Global Economic Outlook and Risks

22

Global Economic Outlook and Risks Is Growth Shifting from Emerging to Advanced Economies? Emilio Rossi [email protected] November 25 th , 2013

Transcript of Global Economic Outlook and Risks

Global Economic Outlook and Risks Is Growth Shifting from Emerging to Advanced Economies?

Emilio Rossi [email protected]

November 25th, 2013

World GDP Growth by Region

2

Assuming that America sorts out its fiscal problems…

…US interest rates are bound to rise over coming months and years.

For the US this would reflect a strengthening economy.

Elsewhere, however, it may be less welcome.

Unhappy response to some very mild US policy pronouncements earlier this year.

The Oxford Economics forecast builds in a gradual rise in US bond yields (to 4 per cent by end-2016), with no financial market shocks.

One Major Cloud Over the Horizon

U.S. INTEREST RATES

3

From the Strongest to the Weakest

The BRICs Is slowdown inevitable ?

The USA Will it surge again ?

Japan Some hope of growth ?

The Euro Zone (and the UK) Little hope of growth ?

4

BRICs - Overall risk fairly stable at 2013 levels

5

6 2010 2011 2012 2013 0

3

6

9

12

China

Brazil

Russia

India

BRIC’s Short-term Interest Rates

EM : Middle class still growing

7

EM - Labor costs remain low

8

(in per cent of GDP; 3 year moving average)

1990 1993 1996 1999 2002 2005 2008 2011 10

20

30

40

India

China

Brazil

Russia

BRIC: Gross Fixed Investment

9

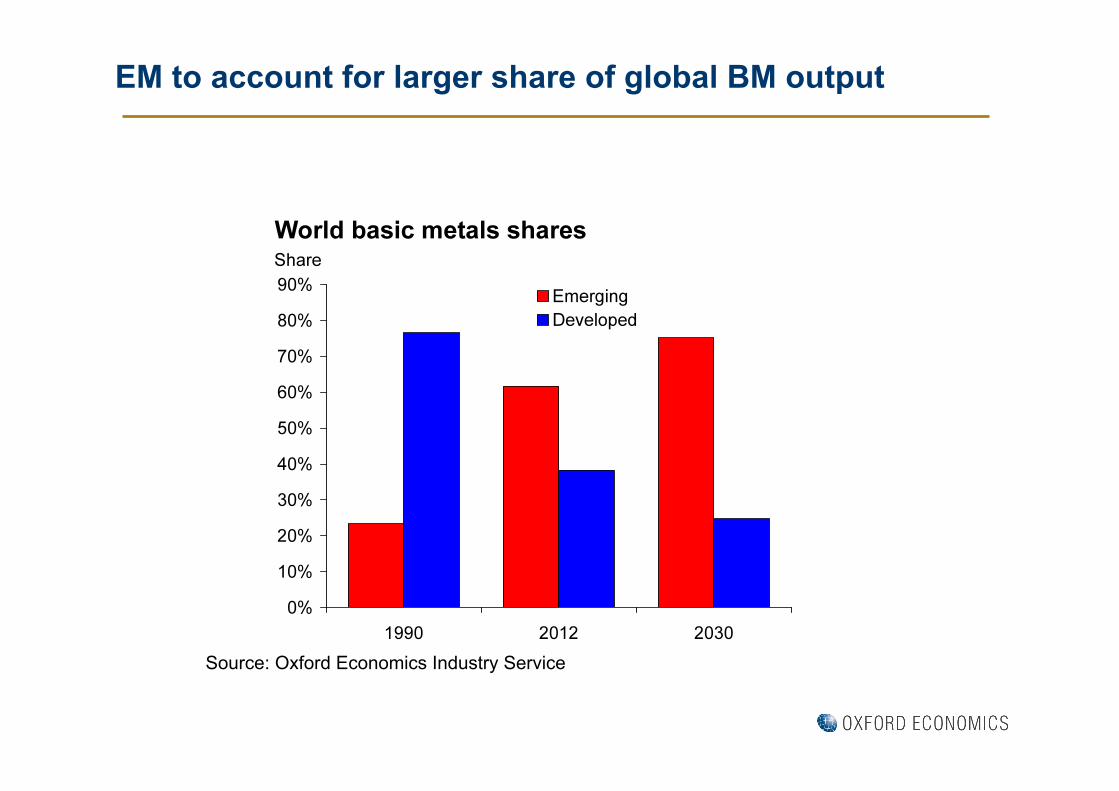

EM to account for larger share of global BM output

Source: Oxford Economics Industry Service

11

BRIC Competitiveness being eroded

From the Strongest to the Weakest

The BRICs Is slowdown inevitable ?

The USA Will it surge again ?

Japan Some hope of growth ?

The Euro Zone (and the UK) Little hope of growth ?

12

1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010 2012 50

70

90

Households

Corporate Sector*

* Non-financial corporations.

2000 2002 2004 2006 2008 2010 2012 90

100

110

120

130

140

150

160

170

* In real terms.

(2000 = 100)

US Debt/GDP Ratios US House Prices*

US construction activity strengthening

14

15

Source: BP

Shale boom helping US competitiveness

US manufacturing recovering nicely

16

From the Strongest to the Weakest

The BRICs Is slowdown inevitable ?

The USA Will it surge again ?

Japan Some hope of growth ?

The Euro Zone (and the UK) Little hope of growth ?

17

Japan’s New Economic Policy Main thrust (Three Arrows) double the monetary base in two years provide a large fiscal stimulus enact significant reforms

Main aims raise inflationary expectations restore economic growth raise equity prices lower the exchange rate

Main risks higher government bond yields (though the BoJ will buy

massive amounts of long-term bonds) raising the consumption tax in 2014

18

Monetary Base

(January 2007 = 100)

2007 2008 2009 2010 2011 2012 2013 2014

50

150

250

350

450

550

United States

UK

Euro Zone

Japan

19

Monetary Base

20

2007 2008 2009 2010 2011 2012 2013 2014

50

150

250

350

450

550

United States

Euro Zone

Japan

UK (January 2007 = 100)

21

Global Growth supports World Trade

From the Strongest to the Weakest

The BRICs Slowdown is inevitable but still high growth

The USA It will surge again if it sorts out its fiscal problems

Japan Some hope of (slow) growth but challenging experiment

The Euro Zone (and the UK)

Little hope of growth ? 22