IRS/Actuary Actuary’s Perspective by Alan E. Kaliski, FCAS, MAAA.

Upload

derrick-doyleCategory

view

230download

0

Generalized Minimum Bias Models

By

Luyang Fu, Ph. D.

Cheng-sheng Peter Wu, FCAS, ASA, MAAA

Agenda

History and Overview of Minimum Bias Method

Generalized Minimum Bias Models

Conclusions

Mildenhall’s Discussion and Our Responses

Q&A

History on Minimum Bias

A technique with long history for actuaries: – Bailey and Simon (1960)– Bailey (1963)– Brown (1988)– Feldblum and Brosius (2002)– In the Exam 9.

Concepts:– Derive multivariate class plan parameters by minimizing a

specified “bias” function

– Use an “iterative” method in finding the parameters

History on Minimum Bias

Various bias functions proposed in the past for minimization

Examples of multiplicative bias functions proposed in the past:

ji jiji

jijiji

jijijiji

jijijiji

yxw

yxrwBiasSquaredChi

yxrwBiasSquared

yxrwBiasBalanced

, ,

2,,

2

,,,

,,,

)(

)(

)(

History on Minimum Bias

Then, how to determine the class plan parameters by minimizing the bias function?

One simple way is the commonly used “iterative” method for root finding:

– Start with a random guess for the values of xi and yj

– Calculate the next set of values for xi and yj using the root finding formula for the bias function

– Repeat the steps until the values converge

Easy to understand and can program in almost any tools

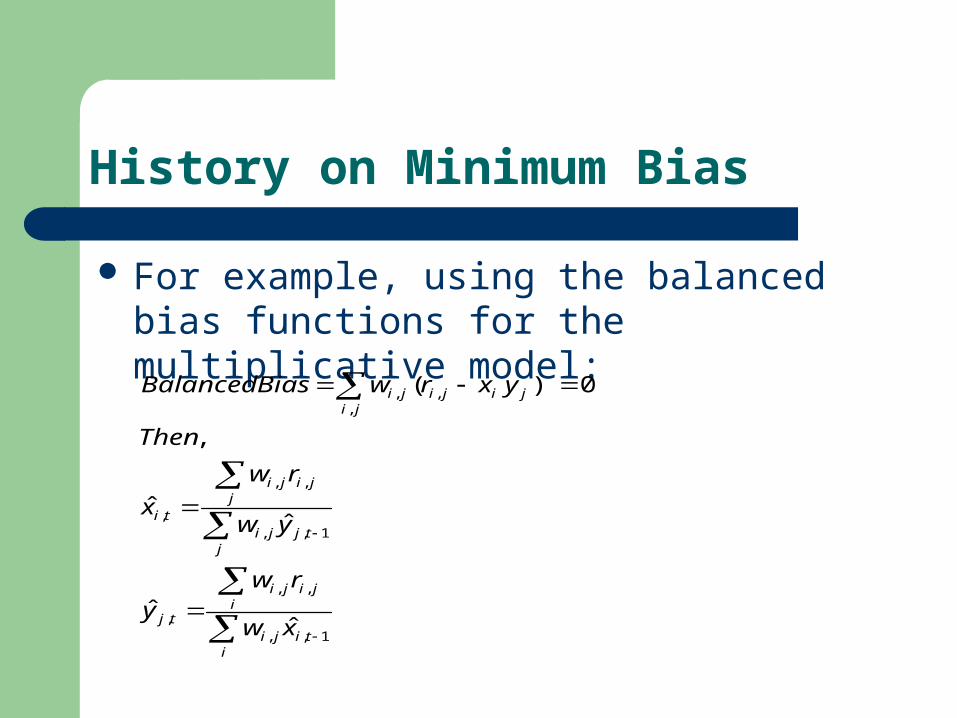

History on Minimum Bias

For example, using the balanced bias functions for the multiplicative model:

itiji

ijiji

tj

jtjji

jjiji

ti

jijijiji

xw

rwy

yw

rw

x

Then

yxrwBiasBalanced

1,,

,,

,

1,,

,,

,

,,,

ˆˆ

ˆˆ

,

0)(

History on Minimum Bias

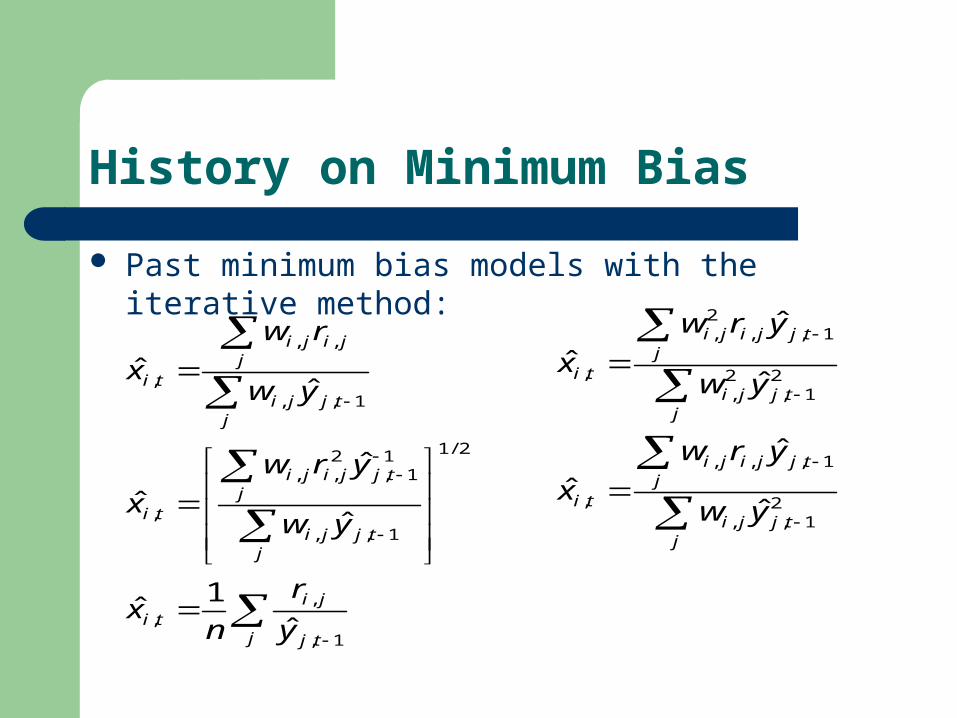

Past minimum bias models with the iterative method:

j tj

jiti

jtjji

jtjjiji

ti

jtjji

jjiji

ti

y

r

nx

yw

yrw

x

yw

rw

x

1,

,,

2/1

1,,

11,

2,,

,

1,,

,,

,

ˆ1

ˆ

ˆ

ˆ

ˆ

ˆˆ

jtjji

jtjjiji

ti

jtjji

jtjjiji

ti

yw

yrw

x

yw

yrw

x

21,,

1,,,

,

21,

2,

1,,2,

,

ˆ

ˆ

ˆ

ˆ

ˆ

ˆ

Issues with the Iterative Method

Two questions regarding the “iterative” method:– How do we know that it will converge?– How fast/efficient that it will converge?

Answers:– Numerical Analysis or Optimization textbooks– Mildenhall (1999)

Efficiency is a less important issue due to the modern computation power

Other Issues with Minimum Bias

What is the statistical meaning behind these models?

More models to try?Which models to choose?

Summary on Minimum Bias

A non-statistical approachBest answers when bias functions are

minimized Use of “iterative” method for root finding

in determining parametersEasy to understand and can program in

many tools

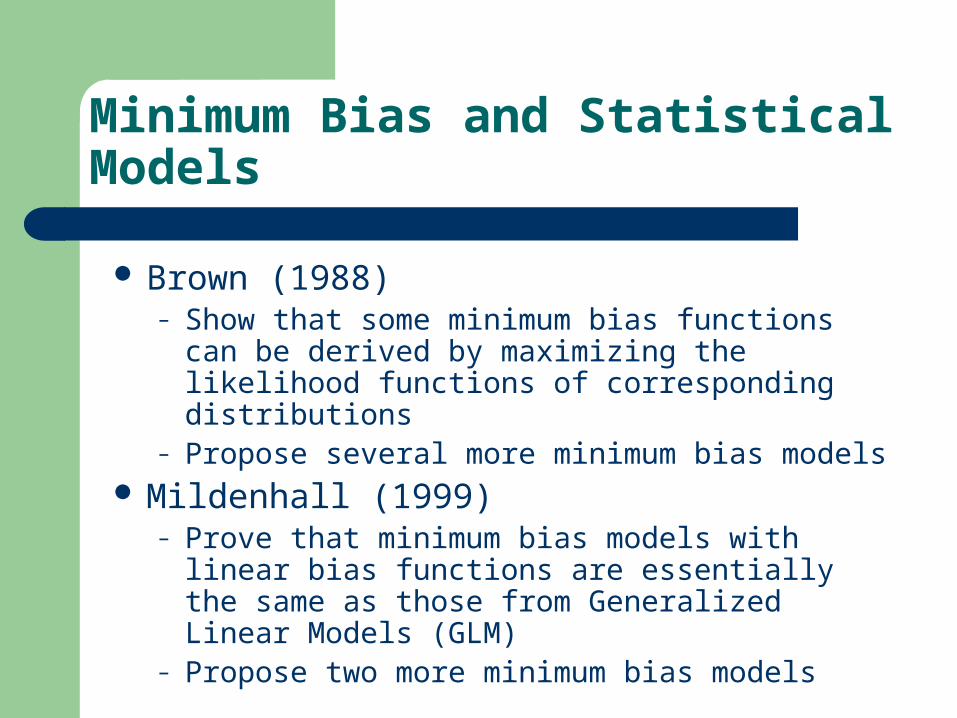

Minimum Bias and Statistical Models

Brown (1988) – Show that some minimum bias functions can be

derived by maximizing the likelihood functions of corresponding distributions

– Propose several more minimum bias models Mildenhall (1999)

– Prove that minimum bias models with linear bias functions are essentially the same as those from Generalized Linear Models (GLM)

– Propose two more minimum bias models

Minimum Bias and Statistical Models

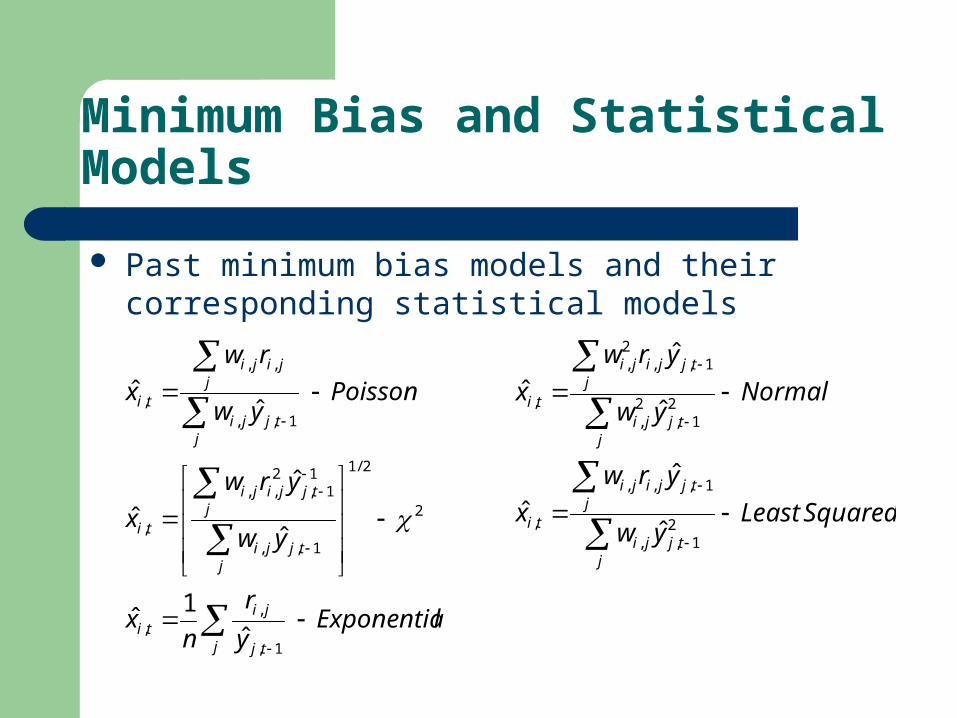

Past minimum bias models and their corresponding statistical models

lExponentiay

r

nx

yw

yrw

x

Poissonyw

rw

x

j tj

jiti

jtjji

jtjjiji

ti

jtjji

jjiji

ti

ˆ

1ˆ

ˆ

ˆ

ˆ

ˆ

ˆ

1,

,,

2

2/1

1,,

11,

2,,

,

1,,

,,

,

SquaredLeastyw

yrw

x

Normalyw

yrw

x

jtjji

jtjjiji

ti

jtjji

jtjjiji

ti

ˆ

ˆ

ˆ

ˆ

ˆ

ˆ

21,,

1,,,

,

21,

2,

1,,2,

,

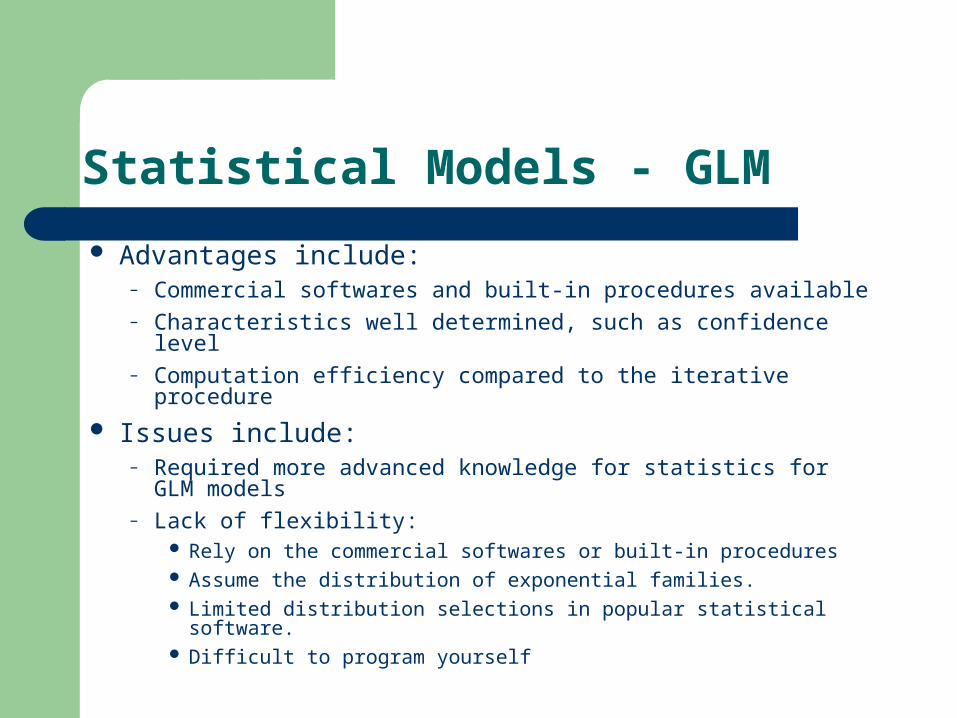

Statistical Models - GLM

Advantages include:– Commercial softwares and built-in procedures available– Characteristics well determined, such as confidence level– Computation efficiency compared to the iterative procedure

Issues include:– Required more advanced knowledge for statistics for GLM

models– Lack of flexibility:

Rely on the commercial softwares or built-in procedures Assume the distribution of exponential families. Limited distribution selections in popular statistical software. Difficult to program yourself

Motivations for Generalized Minimum Bias Models

Can we unify all the past minimum bias models?

Can we completely represent the wide range of GLM and statistical models using Minimum Bias Models?

Can we expand the model selection options that go beyond all the currently used GLM and minimum bias models?

Can we improve the efficiency of the iterative method?

Generalized Minimum Bias Models

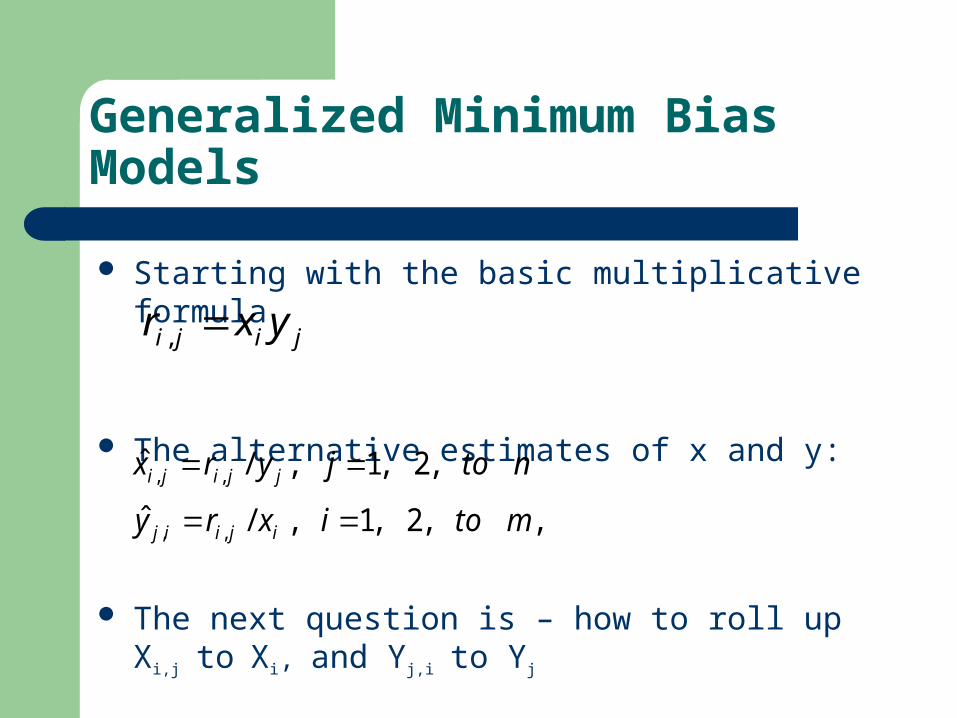

Starting with the basic multiplicative formula

The alternative estimates of x and y:

The next question is – how to roll up Xi,j to Xi, and Yj,i

to Yj

jiji yxr ,

,,2,1,/ˆ

,2,1,/ˆ

,,

,,

mtoixry

ntojyrx

ijiij

jjiji

Possible Weighting Functions

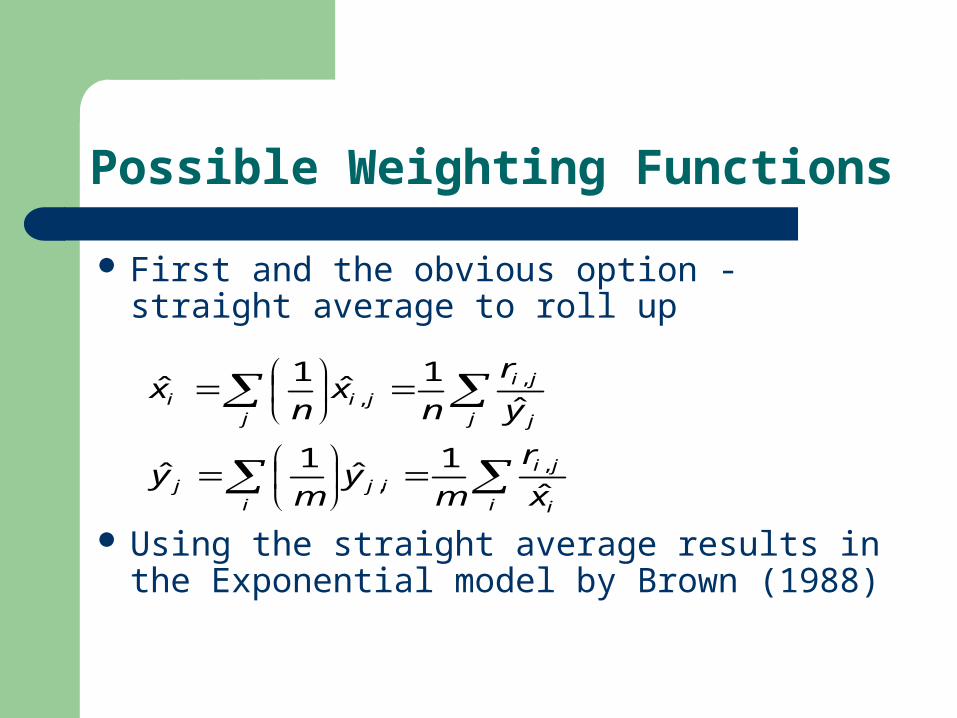

First and the obvious option - straight average to roll up

Using the straight average results in the Exponential model by Brown (1988)

i i

jiij

ij

j j

jiji

ji

x

r

my

my

y

r

nx

nx

ˆ1

ˆ1

ˆ

ˆ1

ˆ1

ˆ

,,

,,

Possible Weighting Functions

Another option is to use the relativity-adjusted exposure as weight function

This is Bailey (1963) model, or Poisson model by Brown (1988).

iiji

ijiji

i

ji

ii

iji

ijiij

ii

iji

ijij

jjji

jjiji

j

ji

jj

jji

jjiji

jj

jji

jjii

xw

rw

x

r

xw

xwy

xw

xwy

yw

rw

y

r

yw

ywx

yw

ywx

ˆˆˆ

ˆˆ

ˆ

ˆˆ

ˆˆˆ

ˆˆ

ˆ

ˆˆ

,

,,,

,

,,

,

,

,

,,,

,

,,

,

,

Possible Weighting Functions

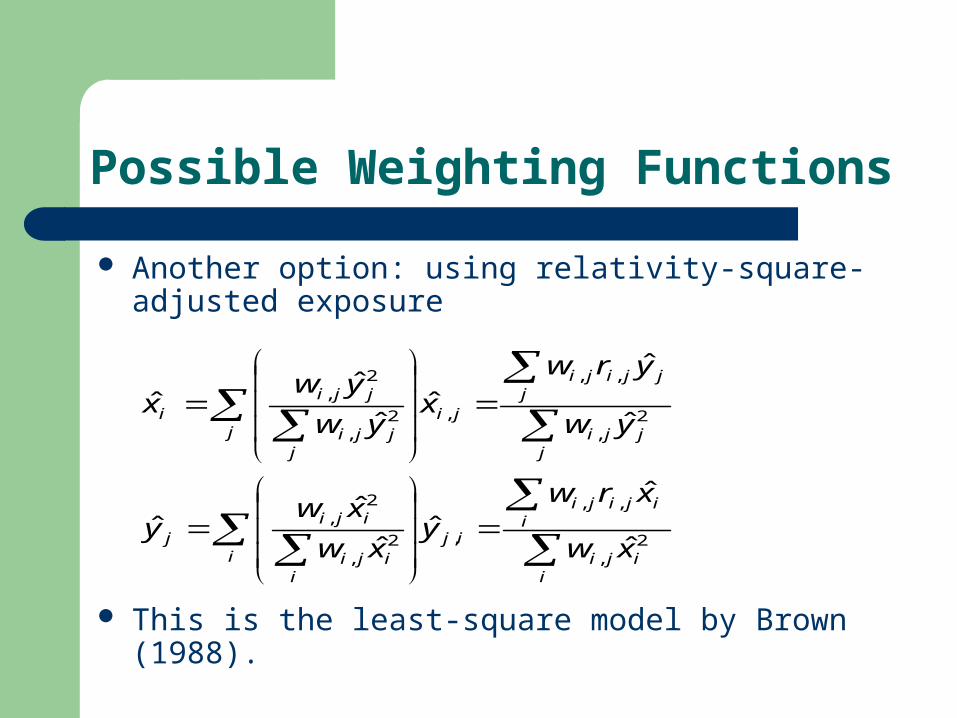

Another option: using the square of relativity-adjusted exposure

This is the normal model by Brown (1988).

iiji

iijiji

iji

iiji

ijij

jjji

jjjiji

jij

jjji

jjii

xw

xrwy

xw

xwy

yw

yrw

xyw

ywx

22,

,2,

,22,

22,

22,

,2,

,22,

22,

ˆ

ˆˆ

ˆ

ˆˆ

ˆ

ˆ

ˆˆ

ˆˆ

Possible Weighting Functions

Another option: using relativity-square-adjusted exposure

This is the least-square model by Brown (1988).

iiji

iijiji

iji

iiji

ijij

jjji

jjjiji

jij

jjji

jjii

xw

xrwy

xw

xwy

yw

yrw

xyw

ywx

2,

,,

,2,

2,

2,

,,

,2,

2,

ˆ

ˆˆ

ˆ

ˆˆ

ˆ

ˆ

ˆˆ

ˆˆ

Generalized Minimum Bias Models

So, the key for generalization is to apply different “weighting functions” to roll up Xi,j to Xi and Yj,i to Yj

Propose a general weighting function of two factors, exposure and relativity:WpXq and WpYq

Almost all published to date minimum bias models are special cases of GMBM(p,q)

Also, there are more modeling options to choose since there is no limitation, in theory, on (p,q) values to try in fitting data – comprehensive and flexible

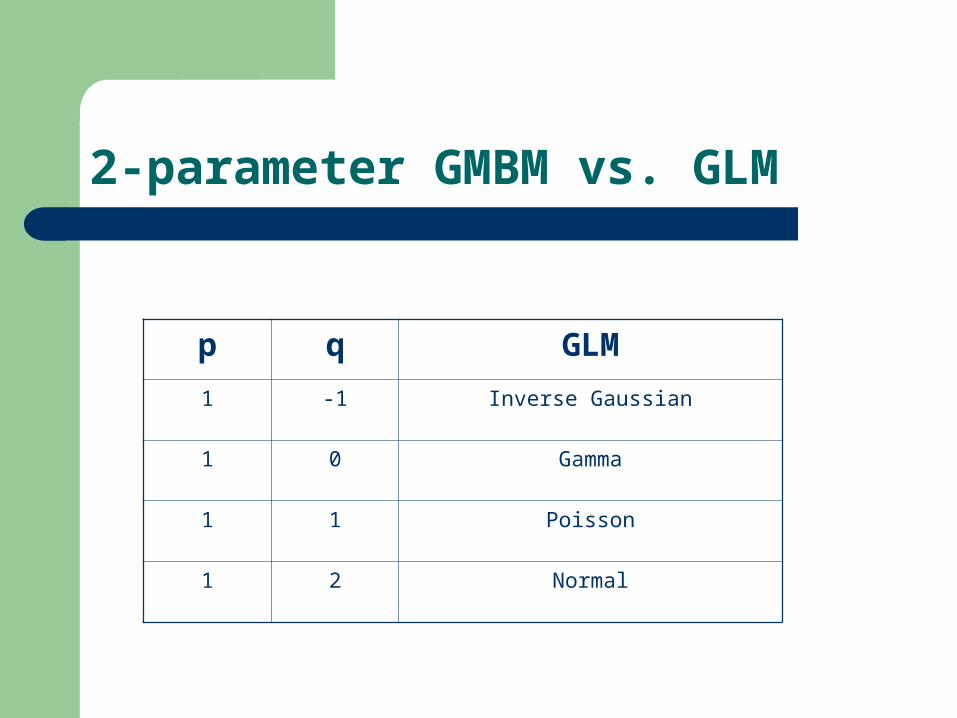

2-parameter GMBM

2-parameter GMBM with exposure and relativity adjusted weighting function are:

i

qi

pji

i

qiji

pji

iji

i

qi

pji

qi

pji

j

j

qj

pji

j

qjji

pji

jij

j

qj

pji

qj

pji

i

xw

xrwy

xw

xwy

yw

yrw

xyw

ywx

1,

1,,

,,

,

,

1,,

,,

,

ˆ

ˆˆ

ˆ

ˆˆ

ˆ

ˆ

ˆˆ

ˆˆ

2-parameter GMBM vs. GLM

p q GLM

1 -1 Inverse Gaussian

1 0 Gamma

1 1 Poisson

1 2 Normal

2-parameter GMBM and GLM

GMBM with p=1 is the same as GLM model with the variance function of

Additional special models:– 0<q<1, the distribution is Tweedie, for pure premium models– 1<q<2, not exponential family– -1<q<0, the distribution is between gamma and inverse

Gaussian After years of technical development in GLM and

minimum bias, at the end of day, all of these models are connected through the game of “weighted average”.

qV 2)(

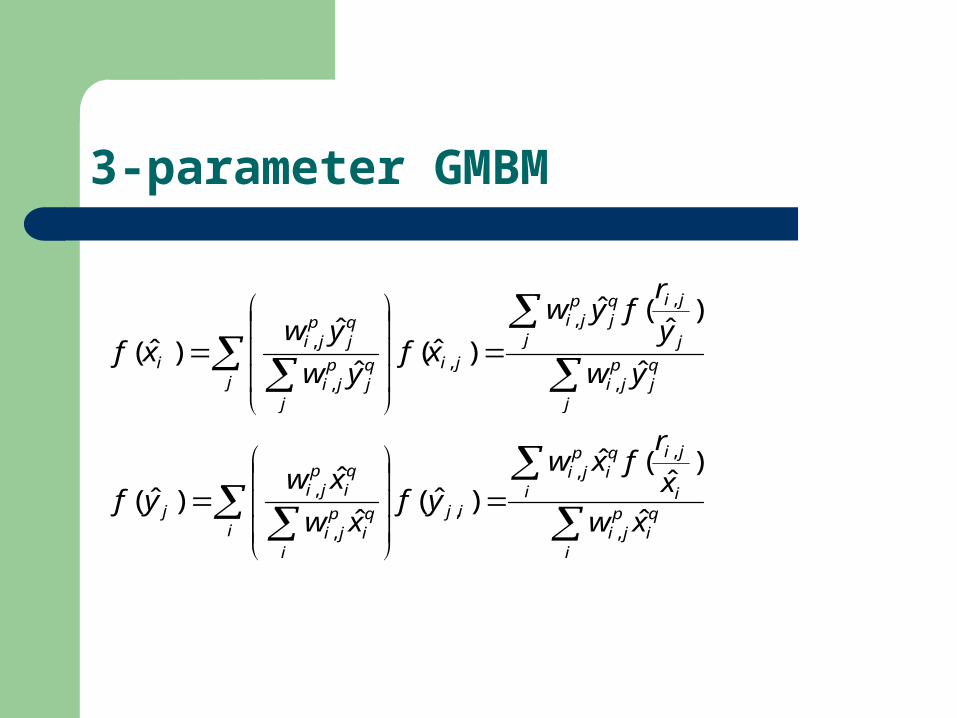

3-parameter GMBM

One model published to date not covered by the 2-parameter GMBM: Chi-squared model by Bailey and Simon (1960)

Further generalization using a similar concept of link function in GLM, f(x) and f(y)

Estimate f(x) and f(y) through the iterative method

Calculate x and y by inverting f(x) and f(y)

3-parameter GMBM

i

qi

pji

i i

jiqi

pji

iji

i

qi

pji

qi

pji

j

j

qj

pji

j j

jiqj

pji

jij

j

qj

pji

qj

pji

i

xw

x

rfxw

yfxw

xwyf

yw

y

rfyw

xfyw

ywxf

ˆ

)ˆ

(ˆ

)ˆ(ˆ

ˆ)ˆ(

ˆ

)ˆ

(ˆ

)ˆ(ˆ

ˆ)ˆ(

,

,,

,,

,

,

,,

,,

,

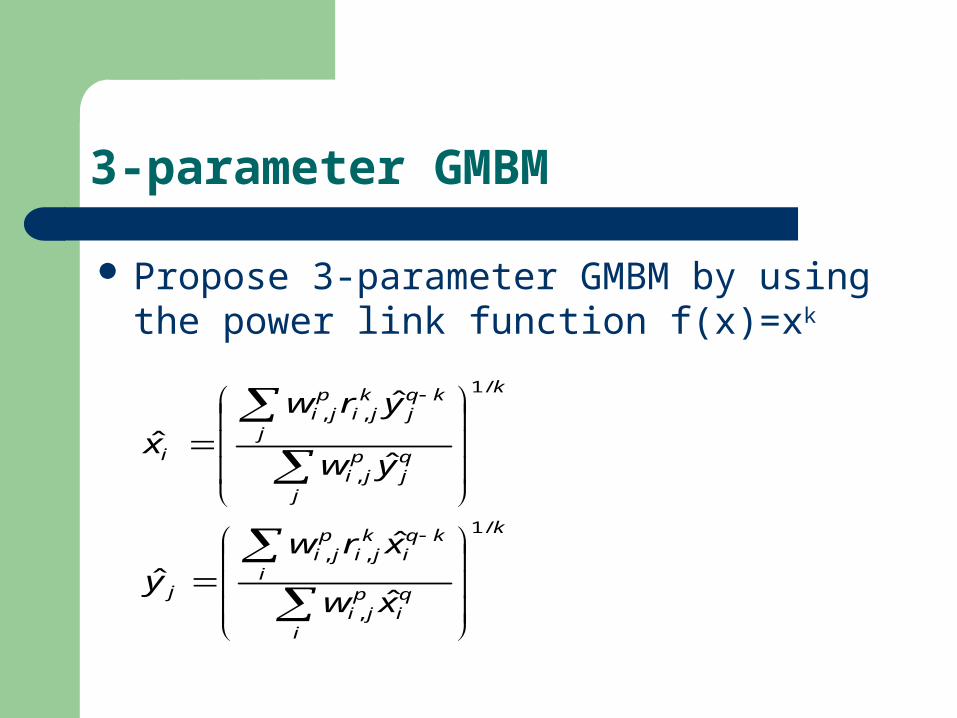

3-parameter GMBM

Propose 3-parameter GMBM by using the power link function f(x)=xk

k

i

qi

pji

i

kqi

kji

pji

j

k

j

qj

pji

j

kqj

kji

pji

i

xw

xrwy

yw

yrw

x

/1

,

,,

/1

,

,,

ˆ

ˆˆ

ˆ

ˆ

ˆ

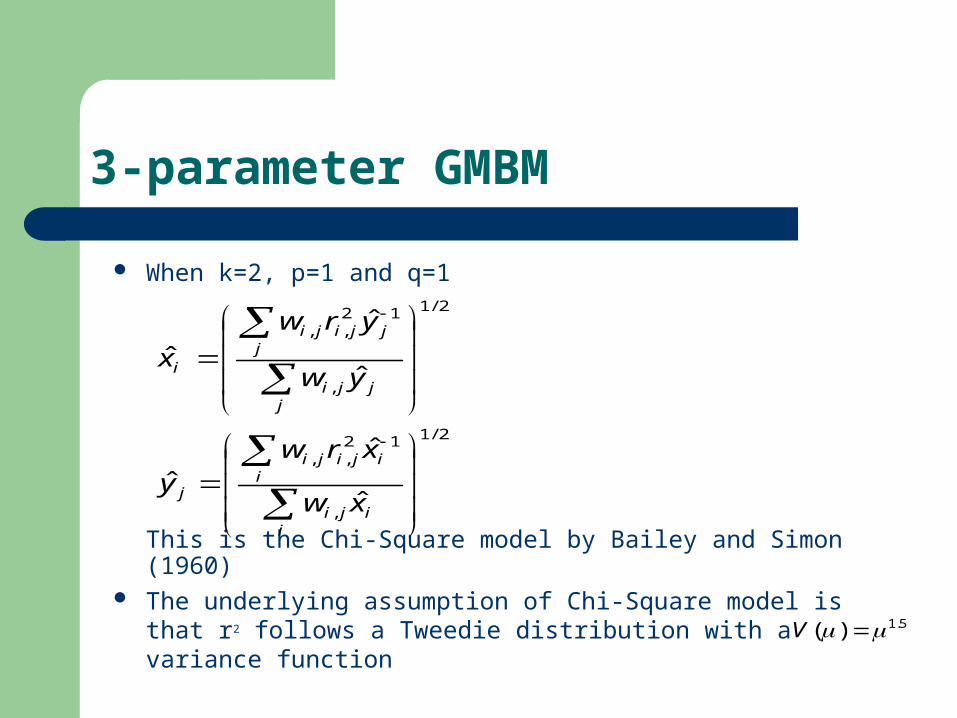

3-parameter GMBM

When k=2, p=1 and q=1

This is the Chi-Square model by Bailey and Simon (1960) The underlying assumption of Chi-Square model is that r2

follows a Tweedie distribution with a variance function

2/1

,

12,,

2/1

,

12,,

ˆ

ˆˆ

ˆ

ˆ

ˆ

iiji

iijiji

j

jjji

jjjiji

i

xw

xrwy

yw

yrw

x

5.1)( V

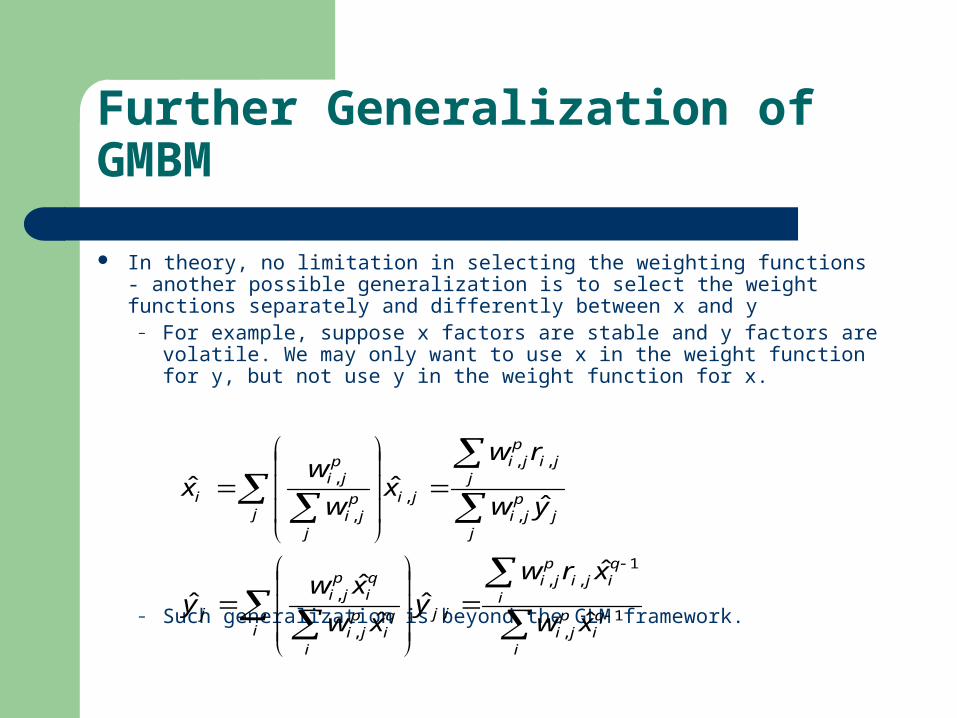

Further Generalization of GMBM

In theory, no limitation in selecting the weighting functions - another possible generalization is to select the weight functions separately and differently between x and y

– For example, suppose x factors are stable and y factors are volatile. We may only want to use x in the weight function for y, but not use y in the weight function for x.

– Such generalization is beyond the GLM framework.

i

qi

pji

i

qiji

pji

iji

i

qi

pji

qi

pji

j

jj

pji

jji

pji

jij

j

pji

pji

i

xw

xrwy

xw

xwy

yw

rw

xw

wx

1,

1,,

,,

,

,

,,

,,

,

ˆ

ˆˆ

ˆ

ˆˆ

ˆˆˆ

Numerical Methodology for the Iterative Method

Use the mean of the response variable as the base Starting points:

Use the latest relativities in the iterations

All the reported GMBMs converge within 8 steps

x

yi

j

,

,

0

0

1

1

itiji

ijiji

tj

jtjji

jjiji

ti

xw

rwy

yw

rw

x

,,

,,

,

1,,

,,

,

ˆˆ

ˆˆ

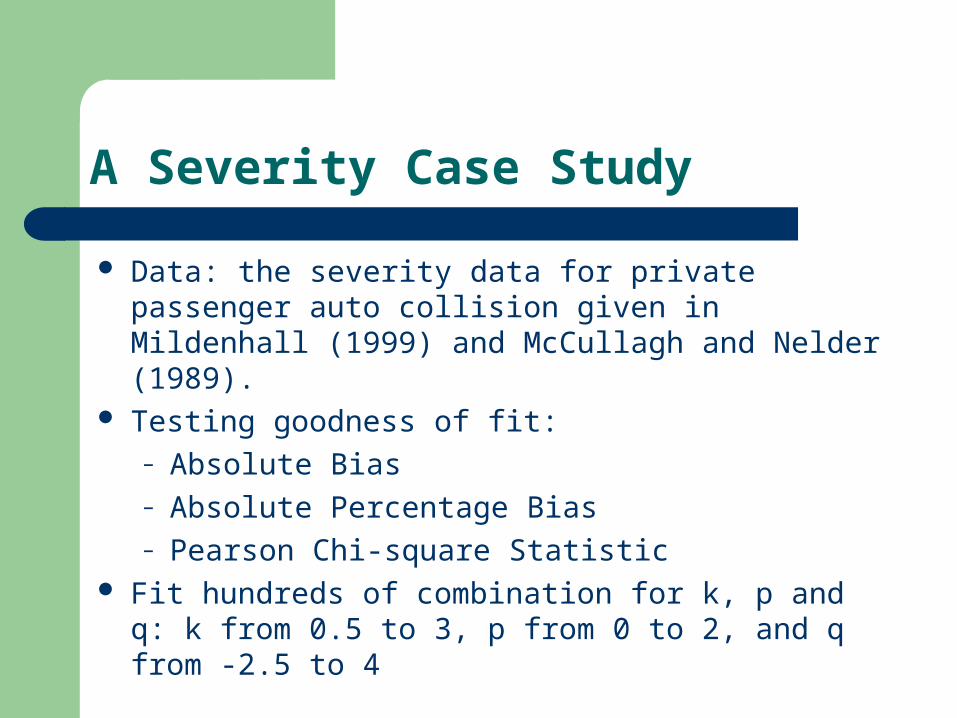

A Severity Case Study

Data: the severity data for private passenger auto collision given in Mildenhall (1999) and McCullagh and Nelder (1989).

Testing goodness of fit:– Absolute Bias– Absolute Percentage Bias– Pearson Chi-square Statistic

Fit hundreds of combination for k, p and q: k from 0.5 to 3, p from 0 to 2, and q from -2.5 to 4

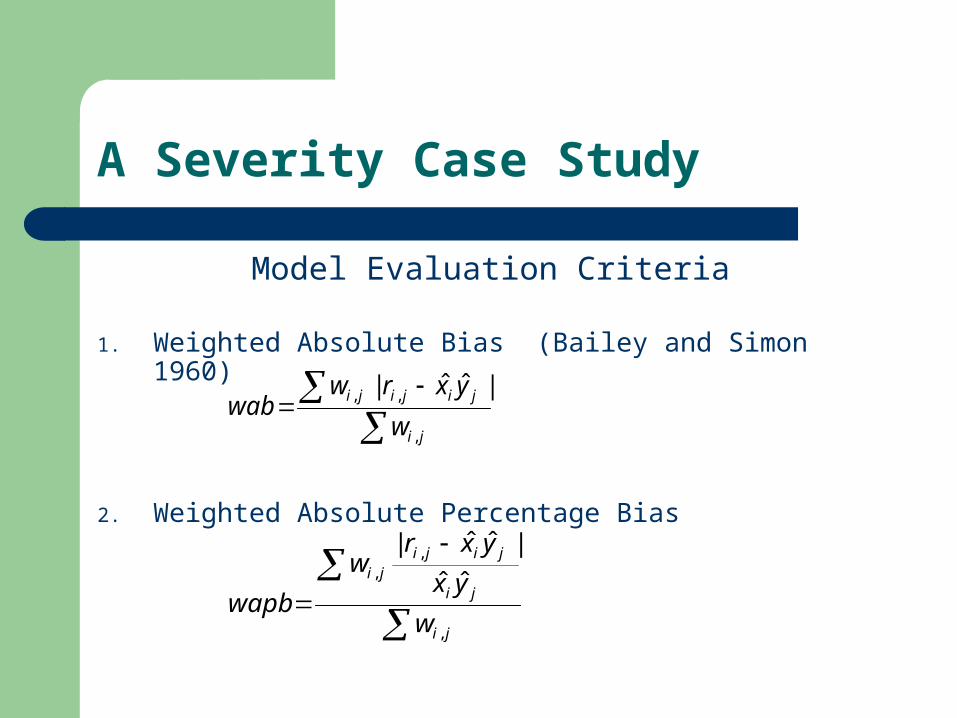

A Severity Case Study

Model Evaluation Criteria

1. Weighted Absolute Bias (Bailey and Simon 1960)

2. Weighted Absolute Percentage Bias

ji

jijiji

w

yxrwwab

,

,, |ˆˆ|

ji

ji

jijiji

w

yx

yxrw

wapb,

,, ˆˆ

|ˆˆ|

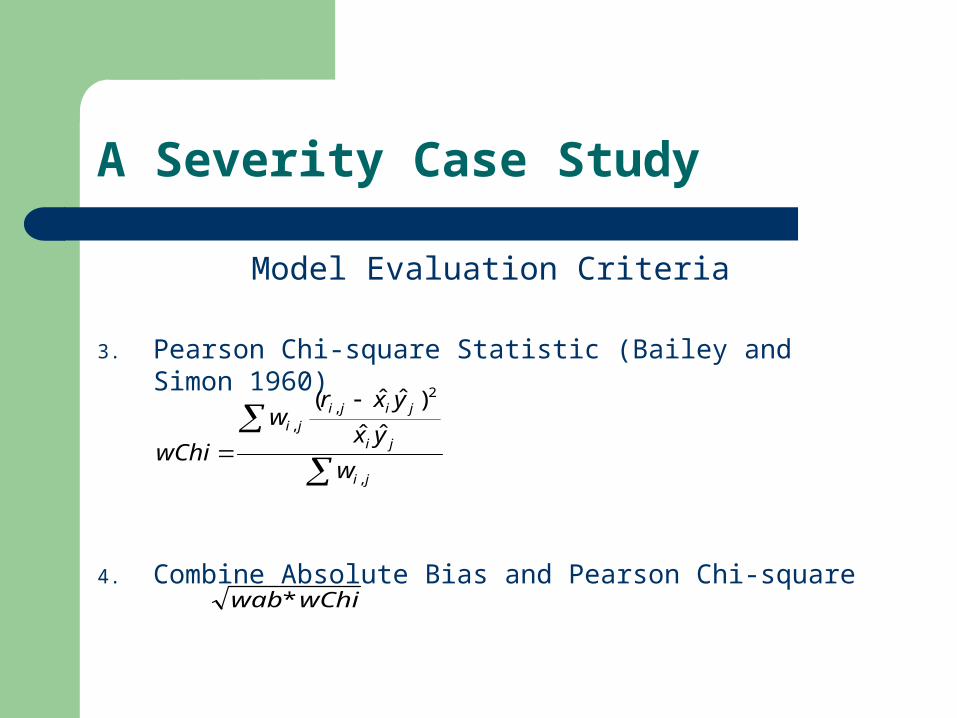

A Severity Case Study

Model Evaluation Criteria

3. Pearson Chi-square Statistic (Bailey and Simon 1960)

4. Combine Absolute Bias and Pearson Chi-square

wChiwab*

ji

ji

jijiji

w

yx

yxrw

wChi,

2,

, ˆˆ

)ˆˆ(

A Severity Case Study

Best Fits

Criterion p q k

wab 2 0 3

wapb 2 0 3

Chi-square 1 1 2

combined 1 -0.5 2.5

Conclusions

• 2 and 3 Parameter GMBM can completely represent GLM models with power variance functions

• All published to date minimum bias models are special cases of GMBM

• GMBM provide additional model options for data fitting• Easy to understand and does not require advanced

statistical knowledge• Can program in many different tools• Calculation efficiency is not a issue because of

modern computer power.

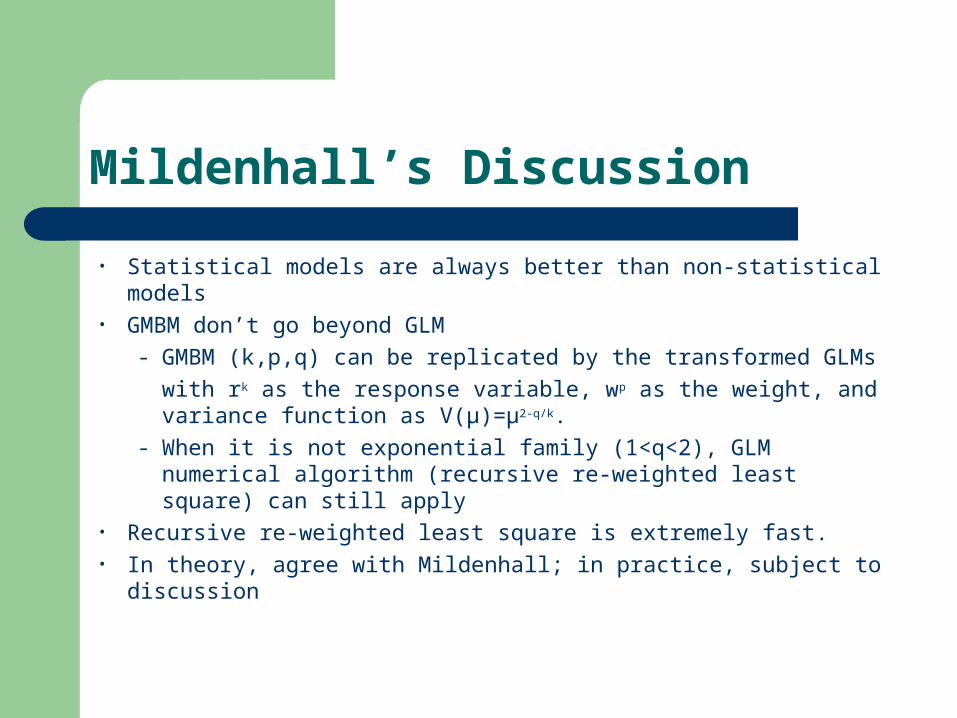

Mildenhall’s Discussion

• Statistical models are always better than non-statistical models• GMBM don’t go beyond GLM

- GMBM (k,p,q) can be replicated by the transformed GLMs

with rk as the response variable, wp as the weight, and variance function as V(μ)=μ2-q/k.

- When it is not exponential family (1<q<2), GLM numerical algorithm (recursive re-weighted least square) can still apply

• Recursive re-weighted least square is extremely fast.• In theory, agree with Mildenhall; in practice, subject to

discussion

Our Responses to Mildenhall’s Discussion

Are statistical models always better in practice?• Require at least intermediate level of statistical

knowledge. • Statistical model results can only be provided by

statistical softwares. For example, GLM is very difficult to implement in Excel without additional software

• Popular statistical softwares provide limited distribution selections.

Our Responses to Mildenhall’s Discussion

Are statistical models always better in practice?• Few softwares provide solutions for distributions

with other power variance functions, such as Tweedie and non-exponential distributions

• It requires advanced statistical and programming knowledge to program the above distributions using the recursive re-weighted least square algorithm

• Costs involved acquiring softwares and knowledge

Our Responses to Mildenhall’s Discussion

Calculation Efficiency Recursive re-weighted least square algorithm

converges with fewer iterations. GMBM also converges fast with actuarial data. It

generally converges within 20 iterations by our experience.

The cost in additional convergence is small and the timing difference between GMBM and GLM is negligible with modern powerful computers.

Q & A