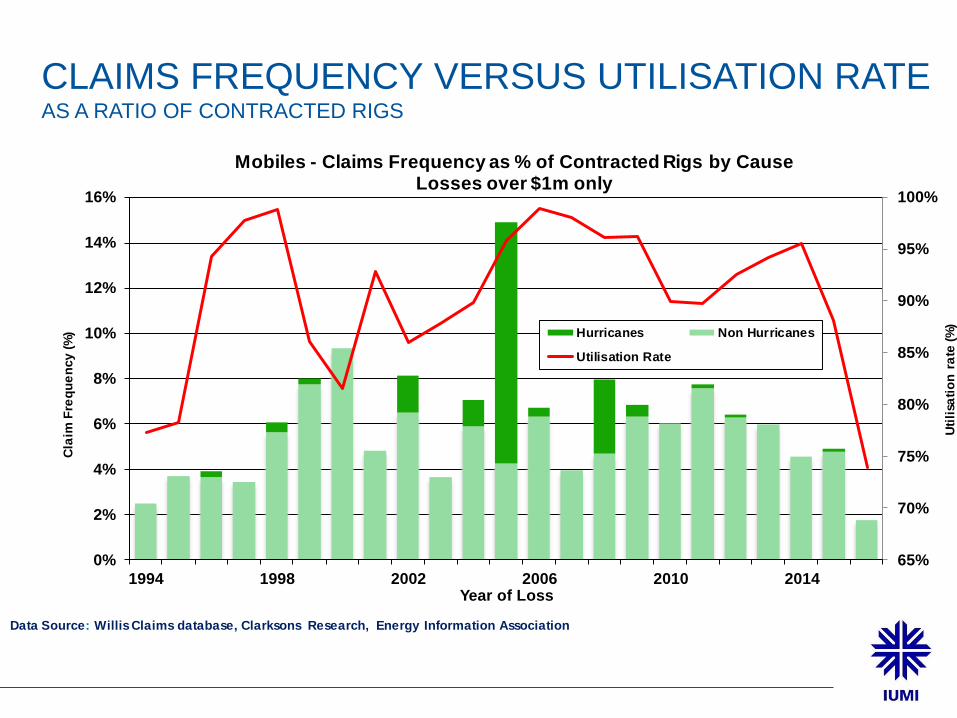

CLAIMS FREQUENCY VERSUS UTILISATION RATEAS A RATIO OF CONTRACTED RIGS

65%

70%

75%

80%

85%

90%

95%

100%

0%

2%

4%

6%

8%

10%

12%

14%

16%

1994 1998 2002 2006 2010 2014

Uti

lisa

tio

n r

ate

(%

)

Cla

im F

req

ue

ncy (

%)

Year of Loss

Mobiles - Claims Frequency as % of Contracted Rigs by CauseLosses over $1m only

Hurricanes Non Hurricanes

Utilisation Rate

Data Source: Willis Claims database, Clarksons Research, Energy Information Association

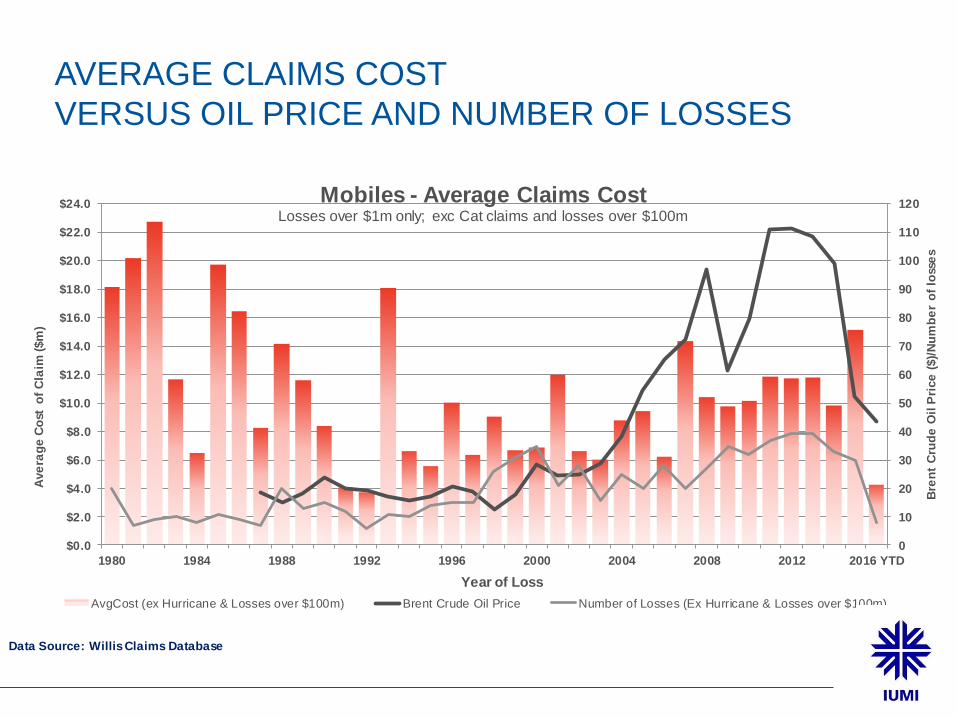

AVERAGE CLAIMS COST

VERSUS OIL PRICE AND NUMBER OF LOSSES

0

10

20

30

40

50

60

70

80

90

100

110

120

$0.0

$2.0

$4.0

$6.0

$8.0

$10.0

$12.0

$14.0

$16.0

$18.0

$20.0

$22.0

$24.0

1980 1984 1988 1992 1996 2000 2004 2008 2012 2016 YTD

Bre

nt

Cru

de

Oil

Pri

ce

($)/

Nu

mb

er

of

loss

es

Ave

rag

e C

ost

o

f C

laim

($m

)

Year of Loss

Mobiles - Average Claims CostLosses over $1m only; exc Cat claims and losses over $100m

AvgCost (ex Hurricane & Losses over $100m) Brent Crude Oil Price Number of Losses (Ex Hurricane & Losses over $100m)

Data Source: Willis Claims Database

HULL CASUALTY TRENDS – FREQUENCY

0.0%

0.1%

0.2%

0.3%

0.4%

in % of Vessels in % of GT

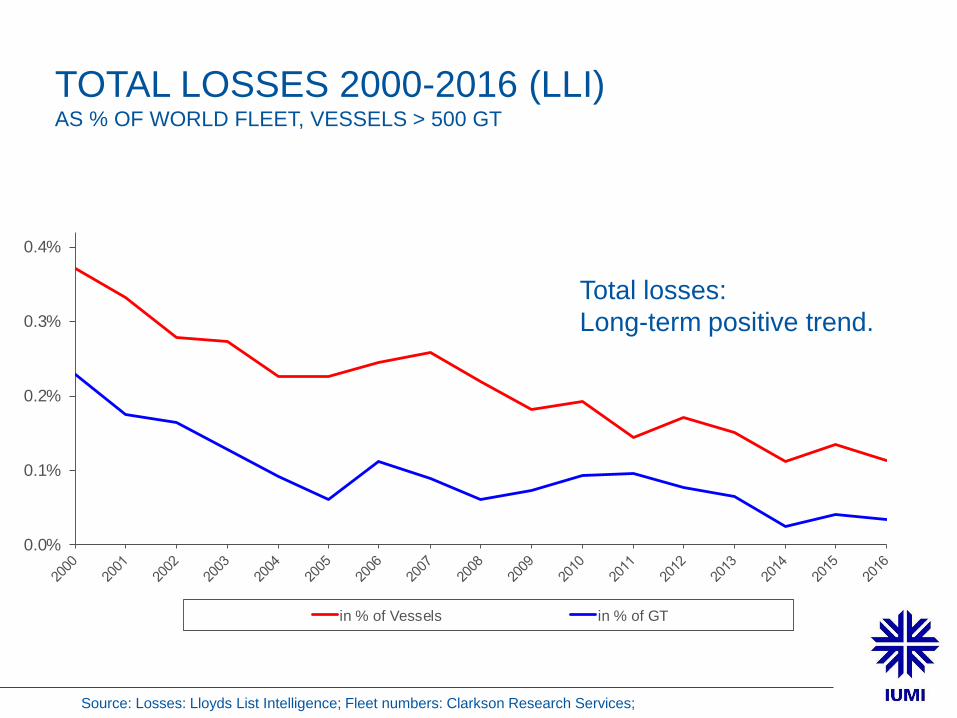

TOTAL LOSSES 2000-2016 (LLI) AS % OF WORLD FLEET, VESSELS > 500 GT

Total losses:

Long-term positive trend.

Source: Losses: Lloyds List Intelligence; Fleet numbers: Clarkson Research Services;

0.0%

0.1%

0.2%

0.3%

in % of Vessels in % of GT

Source: Losses: Lloyds List Intelligence; Fleet numbers: Clarkson Research Services;

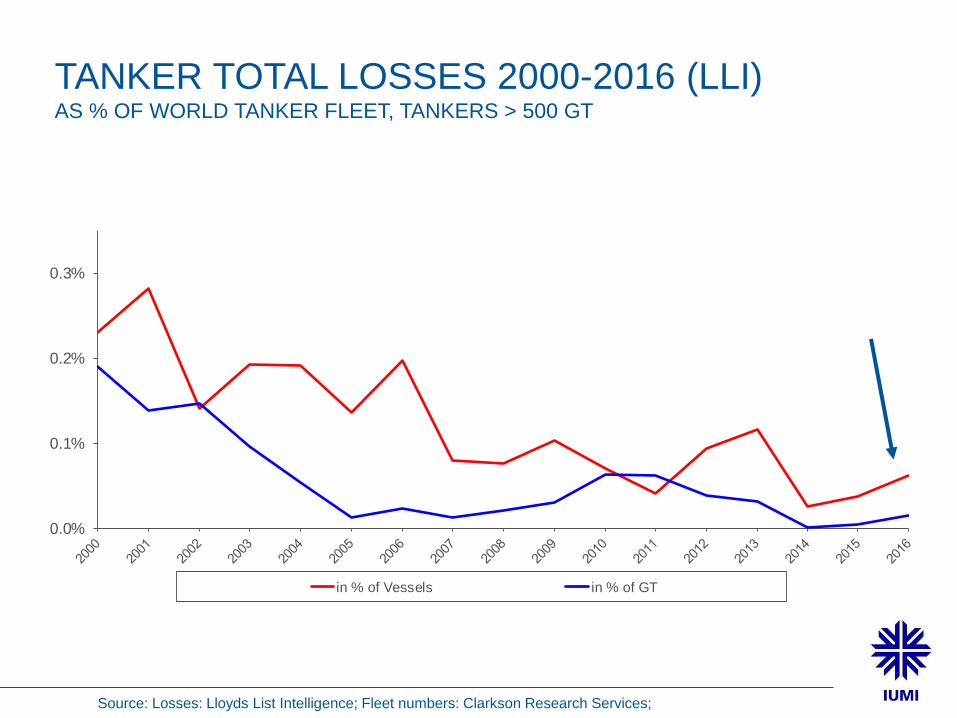

TANKER TOTAL LOSSES 2000-2016 (LLI)AS % OF WORLD TANKER FLEET, TANKERS > 500 GT

0.0%

0.1%

0.2%

0.3%

in % of Vessels in % of GT

Source: Losses: Lloyds List Intelligence; Fleet numbers: Clarkson Research Services;

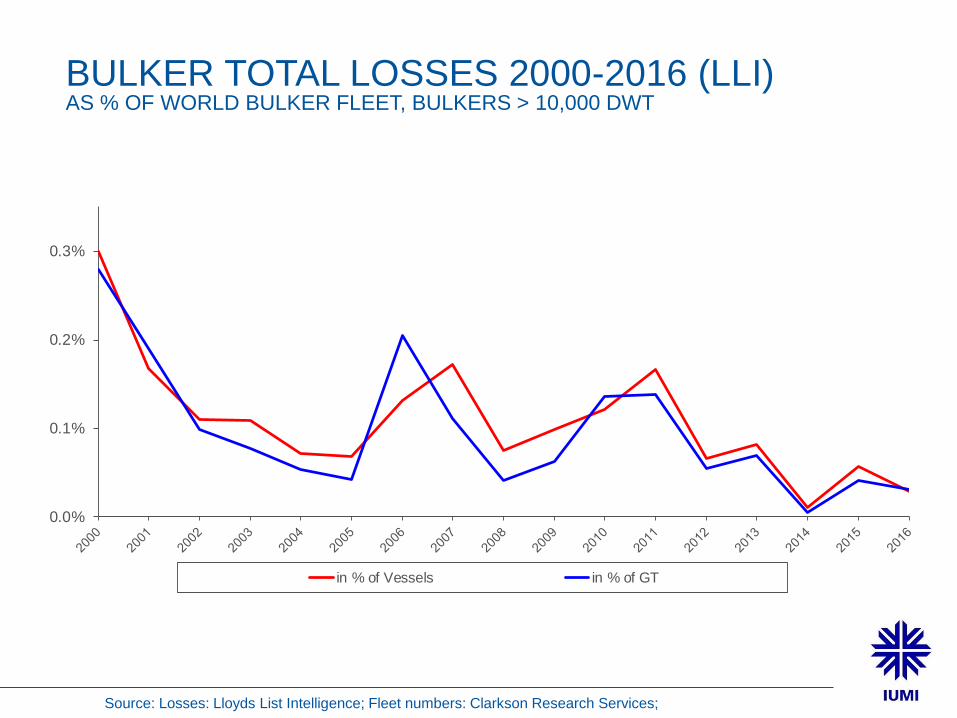

BULKER TOTAL LOSSES 2000-2016 (LLI)AS % OF WORLD BULKER FLEET, BULKERS > 10,000 DWT

0.0%

0.1%

0.2%

0.3%

in % of Vessels in % of GT

Source: Losses: Lloyds List Intelligence; Fleet numbers: Clarkson Research Services;

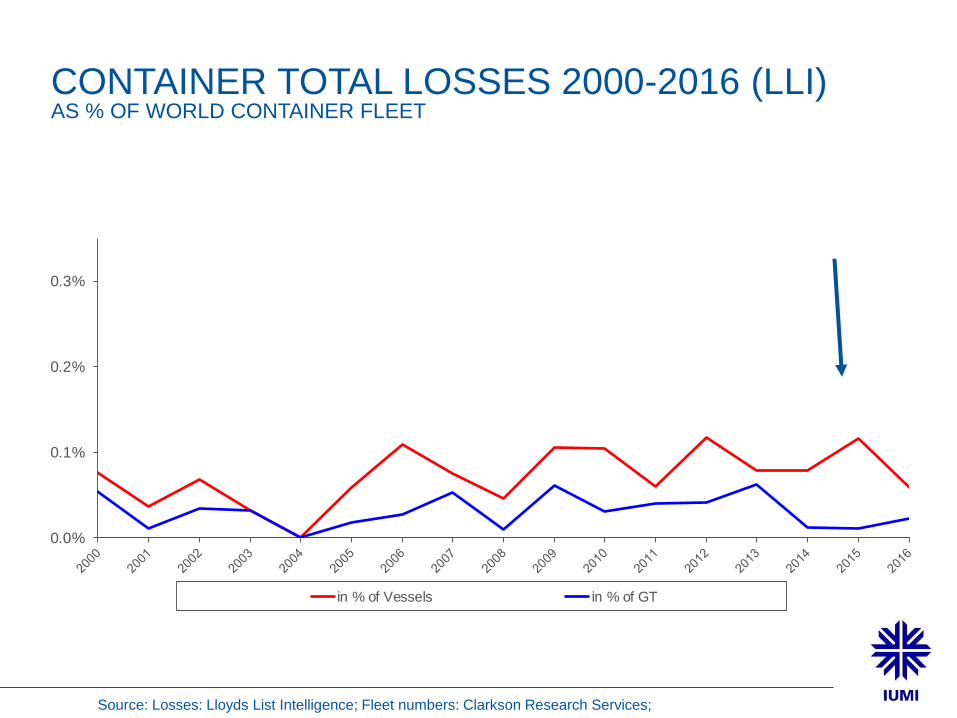

CONTAINER TOTAL LOSSES 2000-2016 (LLI)AS % OF WORLD CONTAINER FLEET

NoMISNordic Marine

Insurance Statistics

CLAIMS FREQUENCY* (NOMIS):

LONG-TERM POSITIVE TREND

0.00%

0.05%

0.10%

0.15%

0.20%

0.25%

0.30%

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

35.0%

40.0%

1996

1997

19

98

19

99

2000

2001

20

02

20

03

20

04

2005

2006

20

07

20

08

2009

2010

20

11

20

12

20

13

2014

2015

20

16

partial claims (left axis) TLO claims (right axis)

Total loss frequency

Partial loss frequency

Pre-financial crisis peak

* = No. of claims divided by no. of insured vessels

0.00%

1.00%

2.00%

3.00%

4.00%

5.00%

6.00%

0%

5%

10%

15%

20%

25%

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

0 - 10,000 USD

10,000 - 500,000 USD

500,000 - 2,000,000 USD

(right axis)

> 2,000,000 USD

(right axis)

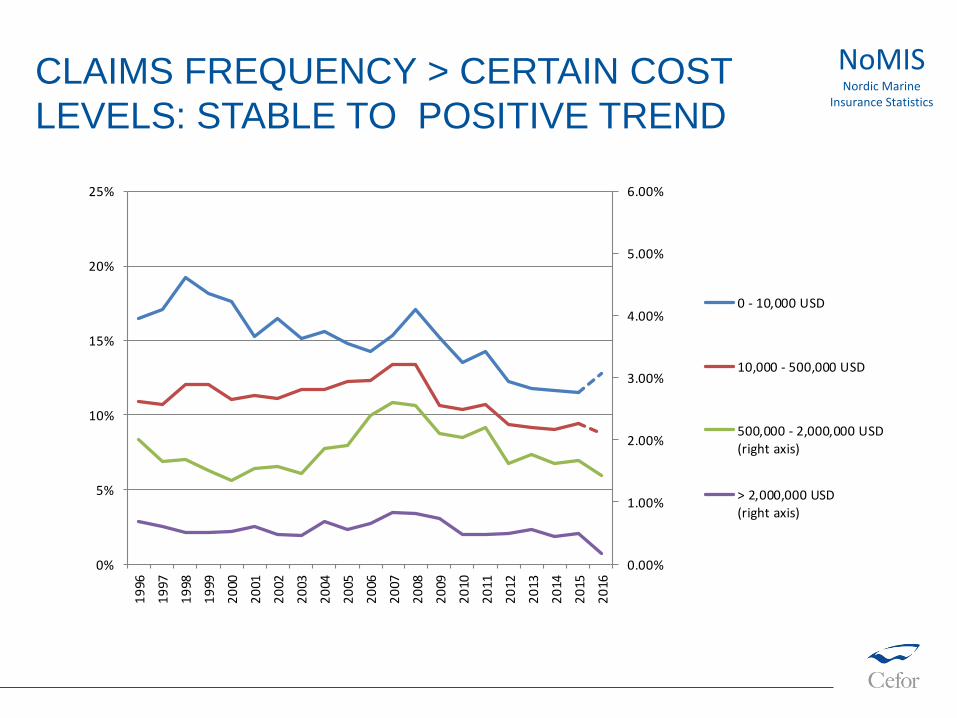

CLAIMS FREQUENCY > CERTAIN COST

LEVELS: STABLE TO POSITIVE TREND

NoMISNordic Marine

Insurance Statistics

HULL CASUALTY TRENDS – COST

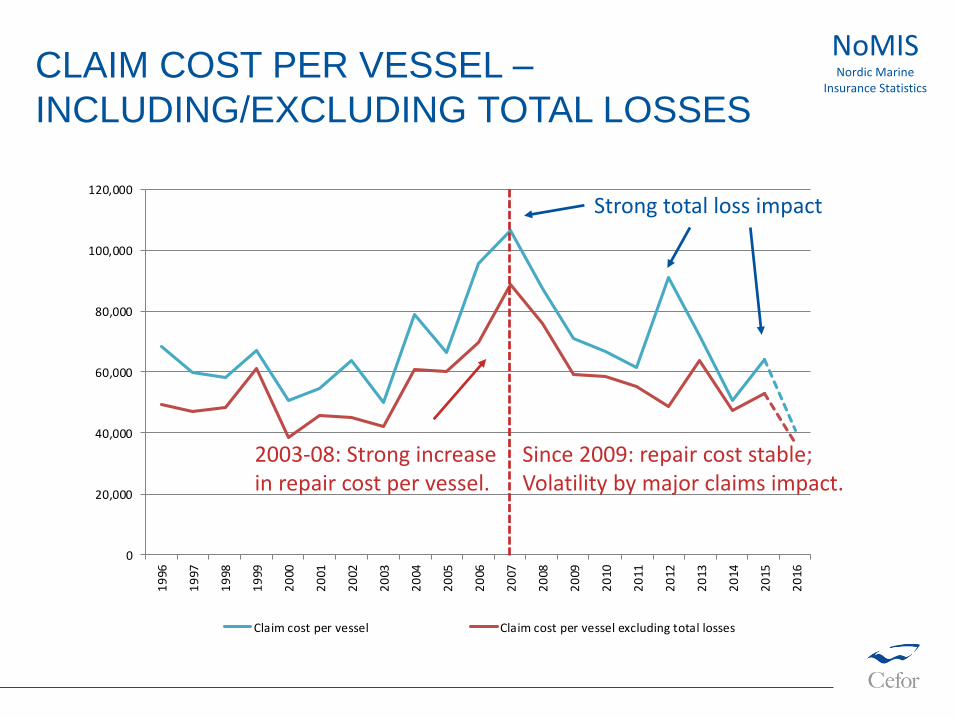

CLAIM COST PER VESSEL –

INCLUDING/EXCLUDING TOTAL LOSSES

0

20,000

40,000

60,000

80,000

100,000

120,000

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

Claim cost per vessel Claim cost per vessel excluding total losses

Strong total loss impact

2003-08: Strong increasein repair cost per vessel.

Since 2009: repair cost stable;Volatility by major claims impact.

NoMISNordic Marine

Insurance Statistics

0

20,000

40,000

60,000

80,000

100,000

120,000

1996

19

97

1998

19

99

2000

20

01

2002

20

03

2004

20

05

2006

20

07

2008

20

09

2010

20

11

2012

20

13

2014

20

15

2016

> 50 MUSD

30-50 MUSD

10-30 MUSD

5-10 MUSD

1-5 MUSD

<= 1 MUSD

IBNR

Claim bands:

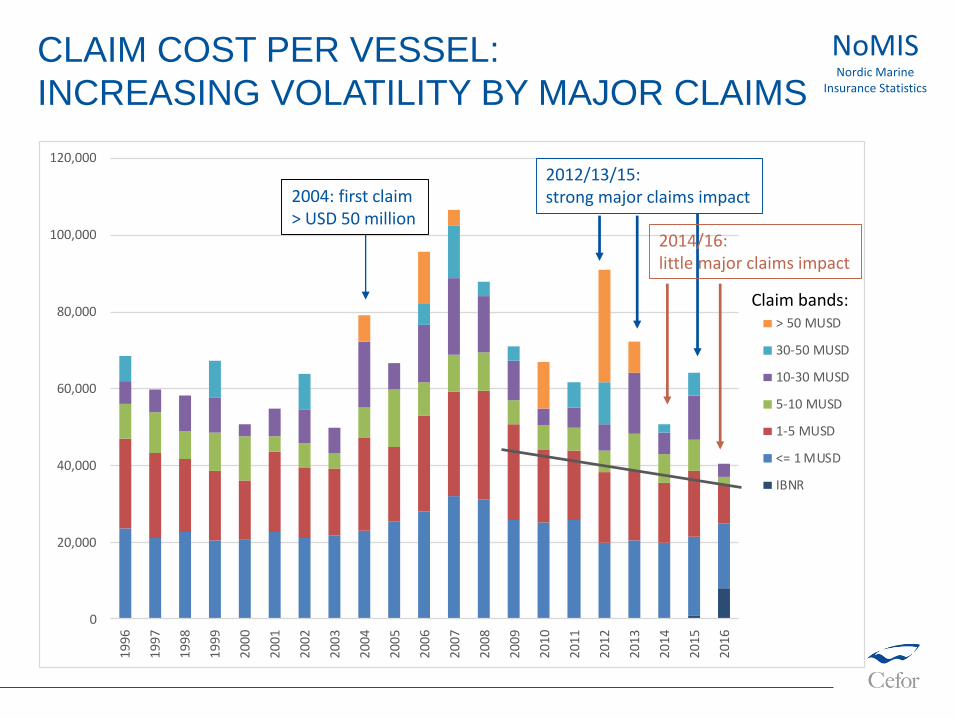

CLAIM COST PER VESSEL:

INCREASING VOLATILITY BY MAJOR CLAIMS

NoMISNordic Marine

Insurance Statistics

2012/13/15:strong major claims impact

2014/16:little major claims impact

2004: first claim > USD 50 million

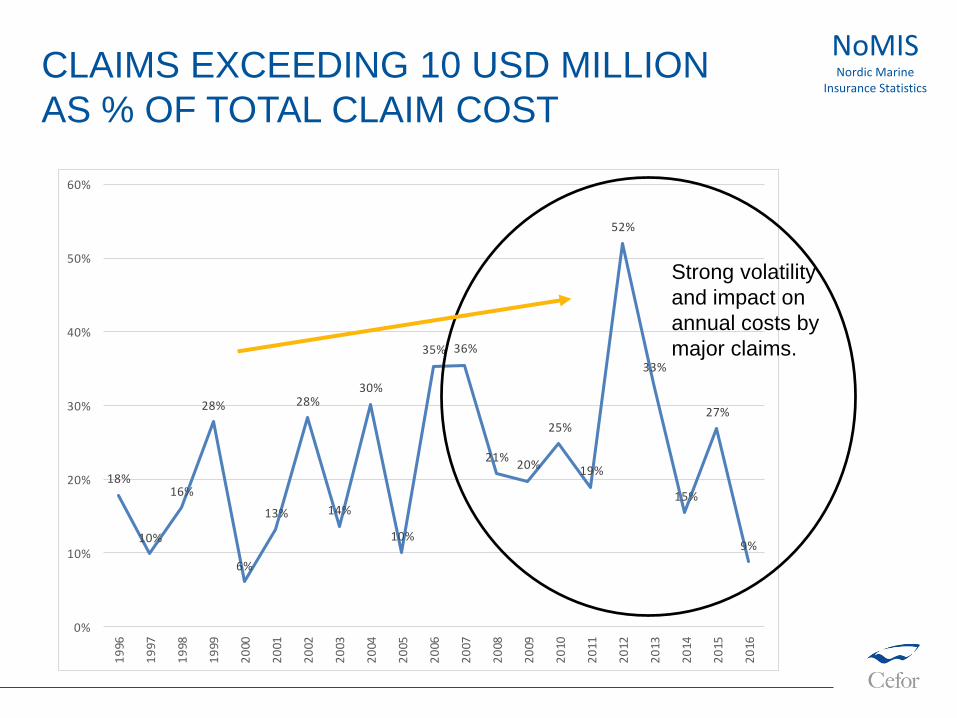

CLAIMS EXCEEDING 10 USD MILLION

AS % OF TOTAL CLAIM COST

18%

10%

16%

28%

6%

13%

28%

14%

30%

10%

35% 36%

21%20%

25%

19%

52%

33%

15%

27%

9%

0%

10%

20%

30%

40%

50%

60%

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

Strong volatility

and impact on

annual costs by

major claims.

NoMISNordic Marine

Insurance Statistics

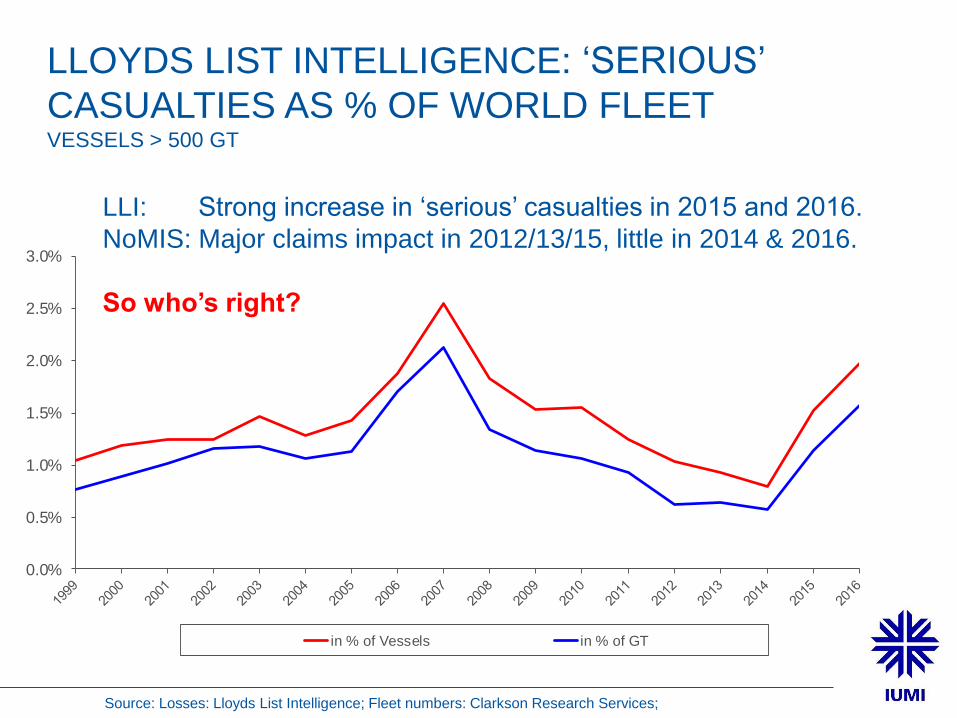

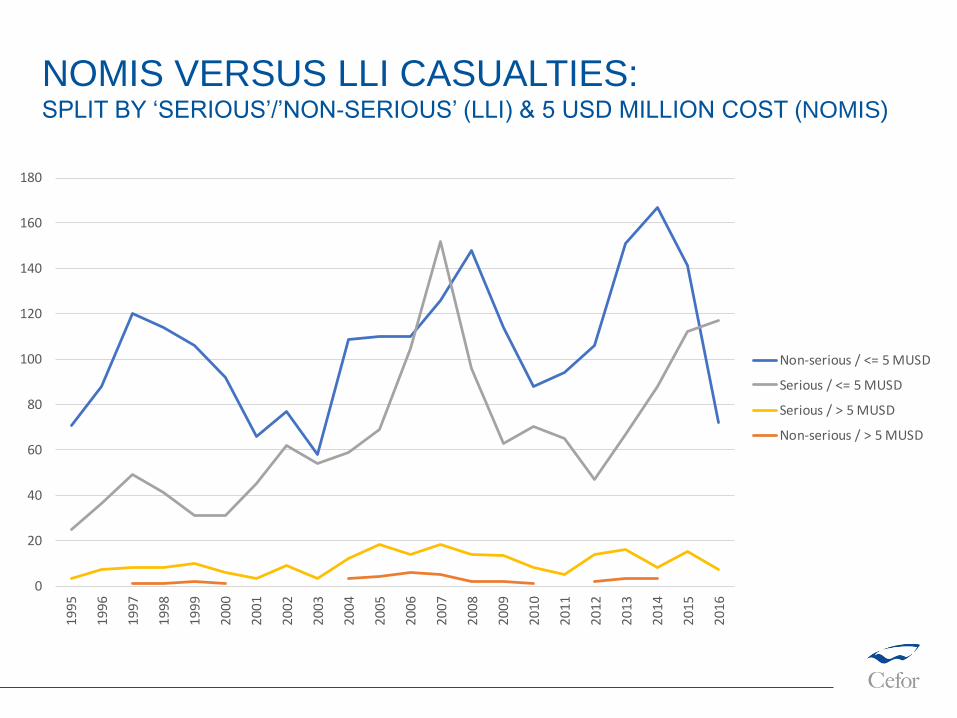

CLAIMS FREQUENCY – ALTERNATIVE FACTS (?)

LLOYDS LIST INTELLIGENCE: ‘SERIOUS’

CASUALTIES AS % OF WORLD FLEETVESSELS > 500 GT

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

in % of Vessels in % of GT

LLI: Strong increase in ‘serious’ casualties in 2015 and 2016.

NoMIS: Major claims impact in 2012/13/15, little in 2014 & 2016.

So who’s right?

Source: Losses: Lloyds List Intelligence; Fleet numbers: Clarkson Research Services;

ANSWER: BOTH!

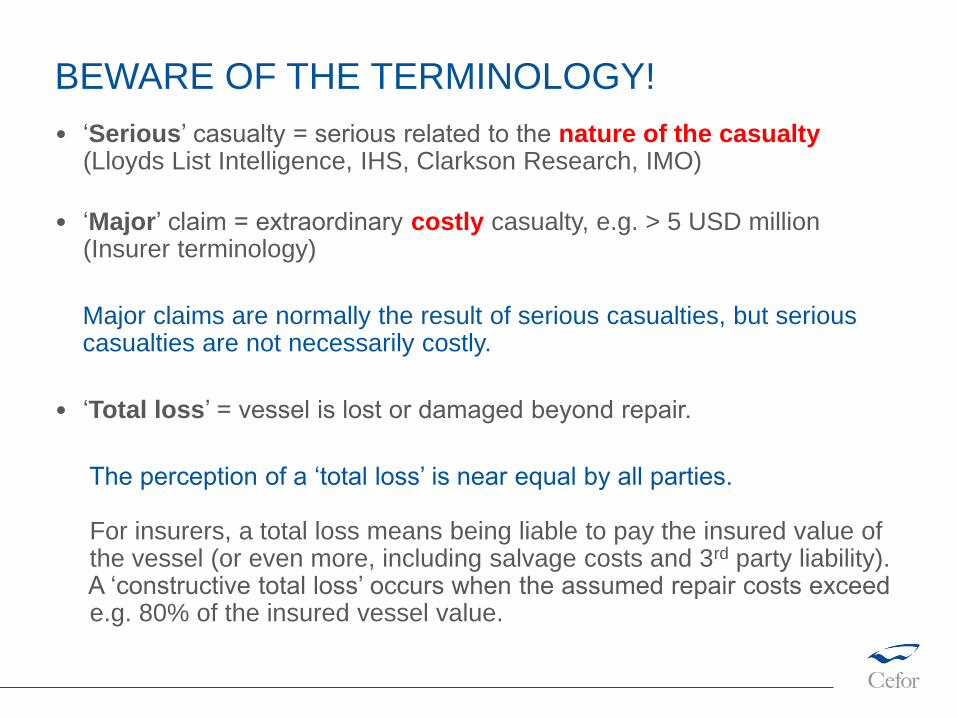

BEWARE OF THE TERMINOLOGY!

• ‘Serious’ casualty = serious related to the nature of the casualty(Lloyds List Intelligence, IHS, Clarkson Research, IMO)

• ‘Major’ claim = extraordinary costly casualty, e.g. > 5 USD million (Insurer terminology)

Major claims are normally the result of serious casualties, but seriouscasualties are not necessarily costly.

• ‘Total loss’ = vessel is lost or damaged beyond repair.

The perception of a ‘total loss’ is near equal by all parties.

For insurers, a total loss means being liable to pay the insured value ofthe vessel (or even more, including salvage costs and 3rd party liability). A ‘constructive total loss’ occurs when the assumed repair costs exceede.g. 80% of the insured vessel value.

NOMIS VERSUS LLI CASUALTIES:SPLIT BY ‘SERIOUS’/’NON-SERIOUS’ (LLI) & 5 USD MILLION COST (NOMIS)

0

20

40

60

80

100

120

140

160

180

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

Non-serious / <= 5 MUSD

Serious / <= 5 MUSD

Serious / > 5 MUSD

Non-serious / > 5 MUSD

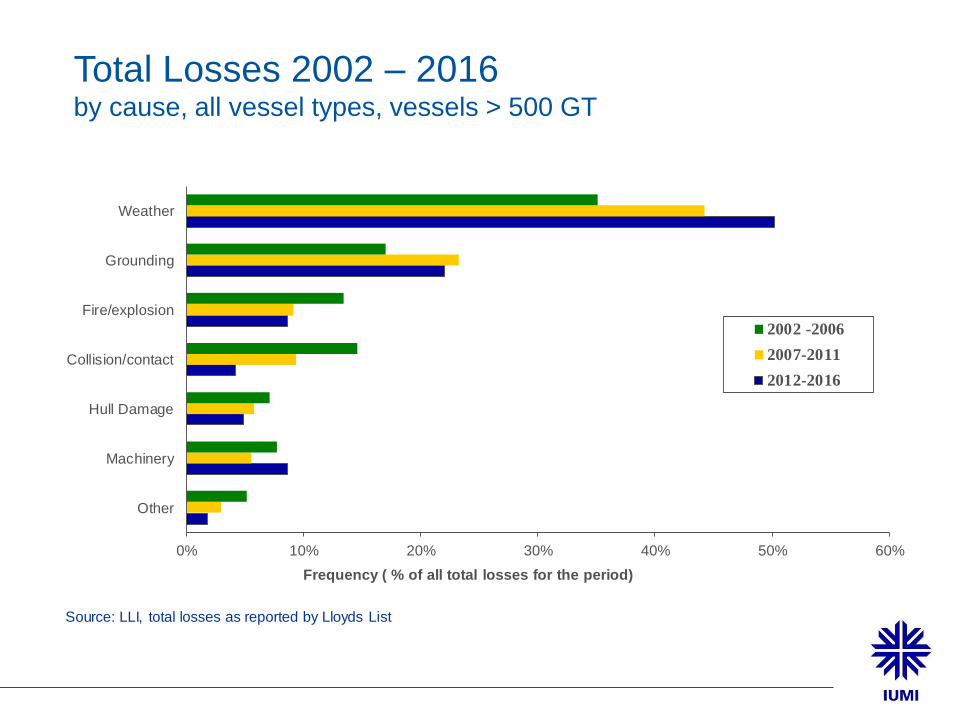

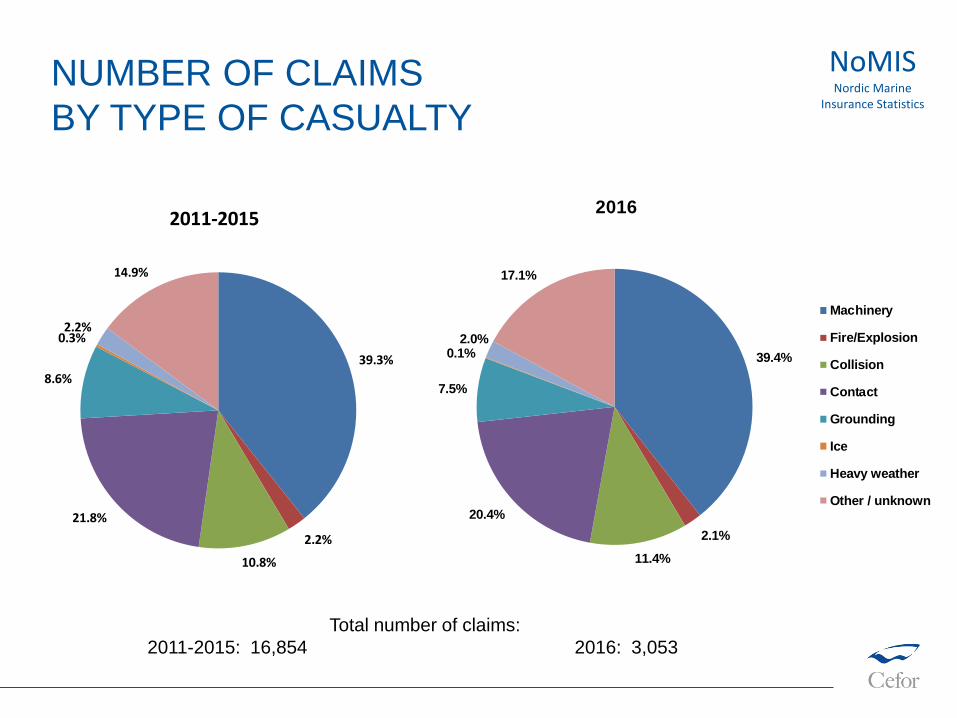

HULL CASUALTIES – BY TYPE OF CASUALTY

0% 10% 20% 30% 40% 50% 60%

Other

Machinery

Hull Damage

Collision/contact

Fire/explosion

Grounding

Weather

Frequency ( % of all total losses for the period)

2002 -2006

2007-2011

2012-2016

Source: LLI, total losses as reported by Lloyds List

Total Losses 2002 – 2016by cause, all vessel types, vessels > 500 GT

Total number of claims:

2011-2015: 16,854 2016: 3,053

39.3%

2.2%

10.8%

21.8%

8.6%

0.3%2.2%

14.9%

2011-2015

Machinery

Fire/Explosion

Collision

Contact

Grounding

Ice

Heavy weather

Other / unknown

39.4%

2.1%

11.4%

20.4%

7.5%

0.1%2.0%

17.1%

2016

Machinery

Fire/Explosion

Collision

Contact

Grounding

Ice

Heavy weather

Other / unknown

NoMISNordic Marine

Insurance Statistics

NUMBER OF CLAIMS

BY TYPE OF CASUALTY

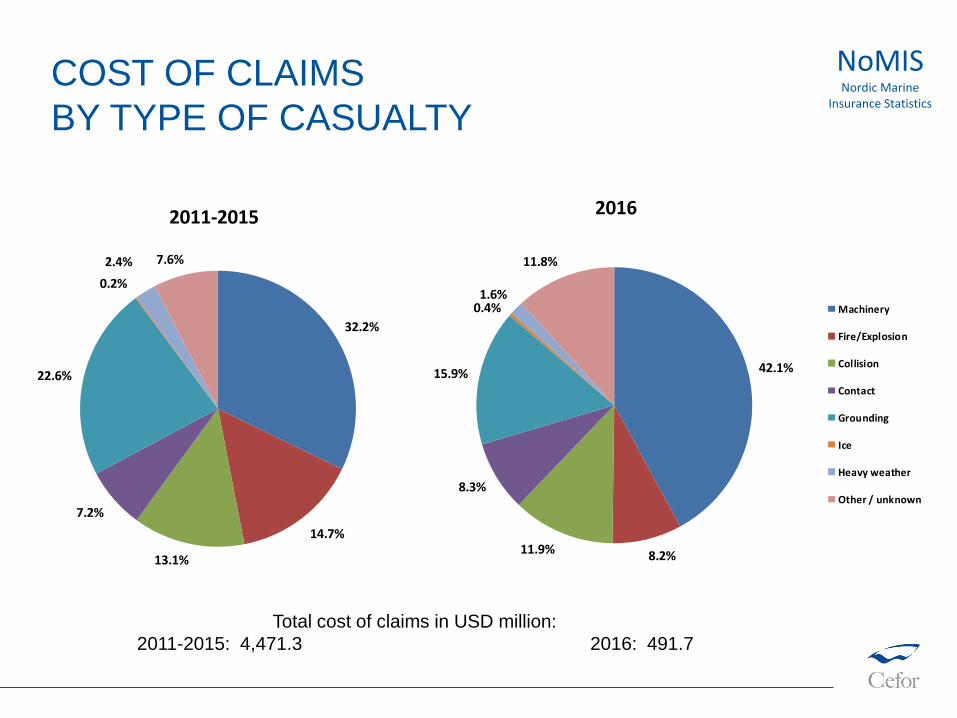

Total cost of claims in USD million:

2011-2015: 4,471.3 2016: 491.7

32.2%

14.7%

13.1%

7.2%

22.6%

0.2%

2.4% 7.6%

2011-2015

Machinery

Fire/Explosion

Collision

Contact

Grounding

Ice

Heavy weather

Other / unknown

42.1%

8.2%11.9%

8.3%

15.9%

0.4%1.6%

11.8%

2016

Machinery

Fire/Explosion

Collision

Contact

Grounding

Ice

Heavy weather

Other / unknown

NoMISNordic Marine

Insurance Statistics

COST OF CLAIMS

BY TYPE OF CASUALTY

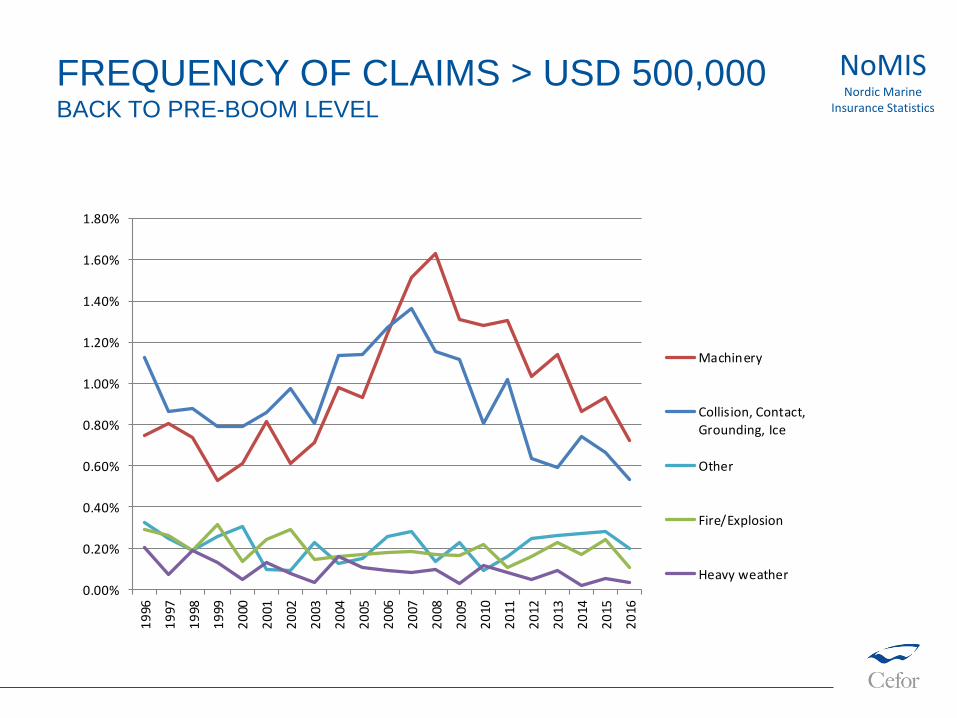

FREQUENCY OF CLAIMS > USD 500,000BACK TO PRE-BOOM LEVEL

NoMISNordic Marine

Insurance Statistics

0.00%

0.20%

0.40%

0.60%

0.80%

1.00%

1.20%

1.40%

1.60%

1.80%

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

Machinery

Collision, Contact,

Grounding, Ice

Other

Fire/Explosion

Heavy weather

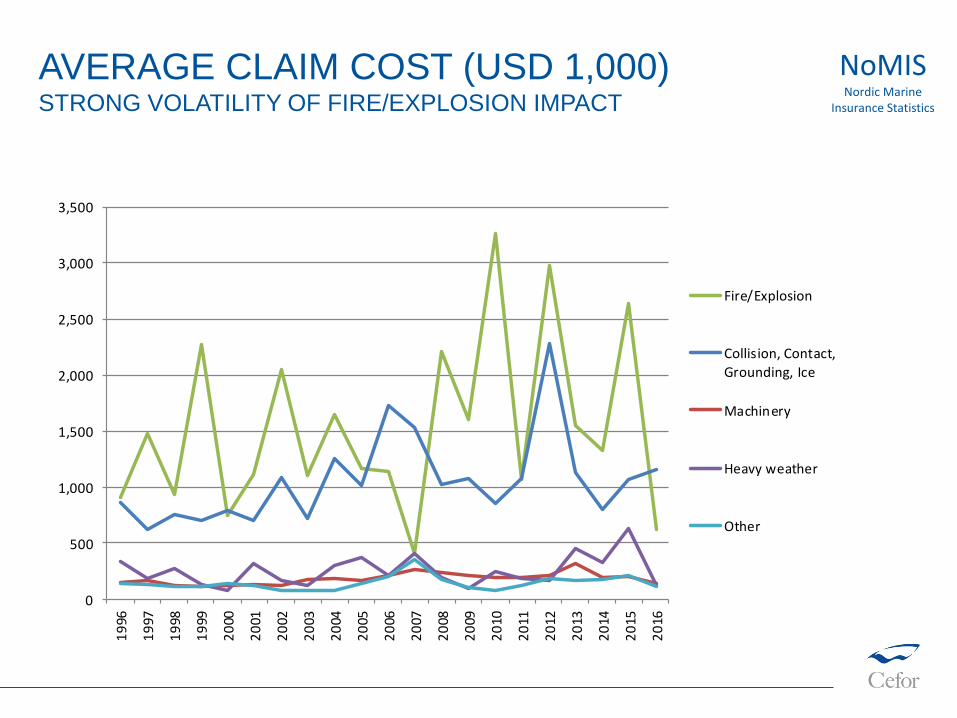

AVERAGE CLAIM COST (USD 1,000)STRONG VOLATILITY OF FIRE/EXPLOSION IMPACT

NoMISNordic Marine

Insurance Statistics

0

500

1,000

1,500

2,000

2,500

3,000

3,500

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

Fire/Explosion

Collision, Contact,

Grounding, Ice

Machinery

Heavy weather

Other

CLAIMS TRENDS

BY AGE GROUP AND VESSEL TYPE

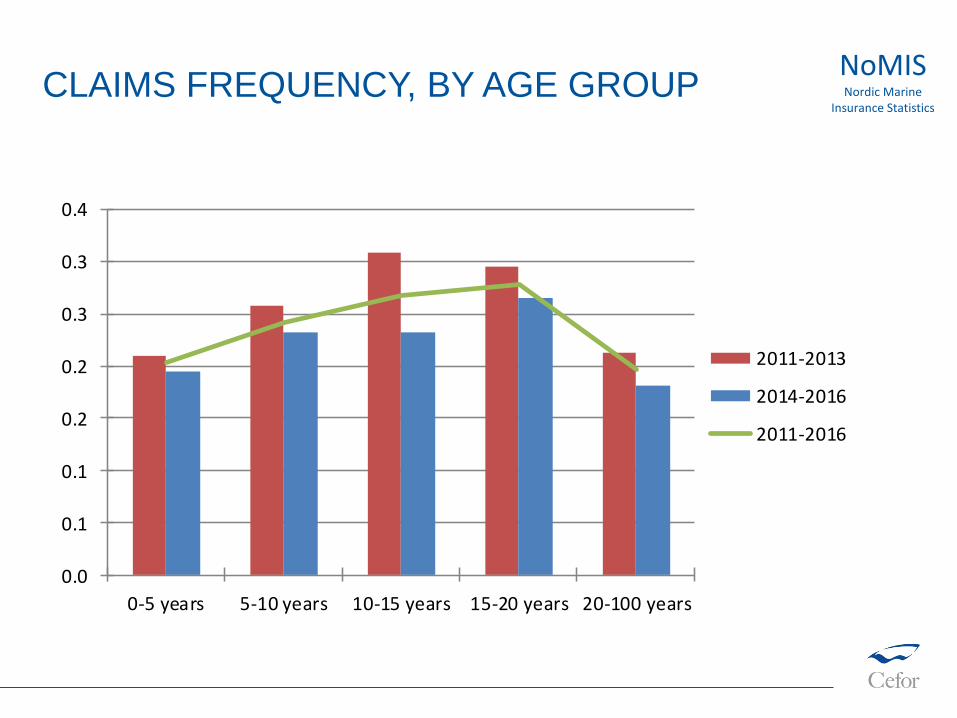

CLAIMS FREQUENCY, BY AGE GROUPNoMISNordic Marine

Insurance Statistics

0.0

0.1

0.1

0.2

0.2

0.3

0.3

0.4

0-5 years 5-10 years 10-15 years 15-20 years 20-100 years

2011-2013

2014-2016

2011-2016

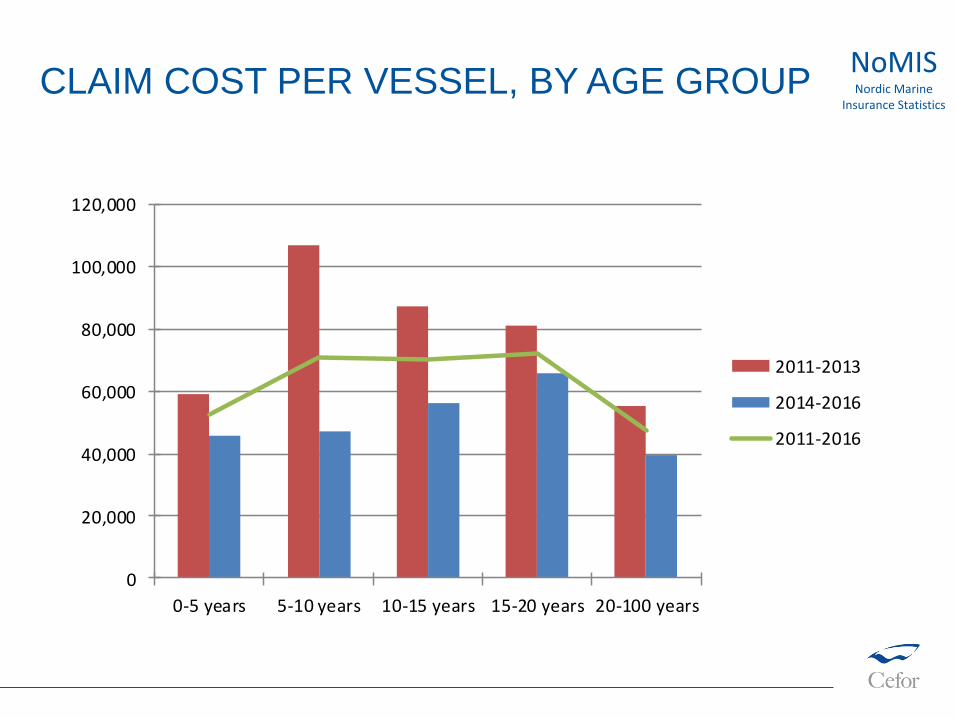

CLAIM COST PER VESSEL, BY AGE GROUPNoMISNordic Marine

Insurance Statistics

0

20,000

40,000

60,000

80,000

100,000

120,000

0-5 years 5-10 years 10-15 years 15-20 years 20-100 years

2011-2013

2014-2016

2011-2016

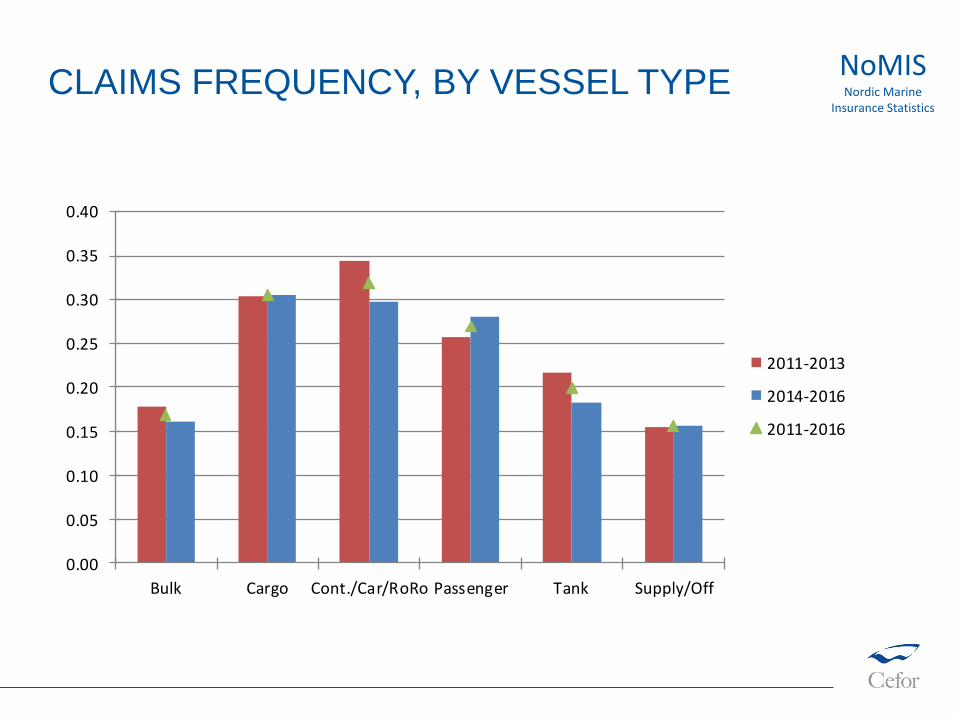

CLAIMS FREQUENCY, BY VESSEL TYPE NoMISNordic Marine

Insurance Statistics

0.00

0.05

0.10

0.15

0.20

0.25

0.30

0.35

0.40

Bulk Cargo Cont./Car/RoRo Passenger Tank Supply/Off

2011-2013

2014-2016

2011-2016

CLAIM COST PER VESSEL, BY VESSEL TYPE NoMISNordic Marine

Insurance Statistics

0

50,000

100,000

150,000

200,000

250,000

300,000

Bulk Cargo Cont./Car/RoRoPassenger Tank Supply/Off

2011-2013

2014-2016

2011-2016

SUMMARY CASUALTY TRENDS

• Total loss frequency: Long-term positive trend continues in 2016 after some increase 2015.

• Overall claims frequency: Long-term stable to downwards trend.

• Repair cost: Increase before financial crisis. Since 2009 relative stable at pre-crisis level.

Correlation with certain parameters (e.g. steel price, USD exchange rate, labour cost).

May be positively influenced by strong USD (repairs paid in other currencies).

• Major (=costly) claims trends:

‐ More expensive single claims.

(increasing vessel sizes, more complex objects)

‐ Increasing Volatility

Strong impact in some years (2012, 2013, 2014), little in other years (2014, 2016).

Difficult to estimate major claims impact for a specific year due to random occurrence.

• ‘Serious’ casualties: Strong increase in 2015 & 2016. Majority of ‘serious’ casualties no

‘major’ claims in terms of cost. A high share of ‘serious’ casualties should nevertheless give

rise to concern and be investigated.

• Lay-ups: Does a higher share of inactive vessels keep the claims frequency/cost at bay?

SPECIAL FOCUS:

- COST DRIVING FACTORS

- EFFECT OF LAY-UP ON CLAIMS FREQUENCY & COST

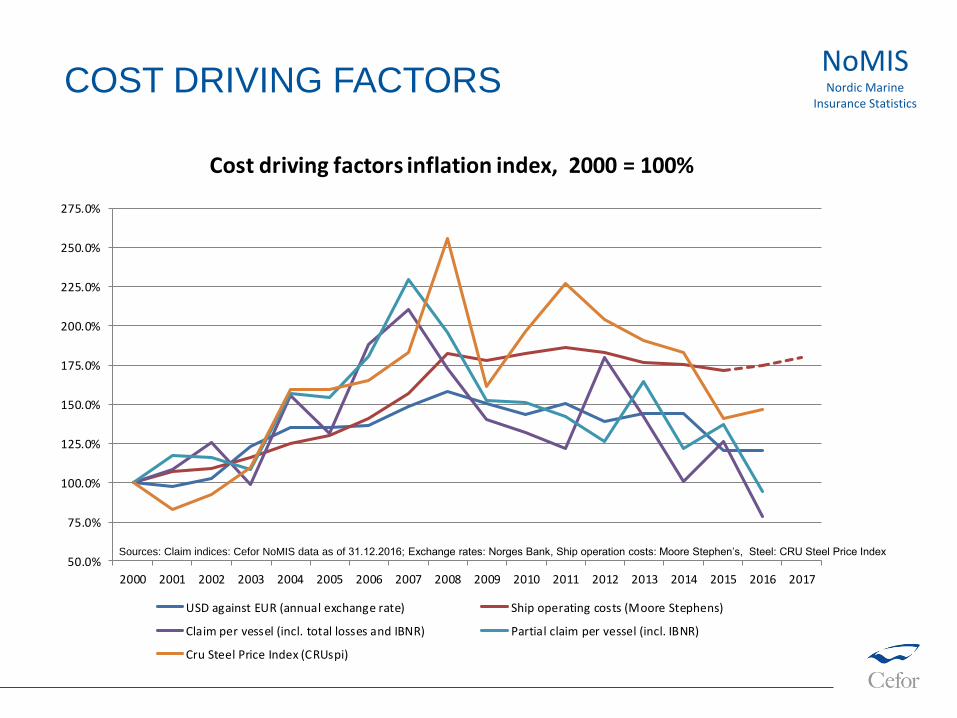

50.0%

75.0%

100.0%

125.0%

150.0%

175.0%

200.0%

225.0%

250.0%

275.0%

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

Cost driving factors inflation index, 2000 = 100%

USD against EUR (annual exchange rate) Ship operating costs (Moore Stephens)

Claim per vessel (incl. total losses and IBNR) Partial claim per vessel (incl. IBNR)

Cru Steel Price Index (CRUspi)

Sources: Claim indices: Cefor NoMIS data as of 31.12.2016; Exchange rates: Norges Bank, Ship operation costs: Moore Stephen’s, Steel: CRU Steel Price Index

COST DRIVING FACTORSNoMISNordic Marine

Insurance Statistics

LAY-UP EFFECT – EXAMPLE:

CONTAINER VESSELS LAID UP IN 2009

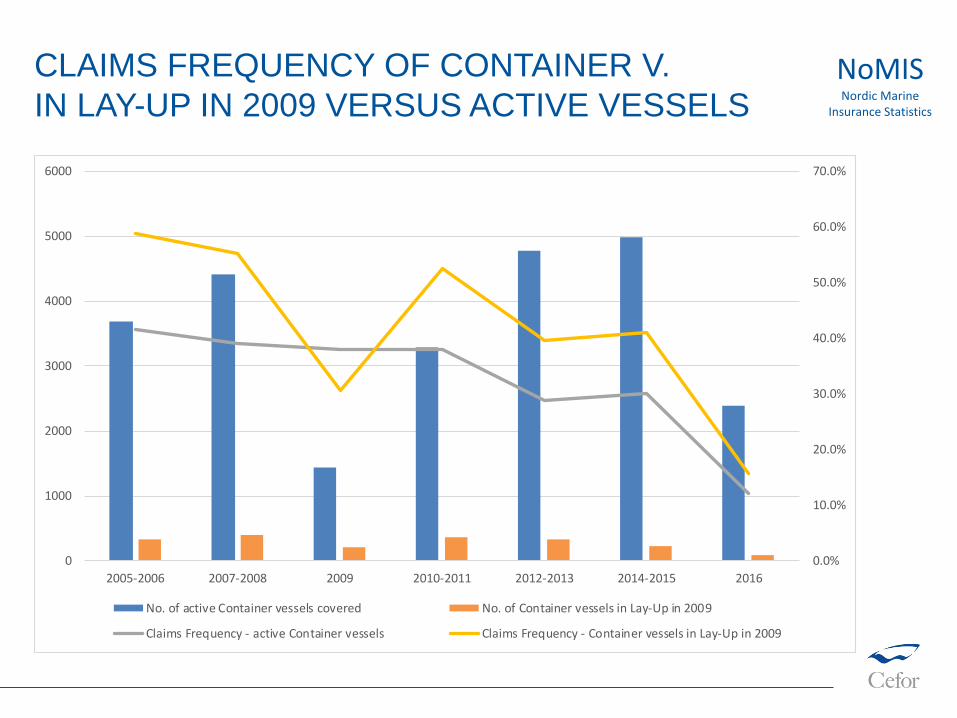

CLAIMS FREQUENCY OF CONTAINER V.

IN LAY-UP IN 2009 VERSUS ACTIVE VESSELS

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

70.0%

0

1000

2000

3000

4000

5000

6000

2005-2006 2007-2008 2009 2010-2011 2012-2013 2014-2015 2016

No. of active Container vessels covered No. of Container vessels in Lay-Up in 2009

Claims Frequency - active Container vessels Claims Frequency - Container vessels in Lay-Up in 2009

NoMISNordic Marine

Insurance Statistics

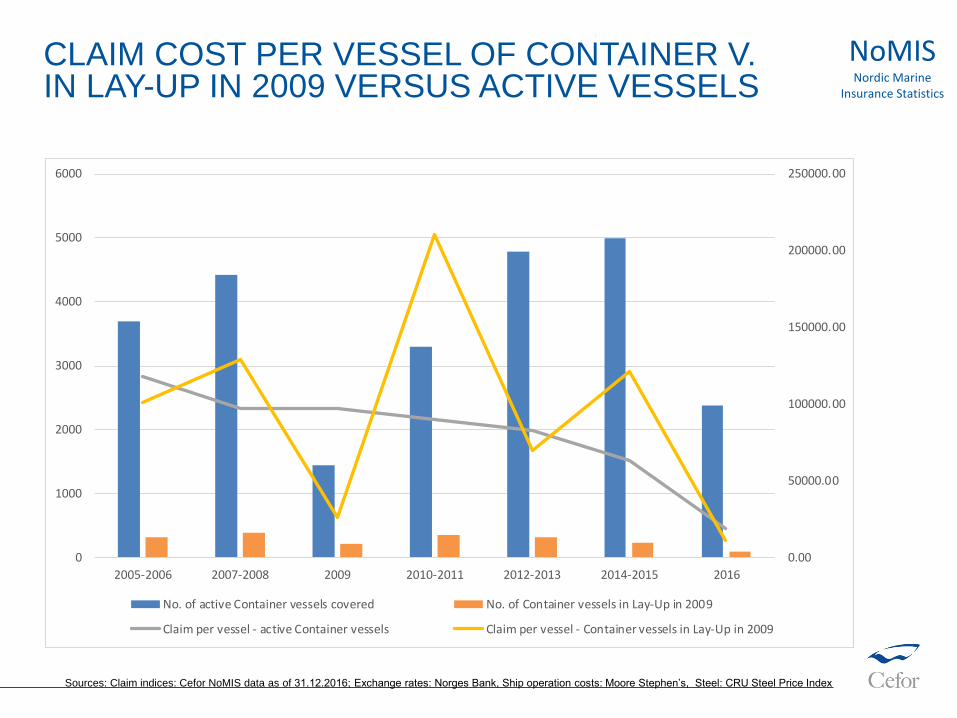

0.00

50000.00

100000.00

150000.00

200000.00

250000.00

0

1000

2000

3000

4000

5000

6000

2005-2006 2007-2008 2009 2010-2011 2012-2013 2014-2015 2016

No. of active Container vessels covered No. of Container vessels in Lay-Up in 2009

Claim per vessel - active Container vessels Claim per vessel - Container vessels in Lay-Up in 2009

Sources: Claim indices: Cefor NoMIS data as of 31.12.2016; Exchange rates: Norges Bank, Ship operation costs: Moore Stephen’s, Steel: CRU Steel Price Index

CLAIM COST PER VESSEL OF CONTAINER V.IN LAY-UP IN 2009 VERSUS ACTIVE VESSELS

NoMISNordic Marine

Insurance Statistics

SUMMARY LAY-UP EFFECT ON CLAIMS TRENDS

Container vessels in lay-up in 2009:

• Claims frequency was reduced by half during the period of inactivity.

• Claims frequency & cost were above average both before and after lay-up period!

Why also before lay-up? Substandard container vessels first put into lay-up?

Supply/Offshore vessels in lay-up in 2016:

• Claims frequency equally reduced during period of inactivity in 2016

• …but claims frequency before lay-up period was normal!

• How claims frequency develops after lay-up period remains to be seen!May be challenging to reactivate complex objects.

ISSUES TO MONITOR

High-value risks

Arctic risks

© Astrid Seltmann

© Astrid Seltmann

© Astrid Seltmann

Navigation

Oil price, fuel quality

New technology

Climate change

Changes in regulation (liabilities)

Human factor/Qualification

Dagfinn Bakke(Foto by Astrid Seltmann)Value accumulation

MSC Safety discussions!

Cyber risk

Fire on RoRo & Container vessels

Internet of things/complex technologies

IUMI REPORTS 2016/17:

IUMI Statistics: https://iumi.com/statistics

Conference publications: Spring statistics on Cargo, Hull, Offshore energy:

Cefor NoMIS Statistics at http://cefor.no/Statistics/NOMIS/

CEFOR PUBLICATIONS 2017 – HULL TRENDSNORDIC MARINE INSURANCE STATISTICS (NOMIS)

Publishing date 6 April 2017: