Global & MENA Fintech - More Capital

12

Global & MENA Fintech Sector Perspective November 2020 Prepared by: Jad Salame Mohamed Ibrahim Saeb Nahas Ramzi Mneimneh Ahmad Tuffaha Phoenician Invest Ltd. (a subsidiary of More Capital) DD-16-118-005, 16, Wework, Hub71, Al Khatem Tower ADGM Square, Al Maryah Island Abu Dhabi, United Arab Emirates Tel: +971 50 671 9088 Email: [email protected] www.phoenicianfunds.com

Transcript of Global & MENA Fintech - More Capital

Global & MENA FintechSector Perspective

November 2020

Prepared by:

Jad SalameMohamed IbrahimSaeb NahasRamzi MneimnehAhmad Tuffaha

Phoenician Invest Ltd. (a subsidiary of More Capital)DD-16-118-005, 16, Wework, Hub71, Al Khatem TowerADGM Square, Al Maryah Island Abu Dhabi, United Arab Emirates

Tel: +971 50 671 9088Email: [email protected]

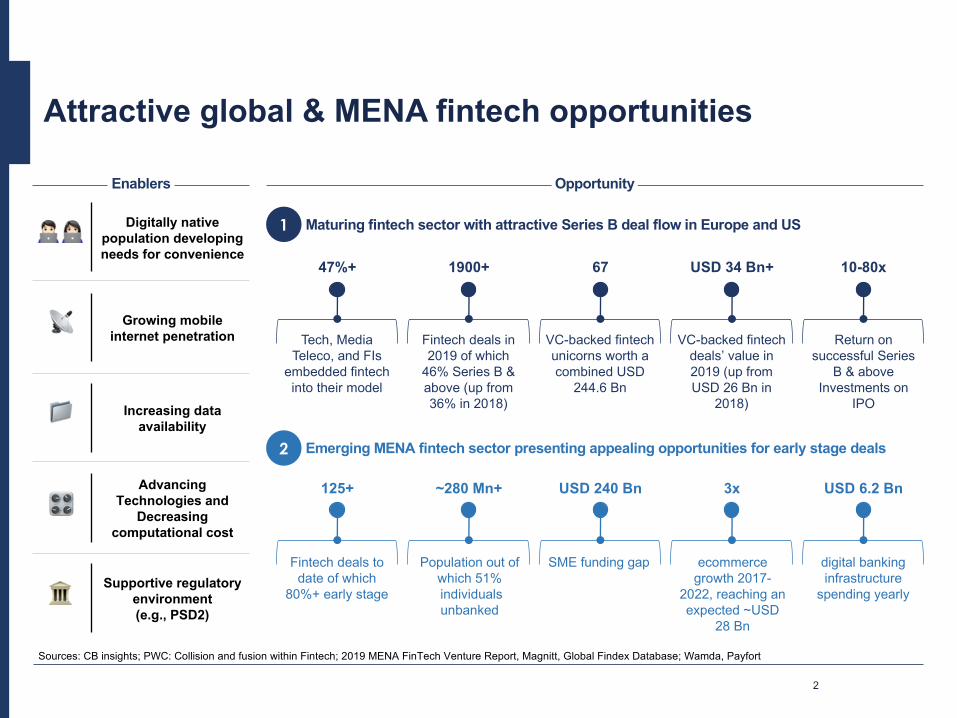

Attractive global & MENA fintech opportunities

Population out of which 51%individuals unbanked

SME funding gap ecommerce growth 2017-

2022, reaching an expected ~USD

28 Bn

Fintech deals to date of which

80%+ early stage

digital banking infrastructure

spending yearly

Emerging MENA fintech sector presenting appealing opportunities for early stage deals

Maturing fintech sector with attractive Series B deal flow in Europe and US

Return on successful Series

B & above Investments on

IPO

VC-backed fintech unicorns worth a combined USD

244.6 Bn

VC-backed fintech deals’ value in 2019 (up from USD 26 Bn in

2018)

Fintech deals in 2019 of which

46% Series B & above (up from 36% in 2018)

Tech, Media Teleco, and FIs

embedded fintech into their model

Digitally native population developing needs for convenience

Growing mobile internet penetration

Increasing data availability

Advancing Technologies and

Decreasing computational cost

Supportive regulatory environment (e.g., PSD2)

Enablers

10-80xUSD 34 Bn+671900+47%+

USD 6.2 Bn3xUSD 240 Bn~280 Mn+125+

Opportunity

Sources: CB insights; PWC: Collision and fusion within Fintech; 2019 MENA FinTech Venture Report, Magnitt, Global Findex Database; Wamda, Payfort

1

2

2

Traditional financial services undergoing paradigm shift

Source: KPMG “Regulation and supervision of Fintech”, 2019

1 GLOBAL FINTECH TRENDS

Prevailing legacy systemsRequiring high costs & long lead times for changes/ adaptation

Limited innovation and customization of products and offeringsCatering to the changing customer behavior and preferences (Digital on-demand approach)

Traditional security technologies Basic business intelligence and analytical tools leaving data open to breaches

Increasing regulatory & compliance requirements Basel III, IFRS9, MiFiD 2

Drivers of Opportunity Emergence of Fintech

Emerging Fintech friendly regulation and open data

legislation e.g., PSD2, Open banking regulation in Europe

Changing Landscape

Emerging regulatory sandboxes for swift solution/ product testing and launch e.g., FCA regulatory sandbox

Availability of advanced technologies, infrastructure

and data at a decreasing cost e.g., AI/ ML, Cloud based

platforms

Updated guidelines on technology and security

management e.g., GDPR in Europe

Digitally enabled products and services Convenient, cheaper and faster user experience and service

Advanced and state of the art infrastructure toolsInnovative technology layers providing banks with agility using contextualized data and customer data analytics

Innovative cybersecurity systemsModern technologies (e.g. Artificial Intelligence) offering robust and secure data environments

Revolutionary new generation platforms Blockchain enabled applications including crypto currencies, decentralized contract validation

3

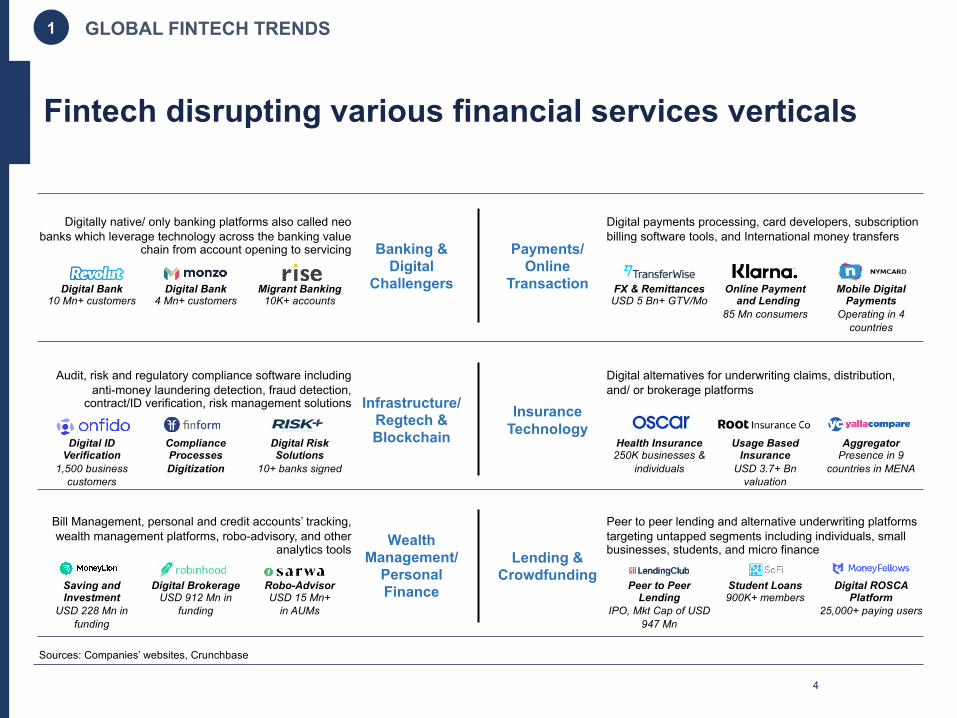

Fintech disrupting various financial services verticals

Digitally native/ only banking platforms also called neo banks which leverage technology across the banking value

chain from account opening to servicing

Audit, risk and regulatory compliance software including anti-money laundering detection, fraud detection,

contract/ID verification, risk management solutions

Bill Management, personal and credit accounts’ tracking, wealth management platforms, robo-advisory, and other

analytics tools

Digital payments processing, card developers, subscription billing software tools, and International money transfers

Digital alternatives for underwriting claims, distribution, and/ or brokerage platforms

Peer to peer lending and alternative underwriting platforms targeting untapped segments including individuals, small businesses, students, and micro financeLending &

Crowdfunding

Wealth Management/

Personal Finance

Insurance Technology

Infrastructure/ Regtech & Blockchain

Payments/ Online

Transaction

Banking & Digital

ChallengersDigital Bank10 Mn+ customers

Digital Bank4 Mn+ customers

FX & RemittancesUSD 5 Bn+ GTV/Mo

Online Paymentand Lending

85 Mn consumers

Health Insurance250K businesses &

individuals

Usage Based Insurance

USD 3.7+ Bnvaluation

Digital ID Verification

1,500 business customers

Compliance Processes Digitization

Student Loans900K+ members

Peer to Peer Lending

IPO, Mkt Cap of USD 947 Mn

Saving and Investment

USD 228 Mn in funding

Digital BrokerageUSD 912 Mn in

funding

Digital ROSCA Platform

25,000+ paying users

Migrant Banking10K+ accounts

Robo-AdvisorUSD 15 Mn+

in AUMs

AggregatorPresence in 9

countries in MENA

Mobile Digital Payments

Operating in 4 countries

Digital Risk Solutions

10+ banks signed

Sources: Companies’ websites, Crunchbase

1 GLOBAL FINTECH TRENDS

4

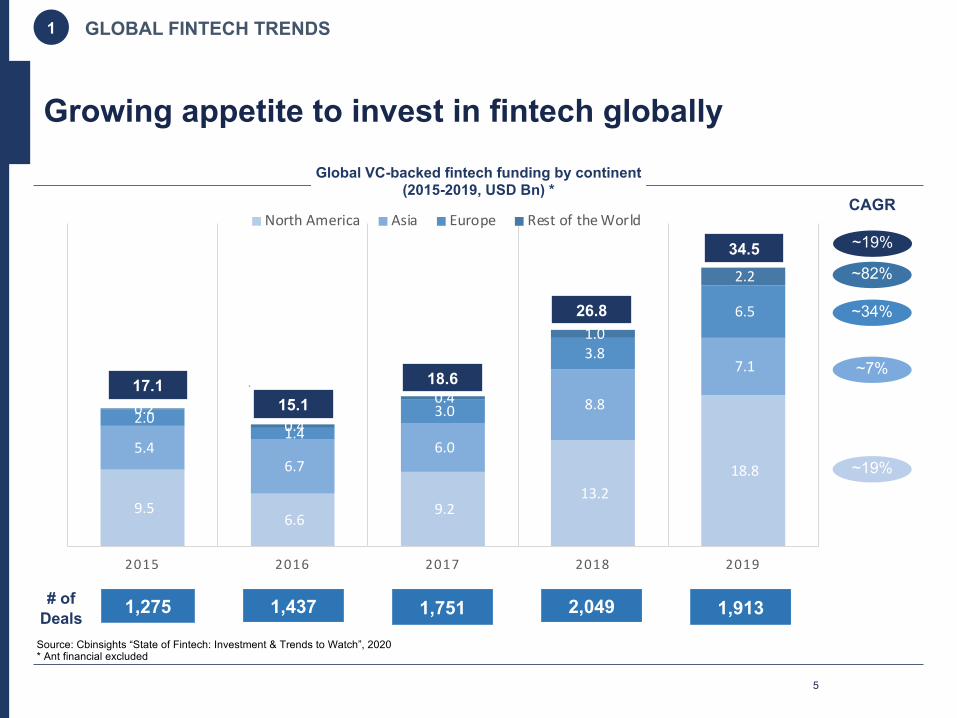

Growing appetite to invest in fintech globally

9.5 6.6

9.2 13.2

18.8 5.4

6.7 6.0

8.8

7.1

2.0 1.4

3.0

3.8

6.5

0.2 0.4

0.4

1.0

2.2

2015 2016 2017 2018 2019

North America Asia Europe Rest of the World

# of Deals 1,275 1,437 1,751

~19%

2,049 1,913

17.1

26.8

18.615.1

34.5

Source: Cbinsights “State of Fintech: Investment & Trends to Watch”, 2020* Ant financial excluded

Global VC-backed fintech funding by continent(2015-2019, USD Bn) *

1 GLOBAL FINTECH TRENDS

~82%

CAGR

~34%

~7%

~19%

5

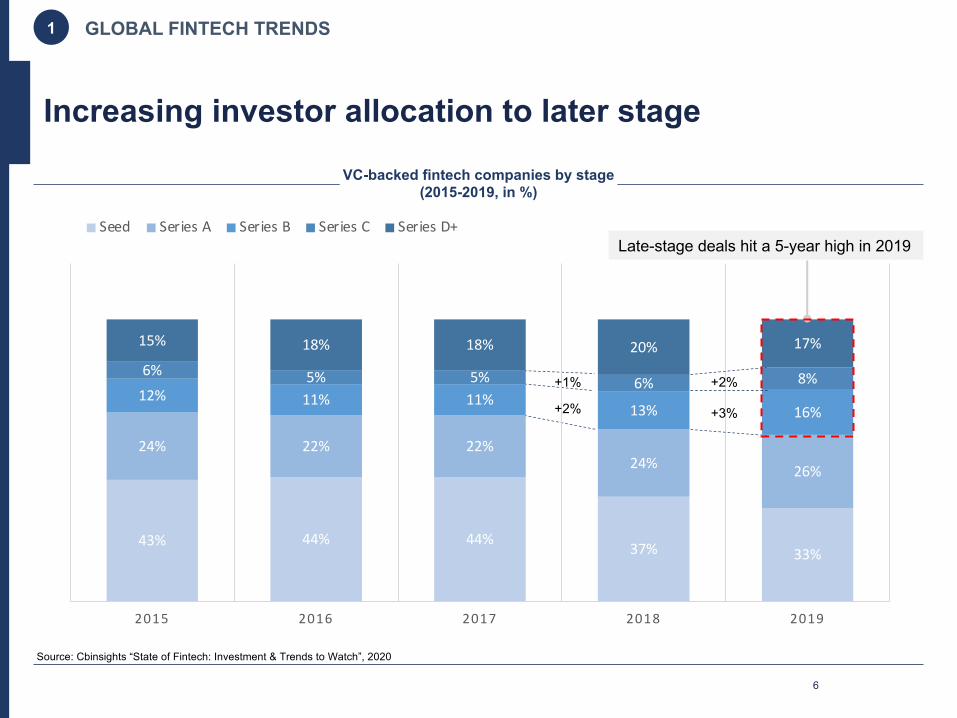

43% 44% 44% 37% 33%

24% 22% 22%24% 26%

12% 11% 11%13% 16%

6% 5% 5% 6% 8%

15% 18% 18% 20% 17%

2015 2016 2017 2018 2019

Seed Series A Series B Series C Series D+

Increasing investor allocation to later stage

VC-backed fintech companies by stage (2015-2019, in %)

1 GLOBAL FINTECH TRENDS

+2%

+3%

Late-stage deals hit a 5-year high in 2019

Source: Cbinsights “State of Fintech: Investment & Trends to Watch”, 2020

+1%

+2%

6

Exit activity showing signs of success in fintech

1 GLOBAL FINTECH TRENDS

§ Institutional investors focusing on the fintech sector and high growth companies (e.g., vertical/horizontal integration with other portfolio companies to realize synergies)

Sales to Financial Institutions or

Network Schemes

Sales to other fintechcompanies

Sales to Private Equity

IPO

Strategic Fit Example Deals

Payment Processing$ 8.3 Bn

Europe (Euronext)

Tax Compliance $ 1.4 Bn

US (NYSE)

§ Financial Institutions/banks/schemes looking to shift from traditional to digitally native solutions, and expand reach to provide a full spectrum of financial services

§ Cross functional acquisitions to diversify offerings, broaden reach and achieve synergies

Exit Mode

§ Companies looking to raise funding through public capital markets and increase their credibility and exposure

Acquired by Paypal$ 2.2 BnEurope

Acquired by Intuit$ 7.1 Bn

US

Acquired by VEP$ 6.5 Bn

US

Acquired by EQT$ 3 Bn

EU

Acquired by Morgan Stanley$ 13 Bn

US

Acquired by Visa$ 5.3 Bn

US

Sources: Mind the bride, Crunchbase “ Fintech M&A”, 2018, Cbinsights “State of Fintech: Investment & Trends to Watch”, 2020

7

Estimated 250 M&A deals in 2018

vs 200 in 2017 (25% Growth)

P2P Lending€ 1.2 Bn

London (LSE)

In particular, Series B remains a sweet spot

Funding Size

1 GLOBAL FINTECH TRENDS

15% Series C

100% Start-upsSeed

9%Series D

USD 50 – 500K

USD 1 – 5 Mn

USD 5 – 20 Mn

USD 20 – 50 Mn

USD 100+ Mn3% Series E & AboveSources: Mind the bridge, Crunchbase “ Fintech M&A”, 2018, Cbinsights, EquityZen, DealRoom

Startups Progression Benchmark (USA, 2018) Exit Return Examples

If a startup were to exit having raised USD 20 Mn+, average multiple on capital raised is > 3x (vs. less than 2.7x exiting before having raised USD 20 Mn)

12 24.5 25

38.3x 16.9x80.1x

Inve

stm

ent

(USD

, Mn)

Ret

urn

at e

xit

USD

8.3

Bn

IPO

Val

uatio

nU

SD 5

.42

Bn

IPO

Val

uatio

n

Series B Series C Series D

17 250 52

6.3x 3.6xN/A

Inve

stm

ent

(USD

, Mn)

Ret

urn

at e

xit

Series A Series B Series C

USD

2.9

Bn

IPO

Val

uatio

n

10 25.8 103

9.4x 1.6x12.5x

Inve

stm

ent

(USD

, Mn)

Ret

urn

at e

xit

Series B-I Series B-II Series C

Series B Rounds

8

48% Series A

30% Series B

USD 50 – 100 Mn

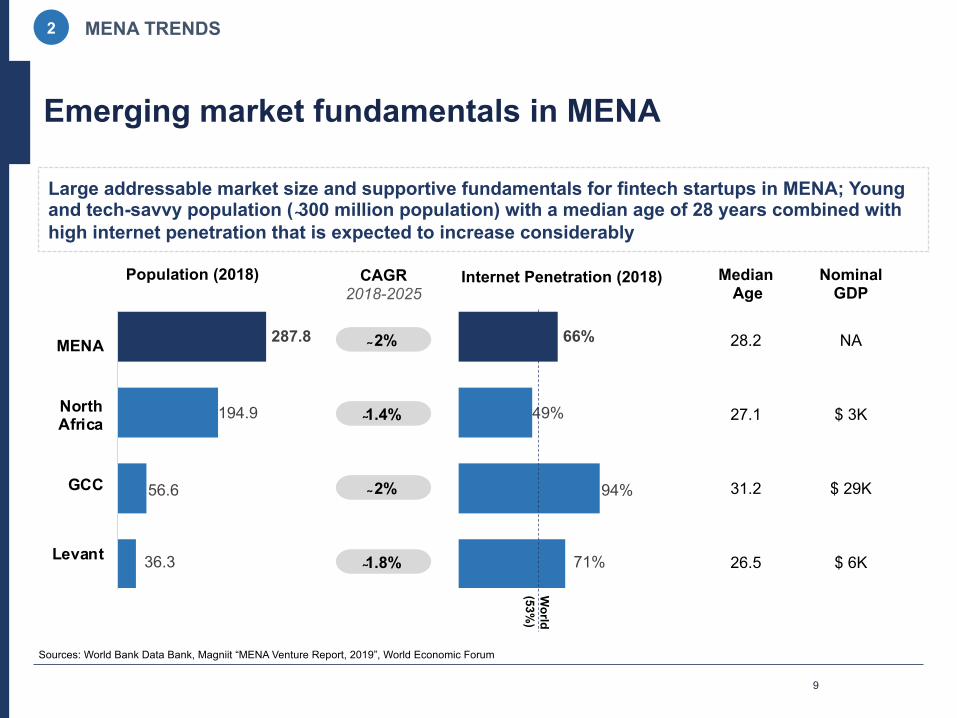

Emerging market fundamentals in MENA

Sources: World Bank Data Bank, Magniit “MENA Venture Report, 2019”, World Economic Forum

2 MENA TRENDS

Large addressable market size and supportive fundamentals for fintech startups in MENA; Young and tech-savvy population ( 300 million population) with a median age of 28 years combined with high internet penetration that is expected to increase considerably

36.3

56.6

194.9

287.8

Levant

GCC

NorthAfrica

MENA

Population (2018)

2%

CAGR 2018-2025

1.4%

2%

1.8% 26.5

31.2

27.1

28.2

MedianAge

$ 6K

$ 29K

$ 3K

NA

Nominal GDP

71%

94%

49%

66%

Internet Penetration (2018)

World

(53%)

9

24.7

7.1 4.41.1 0.3 0 0.020.3

4.50.7 0.4

36.1

44.3

13.8

Egypt Lebanon Jordan Iraq KSA UAE Kuwait

Inflow Outflow

95%

Untapped white spaces with potential for disruption

~150 Mn individuals could be newly included in financial system

Significant need for payments infrastructure driving by e-commerce

OECD avg. Global average middle income countries

Sources: World Bank Data Bank, World Economic Forum, Union of Arab Banks, McKinsey Global Institute, Wamda “State of Fintech”

Share of Loans to SMEs by Arab Banks (2015 - selected countries, %)MENA Banked Population (in % , 2018)

MENA E-commerce Market Value (2017-2022, USD Bn)

2.3 8.9 3.0

10.0

1 0.7

2.9

2.2

6.8

2017 2022

UAE KSA Egypt Rest Of MENA

28.5

8.3

2 MENA TRENDS

77%

37% 35% 49%

GCC Levant North Africa MENA

USD 240 Bn SME credit gap in MENA region with 63% of SMEs not having access to finance

18%

2%

15% 14%8%

GCC Levant North Africa MENA

Total remittances inflows grew 9.3% to USD 53 Bnin 2017

MENA Migrant Remittance (2017- selected countries , USD Bn)

~28%CAGR

10

Early stage and growing ecosystemIn

vest

men

t in

Fint

ech

2019

–U

SD

Bn

100%

NorthAmerica

Europe AsiaPacific

Rest ofthe World

Total

Inve

stm

ent/

GD

P%

of G

DP

54%

19%

21%

6%

28% 25% 35% 12%

2x GDP/ Investment

Sources: CB insights, Wamda, Payfort, IMF, Magniit “MENA venture report, 2019”, thenational.ae

MENA region presents a large opportunity ahead

MENA Fintech LandscapeMENA Venture Investment in Fintech

2 MENA TRENDS

Risk management

solutionsLebanon

Robo-advisoryUAE

Digital credit lendingEgypt

Loan aggregator

UAE

Peer-to-peerUAE

Electronic paymentEgypt

E-wallet/ paymentsUAE

Digital PaymentLebanon

Payment gatewayUAE

Payment solutionsKSA

HR solutionsUAE

BitcoinexchangeTunisia

Blockchainwallet/Exchange

UAE

Mobile remittance

UAE

Acquired AcquiredIPO 2019

Payments & Remittances

Lending

Blockchain

Wealth management Regtech/Banking

PropTech

InsureTech

Equity Crowdfunding

UAE

Migrant BankingUAE

RE Crowdfunding

UAE

RE investment platformUAE

125 MENA Fintech Startups Raised

Funding (2015-2018)

81% early stage

investments

13 Fintech startups exited since 2015

Portfolio management

UAE

Credit risk management

solutions Lebanon

11

MENA estimated at 1% of global

Regulations & initiatives supporting adoption of fintech

SAMA released ”rules governing microfinance companies” in Dec 19, payment regulations released in Jan 20, digital only bank guidelines released in Feb 20, and other regulations as well as experimental permits awareded

Central bank of Egypt developed the “mobile payments regulation” to develop sustainable financial services and shift towards a cash-less economy

ADGM’s Financial Services Regulatory Authority (FSRA) published a guide on the establishment of digital banks followed by a regulatory framework for digital investment managers, or robo-advisers

Central Bank of Bahrain introduced crowdfunding regulations and launched a RegLab

Central Bank of Bahrain introduced crowdfunding regulations

Central Bank of Jordan introduced a new law for electronic transactions and payments

Central Bank of Morocco introduced the Law 103-12 that defines the scope for the creation of the “Payment Institution” status

8 MENA countries have created sandboxes or RegLabs

ReglLabs

Sources: Various Central Bank websites, statements, and regulations, Magniit “MENA venture report, 2019”, Magniit Fintech Saudi 2019-2020

2 MENA TRENDS

Selected examples

12

![[PreMoney MENA 2015] Wamda Capital >> Fares Ghandour & Khaled Talhouni, "ONE REGION, THREE VERTICALS: Fintech, Media & E-Commerce"](https://static.fdocuments.net/doc/165x107/587ba69e1a28ab81758b5f8b/premoney-mena-2015-wamda-capital-fares-ghandour-khaled-talhouni-one.jpg)