Global Communications GAAP Summit 2013 - PwC · Global Communications GAAP Summit 2013 Sheraton...

117

Global Communications GAAP Summit 2013 Sheraton Golf, Rome 17-18 June

Transcript of Global Communications GAAP Summit 2013 - PwC · Global Communications GAAP Summit 2013 Sheraton...

Global Communications GAAP Summit 2013

Sheraton Golf, Rome 17-18 June

PwC

Introduction Pierre-Alain Sur Fi Dolan

Global Communications GAAP Summit

Slide 2

June 2013

PwC

Communication has a rich history…

Slide 3 Global Communications GAAP Summit June 2013

Source: PwC research

Tin Cans

Telegraph

1838

1876

Telephone

Invented by Alexander Graham Bell

1892

Long Distance

First call from Boston to NYC

1896

Radio

1927

Television

1964

Fiber optic

1971

1979

Mobile

1983

Internet

www

1993

Messaging

1998

VOIP

1999

Pager

2007

iPhone

Wireline Era Wireless Era

Android

Start of smartphone mass market

? Future

1810

2G/ GSM (Finland - 1991)

3G (Japan - 2001)

4G/WiMaX (2008)

4G/LTE (2010)

Wireless network technologies

Beyond

PwC

Future points towards a more connected world…

Slide 4

Global Communications GAAP Summit June 2013

Source: PwC research

ommunication Multiple Forms. Numerous devices. Same Experience

Unified communication

Integrated real-time communication

Social Networking & blogging

Will help OTT providers to increase their market. Mobile data and Wi-Fi will make a strong case for OTTs

Internet of Things Connected everything

Video Conferencing & Telepresence

Getting even closer to the virtual world

Device-to-Device Improved user experience and resource utilisation in cellular networks (both licenced and unlicenced) using technologies like Bluetooth, Ethernet, or Wi-Fi

Augmented Reality

Viewing the world through technology overlay

PwC

Top Global Communication Trends

Slide 5

Global Communications GAAP Summit June 2013

Communication Industry Top Trends

1) Smart connected devices to drive mobility trends

2) Mobility demand leading to data explosion

3) Despite new spectrum allocations, spectrum shortage may deepen

4) 4G/ LTE to catch up in emerging markets too

5) Increasing Profitability and Monetisation challenges for operators

6) Content becomes the king

7) M2M communication will grow led by China

8) M-commerce adoption will speed up further

PwC

Smart connected devices to drive mobility trends 1 Despite being in use for more than a decade, smartphones continue to experience robust growth. Tablets are now the next growth wave for devices.

Emerging markets will drive the demand for connected devices

2 Mobility demand leading to data explosion

Asia-pacific and North America will account for two third of global mobile data traffic by 2017. APAC and MEA regions will witness the highest growth.

3 Despite new spectrum allocations, spectrum shortage may deepen

HSPA/HSPA+ and LTE are highly spectral efficient (LTE efficiency = 3-5 times HSDPA), but the wireless data demand has outpaced this efficiency.

Given the finite availability of spectrum, operators are using additional technologies to optimise their mobile resources

Slide 6

Global Communications GAAP Summit June 2013

PwC Slide 7 PwC

Global Communications GAAP Summit June 2013

4G/ LTE to catch up in emerging markets too 4 LTE enabled handsets, demand for better speed, and data traffic growth will trigger LTE deployments across geographies, particularly in emerging markets.

5 Increasing Profitability and Monetisation challenges for operators

Operators today are struggling to enhance their revenue and profitability. While the data usage is skyrocketing, it is failing to generate equivalent dollars.

As the growth slows down, operators, particularly in mature markets are looking to end unlimited data plans and cut handset subsidies

6 Content becomes the king

Growing demand for apps, location-based services, social networks, and videos have made producers of content – app developers, OS vendors, and OTT providers the king of communication value chain. Operators too are shifting their focus from coverage to the content.

PwC Slide 8 PwC

Global Communications GAAP Summit June 2013

M2M communication will grow led by China 7 Growing demand for mhealth solutions, connected automotives, smarter homes/ cities, and mEducation are primarily driving the M2M market.

Deployment of M2M applications can have transformative effect on economies, particularly underdeveloped and developing economies.

8 eCommerce adoption will speed up further

With the world shrinking fast to adjust to the size of smartphones, customers are increasingly using mobile apps for show rooming, shopping, and payments.

PwC

Agenda

Tuesday 18 June

Time Session

08.00 – 08.15 Introduction

08.15 – 09.00 What’s new in accounting?

09.00 – 09.30 Telecom Italia: Market update

09.30 – 10.00 Coffee break

10.00 – 11.15 Workshop 1: The new revenue standard

11.15 – 12.00 Deutsche Telekom: Implementation project, revenue recognition

12.00 – 12.30 Spending wisely - does the market understand the Telco growth story?

12.30 – 13.45 Lunch

13.45 - 15.15 Workshop 2: To buy or to lease?

15.15 – 15.45 Coffee break

15.45 - 16.00 Closing remarks

Today

Global Communications GAAP Summit

Slide 9

June 2013

PwC

Question time In which region are you based?

1) Africa

2) Americas

3) Europe

4) Middle East

5) Asia Pacific

Global Communications GAAP Summit

Slide 10

June 2013

PwC

Question time

The abbreviation SPQR can be found on many Roman statues, buildings, and military standards. What does it stand for?

1) The glory of Rome

2) The senate and people of Rome

3) Made in Italy

4) The property of the city of Rome

Global Communications GAAP Summit

Slide 11

June 2013

June 2013

PwC

Question time

Who were the 2013 champions of Series A football league?

1) Juventus

2) Napoli

3) AC Milan

4) Fiorentina

Global Communications GAAP Summit

Slide 12

June 2013

PwC

What’s new in accounting? Peter Hogarth

Global Communications GAAP Summit

Slide 13

June 2013

Agenda

What’s new in 2013?

The future – The IASB’s agenda

Leases exposure draft

Final thoughts

PwC

What’s new in 2013?

This year ...

Quite a lot!

Global Communications GAAP Summit

Slide 15

June 2013

PwC

What’s new in 2013

Global Communications GAAP Summit

Slide 16

IFRS 10, ‘Consolidated

financial statements

IAS 27, ‘Separate financial

statements

IAS 19, ‘Employee benefits’

IFRS 12, ‘Disclosure of

interests in other entities’

IFRS 13, ‘Fair value

measurement’

IFRS 11, ‘Joint arrangements’

IAS 28, ‘Associates

and JVs’

for EU companies

June 2013

PwC

IFRS 11 Joint Arrangements

• Greater emphasis on contractual rights and obligations:

- Right to share in net assets joint venture

- Right to share in individual assets and liabilities of the joint arrangement joint operation

Global Communications GAAP Summit

Jointly controlled assets

Jointly controlled operations

Jointly controlled entities

Joint operations

Joint ventures

IAS 31 IFRS 11

IFRS 11, ‘Joint arrangements’

Slide 17

June 2013

PwC

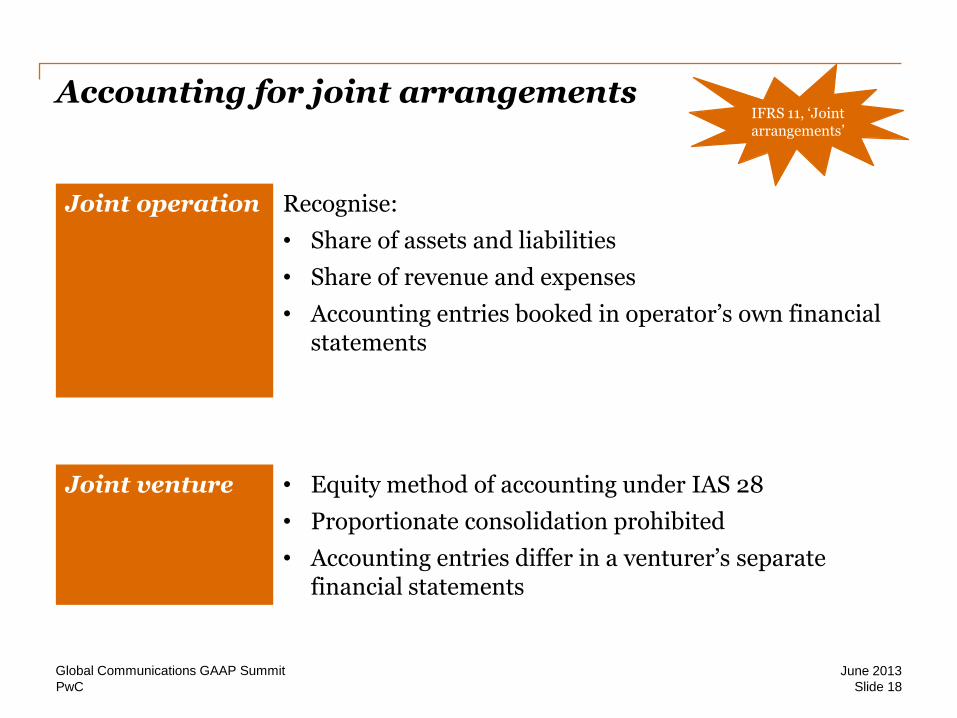

Accounting for joint arrangements

Global Communications GAAP Summit

Joint operation Recognise:

• Share of assets and liabilities

• Share of revenue and expenses

• Accounting entries booked in operator’s own financial statements

Joint venture • Equity method of accounting under IAS 28

• Proportionate consolidation prohibited

• Accounting entries differ in a venturer’s separate financial statements

IFRS 11, ‘Joint arrangements’

Slide 18

June 2013

PwC

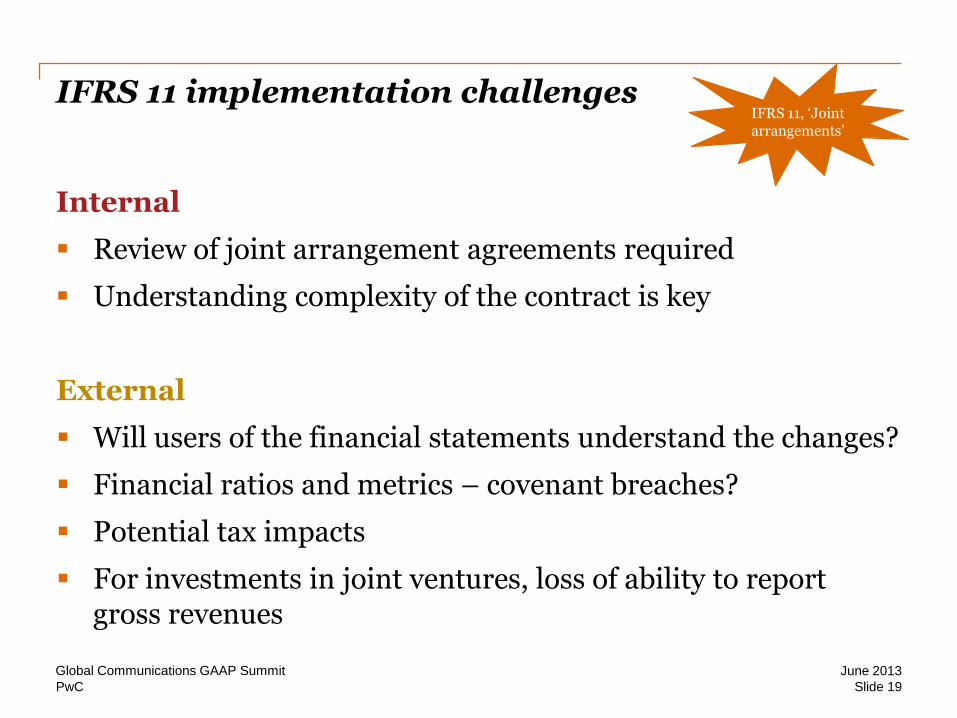

IFRS 11 implementation challenges

Internal

Review of joint arrangement agreements required

Understanding complexity of the contract is key

External

Will users of the financial statements understand the changes?

Financial ratios and metrics – covenant breaches?

Potential tax impacts

For investments in joint ventures, loss of ability to report gross revenues

Global Communications GAAP Summit

IFRS 11, ‘Joint arrangements’

Slide 19

June 2013

PwC

Impact of adopting IFRS 11 – Vodafone Group plc

Global Communications GAAP Summit

Slide 20

Previously

reported

£m

Change

£m

Restated

for IFRS 11

£m

Revenue 46,417 (7,596) 38,821

EBITDA 14,475 (2,856) 11,619

Adjusted operating profit 11,532 (689) 10,843

Profit for the financial year 7,003 - 7,003

Adjusted EPS 14.91p - 14.91p

Free cash flow 6,105 (391) 5,714

Net debt (24,425) 1,424 (23,001)

• Impact on revenue, EBITDA and free cash flow

• Free cash flow impacted such that the Group’s share of the joint venture’s free cash flow previously reported is different to the Group’s share of dividends paid

• It does not impact the Group’s existing rights and obligations in relation to the cash flows of, and dividends from, those joint ventures

• The reduction in net debt primarily results from the deconsolidation of debt raised locally by the joint ventures.

June 2013

PwC

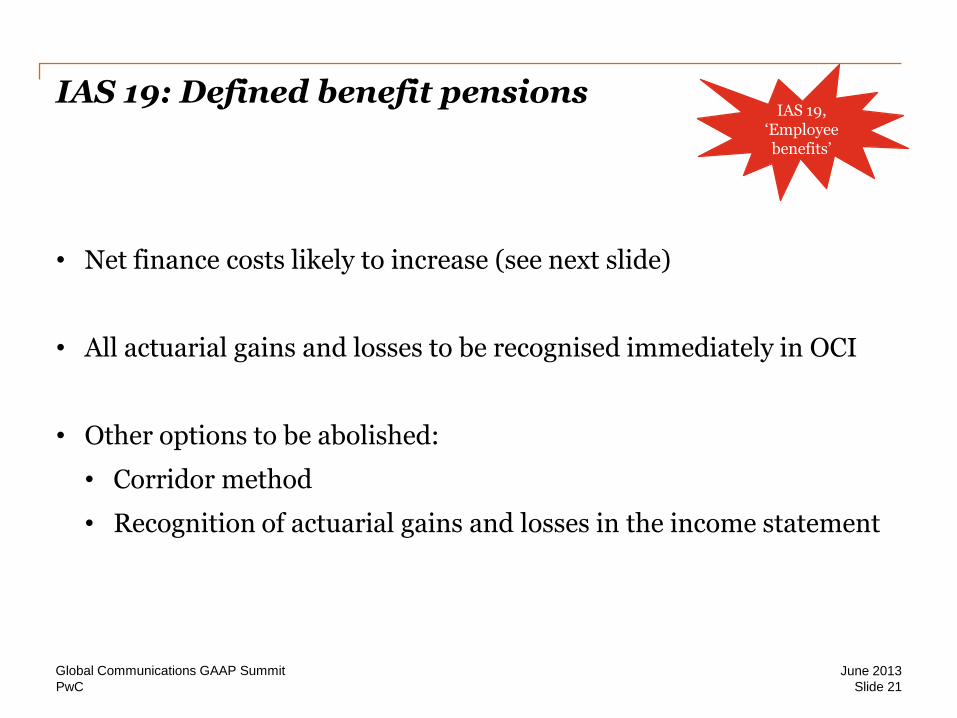

IAS 19: Defined benefit pensions

• Net finance costs likely to increase (see next slide)

• All actuarial gains and losses to be recognised immediately in OCI

• Other options to be abolished:

• Corridor method

• Recognition of actuarial gains and losses in the income statement

Global Communications GAAP Summit

IAS 19, ‘Employee benefits’

Slide 21

June 2013

PwC

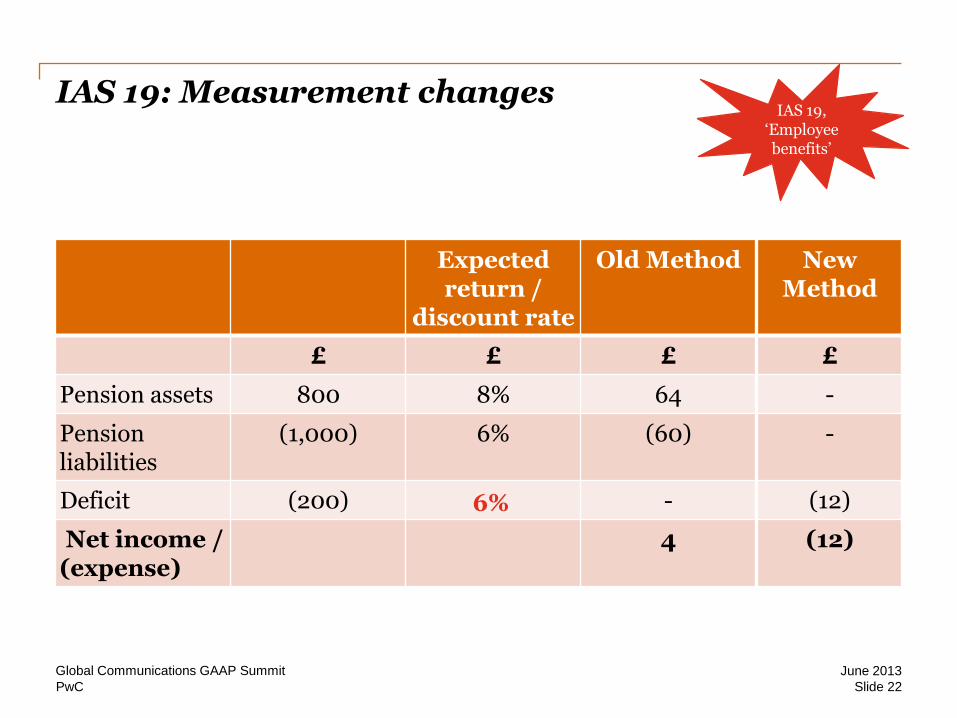

IAS 19: Measurement changes

Global Communications GAAP Summit

Expected return /

discount rate

Old Method

£ £ £

Pension assets 800 8% 64

Pension liabilities

(1,000) 6% (60)

Deficit (200) -

Net income / (expense)

4

New Method

£

-

-

(12)

(12)

6%

Slide 22

IAS 19, ‘Employee benefits’

June 2013

PwC

Other amendments to standards

Global Communications GAAP Summit

Standard Nature of amendment

IAS 1, ‘Presentation of financial statements’

Presentation of Other Comprehensive Income (1 Jul 2012)

IFRS 7, ‘Financial instruments: Disclosures

Offsetting

IAS 12, ‘Income taxes’ Deferred tax accounting for investment property (2012, but 2013 in EU)

IFRS 1, ‘First-time adoption’ Various

Annual improvements Various

Slide 23

June 2013

PwC

New presentation of OCI: Amcor Limited

Global Communications GAAP Summit

Slide 24

June 2013

PwC

Question time

Do you think the various changes to reporting in 2013 will have an impact on your company’s results and/or financial position?

1) Yes, these changes will have a significant impact

2) Yes, but not significant

3) No

4) Don’t know

Global Communications GAAP Summit

Slide 25

June 2013

PwC

What is the Interpretations Committee up to?

• IFRIC 20, ‘Stripping costs’

• IFRIC 21, ‘Levies’

• Project on contingent payments for assets (eg licences) on hold

Global Communications GAAP Summit

Slide 26

“Magyar Telekom Q1 net plummets on new government measures in Hungary”

(source: Reuters, 8 May 2013)

June 2013

PwC

A useful publication!

Global Communications GAAP Summit

Copies available on

your memory

stick

Slide 27

June 2013

The future – the IASB’s agenda

PwC

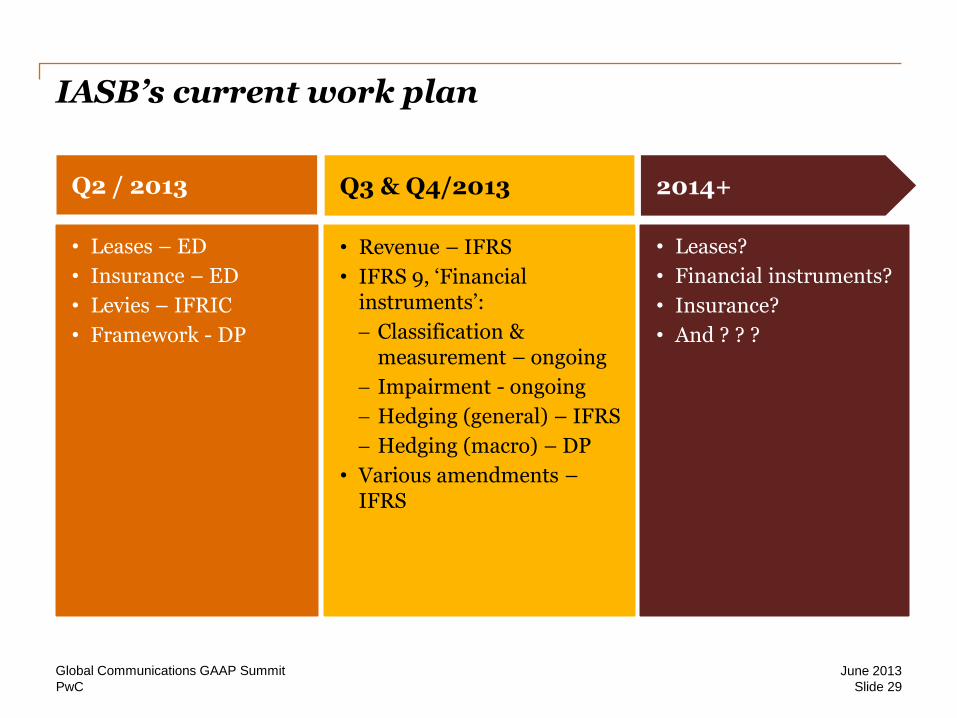

IASB’s current work plan

Global Communications GAAP Summit

• Revenue – IFRS

• IFRS 9, ‘Financial instruments’:

Classification & measurement – ongoing

Impairment - ongoing

Hedging (general) – IFRS

Hedging (macro) – DP

• Various amendments – IFRS

Q3 & Q4/2013

• Leases – ED

• Insurance – ED

• Levies – IFRIC

• Framework - DP

Q2 / 2013

• Leases?

• Financial instruments?

• Insurance?

• And ? ? ?

2014+

Slide 29

June 2013

PwC

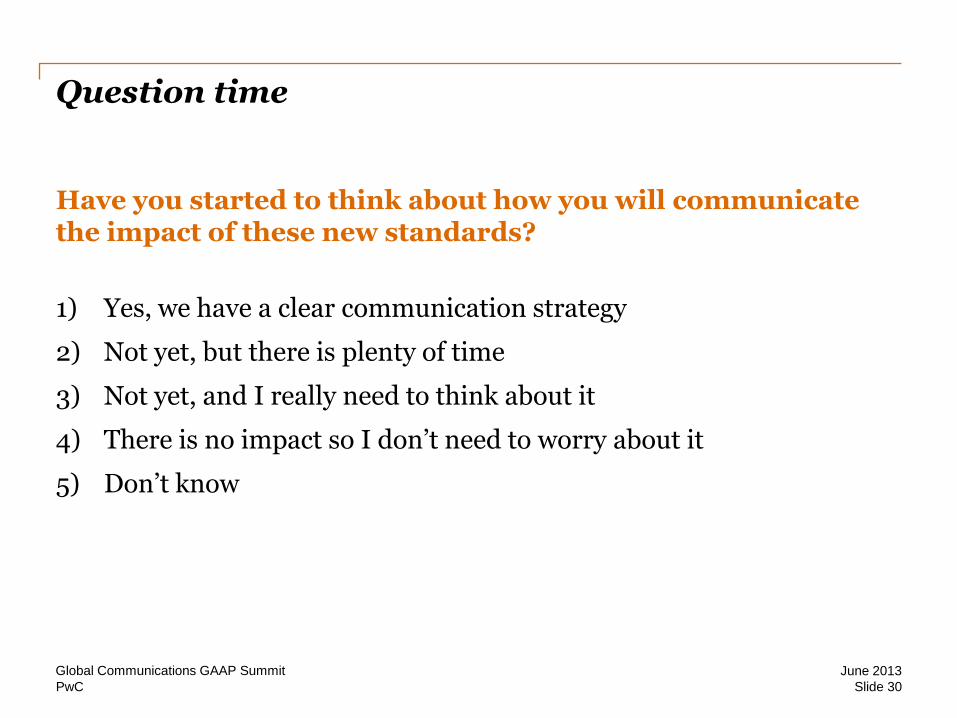

Question time

Have you started to think about how you will communicate the impact of these new standards?

1) Yes, we have a clear communication strategy

2) Not yet, but there is plenty of time

3) Not yet, and I really need to think about it

4) There is no impact so I don’t need to worry about it

5) Don’t know

Global Communications GAAP Summit

Slide 30

June 2013

PwC

The future agenda

• IASB consulted on its agenda in late 2011

• Key points were:

- Complete conceptual framework

- Develop a presentation and disclosure framework

- Focus on post-implementation reviews and responding to implementation issues

- Limit the number of new standards

• IFRS/US GAAP convergence – is it still an objective?

Global Communications GAAP Summit

Slide 31

June 2013

Leases exposure draft

PwC

What’s going on with leases?

Global Communications GAAP Summit

Exposure

Draft issued

Effective

date?

Comment

period ended

Re-deliberations

begin

Re-exposure

Aug 2010

Dec 2010

May 2013

2017?

Jan 2011

Q3 2014?

Final

Standard?

• Exposure draft issued 16 May 2013

• Comments by 13 September 2013

Slide 33

June 2013

PwC

The one constant: All leases ‘on-balance sheet’

All leases on lessee balance sheets, except:

• Short-term leases (<12 months)

• Materiality threshold

• Not leases!

Global Communications GAAP Summit

Slide 34

June 2013

PwC

Five key re-deliberation issues

Global Communications GAAP Summit

Definition of a lease (distinguishing a lease from a service)

Lease term

Variable lease payments

Lessor accounting

Lessee: Expense recognition

Slide 35

June 2013

PwC

Five key re-deliberation issues

Global Communications GAAP Summit

Definition of a lease (distinguishing a lease from a service)

Where are we today? Where might we be?

A lease conveys the right to use a specific asset for a period of time.

Right to use

• right to operate asset; or

• right to control access to asset; or

• take most of output and price neither fixed nor market.

A lease conveys the right to control the use of a specific asset for a period of time.

Right to control use

• direct use of asset; and

• obtain benefits from that use.

So far so good?

Slide 36

June 2013

PwC

Five key re-deliberation issues

Global Communications GAAP Summit

Lease term

Where are we today? Where might we be?

Contractual minimum plus extension periods where ‘reasonably certain’

Contractual minimum plus extension periods where there is a ‘significant economic incentive’.

Is it so different?

Slide 37

June 2013

PwC

Five key re-deliberation issues

Global Communications GAAP Summit

Variable lease payments

Where are we today? Where might we be?

Excluded from minimum lease payments for measurement purposes

Excluded from minimum lease payments for measurement purposes unless vary with rate/index or ‘in-substance fixed’

Is it so different?

Slide 38

June 2013

PwC

Five key re-deliberation issues

Global Communications GAAP Summit

Lessor accounting

Where are we today? Where might we be?

Finance leases

Up-front income plus interest on net investment

Operating leases

Income over term of lease

Some leases

Up-front income plus interest on receivable and residual

Some other leases

Income over term of lease

Is it so different?

Slide 39

June 2013

PwC

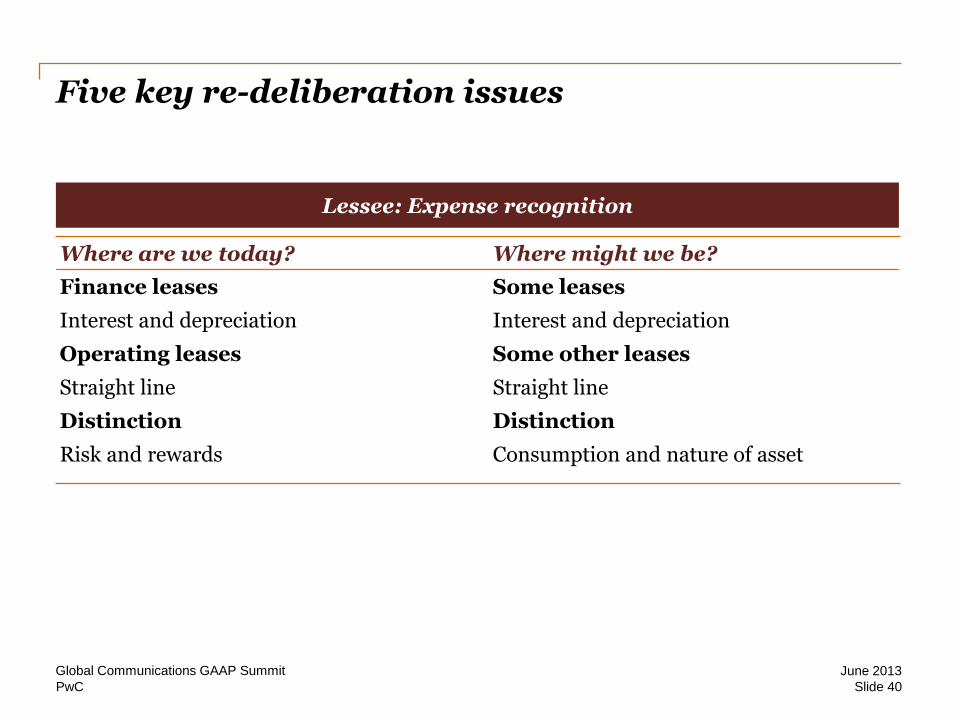

Five key re-deliberation issues

Global Communications GAAP Summit

Lessee: Expense recognition

Where are we today? Where might we be?

Finance leases

Interest and depreciation

Operating leases

Straight line

Distinction

Risk and rewards

Some leases

Interest and depreciation

Some other leases

Straight line

Distinction

Consumption and nature of asset

Slide 40

June 2013

PwC

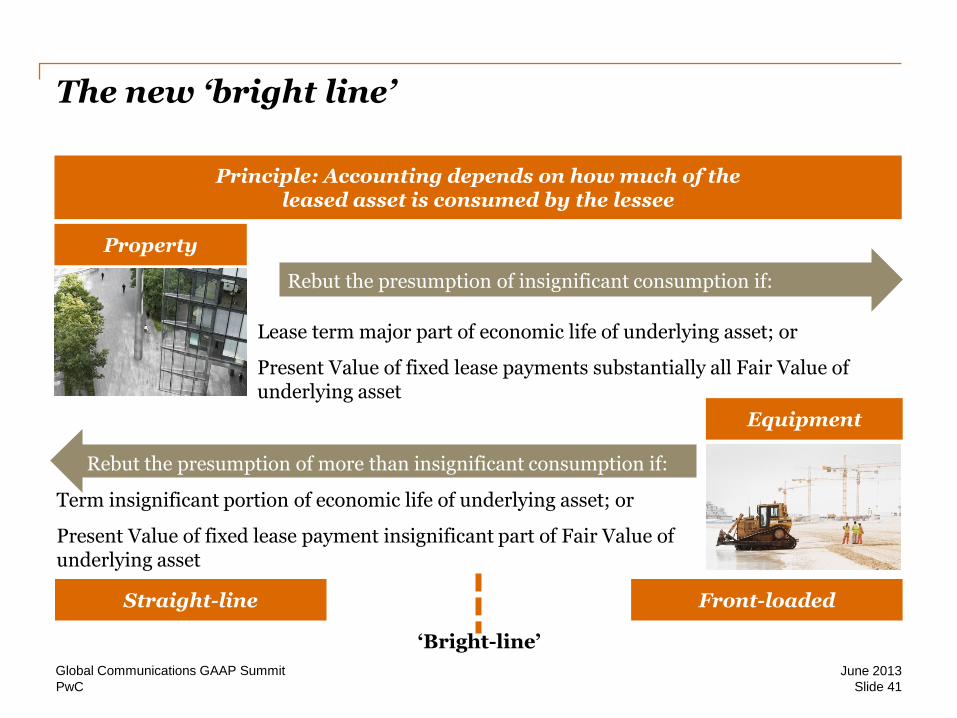

The new ‘bright line’

Global Communications GAAP Summit

Principle: Accounting depends on how much of the leased asset is consumed by the lessee

Rebut the presumption of insignificant consumption if:

Lease term major part of economic life of underlying asset; or

Present Value of fixed lease payments substantially all Fair Value of underlying asset

Straight-line Front-loaded

‘Bright-line’

Property

Equipment

Rebut the presumption of more than insignificant consumption if:

Term insignificant portion of economic life of underlying asset; or

Present Value of fixed lease payment insignificant part of Fair Value of underlying asset

Slide 41

June 2013

PwC

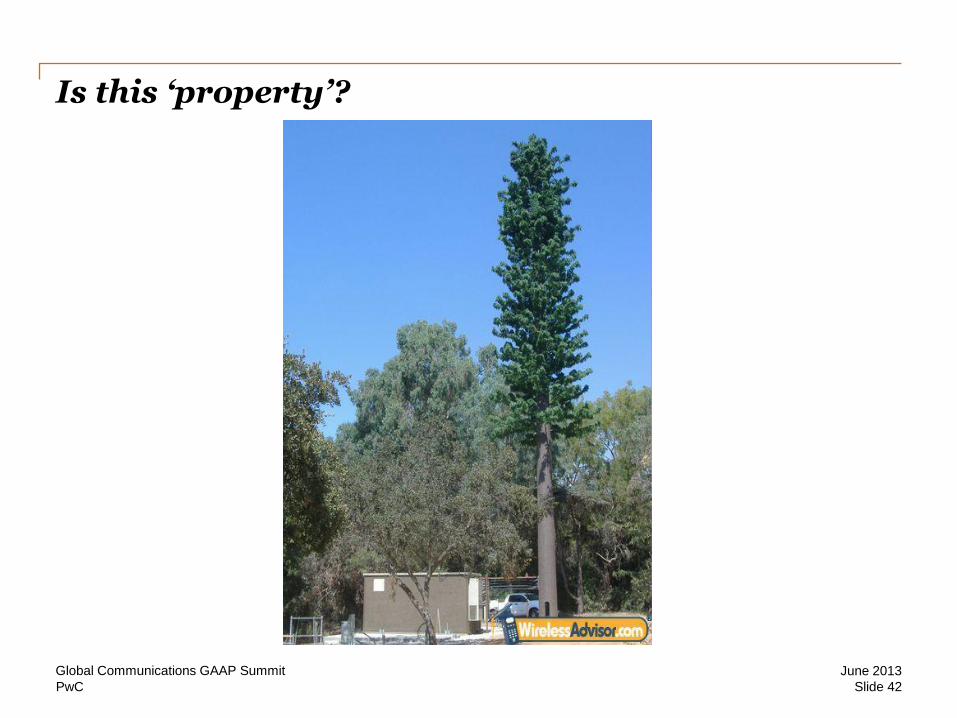

Is this ‘property’?

Global Communications GAAP Summit

Slide 42

June 2013

PwC

Presentation - lessees

Global Communications GAAP Summit

Slide 43

Type A Type B

Income statement Separate amortisation and interest expense

Single ‘rent’ expense

Cash flow ‘Principal’ payments classified as financing ‘Interest’ payments consistent with other interest (operating or financing)

Operating

June 2013

PwC

Presentation - lessors

Global Communications GAAP Summit

Slide 44

Type A Type B

Income statement Income at lease commencement consistent with business model: • Revenue and cost of sales

(‘gross’) if leases an alternative to sale

• Single line item (‘net’) if leases a means of providing finance

Interest income over lease term could be revenue, other income or finance income

Single ‘rent’ income

Cash flow Operating Operating

June 2013

PwC

Question time

At a high level, what do you think of the latest leasing proposals?

1) An improvement on current standards

2) Include some improvements, but not enough to justify the cost of implementation

3) Are not as good as current standards

4) Don’t know

Global Communications GAAP Summit

Slide 45

June 2013

PwC

Question time

Do you think that having all leases ‘on-balance sheet’ will change the way in which investors view your company?

1) It will have a significant impact

2) It will have some impact

3) It will have no impact, as investors already have all the information they need in the disclosure notes

4) No impact at all as my company has no leases

5) Don’t know

Global Communications GAAP Summit

Slide 46

June 2013

PwC

Reactions

Global Communications GAAP Summit

“[This] will not bring about a sufficient improvement in financial reporting to warrant the cost and complexity of changing the existing approach"

(Leaseurope) “The accounting has changed in a way that’s incomprehensible”

(Bill Bosco, president of Leasing 101 and member of the FASB/IASB Lease Project working group)

“[FASB’s Investors Technical Advisory Committee] uniformly agrees that the Board’s decisions in this project would not be an improvement to current accounting”

(ITAC meeting 24 July 2012)

Slide 47

“Obviously, this standard is not a very popular one”

(Hans Hoogervorst, IASB chairman)

June 2013

Final thoughts

PwC

Final thoughts

Significant accounting change for those with joint arrangements in 2013

Potentially more change on the horizon

Competition for capital is fierce

Are you getting your message across?

Global Communications GAAP Summit

Slide 49

June 2013

PwC

Coffee break

Global Communications GAAP Summit

Slide 50

June 2013

PwC

Workshop 1: The new revenue standard

Global Communications GAAP Summit

Slide 51

June 2013

PwC

Workshops

• Two different workshops – all delegates will attend both workshops

› Group 1 – Sala Cosimo

› Group 2 – Sala Giuilano

› Group 3 – Sala Visconti (plenary room)

› Group 4 – Sala Lorenzo

• A listing of the room allocations for this mornings workshop has been placed upon the tables

• After your morning workshop please return to the plenary room (Sala Visconti)

Global Communications GAAP Summit

Slide 52

June 2013

PwC

Deutsche Telekom: Implementation Project Revenue Recognition Michael Brücks Heiko Erckhe

Global Communications GAAP Summit

Slide 53

June 2013

PwC

June 2013 Global Communications GAAP Summit

Slide 54

PwC

June 2013 Global Communications GAAP Summit

Slide 55

PwC

June 2013 Global Communications GAAP Summit

Slide 56

PwC

June 2013 Global Communications GAAP Summit

Slide 57

PwC

June 2013 Global Communications GAAP Summit

Slide 58

PwC

June 2013 Global Communications GAAP Summit

Slide 59

PwC

June 2013 Global Communications GAAP Summit

Slide 60

PwC

June 2013 Global Communications GAAP Summit

Slide 61

PwC

June 2013 Global Communications GAAP Summit

Slide 62

PwC

June 2013 Global Communications GAAP Summit

Slide 63

PwC

June 2013 Global Communications GAAP Summit

Slide 64

PwC

June 2013 Global Communications GAAP Summit

Slide 65

PwC

June 2013 Global Communications GAAP Summit

Slide 66

PwC

June 2013 Global Communications GAAP Summit

Slide 67

PwC

June 2013 Global Communications GAAP Summit

Slide 68

PwC

June 2013 Global Communications GAAP Summit

Slide 69

PwC

June 2013 Global Communications GAAP Summit

Slide 70

PwC

June 2013 Global Communications GAAP Summit

Slide 71

PwC

June 2013 Global Communications GAAP Summit

Slide 72

PwC

June 2013 Global Communications GAAP Summit

Slide 73

PwC

June 2013 Global Communications GAAP Summit

Slide 74

PwC

June 2013 Global Communications GAAP Summit

Slide 75

PwC

June 2013 Global Communications GAAP Summit

Slide 76

PwC

June 2013 Global Communications GAAP Summit

Slide 77

PwC

June 2013 Global Communications GAAP Summit

Slide 78

PwC

June 2013 Global Communications GAAP Summit

Slide 79

PwC

June 2013 Global Communications GAAP Summit

Slide 80

PwC

Spending wisely - does the market understand the Telco growth story? Simon Harris Nirmal Shah

Global Communications GAAP Summit

Slide 81

June 2013

PwC

How are you prioritising your investments?

Do stakeholders understand your

investment rationale?

Global Communications GAAP Summit

Slide 82

$$$

Cross border M&A

Digital and

value added

services

Network capex and

spectrum

Content deals

June 2013

PwC

Question time

Over the next 3 years, where will your company’s (or your client’s) investment efforts be focused?

1) Mergers & acquisitions

2) Content deals

3) Digital and value added services

4) Bandwidth and spectrum

5) Unlikely to be doing any deals

Global Communications GAAP Summit

Slide 83

June 2013

Cross-border M&A

PwC

Cross-border M&A activity

Global Communications GAAP Summit

Slide 85

June 2013

PwC

Appraising M&A targets

Global Communications GAAP Summit

Slide 86

6.Is the pricing of risk management too high?

1. What are the real cash flows likely to be?

2. Where are the key risks?

3. What effect do the risks have on the cash flows?

7. How can I increase the liquidity in the financing markets to reduce my equity exposure?

8.How much equity do I need to put in?

5. How strong are the counterparties that help manage risk?

4.How can these risks be measured, managed, mitigated and allocated?

9.What are my return and equity exposure requirements?

June 2013

Content and value added services

PwC

Telcos are diversifying into other areas

Global Communications GAAP Summit

Slide 88

Content & content delivery Digital and value added services

June 2013

PwC

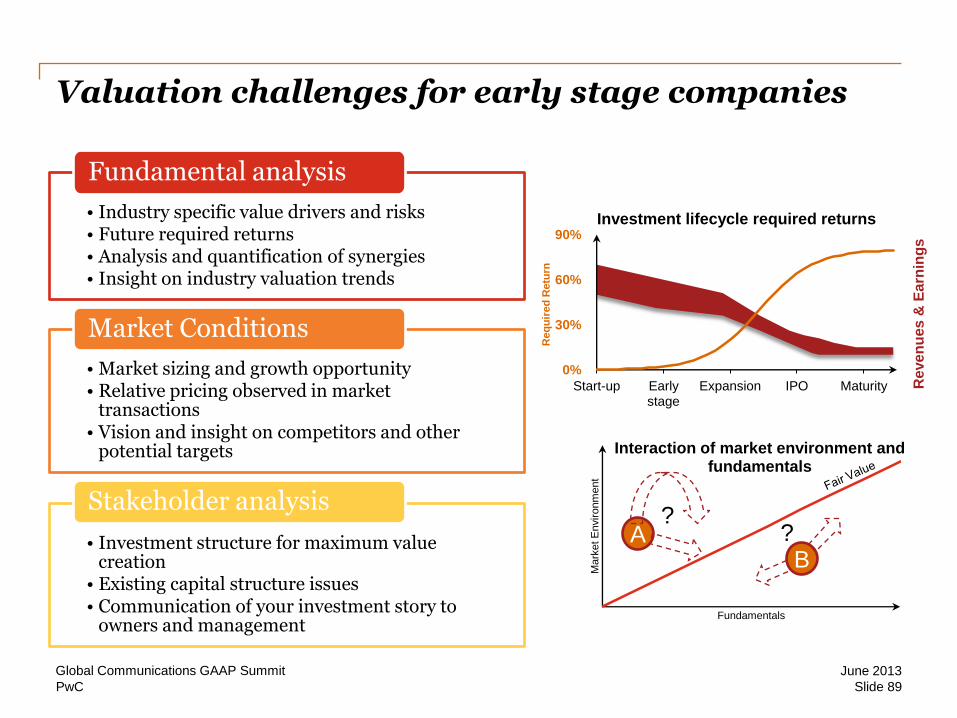

Valuation challenges for early stage companies

• Industry specific value drivers and risks • Future required returns • Analysis and quantification of synergies • Insight on industry valuation trends

Fundamental analysis

• Market sizing and growth opportunity • Relative pricing observed in market

transactions • Vision and insight on competitors and other

potential targets

Market Conditions

• Investment structure for maximum value creation

• Existing capital structure issues • Communication of your investment story to

owners and management

Stakeholder analysis

0%

30%

60%

90%

Start-up Early stage

Expansion IPO Maturity Re

ve

nu

es

& E

arn

ing

s

Investment lifecycle required returns

Mark

et E

nvironm

ent

Fundamentals

Interaction of market environment and fundamentals

A B

? ?

Global Communications GAAP Summit

Slide 89

Req

uir

ed

Retu

rn

June 2013

Spectrum

PwC

Investment in spectrum

Global Communications GAAP Summit

Slide 91

Canadian regulator announces 700

MHz auction to mixed reaction

Over $150bn raised globally in 3G

auctions

Czechs pull plug on

4G spectrum auction

after carriers bid too

much

Did SK Telecom pay

too much in the South

Korean spectrum

auction?

June 2013

PwC

3G vs. 4G

Global Communications GAAP Summit

Slide 92

June 2013

PwC

Spectrum – value drivers

Global Communications GAAP Summit

Slide 93

Efficiency of the auction Uniqueness of the opportunity

Auction design

Number of licences or lots

Marketing

Experience and preparation

Toe hold

Threat of new entrants

Technology neutrality

Market sentiment

Competition between firms

Market forces

Determined by regulatory authority

Determined by external factors

Auction prices

June 2013

PwC

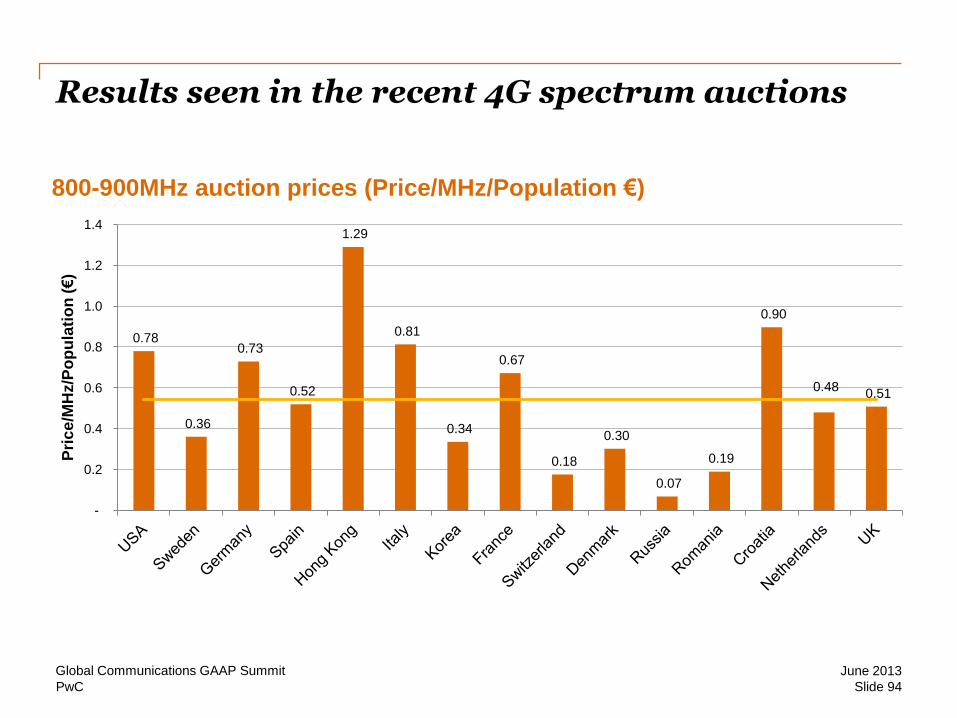

Results seen in the recent 4G spectrum auctions

Global Communications GAAP Summit

Slide 94

0.78

0.36

0.73

0.52

1.29

0.81

0.34

0.67

0.18

0.30

0.07

0.19

0.90

0.48 0.51

-

0.2

0.4

0.6

0.8

1.0

1.2

1.4

Pri

ce

/MH

z/P

op

ula

tio

n (€

)

800-900MHz auction prices (Price/MHz/Population €)

June 2013

PwC

Valuing spectrum can be tricky... as seen in Switzerland

-

20

40

60

80

100

120

140

Orange Sunrise Swisscom

MH

z

Switzerland 4G Spectrum Auction Outcome

800 - 900 MHz 1800 - 2100 MHz 2600 MHz

CHF 155m

CHF 482m CHF 360m

Global Communications GAAP Summit

Slide 95

June 2013

PwC

-

10

20

30

40

50

60

Wind Vodafone Telecom Italia H3G

MH

z

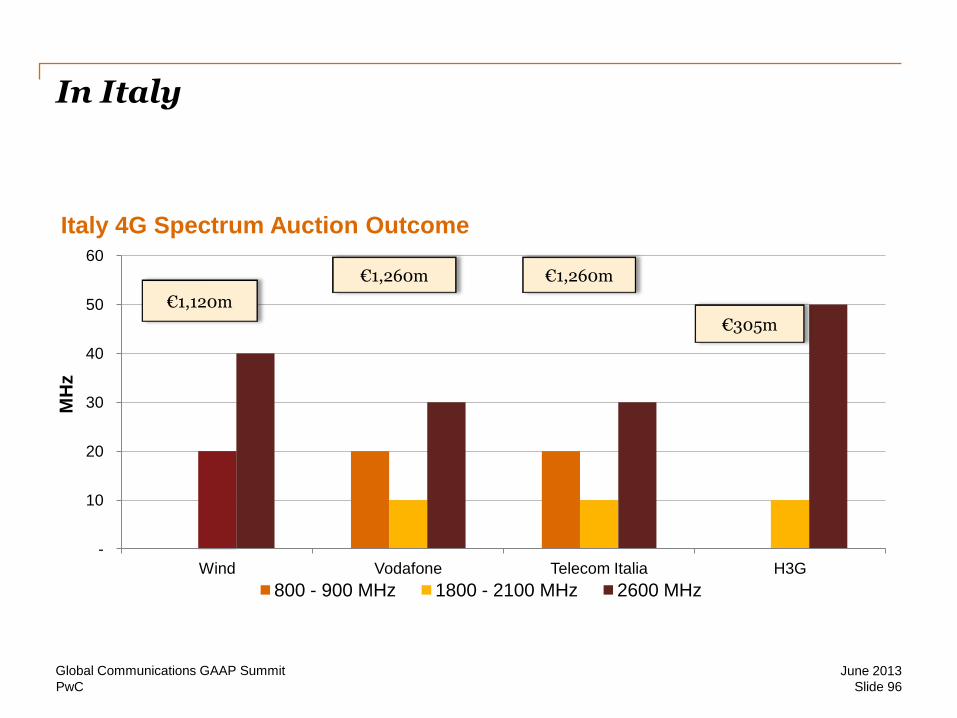

Italy 4G Spectrum Auction Outcome

800 - 900 MHz 1800 - 2100 MHz 2600 MHz

In Italy

€1,120m

€1,260m

€305m

€1,260m

Global Communications GAAP Summit

Slide 96

June 2013

PwC

-

10

20

30

40

50

60

70

80

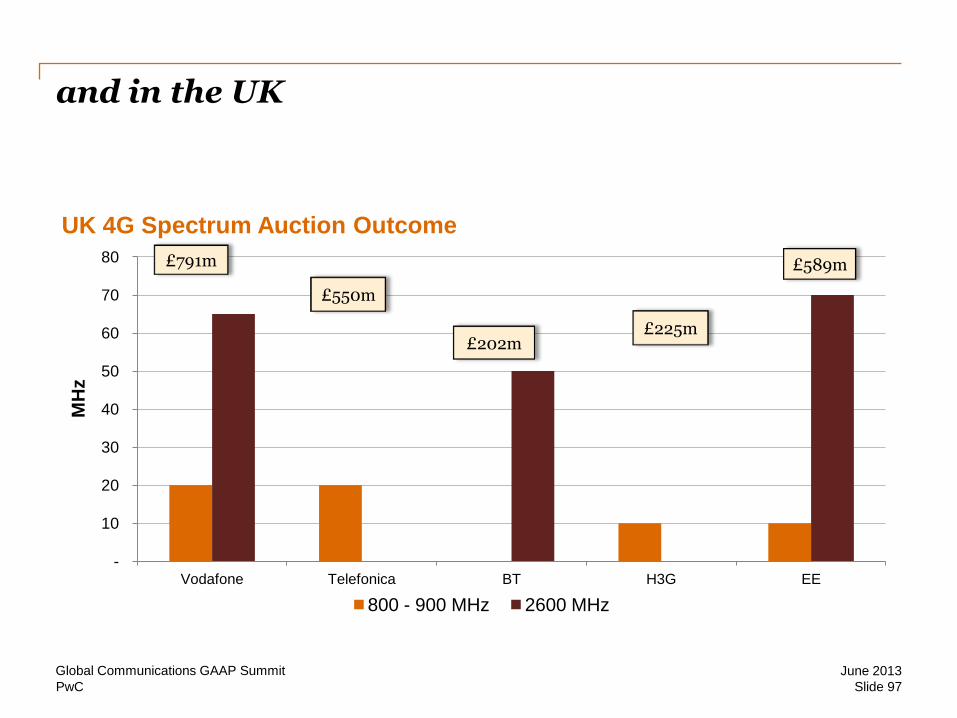

Vodafone Telefonica BT H3G EE

MH

z

UK 4G Spectrum Auction Outcome

800 - 900 MHz 2600 MHz

and in the UK

£791m

£550m

£225m £202m

£589m

Global Communications GAAP Summit

Slide 97

June 2013

PwC

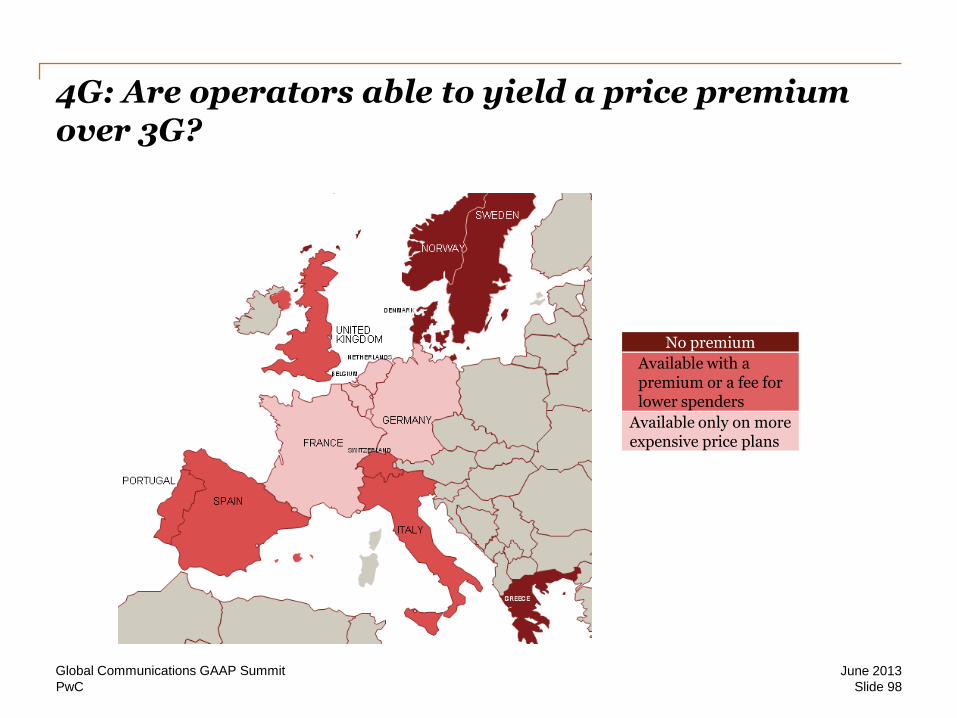

4G: Are operators able to yield a price premium over 3G?

June 2013 Global Communications GAAP Summit

Slide 98

No premium

Available with a premium or a fee for lower spenders

Available only on more expensive price plans

PwC

Return on invested capital

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

20%

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

Europe & N.America Operators Emerging Markets Operators

Technology and Media Companies

Global Communications GAAP Summit

Slide 99

June 2013

PwC

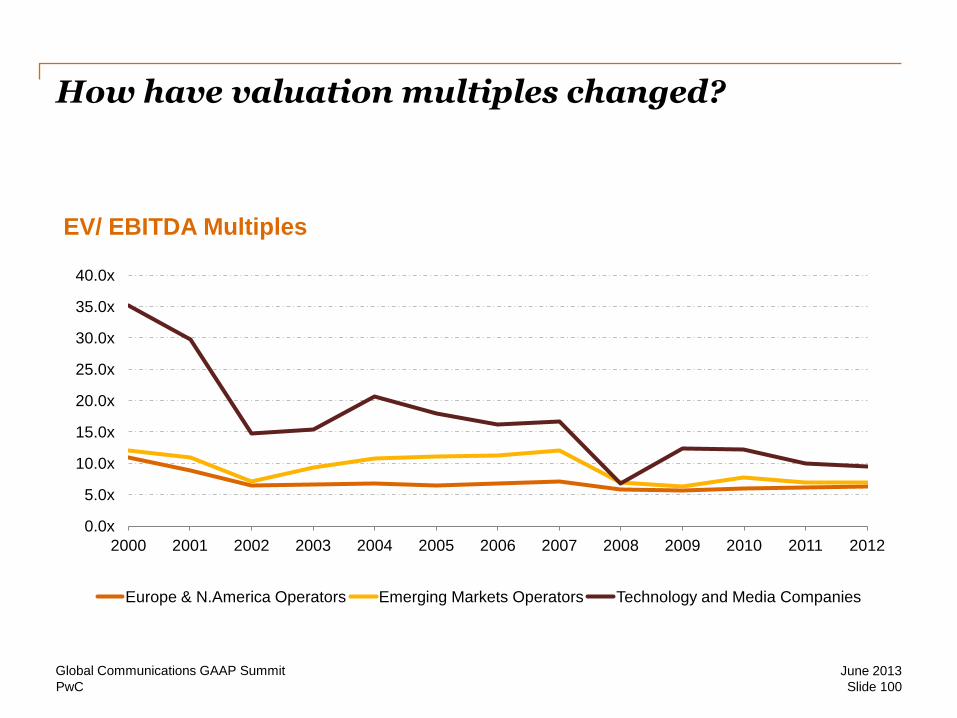

How have valuation multiples changed?

0.0x

5.0x

10.0x

15.0x

20.0x

25.0x

30.0x

35.0x

40.0x

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

EV/ EBITDA Multiples

Europe & N.America Operators Emerging Markets Operators Technology and Media Companies

Global Communications GAAP Summit

Slide 100

June 2013

PwC

Question

In your view, what is the main reason for Telcos being valued on lower valuation multiples (compared to media and technology companies)?

1) There are limited growth opportunities for Telcos

2) The market does not understand the Telco growth story

3) Media and technology companies are more attractive to the investor community

4) There is concern that returns on investment are not high enough to enhance shareholder value

Global Communications GAAP Summit

Slide 101

June 2013

PwC

Workshop 2: To buy or to lease?

Global Communications GAAP Summit

Slide 102

June 2013

PwC

Workshops

Global Communications GAAP Summit

Slide 103

Workshop groups are different for this afternoon

› Group 1 – Sala Cosimo

› Group 2 – Sala Giuilano

› Group 3 – Sala Lorenzo

› Group 4 – Sala Visconti (plenary room)

• After your afternoon workshop please return to the plenary room (Sala Visconti)

June 2013

PwC

Lunch

Lunch will be in the Restaurant Savoia

Global Communications GAAP Summit

Slide 104

June 2013

PwC

Coffee break

Global Communications GAAP Summit

Slide 105

June 2013

• 15:15 – 15:45 – outside by the swimming pool

• Back in Sala Visconti (plenary) at 15:45

PwC

Closing remarks

Global Communications GAAP Summit

Slide 106

June 2013

PwC

From yesterday Integrated Reporting – telling your story

How relevant was this session?

1) Not at all relevant

2) Somewhat relevant

3) Relevant

4) Very relevant

Global Communications GAAP Summit

Slide 107

June 2013

PwC

What’s new in accounting ? How relevant was this session?

1) Not at all relevant

2) Somewhat relevant

3) Relevant

4) Very relevant

Global Communications GAAP Summit

Slide 108

June 2013

PwC

Telecom Italia: Market update

How relevant was this session?

1) Not at all relevant

2) Somewhat relevant

3) Relevant

4) Very relevant

Global Communications GAAP Summit

Slide 109

June 2013

PwC

Workshop 1: The new revenue standard

How relevant was this session?

1) Not at all relevant

2) Somewhat relevant

3) Relevant

4) Very relevant

Global Communications GAAP Summit

Slide 110

June 2013

PwC

Deutsche Telekom: Implementation project Revenue recognition

How relevant was this session?

1) Not at all relevant

2) Somewhat relevant

3) Relevant

4) Very relevant

Global Communications GAAP Summit

Slide 111

June 2013

PwC

Spending wisely - does the market understand the Telco growth story?

How relevant was this session?

1) Not at all relevant

2) Somewhat relevant

3) Relevant

4) Very relevant

Global Communications GAAP Summit

Slide 112

June 2013

PwC

Workshop 2: To buy or to lease?

How relevant was this session?

1) Not at all relevant

2) Somewhat relevant

3) Relevant

4) Very relevant

Global Communications GAAP Summit

Slide 113

June 2013

PwC

Overall, how do you rate the 2013 Global Communications GAAP Summit?

1) Poor

2) Okay

3) Useful

4) Very useful

Global Communications GAAP Summit

Slide 114

June 2013

PwC

If we hold a similar event next year are you or someone from your company likely to attend?

1) Yes

2) No

Global Communications GAAP Summit

Slide 115

June 2013

PwC

Where would you like the next Global Communications GAAP Summit to be held?

Text your suggestions NOW!

Global Communications GAAP Summit

Slide 116

June 2013

Thank you and have a safe journey

This publication has been prepared for general guidance on matters of interest only, and does

not constitute professional advice. You should not act upon the information contained in this

publication without obtaining specific professional advice. No representation or warranty

(express or implied) is given as to the accuracy or completeness of the information contained

in this publication, and, to the extent permitted by law, PricewaterhouseCoopers LLP, its

members, employees and agents do not accept or assume any liability, responsibility or duty of

care for any consequences of you or anyone else acting, or refraining to act, in reliance on the

information contained in this publication or for any decision based on it.

© 2013 PricewaterhouseCoopers LLP. All rights reserved. In this document, “PwC” refers to

PricewaterhouseCoopers LLP (a limited liability partnership in the United Kingdom) which is a

member firm of PricewaterhouseCoopers International Limited, each member firm of which is a

separate legal entity.