Global Imbalances— 2017 External Sector...

28

International Monetary Fund Global Imbalances— 2017 External Sector Report Gustavo Adler and Luis Cubeddu IMF Research Department Bruegel Brussels, September 26, 2017

Transcript of Global Imbalances— 2017 External Sector...

International Monetary Fund

Global Imbalances—2017 External Sector Report

Gustavo Adler and Luis CubedduIMF Research Department

BruegelBrussels, September 26, 2017

I. Recent developmentsII. Assessing external positionsIII. External assessments for 2016IV. Outlook, Risks and PoliciesV. Analytical themes

2

Roadmap

I. Recent developments

3

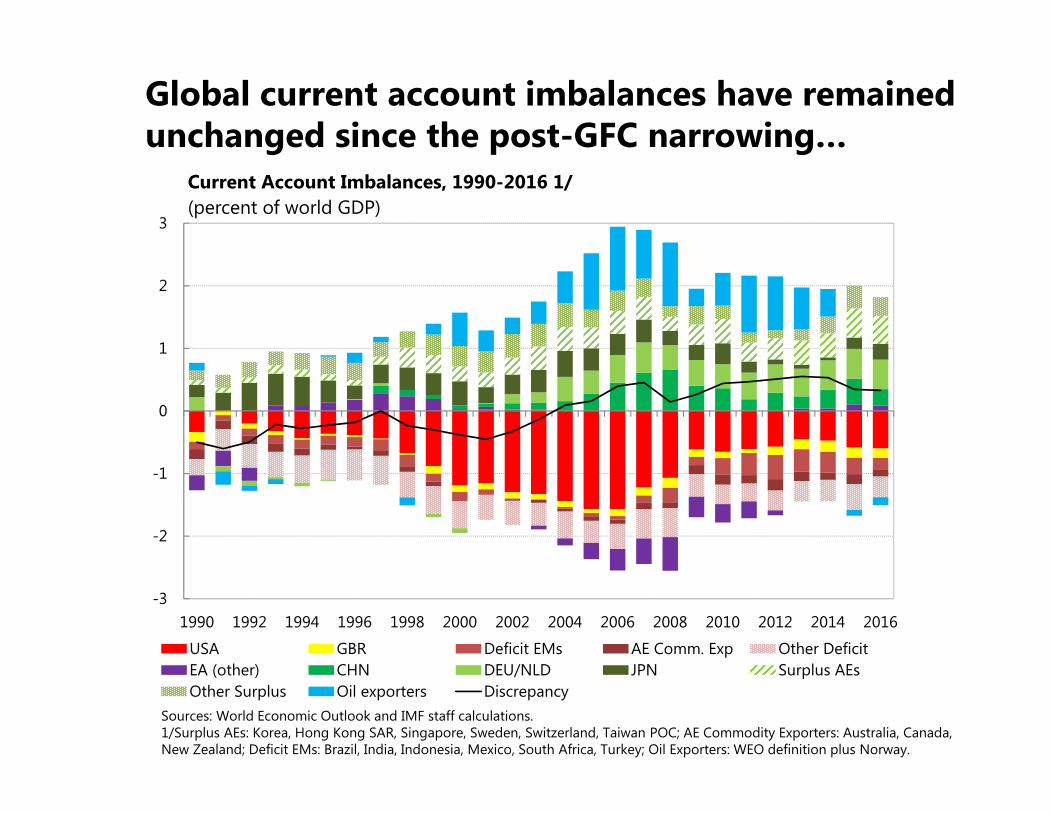

Global current account imbalances have remained unchanged since the post-GFC narrowing…

-3

-2

-1

0

1

2

3

1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010 2012 2014 2016

Current Account Imbalances, 1990-2016 1/ (percent of world GDP)

USA GBR Deficit EMs AE Comm. Exp Other DeficitEA (other) CHN DEU/NLD JPN Surplus AEsOther Surplus Oil exporters Discrepancy

Sources: World Economic Outlook and IMF staff calculations.1/Surplus AEs: Korea, Hong Kong SAR, Singapore, Sweden, Switzerland, Taiwan POC; AE Commodity Exporters: Australia, Canada, New Zealand; Deficit EMs: Brazil, India, Indonesia, Mexico, South Africa, Turkey; Oil Exporters: WEO definition plus Norway.

-20 -10 0 10 20 30

AE Comm. Exp

Oil exporters

Other deficit

EA (other)

DEU/NLD

Deficit EMs

JPN

Surplus AEs

Other surplus

GBR

CHN

USA

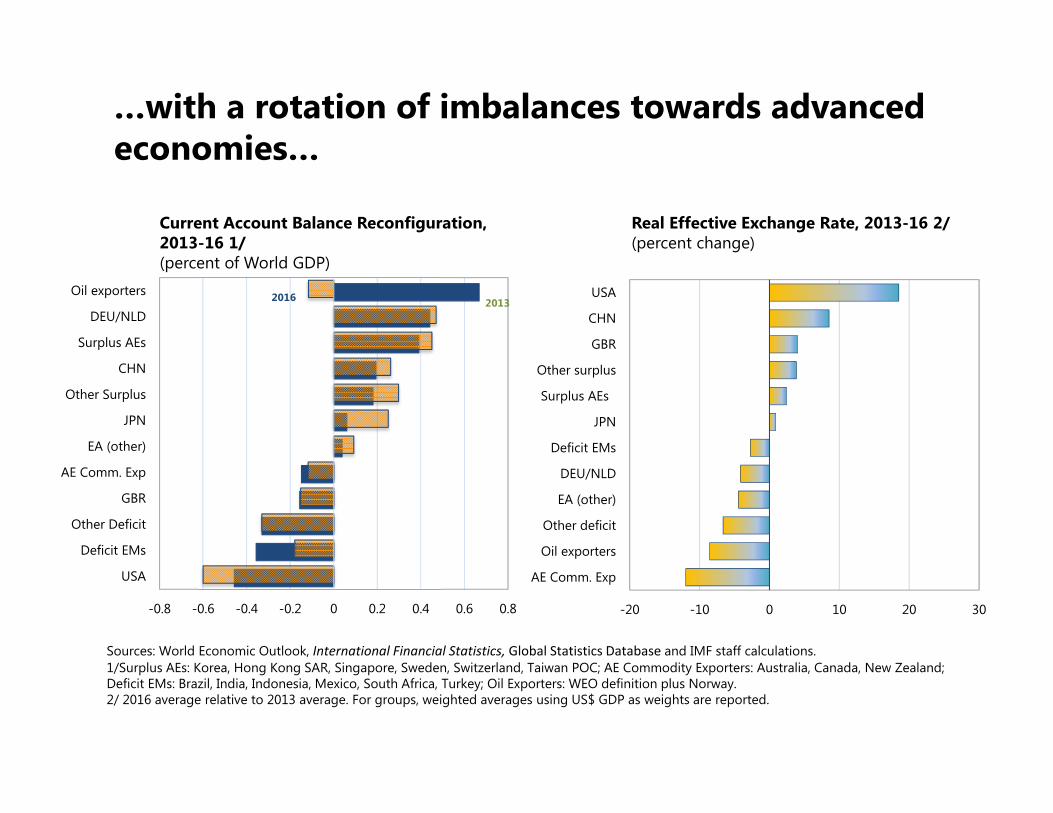

-0.8 -0.6 -0.4 -0.2 0 0.2 0.4 0.6 0.8

USA

Deficit EMs

Other Deficit

GBR

AE Comm. Exp

EA (other)

JPN

Other Surplus

CHN

Surplus AEs

DEU/NLD

Oil exporters 2016 2013

Current Account Balance Reconfiguration, 2013-16 1/(percent of World GDP)

Real Effective Exchange Rate, 2013-16 2/(percent change)

Sources: World Economic Outlook, International Financial Statistics, Global Statistics Database and IMF staff calculations.1/Surplus AEs: Korea, Hong Kong SAR, Singapore, Sweden, Switzerland, Taiwan POC; AE Commodity Exporters: Australia, Canada, New Zealand; Deficit EMs: Brazil, India, Indonesia, Mexico, South Africa, Turkey; Oil Exporters: WEO definition plus Norway.2/ 2016 average relative to 2013 average. For groups, weighted averages using US$ GDP as weights are reported.

…with a rotation of imbalances towards advanced economies…

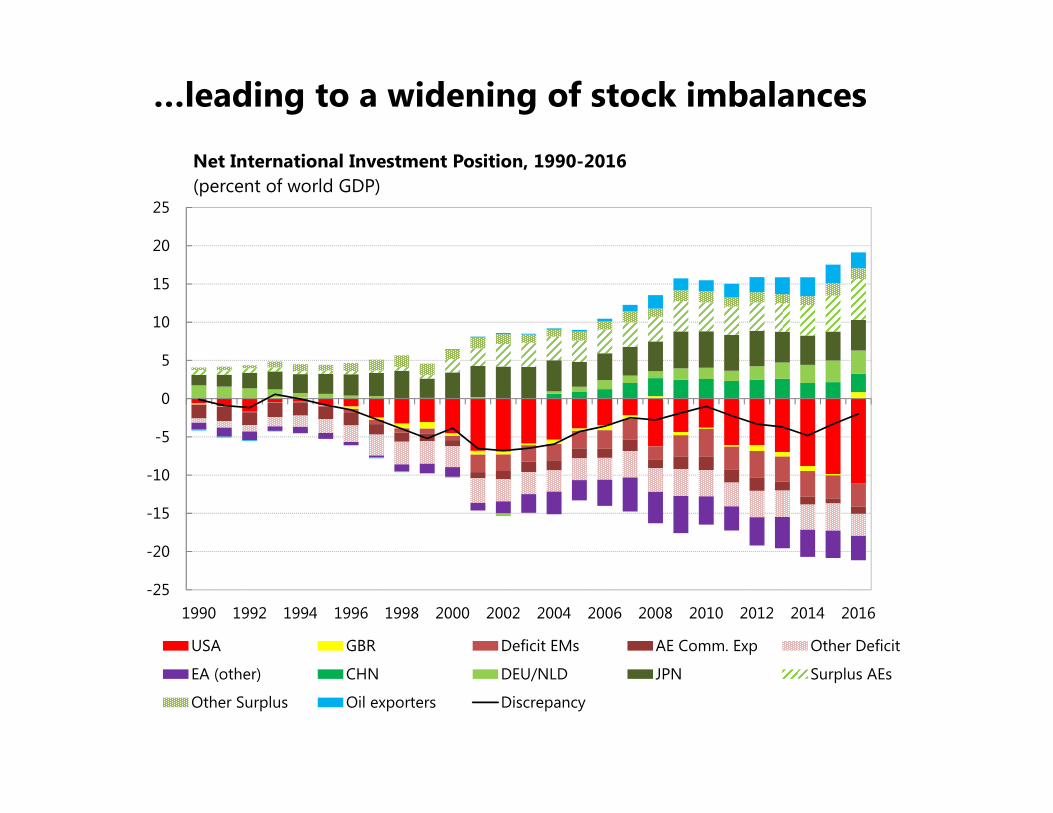

…leading to a widening of stock imbalances

-25

-20

-15

-10

-5

0

5

10

15

20

25

1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010 2012 2014 2016

Net International Investment Position, 1990-2016 (percent of world GDP)

USA GBR Deficit EMs AE Comm. Exp Other Deficit

EA (other) CHN DEU/NLD JPN Surplus AEs

Other Surplus Oil exporters Discrepancy

II. Assessing external positions

7

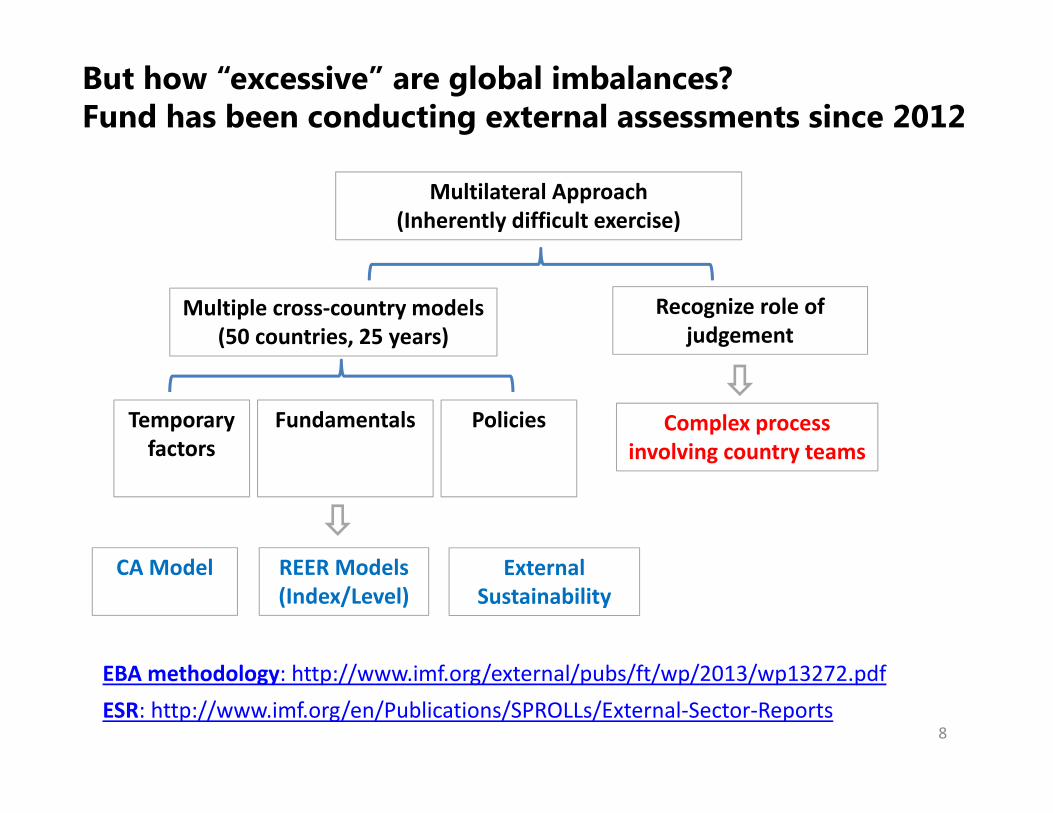

But how “excessive” are global imbalances? Fund has been conducting external assessments since 2012

8

Multilateral Approach(Inherently difficult exercise)

CA Model

Temporary factors

Multiple cross-country models (50 countries, 25 years)

Recognize role of judgement

External Sustainability

REER Models(Index/Level)

Policies Complex process involving country teams

Fundamentals

EBA methodology: http://www.imf.org/external/pubs/ft/wp/2013/wp13272.pdfESR: http://www.imf.org/en/Publications/SPROLLs/External-Sector-Reports

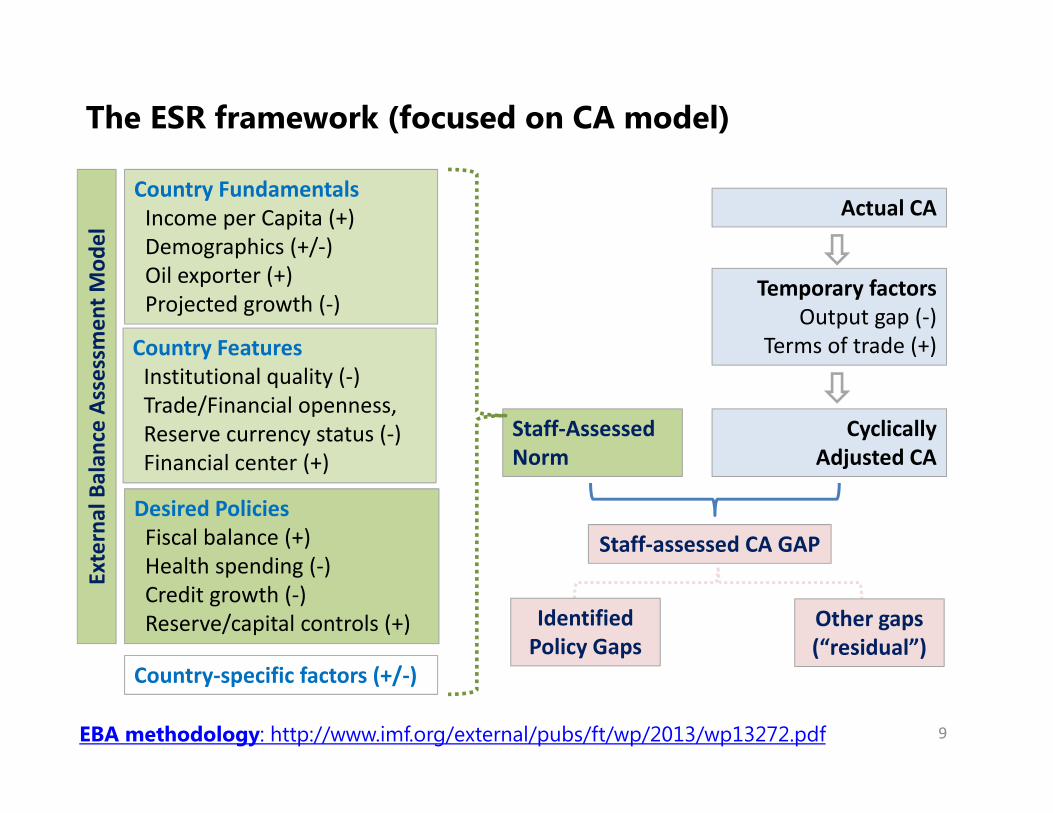

The ESR framework (focused on CA model)

9

Country FundamentalsIncome per Capita (+)Demographics (+/-)Oil exporter (+)Projected growth (-)

Desired PoliciesFiscal balance (+)Health spending (-)Credit growth (-)Reserve/capital controls (+)

Staff-Assessed Norm

Actual CA

Temporary factorsOutput gap (-)

Terms of trade (+)

Cyclically Adjusted CA

Staff-assessed CA GAP

Identified Policy Gaps

Other gaps (“residual”)

Country-specific factors (+/-)

Exte

rnal

Bal

ance

Ass

essm

ent M

odel

EBA methodology: http://www.imf.org/external/pubs/ft/wp/2013/wp13272.pdf

Country FeaturesInstitutional quality (-)Trade/Financial openness,Reserve currency status (-)Financial center (+)

III. External Assessments for 2016

10

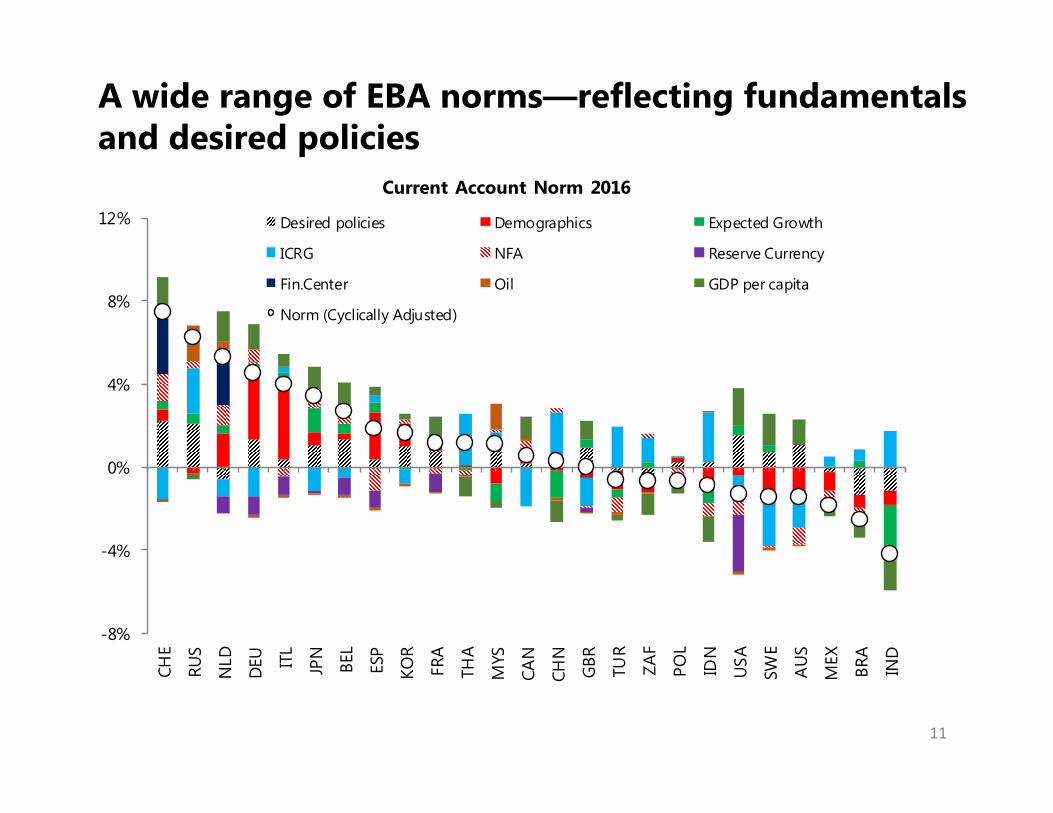

A wide range of EBA norms—reflecting fundamentals and desired policies

11

-8%

-4%

0%

4%

8%

12%

CHE

RUS

NLD

DEU IT

L

JPN

BEL

ESP

KOR

FRA

THA

MYS

CAN

CHN

GBR TU

R

ZAF

POL

IDN

USA

SWE

AU

S

MEX

BRA

IND

Current Account Norm 2016

Desired policies Demographics Expected Growth

ICRG NFA Reserve Currency

Fin.Center Oil GDP per capita

Norm (Cyclically Adjusted)

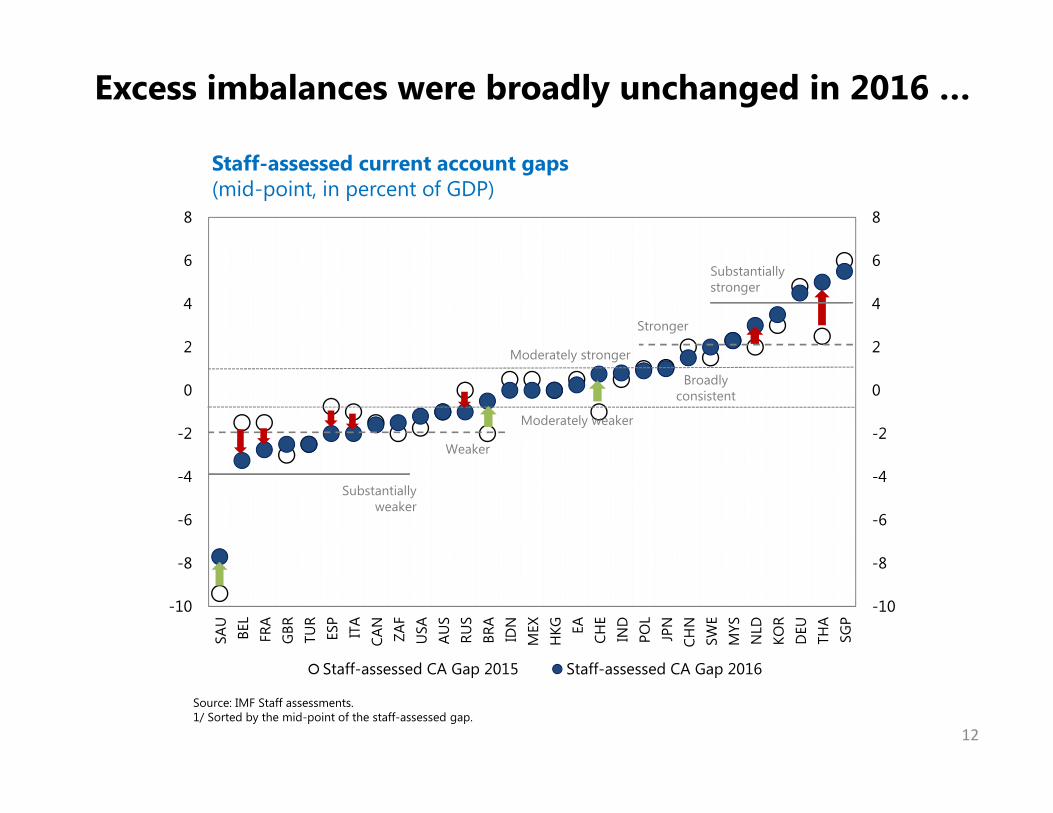

Excess imbalances were broadly unchanged in 2016 …

Staff-assessed current account gaps(mid-point, in percent of GDP)

Source: IMF Staff assessments.1/ Sorted by the mid-point of the staff-assessed gap.

-10

-8

-6

-4

-2

0

2

4

6

8

-10

-8

-6

-4

-2

0

2

4

6

8SA

UBE

LFR

AG

BR TUR

ESP

ITA

CAN

ZAF

USA

AUS

RUS

BRA

IDN

MEX

HKG EA

CHE

IND

POL

JPN

CHN

SWE

MYS

NLD

KOR

DEU

THA

SGP

Staff-assessed CA Gap 2015 Staff-assessed CA Gap 2016

Weaker

Moderately weaker

Broadlyconsistent

Moderately stronger

Stronger

Substantiallystronger

Substantiallyweaker

12

CHNJPN

EA

USA

GBR

DEU

NLD

ESPITA

BEL

FRA

SGP

KOR

SWE

HKG

CHE

AUS

CAN

THA

MYS

POL IND

IDNMEX

RUSBRA

ZAF TUR

-4

-3

-2

-1

0

1

2

3

4

5

6

-20 -15 -10 -5 0 5 10 15 20

Staff-assessed REER GAP(in percent)

Staf

f-as

sess

ed C

A G

AP

(in p

erce

nt o

f GD

P)

OvervaluedUndervaluedWea

ker

Stro

nger

Staff-assessed Current Account and REER Gaps, 2016

Source: IMF Staff assessments.1/ Midpoints of REER and CA Gaps. Shaded area represents general range for "broadly in line" assessment.

Staff-assessed REER gaps in line with CA gaps for most cases.

13

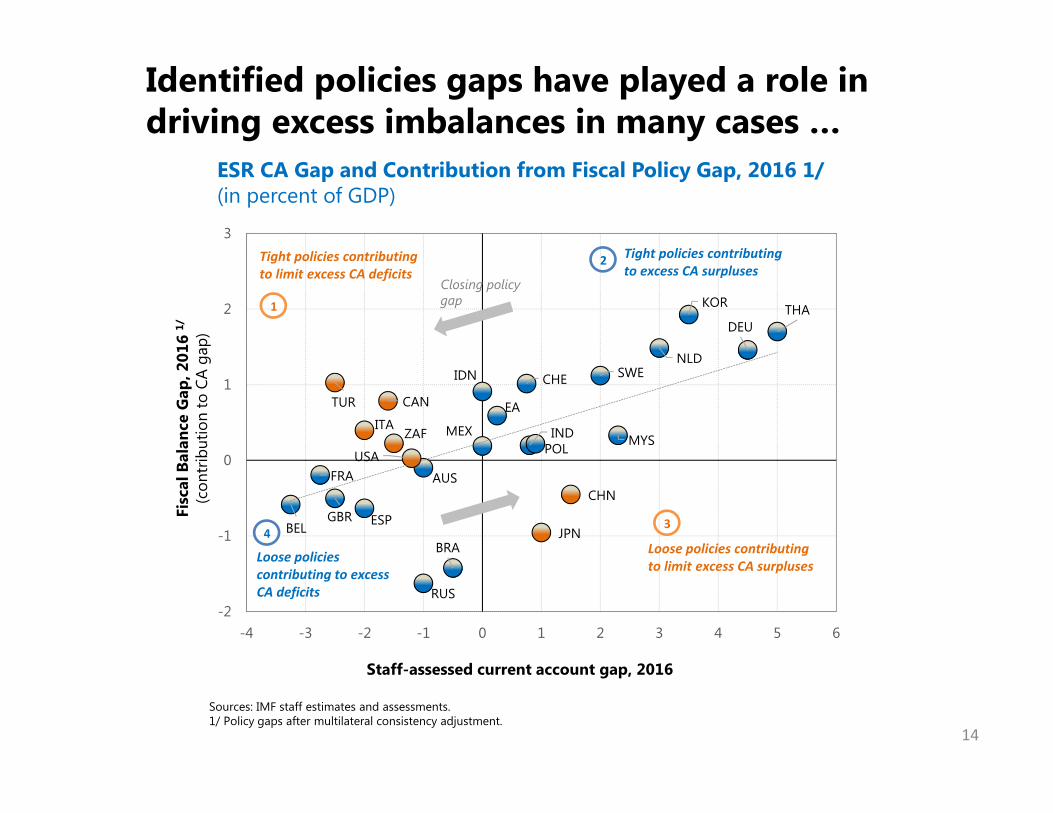

Identified policies gaps have played a role in driving excess imbalances in many cases …

ESR CA Gap and Contribution from Fiscal Policy Gap, 2016 1/ (in percent of GDP)

14

GBR

TUR

ZAF

BRA

USA

CAN

BEL

FRA AUS

CHE

ITA

ESP

RUS

EA

MEX

IDN

INDPOL

JPN

SWE

CHN

NLD

THA

MYS

KOR

DEU

-2

-1

0

1

2

3

-4 -3 -2 -1 0 1 2 3 4 5 6

Staff-assessed current account gap, 2016

Fisc

al B

alan

ce G

ap, 2

016

1/

(con

trib

utio

n to

CA

gap)

Tight policies contributing to excess CA surpluses

Loose policies contributing to excess CA deficits

Tight policies contributing to limit excess CA deficits

Loose policies contributing to limit excess CA surpluses

1

2

43

Closing policy gap

Sources: IMF staff estimates and assessments.1/ Policy gaps after multilateral consistency adjustment.

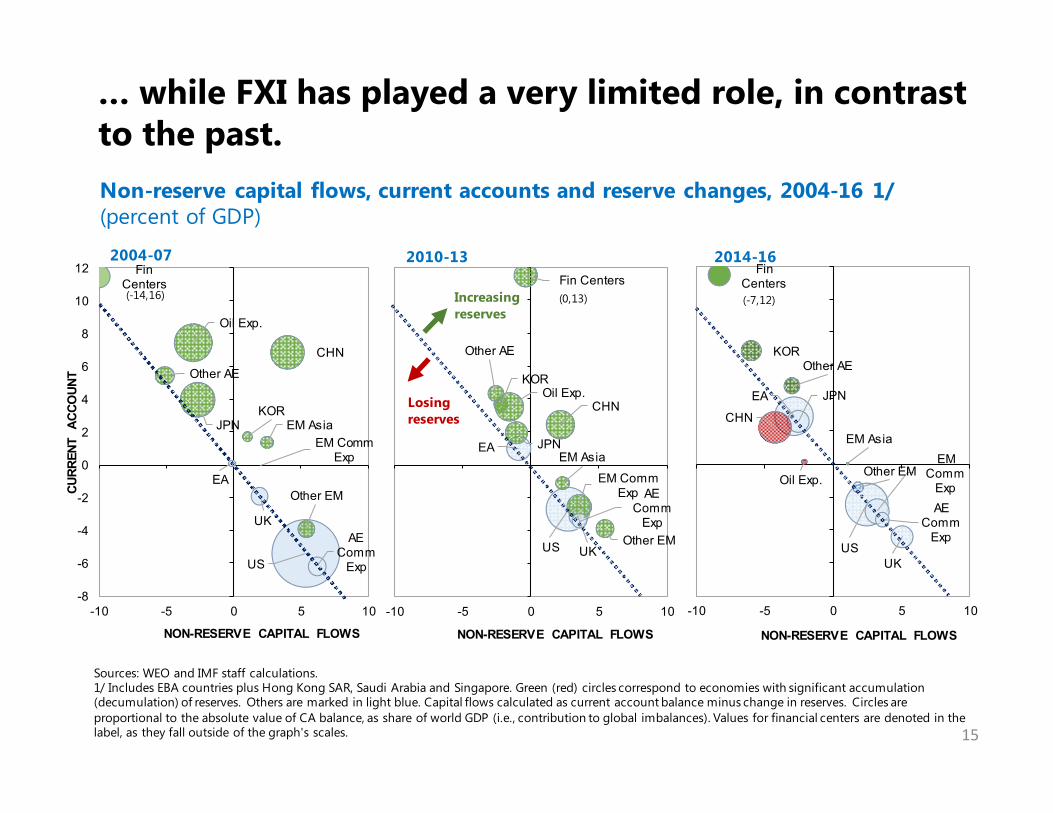

… while FXI has played a very limited role, in contrast to the past.

US

EA JPN

UK

CHN

KOROil Exp.

EM Comm Exp

EM Asia

Other EM

AE Comm

Exp

Other AE

Fin Centers

-8

-6

-4

-2

0

2

4

6

8

10

12

-10 -5 0 5 10

NON-RESERVE CAPITAL FLOWS

(0,13)Increasing reserves

Losing reserves

US

EA JPN

UK

CHN

KOR

Oil Exp.

EM Comm

Exp

EM Asia

Other EM

AE Comm

Exp

Other AE

Fin Centers

-8

-6

-4

-2

0

2

4

6

8

10

12

-10 -5 0 5 10

NON-RESERVE CAPITAL FLOWS

(-7,12)

2010-13 2014-16

Non-reserve capital flows, current accounts and reserve changes, 2004-16 1/(percent of GDP)

US

EA

JPN

UK

CHN

KOR

Oil Exp.

EM Comm Exp

EM Asia

Other EM

AE Comm

Exp

Other AE

Fin Centers

-8

-6

-4

-2

0

2

4

6

8

10

12

-10 -5 0 5 10

CURR

ENT

ACCO

UNT

NON-RESERVE CAPITAL FLOWS

(-14,16)

2004-07

Sources: WEO and IMF staff calculations.1/ Includes EBA countries plus Hong Kong SAR, Saudi Arabia and Singapore. Green (red) circles correspond to economies with significant accumulation (decumulation) of reserves. Others are marked in light blue. Capital flows calculated as current account balance minus change in reserves. Circles are proportional to the absolute value of CA balance, as share of world GDP (i.e., contribution to global imbalances). Values for financial centers are denoted in the label, as they fall outside of the graph's scales. 15

-0.8

-0.6

-0.4

-0.2

0.0

0.2

0.4

0.6

0.8

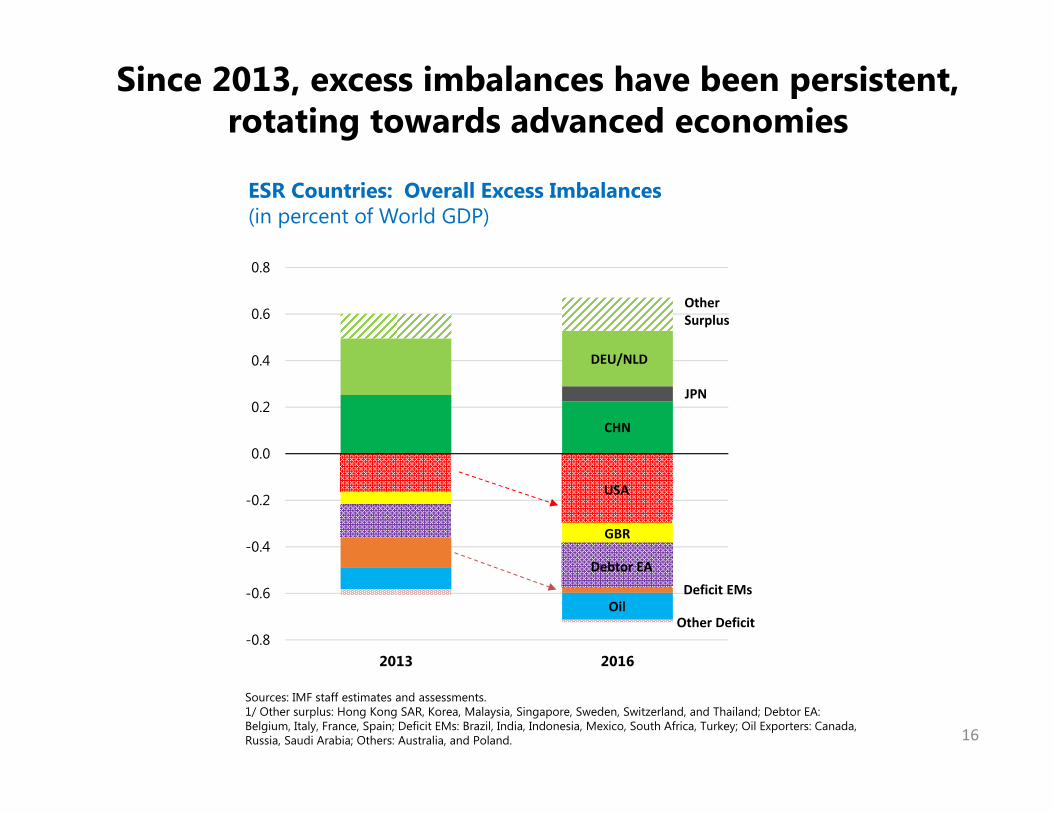

2013 2016

USA

GBR

Debtor EA

Deficit EMsOil

CHN

DEU/NLD

JPN

Other Surplus

Other Deficit

Sources: IMF staff estimates and assessments.1/ Other surplus: Hong Kong SAR, Korea, Malaysia, Singapore, Sweden, Switzerland, and Thailand; Debtor EA: Belgium, Italy, France, Spain; Deficit EMs: Brazil, India, Indonesia, Mexico, South Africa, Turkey; Oil Exporters: Canada, Russia, Saudi Arabia; Others: Australia, and Poland.

ESR Countries: Overall Excess Imbalances (in percent of World GDP)

Since 2013, excess imbalances have been persistent, rotating towards advanced economies

16

IV. Outlook, Risks and Policies

17

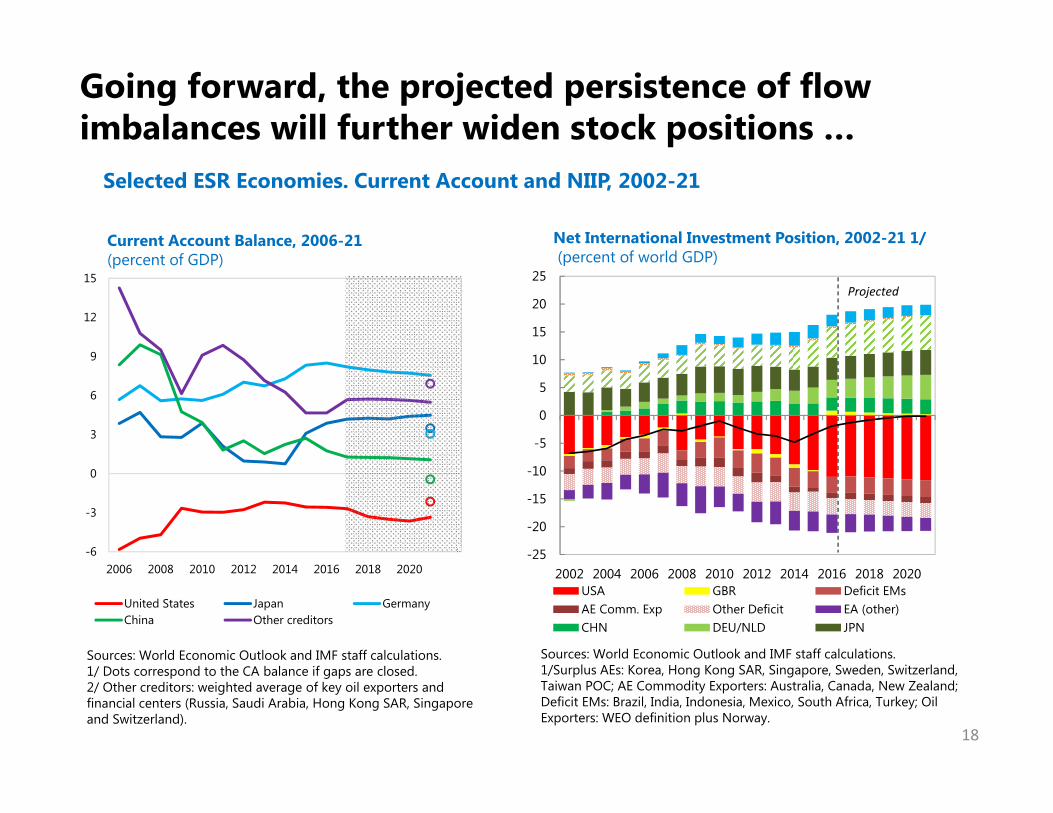

Going forward, the projected persistence of flow imbalances will further widen stock positions …

Selected ESR Economies. Current Account and NIIP, 2002-21

-6

-3

0

3

6

9

12

15

2006 2008 2010 2012 2014 2016 2018 2020

United States Japan GermanyChina Other creditors

Current Account Balance, 2006-21(percent of GDP)

-25

-20

-15

-10

-5

0

5

10

15

20

25

2002 2004 2006 2008 2010 2012 2014 2016 2018 2020USA GBR Deficit EMsAE Comm. Exp Other Deficit EA (other)CHN DEU/NLD JPN

Projected

Sources: World Economic Outlook and IMF staff calculations.1/Surplus AEs: Korea, Hong Kong SAR, Singapore, Sweden, Switzerland, Taiwan POC; AE Commodity Exporters: Australia, Canada, New Zealand; Deficit EMs: Brazil, India, Indonesia, Mexico, South Africa, Turkey; Oil Exporters: WEO definition plus Norway.

Net International Investment Position, 2002-21 1/(percent of world GDP)

18

Sources: World Economic Outlook and IMF staff calculations.1/ Dots correspond to the CA balance if gaps are closed.2/ Other creditors: weighted average of key oil exporters and financial centers (Russia, Saudi Arabia, Hong Kong SAR, Singapore and Switzerland).

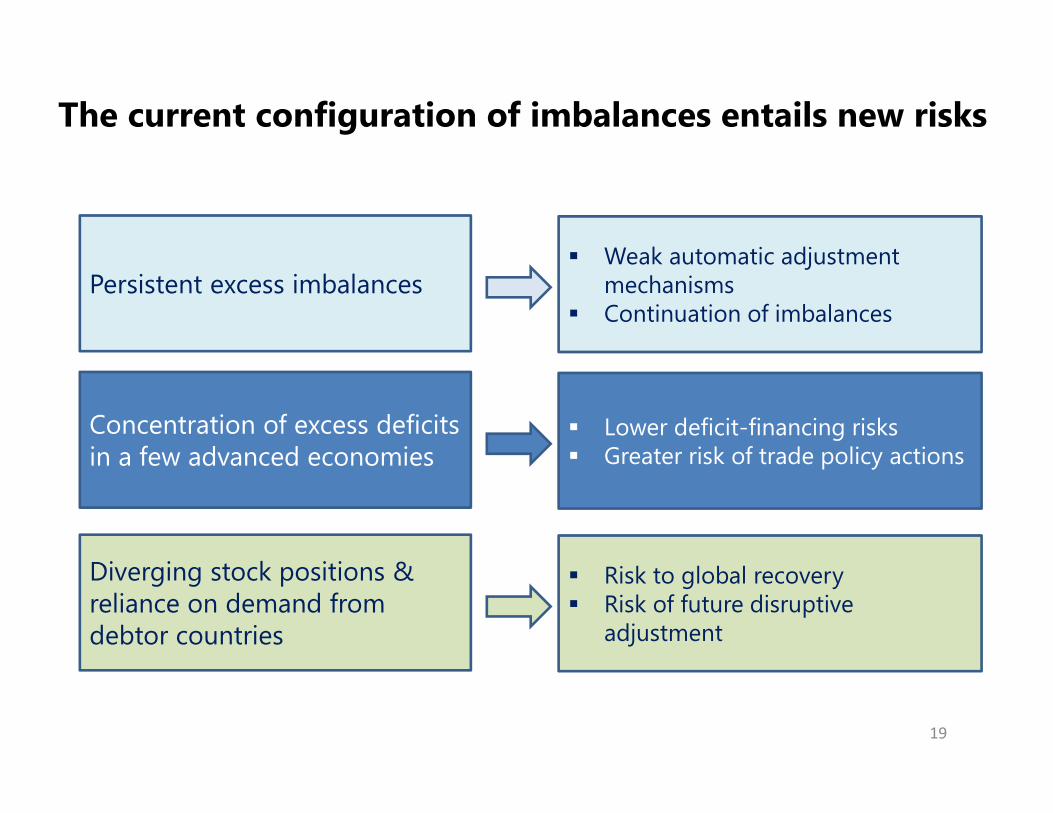

The current configuration of imbalances entails new risks

19

Persistent excess imbalances Weak automatic adjustment

mechanisms Continuation of imbalances

Concentration of excess deficits in a few advanced economies

Lower deficit-financing risks Greater risk of trade policy actions

Diverging stock positions & reliance on demand from debtor countries

Risk to global recovery Risk of future disruptive

adjustment

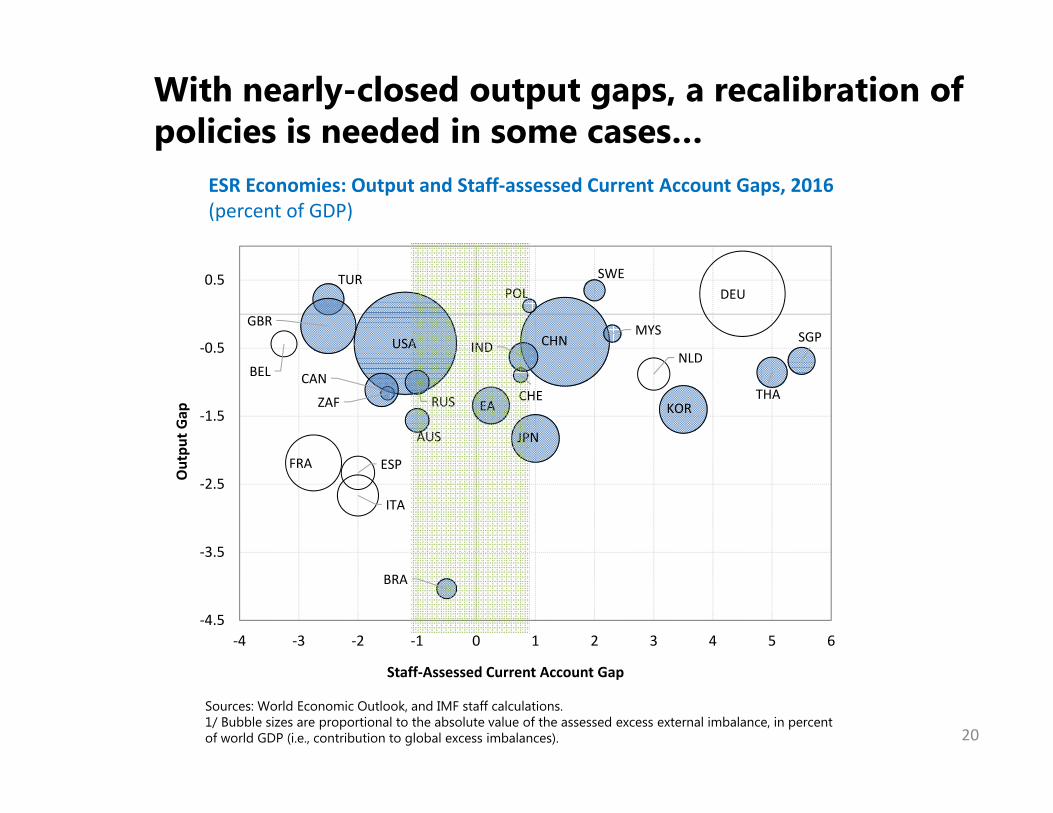

With nearly-closed output gaps, a recalibration of policies is needed in some cases…

BEL

ITA

JPN

USA

AUS

CHN

FRA

KOR

MYS

POL

RUSZAF

SWE

CHE THA

TUR

BRA

CAN

EA

DEU

INDNLD

ESP

GBRSGP

-4.5

-3.5

-2.5

-1.5

-0.5

0.5

-4 -3 -2 -1 0 1 2 3 4 5 6

Out

put G

ap

Staff-Assessed Current Account Gap

ESR Economies: Output and Staff-assessed Current Account Gaps, 2016(percent of GDP)

Sources: World Economic Outlook, and IMF staff calculations. 1/ Bubble sizes are proportional to the absolute value of the assessed excess external imbalance, in percent of world GDP (i.e., contribution to global excess imbalances). 20

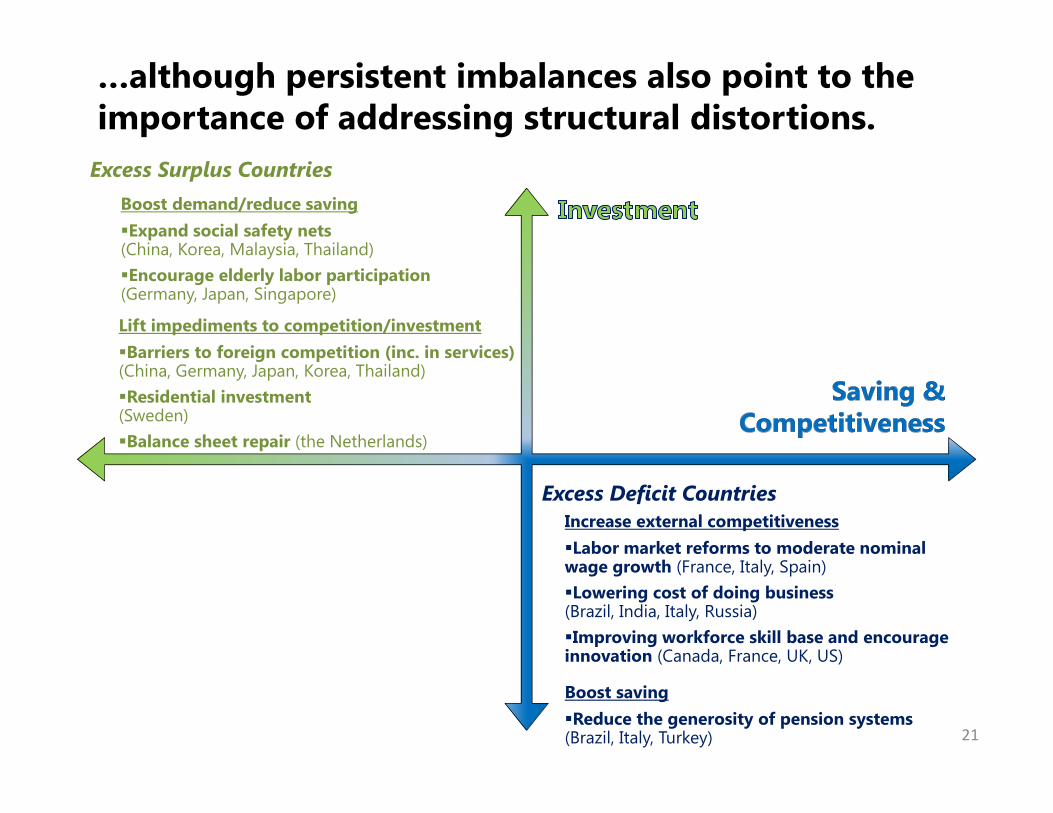

…although persistent imbalances also point to the importance of addressing structural distortions.

Excess Surplus Countries

Excess Deficit Countries

Boost demand/reduce savingExpand social safety nets (China, Korea, Malaysia, Thailand)Encourage elderly labor participation (Germany, Japan, Singapore)

Lift impediments to competition/investmentBarriers to foreign competition (inc. in services)(China, Germany, Japan, Korea, Thailand)Residential investment(Sweden)Balance sheet repair (the Netherlands)

Increase external competitivenessLabor market reforms to moderate nominal wage growth (France, Italy, Spain)Lowering cost of doing business (Brazil, India, Italy, Russia)Improving workforce skill base and encourage innovation (Canada, France, UK, US)

Boost savingReduce the generosity of pension systems(Brazil, Italy, Turkey) 21

V. Analytical themes

22

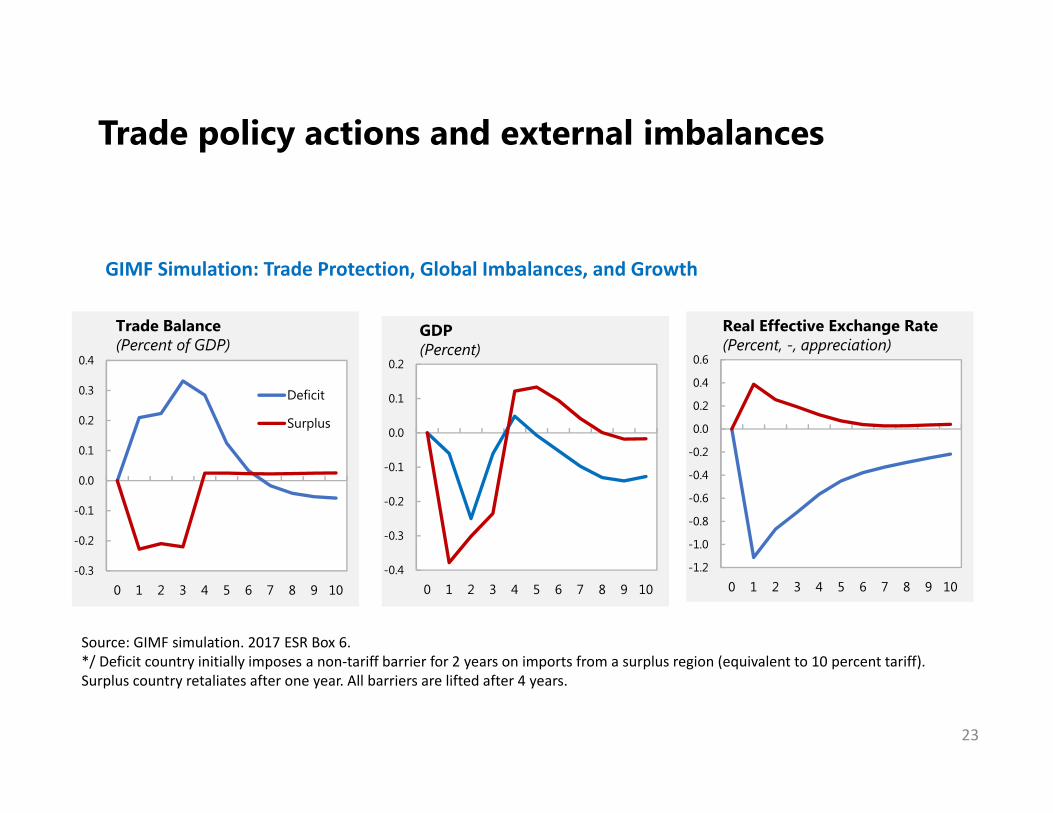

Trade policy actions and external imbalances

GIMF Simulation: Trade Protection, Global Imbalances, and Growth

23

-0.3

-0.2

-0.1

0.0

0.1

0.2

0.3

0.4

0 1 2 3 4 5 6 7 8 9 10

Deficit

Surplus

Trade Balance(Percent of GDP)

-0.4

-0.3

-0.2

-0.1

0.0

0.1

0.2

0 1 2 3 4 5 6 7 8 9 10

GDP(Percent)

-1.2

-1.0

-0.8

-0.6

-0.4

-0.2

0.0

0.2

0.4

0.6

0 1 2 3 4 5 6 7 8 9 10

Real Effective Exchange Rate(Percent, -, appreciation)

Source: GIMF simulation. 2017 ESR Box 6.*/ Deficit country initially imposes a non-tariff barrier for 2 years on imports from a surplus region (equivalent to 10 percent tariff). Surplus country retaliates after one year. All barriers are lifted after 4 years.

24

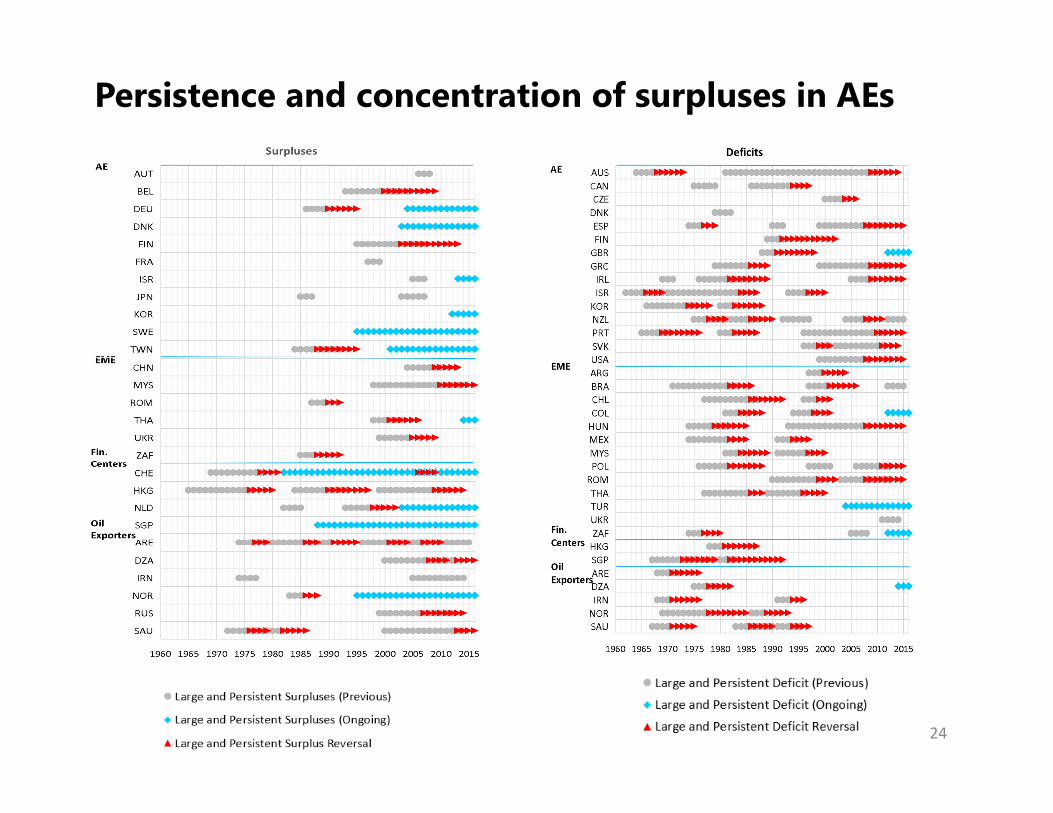

Persistence and concentration of surpluses in AEs

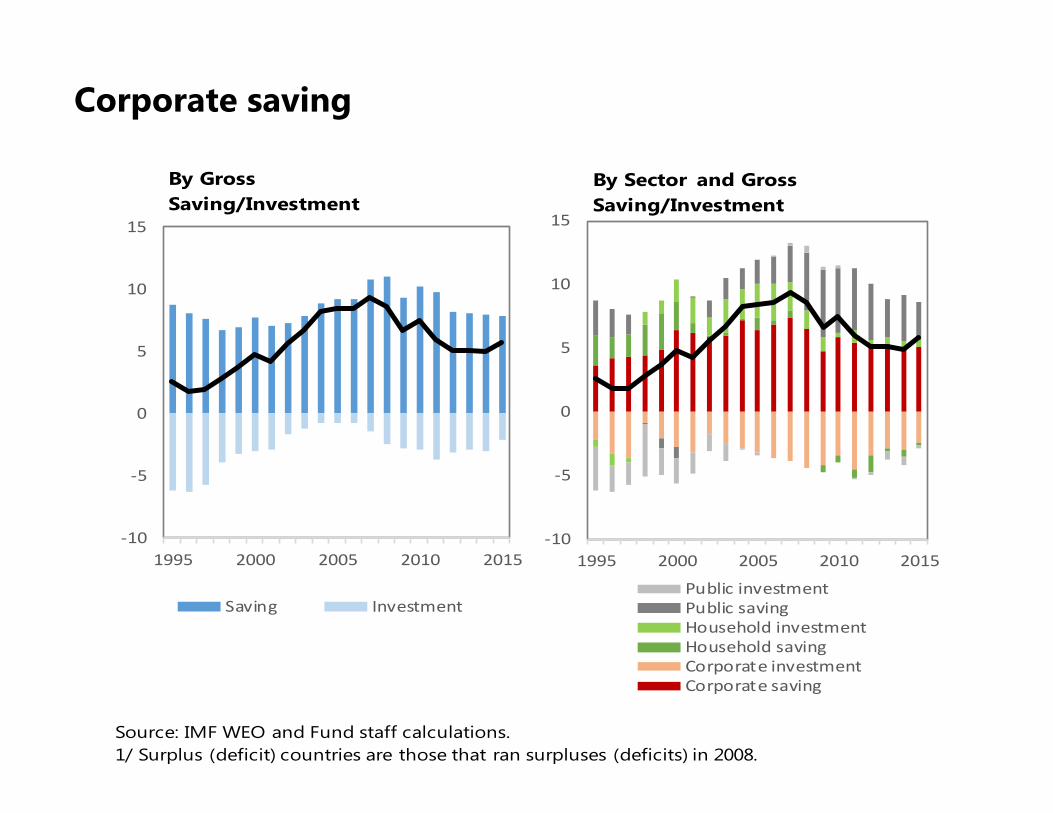

Corporate saving

25

-10

-5

0

5

10

15

1995 2000 2005 2010 2015

Saving Investment

-10

-5

0

5

10

15

1995 2000 2005 2010 2015

Public investmentPublic savingHousehold investmentHousehold savingCorporate investmentCorporate saving

By Gross Saving/Investment

By Sector and GrossSaving/Investment

Source: IMF WEO and Fund staff calculations.1/ Surplus (deficit) countries are those that ran surpluses (deficits) in 2008.

Key TakeawaysExcess imbalances broadly unchanged in 2016

Since 2013, a rotation of excessimbalances towards advanced economies

Persistent imbalances

Recent developments and outlook

Need to recalibrate policies and tackle structural distortions

o Despite narrowing after the GFC, progress in reducing excess global imbalances has stalled in recent years

o Largest excess surpluses driven in part by ‘too tight’ policieso Limited FXI, in contrast to the past

o Since 2013, narrowing of excess deficits in key EMso Larger excess surpluses and deficits in key advanced economies

o With nearly-closed output gaps, tackling external imbalances requires a recalibration of the policy mix in key economies

o Reforms to tackle structural distortions leading to excess external positionso Supporting free trade is key to sustaining the global recovery

o No significant changes since 2016, but elevated policy uncertaintyo Continuation of flow imbalances will further widen stock imbalanceso Reliance on demand from debtor countries

o Persistent excess imbalances (excess surpluses in particular) point to weak automatic adjustment mechanismso Sustained excess imbalances in countries with rigid currency

arrangements (EA, oil exporters)o Structural distortions to saving/investment

26

Some useful links

2017 External Sector Reporthttp://www.imf.org/en/Publications/Policy-Papers/Issues/2017/07/27/2017-

external-sector-report

“Global Imbalances: Avoiding a Tragedy of the Commons” (blog)https://blogs.imf.org/2017/07/28/global-imbalances-avoiding-a-tragedy-of-

the-commons/

“Assessing Global Imbalances: The Nuts and Bolts” (blog)https://blogs.imf.org/2017/06/26/assessing-global-imbalances-the-nuts-and-

bolts/

EBA Methodology (working paper)http://www.imf.org/external/pubs/ft/wp/2013/wp13272.pdf

International Monetary Fund

Global Imbalances—2017 External Sector Report

Gustavo Adler and Luis CubedduIMF Research Department

BruegelBrussels, September 26, 2017