Gains and losses

26

` Gains and losses The effect on risk taking and the influence of government announcements Sven Delahaije Tilburg University Department of Finance 25th of February, 2012

Transcript of Gains and losses

`

Gains and losses The effect on risk taking and the influence of

government announcements

Sven Delahaije

Tilburg University

Department of Finance

25th of February, 2012

S.J.P. Delahaije – Bachelor Thesis 2012 Page 2

Abstract

This study investigates the influence of prior investment results on investors’ future risk

taking. Three psychological biases, loss-aversion, house-money effect and break-even effect

arise as a consequence to prior investment results. These biases have an impact on investors’

risk taking in future investment decisions. This influence is affected by macro-economic

government announcements, which increases the effect of loss-aversion and reduces risk

taking. The type of media which presents this announcement has no impact on this

relationship. A large gain leads to a strong house-money effect and increases risk taking.

Compared to a large gain, a medium size gain has a smaller positive impact on risk taking. A

large loss results in the break-even effect and a large increase in risk taking. A small loss

results in a loss-aversion effect and a significant decrease in the break-even effect. Therefore,

a small loss will decrease future risk taking of investors.

S.J.P. Delahaije – Bachelor Thesis 2012 Page 3

Table of contents

Abstract……………………………….……………………………………………….... 2

Chapter 1:The effects of behavioral finance………………………………………….

1.1 Background………………………………………………………………………...... 4-5

1.2 Problem statement and research questions…………………………………….......... 5

1.3 Thesis structure……………………………………………………………………… 6

Chapter 2: Biases and their effects………………………………………………….....

2.1 The biases……………………………………………………………………............ 7-10

2.1.1 Loss-aversion……………………………………………………………........ 7-8

2.1.2 House-money effect………………………………………………………….. 8-9

2.1.3 Break-even effect…………………………………………………………….. 9-10

2.2 Relevance………...………………………………………………………………….. 10-12

2.2.1 Academic Relevance…………………………………………………………. 10-11

2.2.2 Managerial Relevance………………………………………………………... 11-12

Chapter 3: The model and mediating effect……………………………………….....

3.1 Conceptual model…………………………………………………………………… 13

3.2 The variables………………………………………………………………………… 13

3.3 The type of media…………………………………………………………………… 14

Chapter 4: Research design…………………………………………………………....

4.1 Type of experimental design………………………………………………………… 15

4.2 Respondents and sampling…………………………………………………………... 16

4.2.1 Population……………………………………………………………………. 16

4.2.2 Sample design………………………………………………………………... 16

4.2.3 Sample size……………………………………………………………........... 16

4.3 Design of the experiment………………………………………………………......... 16-17

4.3.1 Manipulation…………………………………………………………………. 18

4.3.2 Treatment…………………………………………………………………….. 19

4.3.3 Instructions …………………………………………………………………... 19-20

Chapter 5: a final overview…………………………………………………………….

5.1 Limitations…………………………………………………………………………... 21

5.2 Conclusions and expected results…………………………………………………… 22-24

S.J.P. Delahaije – Bachelor Thesis 2012 Page 4

Chapter 1 The effects of behavioral finance

1.1 Background

The financial world has failed to explain certain events, focusing only on the rational aspect

of investors’ behavior. However, people’s decision making is affected by factors or biases

and therefore not completely rational. These psychological biases are caused by the cognitive

and emotional weaknesses of people (Baker and Nofsinger, 2002), and can be described as

disturbing cognitive and affective influence on people’s decisions and behavior.

Investors’ behavior is affected by psychological biases which loom as a consequence to

investors’ reaction to historical investment results. Namely, investors’ decisions often are

influenced by historical or sunk costs (Arkes and Blumer, 1985; Thaler, 1980) and by prior

outcomes of investments (Massa and Simonov, 2002).

This paper focuses on the effect of prior gains and losses on future risk taking in investment

decisions. Massa and Simonov (2005) identified two biases as a consequence of prior gains

and losses; loss aversion and house-money effect. Their research was an addition to the

research of Thaler and Johnson (1990), who have identified house-money effect and the

break-even effect.

Loss aversion states that people become less willing to take risks, after experiencing a

financial loss. In other words, there will be a shift towards less risky investment projects

following a prior loss. The house-money effect suggests that prior gains make future losses

less painful, since people have the idea that they are not losing their own money. Thaler and

Johnson (1990) showed in their experiment that around 82% of their participants, continued

to choose a riskier alternative after experiencing a prior gain. Massa and Simonov (2002)

concluded that an 1% increase in wealth, would increase risk taking by 0,26%. The break-

even effect states that people’s preference for alternatives shift to the most risky ones, after

experiencing a prior loss. This shift in risk behavior is the consequence of the fact that people

have the intentions to make up for their losses, so the option or investment opportunity that

offers a chance to break even, seem to be increasingly attractive. Thaler and Johnson (1990)

showed that around 69% of the participants chose the option which contains the possibility to

break even, when they experienced a prior loss.

In addition to these three identified biases, another bias seems to be important in the

determination of investors’ behavior, the influence of government announcements. Recent

studies (Tetlock, 2007 and Peress, 2008) have shown that there is a strong correlation

S.J.P. Delahaije – Bachelor Thesis 2012 Page 5

between stories reported by the media and investors’ behavior. Government announcements

about general macroeconomic trends have an increased frequency since the start of the

financial crisis in 2008. This raises an interesting question: “how do investors react toward

macro-economic announcements made by governments?”. According to Peress (2008)

announcements with more media coverage have a number of effects. He discovered that

there will be a stronger price reaction and a stronger trading volume reaction at the

announcement. This paper focuses on the effects of macroeconomic government

announcements on the risk taking of investors. Do government announcements influence the

identified biases, loss aversion, house-money effect and break-even effect, and therefore

future risk taking? Since collecting data of every individual investor would be necessary to

measure the effect of the biases on future risk taking, which is almost impossible for a large

population, this paper bases its results on a lab experiment. A lab experiment must reveal the

effect of prior gains and losses on future risk taking and how these relationships are

influenced by government announcements. A literature review must explain whether the type

of media representing this government announcement could have an effect on the identified

relationship.

1.2 Problem definition and research questions

Problem statement:

What impact do government announcements have on the behavioral biases of investors, loss-

aversion and house-money effect, caused by prior gains or losses and to what extent does the

type of media representing this announcement influence this relationship?

Research questions:

1. To what extent do market announcements made by government affect the behavioral

biases; loss-aversion, house-money effect and break-even effect?

2. Does the type of media influence the consequences of market announcements?

S.J.P. Delahaije – Bachelor Thesis 2012 Page 6

1.3 Thesis structure

The first part of chapter 2 presents the explanation of the three biases, loss-aversion, house-

money effect and break-even effect. The second part of chapter 2 presents the academic and

managerial relevance. Chapter 3 presents the academic and managerial relevance. In the first

part of chapter 3 the conceptual model is presented. In the second part of chapter 3 the theory

of the type of media is described on the basis of the existing literature. Chapter 4 explains the

method which is used and presents the design of the lab experiment. In chapter 5 the

limitations and expectations/conclusion of this paper are presented.

S.J.P. Delahaije – Bachelor Thesis 2012 Page 7

Chapter 2 Biases and their effects

In this chapter the three biases and their effect on future risk taking are explained. Since these

biases are quite unknown concepts in the financial world, their explanation precedes the

academic and managerial relevance.

2.1 The biases

A lot of research has been conducted on the three identified biases. Thaler and Johnson

(1990) identified in their research the house-money effect and the break-even effect. Massa

and Simonov (2002) concentrated on loss-aversion and the house-money effect. Both group

of researchers continued with their research on the alternative model, the prospect theory of

Kahneman and Tversky (1979). The prospect theory is based on the premise that people treat

risks associated with perceived losses differently from risks associated with perceived gains.

They concluded that “the location of the reference point, and the manner in which choice

problems are coded and edited emerge as critical factors in the analysis of decisions” (1979,

p.288). Massa and Simonov (2005) and Thaler and Johnson (1990) continued on this theory

and discovered three major affects in how people threat risk associated with perceived losses

or perceived gains. In the next paragraphs the three effects are explained and presented as

hypothesis.

2.1.1 Loss-aversion

Loss-aversion hypothesizes that people become less willing to take risks, after experiencing a

financial loss. This behavior can be explained by the prospect theory developed by

Kahneman and Tversky in 1979. They state that if a person prefers a certain prospect (x) to

any risky prospect with an expected value x he/she is risk averse. Kahneman and Tversky

(1979) illustrated the effect of loss-aversion by an experiment conducted among business

students. The business students were confronted with a loss of $7.50 and thereafter asked to

gamble $2.25 on a coin flip. The majority of the students, 60%, declined the gamble.

Thaler and Johnson showed a decrease of over 20% in the number of risk taking participants,

comparing participants confronted with a prior loss and those confronted with a neutral prior

event. Loss-aversion is related to the amount of a prior loss. The effect of loss-aversion

increases together with an increase of a prior loss (Thaler and Johnson, 1990). Thaler and

Johnson (1990) showed that a decrease in wealth of 1% results in a decrease of risk taking of

S.J.P. Delahaije – Bachelor Thesis 2012 Page 8

-0,3%. Loss-aversion has another effect on risk taking, when it involves gains instead of

losses. People confronted with a prior gain will be more willing to take risks. Although, loss-

aversion has an effect in both the case of a loss or gain, the effect is much stronger for prior

losses. This can be explained by the fact that people tend to be more sensitive to decreases in

their wealth than to increases (Thaler et al, 1997). Through empirical estimates, it is found

that losses are weighted about twice as strongly as gains (e.g., Tversky and Kahneman

(1992); Kahneman, Knetsch, and Thaler (1990)). Thaler and Johnson (1990) showed that an

increase in wealth of 1%, results in an increase of risk taking of 0,058%.

The effect of loss-aversion results in two hypothesis:

H1: a relative small prior gain has a positive correlation with risk taking, through the effect

of loss aversion.

A gain in the first event will have a very small increase in the amount of investors who will

choose the riskier projects in the second part of the experiment.

H2: a relative small prior loss has a negative correlation with risk taking, though the effect of

loss aversion.

A loss in the first event, will lead to a decrease in the amount of investors who will choose

the riskier projects in the second investment opportunity.

2.1.2 House-money effect

The house-money effect hypotheses that a prior gain will provoke people to take more risk.

The name of the effect originates from gamblers, which had the feeling after they

experienced a gain that they were not gambling with their own money. The prior gains

function as a mitigating circumstance that makes future losses less painful. Since these losses

become less painful, people increase their willingness to accept risk.

Simonov and Massa showed that a 1% increase in wealth results in an increase of risk taking

by 0,26%.

In the experiment of Thaler and Johnson (1990), only 36% of the students proceeded in a

risky choice after experiencing a loss. Compared to the situation in which the students were

confronted with a prior gain, a prior loss results in a drop of approximately 46% in the

number of students who are willing to choose for a risky alternative.

House-money effect has also impact when involving losses, although there is a significant

decrease in the impact. Simonov and Massa showed that a 1% decrease in wealth results in a

decrease in risk taking of -0, 05%.

S.J.P. Delahaije – Bachelor Thesis 2012 Page 9

The house-money effect results in two hypotheses:

H3: a prior gain has a positive correlation with risk taking as a consequence to the house-

money effect.

A gain in the first event, will lead to a significant increase in the amount of investors who

will choose the riskier projects in the second period.

H4: a prior loss has a negative correlation with risk taking, through the house-money effect.

A loss in the first event, will lead to a small decrease in the amount of investors who will

choose the riskier projects in the second period.

The house-money effect and loss-aversion show both a positive correlation with risk taking

after experiencing a gain. Following a prior loss, these biases show a negative correlation

with risk taking. The difference between these effects can be found in the strength of the

correlation between the change in wealth and the amount of risk taking. The difference is

shown in the fact that the house-money effect has the strongest positive correlation with risk

taking when involving a gain and loss-aversion has the strongest negative correlation with

risk taking when involving a loss. Comparing these two biases, confronted with a prior gain,

the house-money effect has a strong positive correlation with risk taking and loss-aversion

has a weak positive correlation with risk taking. Confronted with a prior loss, the house-

money effect has a weak negative correlation with risk taking and loss-aversion has a strong

negative correlation with risk taking.

2.1.3 Break-even effect

The break-even effect hypothesizes that after experiencing a loss, people will seek for options

that give them the opportunity to break-even. Since these break-even options are often very

risky ones, there will be a shift towards an increase in risk. According to Kahneman and

Tversky (1979) this effect can be based on the fact that changes of the reference point (gain

or loss) alters the preference order for prospects.

Thaler and Johnson showed a percentage of 63-70% of the participants choosing a risky

option which included break-even opportunity, after experiencing a financial loss. People

will increasingly prefer break-even options to other prospects when the initial amount which

is lost increases (Thaler and Johnson, 1990). The break-even effect increases as the initial

amount lost increases.

S.J.P. Delahaije – Bachelor Thesis 2012 Page 10

The break-even effect results in one hypothesis:

H5: a relative big prior loss has a positive correlation with risk taking, through the house-

money effect.

A loss in the first event, will lead to a significant increase in the amount of investors who will

choose the riskiest project.

The break-even effect contradicts the other two biases, because it assumes an increase in risk

taking after experiencing a prior loss, whereas the house-money effect and loss-aversion

assume a decrease in risk taking after experiencing a prior loss.

2.2 Relevance

In this part of the paper the academic and managerial relevance is explained. How does this

paper contribute to existing research and what is the implication for investors in practice?

2.2.1 Academic Relevance

Three biases are indentified which occur as a consequence to prior gains and losses; house-

money effect, loss-aversion and the break-even effect (Thaler and Johnson, 1990; Massa and

Simonov, 2002). Massa and Simonov distinguished between different behavioral theories

and between behavioral and rational hypothesis. This paper continues on the section of

behavioral theories which are identified by Massa and Simonov and by Thaler and Johnson.

In their research they explain the relationship between prior gains or losses and their effect on

risk taking of the investors, caused by the mediating effect of loss-aversion, house-money

effect and the break-even effect.

There is a lot of literature which provides evidence of the conditions under which loss-

aversion, house-money effect or break-even effect occur (Shefrin and Statman, 1985; Glaser

and Weber, 2002; Thaler and Johnson, 1990; Massa and Simonov, 2002). Thaler and

Johnson (1990) discovered that according to the break-even effect prior losses can increase

the willingness to accept gambles, and therefore risk taking. They concluded that the break-

even effect has no an influence on risk taking when experiencing a prior gain. Massa and

Simonov showed that a prior loss has a negative effect on risk taking, according to loss-

aversion. Loss-aversion results in the case of a prior gain into a slight increase in risk taking.

The effect of loss aversion on risk taking is stronger for losses compared to gains (Massa and

Simonov, 2002). The house-money effect results in a strong increase in risk taking following

S.J.P. Delahaije – Bachelor Thesis 2012 Page 11

a prior gain and a slight decrease in risk taking following a prior loss (Thaler and Johnson,

1990).

The innovation of this paper is the addition of a new variable, macro-economic

announcements made by governments. Since the start of the financial crisis in 2008, there has

been an increase in the amount of macro-economic announcements made by governments.

This paper tries to find an answer to the question of how these government announcements

influence the existing biases, loss-aversion, house-money effect and break-even effect, and

therefore influence the risk taking of investors. Research has been conducted about how

market announcements can influence the behavior of investors (Peress, 2008) in which two

main effects have been identified, under reaction and overreaction, as a reaction to news.

Overreaction and under reaction are the consequences of emotion in a behavioral setting,

which causes investors to disproportionally react to new information leading to significant

changes in stock prices or trading volume. The government announcements are presented

through different types of media, for example TV, radio or newspaper. This raises the

question if the type of media has an moderating effect on the relationship between the market

announcements and the biases.

According to Barber and Odean (2008) and Nofsinger (2000) it is not the type of media

which has a direct influence on investors’ behavior, but the exposure and attention that

particular type of media gets. Several factors determine the amount of exposure an particular

type of media gets, like length of the message or time of exposure. Therefore, there are no

huge differences among the types of mass media, although TV seems to have the biggest

exposure. Peress (2008) showed that the amount of media coverage has a number of effects

on investor behavior, leading to a stronger price reaction and trading volume of stocks. The

uninvestigated relationship between market announcements and the behavioral biases, loss-

aversion, house-money effect and the break-even effect is examined by a lab experiment. The

details concerning this experiment can be read in chapter 4.

2.2.2 Managerial Relevance

Psychological biases and emotion can affect investment decisions and result in harming

investors wealth (Shefrin, 2000). The effect on investment decisions is a negative effect,

since psychological biases have a cognitive and affective influence’s on people’s decisions

and behavior. Once investors become aware of the possible biases they are exposed to after

experiencing a specific loss or gain, they could reduce their negative effects. Every single

bias has its own negative consequences for investors.

S.J.P. Delahaije – Bachelor Thesis 2012 Page 12

The break-even effect results from a previous loss and increases the amount of risk an

investor will take. Investors, who have the urge to make up for their previous losses, are

exposed to the break-even effect. This induces the risk of taking excessive risks, just to make

up for historical losses. This type of behavior can lead investors to lose even more, since

higher risk results in a greater probability of a bad result, a loss.

The house-money effect suggests that prior gains increase risk taking. This increase in risk

taking increases the probability to lose the money an investor prior experienced as a gain.

There are two disadvantages indentified as a consequence to the biases. Taking unnecessarily

high risk, which increase the probability of losing money, and on the other hand excessive

reducing risk, which diminishes the probability of earning money.

The loss-aversion theory follows the same line as the house-money effect regarding losses,

there is a decrease of risk taking after a prior loss. Nevertheless, the effect of loss-aversion on

risk taking is stronger than the house-money effect when experiencing a prior loss. The

disadvantage of loss aversion is that it induces investors not to sell losing stocks to winning

ones (Kahneman and Tversky, 1979). Investors, who hold on to losing stocks, could end up

worse, if the losing stocks continue to depreciate.

Overall, the biases have a negative effect on the investment results of investors.

Managers and investors can use the results of this paper, to become aware of the possible

biases they are exposed to. This information can help them to terminate the influence of

emotions on investment decisions, and focus on the rational part of investing, using risk and

reward as a guidance to make decisions. Risk management should become the guidance of

behavior and no longer the psychological biases which are identified in this paper.

S.J.P. Delahaije – Bachelor Thesis 2012 Page 13

Chapter 3 The model and mediating effect

3.1 Conceptual Model

The figure below represents the conceptual model, on which this paper is founded.

3.2 The variables

The conceptual model in this paper consists of one independent variable, the actual gain or

loss by which an investor is confronted. The effect of this independent variable is mediated

by three variables, the psychological biases. Eventually, these mediators have a positive or

negative effect on future risk taking. The influence of the mediators is supposed to be

affected by another variable, the market announcements, although the direction of this

relationship could change depending on the type of media representing the market

announcements.

A gain or loss:

In this paper a gain or loss is defined as: “a loss in overall wealth as a consequence to an

investment”. This definition continues on the research of Massa and Simonov (2005), who

discovered that changes in overall wealth have the greatest influence on future risk taking,

through the psychological biases.

This paper examines the influence of market announcements on the effects on investing after

experiencing a gain or loss, as identified by Massa and Simonov (2005) and Thaler and

Johnson (1990). Since the effects are different for a gain-framed setting compared to a loss-

framed setting, this paper investigates both settings.

Loss-aversion

House-money effect

Break-even effect

Prior gain or loss Risk taking in

investment

Type of media

Government Announcements

S.J.P. Delahaije – Bachelor Thesis 2012 Page 14

3.3 Type of media

Existing literature doesn’t make a clear distinction between the different media based on the

type of the media, but distinguishes media on the amount of exposure and attention it gets.

Nofsinger (2002) stated: “Individual investors motivation to trade is affected by the visibility

of the news, as proxied by the length of the news article.” Barber and Odean (2008)

discovered that the preference of determine the investment choice of investors depends on the

amount of attention that particular investment receives. A second factor determining the

amount of influence the type of media has on the relationship between government

announcements and the biases, are the characteristics of the investor. According to Massa and

Simonov (2005) investors use public available information in different ways. They also stated

that wealthier investors could be less dependent on publicly available information, since they

have their private ones.

Responding to the trend of increased internet usage and the decreasing interest in written

information. Therefore, it is expected that TV and internet have the biggest impact of the

different types of media. Radio, newspaper and articles have less impact on the relationship

between a government announcement and the three identified psychological biases of

investors.

S.J.P. Delahaije – Bachelor Thesis 2012 Page 15

Chapter 4 Research Design

In this chapter, the research method is displayed, which should identify the moderating

influence of market announcements on the behavioral biases, loss aversion, break-even effect

and the house-money effect.

To examine the influence of macro-economic government announcements on the

psychological biases this paper constructs a lab experiment. The choice for a lab experiment

is based on two major advantages. First, in the real world, it is very difficult to observe

investors’ behavior, which derived from a previous loss or gain of that particular investor. To

gather such data, there should be personal contact with a group of individual investors, which

makes a field research practically impossible. Second, because controls and manipulations, an

important part of this experiment, are best done in an artificial setting, a lab experiment is

chosen. This lab experiment, tries to create a real life investment experience, without the

contamination of the relationship investigated.

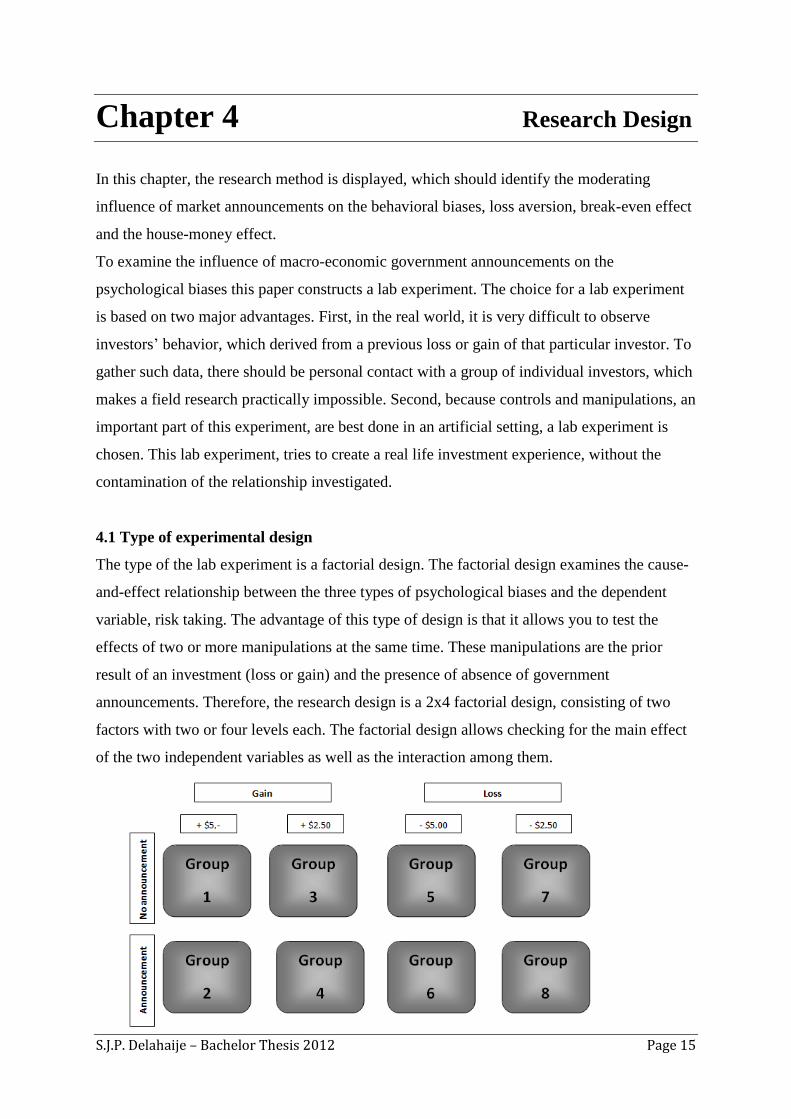

4.1 Type of experimental design

The type of the lab experiment is a factorial design. The factorial design examines the cause-

and-effect relationship between the three types of psychological biases and the dependent

variable, risk taking. The advantage of this type of design is that it allows you to test the

effects of two or more manipulations at the same time. These manipulations are the prior

result of an investment (loss or gain) and the presence of absence of government

announcements. Therefore, the research design is a 2x4 factorial design, consisting of two

factors with two or four levels each. The factorial design allows checking for the main effect

of the two independent variables as well as the interaction among them.

S.J.P. Delahaije – Bachelor Thesis 2012 Page 16

4.2 Respondents and sampling

4.2.1 Population

The population of this paper consists of students of the University of Tilburg. The total

population consists of 13.579 students.

4.2.2 Sample design

The sample design of this research is random sampling. The elements in the population do

have a known and equal chance of being selected as subjects, since the total population is

known.

4.2.3 Sample size

The sample is divided into subsamples, resulting in a minimum sample size of 30 for each

category. The factorial design consists of eight groups, so the preferable sample size is 240.

The sample size should also be preferable ten times (10x) as large as the number of variables

on the study. Since this the model in this research contains two subsets and six variables, a

minimum sample size of 70 are concluded as necessary. A sample size of 240 satisfies this

requirement.

4.3 Design of experiment

The participants face two investment events. In the first investment event the participants are

evenly divided among eight groups. Four of those groups are confronted with a loss or a gain,

the other four groups function as a control group. The second investment opportunity is

presented as a decision to be taken by the participants. Confronting participants with a given

loss or gain should influence the second investment event, the investment decision. The

influence of the first investment event should result in a change in future risk taking in the

second investment decision.

The ideal experiment should contain subjects who make choices for real money. In this

experiment no real money is included, since in the experiment of Johnson and Thaler (1990),

the people who agreed to be real-money subjects, had extremely risk seeking preferences.

In the first investment event participants are randomly assigned to one of the four possible

results. The second investment decision consists of choosing among five types of project, in

which they could invest. No historical information is known about these projects. The

projects vary in the amount of payoff and accompanying probabilities. The projects which

have higher payoffs have a lower accompanying probability. In other words, higher payoffs

S.J.P. Delahaije – Bachelor Thesis 2012 Page 17

go together with lower probabilities. The expected value, the probability of a payoff

multiplied by the monetary outcome, is in every project the same. This condition ensures that

investors won’t choose a project depending on their expected value. The second investment

decision and the money they invest is a mental choice, so it doesn’t consist real money. The

amount of risk of the projects depends on the amount of payoff, probability of payoff and the

variance. The participants receive their final investment result after the second investment

decision.

The two investment events and the projects of the second investment decision are represented

below:

Investment event I

The participants are divided into two groups. One group is the control group and the other the

experimental group. The experimental group is randomly divided into two groups. The first

group of the experimental group is randomly divided into two groups (50%-50%). 50% of the

participants are assigned to a loss of €5000 and 50% are assigned to a gain of €5000. The

second group of the experimental group is also randomly divided into two groups (50%-

50%). 50% of the participants are assigned to a loss of €2500 and 50% are assigned to a gain

of €2500.

These prior gains or losses result in four possible amounts after the first investment decision,

€5000, €7500, €12.500 or €15.000, which the participant uses in the second investment

decision.

The different amounts gained or lost are developed because the different psychological biases

depend on the initial amount gained or lost. By example, the break-even effect arises if the

initial amount lost is relative large. From either of the two sorts of groups, one group is the

control group, to check if the effects are significant.

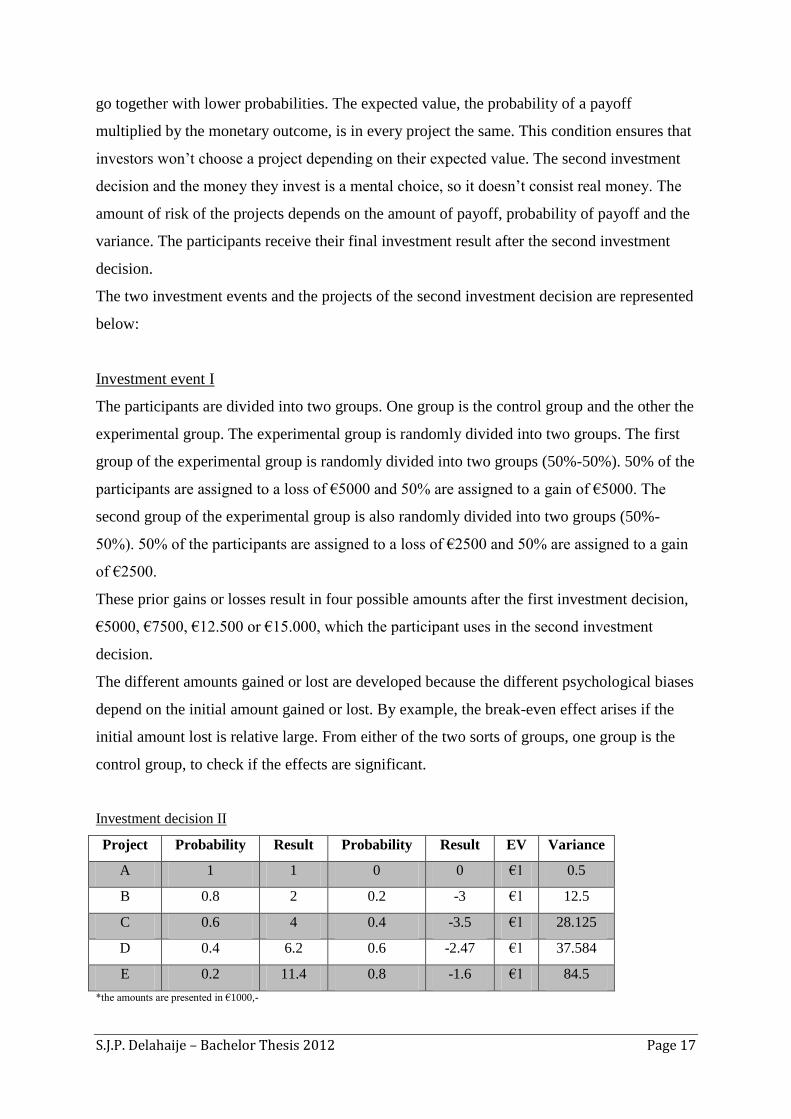

Investment decision II

Project Probability Result Probability Result EV Variance

A 1 1 0 0 €1 0.5

B 0.8 2 0.2 -3 €1 12.5

C 0.6 4 0.4 -3.5 €1 28.125

D 0.4 6.2 0.6 -2.47 €1 37.584

E 0.2 11.4 0.8 -1.6 €1 84.5

*the amounts are presented in €1000,-

S.J.P. Delahaije – Bachelor Thesis 2012 Page 18

4.3.1 Manipulation

The effect of the three biases on future risk taking has already been revealed in the second

chapter of this paper. These results are based on previous research. Therefore, the focus of

this paper is on the possible influence of market announcements on these relationships. The

manipulation in this experiment is done by creating different levels of the moderating

variable, macroeconomic government announcements. This announcement consists of

positive macro-economic news which is presented to the participants after the first investment

decision. The announcement is positive since: “Good news induces both buying and selling,

whereas bad news does not cause abnormal trading by individuals.” (Nofsinger, 2000).

Four groups are confronted with a government announcement, after experiencing a loss or

gain, and four groups are not confronted with a government announcement, after

experiencing a loss or gain. The groups which is confronted with a government

announcement are the control group of the experiment, to check whether the effect of the

government announcement is significant. The control group and the experimental group are

asked to give their overall perception about the future of the market, on a seven-point Likert-

scale. This perception is a control on the government announcement, to check if the

announcement doesn’t positively bias investors perception of the future market.

Government announcement:

The participants read a short story which is presented below. In this story the Dutch

government predicts a growth of the economy the next period.

This government announcement present a simplified example of a government announcement

in real-life. Dominguez and Panthaki (2006) showed that macroeconomic news could

increase the investors perception of uncertainty. This increase of uncertainty is expected to

increase investors bias of loss-aversion. Therefore, participants receiving the government

announcement are expected to show a decrease in risk taking, due to the stronger loss-

aversion bias.

“The Dutch government has become more positive about the growth of the Dutch economy

the coming few months. The government foresees a growth of 2,75 percent of the Dutch

economy this year. The major part of this growth will be realized in the next quarter,

according the Dutch minister of Finance. The minister foresees more and more signs which

confirm the expected growth in the last few months. The most important factor of the

S.J.P. Delahaije – Bachelor Thesis 2012 Page 19

expected growth is the increase in consumer purchasing power. The government expects that

the growth of the Dutch economy will continue next year.”

4.3.2 Treatment

There are eight treatments in this experimental setting. These treatments take place after

participants made their first investment decision. Randomly, 50% of the respondents is

confronted with a loss and 50% is confronted with a gain. The total group of participants is

divided into four groups. These four groups are further divided into two separate groups, each

presented with a different amount lost or gained in the first investment event. The possible

amounts lost or gained are $2500,- and $5000,-. Of the totals of eight groups which arise four

groups are assigned to read a government announcement and the other four groups assigned

to read nothing. This treatment is developed to create an experience comparably with a real-

life investment result and should trigger psychological biases as a consequence to a prior gain

or loss within the participants. Summarized, there are eight treatments caused by the

collaboration of the two variables, prior result and government announcement, in which the

prior result, has four levels and the announcement two levels.

4.3.3 Instructions

This paragraph presents the instructions given to every individual participant.

Instructions:

This experiment simulates a series of investment decisions. Imagine that you are an

individual investor. Last year you invested €10.000 of your money in “Project K”. The results

of your previous investment are presented to you after the instructions. In the investment

decision which follows after the result of Project K is known, you must decide how much of

your capital to split among the projects, which are labeled: “Project A”, “Project B”, “Project

C”, “Project D”, “Project E”.

You are asked how much to invest in either of the projects, ranging from €500, - to your

maximum capital budget.

The initial budget you had last year was €10.000,-, which can increase or decrease depending

on the results of Project K. Your final budget has to be spent completely in the investment

decision.

S.J.P. Delahaije – Bachelor Thesis 2012 Page 20

You will receive some details according every project, in which you could invest. These

details include expected value, variance and the expected outcomes with accompanying

probabilities.

The investment decision will determine the overall return of your investment decisions,

including the results of project K and your current investment decision.

If you have any questions during the experiment, do not hesitate to ask the experimenter.

Thank you for your help!

S.J.P. Delahaije – Bachelor Thesis 2012 Page 21

Chapter 5 a final overview

5.1 Limitations

Since this paper is based on a lab experiment, there are several limitations for the

generalization of the results. The lab experiment doesn’t approximate the complex setting in

which real investors have to operate. There are a lot of factors ruled out, which in reality

could have a huge impact on investors’ behavior.

An example of such factors is the wealth of the investors. Massa and Simonov made this

distinction in their experiment, but it is not present in this experiment. The different reaction

among high and low-wealth investors could be a consequence of borrowing constraints. This

means that if investors increase the proportion of borrowed capital compared to their total

wealth, the willingness to invest in risky assets could decrease.

Another important limitation of this paper is that investors’ risk taking in the financial market

is affected by gains/losses in wealth in its entirety (Simonov and Massa, 2002). This

consideration has the disadvantage that wealth could be affected by a lot of different factors,

also factors which have nothing to do with the result of an initial investment. The advantage

of the experiment is that all these external factors are exterminated, which gives a

concentrated result of how investors behave towards prior gains or losses. Nevertheless, in a

real investment setting, there are a lot of factors influencing investors’ wealth apart from

gains or losses from investment decisions.

The results of the first investment in project K and the investment decision of the participant

succeed one another in a short time period. This relative quick sequence of the result of

project K, resulting in a gain or loss, and the second investment decision could limit the

implications of the results in real life. In real life the results of an investment and a new

investment won’t succeed each other in such a short time. The effects of the prior gains/losses

could be overdone, since the limited time frame does not give the opportunity for the effects

to fade away by time.

S.J.P. Delahaije – Bachelor Thesis 2012 Page 22

5.2 Conclusions and expected results

There are eight groups included in the experiment. Four groups make the experimental group

and four groups make the control group. The experimental group is confronted with the

government announcement, the control group not. The four experimental groups are

confronted with different results before they have to make an investment decision. The

expectations of the effects of these different results on future risk taking are discussed below:

The participant gained €5000, - in the first investment event, with no government

announcement.

In this situation the house-money effect has a huge impact on future risk taking, since the

amount gained is relatively large compared with the initial budget. This effect has the

consequence that participants increase their risk taking significantly. According to Johnson

and Thaler, around 80% of the participants should engage in increased risk taking. In the

experiment this results in a preference for the projects C, D or E.

The participant lost €5000, - in the first investment even, with no government announcement.

The participants are influenced by the break-even effect, since their loss of the first

investment is relatively large compared to the initial budget. Therefore, participants have the

urge to make up for their losses and projects that offer the options to break-even are more

attractive. These projects are high risk projects, so the participant will significantly increase

his/hers risk taking. In the experiment this results in a preference for the projects D or E,

which offers the option to break-even.

The participant gained €2500,- in the first investment event, with no government

announcement.

In this situation the house-money effect will have a medium size impact on participants risk

taking. The participants increase the amount of risk taking, but the increase is less than in the

situation of a gain of €5000,-. This results in the experiment in a preference for project C,D or

E, although fewer participants will choose these options compared to the situation of a gain of

€5000,-.

The participants lost €2500, - in the first investment even, with no government announcement.

The participants are influenced by the break-even effect, although this effect is much smaller

compared with the loss of €5000,-. The decrease of the break-even effect is caused by the fact

that the amount lost is smaller compared to the initial budget. Most of the participants are

S.J.P. Delahaije – Bachelor Thesis 2012 Page 23

expected to become loss-averse and reduce their risk in the investment decision. The

participants try to prevent the loss to become larger. The decrease in the amount of risk

taking of the participants could also be assigned to the house-money effect, but the affect of

loss-aversion compared with the house-money effect is much larger in the case of a loss.

According to Dominguez and Panthaki (2006) the macro-economic government

announcement should increase the participants’ perception of uncertainty. Therefore, the

participants show an increase in the loss-aversion effect. In the experiment, this increase

results in:

showed that macroeconomic news could increase the investors’ perception of uncertainty.

This increase of uncertainty is expected to increase investors’ bias of loss-aversion.

Therefore, participants receiving the government announcement are expected to show a

decrease in risk taking, due to the stronger loss-aversion bias.

The participant gained €5000, - in the first investment event, with government announcement.

In this situation the house-money effect still has a huge impact on future risk taking. There

will be a decrease in the number of participants engaging in increased risk taking compared

with the situation with no government announcement. Compared to the situation with no

announcement, this results in a decreased preference for the projects C, D or E and an

increase in projects A or B.

The participant lost €5000, - in the first investment event, with government announcement.

The break-even effect continues to have the largest impact on risk taking. The increased risk

taking decreases compared to the situation with no announcement, since more participants

will become loss-averse. In the experiment this results in a decreased preference for the

projects D or E and an increased preference for project A, compared with the situation with

no announcement.

The participant gained €2500, - in the first investment event, with government announcement.

In this situation the house-money effect has less impact, compared with the situation with no

government announcement. Therefore, participants show a decrease in the amount of risk

taking. The effect of loss-aversion is larger, so participants show an increased preference for

S.J.P. Delahaije – Bachelor Thesis 2012 Page 24

projects A or B. At the same time, participants show a decreased preference for the projects

C, D or E.

The participant lost €2500, - in the first investment event, with government announcement.

The risk taking of the participants shows a decrease, since the loss-aversion effect becomes

larger. In this situation the influence of loss-aversion shows the largest influence on risk

taking. The break-even effect has still any influence, although this influence is becoming very

small. Since the majority of the participants become loss-averse, their preference is project A.

The effect of the type of media is expected to have no significant influence on the

relationship between the macro-economic government announcement and the three biases.

Massa and Simonov showed that the influence of the type of media depends on the wealth of

the investor. In this experiment the initial capital is equal for all investors, so the influence of

the type of media is expected not to be significant.

S.J.P. Delahaije – Bachelor Thesis 2012 Page 25

References

Arkes, H. R., Blumer, C. (1985) The Psychology of Sunk Costs. Organizational Behavior

and Human Decision Processes, 35, 1, 124-140.

Baker, H.K., Nofsinger, J. R. (2002). Psychological Biases of Investors. Financial Services

Review, 11, 97-116.

Barber, B., Odean, T. (2008). All That Glitters: The Effect of Attention and News on the

Buying Behavior of Individual and Institutional Investors. Review of Financial Studies 21,

785-818

Dominguez, K.M.E., Panthaki, F. (2006) What defines ‘news’ in foreign exchange markets?

Journal of International Money and Finance, 25, 168-198.

Glaser, M., Weber M. (2002) Momentum and Turnover: Evidence from the German stock

market. University Mannheim.

Kahneman, D., Knetsch, J.K., Thaler, R.H. (1990) Anomalies: The Endowment Effect, Loss

Aversion, and Status Quo Bias. The Journal of Economic Perspectives, 5, No. 1, 193-206.

Kahneman, D., Tversky, A. (1979). Prospect theory: An analysis of decision under risk.

Econometrica, 47(2), 263–291.

Massa, M., Simonov, A. (2002) Behavioral biases and investment. Finance Department,

INSEAD. Stockholm school of Economics.

Massa, M., Simonov, A. (2005) Behavioral biases and investment. Review of finance, 9, 483-

507.

Nofsinger, J.R. (2000) Impact of public information on investors. Journal of Banking &

Finance, 25, 1339-1366.

S.J.P. Delahaije – Bachelor Thesis 2012 Page 26

Peress, J. (2008). Media coverage and investors’ attention to earnings announcements,

Working Paper

Shefrin, H. (2000). Beyond Greed and Fear. Harvard Business School Press, Boston.

Shefrin, H.M., and M. Statman. (1985). The Disposition to Sell Winners Too

Early and Ride Losers Too Long: Theory and Evidence. Journal of Finance, vol.

40, no. 3 (July), 777–790.

Thaler, R.H. (1997) The end of behavioral finance. Financial Analysts Journal, 55, 6, 12-17

Thaler, R. H. (1980). Toward a positive theory of consumer choice. Journal of Economic

Behavior and Organization, 1, 39–60.

Thaler, R.H., Johnson, E.J. (1990) Gambling with the house money and trying to break-even:

the effects of prior outcomes on risky choice. Management Science, Vol. 36, No. 6, 643-660

Tetlock, P. (2007). All the News That's Fit to Reprint: Do Investors React to Stale

Information? Working Paper. Columbia University.

Tversky, A., Kahneman, D. (1992) Advances in prospect Theory: cumulative representation

of uncertainty. Journal of Risk and Uncertainty, 5, 4, 297-323.