Global FMCG: Finding Opportunities

38

GLOBAL FMCG: FINDING OPPORTUNITIES PLMA ACCESSING EXPORT MARKETS CONFERENCE REHAN PANDITARATNE, AUGUST 2017

-

Upload

euromonitor-international -

Category

Business

-

view

393 -

download

0

Transcript of Global FMCG: Finding Opportunities

GLOBAL FMCG: FINDING OPPORTUNITIES

PLMA ACCESSING EXPORT MARKETS CONFERENCE

REHAN PANDITARATNE, AUGUST 2017

© Euromonitor International

2

How do brands achieve success in global markets?

GLOBAL FMCG: FINDING OPPORTUNITIES

Grown 5% annually over last 5 years globally despite stagnant domestic Japanese market to reach US$5 billion sales.

Female Empowerment

Ageing

Ethical Consumerism

UrbanisationGrown China outlets from 250 to 2,500 over the last 10 years to reach over US$2 billion in sales.

8% annual global growth over the last 5 years to reach over US$200 million in sales.

Achieved US$1.8 billion absolute growth globally over the last 5 years.

Time Poor Consumption

Grew sales by 50% in Asia over the last 5 years to US$280 million.

INTRODUCTION: GLOBAL OVERVIEW

URBANISATION

TIME POOR CONSUMPTION

EMPOWERED WOMEN

ETHICAL AND GREEN CONSUMERISM

AGEING POPULATIONS

CONCLUSION

© Euromonitor International

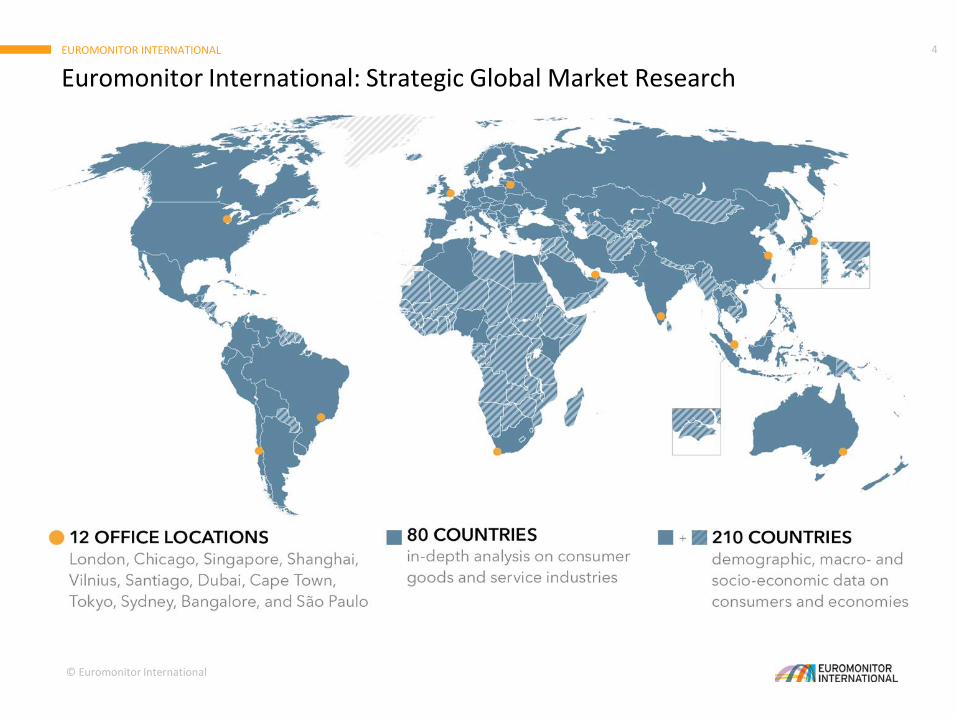

4EUROMONITOR INTERNATIONAL

Euromonitor International: Strategic Global Market Research

© Euromonitor International

5

Global packaged food by categoryINTRODUCTION: GLOBAL OVERVIEW

-1%

0%

1%

2%

3%

4%

5%

6%

7%

8%

0

50

100

150

200

250

300

350

400

450

Re

tail v

alu

e s

ale

s C

AG

R 2

01

1-2

01

6

Re

tail v

alu

e s

ale

s 2

01

6 (U

S$

billio

n)

Packaged Food: Size 2016 and Strength of Global Categories 2011-2016

Retail Value Sales 2016 Retail Value Sales % CAGR 2011-2016

© Euromonitor International

6

Dairy: Asia has surpassed North America and Western Europe in valueINTRODUCTION: GLOBAL OVERVIEW

© Euromonitor International

7

0%

50%

100%

2000 2005 2010 2015 2020 2025 2030

World GDP by Region: 2000-2030

Other Emerging and Developing Countries

Emerging and Developing Asia

Developed Countries0 60 120

Latin America

MENA

Sub-Saharan Africa

Emerging and Developing Asia

% growth

Real GDP Growth in Emerging Regions: 2015-2030

In 2030, this region will

account for 44% of global GDP,

up from just 18% in 2000.

Why Asia Pacific?INTRODUCTION: GLOBAL OVERVIEW

INTRODUCTION: GLOBAL OVERVIEW

URBANISATION

TIME POOR CONSUMPTION

EMPOWERED WOMEN

ETHICAL AND GREEN CONSUMERISM

AGEING POPULATIONS

CONCLUSION

© Euromonitor International

9

China’s urban population expanded by 37%.

China’s rapid urban growth has resulted in a rising number of megacities with populations above 10 million.

China: Nearly a billion people will live in urban areas by 2030URBANISATION

© Euromonitor International

10

Rise of single persons

Later parenting; shrinking families

Expanding middle class with rising

incomes

Better access to education

Better connectivity

High costs of housing; small living spaces

Pressure on infrastructure and

services

Less time for leisure and

physical activity

Pollution and related health

issues

Large gaps between ‘haves’ and ‘have nots’

Impacts of urbanisationURBANISATION

© Euromonitor International

11

Mega Trend: Changing Family Dynamics

The growth of products such as coffee machines, smoothie makers and snack foods is largely linked to people who live alone.

GOING SOLO

Existing Industry Examples• The rise of single-portion cakes and frozen desserts. • Growth in per capita consumption of ready meals, share of small and micro packaging

and more.

Going soloURBANISATION

© Euromonitor International

12

Demand for smaller pack sizes and re-sealable packs, which stand-up pouches are growing.

Much of the growth in stand up pouches will come from Asia Pacific.

0

500

1,000

1,500

2,000

2,500

3,000

3,500

0-50g 51-100g 101-300g

301-500g

501-750g

751-1,000g

Millio

n u

nits

Stand-Up Pouches in Sauces, Dressings and Condiments Packaging by Size Band 2010-

2015

2010 2015

Single-person households drive demand for smaller pack sizes and pouchesURBANISATION

INTRODUCTION: GLOBAL OVERVIEW

URBANISATION

TIME POOR CONSUMPTION

EMPOWERED WOMEN

ETHICAL AND GREEN CONSUMERISM

AGEING POPULATIONS

CONCLUSION

© Euromonitor International

14

Mega Trend: Time as Currency

Focus on convenient and flexible products and solutions that enable consumers to either save time through outsourcing of tasks or multi-task through more flexible packaging options.

OMNIPRESENT CONSUMPTION

Existing Industry Examples• The rise of snack replacements from all corners of the supermarket. The growing

availability of portable breakfast solutions. • A plethora of online food delivery options spanning scratch cooking options to ready-

to-eat services.• Per capita consumption of snack replacements and stand up pouches.

Omnipresent consumptionTIME POOR CONSUMPTION

© Euromonitor International

15

Breakfast Combo

Dual pots, especially those with disposable spoons, are fast

becoming popular with commuting

consumers.

Drinking Yoghurt

Now many yoghurt brands

are simply selling their products with straws to

allow consumption in

beverage-like fashion. Yoplait

variants in China are good examples

of this trend.

It’s All Greek

Positioning as a high protein snack is. From the US to Australia, Brazil to the UK, consumers are buying into the

thick yoghurt variant for satiety

purposes.

Dessertification

“Dessertification”, a trend best exhibited in

chocolate, which replicates restaurant

desserts, has proven to be a

valid alternative to mainstream

snacks.

Snacking yoghurts being used to meet a variety of purposesTIME POOR CONSUMPTION

- - -

© Euromonitor International

16

PepsiCo expands Quaker oats into biscuits, granola and snacksTIME POOR CONSUMPTION

On-the-go porridge

Ready-to-eat supergraincereals and granola

Savoury snacksBreakfast bars

and biscuits

INTRODUCTION: GLOBAL OVERVIEW

URBANISATION

TIME POOR CONSUMPTION

EMPOWERED WOMEN

ETHICAL AND GREEN CONSUMERISM

AGEING POPULATIONS

CONCLUSION

© Euromonitor International

18

05

101520253035404550

% c

onsta

nt

gro

wth

Selected Leading Growth Markets For Female Disposable Income Per Capita 2011/2016

Female empowermentEMPOWERED WOMEN

Female disposable incomes soared in China by 44% over the last 5 years

© Euromonitor International

19

What is driving the obsession with self-image? EMPOWERED WOMEN

The empowerment of women The “selfie culture”

Exposure to idealised images of beauty The power of the online influencer

© Euromonitor International

20

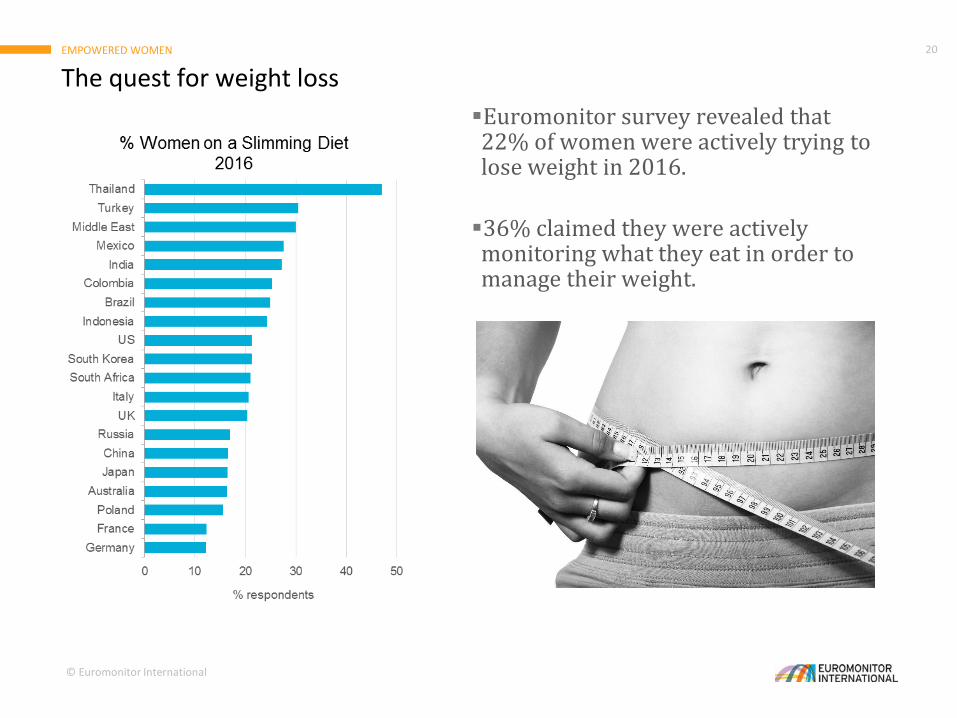

Euromonitor survey revealed that 22% of women were actively trying to lose weight in 2016.

36% claimed they were actively monitoring what they eat in order to manage their weight.

The quest for weight lossEMPOWERED WOMEN

© Euromonitor International

21

The global retail market for weight management was worth US15.9 billion in 2016.

Growth was driven by the two largest categories – meal replacement and weight loss supplements.

0

2,000

4,000

6,000

8,000

10,000

Meal Replacement Weight LossSupplements

Slimming Teas

US

D b

illio

n, c

on

sta

nt 2

01

6 rs

p

Global Sales of Weight Management 2011/2016/2021

2011 2016 2021

0 1,000 2,000 3,000 4,000 5,000 6,000

India

Mexico

Japan

China

US

USD billion

Top Five Markets for Weight Management 2016

Growth in weight managementEMPOWERED WOMEN

INTRODUCTION: GLOBAL OVERVIEW

URBANISATION

POOR CONSUMPTION

EMPOWERED WOMEN

ETHICAL AND GREEN CONSUMERISM

AGEING POPULATIONS

CONCLUSION

© Euromonitor International

23

Selling trustETHICAL AND GREEN CONSUMERISM

Mega Trend: Striving for Authenticity

Trend DescriptionIn a bid to stay safe and knowledgeable about what goes into their bodies, consumers have moved towards “authentic” products. Traceability and transparency are key components of this movement and the digital economy is enabling solutions for brands.

SELLING TRUST

Existing Industry Examples• Single-origin cocoa used by a growing number of premium chocolate brands. • Growing demand for manufacturers to move towards clean label ingredients. • Growing anti-GMO sentiment in the US. • The return of heritage ingredients and ancient grains.

© Euromonitor International

24

Clean labellingETHICAL AND GREEN CONSUMERISM

0

5

10

15

20

25

30

0

10

20

30

40

50

60

70

US

$ b

illi

on

RS

P

Top 10 clean label markets

2015 2015-2020 % Growth

© Euromonitor International

25

Case study on selling trust

ETHICAL AND GREEN CONSUMERISM

Hipp Combiotic, United KingdomSource: Ocado.com

As consumers become more price

conscious and increasingly mistrusting

brands, especially those from the largest

global food manufacturers, there is a shift

towards more “authentic”, niche and

natural products, with consumers seeking

brands that they see as upholding key

values.

© Euromonitor International

26

Scandals came thick and fast over 2013-2015 in China and Taiwan, shaking rebuilt but weak consumer confidence.

That said, international brands are unlikely to carry their superior status as a USP for much longer, as more and more international brands are flogging these markets.

Food scares increase demand, not just for foreign brands…ETHICAL AND GREEN CONSUMERISM

Australia’s Own Milk for Children in China, 2015

© Euromonitor International

27

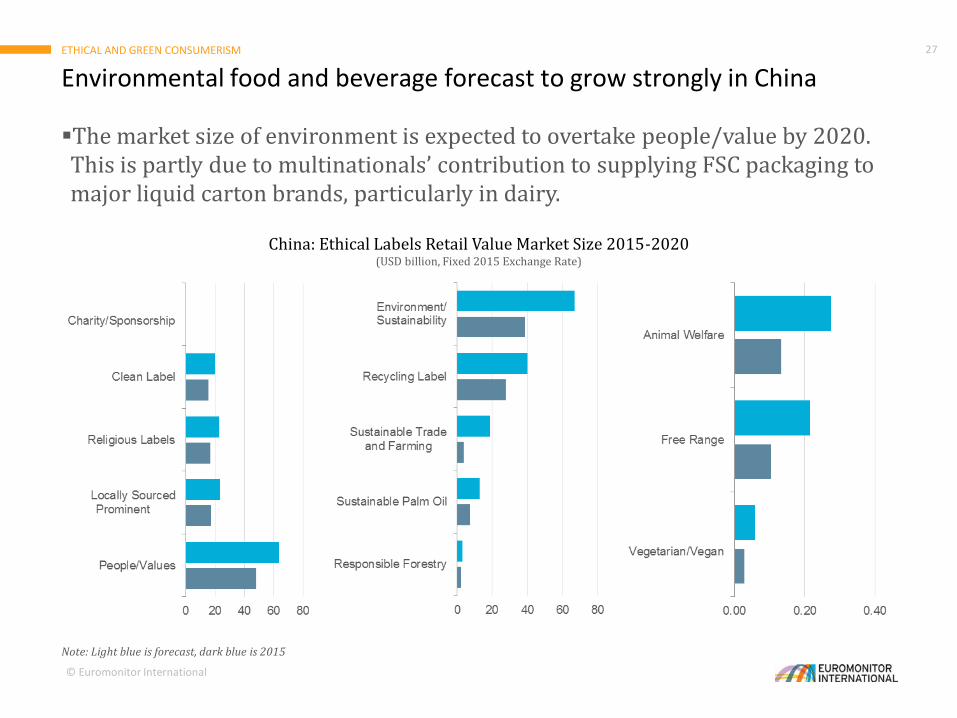

Environmental food and beverage forecast to grow strongly in China ETHICAL AND GREEN CONSUMERISM

China: Ethical Labels Retail Value Market Size 2015-2020 (USD billion, Fixed 2015 Exchange Rate)

Note: Light blue is forecast, dark blue is 2015

The market size of environment is expected to overtake people/value by 2020. This is partly due to multinationals’ contribution to supplying FSC packaging to major liquid carton brands, particularly in dairy.

© Euromonitor International

28

Consumers globally show a growing awareness of naturally derived ingredients, as well a desire that products are sustainably produced.

These concerns are more prevalent in emerging markets, especially in Asia, than in developed markets.

Asian consumers show highest preference for green beautyETHICAL AND GREEN CONSUMERISM

© Euromonitor International

29

Islam is the most popular religion in Asia, so it is unsurprising that the researched countries in the region contributed heavily to sales of packaged food and beverages with a halal claim.

Indonesia, for example, had US18 billion in value sales of products with a claim in 2015; a country where the Muslim population in the country stands at over 85%.

In order to succeed both in Asia and in regions where Muslim populations are growing, particularly Western Europe.

Halal certification in Asia PacificETHICAL AND GREEN CONSUMERISM

INTRODUCTION: GLOBAL OVERVIEW

URBANISATION

TIME POOR CONSUMPTION

EMPOWERED WOMEN

ETHICAL AND GREEN CONSUMERISM

AGEING POPULATIONS

CONCLUSION

© Euromonitor International

31

0 100 200 300

South Korea

Spain

Thailand

Mexico

UK

France

Italy

Germany

Indonesia

Brazil

Russia

Japan

US

India

China

Million

The Biggest 60+ Populations in 2020

The global population will continue to age, on the back of rising life expectancy, falling birth rates and the ageing baby boomers.

China and India will continue to have the largest over 60s populations, and will experience faster ageing than the global average.

The world will continue to age, especially in China and IndiaAGEING POPULATIONS

© Euromonitor International

32

Mental agility

Brain Health Supplements Learning new skills Volunteering Brain training

Health and wellbeing

Disease prevention through self-care and good nutrition

Keeping fit Monitoring weight Emotional wellbeing

Outward appearance

Use of anti-ageing beauty products and supplements

Cosmetic treatments Stylish clothing and accessories

How are consumers challenging ageing?AGEING POPULATIONS

© Euromonitor International

33

Older consumers are increasingly aware that they need to eat healthy and nutritious foods in order to help prevent chronic diseases.

Convenience foods, such as snacks, ready meals, soups and supplement nutrition drinks, are popular among this demographic.

In April 2016, Nestlé announced the opening of a new research and development centre in Singapore, for the creation of new products for ageing consumers in Asia Pacific and across the world.

0

50

100

150

200

250

300

Fortified/Functional Naturally Healthy

US

D b

illio

n, c

on

sta

nt 2

01

5 rs

p

Global Sales Of FF And NH Products 2010/2015

2010 2015

In China, probiotic yoghurt is a burgeoning niche.

In 2010 it was worth

US$2 billion. In 2021 sales of this product will be around US$15 billion.

Untapped potential for foods aimed at seniorsAGEING POPULATIONS

© Euromonitor International

34

Health supplements; natural and fortified foodsChronic diseases

Vitamin D; calcium supplementsLoss of bone denisty

OTC antacids; laxatives; high-fibre foodsDigestive problems

Lutein and other eye supplements; reading glassesEye problems

Hair loss products; colourants; specialist shampoosHair loss

Anti-ageing creams; beauty supplementsLines and wrinkles

Calming and sleeping aidsSleeping difficulties and anxiety

Urinary health supplements; incontinence productsIncontinence

Lethicin and other memory supplements; brain games Memory loss

Old age ailments and commercial opportunitiesAGEING POPULATIONS

© Euromonitor International

35

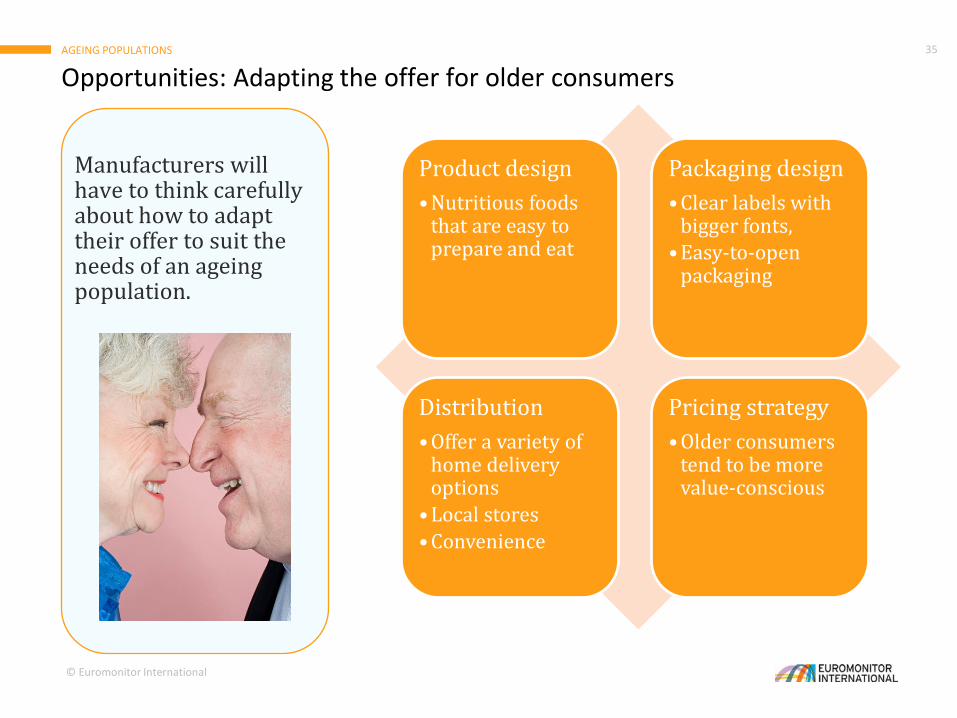

Product design

• Nutritious foods that are easy to prepare and eat

Packaging design

• Clear labels with bigger fonts,

• Easy-to-open packaging

Distribution

• Offer a variety of home delivery options

• Local stores

• Convenience

Pricing strategy

• Older consumers tend to be more value-conscious

Manufacturers will have to think carefully about how to adapt their offer to suit the needs of an ageing population.

Opportunities: Adapting the offer for older consumersAGEING POPULATIONS

INTRODUCTION: GLOBAL OVERVIEW

URBANISATION

WORKING WOMEN AND TIME POOR CONSUMPTION

ETHICAL AND GREEN CONSUMERISM

AGEING POPULATIONS

CONCLUSION

© Euromonitor International

37

Engage older consumers. They are the future.

Understand the evolving needs of female consumers.

Account for the unique ethical and green considerations, especially in Asia.

Leverage urbanisation trends.

Recommendations for FMCG companies exporting globallyCONCLUSION

Time poor consumption in your NPD and channel strategy.

THANK YOU FOR LISTENINGRehan Panditaratne

Consultant

+61 2 9581 9232

https://www.linkedin.com/in/rehanp/