General equilibrium theory - nyu.edu notes Nov1.pdf · eral equilibrium theory per se but also as...

128

General equilibrium theory Lecture notes Alberto Bisin Dept. of Economics NYU November 5, 2011

-

Upload

truongdang -

Category

Documents

-

view

224 -

download

0

Transcript of General equilibrium theory - nyu.edu notes Nov1.pdf · eral equilibrium theory per se but also as...

General equilibrium theoryLecture notes

Alberto BisinDept. of Economics

NYU

November 5, 2011

ii

Contents

1 Introduction 1

2 Demand theory: A quick review 32.1 Consumer theory . . . . . . . . . . . . . . . . . . . . . . . . . 4

2.1.1 Duality . . . . . . . . . . . . . . . . . . . . . . . . . . 82.1.2 Aggregate demand . . . . . . . . . . . . . . . . . . . . 11

2.2 Producer theory . . . . . . . . . . . . . . . . . . . . . . . . . . 12

3 Arrow-Debreu exchange economies 173.1 The economy . . . . . . . . . . . . . . . . . . . . . . . . . . . 173.2 Pareto e¢ ciency . . . . . . . . . . . . . . . . . . . . . . . . . . 173.3 Competitive equilibrium . . . . . . . . . . . . . . . . . . . . . 19

3.3.1 Uniqueness . . . . . . . . . . . . . . . . . . . . . . . . 233.3.2 Local uniqueness . . . . . . . . . . . . . . . . . . . . . 233.3.3 Di¤erentiable approach: A rough primer . . . . . . . . 253.3.4 Competitive equilibrium in production economies . . . 31

3.4 Mathematical appendix . . . . . . . . . . . . . . . . . . . . . . 313.4.1 References . . . . . . . . . . . . . . . . . . . . . . . . . 34

3.5 Strategic foundations . . . . . . . . . . . . . . . . . . . . . . . 34

4 Two-period economies 354.1 Arrow-Debreu economies . . . . . . . . . . . . . . . . . . . . . 354.2 Financial market economies . . . . . . . . . . . . . . . . . . . 38

4.2.1 The stochastic discount factor . . . . . . . . . . . . . . 424.2.2 Arrow theorem . . . . . . . . . . . . . . . . . . . . . . 444.2.3 Existence . . . . . . . . . . . . . . . . . . . . . . . . . 464.2.4 Constrained Pareto optimality . . . . . . . . . . . . . . 474.2.5 Aggregation . . . . . . . . . . . . . . . . . . . . . . . . 54

iii

iv CONTENTS

4.2.6 Asset pricing . . . . . . . . . . . . . . . . . . . . . . . 634.2.7 Some classic representation of asset pricing . . . . . . . 634.2.8 Production . . . . . . . . . . . . . . . . . . . . . . . . 68

5 Asymmetric information 795.1 A simple insurance economy . . . . . . . . . . . . . . . . . . . 80

5.1.1 The Symmetric information benchmark . . . . . . . . . 815.2 The moral hazard economy . . . . . . . . . . . . . . . . . . . . 825.3 The adverse selection economy . . . . . . . . . . . . . . . . . . 855.4 Information revealed by prices . . . . . . . . . . . . . . . . . . 86

5.4.1 References . . . . . . . . . . . . . . . . . . . . . . . . . 90

6 In�nite-horizon economies 936.1 Asset pricing . . . . . . . . . . . . . . . . . . . . . . . . . . . 93

6.1.1 Arrow-Debreu economy . . . . . . . . . . . . . . . . . . 946.1.2 Financial markets economy . . . . . . . . . . . . . . . 946.1.3 Conditional asset pricing . . . . . . . . . . . . . . . . . 956.1.4 Predictability or returns . . . . . . . . . . . . . . . . . 976.1.5 Fundamentals-driven asset prices . . . . . . . . . . . . 98

6.2 Bubbles . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 986.2.1 (Famous) Theoretical Examples of Bubbles . . . . . . . 106

6.3 Double In�nity . . . . . . . . . . . . . . . . . . . . . . . . . . 1086.3.1 Overlapping generations economies . . . . . . . . . . . 111

6.4 Default . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 116

7 To add 123

Chapter 1

Introduction

These notes constitute the material for the second half of the Micro I (�rstyear) graduate course at NYU. They owe much to the brilliant TA�s I had,Sevgi Yuksel and (somewhat in expectations) Bernard Herskovic. The topicof this section of the course is general equilibrium theory (the other section,decision theory, is taught by Ariel Rubinstein).The standard approach to graduate teaching of general equilibrium the-

ory involves introducing a series of theorems on existence, characterization,and welfare properties of competitive equilibria under weaker and weakerassumptions in larger and larger commodity spaces. Such an approach intro-duces the students to precise rigorous mathematical analysis and invariablyimpresses them with the elegance of the theory. Various textbooks take thisapproach, in some form or another:

A. Mas-Colell, M. Whinston, and J. Green (1995): Microeconomic Theory,Oxford University Press, Part 4, is the main reference; it also containsa short introduction to two-period economies.

L. McKenzie (2002), Classical General Equilibrium Theory, MIT Press, is abeautiful modern treatment of the classical theory.

K. Arrow and F. Hahn (1971): General Competitive Analysis, North Hol-land, is the classical treatment of the classical theory.1

1And so is G. Debreu (1972), Theory of Value: An Axiomatic Analysis of EconomicEquilibrium, Cowles Foundation Monographs Series, Yale University Press, an invaluablelittle book for several generations of theorists.

1

2 CHAPTER 1. INTRODUCTION

B. Ellickson (1994): Competitive Equilibrium: Theory and Applications,Cambridge University Press. It contains a useful chapter on non-convexeconomies.

M. Magill andM. Quinzii (1996): Theory of Incomplete Markets, MIT Press,takes a classical theory approach on �nancial market equilibrium intwo-period economies.

The approach adopted in these notes aims instead at introducing gen-eral equilibrium theory per se but also as the canonical microfoundation formacroeconomics and �nance. To this end, the standard theory of generalequilibrium is introduced in its rigour and elegance, but only under restric-tive assumptions, allowing some shortcuts in analysis and proofs. On theother hand, we shall be able to introduce �nancial market equilibria in two-period economies after only a few classes, exposing students to fundamen-tal conceptual notions like complete and incomplete markets, no-arbitragepricing, constained e¢ ciency, equilibria in moral hazard and adverse selec-tion economies, and more. The course ends with a treatment of dynamiceconomies and recursive competitive equilibria. Pedagogically, from two-period to fully dynamic economies the step is rather short, so that we canconcentrate on purely dynamic concepts, like bubbles.

Chapter 2

Demand theory: A quickreview

The consumption set X is the set of admissible levels of consumption of Lexisting commodities. In this section we shall assume

X = RL+; with generic element x:

X is then a convex set, bounded below. For any x; y 2 X; we say x > y ifxl � yl; for any l = 1; 2; :::; L; and xl > yl for at least one l = 1; 2; :::; L:

Assumption 1 The consumer has a utility function1

U : RL+ ! R

which satis�es the following properties,

Strong Monotonicity: y > x ) U(y) > U(x); for any x; y 2 RL+;1In these notes we shall adopt the utility function as a primitive. That is, we shall

assume that any agent�s underlying preference ordering % on X (is complete, transitive,and continuous; so that it) can be represented by a utility function; see Rubinstein (2009).A preference ordering % onX which (is not continuous and hence it) cannot be representedby a utility function is the Lexicographic ordering:

x % y if x1 � y1 or x1 = y1 and xl � yl; for l = 2; :::; L:

3

4 CHAPTER 2. DEMAND THEORY: A QUICK REVIEW

Strict Convexity: U : RL+ ! R is strictly quasi-concave, that is,

U (�x+ (1� �) y) � �U(x) + (1� �)U(y); for any x; y 2 RL+ and � 2 [0; 1]; andU (�x+ (1� �) y) > �U(x) + (1� �)U(y); if x 6= y and � 2 (0; 1)

Di¤erentiability: U : RL+ ! R is C2 on the interior of its domain.

Let rU denote the gradient of the map U : RL+ ! R: Exploiting di¤er-entiability strong monotonicity can be equivalently written as

rU(x) 2 RL++; for any x 2 RL++;

while strict quasi-concavity as

vr2U(x)v < 0 for any v 6= 0 2 RL such that rU(x)v = 0; for any x 2 RL++.

Common properties of utility functions at times studied in applicationsinclude:Quasi-linearity: U(x) = x1 + �(x2; :::; xL); for some � : RL�1+ ! R

satisfying strong monotonicity, strict convexity, and di¤erentiability.

Homotheticity: U(�x) = �U(x); for any � 2 R++:

Examples of homothetic utility functions include:

Cobb Douglas: U(x) = x�1x1��2 ;CES: U(x) = x�1 + x

�2 .

Di¤erentiability is violated, for instance, by Leontief preferences:

U(x) = min f:::; �lxl;:::g ; for some � 2 RL++:

2.1 Consumer theory

Markets are competitive, that is, the consumer takes market prices as given,independent of his decisions (each agent is a price taker). In addition weconsider the case where:

prices are linear : unit price pl of each commodity l is �xed, independent oflevel of individual trades (and the same for all agents);

2.1. CONSUMER THEORY 5

prices are non-negative: this is justi�ed under free disposal, that is, whenagents can freely dispose of any amount of any commodity;

markets are complete: for each commodity l in X there is a market wherethe commodity can be traded.

Given wealth level m, the budget set is:

B(p;m) =

(x 2 X : p � x =

LXl=1

plxl � m)

The budget set is convex, compact, and non-empty for p 2 RL++; m �0:Furthermore, the budget set is homogeneous of degree 0:

B(p;m) = B(�p; �m); for all � > 0:

Consider the consumer�s utility maximization problem,

maxx2B(p;m)

U(x):

For any p 2 RL++;m � 0; under our assumptions on U(x), by the Max-imum theorem, a solution of the consumer�s problem exists. Furthermore,the solution of the consumer�s problem for every p;m induces the consumer�sdemand correspondence x : RL++�R+ ! RL+; x(p;m): Strict quasi-concavityof U(x); again by the Maximum theorem, implies that x(p;m) is a in fact acontinuous function.

Proposition 1 The individual consumer�s demand x(p;m) satis�es the fol-lowing properties:

Homogeneity of degree zero in p;m:

x(p;m) = x(�p; �m) for all p 2 RL++; � > 0;

Continuity: x(p;m) is a continuous function in p;m;

Walras Law: px(p;m) = m;

WARP: for any (p;m); (p0;m0) 2 RL++ � R+ such that x = x(p;m) 6= x0 =x(p0;m0):

if px0 � m; then p0x > m0:

6 CHAPTER 2. DEMAND THEORY: A QUICK REVIEW

Proof. These properties are straightforward consequences of the assump-tions. Homogeneity of degree zero is a consequence of homogeneity of degreezero of the budget set. Continuity follows from the Maximum theorem understrict quasi-concavity of U(x) (weak quasi-concavity would induce an upper-hemi-continuous, convex valued correspondence x : RL++�R+ ! RL+:WARPand Walras law follow easily from strict monotonicity.It is important to notice that WARP does not imply the (uncompensated)

Law of demand, that is,

(p� p0) (x(p;m)� x(p0;m0)) � 0; for m = m0:

Note also that the (uncompensated) Law of demand is equivalently written,exploiting di¤erentiability, as

dpDpx(p;m)dp � 0:

Therefore, WARP does not imply that Dpx(p;m) is negative semi-de�nite.In general in fact, Dpx(p;m) is NOT negative semi-de�nite. If preferencesare homothetic, however, the individual consumer�s demand x(p;m) doessatisfy the (uncompensated) Law of demand. Furthermore, in this case, theindividual consumer�s demand x(p;m) is homogeneous of degree 1 in m:

x(p; �m) = �x(p;m) for all p 2 RL++;m; � > 0:2

WARP on the other hand does imply the (compensated) Law of demand

(p� p0) (x(p;m)� x(p0;m0)) � 0; for m�m0 = (p� p0)x(p0;m0):

Once again, exploiting di¤erentiability we can express the (compensated) Lawof demand through the properties of the Slutsky matrix of compensated pricee¤ects. Consider the following compensated price change:

dp; dm: dm = x � dp

The induced demand change is

dx = Dpx(p;m)dp+Dmx(p;m)dm =

= Dpx(p;m) � dp+Dmx(p;m)(xdp):

2This is a consequence of the fact that homotheticity implies that marginal rates of

substitution,@U(x)@xl

@U(x)@x

l0; for any l; l0; are invariant with respect to expansions along rays from

the origin.

2.1. CONSUMER THEORY 7

De�ne then the Slutsky matrix of compensated price e¤ects as

S(p;m) = Dpx(p;m) +Dmxx:

WARP then implies the following.

Proposition 2 S(p;m) is negative semi de�nite; that is,

dpS(p;m)dp � 0; for any dp 2 RL:

Finally, any solution of the consumer�s problem satis�es the followingsystem of Kuhn Tucker necessary and su¢ cient conditions. In the case ofinterior solutions, these are:

rU � �p = 0

m� p � x = 0;

for some � > 0, the Lagrange multiplier associated to the budget constraint.Local properties of x(p;m) can then be obtained using the Implicit Functiontheorem on the previous �rst order conditions (foc�s):�

r2U ��p��pT 0

� �dxd�

�=

��xT

�dp+

�0�1

�dm

Note that the second order conditions (soc�s) guarantee that�r2U ��p��pT 0

�is invertible

when evaluated at an (x; �; p) satisfying foc�s. A simple proof of this state-ment follows for completeness.Proof. We show that @(y; z) 2 RL+1, (y; z) 6= 0 such that�

r2U ��p��pT 0

� �yz

�=

�r2Uy � �pz��py

�= 0:3

3For any strict quasi concave and C2 function f : RL+ ! R; the matrix�r2f rfrfT 0

�is called bordered Hessian and has a non-zero determinant. Note that

�r2U ��p��pT 0

�is

the bordered Hessian of the Lagrangian.

8 CHAPTER 2. DEMAND THEORY: A QUICK REVIEW

By contradiction, suppose such a (y; z) exists. Then pre-multiplying r2Uy��pz by y, yields:

yr2Uy = �ypz:

But �ypz = 0; and hence yr2Uy = 0: But the second order conditions (soc�s;in turn guaranteed by strict quasi-concavity of the Lagrangian, U(x)��(px�m)), require that vr2Uv < 0 on all v 6= 0 such that (rU � �p) v = 0; acontradiction.

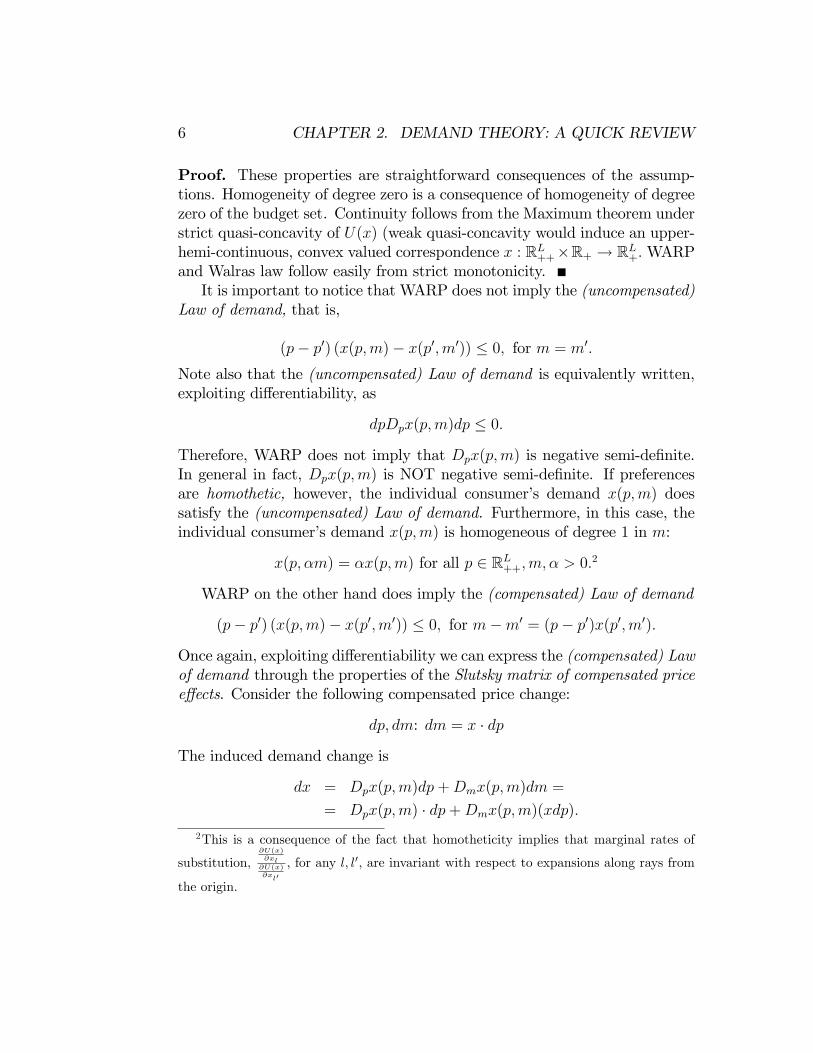

2.1.1 Duality

Let V : RL++ � R+; V (p;m), be de�ned by

V (p;m) = U(x(p;m)):

V (p;m) is the indirect utility function.

Proposition 3 The indirect utility function V (p;m) satis�es the followingproperties:

@V (p;m)=@m = � > 0: the consumer�s marginal utility of wealth equals theshadow value of relaxing the budget constraint;

V (p;m) is homogenous of degree zero in p;m;

@V (p;m)=@pl � 0 for all l; p >> 0;

V (p;m) is quasi-convex in p: the lower contour set�p : V (p;m) � �V

is

convex.

Proof. The properties are straighforward consequences of the assumptionson U(x) and the properties of x(p;m): We leave them to the reader, exceptquasi-convex in p; which is proved as follows. Take any pair p0; p00 such thatV (p0;m); V (p00;m) � �V and consider p̂ = �p0 + (1� �)p00 for � 2 [0; 1]. Notethat for all x such that p̂ � x � m we must have either p0 � x � m and/orp00 � x � m; thus U(x) � �v .Consider the consumer�s cost minimization problem,

minx2X

p � x

s.t:U(x) � u

2.1. CONSUMER THEORY 9

A solution exists for all u � U(0) and p 2 RL++: The solution h(p; u); withh : RL++ � R ! RL+; is typically referred to as compensated - or Hicksian -demand. By the soc�s,

Dph(p; u) is symmetric, negative semi-de�nite.

We say that Hicksian demands h(p; u) satisfy the law of demand.Let e : RL++�R! R+; e(p; u) = p�h(p; u) de�ne the expenditure function.

Proposition 4 The expenditure function e(p; u) has the following properties:

@e(p; u)=@u > 0;

@e(p; u)=@pl � 0 for all l = 1; ::; L;

e(p; u) is homogeneous of degree one in p;

e(p; u) is concave in p:

Proof. The properties are straighforward consequences of the Maximumtheorem and the assumptions on U(x). We leave them to the reader, exceptquasi-concavity in p; which is proved as follows. For any pair p0; p00, considerp̂ = �p0 + (1 � �)p00 for � 2 [0; 1]. Then, for any u, e(p̂; u) = p̂ � h(p̂; u) =�p0 �h(p̂; u)+(1��)p00 �h(p̂; u); which is in turn � �e(p0; u)+(1��)e(p00; u):

For all p 2 RL++, m > 0; u > U(0), the following identities hold:

x(p;m) = h(p; u)for u = V (p;m) and e(p; u) = m:

(2.1)

By the envelope theorem, the compensated demand can be obtained fromthe expenditure function:

h(p; u) = Dpe(p; u):

Hence the properties of h(p; u) can also be obtained from those of e(p; u).Similarly, di¤erentiating the equation de�ning the indirect utility,

V (p;m) = U(x(p;m)� �(px�m)

with respect to p, we obtain Roy�s identity:

rpV (p;m) = ��x(p;m) = �rmV (p;m) � x(p;m):

A brief summary of the duality relationships can be helpful:

10 CHAPTER 2. DEMAND THEORY: A QUICK REVIEW

Figure 2.1: Brief summary of duality relations

2.1. CONSUMER THEORY 11

x(p;m)! h(p; u) Slutsky:

Dpx(p; u)�Dmx xT = Dph(p; u):

V (p;m)! x(p;m) Roy�s identity:

x(p;m) = � 1

rmV (p;m)rpV (p;m):

e(p; u)! h(p; u) Expenditure function properties:

h(p; u) = rpe(p; u):

V (p;m)$ e(p; u) Utility-expenditure duality, for given p 2 RL++:

V (:;m) = e�1(:;m);

e(:; u) = V �1(:; u)

x(p;m)$ h(p; u) Marshallian-Hicks demand duality:

x(p;m) = h(p; V (p;m))

h(p; u) = x(p; e(p; u))

2.1.2 Aggregate demand

It is useful to study in detail the properties of aggregate demand, as a func-tion of wealth. With some abuse of notation, let introduce the notation toindex agents, i = 1; :::; I. Let the wealth of agent i be denoted mi: Fix thedistribution of wealth as follows,

mi = �im for some given �i � 0, for all i,Xi

�i = 1:

The Marshallian demand of any agent i is then denoted xi(p;mi) and

x(p;m) =Xi2Ixi(p;mi)

is the aggregate demand.

12 CHAPTER 2. DEMAND THEORY: A QUICK REVIEW

Aggregate demand trivially inherits several properties from individualdemand, i.e., di¤erentiability, homeogeneity of degree 0, Walras Law. Butdoes x(p;m) satisfy WARP? Not, typically. Take (p;m) and (p0;m0) suchthat x (p0;m0) 6= x (p;m) and

p � x (p0;m0) � m:

It is immediate to see that the following inequality can still hold:

p0 � x (p;m) � m0

(because p�x (p0;m0) � m does not imply p�xi (p0;mi0) � mi for all i; similarlyfor p0 � x (p;m) � m0.)A su¢ cient condition for aggregate demand x (p;m) to satisfy WARP

is that individual Marshallian demands satisfy the (uncompensated) law ofdemand, that is, substitution e¤ects prevail over income e¤ects.

Proposition 5 Suppose xi(p;mi) satis�es the (uncompensated) law of de-mand, that is,

Dpxi(p;mi) is negative semi-de�nite

for all i: Then x (p;m) also satis�es the (uncompensated) law of demandand hence WARP.

2.2 Producer theory

We shall study the production activity of �rms operating in competitivemarkets. A production plan is a y 2 RL, interpreted as the net output of theL goods:

yi < 0 : input

yi > 0 : output

The production set is the set of (technologically feasible) production plans:

Y � RL:

Whenever the commodities which are outputs in the production set are �xed,O � f1; ::; Lg (and hence also the complementary set of those which are in-puts), the outer boundary of Y can typically be represented by a (continuous)

2.2. PRODUCER THEORY 13

production function, describing the maximal output level attainable for anylevel of inputs. In the case where O = f1g ; e.g.,

y1 = f(z) i¤

(y1;�z) 2 Y@y01 > y1 : (y

01;�z) 2 Y

We assume that Y and and f : RL�1+ ! R+ satisfy the following assump-tions:

Regularity Y is nonempty, closed, Y \ RL+ = f0g (no free lunch andpossibility of inaction), and it satis�es free disposal :

y 2 Y and y0 � y ) y0 2 Y

Correspondingly, f : RL�1+ ! R+ is monotonically increasing.

Convexity Y is strictly convex:

y; y0 2 Y ) �y + (1� �)y0 2 intY

Correspondingly, f : RL�1+ ! R+ is strictly concave (has decreasingreturns to scale). (Y is convex,

y 2 Y ) �y 2 Y for all � 2 [0; 1]

corresponds to f : RL�1+ ! R+ is concave - has non-increasing returnsto scale.)

Any �rm chooses a production plan so as to maximize pro�ts:

max p � ys.t. y 2 Y

Existence of a solution requires conditions ensuring that Y is boundedabove. For every p � 0, a solution induces a net supply correspondencey(p):

Proposition 6 The net supply correspondence y(p) satis�es the followingproperties:

14 CHAPTER 2. DEMAND THEORY: A QUICK REVIEW

y(p) is homogeneous of degree 0 in p;

y(p) is a convex-valued correspondence (a single valued function if f :RL�1+ ! R+ is strictly concave).

The value of the solution is a pro�t function �(p) = p � y(p):

Proposition 7 The pro�t function �(p) satis�es the following properties:

�(p) is homogeneous of degree 1 in p;

�(p) is a convex function.

Proof. The properties are straighforward consequences of the propertiesof y(p): We leave them to the reader, except convexity; which is proved asfollows. Take any pair p0; p00 and consider p̂ = �p0 + (1� �)p00 for � 2 (0; 1).Note that �(p̂) = y(p̂) � (�p0 + (1� �)p00) � �y(p0) � p0 + (1 � �)y(p00) � p00= ��(p0) + (1� �)�(p00):Suppose Y is a convex cone,

y 2 Y ) �y 2 Y for all � > 0;

that is, the technology has constant returns to scale: Correspondingly, theproduction function f : RL�1+ ! R+ is homogeneous of degree 1 in its argu-ments and,

- y 2 y(p)) �y 2 y(p) for all � > 0;

- �(p) = 0 for all p:

Whenever f is di¤erentiable, any solution of the �rm�s problem satisfythe following system of foc�s (stated here for the case of interior solutions):

p1Df = w:

Focs are also su¢ cient if f is concave.Assume f is continuously di¤erentiable and strictly concave. Applying

the Implicit Function theorem to foc�s, we obtain:

Dwz =1

p1

�D2f

��1is symmetric, negative de�nite

Furthermore, by the envelope theorem, y(p) = Dp�, so that Dpy = D2�

is:

2.2. PRODUCER THEORY 15

- symmetric,

- positive - recall z = �(y2; ::; yL) ! - semide�nite (by the convexity of �) and

- such that Dpy p = 0 (by the homogeneity of y(p)).

Let p =�p1w

�and y =

�y1z

�: The input level z which solves the �rm�s

choice problem also solves the following problem:

minz2RL�1+

C = wz

s:t: f(z) � y1:This is perfectly analogous to expenditure minimization problem of con-sumer. Hence we know that:

- C(w; y1) is concave in w and such that @C=@y1 > 0 and @C=@wl � 0;l = 1; ::; L� 1;

- z(w; y1) = DwC exhibits the properties of a compensated demand function.

16 CHAPTER 2. DEMAND THEORY: A QUICK REVIEW

Chapter 3

Arrow-Debreu exchangeeconomies

3.1 The economy

The economy is polupated by I consumers with preferences described byU i : RL+ ! R and resources !i 2 RL+, i 2 I = f1; ::; Ig :1 An allocation is anarray (x1; ::; xI) 2 RLI+ , and it is feasible if it satis�es

IXi=1

xi �IXi=1

!i

In the special case in which L = 2, I = 2, feasible allocations can be graphi-cally represented using the Edgeworth Box.Unless otherwise noted, we shall impose the following strong (but not

outrageous) assumptions.

Assumption 2 U i : RL+ ! R is C2 in any open subset of RL+;strictly monotonicin its arguments and strictly quasi-concave. Furthermore, ! 2 RLI++:

3.2 Pareto e¢ ciency

An allocation x 2 RLI+ is Pareto e¢ cient if it is feasible and there is no otherfeasible allocation x̂ 2 RLI+ which Pareto dominates it:

U i(x̂i) � U i(xi) for all i, > for at least one i.1We are conscious of the notational abuse.

17

18 CHAPTER 3. ARROW-DEBREU EXCHANGE ECONOMIES

Pareto dominance de�nes a (social) preference relation over the set of allo-cations RLI+ , which is however incomplete.PE allocations are solutions of the problem:

maxx Ui(xi)

s.t.P

i xi �

Pi !

i

U i0(xi

0) � �U i

0for all i0 6= i

for some given��U i

0�i0 6=i :

The foc�s (for an interior solution) of this problem are:

rU i = �

�i0rU i0 = � for all i0 6= iXi

xi =Xi

!i

where��i

0�i0 6=i and � are the Lagrange multipliers of the two sets of con-

straints above. Thus

rU i = �i0rU i0 for all i0 6= i

and utility gradients are co-linear for all agents (Marginal rates of substitu-tion are equalized across agents).Varying the values of �U i

0for i0 6= i we obtain the set Pareto e¢ cient

allocations, the Pareto frontier.Let the Utility possibility set be the image of the feasible allocations in

the space of utility levels

U =

(U 2 RI

�����U � �U i(xi)�Ii=1 , for some x 2 RLI+ such thatXi

xi �Xi

!i

)

U is closed, convex, bounded above. Furthermore, the set of Pareto optimalutilities is de�ned as

UP = fU 2 U j@U 0 2 U such that U 0 > U g :2

2In our notation, U 0 > U requires U 0i � U i, for any i 2 I; with at least one strictinequality.

3.3. COMPETITIVE EQUILIBRIUM 19

Theorem 8 (Negishi) Let x 2 RLI+ be a Pareto e¢ cient allocation. Thenthere exist a � 2 RI+, � 6= 0, such that

x = argmaxXi2I�iU i(xi)

s.t.Xi

xi �Xi

!i:

Furthermore,�i

�i0= �i

0; for any i0 6= i 2 I:

Proof. Consider a Pareto optimal allocation x; so that U(x) = fU i(xi)gi2I 2UP. Furthermore, U(x) 2 bdry(U), and U is closed, convex, bounded above.An appropriate separating hyperplane theorem then implies that there existsa � 2 RI , � 6= 0, such that

�U(x) � �U; for any U 2 U;

that is,

U(x) = argmaxXi2I�iU i

s.t. U 2 U:

Trivially, then

x = argmaxXi2I�iU i(xi)

s.t.Xi

xi �Xi

!i:

Finally, U is unbounded below, which implies that � 2 RI+:PE allocations support points on the outer boundary of UP .

3.3 Competitive equilibrium

Agents trade in perfectly competitive markets.

20 CHAPTER 3. ARROW-DEBREU EXCHANGE ECONOMIES

A competitive equilibrium is an allocation x = (:::; xi; ::) 2 RLI+ and aprice p 2 RL++ such that

xi 2 argmaxU i(xi)

s.t. pxi � p!i;

for any i 2 I; and Xi

xi �Xi

!i:

Trade is voluntary, hence equilibrium allocations will satisfy individual ra-tionality:

U i(xi) � U i(!i) for all i = 1; :::; I:Letting mi = p!i we can derive agent I�s Marshallian demand from hisconsumer problem, as in the previous chapter. It is convenient, however,represent demand functions in terms of endowments rather than wealth:

xi : RL++ � RL++ ! RL+:

Let zi (p; !i) denote agent i 2 I�s excess demand: zi (p; !i) = xi (p; !i)� !i:Finally, the aggregate excess demand z : RL++ � RLI++ ! RL+ is de�ned as

z (p; !) =Xi2Izi�p; !i

�:

Proposition 9 For any economy ! 2 RLI++ the aggregate excess demandz (p; !) satis�es the following properties:

smoothness: z (p; !) is C1;

homogeneity of degree 0: z (�p; !) = z (p; !) ;for any � > 0;

Walras Law: pz (p; !) = 0; 8p >> 0;

lower boundedness: 9s such that zl (p; !) > �s, 8l 2 L;

boundary property:

pn ! p 6= 0; with pl = 0 for some l;) max fz1(pn; !); :::; zL(pn; !)g ! 1:

Let�s �rst study the welfare properties of competitive equilibrium alloca-tions.

3.3. COMPETITIVE EQUILIBRIUM 21

Theorem 10 (First welfare) All competitive equilibrium allocations arePareto e¢ cient.

Proof. Suppose x = (::; xi; ::) is a competitive equilibrium allocation forsome price p and it is not Pareto e¢ cient. Then there must be anotherallocation x̂ = (::; x̂i; ::) which is feasible and Pareto dominates x. But sincexi is the optimal choice of consumer i at prices p and preferences are stronglymonotone, U i(x̂i) � U i(xi) implies p�x̂i � p�xi for all i and also, p�x̂i � p�!i,with all the previous inequalities being strict for at least some i. Summingthe latter inequality over i yields p �

Pi x̂

i > p �P

i !i which contradicts the

feasibility of x̂:

Theorem 11 (Second welfare) For any Pareto e¢ cient allocation x 2RLI+ , there exist transfers t 2 RLI , such that

Pi ti = 0 and x 2 RLI+ is a

competitive equilibrium allocation (for some prices p 2 RL++) of the economywith initial endowment ! + t 2 RLI+ .

Proof. Let ti = xi � !i for all i. The theorem is an implication of theseparating hyperplane theorem.Let ! = (!i)i2I denote the vector of aggregate endowments:Competitive

equilibrium prices are solutions of:

z(p;!) �Xi

xi(p; p � !i)�Xi

!i = 0;

a system of L equations in L unknowns, the prices p. By Walras law

p � X

i

xi(p; p � !i)�Xi

!i

!= 0; for all p

and hence at most L � 1 equations are independent (the market clearingequation for one market can be o,itted without loss of generality). By ho-mogeneity of degree 0 in p of xi(p; p � !i); for any i 2 I; prices can always benormalized, e.g., restricted without loss of generality to

p 2 �L�1 �(p 2 RL+ :

Xl

pl = 1

);

the L-simplex, a compact ad convex set.

22 CHAPTER 3. ARROW-DEBREU EXCHANGE ECONOMIES

The equilibrium equations can thus be always reduced to L�1 equationsin L� 1 unknowns. Since equations are typically nonlinear, having numberof unknowns less or equal than number of independent equations does notensure a solution exists.

Theorem 12 (Existence) Let z : �L�1 ! RL be a continuous function,such that p � z(p) = 0 for all p. Then there exists p� such that z(p�) � 0:

Sketch of the proof.

Let 'l(p) =pl +max f0; zl(p)gPL

j=1 [pj +max f0; zj(p)g], l = 1; ::L

Note that �L�1 is convex and compact, and ' : �L�1 ! �L�1. Hence bythe Brouwer Fixed Point theorem there is a �xed point p�:

p�l =p�l +max f0; zl(p�)gPLj=1 [pj +max f0; zj(p)g]

, l = 1; ::L.

Then

zl(p�)p�l

LXj=1

�p�j +max f0; zj(p�)g

�= zl(p

�)p�l + zl(p�)max f0; zl(p�)g

and summing over l yields:

0 =Xl

zl(p�)max f0; zl(p�)g ) zl(p

�) � 0 for all l = 1; :::; L:

Since p� satis�es z(p�) � 0 and Walras law, p� � z(p�) = 0,

zl(p�) < 0 i¤ p�l = 0:

But this is impossible under strong monotonicity and hence:

z(p�) = 0:

To properly claim existence of a competitive equilibrium need to face one lastproblem: the consumers�demand is not de�ned for prices on the boundary of�L�1 (when the price of some good is zero). We need to use a limit argument,considering z : �L�1

" ! RL, for�L�1" �

�p 2 RL+ :

Pl pl = 1, pl � " for all l

,

and taking limits as "! 0.

3.3. COMPETITIVE EQUILIBRIUM 23

3.3.1 Uniqueness

Existence of a competitive equilibrium can be proved under quite general con-ditions.3 Equilibria are however unique only under very strong restrictions.Several examples of such restrictions are listed in the following.

The endowment distribution is Pareto e¢ cient, and hence the only equilib-rium is autarchic: xi = !i for all i 2 I:

Preferences satisfy an aggregation condition (so that a representative con-sumer exists) for all p and for given (mh)Hh=1:

Aggregate demand satis�es WARP and equilibria are locally isolated.

Aggregate demand satis�es the gross substitution property:

p0l > pl and p0j = pj; for all j 6= l;=)

zj(p0) > zj(p).

Note that gross substitution implies that the law of demand holds atany equilibrium price. Gross substitution holds for instance for CobbDouglas and CES utility functions (provided � < 1).

3.3.2 Local uniqueness

Let an economy be parametrized by the endowment vector ! 2 RLI++ keepingpreferences (ui)i2I �xed. Furthermore, normalize pL = 1 and eliminate theL-th component of the excess demand. Then

z : RL�1++ � RLI++ ! RL�1

represents an aggregate excess demand for an exchange economy ! = (!i)i2I 2RLI++.

De�nition 13 A p 2 RL++ such that z (p; !) = 0 is regular if Dpz (p; !)has rank L� 1:

3We shall leave this statement essentially unsubstantiated. General equilibrium theory,for more than half a century, has considered this as one of its main objectives.

24 CHAPTER 3. ARROW-DEBREU EXCHANGE ECONOMIES

De�nition 14 An economy ! 2 RLI++ is regular if Dpz (p; !) has rank L� 1for any p 2 RL�1++ such that z (p; !) = 0.

De�nition 15 An equilibrium price p 2 RL�1++ is locally unique if 9 anopen set P such that p 2 P and for any p0 6= p 2 P , z (p0; !) 6= 0:

Proposition 16 A regular equilibrium price p 2 RL�1++ is locally unique.

Proof. Fix an arbitrary ! 2 RLI++: Since Dpz (p; !) has rank L � 1; byregularity of p, the Inverse function theorem - Local (see Math Appendix)applied to the map z : RL�1++ ! RL�1, directly implies local uniqueness of p 2RL�1++ .

Proposition 17 Any economy ! in a full measure Lebesgue subset of RLI++is regular.

We say then that regularity is a generic property in RLI++, as it holds in afull measure Lebesgue subset of RLI++.Proof. The statement follows by the Transversality theorem (see MathAppendix), if z t 0: We now show that z t 0: Pick an arbitrary agenti 2 I: It will be su¢ cient to show that, for any (p; !) 2 RL�1++ � RLI++ suchthat z(p; !) = 0; we can �nd a perturbation d!i 2 RL such that dz =D!iz(p; !)d!

i, for any dz 2 RL�1. Consider any perturbation d!i such thatd!i1 + pd!

i�1 = 0; for d!i�1 = (!il)

L

l=2 : Any such perturbation, leaves eachagent i 2 I demand unchanged and hence it implies D!iz(p; !)d!

i = �d!i�1,for any arbitrary d!i�1 2 RL:

Proposition 18 The set of equilibrium prices of an economy ! 2 RLI++ is asmooth manifold (see Math Appendix) of dimension LI:

Proof. Dpz (p; !) has rank L � 1, as shown in the proof of the previousproposition. The Inverse function theorem - Global (see Math Appendix)applied to z : RL�1++ � RLI++ ! RL�1; directly implies that the set p 2 z�1(0);as a function of ! 2 RLI++, is a smooth manifold of dimension LI:

3.3. COMPETITIVE EQUILIBRIUM 25

3.3.3 Di¤erentiable approach: A rough primer

The di¤erential techniques exploited to study generic local uniqueness canbe expanded to provide a general characterization of competitive equilibriaas a manifold parametrized by endowments. This characterization implies anexistence result. We sketch some of the analysis, just to provide the readerwith the �avor of the arguments.

De�nition 19 The index i(p; !) of a price p 2 RL�1++ such that z (p; !) = 0is de�ned as

i(p; !) = (�1)L�1sign jDpz (p; !)j :The index i(!) of an economy (!i)i2I is de�ned as

i(!) =X

p:z(p;!)=0

i(p; !):

Theorem 20 (Index) For any regular economy ! 2 RLI++, i(!) = 1:

Proof. The theorem is a deep mathematical result whose proof is clearlybeyond the scope of this class. Let it su¢ ce to say that the proof reliescrucially on the boundary property of excess demand. Adventurous readermight want to look at Mas Colell (1985), section 5,6, p. 201-15.

Corollary 21 Any regular economy ! has an odd number of equilibria. Inparticular, any regular economy ! 2 RLI++ has at least one equilibrium.

Corollary 22 Any economy ! 2 RLI++ has at least one equilibrium price p 2RL�1++ :Proof. By contradiction. Suppose there exist an economy ! 2 RLI++ withno equilibrium. Then, ! 2 RLI++ is regular, by de�nition of regularity - acontradiction with previous corollary.

The existence result is then a corollary of the Index theorem. It is usefulto study the simple case in which L = 2: In this case, then, z : R++ ! R.The boundary properties of the excess demand z(p; !) imply that, for any! 2 R2I++;

z(p; !) ! +1 as p! 0

z(p; !) ! �L as p!1:

26 CHAPTER 3. ARROW-DEBREU EXCHANGE ECONOMIES

As a consequence, an equilibrium exists by continuity of z(p; !). Further-more, suppose ! is regular, and let the prices pj such that z(p; !) = 0 beordered, so that pj < pj+1; j = 1; 2; :::: Then @z(p;!)

@pjp=p1 < 0: Actually,

@z(p;!)@p

���p=pjn < 0 for j odd> 0for j even

: As a consequence, i(!) = 1:

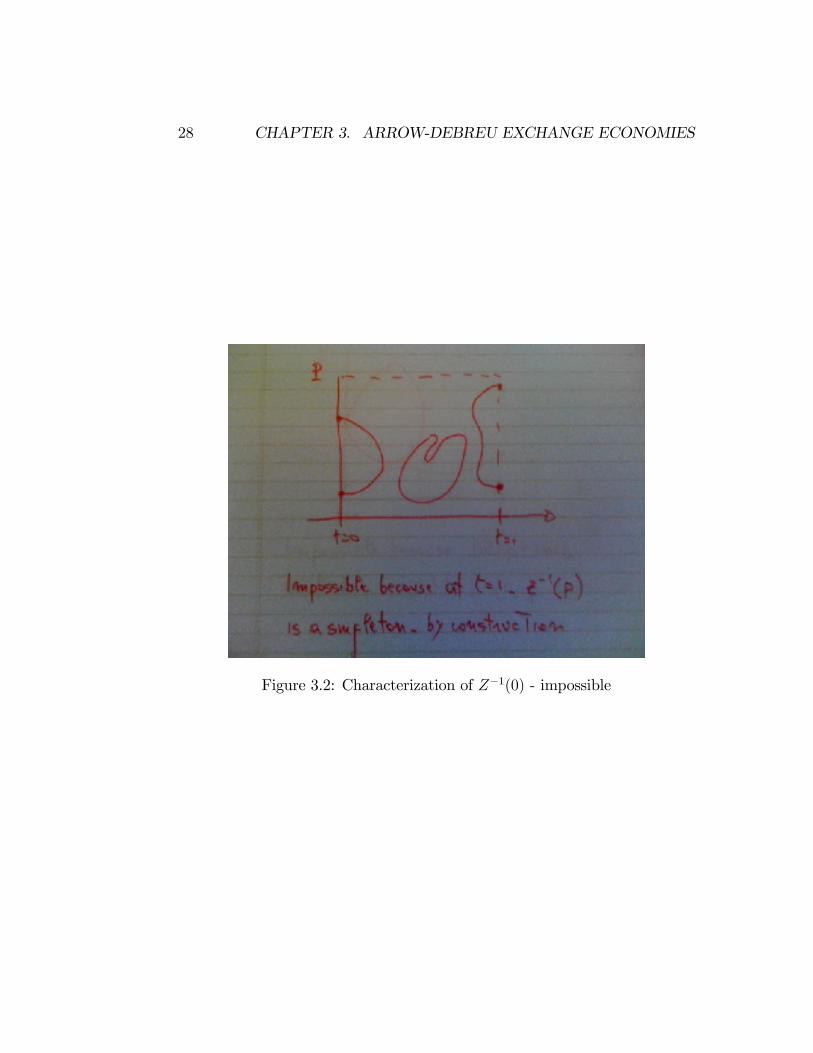

We can also try and give more sense of the arguments, o¤ of the proofof the Index theorem, required for this approach to the existence question.Let ! 2 RLI++ be an arbitrary regular economy. Pick an economy !0 2 RLI++such that there exist a unique price p 2 RL�1++ such that z(p) = 0; andDpz(p) has rank L � 1: One such economy can always be constructed bychoosing !0 2 RLI++ to be a Pareto optimal allocation. In fact, [we can showthat] generic regularity holds in the subset of economies with Pareto optimalendowments. Let t! + (1 � t)!0; for 0 � t � 1; represent a 1-dimensionalsubset of economies. Let Z(p; t) be the map Z : RL�1++ �[0; 1]! RL�1 inducedby Z(p; t) = z(p; t! + (1 � t)!0) for given (!; !0): We say that Z(p; t) is anhomotopy, or that z(p; !) and z(p; !0) are homotopic to each other. [Wecan show that] DZ(p; t) has rank L � 1 in its domain. It follows from theCorollary of the Inverse function theorem - Global (see Math Appendix) thatthe set (p; t) 2 Z�1(0); is a smooth manifold of dimension 1: [We can showthat] prices p can, without loss of generality, be restricted to a compact setP such that Z�1(0)\P � [0; 1] = ?:4 As a consequence Z�1(0) is a compactsmooth manifold of dimension 1: By the Classi�cation theorem (see MathAppendix), Z�1(0) is then homeomorphic to a countable set of segmentsin R and of circles S.5 Regularity of Z�1(0) at the boundary, t = 0 andt = 1 and the property that Z�1(0) \ P � [0; 1] = ? imply that at least onecomponent of Z�1(0) is homeomorphic to a line with boundary at t = 0 andt = 1: It looks confusing, but it�s easier with a few �gures.

The only possible representation of Z�1(0) is then as in the following�gure. Therefore: an equilibrium price p 2 P exists, for any t 2 [0; 1];and furthermore, for a full-measure Lebesgue subset of [0; 1] the number ofequilibria is odd.

4This is a consequence of the boundary conditions of excess demand systems. In otherwords, we could adopt the alternative normalization, restricting prices in the simplex �;a compact set, and show that equilibrium prices are never on @�:

5Along a component of Z�1(0) (a line or a circle), a change in index occurs when themanifold folds.

3.3. COMPETITIVE EQUILIBRIUM 27

Figure 3.1: Characterization of Z�1(0) - impossible

28 CHAPTER 3. ARROW-DEBREU EXCHANGE ECONOMIES

Figure 3.2: Characterization of Z�1(0) - impossible

3.3. COMPETITIVE EQUILIBRIUM 29

Figure 3.3: Characterization of Z�1(0) - impossible

30 CHAPTER 3. ARROW-DEBREU EXCHANGE ECONOMIES

Figure 3.4: Characterization of Z�1(0)

3.4. MATHEMATICAL APPENDIX 31

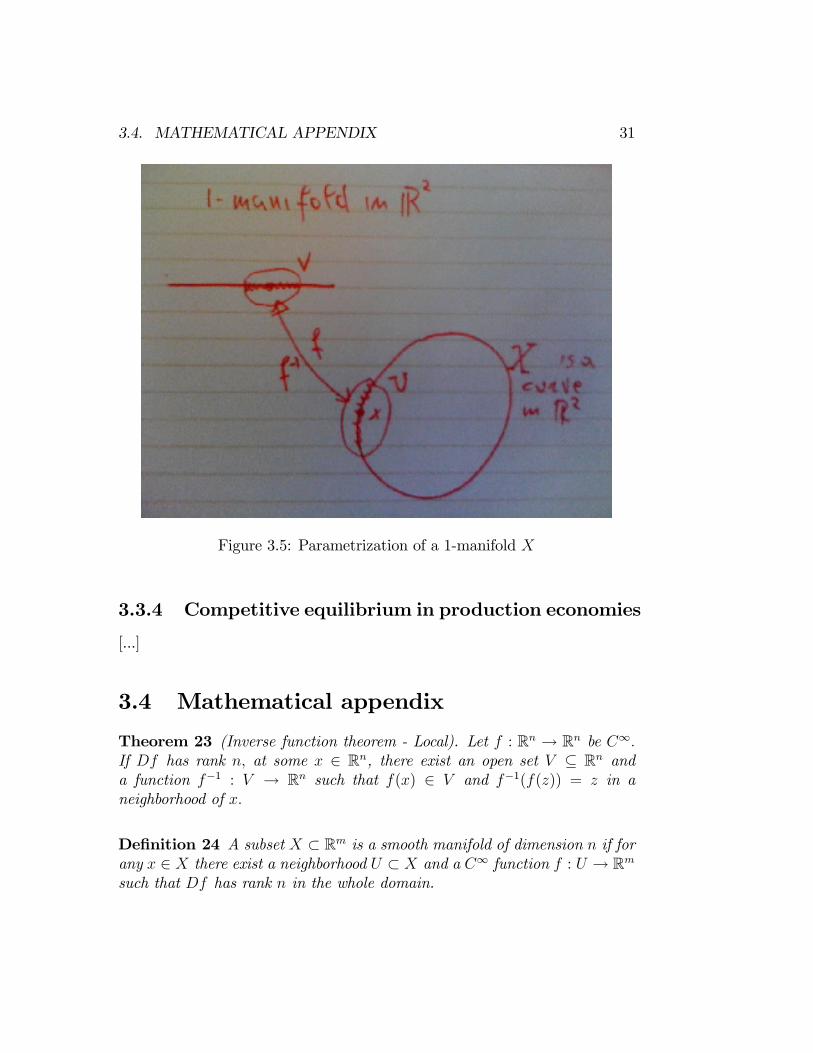

Figure 3.5: Parametrization of a 1-manifold X

3.3.4 Competitive equilibrium in production economies

[...]

3.4 Mathematical appendix

Theorem 23 (Inverse function theorem - Local). Let f : Rn ! Rn be C1:If Df has rank n; at some x 2 Rn, there exist an open set V � Rn anda function f�1 : V ! Rn such that f(x) 2 V and f�1(f(z)) = z in aneighborhood of x:

De�nition 24 A subset X � Rm is a smooth manifold of dimension n if forany x 2 X there exist a neighborhood U � X and a C1 function f : U ! Rmsuch that Df has rank n in the whole domain.

32 CHAPTER 3. ARROW-DEBREU EXCHANGE ECONOMIES

Let f(U) = V: A smooth manifold of dimension n is then locally parame-trized by a restriction of the function f�1 on the open set V \Rn�f0gm�n,in the sense that f�1 maps V \ Rn � f0gm�n onto U; a neighborhood of xon X.

Example 25 An example of a 1-manifold of R2 is S =�x 2 R2

��(x1)2 + (x2)2 = 1,the circle. An explicit parametrization for S can be constructed as follows.Seeing a restriction of f�1on the open set V \ Rn � f0gm�n as a map�i : Rn ! Rm; the following four maps are su¢ cient to parametrize S:

�1(x1) =

�x1;

q1� (x1)2

�if x2 > 0

�2(x1) =

�x1;�

q1� (x1)2

�if x2 < 0

�3(x2) =

�q1� (x2)2; x2

�if x1 > 0

�4(x2) =

��q1� (x2)2; x2

�if x1 < 0

De�nition 26 Let f : Rm ! Rn; m � n; be C1: f is transversal to 0,denoted f t 0; if Df has rank n for any x 2 Rm such that f(x) = 0:

Theorem 27 (Transversality). Let f : Rm++ ! Rn++; m � n; be C1 andtransversal to 0, f t 0: Decompose any vector x 2 Rm++ as x =

�x1x2

�; with

x1 2 Rm�n++ ; x2 2 Rn++: Then Dx2f(x) has rank n for all x in a Lebesguemeasure-1 subset of Rm++:

De�nition 28 A subset X � Rm is a smooth manifold with boundary ofdimension n if for any x 2 X there exist a neighborhood U � X and a C1

function f : U ! Rm�1 �R+ such that Df has rank n in the whole domain.

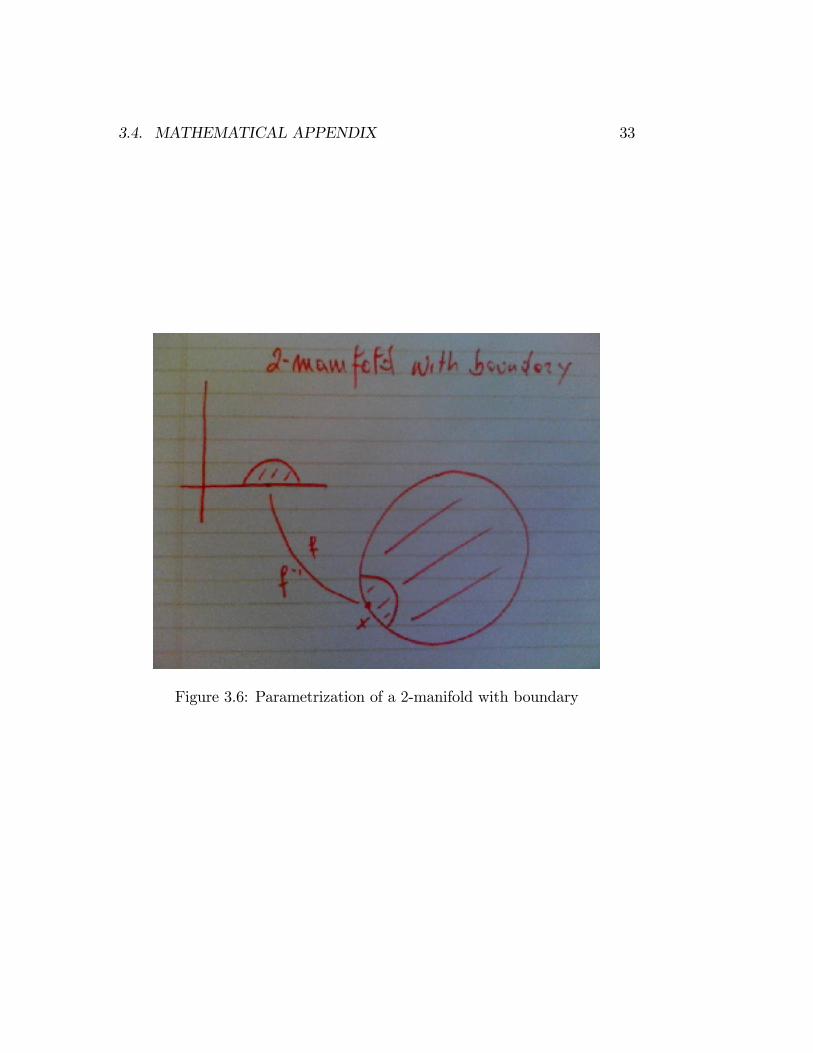

The boundary @X of X is de�ned by @X = f�1(f0gm�1�R+)\X: It canbe shown that, if X � Rm is a smooth manifold with boundary of dimensionn; then @X is a smooth manifold (without boundary) of dimension n� 1:

Example 29 An example of a smooth manifold with boundary of dimension2 in R2 is S =

�x 2 R2

��(x1)2 + (x2)2 � 1, the sphere. A parametrizationfor can be constructed S, by means of a series of maps �i : R2 ! R2+; alongthe lines of the parametrization of the circle, S: Furthermore, @S =S:

3.4. MATHEMATICAL APPENDIX 33

Figure 3.6: Parametrization of a 2-manifold with boundary

34 CHAPTER 3. ARROW-DEBREU EXCHANGE ECONOMIES

Theorem 30 (Inverse function theorem - Global) Let f : Rm ! Rn;m � n; be C1: Suppose that Dxf has rank n for any x 2 Rm. Then f�1(0) =fx 2 Rm jf(x) = 0g is a smooth manifold of dimension m� n:

Corollary 31 Let f : Rn� [0; 1]! Rn be C1: Suppose that Dxf has rank nfor any (x; t) 2 Rn � [0; 1]. Then f�1(0) = f(x; t) 2 Rn � [0; 1] jf(x; t) = 0gis a smooth 1�manifold with boundary:

Theorem 32 (Classi�cation) Every compact smooth 1�manifold is home-omorphic to a disjoint union of countably many copies of segments in R andof S.

Furthermore, @ f�1(0) = fx 2 Rn jf(x; 0) = 0g [ fx 2 Rn jf(x; 1) = 0g :

3.4.1 References

The main reference is:

A. Mas-Colell (1985): The Theory of General Economic Equilibrium: ADi¤erentiable Approach, Econometric Society Monograph, CambridgeUniversity Press.

But, as Andreu told me once, "I do not hate students so much that Iwould give them this book to read." Similar comments hold, in my opinion,for

Y. Balasko (1988): Foundations of the Theory of General Equilibrium, Aca-demic Press.

You are then left with:

A. Mas-Colell, M. Whinston, and J. Green (1995): Microeconomic Theory,Oxford University Press, ch. 17.D.

A. Mas-Colell, Four Lectures on the Di¤erentiable Approach to GeneralEquilibrium Theory, in A. A. Ambrosetti, F. Gori, and R. Lucchetti(eds.), Lecture Notes in Mathematics, No. 1330, Springer-Verlag, Berlin,1986.

3.5 Strategic foundations

[...]

Chapter 4

Two-period economies

In a two-period pure exchange economy we study �nancial market equilib-ria. In particular, we study the welfare properties of equilibria and theirimplications in terms of asset pricing.In this context, as a foundation for macroeconomics and �nancial eco-

nomics, we study su¢ cient conditions for aggregation, so that the standardanalysis of one-good economies is without loss of generality, su¢ cient condi-tions for the representative agent theorem, so that the standard analysis ofsingle agent economies is without loss of generality.The No-arbitrage theorem and the Arrow theorem on the decentraliza-

tion of equilibria of state and time contingent good economies via �nancialmarkets are introduced as useful means to characterize �nancial market equi-libria.

4.1 Arrow-Debreu economies

Consider an economy extending for 2 periods, t = 0; 1. Let i 2 f1; :::; Igdenote agents and l 2 f1; :::; Lg physical goods of the economy. In addition,the state of the world at time t = 1 is uncertain. Let f1; :::; Sg denote thestate space of the economy at t = 1. For notational convenience we typicallyidentify t = 0 with s = 0, so that the index s runs from 0 to S:De�ne n = L(S+1): The consumption space is denoted then by X � Rn+.

Each agent is endowed with a vector !i = (!i0; !i1; :::; !

iS), where !

is 2 RL+;

for any s = 0; :::S. Let ui : X �! R denote agent i�s utility function. Wewill assume:

35

36 CHAPTER 4. TWO-PERIOD ECONOMIES

Assumption 1 !i 2 Rn++ for all i

Assumption 2 ui is continuous, strongly monotonic, strictly quasiconcaveand smooth, for all i (see Magill-Quinzii, p.50 for de�nitions and details).Furthermore, ui has a Von Neumann-Morgernstern representation:

ui(xi) = ui(xi0) +SXs=1

probsui(xis)

Suppose now that at time 0, agents can buy contingent commodities.That is, contracts for the delivery of goods at time 1 contingently to therealization of uncertainty. Denote by xi = (xi0; x

i1; :::; x

iS) the vector of all

such contingent commodities purchased by agent i at time 0, where xis 2 RL+;for any s = 0; :::; S: Also, let x = (x1; :::; xI):Let � = (�0; �1; :::; �S); where �s 2 RL+ for each s; denote the price of

state contingent commodities; that is, for a price �ls agents trade at time 0the delivery in state s of one unit of good l:Under the assumption that the markets for all contingent commodities

are open at time 0, agent i�s budget constraint can be written as1

�0(xi0 � !i0) +

SXs=0

�s(xis � !is) = 0 (4.1)

De�nition 33 An Arrow-Debreu equilibrium is a (x�; ��) such that

1: x�i 2 argmaxui(xi) s.t. �0(xi0 � !i0) +

SXs=0

�s(xis � !is) = 0; and

2:IXi=1

x�i � !is = 0, for any s = 0; 1; :::; S

Observe that the dynamic and uncertain nature of the economy (con-sumption occurs at di¤erent times t = 0; 1 and states s 2 S) does notmanifests itself in the analysis: a consumption good l at a time t and state sis treated simply as a di¤erent commodity than the same consumption goodl at a di¤erent time t0 or at the same time t but di¤erent state s0. This is

1We write the budget constraint with equality. This is without loss of generality undermonotonicity of preferences, an assumption we shall maintain.

4.1. ARROW-DEBREU ECONOMIES 37

the simple trick introduced in Debreu�s last chapter of the Theory of Value.It has the fundamental implication that the standard theory and results ofstatic equilibrium economies can be applied without change to our dynamic)environment. In particular, then, under the standard set of assumptions onpreferences and endowments, an equilibrium exists and the First and SecondWelfare Theorems hold.2

De�nition 34 Let (x�; ��) be an Arrow-Debreu equilibrium. We say that x�

is a Pareto optimal allocation if there does not exist an allocation y 2 XI

such that

1: u(yi) � u(x�i) for any i = 1; :::; I (strictly for at least one i), and

2:IXi=1

yi � !is = 0, for any s = 0; 1; :::; S

Theorem 35 Any Arrow-Debreu equilibrium allocation x� is Pareto Opti-mal.

Proof. By contradiction. Suppose there exist a y 2 X such that 1) and 2)in the de�nition of Pareto optimal allocation are satis�ed. Then, by 1) inthe de�nition of Arrow-Debreu equilibrium, it must be that

��0(yi0 � !i0) +

SXs=0

��s(yis � !is) � 0;

for all i; and

��0(yi0 � !i0) +

SXs=0

��s(yis � !is) > 0;

for at least one i.Summing over i, then

��0

IXi=1

(yi0 � !i0) +SXs=0

��s

IXi=1

(yis � !is) > 0

which contradicts requirement 2) in the de�nition of Pareto optimal alloca-tion.The proof exploits strict monotonicity of preferences. Where?2Having set de�nitions for 2-periods Arrow-Debreu economies, it should be apparent

how a generalization to any �nite T -periods economies is in fact e¤ectively straightforward.In�nite horizon will be dealt with in successive notes.

38 CHAPTER 4. TWO-PERIOD ECONOMIES

4.2 Financial market economies

Consider the 2-period economy just introduced. Suppose now contingentcommodities are not traded. Instead, agents can trade in spot markets andin j 2 f1; :::; Jg assets. An asset j is a promise to pay ajs � 0 units of goodl = 1 in state s = 1; :::; S.3 Let aj = (a

j1; :::; a

jS): To summarize the payo¤s

of all the available assets, de�ne the S � J asset payo¤ matrix

A =

0@ a11 ::: aJ1::: :::a1S ::: aJS

1A :It will be convenient to de�ne as to be the s-th row of the matrix. Note thatit contains the payo¤ of each of the assets in state s.Let p = (p0; p1; :::; pS), where ps 2 RL+ for each s, denote the spot price

vector for goods. That is, for a price pls agents trade one unit of good lin state s: Recall the de�nition of prices for state contingent commodities inArrow-Debreu economies, denoted �: Note the di¤erence. Let good l = 1at each date and state represent the numeraire; that is, p1s = 1, for alls = 0; :::; S.Let xisl denote the amount of good l that agent i consumes in good s. Let

q = (q1; :::; qJ) 2 RJ+, denote the prices for the assets.4 Note that the pricesof assets are non-negative, as we normalized asset payo¤ to be non-negative.Given prices (p; q) and the asset structure A, any agent i picks a con-

sumption vector xi 2 X and a portfolio zi 2 RJ to

maxui(xi)

s.t.

p0(xi0 � !i0) = �qzi

ps(xis � !is) = Asz

i; for s = 1; :::S:

3The non-negativity restriction on asset payo¤s is just for notational simplicity.4Quantities will be row vectors and prices will be column vectors, to avoid the annoying

use of transposes.

4.2. FINANCIAL MARKET ECONOMIES 39

De�nition 36 A Financial markets equilibrium is a (x�; z�; p�; q�) such that

1: x�i 2 argmaxui(xi) s.t.

p0(xi0 � !i0) = �qzi; and

ps(xis � !is) = asz

i; for s = 1; :::S; and furthermore

2:

IXi=1

x�i � !is = 0, for any s = 0; 1; :::; S; andIXi=1

z�i

Financial markets equilibrium is the equilibrium concept we shall careabout. This is because i) Arrow-Debreu markets are perhaps too demanding arequirement, and especially because ii) we are interested in �nancial marketsand asset prices q in particular. Arrow-Debreu equilibrium will be a usefulconcept insofar as it represents a benchmark (about which we have a wealthof available results) against which to measure Financial markets equilibrium.

Remark 37 The economy just introduced is characterized by asset marketsin zero net supply, that is, no endowments of assets are allowed for. It isstraightforward to extend the analysis to assets in positive net supply, e.g.,stocks. In fact, part of each agent i�s endowment (to be speci�c: the projectionof his/her endowment on the asset span, < A >= f� 2 RS : � = Az; z 2RJg) can be represented as the outcome of an asset endowment, ziw; that is,letting !i1 = (!

i11; :::; !

i1S), we can write

!i1 = wi1 + Az

iw

and proceed straightforwardly by constructing the budget constraints and theequilibrium notion.

No Arbitrage

Before deriving the properties of asset prices in equilibrium, we shall investsome time in understanding the implications that can be derived from themilder condition of no-arbitrage. This is because the characterization of no-arbitrage prices will also be useful to characterize �nancial markets equilbria.For notational convenience, de�ne the (S + 1)� J matrix

W =

��qA

�:

40 CHAPTER 4. TWO-PERIOD ECONOMIES

De�nition 38 W satis�es the No-arbitrage condition if there does not exista

there does not exist a z 2 RJ such that Wz > 0:5

The No-Arbitrage condition can be equivalently formulated in the follow-ing way. De�ne the span of W to be

< W >= f� 2 RS+1 : � = Wz; z 2 RJg:

This set contains all the feasible wealth transfers, given asset structure A.Now, we can say that W satis�es the No-arbitrage condition if

< W >\RS+1+ = f0g:

Clearly, requiring that W = (�q; A) satis�es the No-arbitrage condition isweaker than requiring that q is an equilibrium price of the economy (withasset structure A). By strong monotonicity of preferences, No-arbitrage isequivalent to requiring the agent�s problem to be well de�ned. The nextresult is remarkable since it provides a foundation for asset pricing basedonly on No-arbitrage.

Theorem 39 (No-Arbitrage theorem)

< W >\RS+1+ = f0g () 9�̂ 2 RS+1++ such that �̂W = 0:

First, observe that there is no uniqueness claim on the �̂, just existence.Next, notice how �̂W = 0 implies �̂� = 0 for all � 2< W > : It then providesa pricing formula for assets:

�̂W =

0@ :::

��̂0qj + �̂1aj1 + :::+ �̂SajS

:::

1A =

0@ :::0:::

1AJx1

and, rearranging, we obtain for each asset j,

qj = �1aj1 + :::+ �Sa

jS; for �s =

�̂s�̂0

(4.2)

5Wz > 0 requires that all components of Wz are � 0 and at least one of them > 0:

4.2. FINANCIAL MARKET ECONOMIES 41

Note how the positivity of all components of �̂ was necessary to obtain(4.2).Proof. =) De�ne the simplex in RS+1+ as � = f� 2 RS+1+ :

PSs=0 � s = 1g.

Note that by the No-arbitrage condition, < W >T� is empty. The proof

hinges crucially on the following separating result, a version of Farkas Lemma,which we shall take without proof.

Lemma 40 Let X be a �nite dimensional vector space. Let K be a non-empty, compact and convex subset of X. Let M be a non-empty, closed andconvex subset of X. Furthermore, let K and M be disjoint. Then, thereexists �̂ 2 Xnf0g such that

sup�2M

�̂� < inf�2K

�̂� :

Let X = RS+1+ , K = � and M =< W >. Observe that all the requiredproperties hold and so the Lemma applies. As a result, there exists �̂ 2Xnf0g such that

sup�2<W>

�̂� < inf�2�

�̂� : (4.3)

It remains to show that �̂ 2 RS+1++ : Suppose, on the contrary, that thereis some s for which �̂s � 0. Then note that in (4.3 ), the RHS� 0: By (4.3),then, LHS < 0: But this contradicts the fact that 0 2< W > .We still have to show that �̂W = 0, or in other words, that �̂� = 0 for

all � 2< W >. Suppose, on the contrary that there exists � 2< W > suchthat �̂� 6= 0: Since < W > is a subspace, there exists � 2 R such that�� 2< W > and �̂�� is as large as we want. However, RHS is boundedabove, which implies a contradiction.(= The existence of �̂ 2 RS+1++ such that �̂W = 0 implies that �̂� = 0

for all � 2< W > : By contradiction, suppose 9� � 2< W > and such that� � 2 RS+1+ nf0g: Since �̂ is strictly positive, �̂� � > 0; the desired contradiction.

A few �nal remarks to this section.

Remark 41 An asset which pays one unit of numeraire in state s and noth-ing in all other states (Arrow security), has price �s according to (4.2). Suchasset is called Arrow security.

42 CHAPTER 4. TWO-PERIOD ECONOMIES

Remark 42 Is the vector �̂ obtained by the No-arbitrage theorem unique?Notice how (??) de�nes a system of J equations and S unknowns, representedby �. De�ne the set of solutions to that system as

R(q) = f� 2 RS++ : q = �Ag:

Suppose, the matrix A has rank J 0 � J (that it, A has J 0 linearly independentcolumn vectors and J 0 is the e¤ective dimension of the asset space). Ingeneral, then R(q) will have dimension S � J 0. It follows then that, in thiscase, the No-arbitrage theorem restricts �̂ to lie in a S � J 0 + 1 dimensionalset. If we had S linearly independent assets, the solution set has dimensionzero, and there is a unique � vector that solves (??). The case of S linearlyindependent assets is referred to as Complete markets.

Remark 43 Let preferences be Von Neumann-Morgernstern:

ui(xi) = ui(xi0) +X

s=1;:::;S

probsui(xis)

whereX

s=1;:::;S

probs = 1: Let then ms =�sprobs

. Then

qj = E (mAj)

In this representation of asset prices the vector m 2 RS++ is called Stochasticdiscount factor.

4.2.1 The stochastic discount factor

In the previous section we showed the existence of a vector that provides thebasis for pricing assets in a way that is compatible with equilibrium, albeitmilder than that. In this section, we will strengthen our assumptions andstudy asset prices in a full-�edged economy. Among other things, this willallow us to provide some economic content to the vector �Recall the de�nition of Financial market equilibrium. Let MRSis(x

i)denote agent i�s marginal rate of substitution between consumption of thenumeraire good 1 in state s and consumption of the numeraire good 1 atdate 0:

4.2. FINANCIAL MARKET ECONOMIES 43

MRSis(xi) =

@ui(xis)

@xi1s

@ui(xi0)

@xi10

Let MRSi(xi) = (: : :MRSis(xi) : : :) denote the vector of marginal rates

of substitution for agent i, an S dimentional vector. Note that, under theassumption of strong monotonicity of preferences, MRSi(xi) 2 RS++:By taking the First Order Conditions (necessary and su¢ cient for a max-

imum under the assumption of strict quasi-concavity of preferences) withrespect to zij of the individual problem for an arbitrary price vector q, weobtain that

qj =SXs=1

probsMRSis(x

i)ajs = E�MRSi(xi) � aj

�; (4.4)

for all j = 1; :::; J and all i = 1; :::; I; where of course the allocation xi is theequilibrium allocation. At equilibrium, therefore, the marginal cost of onemore unit of asset j, qj, is equalized to the marginal valuation of that agentfor the asset�s payo¤,

PSs=1 probsMRS

is(x

i)ajs.Compare equation (4.4) to the previous equation (4.2). Clearly, at any

equilibrium, condition (4.4) has to hold for each agent i. Therefore, in equi-librium, the vector of marginal rates of substitution of any arbitrary agent ican be used to price assets; that is any of the agents�vector of marginal ratesof substitution (normalized by probabilities) is a viable stochastic discountfactor m:In other words, any vector (: : : probsMRSis(x

i) : : :) belongs to R(q) and ishence a viable � for the asset pricing equation (4.2). But recall that R(q) is ofdimension S�J 0; where J 0 is the e¤ective dimension of the asset space. Thehigher the the e¤ective dimension of the asset space (sloppily said, the larger�nancial markets) the more aligned are agents�marginal rates of substitutionat equilibrium (sloppily said, the smaller are unexploited gains from tradeat equilibrium). In the extreme case, when markets are complete (that is,when the rank of A is S), the set R(q) is in fact a singleton and hence theMRSi(xi) are equalized across agents i at equilibrium: MRSi(xi) = MRS;for any i = 1; :::; I:

Problem 44 Write the Pareto problem for the economy and show that, atany Pareto optimal allocation, x; it is the case that MRSi(xi) = MRS; for

44 CHAPTER 4. TWO-PERIOD ECONOMIES

any i = 1; :::; I: Furthermore, show that an allocation x which satis�es thefeasibility conditions (market clearing) for goods and is such thatMRSi(xi) =MRS; for any i = 1; :::; I: is Pareto optimal.

We conclude that, when markets are Complete, equilibrium allocationsare Pareto optimal. That is, the First Welfare theorem holds for Financialmarket equilibria when markets are Complete.

Problem 45 (Economies with bid-ask spreads)Extend our basic two-periodincomplete market economy by assuming that, given an exogenous vector 2RJ++:

the buying price of asset j is qj + jwhile

the selling price of asset j is qjfor any j = 1; :::; J:and exogenous. Write the budget constraint and theFirst Order Conditions for an agent i�s problem. Derive an asset pricingequationfor qj in terms of intertemporal marginal rates of substitution atequilibrium.

4.2.2 Arrow theorem

The Arrow theorem is the fondamental decentralization result in �nancialeconomics. It states su¢ cient conditions for a form of equivalence betweenthe Arrow-Debreu and the Financial market equilibrium concepts. It wasessentially introduced by Arrow (1952). The proof of the theorem introducesa reformulation of the budget constraints of the Financial market economywhich focuses on feasible wealth transfers across states directly, on the spanof A,

< A >=�� 2 RS : � = Az; z 2 RJ

in particular. Such a reformulation is important not only in itself but as alemma for welfare analysis in Financial market economies.

Proposition 46 Let (x�; ��) represent an Arrow-Debreu equilibrium. Sup-pose rank(A) = S (�nancial markets are Complete). Then (x�; z�; p�; q�) isa Financial market equilibrium, where

��s = �sp�s; for any s = 1; :::; S: and

q� =

SXs=1

probsMRSis(x

i�)As

4.2. FINANCIAL MARKET ECONOMIES 45

Futhermore, the converse also holds: if (x�; z�; p�; q�) is a Financial marketequilibrium of an economy with rank(A) = S, (x�; ��) represents an Arrow-Debreu equilibrium, where ��s = �sp

�s; for any s = 1; :::; S:

Proof. Financial market equilibrium prices of assets q� satisfy No-arbitrage.There exists then a vector �̂ 2 RS+1++ such that �̂W = 0; or q� = �A. Thebudget constraints in the �nancial market economy are

p�0�xi�0 � !i0

�+ q�zi� = 0

p�s�xi�s � !is

�= Asz

i�; for s = 1; :::S:

Substituting q = �A; expanding the �rst equation, and writing the con-straints at time 1 in vector form, we obtain:

p�0�xi�0 � !i0

�+

SXs=1

�sp�s

�xi�s � !is

�= 0 (4.5)266664

::

p�s (xi�s � !is)::

377775 2 < A > (4.6)

But if rank(A) = S; it follows that< A >= RS; and the constraint

266664::

p�s (xi�s � !is)::

377775 2<A > is never binding. Each agent i�s problem is then subject only to

p�0�xi�0 � !i0

�+

SXs=1

�sp�s

�xi�s � !is

�= 0;

the budget constraint in the Arrow-Debreu economy with

��s = �sp�s; for any s = 1; :::; S:

Furthermore, by No-arbitrage

q� =

SXs=1

probsMRSis(x

i�)As:

46 CHAPTER 4. TWO-PERIOD ECONOMIES

Finally, using �s = probsMRSis(x

i�), for any s = 1; :::; S; proves the re-sult. (Recall that, with Complete markets MRSi(xi�) = MRS; for anyi = 1; :::; I.)The converse is straightforward.

4.2.3 Existence

We do not discuss here in detail the issue of existence of a �nancial marketequilibrium when markets are incomplete (when they are complete, existencefollows from the equivalence with Arrow-Debreu equilibrium provided byArrow theorem). A sketch of the proof however follows.The proof is a modi�cation of the existence proof for Arrow-Debreu equi-

librium. By Arrow theorem, fact, we can reduce the equilibrium system to anexcess demand system for consumption goods; that is, we can solve out for theasset portfolios zi�s. The only conceptual problem with the proof is that theboundary condition on the excess demand system might not be guaranteed as

each agent�s excess demand is restricted by

266664::

ps (xis � !is)::

377775 2< A > : Thisis where the Cass trick comes in handy. It is in fact an important Lemma.

Cass trick. For any Financial market economy, consider a modi�ed econ-

omy where the constraint

266664::

ps (xis � !is)::

377775 2< A > is imposed on all

agents i = 2; :::; I but not on agent i = 1: Any equilibrium of theFinancial Market economy is an equilibrium of the modi�ed economy,and any equilibrium of the modi�ed economy is a Financial marketequilibrium.

Proof. Consider an equilibrium of the modi�ed economy in the state-ment. At equilibrium,

PIi=1 ps (x

is � !is) = 0: Therefore,

PIi=2 ps (x

is � !is) =

4.2. FINANCIAL MARKET ECONOMIES 47

�ps (x1s � !1s) : But

266664::

ps (xis � !is)::

377775 2< A >; for any i = 2; :::; I; and

hencePI

i=2 ps (xis � !is) 2< A > : Since

PIi=2 ps (x

is � !is) = �ps (x1s � !1s) ;

it follows that �ps (x1s � !1s) 2< A >; and hence that ps (x1s � !1s) 2<A > : Therefore, the constraint ps (x1s � !1s) 2< A > must necessarily holdat an equilibrium of the modi�ed economy. In other words, the constraintps (x

1s � !1s) 2< A > is not binding at a Financial market equilibrium. The

equivalence between the modi�ed economy and the Financial Market econ-omy is now straightforward.

4.2.4 Constrained Pareto optimality

Under Complete markets, the First Welfare Theorem holds for Financialmarket equilibrium. This is a direct implication of Arrow theorem.

Proposition 47 Let (x�; z�; p�; q�) be a Financial market equilibrium of aneconomy with Complete markets (with rank(A) = S): Then x� is a Paretooptimal allocation.

However, under Incomplete markets Financial market equilibria are gener-ically ine¢ cient in a Pareto sense. That is, a planner could �nd an allocationthat improves some agents without making any other agent worse o¤.

Theorem 48 At a Financial Market Equilibrium (x�; z�; p�; q�) of an incom-plete �nancial market economy, that is, of an economy with rank(A) < S,the allocation x� is generically6 not Pareto Optimal.

6We say that a statement holds generically when it holds for a full Lebesgue-measuresubset of the parameter set which characterizes the economy. In these notes we shallassume that the an economy is parametrized by the endowments for each agent, the assetpayo¤ matrix, and a two-parameter parametrization of utility functions for each agent;see Magill-Shafer, ch. 30 in W. Hildenbrand and H. Sonnenschein (eds.), Handbook ofMathematical Economics, Vol. IV, Elsevier, 1991.

48 CHAPTER 4. TWO-PERIOD ECONOMIES

Proof. From the proof of Arrow theorem, we can write the budget con-straints of the Financial market equilibrium as:

p�0�xi�0 � !i0

�+

SXs=1

�sp�s

�xi�s � !is

�= 0 (4.7)266664

::

p�s (xi�s � !is)::

377775 2 < A > (4.8)

for some � 2 RS++: Pareto optimality of x�requires that there does not existan allocation y such that

1: u(yi) � u(x�i) for any i = 1; :::; I (strictly for at least one i), and

2:IXi=1

yi � !is = 0, for any s = 0; 1; :::; S

Reproducing the proof of the First Welfare theorem, it is clear that, if such

a y exists, it must be that

266664::

p�s (yi�s � !is)::

377775 =2< A >; for some i = 1; :::; I;otherwise the allocation y would be budget feasible for all agent i at theequilibrium prices. Generic Pareto sub-optimality of x� follows then directlyfrom the following Lemma, which we leave without proof.7

Lemma 49 Let (x�; z�; p�; q�) represent a Financial Market Equilibrium ofan economy with rank(A) < S: For a generic set of economies, the con-

straints

266664::

p�s (xi�s � !is)::

377775 2< A > are binding for some i = 1; :::; I.7The proof can be found in Magill-Shafer, ch. 30 in W. Hildenbrand and H. Sonnen-

schein (eds.), Handbook of Mathematical Economics, Vol. IV, Elsevier, 1991. It requiresmathematical tecniques from di¤erential topology which are not appropriate to be intro-duced in this course.

4.2. FINANCIAL MARKET ECONOMIES 49

Remark 50 The Lemma implies a slightly stronger result than generic Paretosub-optimality of Financial market equilibrium for economies with incompletemarkets. It implies in fact that a Pareto improving allocation can be foundlocally around the equilibrium, as a perturbation of the equilibrium.

Pareto optimality might however represent too strict a de�nition of socialwelfare of an economy with frictions which restrict the consumption set, as inthe case of incomplete markets. In this case, markets are assumed incompleteexogenously. There is no reason in the fundamentals of the model why theyshould be, but they are. Under Pareto optimality, however, the social welfarenotion does not face the same contraints. For this reason, we typically de�ne aweaker notion of social welfare, Constrained Pareto optimality, by restrictingthe set of feasible allocations to satisfy the same set of constraints on theconsumption set imposed on agents at equilibrium. In the case of incompletemarkets, for instance, the feasible wealth vectors across states are restrictedto lie in the span of the payo¤ matrix. That can be interpreted as theeconomy�s ��nancial technology�and it seems reasonable to impose the sametechnological restrictions on the planner�s reallocations. The formalizationof an e¢ ciency notion capturing this idea follows. Let xit=1 = (x

is)Ss=1 2 RSL+ ;

and similarly pt=1 = (ps)Ss=1 2 RSL+

De�nition 51 (Diamond, 1968; Geanakoplos-Polemarchakis, 1986) Let (x�; z�; p�; q�)represent a Financial market equilibrium of an economy whose consumptionset at time t = 1 is restricted by

xit=1;2 B(pt=1); for any i = 1; :::; I

In this economy, the allocation x� is Constrained Pareto optimal if there doesnot exist a (y; �) such that

1: u(yi) � u(x�i) for any i = 1; :::; I, strictly for at least one i

2:IXi=1

yis � !is = 0, for any s = 0; 1; :::; S

and3: yit=1 2 B(g�t=1(!; �)); for any i = 1; :::; I

where g�t=1(!; �) is a vector of equilibrium prices for spot markets at t = 1opened after each agent i = 1; :::; I has received income transfer A�i:

50 CHAPTER 4. TWO-PERIOD ECONOMIES

The constraint on the consumption set restricts only time 1 consump-tion allocations. More general constraints are possible but these formulationis consistent with the typical frictions we encounter in economics, e.g., on�nancial markets. It is important that the constraint on the consumptionset depends in general on g�t=1(!; �), that is on equilibrium prices for spotmarkets opened at t = 1 after income transfers to agents. It implicit identi-�es income transfers (besides consumption allocations at time t = 0) as theinstrument available for Constrained Pareto optimality; that is, it implicitlyconstrains the planner implementing Constraint Pareto optimal allocationsto interact with markets, speci�cally to open spot markets after transfers.On the other hand, the planner is able to anticipate the spot price equilib-rium map, g�t=1(!; �); that is, to internalize the e¤ects of di¤erent transferson spot prices at equilibrium.

Proposition 52 Let (x�; z�; p�; q�) represent a Financial market equilibriumof an economy with complete markets (rank(A) = S) and whose consumptionset at time t = 1 is restricted by

xit=1 2 B � RSL+ ; for any i = 1; :::; I

In this economy, the allocation x� is Constrained Pareto optimal.

Crucially, markets are complete and B is independent of prices. Theproof is then a straightforward extension of the First Welfare theorem com-bined with Arrow theorem.8 Constraint Pareto optimality of Financial mar-ket equilibrium allocations is guaranteed as long as the constraint set B isexogenous.

Proposition 53 Let (x�; z�; p�; q�) represent a Financial market equilibriumof an economy with Incomplete markets (rank(A) < S). In this economy,the allocation x� is not Constrained Pareto optimal.

Proof. By the decomposition of the budget constraints in the proof of Arrowtheorem, this economy is equivalent to one with Complete markets whoseconsumption set at time t = 1 is restricted by

xit=1 2 B(g�t=1(!; z)); for any i = 1; :::; I; for any i = 1; :::; I8To be careful, we need to guarantee that monotonicity of preferences on RSL++ results

in monotonicity on B � RSL++: This is the case for B open. Thanks to the students fornoticing this.

4.2. FINANCIAL MARKET ECONOMIES 51

with the set B(g�t=1(!; z)) de�ned implicitly by266664::

g�s(!s; z) (xis � !is)

::

377775 2< A >; for any i = 1; :::; INote �rst of all that, by construction, p�s 2 g�s(!s; z�): Following the proof ofPareto sub-otimality of Financial market equilibrium allocations, it then fol-

lows that if a Pareto-improving y exists, it must be that

266664::

p�s (yi�s � !is)::

377775 =2<

A >; for some i = 1; :::; I; while

266664::

g�s(!s; �) (yis � !is)

::

377775 = A�i, for all

i = 1; :::; I: Generic Constrained Pareto sub-optimality of x� follows thendirectly from the following Lemma, which we leave without proof.9

Lemma 54 Let (x�; z�; p�; q�) represent a Financial Market Equilibrium ofan economy with rank(A) < S: For a generic set of economies, the con-

straints

266664::

g�s(!s; z� + dz) (yis � !is)

::

377775 = A (zi� + dzi), for some dz 2 RJIn f0gsuch that

Xi=1I

dzi = 0; are weakly relaxed for all i = 1; :::; I, strictly for at

least one.10

9The proof is due to Geanakoplos-Polemarchakis (1986). It also requires di¤erentialtopology techniques.10Once again, note that the Lemma implies that a Pareto improving allocation can be

found locally around the equilibrium, as a perturbation of the equilibrium.

52 CHAPTER 4. TWO-PERIOD ECONOMIES

There is a fundamental di¤erence between incomplete market economies,which have typically not Constrained Optimal equilibrium allocations, andeconomies with constraints on the consumption set, which have, on the con-trary, Constrained Optimal equilibrium allocations. It stands out by com-paring the respective trading constraints

g�s(!s; �)(xis�!is) = As�i; for all i and s, vs. xit=1 2 B, for all i:

The trading constraint of the incomplete market economy is determined atequilibrium, while the constraint on the consumption set is exogenous. An-other way to re-phrase the same point is the following. A planner choosing(y; �) will take into account that at each (y; �) is typically associated a dif-ferent trading constraint g�s(!s; �)(x

is � !is) = As�i; for all i and s; while any

agent i will choose (xi; zi) to satisfy p�s(xis � !is) = Aszi; for all s, taking as

given the equilibrium prices p�s:The constrained ine¢ ciency due the dependence of constraints on equilib-

rium prices is sometimes called a pecuniary externality.11 Several examples ofsuch form of externality/ine¢ ciency have been developed recently in macro-economics. Some examples are:

- Thomas, Charles (1995): "The role of �scal policy in an incomplete marketsframework," Review of Economic Studies, 62, 449�468.

- Krishnamurthy, Arvind (2003): "Collateral Constraints and the Ampli�-cation Mechanism,"

Journal of Economic Theory, 111(2), 277-292.

- Caballero, Ricardo J. and Arvind Krishnamurthy (2003): "Excessive Dol-lar Debt: Financial Development and Underinsurance," Journal of Fi-nance, 58(2), 867-94.

- Lorenzoni, Guido (2008): "Ine¢ cient Credit Booms," Review of EconomicStudies, 75 (3), 809-833.

- Kocherlakota, Narayana (2009): "Bursting Bubbles: Consequences andCauses,"

http://www.econ.umn.edu/~nkocher/km_bubble.pdf.

11The name is due to Joe Stiglitz (or is it Greenwald-Stiglitz?).

4.2. FINANCIAL MARKET ECONOMIES 53

- Davila, Julio, Jay Hong, Per Krusell, and Victor Rios Rull (2005): "Con-strained E¢ ciency in the Neoclassical Growth Model with UninsurableIdiosyncractic Shocks," mimeo, University of Pennsylvania.

Remark 55 Consider an economy whose constraints on the consumption setdepend on the equilibrium allocation:

xit=1 2 B(x�t=1; z�); for any i = 1; :::; I

This is essentially an externality in the consumption set. It is not hard toextend the analysis of this section to show that this formulation introducesine¢ ciencies and equilibrium allocations are Constraint Pareto sub-optimal.

Corollary 56 Let (x�; z�; p�; q�) represent a Financial market equilibrium ofa 1-good economy (L = 1) with Incomplete markets (rank(A) < S). In thiseconomy, the allocation x� is Constrained Pareto optimal.Proof. The constraint on the consumption set implied by incomplete mar-kets, if L = 1, can be written

(xis � !is) = Aszi:

It is independent of prices, of the form xit=1 2 B.

Remark 57 Consider an alternative de�nition of Constrained Pareto opti-mality, due to Grossman (1970), in which constraints 3 are substituted by

30:

266664::

p�s (xi�s � !is)::

377775 = Azi; for any i = 1; :::; Iwhere p� is the spot market Financial market equilibrium vector of prices.That is, the planner takes the equilibrium prices as given. It is immediate toprove that, with this de�nition of Constrained Pareto optimality, any Finan-cial market equilibrium allocation x�of an economy with Incomplete marketsis in fact Constrained Pareto optimal, independently of the �nancial marketsavailable (rank(A) � S):

54 CHAPTER 4. TWO-PERIOD ECONOMIES

Problem 58 Consider a Complete market economy (rank(A) = S) whosefeasible set of asset portfolios is restricted by:

zi 2 Z ( RJ ; for any i = 1; :::; I

A typical example is borrowing limits:

zi � �b; for any i = 1; :::; I

Are equilibrium allocations of such an economy Constrained Pareto optimal(also if L > 1)?

Problem 59 Consider a 1-good (L = 1) Incomplete market economy (rank(A) <S) which lasts 3 periods. De�ne an Financial market equilibrium for thiseconomy as well as Constrained Pareto optimality. Are Financial marketequilibrium allocations of such an economy Constrained Pareto optimal?

Problem 60 Extend our basic two-period incomplete market economy by as-suming that, given an exogenous vector 2 RJ++:

the buying price of asset j is qj + j

whilethe selling price of asset j is qj

for any j = 1; :::; J:and exogenous. 1) Suppose the asset payo¤ matrix isfull rank. Do you expect �nancial market equilibria to be Pareto e¢ cient?Carefully justify your answer. (I am not asking for a formal proof, thoughyou could actually prove this.) 2) Continue to suppose the asset payo¤ matrixis full rank. How would you de�ne Constrained Pareto e¢ ciency in thiseconomy? Do you expect �nancial market equilibria to be Constrained Paretoe¢ cient? Carefully justify your answer. (I am really not asking for a formalproof.)

4.2.5 Aggregation

Agent i�s optimization problem in the de�nition of Financial market equi-librium requires two types of simultaneous decisions. On the one hand, theagent has to deal with the usual consumption decisions i.e., she has to decidehow many units of each good to consume in each state. But she also has

4.2. FINANCIAL MARKET ECONOMIES 55