GFE/TIL AND COC WORKFLOW - eprmg.net · GFE/TIL and COC Workflow 08/20/2013 Rev. 4/3/2014 GFE/TIL...

22

GFE/TIL and COC Workflow 08/20/2013 Rev. 4/3/2014 GFE/TIL AND COC WORKFLOW 1 Table of Contents Page 1 of the GFE ................................................................................................................................................... 2 Tolerance Levels ................................................................................................................................................... 5 Page 2 of the GFE ................................................................................................................................................... 7 Box 6 of the GFE .................................................................................................................................................. 12 How to Calculate Transfer Tax ............................................................................................................................ 13 Page 3 of the GFE ................................................................................................................................................. 14 Events Triggering Re-disclosure ........................................................................................................................... 15 Re-disclosure Process .......................................................................................................................................... 18 Using the TIL Calculator ...................................................................................................................................... 19 Calculating the TIL and Redisclosing .................................................................................................................... 20

-

Upload

truongkhuong -

Category

Documents

-

view

224 -

download

0

Transcript of GFE/TIL AND COC WORKFLOW - eprmg.net · GFE/TIL and COC Workflow 08/20/2013 Rev. 4/3/2014 GFE/TIL...

GFE/TIL and COC Workflow 08/20/2013 Rev. 4/3/2014

GFE/TIL AND COC WORKFLOW

1

Table of Contents

Page 1 of the GFE ................................................................................................................................................... 2

Tolerance Levels ................................................................................................................................................... 5

Page 2 of the GFE ................................................................................................................................................... 7

Box 6 of the GFE .................................................................................................................................................. 12

How to Calculate Transfer Tax ............................................................................................................................ 13

Page 3 of the GFE ................................................................................................................................................. 14

Events Triggering Re-disclosure ........................................................................................................................... 15

Re-disclosure Process .......................................................................................................................................... 18

Using the TIL Calculator ...................................................................................................................................... 19

Calculating the TIL and Redisclosing .................................................................................................................... 20

GFE/TIL and COC Workflow 08/20/2013 Rev. 4/3/2014

GFE/TIL AND COC WORKFLOW

2

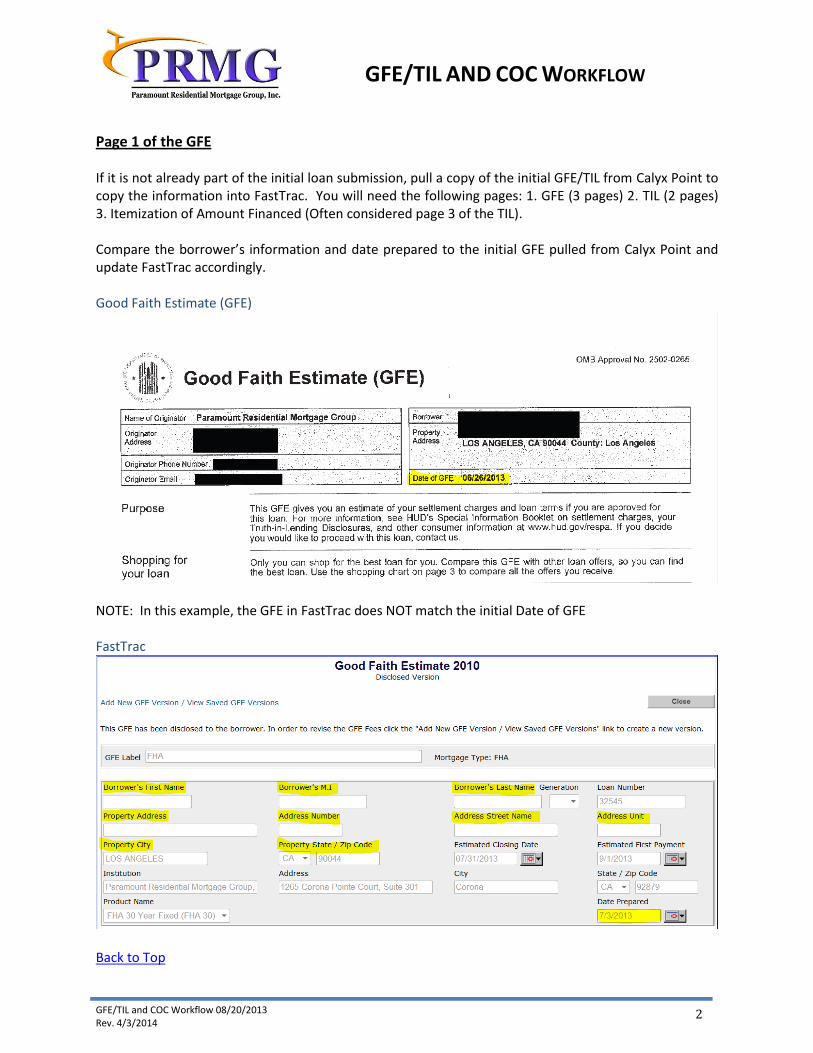

Page 1 of the GFE If it is not already part of the initial loan submission, pull a copy of the initial GFE/TIL from Calyx Point to copy the information into FastTrac. You will need the following pages: 1. GFE (3 pages) 2. TIL (2 pages) 3. Itemization of Amount Financed (Often considered page 3 of the TIL). Compare the borrower’s information and date prepared to the initial GFE pulled from Calyx Point and update FastTrac accordingly. Good Faith Estimate (GFE)

NOTE: In this example, the GFE in FastTrac does NOT match the initial Date of GFE FastTrac

Back to Top

GFE/TIL and COC Workflow 08/20/2013 Rev. 4/3/2014

GFE/TIL AND COC WORKFLOW

3

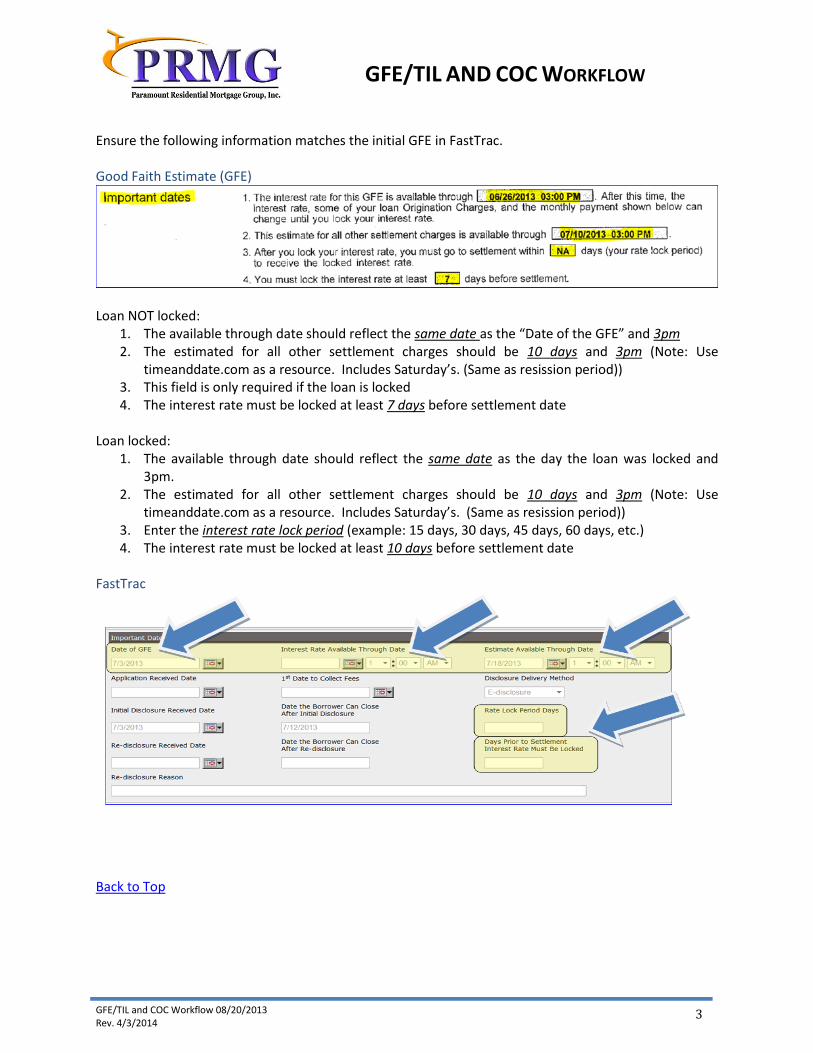

Ensure the following information matches the initial GFE in FastTrac. Good Faith Estimate (GFE)

Loan NOT locked:

1. The available through date should reflect the same date as the “Date of the GFE” and 3pm 2. The estimated for all other settlement charges should be 10 days and 3pm (Note: Use

timeanddate.com as a resource. Includes Saturday’s. (Same as resission period)) 3. This field is only required if the loan is locked 4. The interest rate must be locked at least 7 days before settlement date

Loan locked:

1. The available through date should reflect the same date as the day the loan was locked and 3pm.

2. The estimated for all other settlement charges should be 10 days and 3pm (Note: Use timeanddate.com as a resource. Includes Saturday’s. (Same as resission period))

3. Enter the interest rate lock period (example: 15 days, 30 days, 45 days, 60 days, etc.) 4. The interest rate must be locked at least 10 days before settlement date

FastTrac

Back to Top

GFE/TIL and COC Workflow 08/20/2013 Rev. 4/3/2014

GFE/TIL AND COC WORKFLOW

4

Ensure the following information matches the initial GFE in FastTrac. Good Faith Estimate (GFE)

FastTrac

Back to Top

GFE/TIL and COC Workflow 08/20/2013 Rev. 4/3/2014

GFE/TIL AND COC WORKFLOW

5

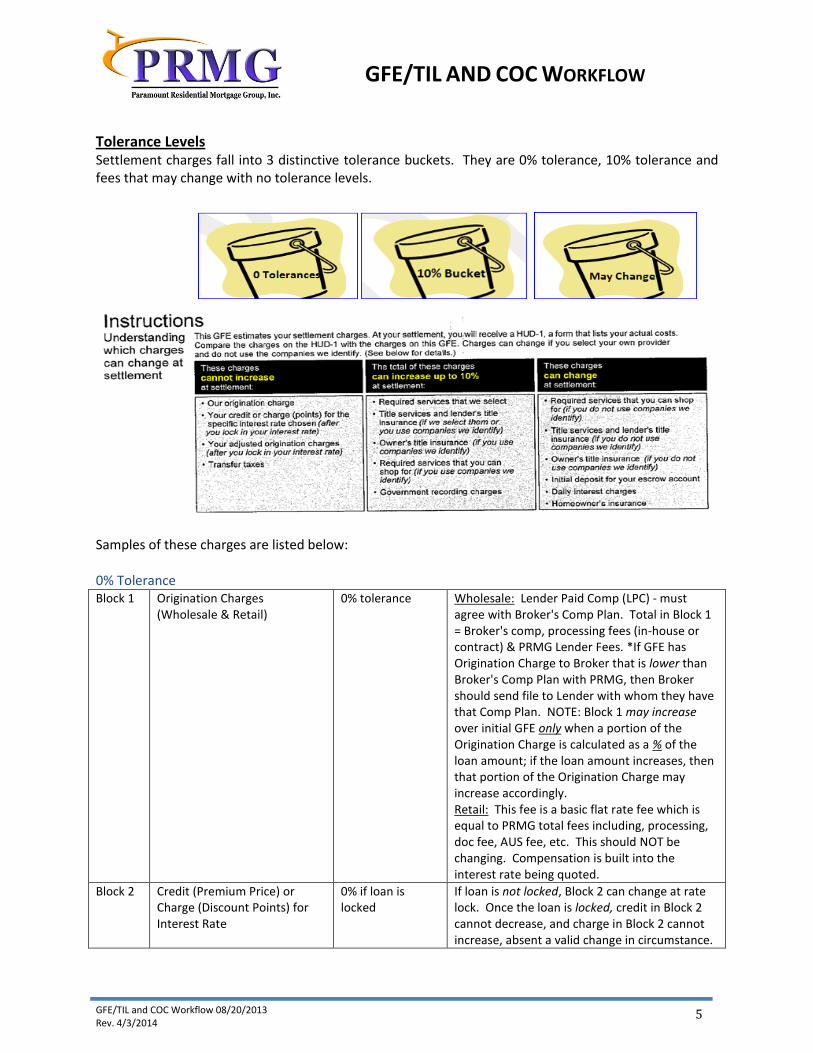

Tolerance Levels Settlement charges fall into 3 distinctive tolerance buckets. They are 0% tolerance, 10% tolerance and fees that may change with no tolerance levels.

Samples of these charges are listed below: 0% Tolerance Block 1 Origination Charges

(Wholesale & Retail) 0% tolerance Wholesale: Lender Paid Comp (LPC) - must

agree with Broker's Comp Plan. Total in Block 1 = Broker's comp, processing fees (in-house or contract) & PRMG Lender Fees. *If GFE has Origination Charge to Broker that is lower than Broker's Comp Plan with PRMG, then Broker should send file to Lender with whom they have that Comp Plan. NOTE: Block 1 may increase over initial GFE only when a portion of the Origination Charge is calculated as a % of the loan amount; if the loan amount increases, then that portion of the Origination Charge may increase accordingly. Retail: This fee is a basic flat rate fee which is equal to PRMG total fees including, processing, doc fee, AUS fee, etc. This should NOT be changing. Compensation is built into the interest rate being quoted.

Block 2 Credit (Premium Price) or Charge (Discount Points) for Interest Rate

0% if loan is locked

If loan is not locked, Block 2 can change at rate lock. Once the loan is locked, credit in Block 2 cannot decrease, and charge in Block 2 cannot increase, absent a valid change in circumstance.

GFE/TIL and COC Workflow 08/20/2013 Rev. 4/3/2014

GFE/TIL AND COC WORKFLOW

6

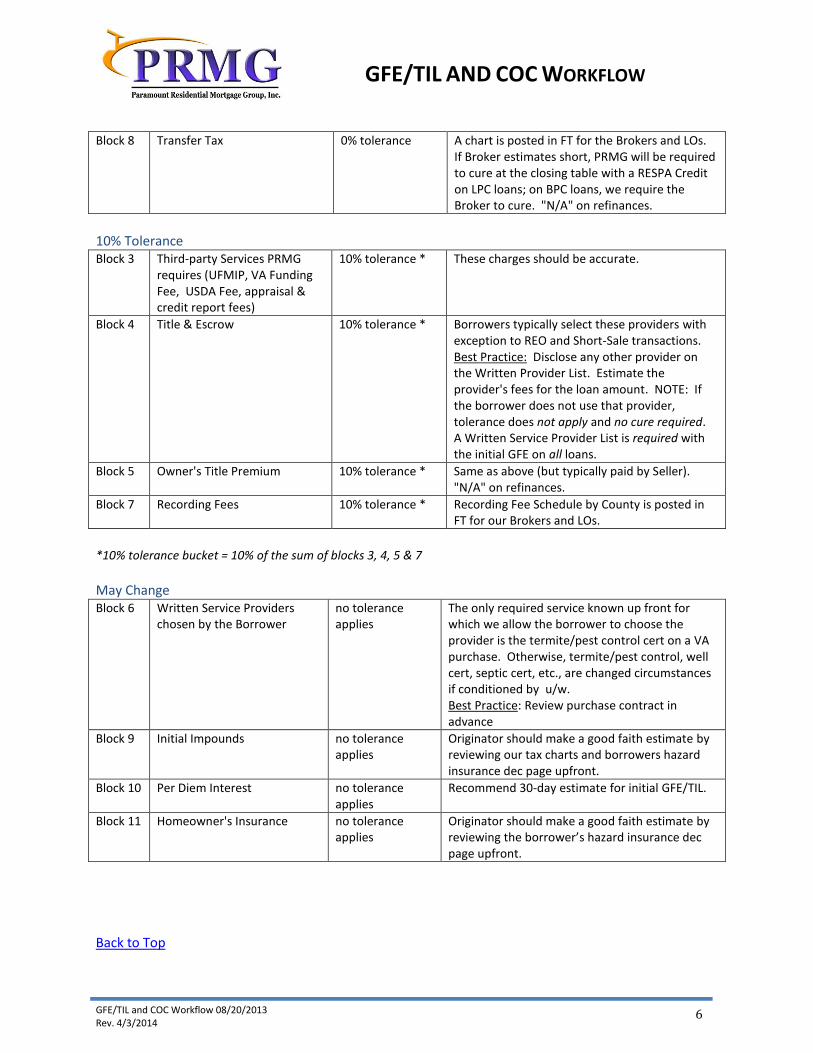

Block 8 Transfer Tax 0% tolerance A chart is posted in FT for the Brokers and LOs. If Broker estimates short, PRMG will be required to cure at the closing table with a RESPA Credit on LPC loans; on BPC loans, we require the Broker to cure. "N/A" on refinances.

10% Tolerance Block 3 Third-party Services PRMG

requires (UFMIP, VA Funding Fee, USDA Fee, appraisal & credit report fees)

10% tolerance * These charges should be accurate.

Block 4 Title & Escrow

10% tolerance * Borrowers typically select these providers with exception to REO and Short-Sale transactions. Best Practice: Disclose any other provider on the Written Provider List. Estimate the provider's fees for the loan amount. NOTE: If the borrower does not use that provider, tolerance does not apply and no cure required. A Written Service Provider List is required with the initial GFE on all loans.

Block 5 Owner's Title Premium 10% tolerance * Same as above (but typically paid by Seller). "N/A" on refinances.

Block 7 Recording Fees 10% tolerance * Recording Fee Schedule by County is posted in FT for our Brokers and LOs.

*10% tolerance bucket = 10% of the sum of blocks 3, 4, 5 & 7

May Change Block 6 Written Service Providers

chosen by the Borrower no tolerance applies

The only required service known up front for which we allow the borrower to choose the provider is the termite/pest control cert on a VA purchase. Otherwise, termite/pest control, well cert, septic cert, etc., are changed circumstances if conditioned by u/w. Best Practice: Review purchase contract in advance

Block 9 Initial Impounds no tolerance applies

Originator should make a good faith estimate by reviewing our tax charts and borrowers hazard insurance dec page upfront.

Block 10 Per Diem Interest no tolerance applies

Recommend 30-day estimate for initial GFE/TIL.

Block 11 Homeowner's Insurance no tolerance applies

Originator should make a good faith estimate by reviewing the borrower’s hazard insurance dec page upfront.

Back to Top

GFE/TIL and COC Workflow 08/20/2013 Rev. 4/3/2014

GFE/TIL AND COC WORKFLOW

7

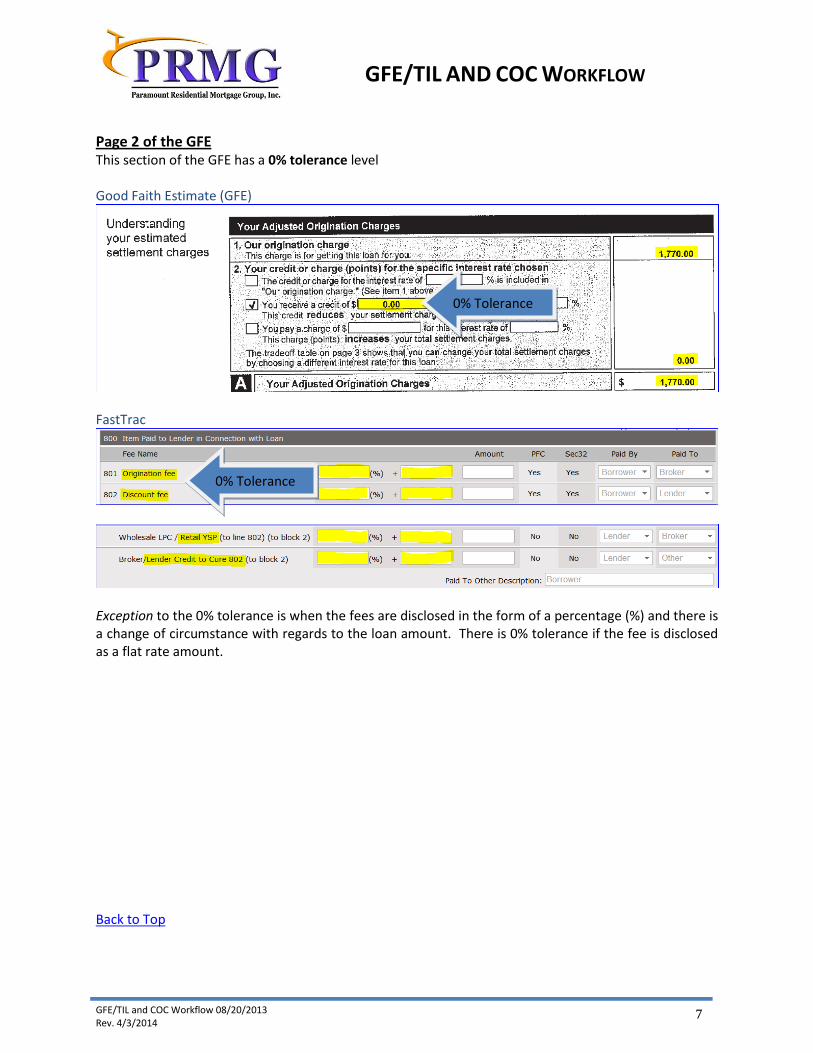

Page 2 of the GFE This section of the GFE has a 0% tolerance level Good Faith Estimate (GFE)

FastTrac

Exception to the 0% tolerance is when the fees are disclosed in the form of a percentage (%) and there is a change of circumstance with regards to the loan amount. There is 0% tolerance if the fee is disclosed as a flat rate amount. Back to Top

0% Tolerance

0% Tolerance

GFE/TIL and COC Workflow 08/20/2013 Rev. 4/3/2014

GFE/TIL AND COC WORKFLOW

8

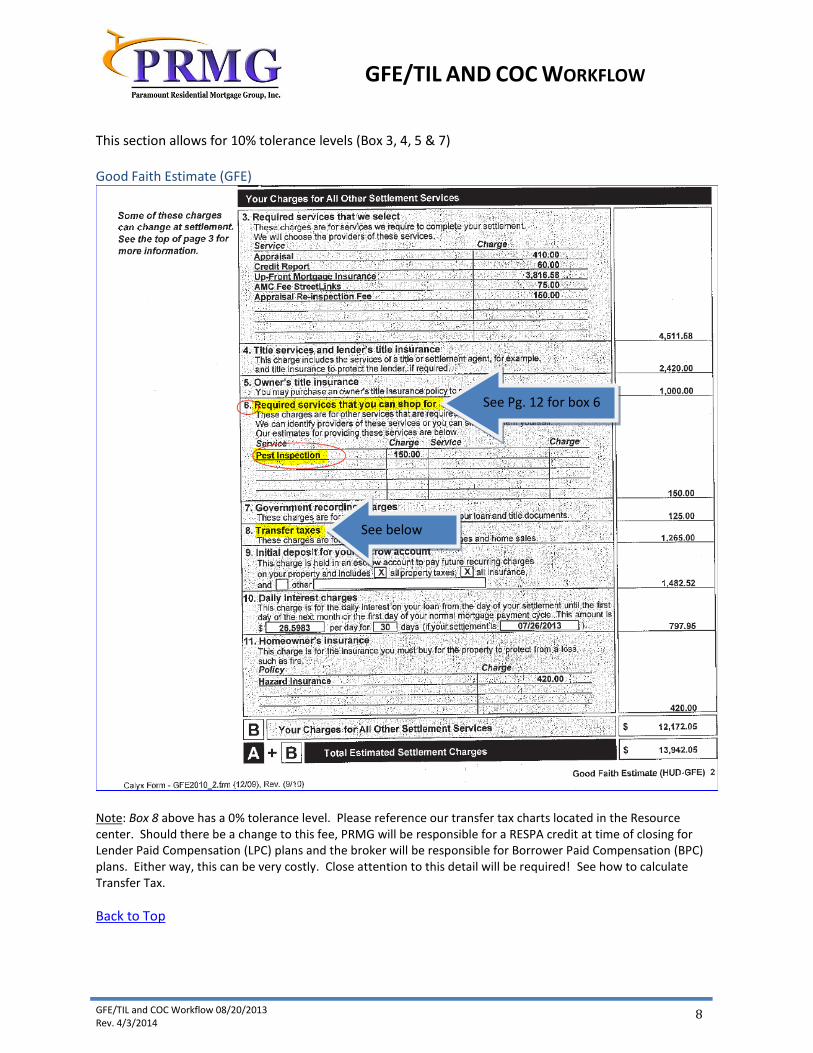

This section allows for 10% tolerance levels (Box 3, 4, 5 & 7) Good Faith Estimate (GFE)

Note: Box 8 above has a 0% tolerance level. Please reference our transfer tax charts located in the Resource center. Should there be a change to this fee, PRMG will be responsible for a RESPA credit at time of closing for Lender Paid Compensation (LPC) plans and the broker will be responsible for Borrower Paid Compensation (BPC) plans. Either way, this can be very costly. Close attention to this detail will be required! See how to calculate Transfer Tax.

Back to Top

See Pg. 12 for box 6

See below note

GFE/TIL and COC Workflow 08/20/2013 Rev. 4/3/2014

GFE/TIL AND COC WORKFLOW

9

FastTrac

Back to Top

10% Tolerance applies

10% Tolerance applies

GFE/TIL and COC Workflow 08/20/2013 Rev. 4/3/2014

GFE/TIL AND COC WORKFLOW

10

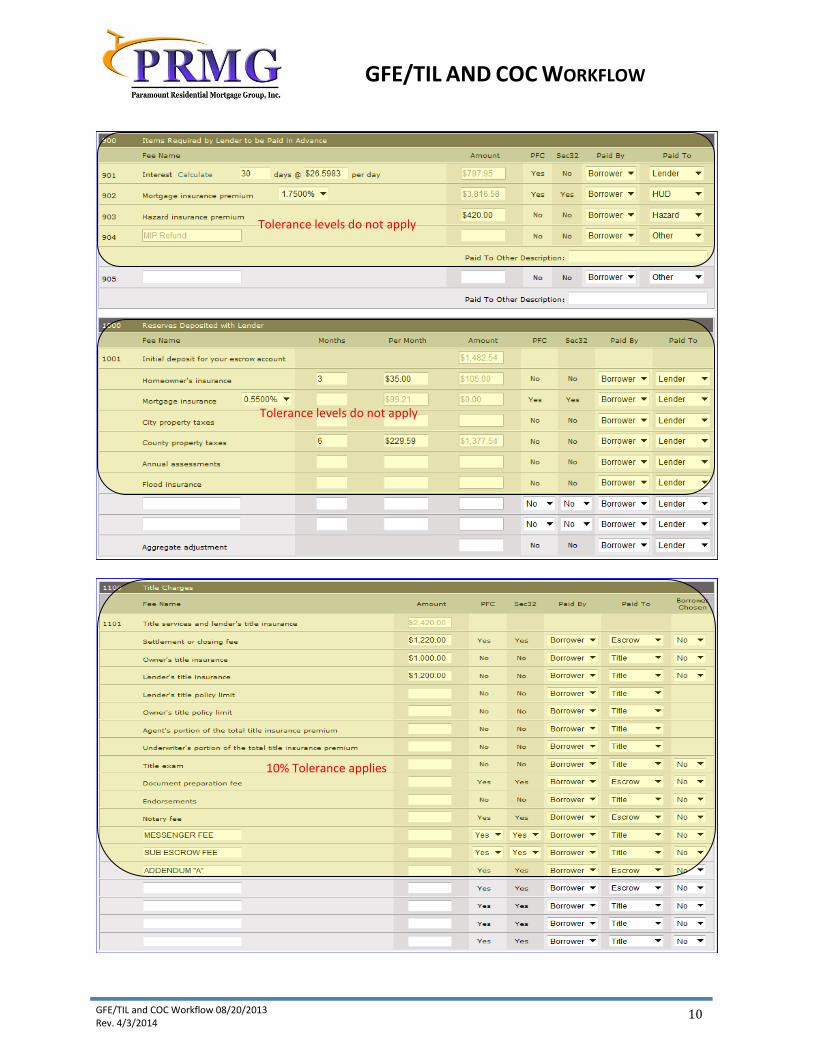

Tolerance levels do not apply

Tolerance levels do not apply

10% Tolerance applies

GFE/TIL and COC Workflow 08/20/2013 Rev. 4/3/2014

GFE/TIL AND COC WORKFLOW

11

Back to Top

Back to Top

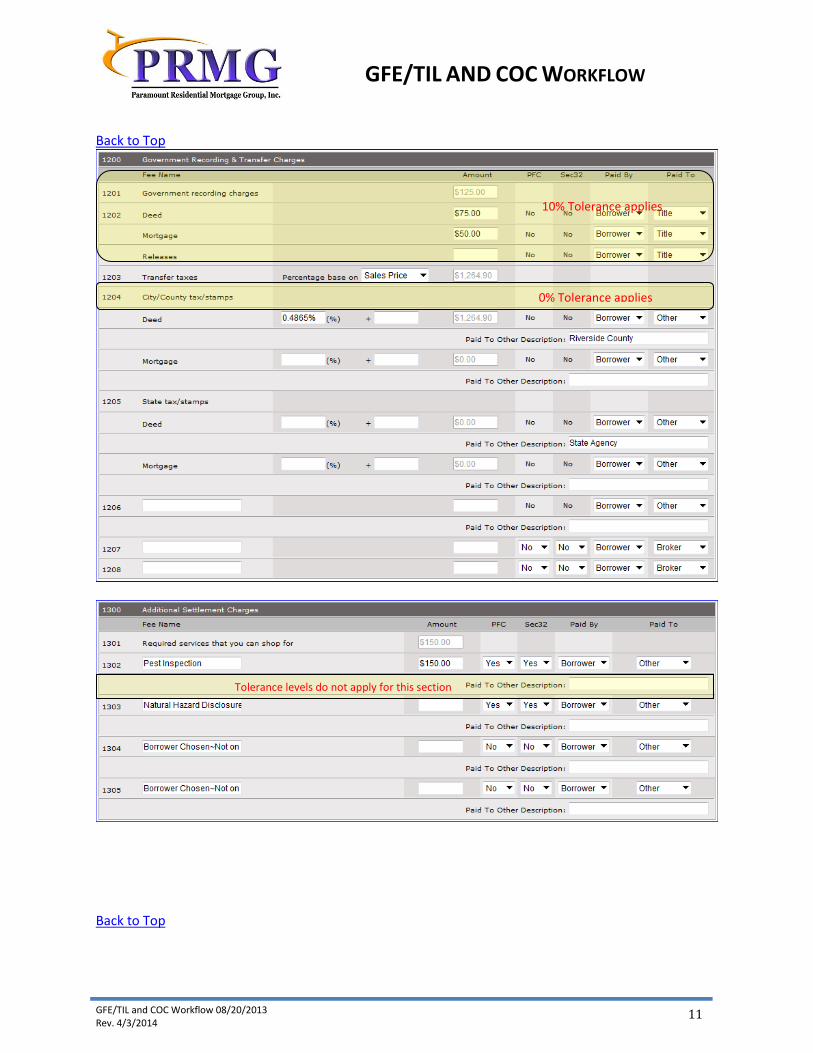

0% Tolerance applies

10% Tolerance applies

Tolerance levels do not apply for this section

GFE/TIL and COC Workflow 08/20/2013 Rev. 4/3/2014

GFE/TIL AND COC WORKFLOW

12

Box 6 of the GFE Written List of Providers Notice box 6 does not have a tolerance level if the borrower choses to go with someone from the Written Providers List. Best practice is to review the purchase contract in advance vs. waiting for an Underwriter to condition the loan for a termite report, well certificate, septic certificate, etc. If the purchase contract and/or the Appraiser calls for it, the Underwriter will also call for it.

Good Faith Estimate (GFE)

FastTrac

Written Providers List

Back to Top

Tolerance levels do not apply if the borrower chooses to use a Provider from the Written Provider list

GFE/TIL and COC Workflow 08/20/2013 Rev. 4/3/2014

GFE/TIL AND COC WORKFLOW

13

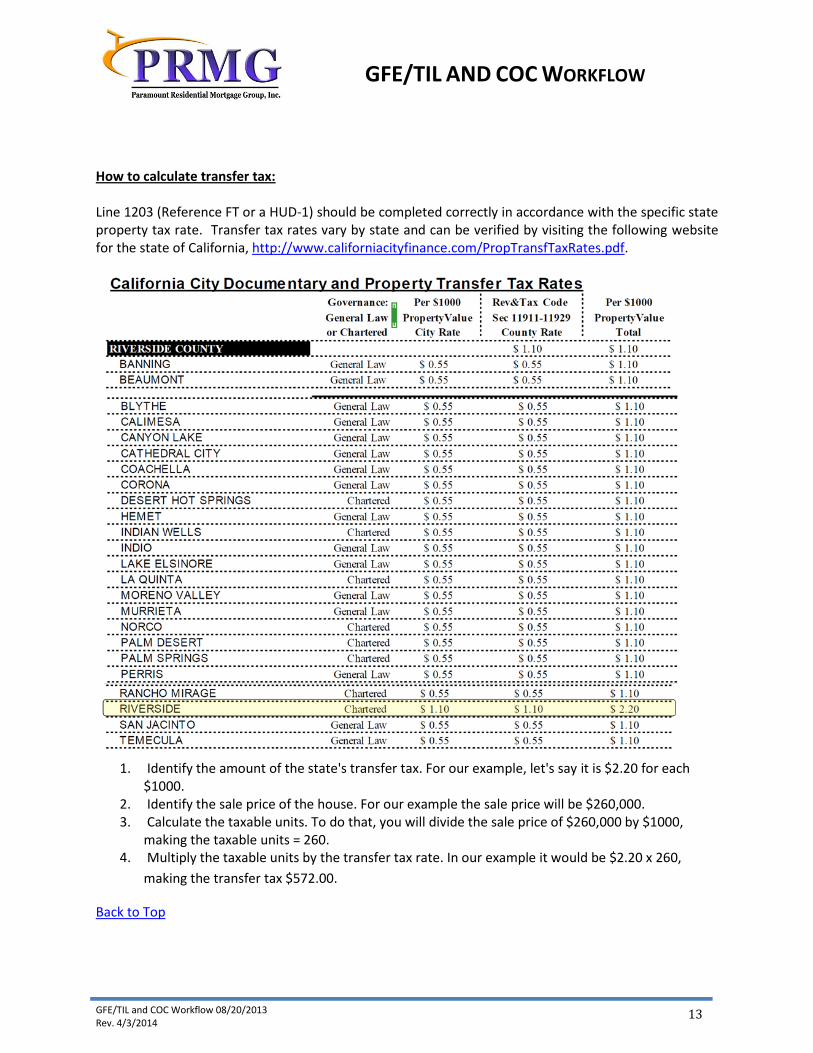

How to calculate transfer tax: Line 1203 (Reference FT or a HUD-1) should be completed correctly in accordance with the specific state property tax rate. Transfer tax rates vary by state and can be verified by visiting the following website for the state of California, http://www.californiacityfinance.com/PropTransfTaxRates.pdf.

1. Identify the amount of the state's transfer tax. For our example, let's say it is $2.20 for each

$1000. 2. Identify the sale price of the house. For our example the sale price will be $260,000. 3. Calculate the taxable units. To do that, you will divide the sale price of $260,000 by $1000,

making the taxable units = 260. 4. Multiply the taxable units by the transfer tax rate. In our example it would be $2.20 x 260,

making the transfer tax $572.00.

Back to Top

GFE/TIL and COC Workflow 08/20/2013 Rev. 4/3/2014

GFE/TIL AND COC WORKFLOW

14

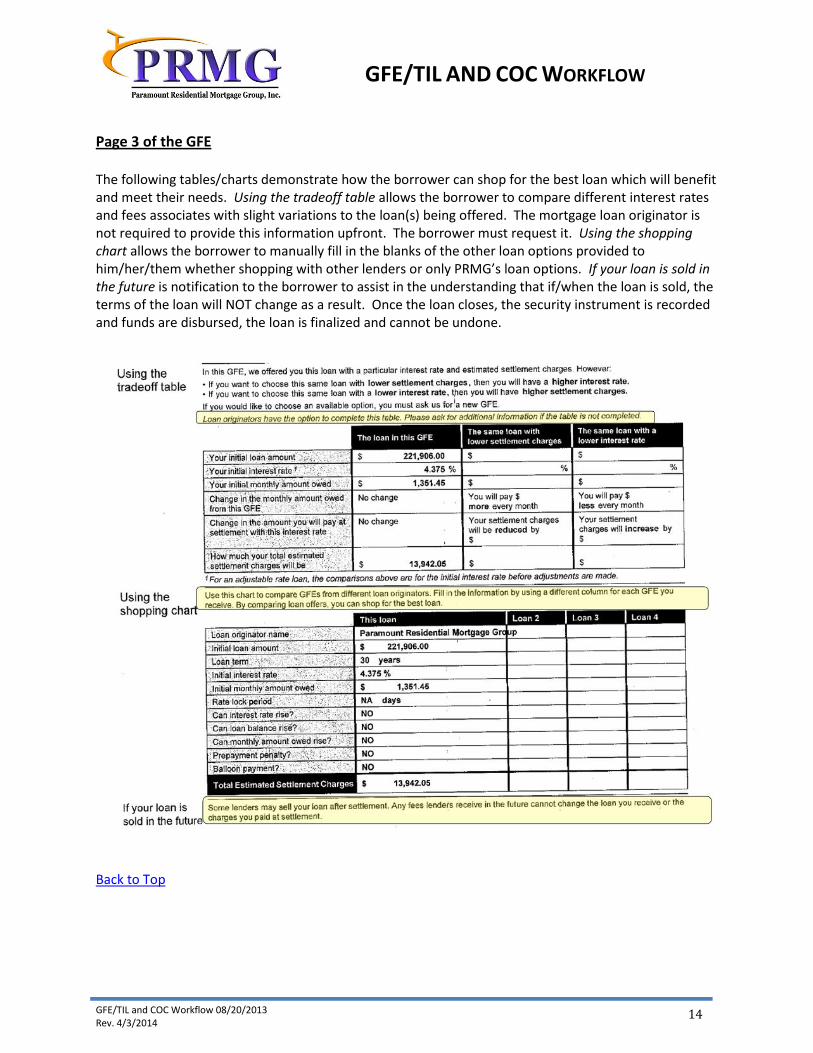

Page 3 of the GFE The following tables/charts demonstrate how the borrower can shop for the best loan which will benefit and meet their needs. Using the tradeoff table allows the borrower to compare different interest rates and fees associates with slight variations to the loan(s) being offered. The mortgage loan originator is not required to provide this information upfront. The borrower must request it. Using the shopping chart allows the borrower to manually fill in the blanks of the other loan options provided to him/her/them whether shopping with other lenders or only PRMG’s loan options. If your loan is sold in the future is notification to the borrower to assist in the understanding that if/when the loan is sold, the terms of the loan will NOT change as a result. Once the loan closes, the security instrument is recorded and funds are disbursed, the loan is finalized and cannot be undone.

Back to Top

GFE/TIL and COC Workflow 08/20/2013 Rev. 4/3/2014

GFE/TIL AND COC WORKFLOW

15

Events Triggering Re-disclosure There are certain events that will trigger a loans requirement to be redisclosed.

1. Change of Circumstance (COC) 2. Locked interest rate 3. TIL APR increases > .125% from previous TIL APR

1. Changed Circumstance

a. Definition of changed circumstance: i. Act of God or other emergency

ii. Information regarding the borrower or the loan on which the originator relied in providing the GFE that changes or is later found to be inaccurate

iii. New information regarding the borrower or the loan

b. Examples of what may be considered to be a changed circumstance: i. Interest rate lock

ii. Appraisal comes in low and PMI must be added iii. PMI program changes after loan was originated iv. Borrower’s credit score drops v. Appraisal triggers pricing adjustment for lower LTV, or lower LTV combined

with FICO vi. Borrower requests a change in the loan amount, loan program or terms

vii. Loan is flipped from Conventional to FHA, requiring UFMIP viii. Escrow waiver (from impounds) is added

ix. Property usage changes (e.g., from OO to NOO) x. VA entitlement previously used (not known at loan origination or evident in

the application package/credit report) xi. The underwriter conditions for a service not previously listed in Block 6

(e.g., pest cert, well cert, septic cert, roof cert, etc.) xii. Lock extension(s):

Seller delays approval on short sale

Appraisal identifies repairs that are not completed on time

Borrower delays submission of approval conditions

Escrow or settlement agent delays the loan closing

Note: A loan may be flipped to BPC to LPC, and vice versa, at any time during the process, provided the amount in Block 1 does not increase. This does not necessarily trigger a changed circumstance or revised GFE.

c. Not a changed circumstance:

i. Oops! ii. Errors on the initial (or a subsequent) GFE

iii. GFE issued on a TBD property, and a property address is later identified iv. Omission or error in amount of UFMIP or VA Funding Fee v. PRMG delays, busy or otherwise

Back to Top

GFE/TIL and COC Workflow 08/20/2013 Rev. 4/3/2014

GFE/TIL AND COC WORKFLOW

16

2. Interest Rate Lock

a. GFE i. A revised GFE must be issued to the borrower, even if the loan terms,

interest rate and fees are unchanged from the initial GFE, within three business days of the lock date

“Business Days” for this purpose excludes Saturdays, Sundays and legal holidays

Wholesale: The Broker may issue the locked GFE o If the rate is locked prior to submission to PRMG, then the

locked GFE should be included in the submission package o If the rate was locked more than three business days prior

to PRMG’s receipt of the application, then the Broker was required to issue it

ii. The re-issuance of a locked HUD requirement, because the interest rate expiration date in Line 2 of the GFE will change, and we must inform the borrower of the date by which the loan must close

iii. Complete a Changed Circumstance form for initial interest rate lock iv. The loan cannot go to docs for at least one business day after a revised GFE

is delivered to the borrower:

Cannot go to docs same day a revised GFE is issued, even if will be signed on a later date

The last (final) GFE must be dated prior to the Note date

Encourage brokers and retail loan originators to supply borrowers’ email addresses

Mail delivery stretches that one business day to three

3. TIL APR increases by more than .125% a. If the APR increases by more than 0.125% over the initial APR or last disclosed TIL, a

revised TIL must be given along with the GFE -- within three business days of the change date

TIL must include an Itemization of Amount Financed

Mail delivery stretches the three-day wait period to six business days

The 0.125% tolerance in the APR applies to both ARMs and Fixed-rate loans

Setting the per diem interest to 30 days at loan opening will buffer the initial APR

i. Adjust the per diem interest to the number of days

Lock expiration date, or

Date the loan is expected to close (e.g., the last business day of the month)

ii. Whenever there is a change in the loan terms that increases the APR by more than 0.125% over the APR in the last disclosed TIL, a new GFE and TIL need to go to the borrower – because the loan term that spiked the increase in the APR is likely the interest rate or a fee, which also must be disclosed in the GFE.

Back to Top

GFE/TIL and COC Workflow 08/20/2013 Rev. 4/3/2014

GFE/TIL AND COC WORKFLOW

17

iii. The loan cannot go to docs for at least three business days after a revised TIL is delivered to the borrower.

Issue your revised GFE/TIL the same day that the change (lock) takes place

Waiting three business days from the rate lock or changed circumstance date to deliver revised GFE/TIL may delay closing

If the disclosures are mailed out to the borrower then the waiting period becomes 6 business days rather than 3 business days.

Back to Top

GFE/TIL and COC Workflow 08/20/2013 Rev. 4/3/2014

GFE/TIL AND COC WORKFLOW

18

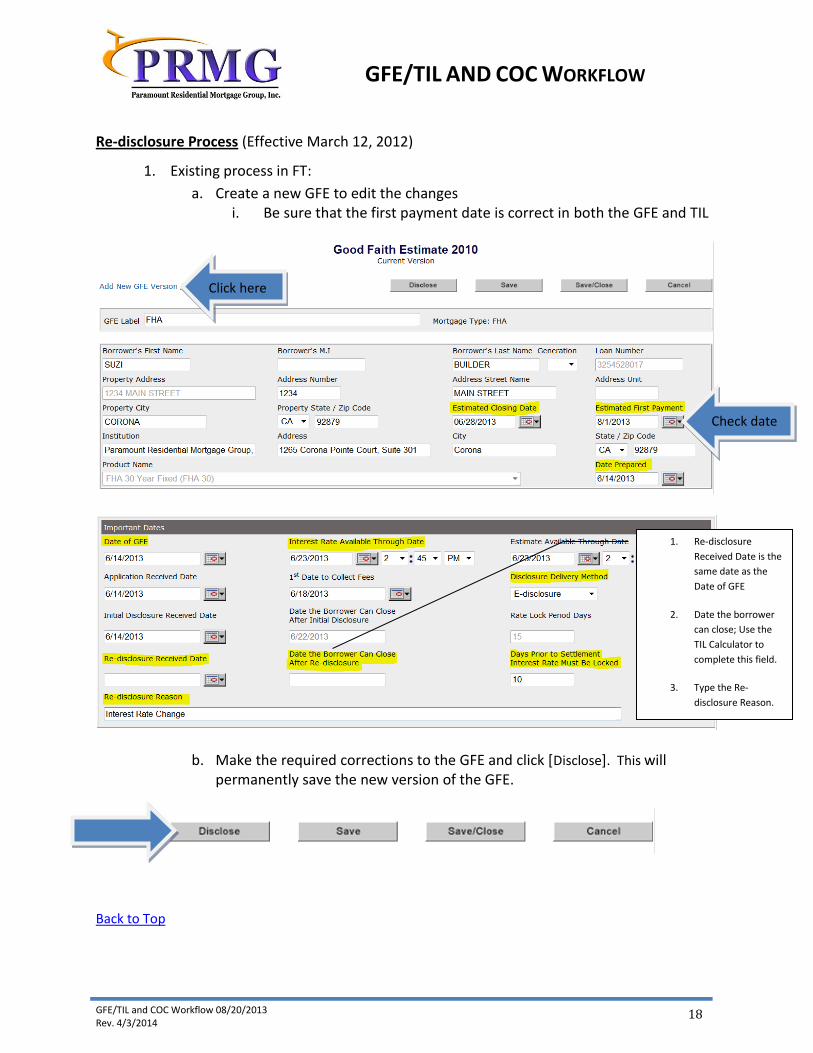

Re-disclosure Process (Effective March 12, 2012)

1. Existing process in FT:

a. Create a new GFE to edit the changes i. Be sure that the first payment date is correct in both the GFE and TIL

b. Make the required corrections to the GFE and click [Disclose]. This will permanently save the new version of the GFE.

Back to Top

1. Re-disclosure

Received Date is the

same date as the

Date of GFE

2. Date the borrower

can close; Use the

TIL Calculator to

complete this field.

3. Type the Re-

disclosure Reason.

Check date

Click here

GFE/TIL and COC Workflow 08/20/2013 Rev. 4/3/2014

GFE/TIL AND COC WORKFLOW

19

Using the TIL Calculator Every loan is required to include a completed copy of this calculator. Instructions are included on the form, but the basic overview includes the following: A loan may not close within a set period of time after it was originally or subsequently re-disclosed to the borrower. The borrower must have sufficient time to review the cost of a loan and decide if they are comfortable moving forward. Adhering to the Federal Government’s Regulatory waiting period(s) is/are appropriate for the consumer and required by law. Fields indicated in Green on the form are editable fields that will include criteria specific to the individual loan being worked on. They are the Accurate Business Day field (PRMG is not open for business on Saturday, so this will always be “2”), Application Date field (from the signature page of the 1003), Early Disclosure Date field (from the date of the initial GFE), and the Re-disclosure Date field (required only if the Annual Percentage Rate (APR) shown on page 1, box 1 of the Re-Disclosed TIL has increased by more than .125% from the initial TIL on the date of the Change of Circumstance). Date fields are input in the following format xx/xx/xxxx. Once input correctly, they will produce the dates in the boxes beneath them after which the applicable activities can happen. Read the form screen shot below for more details.

Back to Top

GFE/TIL and COC Workflow 08/20/2013 Rev. 4/3/2014

GFE/TIL AND COC WORKFLOW

20

Calculating the TIL and re-disclosing To keep up with compliance, the TIL must be recalculated to ensure there is no increase of more than .125% to the APR as an increase requires re-disclosure of the GFE/TIL to the borrower. Most of the information will auto-populate from the GFE screen. Ensure accuracy by reviewing each section and update accordingly. Click on [Calculate]. The TIL has been re-calculated. Click on [Save/Close].

2. Click on [Re-disclosure - DocMagic] in FastTrac menu

Note: This is ONLY a portal used for submitting the re-disclosure request to DocMagic. When

processed, an internal re-disclosure package will be returned to FastTrac. Prior to submitting a re-

disclosure request, follow the above referenced outline and create a new GFE with the changes in the

FastTrac GFE screen, DISCLOSE the new version of the GFE, then open and calculate the TIL screen.

Back to Top

Check Date

GFE/TIL and COC Workflow 08/20/2013 Rev. 4/3/2014

GFE/TIL AND COC WORKFLOW

21

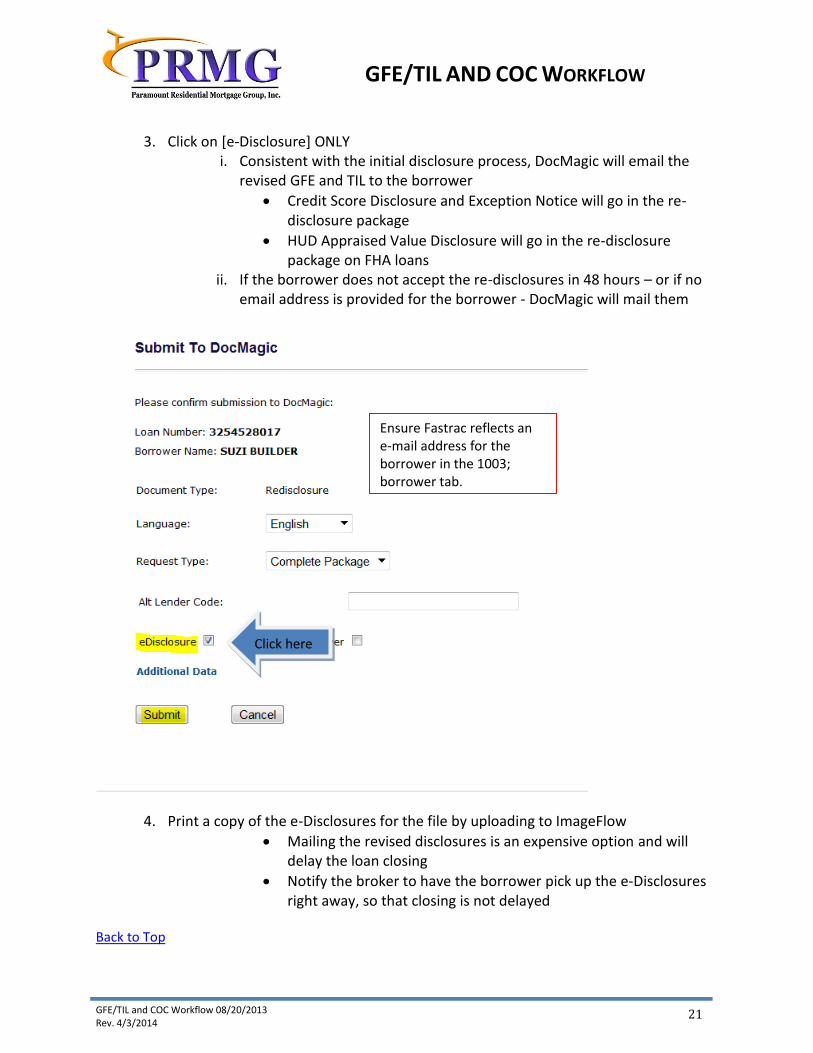

3. Click on [e-Disclosure] ONLY i. Consistent with the initial disclosure process, DocMagic will email the

revised GFE and TIL to the borrower

Credit Score Disclosure and Exception Notice will go in the re-disclosure package

HUD Appraised Value Disclosure will go in the re-disclosure package on FHA loans

ii. If the borrower does not accept the re-disclosures in 48 hours – or if no email address is provided for the borrower - DocMagic will mail them

4. Print a copy of the e-Disclosures for the file by uploading to ImageFlow

Mailing the revised disclosures is an expensive option and will delay the loan closing

Notify the broker to have the borrower pick up the e-Disclosures right away, so that closing is not delayed

Back to Top

Click here

Ensure Fastrac reflects an e-mail address for the borrower in the 1003; borrower tab.

GFE/TIL and COC Workflow 08/20/2013 Rev. 4/3/2014

GFE/TIL AND COC WORKFLOW

22

5. New Flood Certification Process

1. Flood Cert

a. DocMagic will return the life-of-loan Flood Cert in our re-disclosure package

b. Flood Cert should print out with the GFE and TIL for the file

2. Flood Notice to Borrower a. DocMagic will include the Flood Notice to the borrower with the GFE and TIL,

if the property is in a special flood hazard area

b. We are required to notify the borrower if the property is in a special flood hazard zone within a reasonable time – which is generally defined as three business days -- prior to docs/closing

6. Florida and other flood-prone areas:

If you need to get the Flood Notice out to the borrower sooner for purposes of procuring flood insurance coverage:

a. Click on www.freeflood.net (free website)

iv. This website will indicate the flood zone in which the property is located, but it will not give you a Flood Cert

v. The appraisal may indicate that the property is in a special flood hazard area, but the appraisal generally is not deemed to be a reliable source for flood zone data

b. Send manual Notice to Borrower of Property in Special Flood Hazard Area

c. On refinances where the borrower already has flood coverage in place, the timing (i.e., ten days prior to closing) is not as critical

d. On purchases, it is more critical that we notify the borrower that the property is in a flood hazard zone in order to give the borrower time to:

vi. Procure flood insurance coverage, or vii. Cancel the purchase transaction

e. When you submit re-disclosures to DocMagic at a later date, you will get the

Flood Cert, and DocMagic will send another Flood Notice to the borrower. Back to Top