Global & Local Innovation Networks & Hierarchies in … & Local Innovation Networks & Hierarchies in...

11

Global & Local Innovation Networks & Hierarchies in Medical Biotechnology PD Philip Cooke Universities of Cardiff, Toulouse & Aalborg Presented to Centre for Innovation & Structural Change Conference Transforming Manufacturing Hubs into Internationally Competitive Clusters in Medical Technology: The Experiences of Massachusetts and Ireland Thursday 28th October 2010, Bailey Allen Hall, NUI Galway Aims of the paper • To analyse some key dynamics in biotechnology innovation processes • To anatomise some key biotechnology clusters in leading and learning clusters • To investigate the nature and connectivity of global biotechnology networks • To identify some key network hierarchies and consider lessons for Ireland

Transcript of Global & Local Innovation Networks & Hierarchies in … & Local Innovation Networks & Hierarchies in...

Global & Local Innovation Networks& Hierarchies in Medical

Biotechnology

PD Philip CookeUniversities of Cardiff, Toulouse & Aalborg

Presented to Centre for Innovation & Structural ChangeConference

Transforming Manufacturing Hubs into InternationallyCompetitive

Clusters in Medical Technology:The Experiences of Massachusetts and Ireland

Thursday 28th October 2010, Bailey Allen Hall, NUI Galway

Aims of the paper

• To analyse some key dynamics inbiotechnology innovation processes

• To anatomise some key biotechnologyclusters in leading and learning clusters

• To investigate the nature and connectivity ofglobal biotechnology networks

• To identify some key network hierarchies andconsider lessons for Ireland

Main Bioscience Competitors

Country Companies Public Cos. Market Cap.*Revenues* Employees* Pipeline*

USA 1,457 307 €205 bn. €27 bn. 191,000 872UK 331 46 €9.4 bn. €3 bn. 22,000 194Switzerland 129 5 €7.3 bn. €2 bn. 8,000 79France 239 6 €0.5 bn. €0.3 bn. 9,655 31Germany 369 13 €0.5 bn. €0.5 bn. 13,386 15

Table 2: Main International Bioscience Competitors, 2003Source: BIGT (2004)NB: * Public Company Data Only

Product PipelinesCountry Pre-clinical Phase 1 Phase 2 Phase 3 Pipeline Products

USA 584 96 148 44 872UK 65 50 56 23 194Switzerland 45 12 11 11 79Sweden 14 8 10 0 32France 16 8 6 1 31Denmark 14 5 5 4 28Italy 9 0 4 3 16Israel 2 3 6 4 15Germany 7 4 3 1 15Norway 8 2 2 3 15Netherlands 9 1 1 0 11Finland 9 1 0 0 10Ireland 2 0 2 3 7Belgium 2 0 1 3 3Total Europe 202 94 107 53 456

Table 3: Product Pipeline of Public Bioscience Companies WorldwideSource: BIGT (2004)

Productivity Decline for Pharma

Date US NCE Approvals R&D Expenditure $ billions(2001)

1963 19 21967 20 21971 18 31975 17 31979 16 31983 16 41987 19 51991 25 81995 25 151996 45 171997 37 181998 23 221999 32 252001 23 30

Table 4: Declining Pharmaceutical Productivity Over TimeSource: BIGT (2004)

United States Pharma-Biotech R&D Split

R&D expenditure

0

10

20

30

40

50

60

1998 99 2000 01 02 03 04

$bn Biotech

Big pharma

US Pharma-Biotech Innovation Performance

New drugs approved by the FDA

0

5

10

15

20

25

30

1998 99 2000 01 02 03 04

Biotech Big pharma

Key cluster rankings

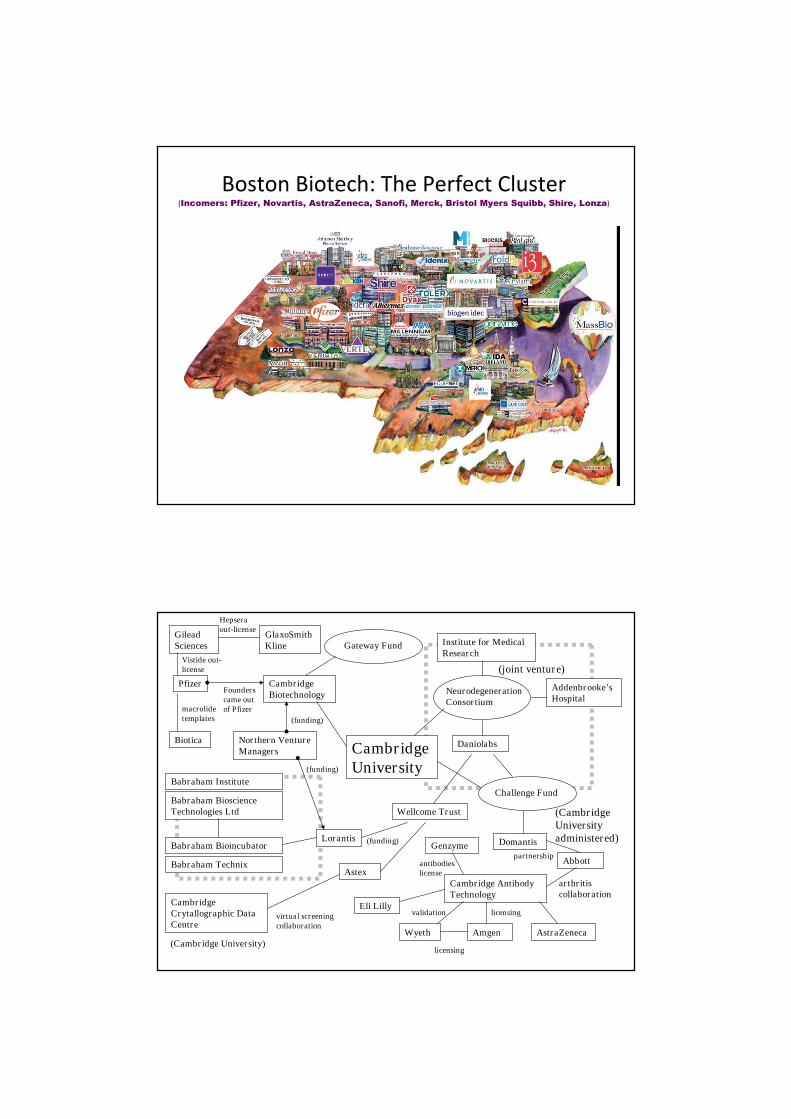

Boston: A TextbookBiosciences Megacentre

Boston Biotech: The Perfect Cluster(Incomers: Pfizer, Novartis, AstraZeneca, Sanofi, Merck, Bristol Myers Squibb, Shire, Lonza)

Addenbrooke’sHospital

CambridgeBiotechnology

Northern VentureManagers Cambridge

University

Pfizer

Lorantis

Cambridge AntibodyTechnology

Domantis

Abbott

Eli Lilly

Astex

Daniolabs

NeurodegenerationConsortium

Gateway Fund

Biotica

Babraham Institute

Babraham Bioincubator

Babraham Technix

Babraham BioscienceTechnologies Ltd Wellcome Trust

Wyeth Amgen AstraZeneca

CambridgeCrytallographic DataCentre

GlaxoSmithKline

GileadSciences

(joint venture)

(CambridgeUniversityadministered)

Institute for MedicalResearch

Challenge Fund

Founderscame outof Pfizermacrolide

templates

Vistide out-license

Hepseraout-license

virtual screeningcollaboration

(Cambridge University)

(funding)

partnership

arthritiscollaboration

(funding)

licensing

licensing

Genzyme

antibodieslicense

validation

(funding)

Boston Cluster

DBFAbroad

DBFNon-proximate

DBFProximate

Research InstituteProximate

DBFR&D Organiser

Research InstituteNon-proximate

Big PharmaProximate

Big PharmaNon-proximate

Sankyo (CA), Kirin (CA), Chugai (CA), Monsanto (MO), Abbott (IL), Bayer (NC),Paine Webber (NJ), Roche (NJ), Pharmacia Upjohn (NJ), Wyeth (PA) ScheringPlough (NJ), DuPont (DL), Rhone Poulenc (PA), Hoechst (NJ), Bristol MyersSquibb (NJ), Merck (NJ).

RWJohnson

(SD)

Stanford(SV)

BurnhamInstitute

(SD)

Alpha-Gene(G.Bos)

GeneticsInstitute(G. Bos)

ArQule(G. Bos)

Dyax(Camb)

Ariad(Camb)

Gene Therapy(G. Bos)

Genzyme(Camb)

Harvard(Camb)

Ontogeny(Camb)

Acadia(SD)

ICA Gen(NC)

Aurora (SD)

Chiron (SF)

Scriptgen(SD)

Scios (SD)

Genentech(SF)

Signal (SD)

Affymax(PA)

Immunex (WA)

Corvas (SD)

Genovo (PA)

Cytogen(PA)

MorphoSys (G) CambridgeAntibody Tech. (UK) Solvay (BE)

California Biosciences Cluster

proximate

roximate

Research Institute

DBF R&D Originator

Research Instituteproximate

Big Pharma Proximate

Proximate

Axys(SF)

Lynx(SV)

Incyte(SV)

Hyseq(SF)

Sanga-mo(SF)

PerkinElmer (SV)

KirinBiosciences

(SD)

Roche (SW), Pharmacia (SD), BASF (G), Hoechst (G), Rhone-Poulenc (F), Novo Nordisk(DK), Novartis (SW), Glaxo (UK), AstraZeneca (SD/UK), Bayer (G), Boehringer Ing. (G)Kirin (J).

Becton Dickinson (NJ), Pharmacia-Upjohn (NJ), Bristol Myers Squibb (NJ), BASF (NJ),Eli Lilly (IN), Abbott (IL), Monsanto (MO), Merck (NJ), J&J (NJ), Hoechst (NJ), Rhone-Poulenc (PA), DuPont (DL), Pfizer (NY), Schering Plough NJ), Novo Nordisk (NJ),Novartis (NY), Parke Davis (NJ), Glaxo (NC), AstraZeneca (MA), Bayer (NC), WarnerLambert (NJ), Procter & Gamble (OH) Boehringer Ingelheim (CT), Roche (NJ).

Irori(SD)

Trega(SD)

Script-gen(SD

Combi-Chem

(SD)Aurora

(SD)

UCSF

Cytovia(SD)

Lum-inex(TX)

ProteinDesign

(SV)

Isis(SD) Ono

(SF) Genentech(SF)

ZymoGenet

-ics(WA)

Ariad(MA)

Siddco (AZ)

Millen-nium(MA)

Biogen (MA)

NWNeu-ro

(OR)

Icos(WA)

Organon(NL)

Allelix(CAN)

Publishing Collaborations: Top 4 US BioscienceJournals

Stockholm Sydney

Uppsala Lund Copenhagen

San Diego San Fran Toronto

Tokyo

Boston Montreal

Jerusalem

New York

Cambridge(MA)

Singapore

Zurich

Cam(UK)

London

Geneva London

Oxford

1-2 3-56-7 >8

UCSD

Salk

SRI

BI

UCSF

SU

UBer

HMS

GH

MIT

HU

NYU

ColmU

RU

UU

USRIT

KI

OUJRH

CamU

MSR

ULSUAS

UTTML

UM

NUSDSI

UToTIT

HeUHaH

UNSW

UCL ICL

NIMR

ZU

BPRCUG

UCop

Graphic 2: Publishing Collaborations in 4 leading US Bioscience Journals

Publishing Collaborations: Top 5 EuropeanBioscience Journals

Stockholm Sydney

Copenhagen

Uppsala Lund

San Diego San Fran Toronto

Tokyo

Jerusalem Boston Montreal

New York

Munich Cambridge(MA)

Singapore

Zurich

Cam(UK)

London

Geneva London

Oxford

1 2-3>4:

UCSD

Salk

SRI

BI

UCSF

SU

UBer

HMS

GH

BUMIT

HU HU

MSSM

NYU

ColmU

RU

NVIUU

USRIT

KI

OUJRH

CamU

MSR

ULSUAS

UTTML

UM

NUSDSI

UToTIT

HeUHaH

UNSW

UCL ICL

LRINIMR

ZU

BPRCUG

UCopCBSP

MIPSUM

Graphic 1: Publishing Collaborations in 5 Leading European BioscienceJournals

Global Biotechnology Co-Patenting: 1998-2004

Paris Stockholm Copenhagen

San Diego Toronto

Tokyo

Jerusalem Boston Montreal

New York

Munich Cambridge(MA)

Singapore

Zurich Cam(UK)

London

London

Geneva Oxford

1-2 3-56-8 9+

UCSD

SG, Inc Salk

SRISP

LP

T,Inc SPhU

UCSFSU

G.IncAN

SI

HMSBWH

UMGH

CMCCHU

MITMP

WIBiogen

LugwigNYU

NFC MSK

RU

UP

OUJRH

CAT

CU

UToHSC

UMoMcU

NUSDSI

UUToSEC

HeU

Hadasit

RITKI

ICRTUL

MRC CRCT

ZUETH

FSA

RVAU

MPGFW

Global Bioscience Publication Shares

HMS

HMS HMS

HMS HMS

HMS

Stanford Uni

Stanford Uni

Stanford Uni

Stanford Uni

Stanford Uni

UCSF

UCSF

UCSF

UCSF

UCSF

UCSF

UCSF

UBerkley

UBerkley

UBerkleyUCSD

UCSD

UCSD

UCSD

UCSD

UCSD

RU

RU

MIT

MIT

MIT

Salk

Cam Uni

Cam Uni

Cam Uni

Cam Uni

KI

KIKI

Scripps

Scripps

Scripps

NYU

NYUUCL

UT

Zurich Uni

Zurich Uni

Hebrew UniHMS

Stanford Uni

Stanford Uni

UBerkley

UCSDRU RU

RU

RU

RU

MIT

MIT

MIT

SalkSalk

Salk

SalkCam Uni

Cam Uni

KI

Scripps

NYU

UCL

UT

UT

Hebrew Uni1.00

10.00

Immun

olog

y

Molecular

Biolo

gy&Gen

etics

Microbiolo

gy

Neuros

cienc

e

Biotec

hnolog

y&Ap

pliedMicrob

iology

Cell&

Deve

lopm

ental B

iolog

y

Biop

hysics

&Bioc

hemist

ry

HM S

Stanfo rdUni

UCSF

UBerkley

UCSD

RU

M IT

Salk

Cam Uni

KI

Scripps

NYU

UCL

UT

ZurichUni

HebrewUni

Bioscience Led The Way

• 1992-2002 biochemistry & molecular biology most cited US &EU patent fields >46%.

• Pharmaceuticals firms outsourced 30% 2003 R&D budgets.Reached 50% by 2005, expected 2010

• Bioregions co-publish with each other and leading bioregionsdominate a global innovation system

• No longer dominated by corporate in-house R&D• Regional knowledge domains

Now Others Follow• Open innovation (Chesbrough, 2003)• Philips ‘Sense & Simplicity’ rebranding, R&D strategy

based on ‘open innovation’• Cisco & Microsoft practise ‘open innovation’ through

acquisition• Dupont closed its central laboratories• Lucent, IBM practise ‘open innovation’• German auto industry now ‘managed’ by Frankfurt design

& engineering consultancies• Procter & Gamble/Gillette funded by ‘C&D’ open

innovation

Conclusions

• Key dynamics in biotechnology innovationprocesses are ‘neo-linear’ Labe-DBFs-Pharma

• Leading biotechnology clusters have richgeographic proximities, learning ones don’t

• The nature and connectivity of globalbiotechnology networks are exclusive and US-led

• Key network hierarchies are Greater Boston andHMS at the global peak.

• Ireland has a global biopharma player (Elan) butlacks cluster specificity. Other small countrieshave DBF clusters