Gateway Distriparks Ltd - Business...

15

Gateway Distriparks Ltd

Transcript of Gateway Distriparks Ltd - Business...

Gateway Distriparks Ltd

Page | 1

II nnii tt

ii aatt ii

nngg

CCoo

vvee

rr aagg

ee

tt iiaa

tt iinn

gg CC

oovv

eerr aa

ggee

tt iinn

gg CC

oovv

eerr aa

ggee

gg CC

oovv

eerr aa

ggee

CCoo

vvee

rr aagg

ee

vvee

rr aagg

ee

rr aagg

ee

ggee

Gateway Distriparks Ltd

IINN

II TT

II AA

TTII NN

GG CC

OOVV

EERR

AAGG

EE ––

1133

tthh

SSee

ppttee

mmbb

eerr 22

0011

22

4

Recommendation BUY Gateway to growth!

Gateway Distriparks Ltd (GDL) is an integrated logistics player in the container movement space. It operates in three segments viz Container Freight Stations (CFS), Container Rail Operator (CTO) and Cold Chain Logistics. The company’s core business in CFS continues to remain a cash cow with EBIDTA margins of ~ 54%. CFS segment saw pressure on volumes in FY12 due to low traction at the JNPT port, however realizations have remained firm. With added capacities coming up at the Kochi port and expansion at the JNPT port, we expect CFS volumes to grow by 2.8% in FY13E and by 2.4% in FY14E. The investments in the Rail segment are getting paid off for GDL with its revenues growing by 40% in FY12 and its EBIDTA/TEU growing by a CAGR of 21% between FY10-12. The company is planning to add 5-6 rakes in FY13E and also start new shorter routes which would see rise in volumes while we expect marginal growth in margins in FY13E. Lastly, GDL is increasing its capacity in the cold chain segment by almost 2.5x of which we believe mostly would reflect in the FY13E revenues. GDL has become a Logistics conglomerate by positioning itself as one of the largest CFS player and as the largest private Container Train Operator in India. Their investment in the fast growing cold chain segment is also gaining momentum. GDL’s core business is high cash generating business with low consolidated debt of ~ Rs.104 crore as in FY12. ROE has improved from 14.3% in FY11 to 18.4% in FY12. At CMP, the stock is trading at an EV/EBIDTA and P/E of 4.8 and 10.2x its FY13E earnings respectively and looks attractive. We recommend a BUY on the stock with a price target of Rs.178 which is 28% upside from current levels.

Expansion across segments – GDL has added capacity of 50000 TEUs at the Kochi port which has got partially operational in the Q4FY12 quarter. It is expected to be fully operational by Sep 2012 once the warehouse is fully constructed. The company is also adding up capacity of additional 60000 TEUs at its JNPT operations which we believe should reflect in the FY14E revenues. We expect volumes in FY13E in the CFS segment to grow by 2.8% in FY13E and by 2.4% in FY14E.

GDL is adding up 5-6 rakes in the current fiscal in the Rail segment. They are also adding up shorter Rail routes to avoid rakes going empty. We believe this should affect the margins in the short term, however would improve the volumes and utilizations of the Rail segment significantly. We expect the volumes in this segment to grow by 13.4% % in FY13E and by 9.2% in FY14E.

GDL is expanding its capacity of pallets in the cold chain segment from 18000 in FY12 to 46000 in FY13E. Currently, this segment contributes ~ 7.5% of GDL’s revenues, 5.5% of EBIDTA and 2.5% of PAT (due to higher taxes). We expect this segment to grow by 75% in revenues to reach Rs.107 crores in FY13E.

Operational Efficiency across the segments – The EBIDTA/TEU of the CFS and Rail segments have been growing a CAGR of 23% and 21% respectively over FY10-12. The EBIDTA margins in the cold chain segment have remained stable at ~22% over the years. Consolidated margins of the company have grown by 309 bps in FY12 to 30.4%.

CMP Rs.140

Target Price Rs. 178

Sector Logistics

Stock Details

BSE Code 532662

NSE Code GDL

Bloomberg Code GDPLIN

Market Cap (Rs cr) 1485

Free Float (%) 59.60

52- wk HI/Lo (Rs) 159/118

Avg. volume BSE (Quarterly)

73,919

Face Value (Rs) 10

Dividend (FY 11) 30%

Shares o/s (Crs) 10.8

Relative Performance

1Mth 3Mth 1Yr

Gateway 3.6% 1.8% 1.0%

Sensex 1.2% 7.1% 8.2%

120

125

130

135

140

145

150

155

160

Shareholding Pattern 31

st Mar 12

Promoters Holding 40.40%

Institutional (Incl. FII) 44.78%

Corporate Bodies 5.08%

Public & others 9.74%

Kavita Vempalli – Research Analyst (022 3926-8173) [email protected]

Amrita Burde – Research Associate (022 3926-8223) [email protected]

Sunil Jain – VP Retail Head (022 3926-8196) [email protected]

Consolidated Net Sales

(Rs cr) Growth

(%) EBITDA (Rs cr)

Margin (%) PAT

(Rs cr) Margin

(%) EPS (Rs)

PE (x)

EV/EBITDA (x)

FY12A 823.5 36.2% 250.4 30.4% 132.0 16.0% 12.18 11.5 5.8

FY13E 947.7 15.1% 288.4 30.4% 149.0 15.7% 13.74 10.2 5.0

FY14E 1068.7 12.8% 329.0 30.8% 168.4 15.8% 15.54 9.0 4.5

Page | 2

II nnii tt

ii aatt ii

nngg

CCoo

vvee

rr aagg

ee

tt iiaa

tt iinn

gg CC

oovv

eerr aa

ggee

tt iinn

gg CC

oovv

eerr aa

ggee

gg CC

oovv

eerr aa

ggee

CCoo

vvee

rr aagg

ee

vvee

rr aagg

ee

rr aagg

ee

ggee

Gateway Distriparks Ltd

IINN

II TT

II AA

TTII NN

GG CC

OOVV

EERR

AAGG

EE ––

1133

tthh

SSee

ppttee

mmbb

eerr 22

0011

22

Company Overview

Gateway Distriparks Limited is a logistics facilitator and operates in three verticals; namely – Container Freight Stations (CFS), Inland Container Depots (ICD) with rail movement of containers to major maritime ports, and Cold Chain logistics.

The company’s CFSs offer transportation & storage, general and bonded warehousing, empty handling and several value added services. GDL operates container freight station on a pan India basis with strategic locations at JNPT, Chennai, Vizag and Kochi. GDL also had acquired rights to manage and operate Punjab Government’s Container Freight Station in 2006 for 15 years at JNPT.

GDL's rail operations are handled by its subsidiary, Gateway Rail Freight Limited (Gateway Rail) in which the Blackstone Group of USA has made a private equity investment through Blackstone GPV Capital Partners (Mauritius) V-H Ltd. Gateway Rail provides inter-modal logistics and operates its own Inland Container Depots/Dry Ports. In 2009, Blackstone invested Rs.300 crore in the rail subsidiary through cumulative convertible preference shares (CCPS) which helped the company to reduce its debts. Blackstone would hold a 37.3% to 49.9% stake depending upon the achievement of certain performance parameters. These CCPS cannot be redeemed and are compulsorily converted either by GDL or by Blackstone. GDL can exercise the call option to buy the CCPS from Blackstone after 5 years or Blackstone will have a put option to sell the shares after 10 years from the time of investment.

GDL’s cold storage business is run under the name of Snowman Logistics Ltd (SLL). GDL acquired 50.1 % in Snowman Frozen Foods Ltd to enter cold chain logistics business in JV with Mitsubishi in Nov 2006. Today, it runs through its JV with Mitsubishi, Nichirei Corporation of Japan and IFC (World Bank). In March 2010, International Finance Corporation invested Rs. 24.89 crs in the equity capital of the company. Mitsubishi Corporation, Mitsubishi Logistics Corporation and Nichirei Logistics Group Inc. are other shareholders in SLL. Snowman has a pan-India presence that offers comprehensive warehousing, transportation and distribution services. It has a fleet size of more than 100+ owned and leased reefer vehicles.

GDL’s business verticals

Source: Company & Nirmal Bang Research

Page | 3

II nnii tt

ii aatt ii

nngg

CCoo

vvee

rr aagg

ee

tt iiaa

tt iinn

gg CC

oovv

eerr aa

ggee

tt iinn

gg CC

oovv

eerr aa

ggee

gg CC

oovv

eerr aa

ggee

CCoo

vvee

rr aagg

ee

vvee

rr aagg

ee

rr aagg

ee

ggee

Gateway Distriparks Ltd

IINN

II TT

II AA

TTII NN

GG CC

OOVV

EERR

AAGG

EE ––

1133

tthh

SSee

ppttee

mmbb

eerr 22

0011

22

Revenue Break up

53%

38% 39% 38%40%

55% 53% 55%

8% 7% 8% 7%

0%

10%

20%

30%

40%

50%

60%

FY09 FY10 FY11 FY12

CFS Rail Snowman Source: Company & Nirmal Bang Research

Key milestones

1998 Completed phase I of development and commenced commercial operations at Navi Mumbai with container handling capacity at 48,000 TEUs/annum

2001 Completed phase II expansion at Navi Mumbai

Container handling capacity increases to 1,20,000 TEUs/annum

IDFC invested Rs.26 crores into GDL equity 2003 Completed phase III expansion at Navi Mumbai

Container handling capacity increases to 1,80,000 TEUs/annum. 2004 Acquisition of ICD at Garhi Harsaru, Gurgaon

Joint venture for CFS at Vizag

Acquisition of CFS at Chennai, construction of warehouse at CFS Navi Mumbai increase in capacity to 2,16,000 TEUs per annum

Temasek (Singapore) acquires 10% equity stake in GDL 2005 GDL got listed on the Stock Exchanges in India in March 2005

GDR Issue of US$ 85 Million in Dec 2005 2006 First container train rolls out of GDL's rail ICD at Garhi Harsaru, Gurgaon through

the tie-up with CONCOR in May 2006

Gateway Rail Freight Ltd. formed and over 60 acres of land in Faridabad District was acquired for 2nd rail ICD

JV with Chakiat Agencies for subsidiary – Gateway Distriparks (Kerala) Pvt. Ltd. , to start a CFS on 17 acres of land at Cochin

Acquisition of 50.1 % in Snowman Frozen Foods Ltd to enter cold chain logistics business in JV with Mitsubishi in Nov 2006

2007 GRFL signs concession agreement with Indian Railways to operate container trains in Jan 2007

GDL takes over Punjab Conware's CFS near JNPT, Navi Mumbai under 15 years' Operation & Management (O&M) Agreement in Feb 2007

Gateway Rail commenced rail movement of containers through own rakes 2008 Gateway Rail receives & deploys 8 container trains in the EXIM and domestic

routes 2010 Rs.25 Crores Invested by IFC in Snowman Logistics Ltd. for a 20 % stake in March

2010

Rs.300 Crores invested by Blackstone in GRFL in August 2010

GDKL won the bid to set up CFS opposite Vallarpadam, Kochi in Oct 2010 Source: Company

Page | 4

II nnii tt

ii aatt ii

nngg

CCoo

vvee

rr aagg

ee

tt iiaa

tt iinn

gg CC

oovv

eerr aa

ggee

tt iinn

gg CC

oovv

eerr aa

ggee

gg CC

oovv

eerr aa

ggee

CCoo

vvee

rr aagg

ee

vvee

rr aagg

ee

rr aagg

ee

ggee

Gateway Distriparks Ltd

IINN

II TT

II AA

TTII NN

GG CC

OOVV

EERR

AAGG

EE ––

1133

tthh

SSee

ppttee

mmbb

eerr 22

0011

22

Investment Rationale Rail segment leading the show

GDL started its Rail business in 2007 after the Indian government opened up the sector for private

participation. The company operates 21 owned and 3 leased rakes through its 3 ICD’s and has plans to

increase the capacity going forward. GDL is the second largest container rail operator in India only after

Container Corporation of India (Concor). Its ICD’s are located at Garhi (Gurgaon), Ludhiana and Faridabad

(Started operations in Feb’12, not yet rail linked. Should get rail linked in 2-3 months). These ICD’s are

connected well to Mundra, JNPT and Pipavav ports. In 2009, Blackstone invested Rs.3 bn in the rail subsidiary

through cumulative convertible preference shares which helped the company to reduce its debts. The

company plans to add 5-6 rakes (owned or leased) in the current fiscal with a capex of Rs.150 crores or more.

ICD Capacity

ICD Land (in acres) Capacity - TEU's

Garhi 90 120000

Ludhiana 33 144000

Faridabad (not yet operational) 66 90000-96000

Source: Company

Despite being a capital intensive business, GDL Rail has been able to breakeven in Q3FY11. As in FY12, Rail

segment contributed almost 55% of the total sales of the company. Almost 87% of the rail business comes

from the EXIM trade and GDL has almost doubled the revenues of the rail segment in the past two years to

reach Rs.450 crores in FY12.

Source: Company Data, Nirmal Bang Research

Revenues from the rail segment look extrapolated in Q4FY12 because of the change in reporting pattern.

Annual terminal charges which earlier used to get net off were shown separately during the Q4FY12 quarter.

Page | 5

II nnii tt

ii aatt ii

nngg

CCoo

vvee

rr aagg

ee

tt iiaa

tt iinn

gg CC

oovv

eerr aa

ggee

tt iinn

gg CC

oovv

eerr aa

ggee

gg CC

oovv

eerr aa

ggee

CCoo

vvee

rr aagg

ee

vvee

rr aagg

ee

rr aagg

ee

ggee

Gateway Distriparks Ltd

IINN

II TT

II AA

TTII NN

GG CC

OOVV

EERR

AAGG

EE ––

1133

tthh

SSee

ppttee

mmbb

eerr 22

0011

22

This is just a pass through income which is not comparable. Margins of the Rail segment saw a dip in the

current quarter with the company starting two new networks Sanand in Gujarat and Jodhpur in Rajasthan

connecting with Mundra/Pipavav. This has helped the volumes and affected the margins since the new routes

have come at lower margins.

Source: Company Data, Nirmal Bang Research

Over the years, Rail segment has become the driver of growth for GDL. It now contributes almost 55% in

revenues, 28.5% of EBIDTA and 17% of PAT for GDL. EBIDTA/TEU has shown improvement on the back of

good operational efficiency. Contribution to PAT is lower comparatively due to higher depreciation costs

involved. However, going forward, we feel this contribution should improve on the back of:

Higher Utilization levels – GDL has plans to utilize its ICDs optimally and thus increase the services by

expanding the connectivity by introducing more routes. This would bring in more business by utilizing

storage services at ICD’s. Further, GDL also provides last mile connectivity for its customers through

its own fleet of trailers. Lastly, the company is investing in sidings of ICD’s to reduce the parking

charges it pays to Indian railways.

Higher Volumes due to inclusion of shorter routes – GDL has lately introduced new networks to

avoid empty return running of rakes. These routes are Sanand in Gujarat and Jodhpur in Rajasthan

connecting with Mundra/Pipavav. Management believes this would be the trend going forward as

well. This move has affected the margins in Q4FY12 quarter; however, we believe in the long run

overall margins should improve on the back of higher utilizations and higher volumes.

Rail Revenues and margins

Source: Company Data, Nirmal Bang Research

3875.40 3925.02

3757.813866.78

4184.67

3494.62

3951.28

3664.83

4107.84

3000

3200

3400

3600

3800

4000

4200

4400

Q4FY11 Q1FY12 Q2FY12 Q3FY12 Q4FY12 Q1FY13 FY12 FY13E FY14E

EBIDTA/TEU - Rail

449.55 509.69573.5015.9%

17.0%

18.5%

14%

15%

16%

17%

18%

19%

0

100

200

300

400

500

600

700

FY12 FY13E FY14E

Revenues EBIDTA margin %

Page | 6

II nnii tt

ii aatt ii

nngg

CCoo

vvee

rr aagg

ee

tt iiaa

tt iinn

gg CC

oovv

eerr aa

ggee

tt iinn

gg CC

oovv

eerr aa

ggee

gg CC

oovv

eerr aa

ggee

CCoo

vvee

rr aagg

ee

vvee

rr aagg

ee

rr aagg

ee

ggee

Gateway Distriparks Ltd

IINN

II TT

II AA

TTII NN

GG CC

OOVV

EERR

AAGG

EE ––

1133

tthh

SSee

ppttee

mmbb

eerr 22

0011

22

CFS continues to breed cash

GDL is one of the largest CFS operators in India with a capacity to handle 4,90,000 TEU’s annually. This

segment has grown steadily for the company and had contributed almost 66% of the EBIDTA in FY12. CFS

business continues to remain the cash cow of the company with very high margins of almost ~ 54%.

Moreover, working capital requirement is also very low for this segment and debt portion very minimal.

CFS Capacity Details

CFS Land (in acres) Capacity - TEU's

Mumbai-JNPT 62 300000

Chennai 20 90000

Vizag 20 50000

Kochi 6.5 50000

Source: Company data, Nirmal Bang Securities

Volumes of the CFS segment has taken a hit from the past 3 quarters and remained flat in FY12 on the back of

slower economy growth and secondly due to rupee depreciation affecting imports at the ports. Volumes went

down at the JNPT CFS while they remained stable at the Chennai and Vizag ports mitigating higher impact on

volumes. However, realizations of the CFS segment grew almost 38% in FY12 on the back of higher dwell time.

Consequently, due to better operational management, EBIDTA/TEU also has grown by 41% in FY12.

GDL has commissioned its Kochi CFS in Q4FY12 and partial operations have started and complete operations

would begin once the warehouse is constructed by September 2012. In addition, the company is also adding

up capacity at its JNPT port of 60,000 TEU’s in the latter half of FY13. Moreover, the company also has

additional land of 22 acres in Kochi near the port which can be utilized for future expansion. We expect CFS

volumes to grow by 2.8% in FY13E and by 2.4% in FY14E.

Source: Company Data, Nirmal Bang Research

3271.12758.62975.6

3634.54156.5

3417.3

4875.34815.35224.1

4904.54347.6

4949.35248.25510.6

0

1000

2000

3000

4000

5000

6000

EBIDTA/TEU - CFS

Page | 7

II nnii tt

ii aatt ii

nngg

CCoo

vvee

rr aagg

ee

tt iiaa

tt iinn

gg CC

oovv

eerr aa

ggee

tt iinn

gg CC

oovv

eerr aa

ggee

gg CC

oovv

eerr aa

ggee

CCoo

vvee

rr aagg

ee

vvee

rr aagg

ee

rr aagg

ee

ggee

Gateway Distriparks Ltd

IINN

II TT

II AA

TTII NN

GG CC

OOVV

EERR

AAGG

EE ––

1133

tthh

SSee

ppttee

mmbb

eerr 22

0011

22

Source: Company Data, Nirmal Bang Research

Snowman - Small but growing exponentially

GDL acquired stake in Snowman Logistics Ltd in 2006 and today owns 53.12% ownership. The other investors

are Mitsubishi Corp & Nichirei Corp of Japan (25.92%) and IFC (19.99%). The company operates cold stores

and a fleet of refrigerated trucks giving wholesome services of warehousing, distribution and transportation.

Currently, the company has a pallet size of 18,280 across 20 locations and plans to expand them to 46,340 by

FY13 at an investment of Rs.100 crores. Company’s major clientele include HUL, Amul, Baskin & Robbins,

Ferrero Rocher, Mars Chocolates, Pizza Hut and KFC.

The % of revenue contribution to the total revenues has been increasing over the last few quarters.

Source: Company Data, Nirmal Bang Research

Snowman contributed 7.5% to revenues, 5.5% to EBIDTA and 2.5% to PAT in FY12. PAT was comparatively

lower due to higher taxes. We expect this segment to grow by 75% in revenues in FY13E on the back of

capacity expansion and favourable environment for the growth of cold storage segment.

8067.48817.4 9002.2

9795.39136.3

8300.29171.2 9629.7 10111.2

0

2000

4000

6000

8000

10000

12000

Q4FY11 Q1FY12 Q2FY12 Q3FY12 Q4FY12 Q1FY13 FY12 FY13E FY14E

Revenue/TEU - CFS

9.9 10.0 11.4 13.9 13.4 13.7 16.318.5 22.0

7.6%7.1% 7.2%

8.2% 7.3% 7.3%8.3%

9.2% 9.4%

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

0

5

10

15

20

25

Q1FY11 Q2FY11 Q3FY11 Q4FY11 Q1FY12 Q2FY12 Q3FY12 Q4FY12 Q1FY13

Revenues (Rs in Crs) % of total

Cold storage Revenues

Page | 8

II nnii tt

ii aatt ii

nngg

CCoo

vvee

rr aagg

ee

tt iiaa

tt iinn

gg CC

oovv

eerr aa

ggee

tt iinn

gg CC

oovv

eerr aa

ggee

gg CC

oovv

eerr aa

ggee

CCoo

vvee

rr aagg

ee

vvee

rr aagg

ee

rr aagg

ee

ggee

Gateway Distriparks Ltd

IINN

II TT

II AA

TTII NN

GG CC

OOVV

EERR

AAGG

EE ––

1133

tthh

SSee

ppttee

mmbb

eerr 22

0011

22

Industry Government spend to rise on port development The government has proposed an investment of Rs 73,794 crore for development of various ports in the 12th Five Year Plan (2012-17) and has set a target of enhancing the capacity of major ports to 1,229.2 mn tonnes per annum (MTPA) by the end of Mar'17 from 689.8 MTPA at the end of Mar’12. Also, according to Centre for Monitoring Indian Economy (CMIE), cargo traffic at all ports in the country will witness a 5.4% growth in FY 2012-13. This is expected to be contributed by jump in crude oil imports and coal traffic.

With such efforts taken on developing the ports to discard infrastructure bottlenecks, the container handling capacity at the major ports will increase and will be able to cater to the increasing traffic. This is positive for players with high exposure in the containerization business and the CFS operators are very certain that business will remain bullish for the next ten years if better facilities are to be made viable.

JNPT is in the process of almost doubling its capacity to reduce the congestion at its port. JNPT is likely to invite fresh bids after a consortium led by Port of Singapore Authority and ABG Infra failed to sign the deal almost a year since the bids were opened for construction of the 4

th terminal. JNPT currently has a capacity of

4.1mn TEUs and CT-4 would add up another 4.8 mn TEUs. A 5th

terminal is also being designed post which the total capacity of the JNPT port should shoot up to 10 mn TEUs.

As per National Association of Container Freight Stations, the combined container traffic from Chennai, Ennore and L&T's Katupalli ports will increase by about 4 times, to around 8 million TEUs from the present 1.6 million TEUs in the next five years.

Certain development projects at Vizag Port are also in the anvil for enhancing the capacity to 110 million tonnes by 2014-15.

Scope for Containerized EXIM to grow The major ports together handle 70% of India’s external trade by volume shipped by sea. The containerisation business in India is at a growth stage and accounts for 65% of total cargo being shipped through containers, unlike the international rate of nearly 75-80%. This is expected to grow in the coming years with ongoing expansion works like development of new ports and the dedicated freight corridor.

Figures in Mn TEUs FY07 FY08 FY09 FY10 FY11 FY12

Container traffic at major ports 5.4 6.6 5.1 5.0 7.5 7.8 Source: IPA

According to reports, various plans are in place to increase the capacity of major ports from 670.13 million tonnes in 2010-11 to 1,459.53 million tonnes by 2019-20. Similarly, there are plans to increase the capacity of non-major ports from 390 million tonnes in 2010-11 to 1,670.513 million tonnes in 2019-20. EXIM container throughput is expected to almost double in 6 years from 1,14,040 Mn MT in FY11 to 2,25,095 mn MT in FY17. Indian Ports Association has forecasted the India’s EXIM volumes at major Indian ports to grow at 6.5% CAGR during FY08‐26E and containerized cargo handling at major ports to grow at 12% CAGR during the same period. Such growth in containerization will propel the demand for ICDs and CFSs.

Page | 9

II nnii tt

ii aatt ii

nngg

CCoo

vvee

rr aagg

ee

tt iiaa

tt iinn

gg CC

oovv

eerr aa

ggee

tt iinn

gg CC

oovv

eerr aa

ggee

gg CC

oovv

eerr aa

ggee

CCoo

vvee

rr aagg

ee

vvee

rr aagg

ee

rr aagg

ee

ggee

Gateway Distriparks Ltd

IINN

II TT

II AA

TTII NN

GG CC

OOVV

EERR

AAGG

EE ––

1133

tthh

SSee

ppttee

mmbb

eerr 22

0011

22

Government initiatives to boost Exports The government recently unveiled a seven-point strategy to boost India's merchandise exports that have been impacted by sluggish demand from Europe and US. This includes interest subsidy scheme on labour intensive exports by a year to March 2013, declared 7 countries as focus areas, offered special sops for export units in North-East and made ecommerce and courier exports out of Delhi and Mumbai eligible for the export benefits. The foreign trade policy 2009-14 has set a target of $446 billion exports by 2014 from $303billion at the end of 2012. This is a positive trigger for the logistics sector where the growth of the sector has a positive correlation with EXIM trade.

Source: Ministry of Commerce

-40%

-20%

0%

20%

40%

60%

80%

100% Exports and Non-Oil Import Growth (YoY)

Exports Non-Oil import

Source: Ministry of commerce

Cold storage logistics players see huge potential ahead Cold chains total market in India was estimated to be ~ Rs 100bn in 2008. The market is estimated to reach ~ Rs 325bn in 2015. The industry is expected to grow at 20-25 % CAGR over the next few years.

India, at present does not have a comprehensive cold chain network and hence has been witnessing 30-35% wastage of perishable produce every year. This wastage is largely due to the absence of appropriate infrastructure, both static and mobile, In India; currently the cold chain market is highly fragmented with more than 3,500 companies in the whole value system. With the growing need of transportation of perishable products, there lies a huge potential in this segment.

Source: Technopak

182

250303.7

366

446

0

100

200

300

400

500

2009-10 2010-11 2011-12 2012-13 E 2013-14 E

Exports in US $ bn

Page | 10

II nnii tt

ii aatt ii

nngg

CCoo

vvee

rr aagg

ee

tt iiaa

tt iinn

gg CC

oovv

eerr aa

ggee

tt iinn

gg CC

oovv

eerr aa

ggee

gg CC

oovv

eerr aa

ggee

CCoo

vvee

rr aagg

ee

vvee

rr aagg

ee

rr aagg

ee

ggee

Gateway Distriparks Ltd

IINN

II TT

II AA

TTII NN

GG CC

OOVV

EERR

AAGG

EE ––

1133

tthh

SSee

ppttee

mmbb

eerr 22

0011

22

Financial Performance Q1FY13 Result Analysis Consolidated results:

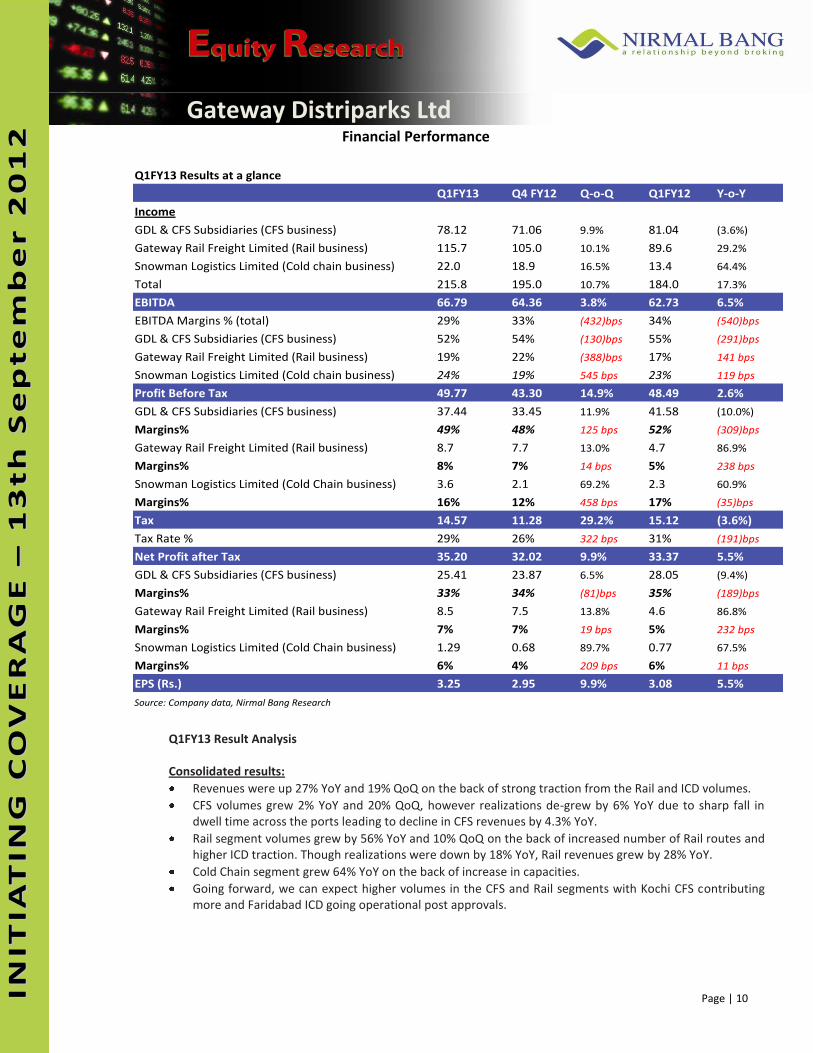

Revenues were up 27% YoY and 19% QoQ on the back of strong traction from the Rail and ICD volumes.

CFS volumes grew 2% YoY and 20% QoQ, however realizations de-grew by 6% YoY due to sharp fall in dwell time across the ports leading to decline in CFS revenues by 4.3% YoY.

Rail segment volumes grew by 56% YoY and 10% QoQ on the back of increased number of Rail routes and higher ICD traction. Though realizations were down by 18% YoY, Rail revenues grew by 28% YoY.

Cold Chain segment grew 64% YoY on the back of increase in capacities.

Going forward, we can expect higher volumes in the CFS and Rail segments with Kochi CFS contributing more and Faridabad ICD going operational post approvals.

Q1FY13 Results at a glance

Q1FY13 Q4 FY12 Q-o-Q Q1FY12 Y-o-Y

Income

GDL & CFS Subsidiaries (CFS business) 78.12 71.06 9.9% 81.04 (3.6%)

Gateway Rail Freight Limited (Rail business) 115.7 105.0 10.1% 89.6 29.2%

Snowman Logistics Limited (Cold chain business) 22.0 18.9 16.5% 13.4 64.4%

Total 215.8 195.0 10.7% 184.0 17.3%

EBITDA 66.79 64.36 3.8% 62.73 6.5%

EBITDA Margins % (total) 29% 33% (432)bps 34% (540)bps

GDL & CFS Subsidiaries (CFS business) 52% 54% (130)bps 55% (291)bps

Gateway Rail Freight Limited (Rail business) 19% 22% (388)bps 17% 141 bps

Snowman Logistics Limited (Cold chain business) 24% 19% 545 bps 23% 119 bps

Profit Before Tax 49.77 43.30 14.9% 48.49 2.6%

GDL & CFS Subsidiaries (CFS business) 37.44 33.45 11.9% 41.58 (10.0%)

Margins% 49% 48% 125 bps 52% (309)bps

Gateway Rail Freight Limited (Rail business) 8.7 7.7 13.0% 4.7 86.9%

Margins% 8% 7% 14 bps 5% 238 bps

Snowman Logistics Limited (Cold Chain business) 3.6 2.1 69.2% 2.3 60.9%

Margins% 16% 12% 458 bps 17% (35)bps

Tax 14.57 11.28 29.2% 15.12 (3.6%)

Tax Rate % 29% 26% 322 bps 31% (191)bps

Net Profit after Tax 35.20 32.02 9.9% 33.37 5.5%

GDL & CFS Subsidiaries (CFS business) 25.41 23.87 6.5% 28.05 (9.4%)

Margins% 33% 34% (81)bps 35% (189)bps

Gateway Rail Freight Limited (Rail business) 8.5 7.5 13.8% 4.6 86.8%

Margins% 7% 7% 19 bps 5% 232 bps

Snowman Logistics Limited (Cold Chain business) 1.29 0.68 89.7% 0.77 67.5%

Margins% 6% 4% 209 bps 6% 11 bps

EPS (Rs.) 3.25 2.95 9.9% 3.08 5.5%

Source: Company data, Nirmal Bang Research

Page | 11

II nnii tt

ii aatt ii

nngg

CCoo

vvee

rr aagg

ee

tt iiaa

tt iinn

gg CC

oovv

eerr aa

ggee

tt iinn

gg CC

oovv

eerr aa

ggee

gg CC

oovv

eerr aa

ggee

CCoo

vvee

rr aagg

ee

vvee

rr aagg

ee

rr aagg

ee

ggee

Gateway Distriparks Ltd

IINN

II TT

II AA

TTII NN

GG CC

OOVV

EERR

AAGG

EE ––

1133

tthh

SSee

ppttee

mmbb

eerr 22

0011

22

Risks to Recommendation

Dependence of economic growth: Logistics industry is closely linked to the country’s economic growth and any slowdown in economic activities or decline in EXIM trade will impact the growth of GDL.

Absence of proper infrastructure: Growth of GDL can be hampered by a lack of good quality of infrastructure of roads, railways or ports.

Revision in haulage charges: Any adverse revision in haulage charge can impact the viability of transportation by rail.

Increase in Fuel Cost: Any further surge in fuel costs will impact the business even more as the operational expenses would go up.

44% of the Promoters shares are pledged.

Peer comparison

FY13E FY14E FY13E FY14E FY13E FY14E FY13E FY14E FY13E FY14E FY13E FY14E FY13E FY14E

Gateway Distriparks 879.2 991.6 281.0 320.5 18.3% 19.0% 15.3% 16.6% 5.1 4.5 1.6 1.5 10.4 9.2

ConCor 4516.4 4939.3 1113.6 1212.0 15.6% 14.8% 14.7% 14.0% 7.8 6.8 1.9 1.7 12.2 11.7

Allcargo 3589.9 3886.1 429.1 492.3 13.9% 14.5% 10.8% 12.0% 4.8 3.8 0.6 0.5 7.6 6.3

Transport Corp 2001.8 2185.2 160.7 185.1 16.2% 17.1% 15.9% 16.5% 4.9 4.35 0.35 0.35 7.2 6.2

Source: NB Research

PESales EBITDA ROE ROCE EV/EBIDTA EV/Sales

Page | 12

II nnii tt

ii aatt ii

nngg

CCoo

vvee

rr aagg

ee

tt iiaa

tt iinn

gg CC

oovv

eerr aa

ggee

tt iinn

gg CC

oovv

eerr aa

ggee

gg CC

oovv

eerr aa

ggee

CCoo

vvee

rr aagg

ee

vvee

rr aagg

ee

rr aagg

ee

ggee

Gateway Distriparks Ltd

IINN

II TT

II AA

TTII NN

GG CC

OOVV

EERR

AAGG

EE ––

1133

tthh

SSee

ppttee

mmbb

eerr 22

0011

22

Valuation and Recommendation GDL has become a Logistics conglomerate by positioning itself as one of the largest CFS player and as the largest private Container Train Operator in India. Their investment in the fast growing cold chain segment is also gaining momentum. At CMP, the stock is trading at an EV/EBIDTA and P/E of 4.4 and 10.2x its FY13E earnings respectively and looks attractive. We recommend a BUY on the stock with a price target of Rs.178 which is 28% upside from current levels.

PE Band

Page | 13

II nnii tt

ii aatt ii

nngg

CCoo

vvee

rr aagg

ee

tt iiaa

tt iinn

gg CC

oovv

eerr aa

ggee

tt iinn

gg CC

oovv

eerr aa

ggee

gg CC

oovv

eerr aa

ggee

CCoo

vvee

rr aagg

ee

vvee

rr aagg

ee

rr aagg

ee

ggee

Gateway Distriparks Ltd

IINN

II TT

II AA

TTII NN

GG CC

OOVV

EERR

AAGG

EE ––

1133

tthh

SSee

ppttee

mmbb

eerr 22

0011

22

F Financial Performance

Profitability (Rs. In Cr) FY11A FY12A FY13E FY14E Financial Health (Rs. In Cr) FY11A FY12A FY13E FY14E

Revenues 604.5 823.5 947.7 1068.7 Share Capital 108.0 108.3 108.3 108.3

% change 15.0% 36.2% 15.1% 12.8% Reserves & Surplus 579.9 639.5 748.4 769.2

Total Shareholders Funds 687.9 747.8 856.6 877.4

EBITDA 165.1 250.4 288.4 329.0 Minority Interest 61.0 66.3 72.7 80.0

EBITDA growth (%) 20.2% 51.6% 15.2% 14.1% Comp Conv Pref Shares 295.8 295.8 295.8 295.8

Non-Current Liabilities

Depn & Amort 50.2 62.8 69.5 76.2 Long term Borrowings 114.1 103.7 134.8 148.2

Operating income 114.9 187.6 219.0 252.8 Deferred Tax Liabilites (net) 14.0 14.0 14.0 14.0

Interest 18.7 13.5 13.5 14.8 Long term Provisions 3.7 4.7 5.4 6.3

Other Income 7.4 12.4 7.4 6.2 Total Non- Current Liabilites 131.9 122.4 154.2 168.5

PBT 104.1 186.4 212.8 244.1 Current Liabilties

Tax 4.4 50.8 57.5 68.3 Trade Payables 26.3 23.1 23.5 24.7

PAT 99.7 135.6 155.3 175.8 Other Current Liabilites 42.0 52.1 62.5 68.7

Minority interest 3.0 3.6 6.4 7.3 Short term Provisions 39.6 41.0 49.3 59.1

PAT after M.I 96.8 132.0 149.0 168.4 Total Current Liabilites 107.9 116.2 135.3 152.5

No of Shares 10.8 10.8 10.8 10.8 Total Equity & Liabilities 1284.5 1348.5 1514.6 1574.3

EPS 8.93 12.18 13.74 15.54 Assets

Cash per share 12.72 15.35 18.51 17.57 Fixed Assets 940.1 986.1 1086.1 1136.1

Quarterly (Rs. In Cr) Sep.11 Dec.11 Mar.12 June.12 Goodwill on Consolidation 31.0 31.0 31.0 31.0

Revenue 188.8 195.2 195.0 232.8 Total Non Current Assets 1035.9 1081.0 1183.7 1239.5

EBITDA 61.2 62.2 64.4 66.8 Current Assets

Dep & Amortisation 1.8 1.8 1.8 1.2 Trade Receivables 62.4 66.4 92.1 103.9

Op Income 59.4 60.4 62.6 65.6 Cash Balances 137.7 166.2 200.4 190.2

Interest 3.3 3.2 3.4 3.7 Short Term Loans & Advances 31.4 27.0 29.7 31.1

Other Inc. 0.0 3.1 2.4 2.6 Total Current Assets 248.6 267.5 330.9 334.8

PBT 47.4 47.3 43.3 49.8 Total Assets 1284.5 1348.5 1514.6 1574.3

Tax 13.9 14.2 11.3 14.6 Cash Flow (Rs. In Cr) FY11A FY12A FY13E FY14E

PAT 33.5 33.1 32.0 35.2 Operating

EPS (Rs.) 3.1 3.1 3.0 3.2 OP before WC 165.1 250.4 288.4 329.0

Performance Ratio FY11A FY12A FY13E FY14E Change in WC (48.6) 1.4 (12.9) (2.6)

EBITDA margin (%) 27.3% 30.4% 30.4% 30.8% (-) Tax (4.4) (50.8) (57.5) (68.3)

PAT margin (%) 16.0% 16.0% 15.7% 15.8% CF from Operation 112.1 201.0 218.0 258.0

ROE (%) 14.3% 18.4% 18.6% 19.4% Investment

ROCE (%) 9.6% 14.8% 14.9% 16.4% Capex (100.9) (272.8) (153.0) (185.0)

Per Share Data FY11A FY12A FY13E FY14E Other Investment 2.0 13.0 0.0 0.0

Reported EPS 8.9 12.2 13.7 15.5 Other Income 7.4 12.4 7.4 6.2

BV per share 63.5 69.1 79.1 81.0 Total Investment (91.5) (247.5) (145.6) (178.8)

Dividend per share 6.0 6.0 6.9 7.8 Financing

Valuation Ratio FY11A FY12A FY13E FY14E Change in equity capital 0.09 0.28 0.00 0.00

Price Earnings (x) 15.7 11.5 10.2 9.0 Dividend Paid (incl Tax) (75.6) (75.5) (86.5) (97.9)

Price / Book Value (x) 2.2 2.0 1.8 1.7 Interest Paid (18.7) (13.5) (13.5) (14.8)

EV / Sales 2.5 1.8 1.5 1.4 Loans & Others 131.8 163.7 61.8 23.3

EV / EBITDA 9.0 5.8 5.0 4.5 Total Financing 37.6 75.0 (38.2) (89.4)

Net Chg. in Cash 58.2 28.5 34.2 (10.2)

Cash at beginning 79.5 137.7 166.2 200.4

Cash at end 137.7 166.2 200.4 190.2

Source: Company data, Nirmal Bang Securities

Page | 14

II nnii tt

ii aatt ii

nngg

CCoo

vvee

rr aagg

ee

tt iiaa

tt iinn

gg CC

oovv

eerr aa

ggee

tt iinn

gg CC

oovv

eerr aa

ggee

gg CC

oovv

eerr aa

ggee

CCoo

vvee

rr aagg

ee

vvee

rr aagg

ee

rr aagg

ee

ggee

Gateway Distriparks Ltd

IINN

II TT

II AA

TTII NN

GG CC

OOVV

EERR

AAGG

EE ––

1133

tthh

SSee

ppttee

mmbb

eerr 22

0011

22

Notes

Disclaimer:

This Document has been prepared by Nirmal Bang Research (A Division of Nirmal Bang Securities Pvt Ltd). The information, analysis and

estimates contained herein are based on Nirmal Bang Research assessment and have been obtained from sources believed to be reliable. This

document is meant for the use of the intended recipient only. This document, at best, represents Nirmal Bang Research opinion and is meant for

general information only. Nirmal Bang Research, its directors, officers or employees shall not in any way be responsible for the contents stated

herein. Nirmal Bang Research expressly disclaims any and all liabilities that may arise from information, errors or omissions in this connection. This

document is not to be considered as an offer to sell or a solicitation to buy any securities. Nirmal Bang Research, its affiliates and their employees

may from time to time hold positions in securities referred to herein. Nirmal Bang Research or its affiliates may from time to time solicit from or

perform investment banking or other services for any company mentioned in this document.

Nirmal Bang Research (Division of Nirmal Bang Securities Pvt Ltd)

B-2, 301/302, Marathon Innova, Opp. Peninsula Corporate Park

Off. Ganpatrao Kadam Marg Lower Parel (W), Mumbai-400013 Board No. : 91 22 3926 8000/8001

Fax. : 022 3926 8010