Global Economic, Market and Insurance Outlook - iumi.com · ab Page 3 Overview A global growth...

28

ab Global Economic, Market and Insurance Outlook Kurt Karl IUMI 2008 Conference Vancouver, Canada Sept. 2008

Transcript of Global Economic, Market and Insurance Outlook - iumi.com · ab Page 3 Overview A global growth...

abGlobal Economic, Market and Insurance Outlook

Kurt Karl

IUMI

2008 Conference

Vancouver, Canada

Sept. 2008

ab

Page 2

Agenda

Global economic outlook

Outlook for major asset classes

Global P&C outlook

ab

Page 3

Overview

A global growth slowdown is underway, with US basically in a recession.

Inflation remains a problem for Central banks, so monetary easing will be cautious

Market volatility likely to continue. Spreads will remain wide. Equity markets weak at least until end-2008.

Despite impact on asset valuations, P&C market shows few signs of hardening.

ab

Page 4

What is a recession?

Common definition: Two quarters in a row of negative “real” GDP growth (real GDP = after-inflation Gross Domestic Product)

Growth in output of goods and services becomes negative (real income falls), unemployment rises, manufacturing down, sales down

Definition of recession

Expansionary Phase

Slowdown in economy

Recession is certain

Recovery is uncertain

Phases of the business cycle

We’re close to here, right now

Credit spreads become tighter & robust investment opportunities diminish.

Eventually, asset prices are too high, relative to the risk

Markets are volatile and the forecasts for recessions are mixed.

Most indicators imply that a recession is underway.

Market sentiment turns very pessimistic.

There are indications of an economic recovery, but these are inconclusive, so uncertainty is high.

Sources: Swiss Re Economic Research & Consulting

ab

Page 5

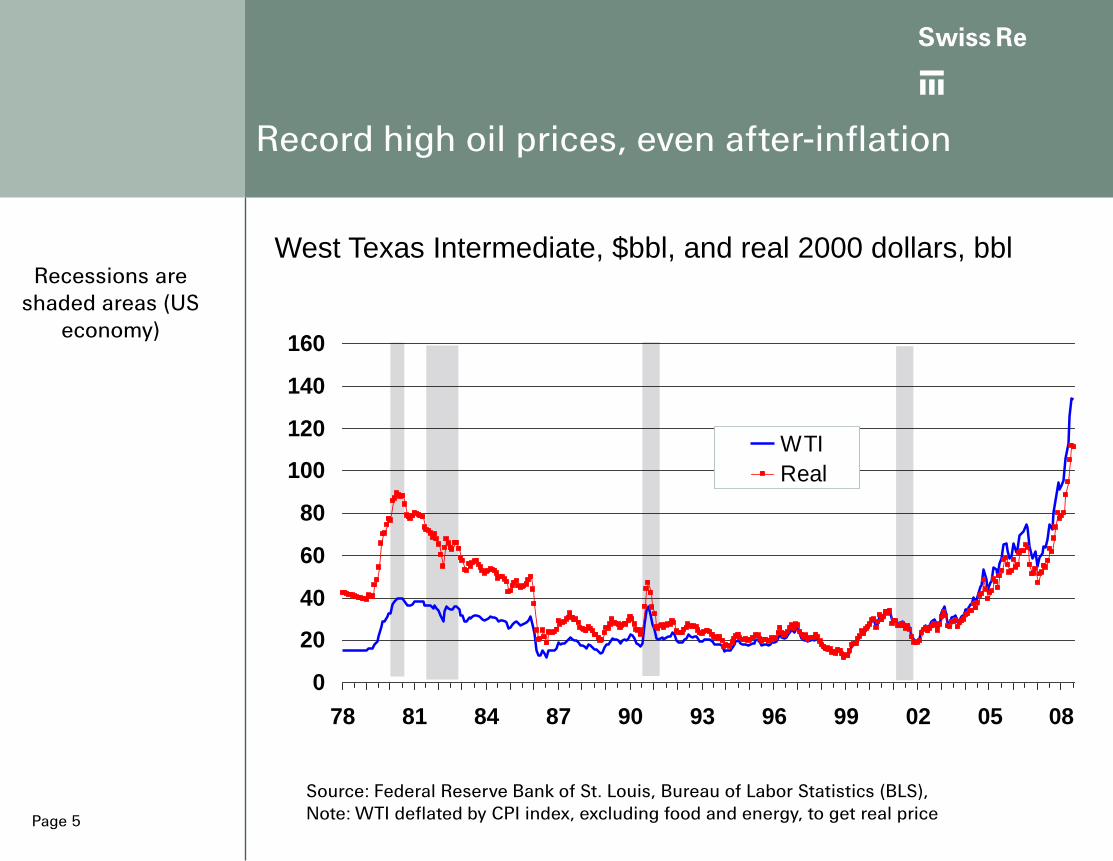

Source: Federal Reserve Bank of St. Louis, Bureau of Labor Statistics (BLS), Note: WTI deflated by CPI index, excluding food and energy, to get real price

West Texas Intermediate, $bbl, and real 2000 dollars, bbl

Record high oil prices, even after-inflation

0

20

40

60

80

100

120

140

160

78 81 84 87 90 93 96 99 02 05 08

WTI

Real

Recessions are shaded areas (US

economy)

ab

Page 6

Sources: World Bank, Swiss Re Economic Research & Consulting

World GDP Growth

0

1

2

3

4

5

6

7

8

61 65 69 73 77 81 85 89 93 97 01 05

GDP growth

Recessions are shaded areas

(Global economy)

Recessions

ab

Page 7

Global Marine Insurance:

Gross Premium Hull vs. World

Gross Tonnage: Uncorrelated

0

1

2

3

4

5

6

94 95 96 97 98 99 00 01 02 03 04 05 06e 07e

0

100

200

300

400

500

600

700

800

900

Gross premiums GT in m

World Hull PremiumIn USD bn

World Fleet Tonnage m

Source: Lloyd’s Register World Fleet Stats / IUMI / Cefor / Swiss Re estimate

ab

Page 8

Global Marine Insurance:

Gross Premium Cargo vs.

International Trade Volume

0

1

2

3

4

56

7

8

9

10

11

12

94 95 96 97 98 99 00 01 02 03 04 05 06 07e

0

2000

4000

6000

8000

10000

12000

14000

16000

Gross Premiums Int.Trade Volume

WorldwideCargo PremiumIn USD bn

WorldwideTrade Volume

in USD bn

Source: Aon Ren Rep / IUMI / Cefor / SR est./World Bank

ab

Page 9

The US-dollar has depreciated, but

appears to be stabilizing

Source: Bloomberg

USD nominal effective exchange rate

70

80

90

100

110

120

130

1995 1997 1999 2001 2003 2005 2007

ab

Page 10

Percent

Source: Bureau of Labor Statistics, NBER, SR Economic Research & Consulting

Inflation rises into a recession, then falls

Inflation is

year-over-year

rate

US All-items CPI and yield on 10-yrTreasury note, 1959 – 2008Q1

0

2

4

6

8

10

12

14

16

59 62 65 68 71 74 77 80 83 86 89 92 95 98 01 04 07

T-note CPI

ab

Page 11

0

1

2

3

4

59 62 65 68 71 74 77 80 83 86 89 92 95 98 01 04 07

Spread, %

Spread of Baa to 20-year T-bondPercent

Credit spreads rise into, then fall after

a recession

Source: Moody’s, Federal Reserve Board, NBER, SR Economic Research & Consulting

ab

Page 12

-30

-20

-10

0

10

20

30

40

50

59 62 65 68 71 74 77 80 83 86 89 92 95 98 01 04 07

Core CPI

Year-over-year

growth, %S&P 500 index

Stock markets tend to decline in

recessions

Source: Standard & Poor’s, NBER, SR Economic Research & Consulting

Stock markets tend to

recover before the end

of recessions. They do

not forecast

recessions

consistently.

ab

Page 13

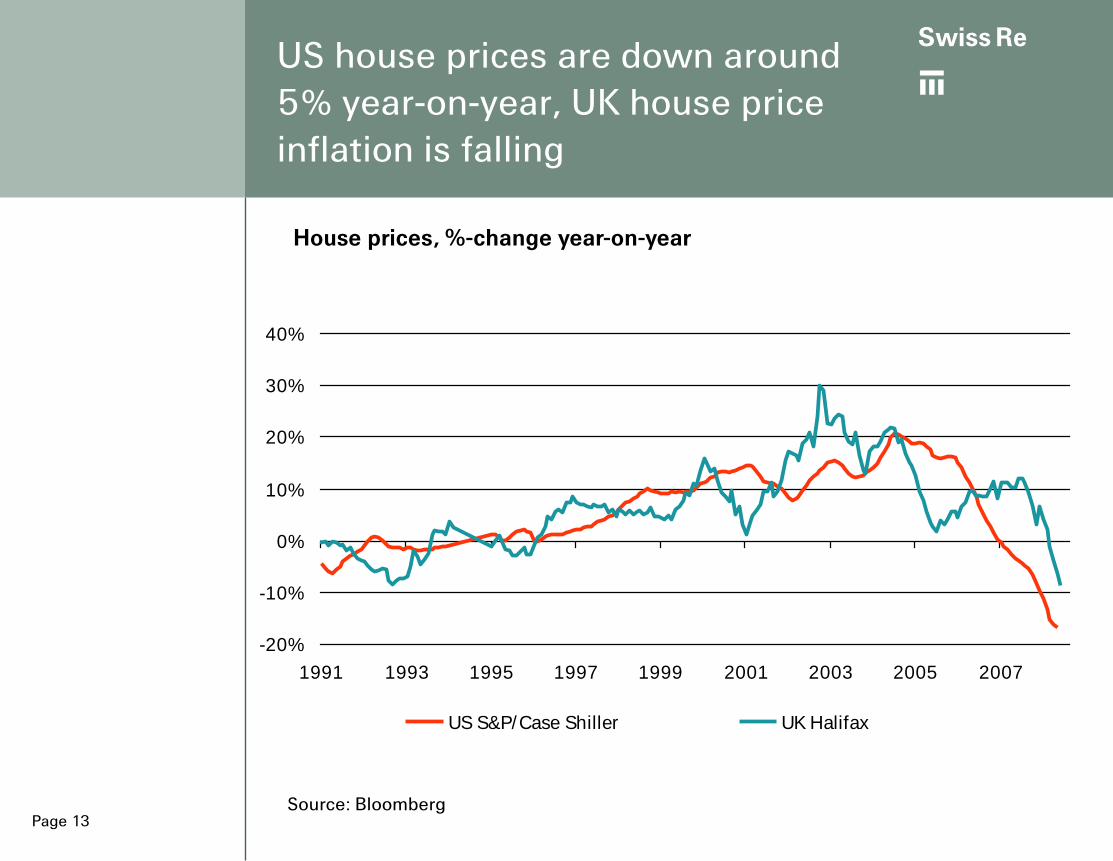

US house prices are down around

5% year-on-year, UK house price

inflation is falling

Source: Bloomberg

House prices, %-change year-on-year

-20%

-10%

0%

10%

20%

30%

40%

1991 1993 1995 1997 1999 2001 2003 2005 2007

US S&P/Case Shiller UK Halifax

ab

Page 14

% change year ago,3-month mov. avg.

Source: National Association of Realtors

-15

-10

-5

0

5

10

15

20

91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08

Home prices

Housing prices: signs of a floor?

Single-Family Existing homes sold, median price

ab

Page 15

0

2

4

6

8

10

12

14

16

18

70 73 76 79 82 85 88 91 94 97 00 03 06

UK US Japan Germany

Source: Reuters EcoWin

Long-term bond yields remain low

10-year government bond yields, percent

Government bonds

ab

Page 16

Corporate bond credit spreads

have surged

Source: Lehman Brothers

Corporate bond spreads (Investment grade, basis points, since 1989)

0

50

100

150

200

250

300

90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08

US Euroland

ab

Page 17

P/E Ratios remain relatively low

Source: Bloomberg

P/E Ratios

Equity marketvaluation

0

10

20

30

40

50

60

70

1990 1992 1994 1996 1998 2000 2002 2004 2006 2008

US S&P 500 EU FTSE Eurotop 100

ab

Page 18

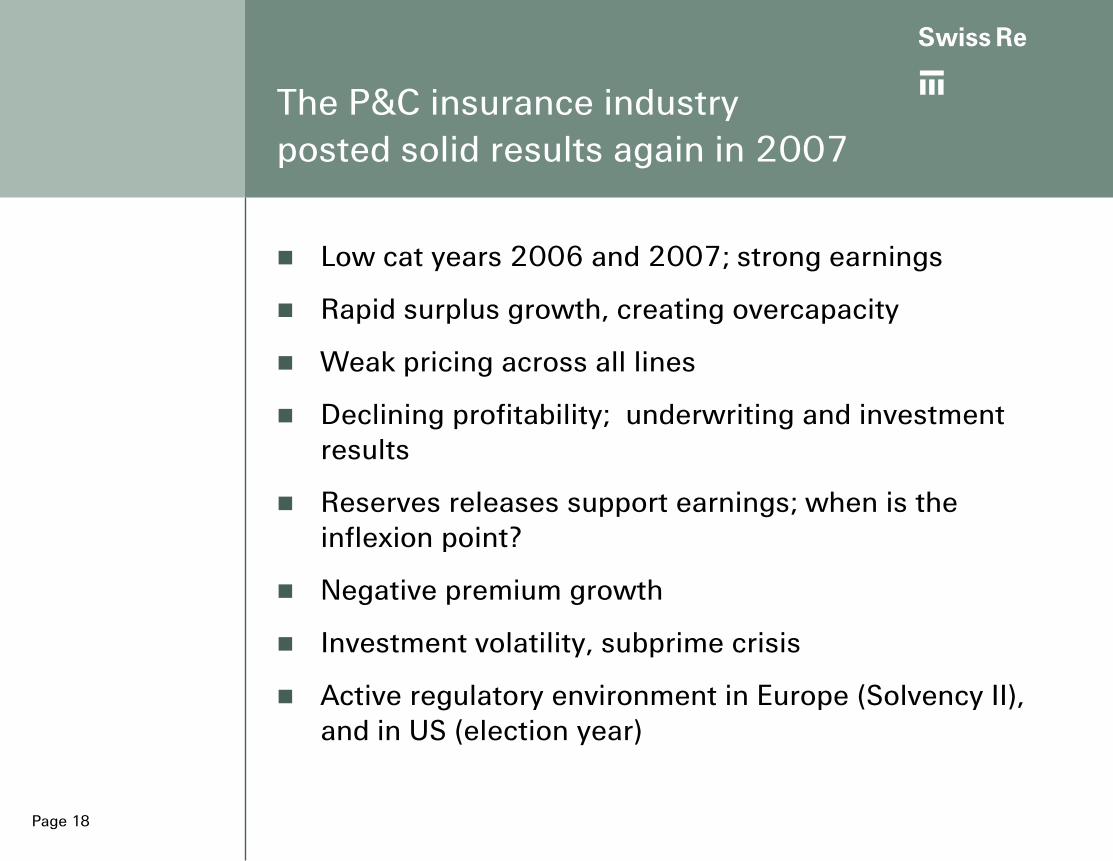

Low cat years 2006 and 2007; strong earnings

Rapid surplus growth, creating overcapacity

Weak pricing across all lines

Declining profitability; underwriting and investment results

Reserves releases support earnings; when is the inflexion point?

Negative premium growth

Investment volatility, subprime crisis

Active regulatory environment in Europe (Solvency II), and in US (election year)

The P&C insurance industry

posted solid results again in 2007

ab

Page 19

Property and business interruption losses(USD billion, at 2006 prices)

$0

$20

$40

$60

$80

$100

19

70

19

72

19

74

19

76

19

78

19

80

19

82

19

84

19

86

19

88

19

90

19

92

19

94

19

96

19

98

20

00

20

02

20

04

20

06

Weather-related Nat Cats Man-made disasters Earthquake/ tsunami

Cat losses were relatively low in

2007/06, but long-term trend is up

Note: NFIP flood losses in US included (since 1970). Source: Swiss Re, sigma No 1/2008

Katrina Rita Wilma (2005)

Ivan Charley Frances (2004)

Sept. 11

Andrew (1992) Lothar (1999)

US cat losses for first and second quarter 2008 are above average

ab

Page 20

2004 2005 2006

98% 98% 95%

4.2% 4.6% 4.1%

11% 11% 12%

Global P&C industry profitability

peaked in 2006

Combined ratio

Investment yield [2]

ROE

[1] Sample of major non-life insurance markets consists of Canada, Germany, France, UK, USA, and Japan [2] including realized capital gains,Sources: A.M. Best, forecasts by Swiss Re Economic Research & Consulting

2007E

97%

3.7%

10%

Key performance indicators for major non-life insurance markets[1]

ab

Page 21

US price trends are down and have

converged between businesses, similar

globally

-20%

-15%

-10%

-5%

0%

5%

10%

15%

3Q05 1Q06 3Q06 1Q07 3Q07 1Q08

Manufacturing Contracting

Service Habitational

Public Entity Transportation

Energy

-20%

-15%

-10%

-5%

0%

3Q05 1Q06 3Q06 1Q07 3Q07 1Q08

Small Medium

Large Jumbo

Source: MarketScout, Economic Research & Consulting

Commercial rate trendsby industry group

Commercial rate trendsby client size

ab

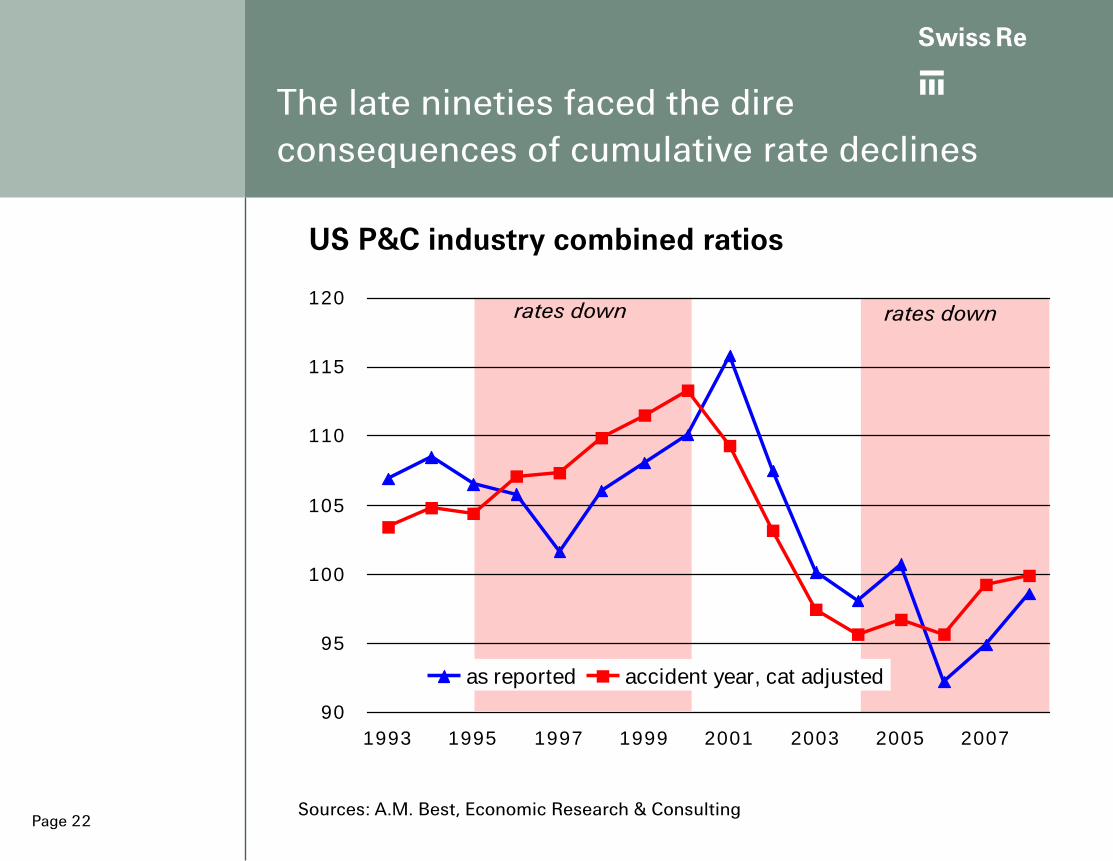

Page 22

90

95

100

105

110

115

120

1993 1995 1997 1999 2001 2003 2005 2007

as reported accident year, cat adjusted

The late nineties faced the dire

consequences of cumulative rate declines

Sources: A.M. Best, Economic Research & Consulting

US P&C industry combined ratios

rates down rates down

ab

Page 23

Effects of the credit crisis on

insurers

Effects on insurance companies as investors

– Subprime exposure, but this is manageable

– Equity market volatility, spreads widen

– Government bond yields remain low

Effects on insurance companies as providers of insurance coverage

– D&O/E&O insurance policies

– Mortgage guaranty / Monoline financial guarantors

Insurers face higher costs of capital

– Prices for equity and hybrid capital have declined

– Credit spreads widened

– Leveraged capital is withdrawing from the insurance space

ab

Page 24

Inflation risks and insurers

Inflation rising globally

Risk

Oil, food and commodity prices rising

Steel prices up 200% since 2001

Weak USD boosts inflation in US and EMs with dollar-pegs

Expectation: Inflation will moderate with global growth

Insurers long-tail lines could fare well under this scenario

Risk: Severe recession scenario: elevated inflation, substantially higher short term rates (even Fed needs to raise rates), higher long-term rates and substantially lower stock markets and more defaults

Insurers’ long-tail lines – not so well!

Insurers’ assets – not so well either!

Risk: Severe recession from worsening credit crisis

ab

Page 25

Industry trends require

maintaining underwriting discipline

Slow growth environment ahead

Rates will be falling through 2008-09 resulting in deteriorating accident year loss ratios

Frequency and severity of weather catastrophes will likely increase, compared to 2006 and 2007

Favorable loss reserve contributions from prior years will shrink

High volatity, low expected investment returns in all asset classes in the medium-term

M&A can be expected to continue and possibly accelerate in 2008-09

Disciplined underwriting, protecting earnings, and capital management are crucial, particularly with the low investment yields

ab

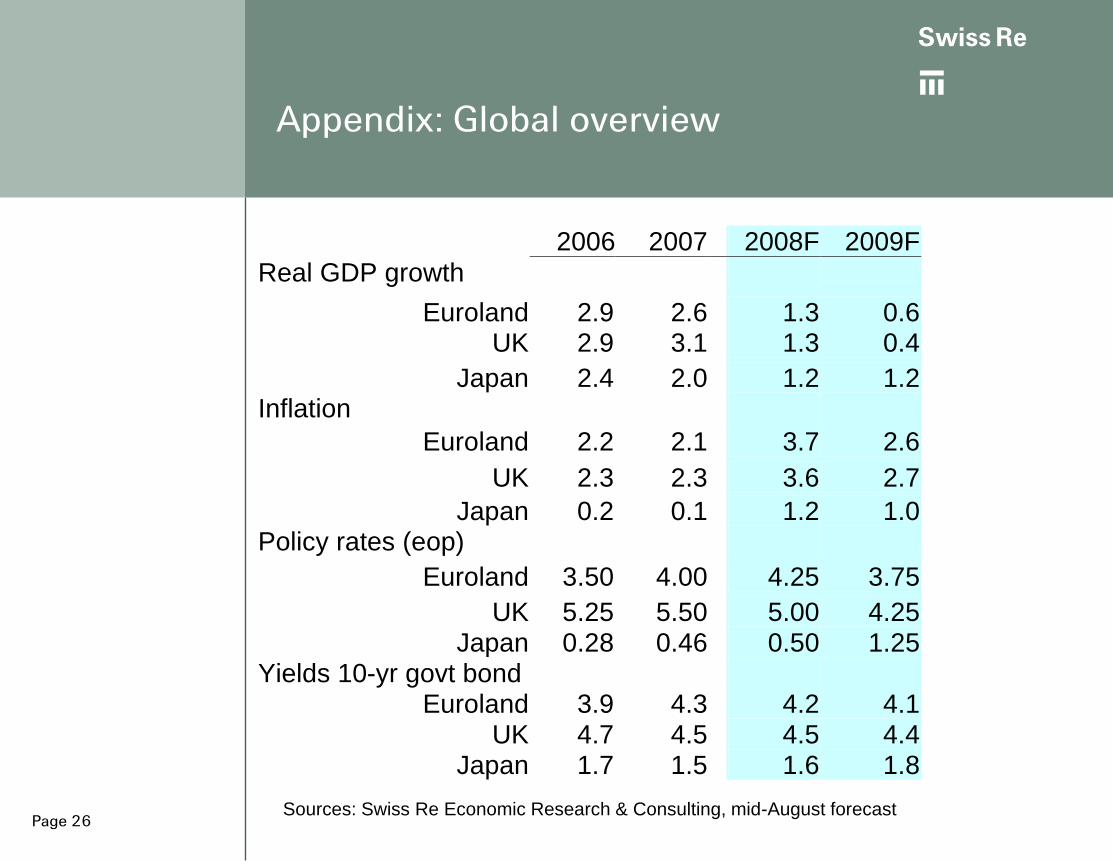

Page 26

2006 2007 2008F 2009F

Real GDP growth

Euroland 2.9 2.6 1.3 0.6 UK 2.9 3.1 1.3 0.4

Japan 2.4 2.0 1.2 1.2 Inflation

Euroland 2.2 2.1 3.7 2.6

UK 2.3 2.3 3.6 2.7

Japan 0.2 0.1 1.2 1.0 Policy rates (eop)

Euroland 3.50 4.00 4.25 3.75

UK 5.25 5.50 5.00 4.25 Japan 0.28 0.46 0.50 1.25

Yields 10-yr govt bond Euroland 3.9 4.3 4.2 4.1

UK 4.7 4.5 4.5 4.4 Japan 1.7 1.5 1.6 1.8

Sources: Swiss Re Economic Research & Consulting, mid-August forecast

Appendix: Global overview

ab

Page 27

2005 2006 2007 2008F 2009F

Annual Averages:

Real GDP 3.1 2.9 2.2 1.3 1.0 CPI 3.4 3.2 2.9 4.7 2.4

End-of-Period:

Fed Funds 4.25 5.25 4.25 2.00 3.5

10-yr T-note 4.4 4.7 4.0 3.8 4.2

Appendix: U.S. economic outlook

Sources: Federal Reserve Board, Swiss Re Economic Research & Consulting

ab

Page 28

Questions?

To be put on the e-mail distribution list for Swiss Re’s US Economic Outlook, or other country outlooks contact:

This presentation, prepared by Swiss Re’s Economic Research & Consulting, is for information purposes only. It is not intended as an offer or solicitation for the

purchase or sale of any financial instrument. The information contained in this document has been obtained from sources believed to be reliable; however, its

accuracy and completeness cannot be guaranteed. The views reflected herein are subject to change without notice. They are the views of Swiss Re Economic

Research & Consulting and may differ from Swiss Re Asset Management and Conning Asset Management.